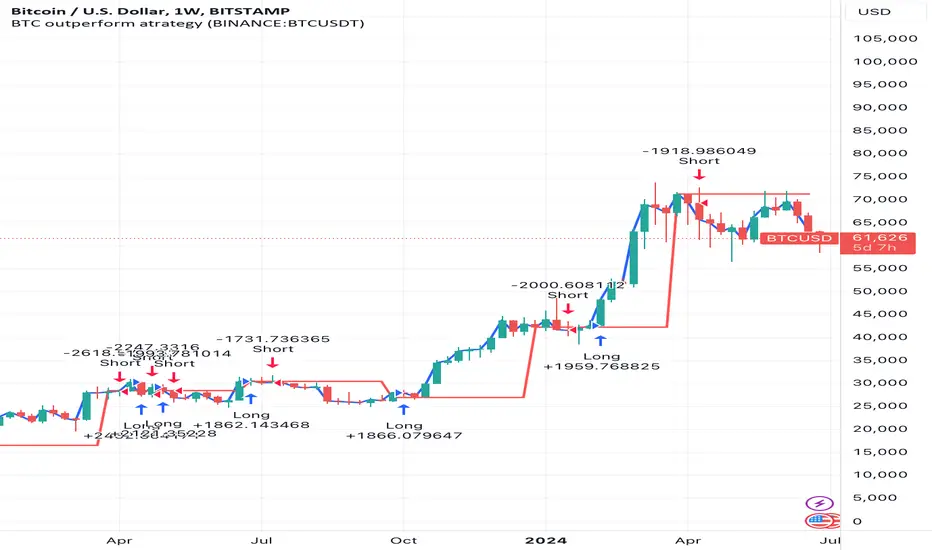

BTC outperform atrategy### Code Description

This Pine Script™ code implements a simple trading strategy based on the relative prices of Bitcoin (BTC) on a weekly and a three-month basis. The script plots the weekly and three-month closing prices of Bitcoin on the chart and generates trading signals based on the comparison of these prices. The code can also be applied to Ethereum (ETH) with similar effectiveness.

### Explanation

1. **Inputs and Variables**:

- The user selects the trading symbol (default is "BINANCE:BTCUSDT").

- `weeklyPrice` retrieves the closing price of the selected symbol on a weekly interval.

- `monthlyPrice` retrieves the closing price of the selected symbol on a three-month interval.

2. **Plotting Data**:

- The weekly price is plotted in blue.

- The three-month price is plotted in red.

3. **Trading Conditions**:

- A long position is suggested if the weekly price is greater than the three-month price.

- A short position is suggested if the three-month price is greater than the weekly price.

4. **Strategy Execution**:

- If the long condition is met, the strategy enters a long position.

- If the short condition is met, the strategy enters a short position.

This script works equally well for Ethereum (ETH) by changing the symbol input to "BINANCE:ETHUSDT" or any other desired Ethereum trading pair.

Индикаторы и стратегии

HMA Crossover 1H with RSI, Stochastic RSI, and Trailing StopThe strategy script provided is a trading algorithm designed to help traders make informed buy and sell decisions based on certain technical indicators. Here’s a breakdown of what each part of the script does and how the strategy works:

Key Components:

Hull Moving Averages (HMA):

HMA 5: This is a Hull Moving Average calculated over 5 periods. HMAs are used to smooth out price data and identify trends more quickly than traditional moving averages.

HMA 20: This is another HMA but calculated over 20 periods, providing a broader view of the trend.

Relative Strength Index (RSI):

RSI 14: This is a momentum oscillator that measures the speed and change of price movements over a 14-period timeframe. It helps identify overbought or oversold conditions in the market.

Stochastic RSI:

%K: This is the main line of the Stochastic RSI, which combines the RSI and the Stochastic Oscillator to provide a more sensitive measure of overbought and oversold conditions. It is smoothed with a 3-period simple moving average.

Trading Signals:

Buy Signal:

Generated when the 5-period HMA crosses above the 20-period HMA, indicating a potential upward trend.

Additionally, the RSI must be below 45, suggesting that the market is not overbought.

The Stochastic RSI %K must also be below 39, confirming the oversold condition.

Sell Signal:

Generated when the 5-period HMA crosses below the 20-period HMA, indicating a potential downward trend.

The RSI must be above 60, suggesting that the market is not oversold.

The Stochastic RSI %K must also be above 63, confirming the overbought condition.

Trailing Stop Loss:

This feature helps protect profits by automatically selling the position if the price moves against the trade by 5%.

For sell positions, an additional trailing stop of 100 points is included.

Advanced Gold Scalping Strategy with RSI Divergence# Advanced Gold Scalping Strategy with RSI Divergence

## Overview

This Pine Script implements an advanced scalping strategy for gold (XAUUSD) trading, primarily designed for the 1-minute timeframe. The strategy utilizes the Relative Strength Index (RSI) indicator along with its moving average to identify potential trade setups based on divergences between price action and RSI movements.

## Key Components

### 1. RSI Calculation

- Uses a customizable RSI length (default: 60)

- Allows selection of the source for RSI calculation (default: close price)

### 2. Moving Average of RSI

- Supports multiple MA types: SMA, EMA, SMMA (RMA), WMA, VWMA, and Bollinger Bands

- Customizable MA length (default: 3)

- Option to display Bollinger Bands with adjustable standard deviation multiplier

### 3. Divergence Detection

- Implements both bullish and bearish divergence identification

- Uses pivot high and pivot low points to detect divergences

- Allows for customization of lookback periods and range for divergence detection

### 4. Entry Conditions

- Long Entry: Bullish divergence when RSI is below 40

- Short Entry: Bearish divergence when RSI is above 60

### 5. Trade Management

- Stop Loss: Customizable, default set to 11 pips

- Take Profit: Customizable, default set to 33 pips

### 6. Visualization

- Plots RSI line and its moving average

- Displays horizontal lines at 30, 50, and 70 RSI levels

- Shows Bollinger Bands when selected

- Highlights divergences with "Bull" and "Bear" labels on the chart

## Input Parameters

- RSI Length: Adjusts the period for RSI calculation

- RSI Source: Selects the price source for RSI (close, open, high, low, hl2, hlc3, ohlc4)

- MA Type: Chooses the type of moving average applied to RSI

- MA Length: Sets the period for the moving average

- BB StdDev: Adjusts the standard deviation multiplier for Bollinger Bands

- Show Divergence: Toggles the display of divergence labels

- Stop Loss: Sets the stop loss distance in pips

- Take Profit: Sets the take profit distance in pips

## Strategy Logic

1. **RSI Calculation**:

- Computes RSI using the specified length and source

- Calculates the chosen type of moving average on the RSI

2. **Divergence Detection**:

- Identifies pivot points in both price and RSI

- Checks for higher lows in RSI with lower lows in price (bullish divergence)

- Checks for lower highs in RSI with higher highs in price (bearish divergence)

3. **Trade Entry**:

- Enters a long position when a bullish divergence is detected and RSI is below 40

- Enters a short position when a bearish divergence is detected and RSI is above 60

4. **Position Management**:

- Places a stop loss order at the entry price ± stop loss pips (depending on the direction)

- Sets a take profit order at the entry price ± take profit pips (depending on the direction)

5. **Visualization**:

- Plots the RSI and its moving average

- Draws horizontal lines for overbought/oversold levels

- Displays Bollinger Bands if selected

- Shows divergence labels on the chart for identified setups

## Usage Instructions

1. Apply the script to a 1-minute XAUUSD (Gold) chart in TradingView

2. Adjust the input parameters as needed:

- Increase RSI Length for less frequent but potentially more reliable signals

- Modify MA Type and Length to change the sensitivity of the RSI moving average

- Adjust Stop Loss and Take Profit levels based on current market volatility

3. Monitor the chart for Bull (long) and Bear (short) labels indicating potential trade setups

4. Use in conjunction with other analysis and risk management techniques

## Considerations

- This strategy is designed for short-term scalping and may not be suitable for all market conditions

- Always backtest and forward test the strategy before using it with real capital

- The effectiveness of divergence-based strategies can vary depending on market trends and volatility

- Consider using additional confirmation signals or filters to improve the strategy's performance

Remember to adapt the strategy parameters to your risk tolerance and trading style, and always practice proper risk management.

