Selected Dates Filter by @zeusbottradingWe are presenting you feature for strategies in Pine Script.

This function/pine script is about NOT opening trades on selected days. Real usage is for bank holidays or volatile days (PPI, CPI, Interest Rates etc.) in United States and United Kingdom from 2020 to 2030 (10 years of dates of bank holidays in mentioned countries above). Strategy is simple - SMA crossover of two lengts 14 and 28 with close source.

In pine script you can see we picked US and GB bank holidays. If you add this into your strategy, your bot will not open trades on those days. You must make it a rule or a condition. We use it as a rule in opening long/short trades.

You can also add some of your prefered dates, here is just example of our idea. If you want to add your preffered days you can find them on any site like forexfactory, myfxbook and so on. But don’t forget to add function “time_tradingday ! = YourChoosedDate” as it is writen lower in the pine script.

Sometimes the date is substituted for a different day, because the day of the holiday is on Saturday or Sunday.

Made with ❤️ for this community.

If you have any questions or suggestions, let us know.

The script is for informational and educational purposes only. Use of the script does not constitutes professional and/or financial advice. You alone the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold zeusbottrading TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script.

Индикаторы и стратегии

DRM StrategyOne of the ways I go when I develop strategies is by reducing the number of parameters and removing fixed parameters and levels.

In this strategy, I'm trying to create an RSI indicator with a dynamic length.

Length is computed based on the correlation between Price and its momentum.

You can set min and max values for the RSI, and if the correlation is close to 1, we'll be at a min RSI value. When it's -1, we'll be at the max level.

I got this idea from Sofien Kaabar's book.

The strategy is super simple, and there might be much room for improvement.

Performance on the deep backtesting is not excellent, so I think the strategy needs some filters for regimes, etc.

Thanks to @MUQWISHI for helping me code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

supertrend with multiple filter strategythis indicator filters buy and sell signal from the supertrend base on various condition that the user can manually select.

as of now the following filter are included

buy and sell filter;

-Macd

-CCI

-EMA200

-LUX TRAMA

-Stochastic rsi

-MFI

EXIT SIGNAL CAN BE CHOSE BETWEEN ATR BAND OR BOLLINGER BAND

i am planning on keeping to add filters so if you have suggestion fell free to message me.

12/26-IT strategyBase of this Strategy is crossover of 12EMA on 26EMA.

Also multiple other criteria has to meet for buy signal, Criterias mentioned below

//////////////////////////////////

There two entry option to select. Either one or both can be selected:

1. Only 12/26 Cross over

a. 12/26 crossover.

b. RSI (14) value to be between a range (RSI is inbuilt, but lower and upper range can be defined in settings)

c. MACD (12, 26) to be positive and above signal line (this is inbuilt)

2. Recent 12/26 Cross over and closing above pivot point(resistance)

a. 12/26 crossover has to be recent, CrossOverLookbackCandles value will look for crossover in # previous candles..

b. RSI (14) value to be between a range (RSI is inbuilt, but lower and upper range can be defined in settings)

c. MACD (12, 26) to be positive and above signal line (this is inbuilt)

d. closing above resistance line

//////////////////////////////////

For Exit we have three options. you can select any SL as per your need, multiple SLs can also be selected

1. Trailing Stop Loss.

Source for TSL is adjustable(open, close, high or low), also you have to mention % below your source TSL has to be placed.

Once closing is below TSL, exit will be triggered.

2. Closing below 7SMA

After 7SMA SL is enabled, 7SMA will be plotted on chart and exit signal will be triggered when closing is below 7SMA.

Choose this option for LESS risk and rewards

3. 12/26 Crossdown

Once 12EMA crossdown below 26EMA, exit will be triggered.

Choose this option for HIGH risk and rewards

//////////////////////////////////

Resistance line is plotted based on left and right candles, if 10(can be changed) is used for both left and right, indicator will look for 10 candles in left and 10 candles in right and if both left and right candle are lower then a line is plotted.