MA MACD BB BackTesterOverview:

This Pine Script™ code provides a comprehensive backtesting tool that combines Moving Average (MA), Moving Average Convergence Divergence (MACD), and Bollinger Bands (BB). It is designed to help traders analyze market trends and make informed trading decisions by testing various strategies over historical data.

Key Features:

1. Customizable Indicators:

Moving Average (MA): Smooths out price data for clearer trend direction.

MACD: Measures trend momentum through MACD Line, Signal Line, and Histogram.

Bollinger Bands (BB): Identifies overbought or oversold conditions with upper and lower bands.

2. Flexible Trading Direction: Choose between long or short positions to adapt to different market conditions.

3. Risk Management: Efficiently allocate your capital with customizable position sizes.

4. Signal Generation:

Buy Signals: Triggered by crossovers for MACD, MA, and BB.

Sell Signals: Triggered by crossunders for MACD, MA, and BB.

5. Automated Trading: Automatically enter and exit trades based on signal conditions and strategy parameters.

How It Works:

1. Indicator Selection: Select your preferred indicator (MA, MACD, BB) and trading direction (Long/Short).

2. Risk Management Configuration: Set the percentage of capital to allocate per position to manage risk effectively.

3.Signal Detection: The algorithm identifies and plots buy/sell signals directly on the chart based on the chosen indicator.

4. Trade Execution: The strategy automatically enters and exits trades based on signal conditions and configured strategy parameters.

Use Cases:

- Backtesting: Evaluate the effectiveness of trading strategies using historical data to understand potential performance.

- Strategy Development: Customize and expand the strategy to incorporate additional indicators or conditions to fit specific trading styles.

ADDONS That Affect Strategy:

1. Indicator Parameters:

Adjustments to the settings of MACD (e.g., fast length, slow length), MA (e.g., length), and BB (e.g., length, multiplier) will directly impact the detection of signals and the strategy's performance.

2. Trading Direction:

Changing the trading direction (Long/Short) will alter the entry and exit conditions based on the detected signals.

3. Risk Management Settings:

Modifying the position size percentage affects capital allocation and overall risk exposure per trade.

ADDONS That Do Not Affect Strategy:

1. Visual Customizations:

Changes to the color, shape, and style of the plotted lines and signals do not impact the core functionality of the strategy but enhance visual clarity.

2. Text and Labels:

Modifying text labels for the signals (such as renaming "Buy MACD" to "MACD Buy Signal") is purely cosmetic and does not influence the strategy’s logic or outcomes.

Notes:

- Customization: The indicator is highly customizable to fit various trading styles and market conditions.

- Risk Management: Adjust position sizes and risk parameters according to your risk tolerance and account size.

- Optimization: Regularly backtest and optimize parameters to adapt to changing market dynamics for better performance.

Getting Started:

-Add the script to your chart.

-Adjust the input parameters to suit your analysis preferences.

-Observe the marked buy and sell signals on your chart to make informed trading decisions.

Uptrick:Intensity IndexPurpose:

The "Uptrick: Intensity Index" strategy is designed to provide traders with insights into the trend intensity of security by combining multiple moving averages and their relative positions. This versatile tool can be used effectively by both short-term and long-term traders to identify potential buy and sell signals based on specific conditions.

Explanation:

Input Parameters and Customization:

Moving Averages Lengths:

Adjust MA1, MA2, and MA3 lengths to change the calculation periods for the moving averages.

Trend Intensity Index SMA Length:

Adjust the length of the SMA applied to the TII.

Plot Colors:

Change the colors of the TII and TII MA plots for better visualization.

Background Colors and Transparency:

Set different colors for positive and negative TII MA values.

Control the transparency of the background color.

---------------------------------------------------------------------------

MA1 (Length 10): Short-term moving average, useful for capturing short-term market trends.

MA2 (Length 20): Medium-term moving average, providing a balanced view of market trends.

MA3 (Length 50): Long-term moving average, offering insights into long-term market trends.

The script calculates the relative positions of the closing price to each moving average (rel1, rel2, rel3) to determine how far the current price deviates from each average.

Trend Intensity Index (TII):

The TII is calculated as the average of the relative positions (rel1, rel2, rel3), multiplied by 100 to convert it into a percentage. This index reflects the overall intensity of the trend, considering short-term, medium-term, and long-term perspectives.

The TII is plotted in blue, providing a visual representation of trend intensity.

SMA of TII:

An additional SMA is applied to the TII (matii) to smooth out fluctuations and provide a clearer long-term trend signal.

The SMA of TII is plotted in orange, offering a reference for long-term trend analysis.

Determining Potential Price Movements:

For Short-Term Traders:

When the blue TII line crosses above the orange SMA of TII line, it indicates a potential buy signal.

When the blue TII line crosses below the orange SMA of TII line, it indicates a potential sell signal.

For Long-Term Traders:

When the orange SMA of TII line crosses above the highlighted 0 line, it indicates a potential buy signal.

When the orange SMA of TII line crosses below the highlighted 0 line, it indicates a potential sell signal.

Plotting and Visualization:

The TII and its SMA are plotted with distinct colors for easy identification.

A horizontal line at 0 is plotted in gray to serve as a reference point for long-term trend signals.

The background color changes based on the value of the SMA of TII (matii):

Green background for matii values above 0, indicating bullish conditions.

Red background for matii values below 0, indicating bearish conditions.

Utility and Potential Usage:

The "Uptrick: Intensity Index" indicator is a powerful tool for both short-term and long-term traders, offering clear buy and sell signals based on the crossover of the TII and its SMA, as well as the position of the SMA relative to the zero line.

By consolidating multiple moving averages and their relative positions into a single indicator, traders can gain comprehensive insights into market trends and intensity.

The ability to adjust all inputs and toggle visibility options enhances the flexibility and utility of the indicator, making it suitable for various trading styles and market conditions.

Through its versatile design and advanced features, the "Uptrick: Intensity Index" indicator equips traders with actionable insights into trend intensity and potential price movements. By integrating this robust tool into their trading strategies, traders can navigate the markets with greater precision and confidence, thereby enhancing their trading outcomes.

WHAT SETTINGS TO HAVE FOR THE MOVING AVERAGE:

Short-term traders (day traders) might prefer a shorter SMA length (e.g., 5-20 periods) as they are looking for quick signals and react to price changes more rapidly.

Medium-term traders (swing traders) might opt for a medium SMA length (e.g., 20-50 periods) which can filter out some noise and provide a clearer signal on the trend.

Long-term traders (position traders) might choose a longer SMA length (e.g., 50-200 periods) to get a broader view of the market trend and avoid reacting to short-term fluctuations.

Versatile Moving Average StrategyVersatile Moving Average Strategy (VMAS)

Overview:

The Versatile Moving Average Strategy (VMAS) is designed to provide traders with a flexible approach to trend-following, utilizing multiple types of moving averages. This strategy allows for customization in choosing the moving average type and length, catering to various market conditions and trading styles.

Key Features:

- Multiple Moving Average Types: Choose from SMA, EMA, SMMA (RMA), WMA, VWMA, HULL, LSMA, and ALMA to best suit your trading needs.

- Customizable Inputs: Adjust the moving average length, source of price data, and stop-loss source to fine-tune the strategy.

- Target Percent: Set the percentage difference between successive profit targets to manage your risk and rewards effectively.

- Position Management: Enable or disable long and short positions, allowing for versatility in different market conditions.

- Commission and Slippage: The strategy includes realistic commission settings to ensure accurate backtesting results.

Strategy Logic:

1. Moving Average Calculation: The selected moving average is calculated based on user-defined parameters.

2. Entry Conditions:

- A long position is entered when the entry source crosses over the moving average, if long positions are enabled.

- A short position is entered when the entry source crosses under the moving average, if short positions are enabled.

3. Stop-Loss: Positions are closed if the stop-loss source crosses the moving average in the opposite direction.

4. Profit Targets: Multiple profit targets are defined, with each target set at an incremental percentage above (for long positions) or below (for short positions) the entry price.

Default Properties:

- Account Size: $10000

- Commission: 0.01% per trade

- Risk Management: Positions are sized to risk 80% of the equity per trade, because we get very tight stoploss when position is open.

- Sample Size: Backtesting has been conducted to ensure a sufficient sample size of trades, ideally more than 100 trades.

How to Use:

1. Configure Inputs: Set your preferred moving average type, length, and other input parameters.

2. Enable Positions: Choose whether to enable long, short, or both types of positions.

3. Backtest and Analyze: Run backtests with realistic settings and analyze the results to ensure the strategy aligns with your trading goals.

4. Deploy and Monitor: Once satisfied with the backtesting results, deploy the strategy in a live environment and monitor its performance.

This strategy is suitable for traders looking to leverage moving averages in a versatile and customizable manner. Adjust the parameters to match your trading style and market conditions for optimal results.

Note: Ensure the strategy settings used for publication are the same as those described here. Always conduct thorough backtesting before deploying any strategy in a live trading environment.

Strategic Multi-Step Supertrend - Strategy [presentTrading]The code is mainly developed for me to stimulate the multi-step taking profit function for strategies. The result shows the drawdown can be reduced but at the same time reduced the profit as well. It can be a heuristic for futures leverage traders.

█ Introduction and How it is Different

The "Strategic Multi-Step Supertrend" is a trading strategy designed to leverage the power of multiple steps to optimize trade entries and exits across the Supertrend indicator. Unlike traditional strategies that rely on single entry and exit points, this strategy employs a multi-step approach to take profit, allowing traders to lock in gains incrementally. Additionally, the strategy is adaptable to both long and short trades, providing a comprehensive solution for dynamic market conditions.

This template strategy lies in its dual Supertrend calculation, which enhances the accuracy of trend detection and provides more reliable signals for trade entries and exits. This approach minimizes false signals and increases the overall profitability of trades by ensuring that positions are entered and exited at optimal points.

BTC 6h L/S Performance

█ Strategy, How It Works: Detailed Explanation

The "Strategic Multi-Step Supertrend Trader" strategy utilizes two Supertrend indicators calculated with different parameters to determine the direction and strength of the market trend. This dual approach increases the robustness of the signals, reducing the likelihood of entering trades based on false signals. Here is a detailed breakdown of how the strategy operates:

🔶 Supertrend Indicator Calculation

The Supertrend indicator is a trend-following overlay on the price chart, typically used to identify the direction of the trend. It is calculated using the Average True Range (ATR) to ensure that the indicator adapts to market volatility. The formula for the Supertrend indicator is:

Upper Band = (High + Low) / 2 + (Factor * ATR)

Lower Band = (High + Low) / 2 - (Factor * ATR)

Where:

- High and Low are the highest and lowest prices of the period.

- Factor is a user-defined multiplier.

- ATR is the Average True Range over a specified period.

The Supertrend changes its direction based on the closing price in relation to these bands.

🔶 Entry-Exit Conditions

The strategy enters long positions when both Supertrend indicators signal an uptrend, and short positions when both indicate a downtrend. Specifically:

- Long Condition: Supertrend1 < 0 and Supertrend2 < 0

- Short Condition: Supertrend1 > 0 and Supertrend2 > 0

- Long Exit Condition: Supertrend1 > 0 and Supertrend2 > 0

- Short Exit Condition: Supertrend1 < 0 and Supertrend2 < 0

🔶 Multi-Step Take Profit Mechanism

The strategy features a multi-step take profit mechanism, which allows traders to lock in profits incrementally. This is achieved through four user-configurable take profit levels. For each level, the strategy specifies a percentage increase (for long trades) or decrease (for short trades) in the entry price at which a portion of the position is exited:

- Step 1: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent1 / 100)

- Step 2: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent2 / 100)

- Step 3: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent3 / 100)

- Step 4: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent4 / 100)

This staggered exit strategy helps in locking profits at multiple levels, thereby reducing risk and increasing the likelihood of capturing the maximum possible profit from a trend.

BTC Local

█ Trade Direction

The strategy is highly flexible, allowing users to specify the trade direction. There are three options available:

- Long Only: The strategy will only enter long trades.

- Short Only: The strategy will only enter short trades.

- Both: The strategy will enter both long and short trades based on the Supertrend signals.

This flexibility allows traders to adapt the strategy to various market conditions and their own trading preferences.

█ Usage

1. Add the strategy to your trading platform and apply it to the desired chart.

2. Configure the take profit settings under the "Take Profit Settings" group.

3. Set the trade direction under the "Trade Direction" group.

4. Adjust the Supertrend settings in the "Supertrend Settings" group to fine-tune the indicator calculations.

5. Monitor the chart for entry and exit signals as indicated by the strategy.

█ Default Settings

- Use Take Profit: True

- Take Profit Percentages: Step 1 - 6%, Step 2 - 12%, Step 3 - 18%, Step 4 - 50%

- Take Profit Amounts: Step 1 - 12%, Step 2 - 8%, Step 3 - 4%, Step 4 - 0%

- Number of Take Profit Steps: 3

- Trade Direction: Both

- Supertrend Settings: ATR Length 1 - 10, Factor 1 - 3.0, ATR Length 2 - 11, Factor 2 - 4.0

These settings provide a balanced starting point, which can be customized further based on individual trading preferences and market conditions.

Chande Momentum Oscillator (CMO) Buy Sell Strategy [TradeDots]The "Chande Momentum Oscillator (CMO) Buy Sell Strategy" leverages the CMO indicator to identify short-term buy and sell opportunities.

HOW DOES IT WORK

The standard CMO indicator measures the difference between recent gains and losses, divided by the total price movement over the same period. However, this version of the CMO has some limitations.

The primary disadvantage of the original CMO is its responsiveness to short-term volatility, making the signals less smooth and more erratic, especially in fluctuating markets. This instability can lead to misleading buy or sell signals.

To address this, we integrated the concept from the Moving Average Convergence Divergence (MACD) indicator. By applying a 9-period exponential moving average (EMA) to the CMO line, we obtained a smoothed signal line. This line acts as a filter, identifying confirmed overbought or oversold states, thereby reducing the number of false signals.

Similar to the MACD histogram, we generate columns representing the difference between the CMO and its signal line, reflecting market momentum. We use this momentum indicator as a criterion for entry and exit points. Trades are executed when there's a convergence of CMO and signal lines during an oversold state, and they are closed when the CMO line diverges from the signal line, indicating increased selling pressure.

APPLICATION

Since the 9-period EMA smooths the CMO line, it's less susceptible to extreme price fluctuations. However, this smoothing also makes it more challenging to breach the original +50 and -50 benchmarks.

To increase trading opportunities, we've tightened the boundary ranges. Users can customize the target benchmark lines in the settings to adjust for the volatility of the underlying asset.

The 'cool down period' is essentially the number of bars that await before the next signal generation. This feature is employed to dodge the occurrence of multiple signals in a short period.

DEFAULT SETUP

Commission: 0.01%

Initial Capital: $10,000

Equity per Trade: 80%

Signal Cool Down Period: 5

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

VAWSI and Trend Persistance Reversal Strategy SL/TPThis is a completely revamped version of my "RSI and ATR Trend Reversal Strategy."

What's New?

The RSI has been replaced with an original indicator of mine, the "VAWSI," as I've elected to call it.

The standard RSI measures a change in an RMA to determine the strength of a movement.

The VAWSI performs very similarly, except it uses another original indicator of mine, the VAWMA.

VAWMA stands for "Volume (and) ATR Weight Moving Average." It takes an average of the volume and ATR and uses the ratio of each bar to weigh a moving average of the source.

It has the same formula as an RSI, but uses the VAWMA instead of an RMA.

Next we have the Trend Persistence indicator, which is an index on how long a trend has been persisting for. It is another original indicator. It takes the max deviation the source has from lowest/highest of a specified length. It then takes a cumulative measure of that amount, measures the change, then creates a strength index with that amount.

The VAWSI is a measure of an emerging trend, and the Trend Persistence indicator is a measure of how long a trend has persisted.

Finally, the 3rd main indicator, is a slight variation of an ATR. Rather than taking the max of source - low or high- source and source - source , it instead takes the max of high-low and the absolute value of source - the previous source. It then takes the absolute value of the change of this, and normalizes it with the source.

Inputs

Minimum SL/TP ensures that the Stop Loss and Take Profit still exist in untrendy markets. This is the minimum Amount that will always be applied.

VAWSI Weight is a divided by 100 multiplier for the VAWSI. So value of 200 means it is multiplied by 2. Think of it like a percentage.

Trend Persistence weight and ATR Weight are applied the same. Higher the number, the more impactful on the final calculation it is.