Source has to be selected (close or high)

//////////////////////////////////

Qty mentioned in Buy trigger will be based on BUYVALUE entered

//////////////////////////////////

Multiple Target option is available, if first target is matched how much percentage of qty to be sold can be defined.

If you wish to have only one Target, then exit qty in first target must be 100

Wolfe Strategy [Trendoscope]Hello Everyone,

Wish you all Merry X-Mas and happy new year. Lets start 2023 with fresh new strategy built on Wolfe Indicator. Details of the indicator can be found here

🎲 Wolfe Concept

Wolfe concept is simple. Whenever a wedge is formed, draw a line joining pivot 1 and 4 as shown in the chart below:

For simplicity, we will only consider static value for Target and Stop. But, entry is done based on breaking the triangle. Revised strategy looks something like this:

🎲 Settings

Settings are simple and details of each are provided via tooltips.

Out of these, the most important one is minimum risk reward ratio. If you set lower risk reward threshold then losing few trades may generate more losses than more winning trades. Similarly higher value will filter out most of the trades and may not work efficiently. Default value set to 1 to make sure optimal risk reward is present before placing trade. Also make note that since the entry bar is always moving towards stop, as and when pattern progress, the RR will also increase. Hence, a pattern which is below RR threshold may become good to trade at certain point of time in future.

🎲 Strategy Parameters

Default strategy parameters are initialised via definition. Margins are set to 100 to disable leveraged trades. Appropriate values are chosen for other parameters. These can be altered based on individual strategy and trading plan.

As the strategy concentrates on the single pattern, number of trades generated are comparatively less. But, there is chance to increase the algorithm further to catch more such patterns on larger scale. Will try to work on them in next versions.

🎲 Pine Strategy limitations

Backtest can only be done on one direction as pine strategy cannot have both long and short open trades together. Hence, it is mandatory to chose either long/short trades in settings.

Since pyramiding is limited to 1, there is possibility of a pattern not generating trade even though the entry conditions are met. They are just based on pine limitations and not necessarily mean patterns are not good for placing trades.

Simple Momentum and Trend, Fixed PnL Strategy for SPY 1D [SR]This strategy uses an ATR rule to assess momentum and a TSI rule to assess bullish or bearishness

It has a fixed stop at 50 points, and fixed take profit at 300 pips

It provides a very satisfyingly smooth equity line with a max drawdown below 5% and realized profit over 200%

This is the initial version as I work out optimizations and add plots to the chart based on the strategy's actions.

I would love to get the community's feedback and help as I'm new. Not sure how to limit the date range of the backtest to make it more realistic. I'm also not certain how to plot it best.

BankNifty_Bullish_Intraday

The script uses following mechanism to give a signal of BUY if multiple parameters evaluated are all passed.

ENTRY-

1. 5 min MACD should be more than its previous tick

2. 15 min MACD should be more than its previous tick

3. 60 min MACD should be more than its previous tick

4. ADX should be more than 12

5. RSI should be more than 60

6. Stochastic %k should have cross over with %d

7. Bollinger band upper band value should be more than previous tick

EXIT

If the 5 min bar price closes below 5 min EMA , it gives an exit signal.

BankNifty_Bearish_Intraday

The script uses following mechanism to give a signal of SELL if multiple parameters evaluated are all passed.

ENTRY-

1. 5 min MACD should be less than its previous tick

2. 15 min MACD should be less than its previous tick

3. 60 min MACD should be less than its previous tick

4. ADX should be more than 12

5. RSI should be less than 40

6. Stochastic %k should have negative cross over with %d

7. Bollinger band lower band value should be less than previous tick

EXIT

If the 5 min bar price closes above 5 min EMA , it gives an exit signal.