Combination Mult is an outright multiplier to the final calculation. So a 2.0 = * 2.0

Trend Persistence Smoothing Length is the length of the weighted moving average applied to the Trend Persistence Strength index.

Length Cycle Decimal is a replacement of length for the script.

Here we used BlackCat1402's Dynamic Length Calculation, which can be found on his page. With his permission we have implemented it into this script. Big shout out to them for not only creating, but allowing us to use it here.

The Length Cycle Decimal is used to calculate the dynamic length. Because TradingView only allows series int for their built-in library, a lot of the baseline indicators we use have to be manually recreated as functions in the following section.

The Strategy

As usual, we use Heiken Ashi values for calculations.

We begin by establishing the minimum SL/TP for use later.

Next we determine the amount of bars back since the last crossup or crossdown of our threshold line.

We then perform some normalization of our multipliers. We want a larger trend or larger VAWSI amount to narrow the threshold, so we have 1 divide them. This way, a higher reading outputs a smaller number and vice versa. We do this for both Trend Persistence, and the VAWSI.

The VAWSI we also normalize, where rather than it being a 0-100 reading of trend direction and strength, we absolute it so that as long as a trend is strong, regardless of direction, it will have a higher reading. With these normalized values, we add them together and simply subtract the ATR measurement rather than having 1 divide it.

Here you can see how the different measurements add up. A lower final number suggests imminent reversal, and a higher final number suggests an untrendy or choppy market.

ATR is in orange, the Trend Persistence is blue, the VAWSI is purple, and the final amount is green.

We take this final number and depending on the current trend direction, we multiply it by either the Highest or Lowest source since the last crossup or crossdown. We then take the highest or lowest of this calculation, and have it be our Stop Loss or Take Profit. This number cannot be higher/lower than the previous source to ensure a rapid spike doesn't immediately close your position on a still continuing trend. As well, the threshold cannot be higher/ lower than the the specified Stop Loss and Take Profit

Only after the source has fully crossed these lines do we consider it a crossup or crossdown. We confirm this with a barstate.isconfirmed to prevent repainting. Next, each time there is a crossup or crossdown we enter a long or a short respectively and plot accordingly.

I have the strategy configured to "process on order close" to ensure an accurate backtesting result. You could also set this to false and add a 1 bar delay to the "if crossup" and "if crossdown" lines under strategy so that it is calculated based on the open of the next bar.

Final Notes

The amounts have been preconfigured for performance on RIOT 5 Minute timeframe. Other timeframes are viable as well. With a few changes to the parameters, this strategy has backtested well on NVDA, AAPL, TSLA, and AMD. I recommend before altering settings to try other timeframes first.

This script does not seem to perform nearly as well in typically untrendy and choppy markets such as crypto and forex. With some setting changes, I have seen okay results with crypto, but overfitting could be the cause there.

Thank you very much, and please enjoy.

Custom Signal Oscillator StrategyThe CSO is made to help traders easily test their theories by subtracting the difference between two customizable plots(indicators) without having to search for strategies. The general purpose is to provide a tool to users without coding knowledge.

How to use :

Apply the indicator(s) to test

Go to the CSO strategy input settings and select the desired plots from the added indicators. (The back test will enter long or short depending on the fast signal crosses on the slow signal)

Pull up the strategy tester

Adjust the input settings on the selected indicator(s) to back test

For example, the published strategy is using the basis lines from two Donchian channels with varying length. This can be utilized with multiple overlays on the chart and oscillators that are operating on the same scale with each other. Since chart glows aren't extremely common, a glow option is included to stand out on the chart as the chain operator. A long only option for is also included for versatility.

Chande Kroll Trend Strategy (SPX, 1H) | PINEINDICATORSThe "Chande Kroll Stop Strategy" is designed to optimize trading on the SPX using a 1-hour timeframe. This strategy effectively combines the Chande Kroll Stop indicator with a Simple Moving Average (SMA) to create a robust method for identifying long entry and exit points. This detailed description will explain the components, rationale, and usage to ensure compliance with TradingView's guidelines and help traders understand the strategy's utility and application.

Objective

The primary goal of this strategy is to identify potential long trading opportunities in the SPX by leveraging volatility-adjusted stop levels and trend-following principles. It aims to capture upward price movements while managing risk through dynamically calculated stops.

Chande Kroll Stop Parameters:

Calculation Mode: Offers "Linear" and "Exponential" options for position size calculation. The default mode is "Exponential."

Risk Multiplier: An adjustable multiplier for risk management and position sizing, defaulting to 5.

ATR Period: Defines the period for calculating the Average True Range (ATR), with a default of 10.

ATR Multiplier: A multiplier applied to the ATR to set stop levels, defaulting to 3.

Stop Length: Period used to determine the highest high and lowest low for stop calculation, defaulting to 21.

SMA Length: Period for the Simple Moving Average, defaulting to 21.

Calculation Details:

ATR Calculation: ATR is calculated over the specified period to measure market volatility.

Chande Kroll Stop Calculation:

High Stop: The highest high over the stop length minus the ATR multiplied by the ATR multiplier.

Low Stop: The lowest low over the stop length plus the ATR multiplied by the ATR multiplier.

SMA Calculation: The 21-period SMA of the closing price is used as a trend filter.

Entry and Exit Conditions:

Long Entry: A long position is initiated when the closing price crosses over the low stop and is above the 21-period SMA. This condition ensures that the market is trending upward and that the entry is made in the direction of the prevailing trend.

Exit Long: The long position is exited when the closing price falls below the high stop, indicating potential downward movement and protecting against significant drawdowns.

Position Sizing:

The quantity of shares to trade is calculated based on the selected calculation mode (linear or exponential) and the risk multiplier. This ensures position size is adjusted dynamically based on current market conditions and user-defined risk tolerance.

Exponential Mode: Quantity is calculated using the formula: riskMultiplier / lowestClose * 1000 * strategy.equity / strategy.initial_capital.

Linear Mode: Quantity is calculated using the formula: riskMultiplier / lowestClose * 1000.

Execution:

When the long entry condition is met, the strategy triggers a buy signal, and a long position is entered with the calculated quantity. An alert is generated to notify the trader.

When the exit condition is met, the strategy closes the position and triggers a sell signal, accompanied by an alert.

Plotting:

Buy Signals: Indicated with an upward triangle below the bar.

Sell Signals: Indicated with a downward triangle above the bar.

Application

This strategy is particularly effective for trading the SPX on a 1-hour timeframe, capitalizing on price movements by adjusting stop levels dynamically based on market volatility and trend direction.

Default Setup

Initial Capital: $1,000

Risk Multiplier: 5

ATR Period: 10

ATR Multiplier: 3

Stop Length: 21

SMA Length: 21

Commission: 0.01

Slippage: 3 Ticks

Backtesting Results

Backtesting indicates that the "Chande Kroll Stop Strategy" performs optimally on the SPX when applied to the 1-hour timeframe. The strategy's dynamic adjustment of stop levels helps manage risk effectively while capturing significant upward price movements. Backtesting was conducted with a realistic initial capital of $1,000, and commissions and slippage were included to ensure the results are not misleading.

Risk Management

The strategy incorporates risk management through dynamically calculated stop levels based on the ATR and a user-defined risk multiplier. This approach ensures that position sizes are adjusted according to market volatility, helping to mitigate potential losses. Trades are sized to risk a sustainable amount of equity, adhering to the guideline of risking no more than 5-10% per trade.

Usage Notes

Customization: Users can adjust the ATR period, ATR multiplier, stop length, and SMA length to better suit their trading style and risk tolerance.

Alerts: The strategy includes alerts for buy and sell signals to keep traders informed of potential entry and exit points.

Pyramiding: Although possible, the strategy yields the best results without pyramiding.

Justification of Components

The Chande Kroll Stop indicator and the 21-period SMA are combined to provide a robust framework for identifying long trading opportunities in trending markets. Here is why they work well together:

Chande Kroll Stop Indicator: This indicator provides dynamic stop levels that adapt to market volatility, allowing traders to set logical stop-loss levels that account for current price movements. It is particularly useful in volatile markets where fixed stops can be easily hit by random price fluctuations. By using the ATR, the stop levels adjust based on recent market activity, ensuring they remain relevant in varying market conditions.

21-Period SMA: The 21-period SMA acts as a trend filter to ensure trades are taken in the direction of the prevailing market trend. By requiring the closing price to be above the SMA for long entries, the strategy aligns itself with the broader market trend, reducing the risk of entering trades against the overall market direction. This helps to avoid false signals and ensures that the trades are in line with the dominant market movement.

Combining these two components creates a balanced approach that captures trending price movements while protecting against significant drawdowns through adaptive stop levels. The Chande Kroll Stop ensures that the stops are placed at levels that reflect current volatility, while the SMA filter ensures that trades are only taken when the market is trending in the desired direction.

Concepts Underlying Calculations

ATR (Average True Range): Used to measure market volatility, which informs the stop levels.

SMA (Simple Moving Average): Used to filter trades, ensuring positions are taken in the direction of the trend.

Chande Kroll Stop: Combines high and low price levels with ATR to create dynamic stop levels that adapt to market conditions.

Risk Disclaimer

Trading involves substantial risk, and most day traders incur losses. The "Chande Kroll Stop Strategy" is provided for informational and educational purposes only. Past performance is not indicative of future results. Users are advised to adjust and personalize this trading strategy to better match their individual trading preferences and risk tolerance.

Intelle_city - World Cycle - Ath & Atl - Logarithmic - Strategy.Overview

Indicators: Strategy !

INTELLECT_city - World Cycle - ATH & ATL - Timeframe 1D and 1W - Logarithmic - Strategy - The Pi Cycle Top and Bottom Oscillator is an adaptation of the original Pi Cycle Top chart. It compares the 111-Day Moving Average circle and the 2 * 350-Day Moving Average circle of Bitcoin’s Price. These two moving averages were selected as 350 / 111 = 3.153; An approximation of the important mathematical number Pi.

When the 111-Day Moving Average circle reaches the 2 * 350-Day Moving Average circle, it indicates that the market is becoming overheated. That is because the mid time frame momentum reference of the 111-Day Moving Average has caught up with the long timeframe momentum reference of the 2 * 350-Day Moving Average.

Historically this has occurred within 3 days of the very top of each market cycle.

When the 111 Day Moving Average circle falls back beneath the 2 * 350 Day Moving Average circle, it indicates that the market momentum of that cycle is significantly cooling down. The oscillator drops down into the lower green band shown where the 111 Day Moving Average is moving at a 75% discount relative to the 2 * 350 Day Moving Average.

Historically, this has highlighted broad areas of bear market lows.

IMPORTANT: You need to set a LOGARITHMIC graph. (The function is located at the bottom right of the screen)

IMPORTANT: The INTELLECT_city indicator is made for a buy-sell strategy; there is also a signal indicator from INTELLECT_city

IMPORTANT: The Chart shows all cycles, both buying and selling.

IMPORTANT: Suitable timeframes are 1 daily (recommended) and 1 weekly

-----------------------------

Описание на русском:

-----------------------------

Обзор индикатора

INTELLECT_city - World Cycle - ATH & ATL - Timeframe 1D and 1W - Logarithmic - Strategy - Логарифмический - Сигнал - Осциллятор вершины и основания цикла Пи представляет собой адаптацию оригинального графика вершины цикла Пи. Он сравнивает круг 111-дневной скользящей средней и круг 2 * 350-дневной скользящей средней цены Биткойна. Эти две скользящие средние были выбраны как 350/111 = 3,153; Приближение важного математического числа Пи.

Когда круг 111-дневной скользящей средней достигает круга 2 * 350-дневной скользящей средней, это указывает на то, что рынок перегревается. Это происходит потому, что опорный моментум среднего временного интервала 111-дневной скользящей средней догнал опорный момент импульса длинного таймфрейма 2 * 350-дневной скользящей средней.

Исторически это происходило в течение трех дней после вершины каждого рыночного цикла.

Когда круг 111-дневной скользящей средней опускается ниже круга 2 * 350-дневной скользящей средней, это указывает на то, что рыночный импульс этого цикла значительно снижается. Осциллятор опускается в нижнюю зеленую полосу, показанную там, где 111-дневная скользящая средняя движется со скидкой 75% относительно 2 * 350-дневной скользящей средней.

Исторически это высветило широкие области минимумов медвежьего рынка.

ВАЖНО: Выставлять нужно ЛОГАРИФМИЧЕСКИЙ график. (Находиться функция с правой нижней части экрана)

ВАЖНО: Индикатор INTELLECT_city сделан для стратегии покупок продаж, есть также и сигнальный от INTELLECT_сity

ВАЖНО: На Графике видны все циклы, как на покупку так и на продажу.

ВАЖНО: Подходящие таймфреймы 1 дневной (рекомендовано) и 1 недельный

-----------------------------

Beschreibung - Deutsch

-----------------------------

Indikatorübersicht

INTELLECT_city – Weltzyklus – ATH & ATL – Zeitrahmen 1T und 1W – Logarithmisch – Strategy – Der Pi-Zyklus-Top- und Bottom-Oszillator ist eine Anpassung des ursprünglichen Pi-Zyklus-Top-Diagramms. Er vergleicht den 111-Tage-Gleitenden-Durchschnittskreis und den 2 * 350-Tage-Gleitenden-Durchschnittskreis des Bitcoin-Preises. Diese beiden gleitenden Durchschnitte wurden als 350 / 111 = 3,153 ausgewählt; eine Annäherung an die wichtige mathematische Zahl Pi.

Wenn der 111-Tage-Gleitenden-Durchschnittskreis den 2 * 350-Tage-Gleitenden-Durchschnittskreis erreicht, deutet dies darauf hin, dass der Markt überhitzt. Das liegt daran, dass der Momentum-Referenzwert des 111-Tage-Gleitenden-Durchschnitts im mittleren Zeitrahmen den Momentum-Referenzwert des 2 * 350-Tage-Gleitenden-Durchschnitts im langen Zeitrahmen eingeholt hat.

Historisch gesehen geschah dies innerhalb von 3 Tagen nach dem Höhepunkt jedes Marktzyklus.

Wenn der Kreis des 111-Tage-Durchschnitts wieder unter den Kreis des 2 x 350-Tage-Durchschnitts fällt, deutet dies darauf hin, dass die Marktdynamik dieses Zyklus deutlich nachlässt. Der Oszillator fällt in das untere grüne Band, in dem der 111-Tage-Durchschnitt mit einem Abschlag von 75 % gegenüber dem 2 x 350-Tage-Durchschnitt verläuft.

Historisch hat dies breite Bereiche mit Tiefstständen in der Baisse hervorgehoben.

WICHTIG: Sie müssen ein logarithmisches Diagramm festlegen. (Die Funktion befindet sich unten rechts auf dem Bildschirm)

WICHTIG: Der INTELLECT_city-Indikator ist für eine Kauf-Verkaufs-Strategie konzipiert; es gibt auch einen Signalindikator von INTELLECT_city

WICHTIG: Das Diagramm zeigt alle Zyklen, sowohl Kauf- als auch Verkaufszyklen.

WICHTIG: Geeignete Zeitrahmen sind 1 täglich (empfohlen) und 1 wöchentlich

BBTrend w SuperTrend decision - Strategy [presentTrading]This strategy aims to improve upon the performance of Traidngview's newly published "BB Trend" indicator by incorporating the SuperTrend for better trade execution and risk management. Enjoy :)

█Introduction and How it is Different

The "BBTrend w SuperTrend decision - Strategy " is a trading strategy designed to identify market trends using Bollinger Bands and SuperTrend indicators. What sets this strategy apart is its use of two Bollinger Bands with different lengths to capture both short-term and long-term market trends, providing a more comprehensive view of market dynamics. Additionally, the strategy includes customizable take profit (TP) and stop loss (SL) settings, allowing traders to tailor their risk management according to their preferences.

BTCUSD 4h Long Performance

█ Strategy, How It Works: Detailed Explanation

The BBTrend strategy employs two key indicators: Bollinger Bands and SuperTrend.

🔶 Bollinger Bands Calculation:

- Short Bollinger Bands**: Calculated using a shorter period (default 20).

- Long Bollinger Bands**: Calculated using a longer period (default 50).

- Bollinger Bands use the standard deviation of price data to create upper and lower bands around a moving average.

Upper Band = Middle Band + (k * Standard Deviation)

Lower Band = Middle Band - (k * Standard Deviation)

🔶 BBTrend Indicator:

- The BBTrend indicator is derived from the absolute differences between the short and long Bollinger Bands' lower and upper values.