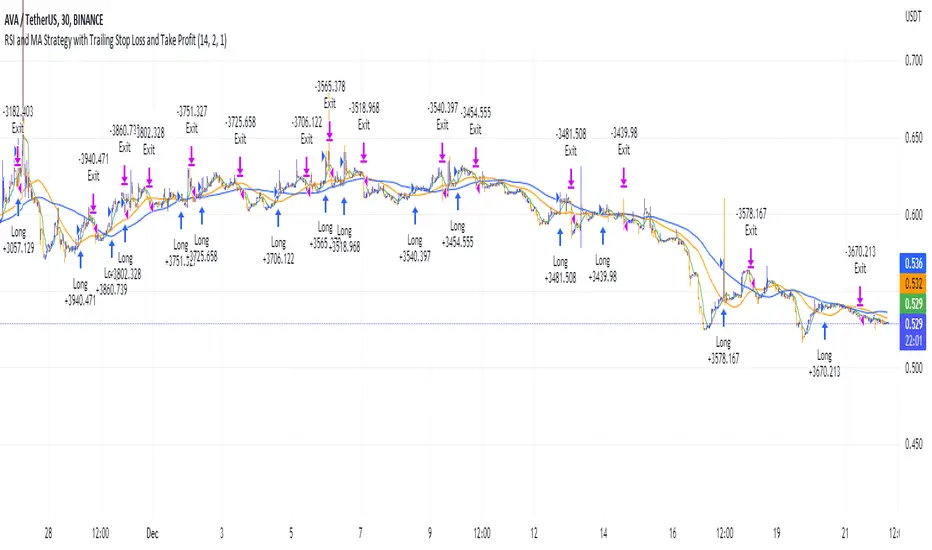

RSI and MA with Trailing Stop Loss and Take Profit (by Coinrule)The relative strength index is a momentum indicator used in technical analysis. It measures the speed and magnitude of a coin's recent price changes to evaluate overvalued or undervalued conditions in the price of that coin. The RSI is displayed as an oscillator (a line graph essentially) on a scale of zero to 100. When the RSI reaches oversold levels, it can provide a signal to go long. When the RSI reaches overbought levels, it can mark a good exit point or alternatively, an entry for a short position. Traditionally, an RSI reading of 70 or above indicates an overbought situation. A reading of 30 or below indicates an oversold condition.

A moving average (MA) calculates the average of a selected range of prices, usually closing prices, by the number of periods in that range. Essentially it is used to help smooth out price data by creating a constantly updated average price.

The Strategy enters and closes trades when the following conditions are met:

Entry Conditions:

RSI is greater than 50

MA9 is greater than MA50

RSI increases by 5

Exit Conditions:

Price increases by 1% trailing

Price decreases by 2% trailing

This strategy is back-tested from 1 January 2022 to simulate how the strategy would work in a bear market. The strategy provides good returns.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

Weird Renko StratThis strategy uses Renko, it generates a signal when there is a reversal in Renko. When using historical data, it provides a good entry and an okay exit. However, in a real-time environment, this strategy is subject to repaint and may produce a false signal.

As a result, the backtesting result should not be used as a metric to predict future results. It is highly recommended to forward-test the strategy before using it in real trading. I forward test it from 12/18/2022 to 12/21/2022 in paper trading, using the alert feature in Tradingview. I made 60 trades trading the BTCUSDT BINANCE 3 min with 26 as the param and under the condition that I use 20x margin, compounding my yield, and having 0 trading fee, a steady loss is generated: from $10 to $3.02.

This is quite interesting. As if I flip the signal from "Long" to "Short" and another way too, it will be a steady profit from $10 to $21.85. Hence, if I'm trying to anti-trade the real-time alert signal, the current "4 Days Result" will be good. Nevertheless, I still have to forward-test it for longer to see if it will fail eventually.