BBTrend = (|Short Lower - Long Lower| - |Short Upper - Long Upper|) / Short Middle * 100

🔶 SuperTrend Indicator:

- The SuperTrend indicator is calculated using the average true range (ATR) and a multiplier. It helps identify the market trend direction by plotting levels above and below the price, which act as dynamic support and resistance levels. * @EliCobra makes the SuperTrend Toolkit. He is GOAT.

SuperTrend Upper = HL2 + (Factor * ATR)

SuperTrend Lower = HL2 - (Factor * ATR)

The strategy determines market trends by checking if the close price is above or below the SuperTrend values:

- Uptrend: Close price is above the SuperTrend lower band.

- Downtrend: Close price is below the SuperTrend upper band.

Short: 10 Long: 20 std 2

Short: 20 Long: 40 std 2

Short: 20 Long: 40 std 4

█ Trade Direction

The strategy allows traders to choose their trading direction:

- Long: Enter long positions only.

- Short: Enter short positions only.

- Both: Enter both long and short positions based on market conditions.

█ Usage

To use the "BBTrend - Strategy " effectively:

1. Configure Inputs: Adjust the Bollinger Bands lengths, standard deviation multiplier, and SuperTrend settings.

2. Set TPSL Conditions: Choose the take profit and stop loss percentages to manage risk.

3. Choose Trade Direction: Decide whether to trade long, short, or both directions.

4. Apply Strategy: Apply the strategy to your chart and monitor the signals for potential trades.

█ Default Settings

The default settings are designed to provide a balance between sensitivity and stability:

- Short BB Length (20): Captures short-term market trends.

- Long BB Length (50): Captures long-term market trends.

- StdDev (2.0): Determines the width of the Bollinger Bands.

- SuperTrend Length (10): Period for calculating the ATR.

- SuperTrend Factor (12): Multiplier for the ATR to adjust the SuperTrend sensitivity.

- Take Profit (30%): Sets the level at which profits are taken.

- Stop Loss (20%): Sets the level at which losses are cut to manage risk.

Effect on Performance

- Short BB Length: A shorter length makes the strategy more responsive to recent price changes but can generate more false signals.

- Long BB Length: A longer length provides smoother trend signals but may be slower to react to price changes.

- StdDev: Higher values create wider bands, reducing the frequency of signals but increasing their reliability.

- SuperTrend Length and Factor: Shorter lengths and higher factors make the SuperTrend more sensitive, providing quicker signals but potentially more noise.

- Take Profit and Stop Loss: Adjusting these levels affects the risk-reward ratio. Higher take profit percentages can increase gains but may result in fewer closed trades, while higher stop loss percentages can decrease the likelihood of being stopped out but increase potential losses.

Momentum Alligator 4h Bitcoin StrategyOverview

The Momentum Alligator 4h Bitcoin Strategy is a trend-following trading system that operates on dual time frames. It utilizes the 1D Williams Alligator indicator to identify the prevailing major price trend and seeks trading opportunities on the 4-hour (4h) time frame when the momentum is turning up. The strategy is designed to close trades if the trend fails to develop or holding position if price continues increasing without any significant correction. Note that this strategy is specifically tailored for the 4-hour time frame.

Unique Features

2-layers market noise filtering system: Trades are only initiated in the direction of the 1D trend, determined by the Williams Alligator indicator. This higher time frame confirmation filters out minor trade signals, focusing on more substantial opportunities. At the same time, strategy has additional filter on 4h time frame with Awesome Oscillator which is showing the current price momentum.

Flexible Risk Management: The strategy exclusively opens long positions, resulting in fewer trades during bear markets. It incorporates a dynamic stop-loss mechanism, which can either follow the jaw line of the 4h Alligator or a user-defined fixed stop-loss. This flexibility helps manage risk and avoid non-trending markets.

Methodology

The strategy initiates a long position when the d-line of Stochastic RSI crosses up it's k-line. It means that there is a high probability that price momentum reversed from down to up. To avoid overtrading in potentially choppy markets, it skips the next two trades following a winning trade, anticipating sideways movement after a significant price surge.

This strategy has two layers trades filtering system: 4h and 1D time frames. The first one is awesome oscillator. It shall be increasing and value has to be higher than it's 5-period SMA. This is an additional confirmation that long trade is opened in the direction of the current momentum. As it was mentioned above, all entry signals are validated against the 1D Williams Alligator indicator. A trade is only opened if the price is above all three lines of the 1D Alligator, ensuring alignment with the major trend.

A trade is closed if the price hits the 4h jaw line of the Alligator or reaches the user-defined stop-loss level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 2% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Stochastic RSI on 4h time frame to open long trade when momentum started reversing to the upside. On the one hand, Stochastic RSI is one of the most sensitive indicator, which allows to react fast on the potential trend reversal. On the other hand, this indicator can be too sensitive and provide a lot of false trend changing signals. To eliminate this weakness we use two-layers trades filtering system.

The first layer is the 4h Awesome oscillator. This is less sensitive momentum indicator. Usually it starts increasing when price has already passed significant distance from the actual reversal point. The strategy opens long trade only is Awesome oscillator is increasing and above it's 5-period SMA. This approach increases the probability to filter the false signals during the choppy market or if the reversal is false.

The second layer filter is the Williams Alligator indicator on 1D time frame. The 1D Alligator serves as a filter for identifying the primary trend and increases probability to avoid the trades with low potential because trading against major trend usually is more risky. It's much better to catch the trend continuation than local bounce.

Last but not least feature of this strategy is close trades condition. It uses the flexible approach. First of all, user can set up the fixed stop-loss according to his own risk-tolerance, by default this value is 2% of price movement. It restricts the potential loss at the moment when trade has just been opened. Moreover strategy utilizes the 4h Williams Alligator's jaw line to exit the trade. If price fell below it trade is closed. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results:

Operating window: Date range of backtests is 2021.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -3.04%

Maximum Single Profit: +29.67%

Net Profit: +6228.01 USDT (+62.28%)

Total Trades: 118 (24.58% win rate)

Profit Factor: 1.71

Maximum Accumulated Loss: 1527.69 USDT (-11.52%)

Average Profit per Trade: 52.78 USDT (+0.89%)

Average Trade Duration: 60 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use:

Add the script to favorites for easy access.

Apply to the 4h timeframe desired chart (optimal performance observed on the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Random Entry and ExitStrategy for Researching Whether It Is Possible to Earn Consistently by Opening Random Trades

The essence of the strategy lies in generating random entries and exits based on pseudorandom numbers. The generation of pseudorandom numbers is performed by the function random_number based on the value of the seed variable. The variables entry_threshold and exit_threshold control the frequency of entries and exits. Lower values mean less frequent trades. To increase the number of trades, increase the values of these variables.

The strategy was created as part of research into whether it is possible to earn randomly in financial markets by making chaotic actions of opening and closing trades. However, it adheres to a few rules: open only long positions (in the direction of the global trend) and do not use leverage. Positions are opened with the entire available capital.

100 generations of the strategy on the daily chart of the S&P 500 (seed 1-101) give 100% positive mathematical expectations. Similar results are observed on higher timeframes of assets that are in a global uptrend.

There is also the possibility of opening only short positions for the research. Note that the logic of the strategy is built in such a way that only one trading direction can operate simultaneously (either longs or shorts). On higher timeframes, random shorts show negative results. Positive mathematical expectations for short positions can be found on lower timeframes (1 min, etc.), where a large amount of noise is observed.

---------------------------------------------------------------------------------------------------

Стратегия для исследования, можно ли стабильно зарабатывать при открытии случайных сделок

Суть стратегии заключается в генерации случайных входов и выходов на основе псевдослучайных чисел. Генерация псевдослучайных чисел происходит функцией random_number на основе значения переменной seed. Переменные entry_threshold и exit_threshold контролируют частоту входов и выходов. Более низкие значения означают менее частые сделки. Для увеличения количества сделок - увеличивайте значения переменных.

Стратегия создавалась в рамках исследования вопроса, можно ли случайным образом зарабатывать на фин. рынках, совершая хаотичные открытия и закрытия сделок. НО, придерживаясь нескольких правил: открывать только длинные позиции (в сторону глобального тренда) и не использовать кредитные плечи. Открытие позиций происходит на весь доступный капитал.

100 генераций стратегии на дневном графике S&P500 (seed 1-101) дают 100% положительных математических ожиданий. Похожие результаты наблюдаются на высоких таймфреймах активов, которые глобально находятся в восходящем тренде.

Также для исследования предусмотрена возможность открытия только коротких позиций. Обратите внимание, что логика стратегии построена таким образом, что одновременно может работать только одно направление торговли (либо лонги, либо шорты). На старших таймфреймах случайные шорты показывают негативные результаты. Положительное математическое ожидание для коротких позиций можно обнаружить на младших таймфреймах (1 min, etc), где наблюдается большое количество шумов.

Bitcoin Futures vs. Spot Tri-Frame - Strategy [presentTrading]Prove idea with a backtest is always true for trading.

I developed and open-sourced it as an educational material for crypto traders to understand that the futures and spot spread may be effective but not be as effective as they might think. It serves as an indicator of sentiment rather than a reliable predictor of market trends over certain periods. It is better suited for specific trading environments, which require further research.

█ Introduction and How it is Different

The "Bitcoin Futures vs. Spot Tri-Frame Strategy" utilizes three different timeframes to calculate the Z-Score of the spread between BTC futures and spot prices on Binance and OKX exchanges. The strategy executes long or short trades based on composite Z-Score conditions across the three timeframes.

The spread refers to the difference in price between BTC futures and BTC spot prices, calculated by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges.

BTCUSD 1D L/S Performance

█ Strategy, How It Works: Detailed Explanation

🔶 Calculation of the Spread

The spread is the difference in price between BTC futures and BTC spot prices. The strategy calculates the spread by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges. This spread serves as the primary metric for identifying trading opportunities.

Spread = Weighted Average Futures Price - Weighted Average Spot Price

🔶 Z-Score Calculation

The Z-Score measures how many standard deviations the current spread is from its historical mean. This is calculated for each timeframe as follows:

Spread Mean_tf = SMA(Spread_tf, longTermSMA)

Spread StdDev_tf = STDEV(Spread_tf, longTermSMA)

Z-Score_tf = (Spread_tf - Spread Mean_tf) / Spread StdDev_tf

Local performance

🔶 Composite Entry Conditions

The strategy triggers long and short entries based on composite Z-Score conditions across all three timeframes:

- Long Condition: All three Z-Scores must be greater than the long entry threshold.

Long Condition = (Z-Score_tf1 > zScoreLongEntryThreshold) and (Z-Score_tf2 > zScoreLongEntryThreshold) and (Z-Score_tf3 > zScoreLongEntryThreshold)

- Short Condition: All three Z-Scores must be less than the short entry threshold.

Short Condition = (Z-Score_tf1 < zScoreShortEntryThreshold) and (Z-Score_tf2 < zScoreShortEntryThreshold) and (Z-Score_tf3 < zScoreShortEntryThreshold)

█ Trade Direction

The strategy allows the user to specify the trading direction:

- Long: Only long trades are executed.

- Short: Only short trades are executed.

- Both: Both long and short trades are executed based on the Z-Score conditions.

█ Usage

The strategy can be applied to BTC or Crypto trading on major exchanges like Binance and OKX. By leveraging discrepancies between futures and spot prices, traders can exploit market inefficiencies. This strategy is suitable for traders who prefer a statistical approach and want to diversify their timeframes to validate signals.

█ Default Settings

- Input TF 1 (60 minutes): Sets the first timeframe for Z-Score calculation.

- Input TF 2 (120 minutes): Sets the second timeframe for Z-Score calculation.

- Input TF 3 (180 minutes): Sets the third timeframe for Z-Score calculation.

- Long Entry Z-Score Threshold (3): Defines the threshold above which a long trade is triggered.

- Short Entry Z-Score Threshold (-3): Defines the threshold below which a short trade is triggered.

- Long-Term SMA Period (100): The period used to calculate the simple moving average for the spread.

- Use Hold Days (true): Enables holding trades for a specified number of days.

- Hold Days (5): Number of days to hold the trade before exiting.

- TPSL Condition (None): Defines the conditions for taking profit and stop loss.

- Take Profit (%) (30.0): The percentage at which the trade will take profit.

- Stop Loss (%) (20.0): The percentage at which the trade will stop loss.

By fine-tuning these settings, traders can optimize the strategy to suit their risk tolerance and trading style, enhancing overall performance.

Double Vegas SuperTrend Enhanced - Strategy [presentTrading]

█ Introduction and How It Is Different

The "Double Vegas SuperTrend Enhanced" strategy is a sophisticated trading system that combines two Vegas SuperTrend Enhanced. Very Powerful!

Let's celebrate the joy of Children's Day on June 1st! Enjoyyy!

BTCUSD LS performance

The strategy aims to pinpoint market trends with greater accuracy and generate trades that align with the overall market direction.

This approach differentiates itself by integrating volatility adjustments and leveraging the Vegas Channel's width to refine the SuperTrend calculations, resulting in a dynamic and responsive trading system.

Additionally, the strategy incorporates customizable take-profit and stop-loss levels, providing traders with a robust framework for risk management.

-> check Vegas SuperTrend Enhanced - Strategy

█ Strategy, How It Works: Detailed Explanation

🔶 Vegas Channel and SuperTrend Calculations

The strategy initiates by calculating the Vegas Channel, which is derived from a simple moving average (SMA) and the standard deviation (STD) of the closing prices over a specified window length. This channel helps in measuring market volatility and forms the basis for adjusting the SuperTrend indicator.

Vegas Channel Calculation:

- vegasMovingAverage = SMA(close, vegasWindow)

- vegasChannelStdDev = STD(close, vegasWindow)

- vegasChannelUpper = vegasMovingAverage + vegasChannelStdDev

- vegasChannelLower = vegasMovingAverage - vegasChannelStdDev

SuperTrend Multiplier Adjustment:

- channelVolatilityWidth = vegasChannelUpper - vegasChannelLower

- adjustedMultiplier = superTrendMultiplierBase + volatilityAdjustmentFactor * (channelVolatilityWidth / vegasMovingAverage)

The adjusted multiplier enhances the SuperTrend's sensitivity to market volatility, making it more adaptable to changing market conditions.

BTCUSD Local picture.

🔶 Average True Range (ATR) and SuperTrend Values

The ATR is computed over a specified period to measure market volatility. Using the ATR and the adjusted multiplier, the SuperTrend upper and lower levels are determined.

ATR Calculation:

- averageTrueRange = ATR(atrPeriod)

**SuperTrend Calculation:**

- superTrendUpper = hlc3 - (adjustedMultiplier * averageTrueRange)

- superTrendLower = hlc3 + (adjustedMultiplier * averageTrueRange)

The SuperTrend levels are continuously updated based on the previous values and the current market trend direction. The market trend is determined by comparing the closing prices with the SuperTrend levels.

Trend Direction:

- If close > superTrendLowerPrev, then marketTrend = 1 (bullish)

- If close < superTrendUpperPrev, then marketTrend = -1 (bearish)

🔶 Trade Entry and Exit Conditions

The strategy generates trade signals based on the alignment of both SuperTrends. Trades are executed only when both SuperTrends indicate the same market direction.

Entry Conditions:

- Long Position: Both SuperTrends must signal a bullish trend.

- Short Position: Both SuperTrends must signal a bearish trend.

Exit Conditions:

- Positions are exited if either SuperTrend reverses its trend direction.

- Additional conditions include holding periods and configurable take-profit and stop-loss levels.

█ Trade Direction

The strategy allows traders to specify the desired trade direction through a customizable input setting. Options include:

- Long: Only enter long positions.

- Short: Only enter short positions.

- Both: Enter both long and short positions based on the market conditions.

█ Usage

To utilize the "Double Vegas SuperTrend Enhanced" strategy, traders need to configure the input settings according to their trading preferences and market conditions. The strategy includes parameters for ATR periods, Vegas Channel window lengths, SuperTrend multipliers, volatility adjustment factors, and risk management settings such as hold days, take-profit, and stop-loss percentages.

█ Default Settings

The strategy comes with default settings that can be adjusted to fit individual trading styles:

- trade Direction: Both (allows trading in both long and short directions for maximum flexibility).