Dive into the setting of the strategy

- Margin is the leverage you use. 1 means 1x, 10 means 10x. It affects the backtest yield when you backtest

- Compound Yield button is for compound calculation, disable it to go back to normal backtesting

- Anti Strategy button is to do the opposite direction trade, when the original strat told you to "Long", you "Short" instead. Enable it to use the feature

- Param is the block size for the Renko chart

- Drawdown is just a visual tool for you in case you want to place a stop loss (represent by the semitransparent red area in the chart)

- From date Thru Date is to specify the backtest range of the strategy, This feature is turned off by default. It is controlled by the Max Backtest Timeframe which will be explain below

- Max Backtest Timeframe control the From date Thru Date function, disable it to enable the From Date Thru Date function

Param is the most important input in this strategy as it directly affects performance. It is highly recommended to backtest nearly all the possible parameters before deploying it in real trading. Some factors should be considered:

- Price of the asset (like an asset of 1 USD vs an asset of 10000 USD required different param)

- Timeframe (1-minute param is different than 1-month param)

I believe this is caused by the volatility of the selected timeframe since different timeframe has different volatility. Param should be fine-tuned before usage.

Here is the param I'm using:

BTCUSDT BINANCE 3min: 26

BTCUSDT BINANCE 5min: 28

BTCUSDT BINANCE 1day: 15

Background of the strategy:

- The strategy starts with $10 at the start of backtesting (customizable in setting)

- The trading fee is set to 0.00% which is not common for most of the popular exchanges (customizable in setting)

- The contract size is not a fixed amount, but it uses your balance to buy it at the open price. If you are using the compound mode, your balance will be your current total balance. If you are using the non-compound mode, it will just use the $10 you start with unless you change the amount you start with. If you are using a margin higher than 1, it will calculate the corresponding contract size properly based on your margin. (Only these options are allowed, you are not able to change them without changing the code)

M0PB (Momentum Pullback)Long/short strategy that identifies extreme readings on the rsi as a *momentum signal*, unlike most RSI strategies the script will look to buy or sell the first pullback in the direction of the extreme RSI reading.

Enters positions on the first pullback to the 5ema(low)/ 5ema(high) and exits at rolling 12 bar high/ low. The rolling high/ low feature means that if the price enters into a prolonged consolidation the profit target will begin to reduce with each new bar. The best trades tend to work within 2-6 bars.

Built for use on 5 min intervals on FX, Indexes, and Crypto. Lower than 5 minute time frames tend to be noisier and mean more commissions and a higher risk of slippage so the suggested timeframe is 5 mins.

Hard stop is X ATR (users can experiment with this) from the position entry price. This can be adjusted in user inputs.

There is a lot of slack left in entries and exits but the overall strategy is fairly robust across timeframes and markets and has between 60%-70% win rate with larger winners.

Signals that occur from economic news volatility are best avoided.

VWMA/SMA 3Commas BotThis strategy utilizes two pairs of different Moving Averages, two Volume-Weighted Moving Averages (VWMA) and two Simple Moving Averages (SMA).

There is a FAST and SLOW version of each VWMA and SMA.

The concept behind this strategy is that volume is not taken into account when calculating a Simple Moving Average.

Simple Moving Averages are often used to determine the dominant direction of price movement and to help a trader look past any short-term volatility or 'noise' from price movement, and instead determine the OVERALL direction of price movement so that one can trade in that direction (trend-following) or look for opportunities to trade AGAINST that direction (fading).

By comparing the different movements of a Volume-Weighted Moving Average against a Simple Moving Average of the same length, a trader can get a better picture of what price movements are actually significant, helping to reduce false signals that might occur from only using Simple Moving Averages.

The practical applications of this strategy are identifying dominant directional trends. These can be found when the Volume Weighted Moving Average is moving in the same direction as the Simple Moving Average, and ideally, tracking above it.

This would indicate that there is sufficient volume supporting an uptrend or downtrend, and thus gives traders additional confirmation to potentially look for a trade in that direction.

One can initially look for the Fast VWMA to track above the Fast SMA as your initial sign of bullish confirmation (reversed for downtrending markets). Then, when the Fast VWMA crosses over the Slow SMA, one can determine additional trend strength. Finally, when the Slow VWMA crosses over the Slow SMA, one can determine that the trend is truly strong.

Traders can choose to look for trade entries at either of those triggers, depending on risk tolerance and risk appetite.