- ATR Periods: 10 for SuperTrend 1 and 5 for SuperTrend 2 (shorter ATR period results in more sensitivity to recent price movements).

- Vegas Window Lengths: 100 for SuperTrend 1 and 200 for SuperTrend 2 (longer window length results in smoother moving averages and less sensitivity to short-term volatility).

- SuperTrend Multipliers: 5 for SuperTrend 1 and 7 for SuperTrend 2 (higher multipliers lead to wider SuperTrend channels, reducing the frequency of trades).

- Volatility Adjustment Factors: 5 for SuperTrend 1 and 7 for SuperTrend 2 (higher adjustment factors increase the responsiveness to changes in market volatility).

- Hold Days: 5 (defines the minimum duration a position is held, ensuring trades are not exited prematurely).

- Take Profit: 30% (sets the target profit level to lock in gains).

- Stop Loss: 20% (sets the maximum acceptable loss level to mitigate risk).

Mateo's Time of Day Analysis LEThis strategy takes a trade every day at a specified time and then closes it at a specified time.

The purpose of this strategy is to help determine if there are better times to day to buy or sell.

I was originally inspired to write this when a YouTuber stated that SPX had been up during the last 30 minutes of the day over 80% of the time the past year. No matter who says it, test it, and in my opinion, TradingView is one of the easiest placed to do that! Unfortunately, that particular claim did not turn out to be accurate, but this tool remains for those who want to optimize timing their entries and exits at specific times of day.

market slayerInput Parameters:

Various input parameters allow customization of the strategy, including options to show trend confirmation, specify trend timeframes and values, set SMA lengths, enable take profit and stop loss, and define their respective values.

Calculations:

Simple Moving Averages (SMAs) are calculated based on the specified lengths.

Buy and sell signals are generated based on the crossover and crossunder of the short and long SMAs.

Confirmation Bars:

Functions are defined to determine bullish or bearish confirmation bars based on certain conditions.

These confirmation bars are used to confirm trend direction and generate additional signals.

Plotting:

SMAs are plotted on the chart.

Trend labels and signal markers are plotted based on the calculated conditions.

Trade Signals:

Buy and sell conditions are defined based on the crossover/crossunder of SMAs and confirmation of trend direction.

Strategy entries and exits are executed accordingly.

Take Profit and Stop Loss:

Optional take profit and stop loss functionality is included.

Trades are automatically closed when profit or loss thresholds are reached.

Closing Trades:

Trades are also closed based on changes in trend confirmation bars to ensure alignment with the overall market direction.

Alerts:

Alert conditions are defined for opening and closing trades, providing notifications when certain conditions are met.

Overall, this script aims to provide a systematic approach to trading by combining moving average crossovers with trend confirmation bars, along with options for risk management through take profit and stop loss orders. Users can customize various parameters to adapt the strategy to different market conditions and trading preferences.

The script uses the request.security() function with the lookahead parameter set to barmerge.lookahead_on to access data from a higher timeframe within the Pine Script on TradingView. Let's break down why it's used:

Higher Timeframe Analysis:

By default, Pine Script operates on the timeframe of the chart it's applied to. However, in trading strategies, it's common to incorporate signals or data from higher timeframes to confirm or validate signals generated on lower timeframes. This helps traders to align their trades with the broader market trend.

Trend Confirmation:

In this script, the confirmationTrendTimeframe parameter allows users to specify a higher timeframe for trend confirmation. The request.security() function fetches the data from this higher timeframe and applies the defined conditions to confirm the trend direction.

Lookahead Behavior:

The lookahead parameter set to barmerge.lookahead_on ensures that the script considers the most up-to-date information available on the higher timeframe when making trading decisions on the lower timeframe. This prevents the script from lagging behind or using outdated data, enhancing the accuracy of trend confirmation.

Usage in confirmationTrendBullish and confirmationTrendBearish:

These variables are assigned the values returned by the request.security() function, which represents the bullish or bearish trend confirmation based on the conditions applied to the data from the higher timeframe.

Entry Fragger - Strategy

For basic instructions please visit my other script "Entry Fragger".

The Signal Logic is explained there.

v1.4:

- Added advanced backtesting with fully customizable entries.

- Fully automated Buy Signals (profitable).

- Adjustable timeframes for signal logic. (requested)

Every setting affects the accuracy and profitability greatly now, based on settings applied.

The strategy performs best on high timeframes with larger capital and no leverage.

Useless for Forex, but absolutely smashes stocks and crypto on mid to high timeframes.

Please read through my other scripts description.

Set values as preferred and try your assets.

It does NOT work on low timeframes and forex!

Hint: BTC 4H, Custom Timeframe 1h, Moon Mode and Show Sell Signals enabled, R2R: 2.

KumoTrade Ichimoku StrategyThe KumoTrade Ichimoku Strategy is an advanced trading strategy designed to help users identify market trends and potential trading opportunities using the Ichimoku Kinko Hyo technical analysis indicator. This strategy leverages the Ichimoku cloud (Kumo) along with other crucial indicators such as the Tenkan-sen and Kijun-sen lines to generate strong signals.

Main Components of the Strategy:

Tenkan-sen (Conversion Line): Indicates the short-term direction of the price, typically calculated as the average of the highest high and the lowest low over the past 9 periods.

Kijun-sen (Base Line): Indicates the medium-term direction of the price, usually calculated as the average of the highest high and the lowest low over the past 26 periods.

Senkou Span A and Senkou Span B: These two lines form the cloud (Kumo), which projects future support and resistance levels.

Chikou Span (Lagging Span): Plots the current closing price 26 periods back to measure the market's momentum.

Strategy Rules:

Bullish Bias (Bias Bull): Indicates that the prices are in a long-term uptrend. In this strategy, this is confirmed if the low prices are above the daily EMA (Exponential Moving Average).

Kijun Sen Touch Down: Occurs when prices cross below the Kijun-sen line and then close back above it, indicating a potential bullish reversal.

Tenkan-Kijun Cross Up: A bullish signal generated when the Tenkan-sen line crosses above the Kijun-sen line.

Close Over Tenkan and Kijun: A strong bullish signal when the close price crosses above both the Tenkan-sen and Kijun-sen lines.

Trading Setups:

Long Setup: Generated when the Kijun-sen is above the highest point of the Kumo (senkou_max) and the closing price is below the lowest point of the Kumo (senkou_min). This setup is checked over the last 21 bars.

Short Setup: Generated when the Kijun-sen is below the lowest point of the Kumo (senkou_min) and the closing price is above the highest point of the Kumo (senkou_max). This setup is also checked over the last 21 bars. (Not avalible yet)

Entry Conditions:

Ultra Long Entry: This condition checks for a bullish bias, the Tenkan-Kijun cross up or Kijun Sen touch down, high volume, and that the price is not within the Kumo cloud.

Main Long Entry: This condition requires the closing price to be above the Kumo cloud, a green Kumo cloud, a bullish bias, the Tenkan rule, and that the price is not within the Kumo cloud.

Exit Conditions:

A trailing stop loss is implemented to protect profits. The stop loss level is dynamically updated based on the highest high of the last 5 bars minus three times the ATR (Average True Range) value.

Visuals on the Chart:

The Tenkan-sen and Kijun-sen lines are plotted for visual reference.

The Kumo cloud is displayed with different colors indicating bullish (green) or bearish (red) conditions.

Entry points are marked on the chart, and the trailing stop loss levels are plotted as well.

The KumoTrade Ichimoku Strategy aims to provide a comprehensive approach to trading by combining multiple aspects of the Ichimoku indicator to generate reliable trading signals and manage risk effectively.

Korneev Reverse RSIRethinking the Legendary Relative Strength Index by John Welles Wilder

The essence of the new approach lies in the reverse use of the so-called "overbought" and "oversold" zones. In his 1978 book, "New Concepts in Technical Trading Systems," where the RSI mechanism was thoroughly described, Wilder writes that one way to use the oscillator is to open a long position when the RSI drops into oversold territory (below 30) and to open a short position when the RSI rises to overbought levels (above 70). However, backtesting this strategy with such inputs yields rather mediocre results.

Based on the calculation formula, the RSI calculates the rate of price change over a certain period. Therefore, overbought and oversold zones will have relative significance (relative to the set calculation period). It is no coincidence that the word "relative" was added to the name of the oscillator. It is worth accepting as an axiom the assertion that the price of an asset is fair at every moment in time.