Furthermore, this strategy can be used to identify divergence or weakness in trending movements. This is very helpful for identifying potential areas to exit one's trade or even look for counter-trend trades (reversals).

These moments occur when the Volume-Weighted Moving Average, either fast or slow, begins to trade in the opposite direction as their Simple Moving Average counterpart.

For instance, if price has been trending upwards for awhile, and the Fast VWMA begins to trade underneath the Fast SMA, this is an indication that volume is beginning to falter. Uptrends need appropriate volume to continue moving with momentum, so when we see volume begin to falter, it can be a potential sign of an upcoming reversal in trend.

Depending on how quickly one wants to enter into a movement, one could look for crosses of the Fast VWMA under/over the Fast SMA, crosses of the Fast VWMA over/under the Slow SMA, or crosses over/under of the Slow VWMA and the Slow SMA.

This concept was originally published here on TradingView by ProfitProgrammers.

Here is a link to his original indicator script:

I have added onto this concept by:

converting the original indicator into a strategy tester for backtesting

adding the ability to conveniently test long or short strategies, or both

adding the ability to calculate dynamic position sizes

adding the ability to calculate dynamic stop losses and take profit levels using the Average True Range

adding the ability to exit trades based on overbought/oversold crosses of the Stochastic RSI

conveniently switch between different thresholds or speeds of the Moving Average crosses to test different strategies on different asset classes

easily hook this strategy up to 3Commas for automation via their DCA bot feature

Full credit to ProfitProgrammers for the original concept and idea.

Any feedback or suggestions are greatly appreciated.

Time Based Crypto DayTrade StrategyThis is a time based strategy, designed to enter and exit within the same day of the week, using different hours for entry and exit.

The script is long only direction, and it has no risk management inside, so use it with caution.

At the same time you can also calculate each individual hour return within a certain day, and make your own idea about the best moments to be enter.

In order to filter a bit from the bad trades, I have applied an ATR filter, to check if that volatility is rising in order to help eliminate some of the bad trades when there is no volatility around.

For this example, on BTC, it seems that for the last years, on tuesday and thursday, enterring at the beginning of the daily candle, 01:00hours and exit at 00:00 hours, seems to give positive results giving the idea that can be converted in some sort of edge into our favor.

However dont take this entirelly for granted and conduct your own searches

I11L - Meanreverter 4h---Overview---

The system buys fear and sells greed.

Its relies on a Relative Strength Index (RSI) and moving averages (MA) to find oversold and overbought states.

It seems to work best in market conditions where the Bond market has a negative Beta to Stocks.

Backtests in a longer Timeframe will clearly show this.

---Parameter---

Frequency: Smothens the RSI curve, helps to "remember" recent highs better.

RsiFrequency: A Frequency of 40 implies a RSI over the last 40 Bars.

BuyZoneDistance: Spacing between the different zones. A wider spacing reduces the amount of signals and icnreases the holding duration. Should be finetuned with tradingcosts in mind.

AvgDownATRSum: The multiple of the Average ATR over 20 Bars * amount of opentrades for your average down. I choose the ATR over a fixed percent loss to find more signals in low volatility environments and less in high volatility environments.

---Some of my thoughts---

Be very careful about the good backtesting performance in many US-Stocks because the System had a favourable environment since 1970.

Be careful about the survivorship bias as well.

52% of stocks from the S&P500 were removed since 2000.

I discount my Annual Results by 5% because of this fact.

You will find yourself quite often with very few signals because of the high market correlation.

My testing suggests that there is no expected total performance difference between a signal from a bad and a signal from a good market condition but a higher volatility.

I am sharing this strategy because i am currently not able to implement it as i want to and i think that meanreversion is starting to be taken more serious by traders.

The challange in implementing this strategy is that you need to be invested 100% of the time to retrieve the expected annual performance and to reduce the fat tail risk by market crashes.

EURUSD COT Trend StrategyThis is a long term/investment type of strategy designed to have a good idea about where the big trend direction is headed.

Its logic, its made entirely on the COT report, mainly from looking into the net non comercial positions aka the speculators.

For bullish trend we look that the difference between long non comercial vs short non comercial is higher than 0

For bearish trend we look that the difference between long non comercial vs short non comercial is lower than 0.

This is mainly as an educational tool, for a full strategy, I recommend implement other things into it, like technical analysis or risk management.

If you have any questions, please let me know !

RSI Divergence Strategywhat is "RSI Divergence Strategy"?

it is a RSI strategy based this indicator:

what it does?

it gives buy or sell signals according to RSI Divergences. it also has different variables such as "take profit", "stop loss" and trailing stop loss.

how it does it?

it uses the "RSI Divergence" indicator to give signal. For detailed information on how it works, you can visit the link above. The quantity of the inputs is proportional to the rsi values. Long trades are directly traded with "RSI" value, while short poses are traded with "100-RSI" value.

How to use it?

The default settings are for scalp strategy but can be used for any type of trading strategy. you can develop different strategies by changing the sections. It is quite simple to use.

RSI length is length of RSİ

source is source of RSİ

RSİ Divergence lenght is length of line on the RSI

The "take profit", "stop" and "trailing stop" parts used in the "buy" group only affect buys. The "sell" group is similarly independent of the variables in the "buy" group.

The "zoom" section is used to enlarge or reduce the indicator. it only changes the appearance, it does not affect the results of the strategy.

Breakeven Line DemoPlug the breakeven line code into the bottom of your strategy to get visualization of your breakeven price. Line is green when net position is long, red when net short and invisible when strategy is risk neutral. Most useful for strategies which use pyramiding (successive entries in same direction stacked upon each other) as it can be difficult to track where prices needs to return to to allow closing in profit. Disclaimer: the strategy logic is garbage do not use it. It is only there so you can see how Breakeven Line logic is implemented.

Fast EMA above Slow EMA with MACD (by Coinrule)An exponential moving average ( EMA ) is a type of moving average (MA) that places a greater weight and significance on the most recent data points. The exponential moving average is also referred to as the exponentially weighted moving average . An exponentially weighted moving average reacts more significantly to recent price changes than a simple moving average simple moving average ( SMA ), which applies an equal weight to all observations in the period.

Moving average convergence divergence ( MACD ) is a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price. The MACD is calculated by subtracting the 26-period exponential moving average ( EMA ) from the 12-period EMA .

The result of that calculation is the MACD line. A nine-day EMA of the MACD called the "signal line," is then plotted on top of the MACD line, which can function as a trigger for buy and sell signals. Traders may buy the coin when the MACD crosses above its signal line and sell—or short—the security when the MACD crosses below the signal line. Moving average convergence divergence ( MACD ) indicators can be interpreted in several ways, but the more common methods are crossovers, divergences, and rapid rises/falls.

The Strategy enters and closes the trade when the following conditions are met:

LONG

The MACD histogram turns bullish

EMA8 is greater than EMA26

EXIT

Price increases 3% trailing

Price decreases 1% trailing

This strategy is back-tested from 1 January 2022 to simulate how the strategy would work in a bear market and provides good returns.

Pairs that produce very strong results include AXSUSDT on the 5-minute timeframe. This short timeframe means that this strategy opens and closes trades regularly.

Additionally, the trailing stop loss and take profit conditions can also be changed to match your needs.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

[-_-] Level Breakout, Auto Backtesting StrategyDescription:

A Long only strategy based on breakout from a certain level formed by High price. It has auto-backtesting capabilities (you set ranges for the three main parameters: Lookback, TP and SL; the strategy then goes through different combinations of those parameters and displays a table with results that you can sort by Percentage of profitable trades AND/OR Net profit AND/OR Number of trades). So you can, for example, sort only by Net profit to find combination of parameters that gives highest net profit, or sort by Net profit and Percentage profitable to find a combination of parameters that gives the best balance between profitability and profit. The auto-backtesting also takes into account the commission which is set in % in the inputs (make sure to set the same value in properties of the strategy so that auto-backtesting and real backtesting results match).

NOTE: auto-backtesting only find the best combinations and displays them in a table, you will then need to manually set the Lookback, TP and SL inputs for real backtesting to match.

Parameters:

- Lookback -> # of bars for filtering signals; recommended range from 2 to 5

- TP (%) -> take profit; recommended range from 5 to 10

- SL (%) -> stop loss; recommended range from 1 to 5

- Commission (%) -> commission per trade

- Min/Max Lookback -> lookback range for auto-backtesting

- Min/Max TP -> take profit range for auto-backtesting

- Min/Max SL -> stop loss range for auto-backtesting

- Percentage profitable -> sort by percentage of profitable trades

- Net profit -> sort by net profit

- Number of trades -> sort by number of trades

Trend Following based on Trend ConfidenceThis is a Trend Following strategy based on the Trend Confidence indicator.

The goal of this strategy is to be a simple Trend Following strategy, but also to be as precise as possible when it comes to the question 'how confident are we that a linear trend is ongoing?'. For this we calculate the 'confidence' of a linear trend in the past number of closing prices. The idea of this strategy is that past a certain confidence, the ongoing linear trend is more likely to continue than not.

Trend Confidence:

The Trend Confidence shows us how strong of a linear trend the price has made in the past number (given by Length parameter) of closing prices. The steepness of the price change makes the Trend Confidence more extreme (more positive for an uptrend or more negative for a downtrend), and the deviation from a straight line makes the Trend Confidence less extreme (brings the confidence closer to 0). This way we can filter out signals by wild/sudden price moves that don't follow a clear linear trend.

Math behind the Trend Confidence:

A linear fit is made on the past number of closing prices, using Ordinary Linear Regression. We have the steepness of the linear fit: b in y=a+bx . And we have the standard deviation of the distances from the closing prices to the linear fit: sd . The Trend Confidence is the ratio b/sd .

Entries and Exits:

For entry and exit points we look at how extreme the Trend Confidence is. The strategy is based on the assumption that past a certain confidence level, the ongoing linear trend is more likely to continue than not.

So when the Trend Confidence passes above the 'Long entry" threshold, we go Long. After that when the Trend Confidence passes under the 'Long exit' threshold, we exit. The Long entry should be a positive value so that we go Long once a linear uptrend with enough confidence has been detected.

When the Trend Confidence passes below the 'Short entry' threshold, we go Short. After that when the Trend Confidence passes above the 'Short exit' threshold, we exit. The Short entry should be a negative value so that we go Short once a linear downtrend with enough confidence has been detected.

Default Parameters:

The strategy is intended for BTC-USD market, 4 hour timeframe. The strategy also works on ETH-USD with similar parameters.

The Length is arbitrarily set at 30, this means we look at the past 30 closing prices to determine a linear trend. Note that changing the length will change the range of Trend Confidence values encountered.

The default entry and exit thresholds for Longs and Shorts do not mirror each other. This is because the BTC-USD market goes up more heavily and more often than it goes down. So the ideal parameters for Longs and Shorts are not the same.

The positive results of the strategy remain when the parameters are slightly changed (robustness check).

The strategy uses 100% equity per trade, but has a 10% stop loss so that a maximum of 10% is risked per trade.

Commission is set at 0.1% as is the highest commission for most crypto exchanges.

Slippage is set at 5 ticks, source for this is theblock.co.

Ichimoku Cloud with MACD and Trailing Stop Loss (by Coinrule)The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. It does this by taking multiple averages and plotting them on a chart. It also uses these figures to compute a “cloud” that attempts to forecast where the price may find support or resistance in the future.

The Ichimoku Cloud was developed by Goichi Hosoda, a Japanese journalist, and published in the late 1960s. It provides more data points than the standard candlestick chart. While it seems complicated at first glance, those familiar with how to read the charts often find it easy to understand with well-defined trading signals.

The Ichimoku Cloud is composed of five lines or calculations, two of which comprise a cloud where the difference between the two lines is shaded in.

The lines include a nine-period average, a 26-period average, an average of those two averages, a 52-period average, and a lagging closing price line.

The cloud is a key part of the indicator. When the price is below the cloud, the trend is down. When the price is above the cloud, the trend is up.

The above trend signals are strengthened if the cloud is moving in the same direction as the price. For example, during an uptrend, the top of the cloud is moving up, or during a downtrend, the bottom of the cloud is moving down.

The MACD is a trend following momentum indicator and provides identification of short-term trend direction. In this variation it utilises the 12-period as the fast and 26-period as the slow length EMAs, with signal smoothing set at 9.

This strategy combines the Ichimoku Cloud with the MACD indicator to better enter trades.

Long/Exit orders are placed when three basic signals are triggered.

Long Position:

Tenkan-Sen is above the Kijun-Sen

Chikou-Span is above the close of 26 bars ago

Close is above the Kumo Cloud

MACD line crosses over the signal line

Exit Position:

Price increases 3% trailing

Price decreases 3% trailing

The script is backtested from 1 June 2022 and provides good returns.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

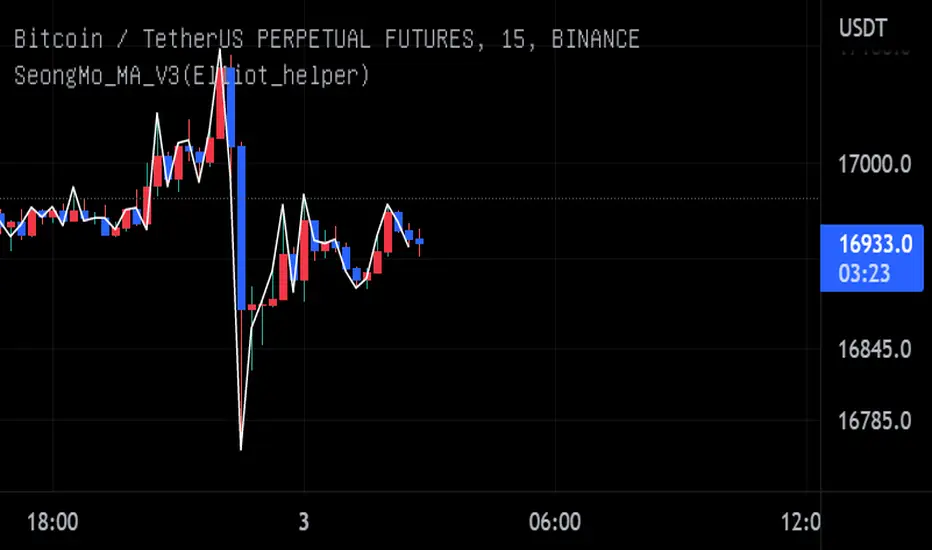

SeongMo_MA_V3(Elliot_helper)Made to make it easier to count Elliott waves.

If you renew your new high price, you'll continue your new high price

When the new low is renewed, the new low is continued.

If you are within the range of the previous candle, use the ratio of the difference between the median value of the previous candle and the closing price of the current candle to determine whether to continue the high or low price.

If a can with a tail that updates a new high price and a new low price at the same time comes out, the phrase "Check_candle!" appears to mean that you should check it with a lower time zone candle.

I11L - Reversal Trading Ideas by Larry ConnorsThis is my own Twist on Larry Connors Simple Tradingideas.

It Combines the RSI, Averaging In and the Lowest Bars in a Single System.

The current Configuration is designed for the Daily Timeframe.

Feel free to play with the Parameters and keep in mind that Larry Intended to buy fear and sell the greed!

The Rules are the following:

---Buy---

Buy, if the lowest Bar of your Configuration has been hit (default is set to 7).

---Average Down--

Buy, if the lowest Bar of your Configuration * Your open trades has been hit AND only if the buyin is atleast 1% cheaper.

---Close---

Close, if the RSI closes above a certain level (default is set to 70).

---TP---

There is no TP

---SL---

There is no SL, so be cautions of your tail Risk!