arpit bollinger bandStrategy Overview:

This strategy utilizes Bollinger Bands based on a 20-period Exponential Moving Average (EMA) with a standard deviation multiplier of 1.5. It is designed to generate early trading signals based on the relationship between the price action and the Bollinger Bands.

Bollinger Bands Calculation:

The upper Bollinger Band is calculated as the 20-period EMA of the closing prices plus 1.5 times the standard deviation of the same period.

The lower Bollinger Band is calculated as the 20-period EMA of the closing prices minus 1.5 times the standard deviation.

Entry Criteria:

Buy Signal: A buy signal is generated when the current candle's high exceeds the high of the candle two periods ago, which had closed below the lower Bollinger Band. This condition implies an anticipation of a bullish reversal.

Sell Signal: A sell signal is generated when the current candle's low falls below the low of the candle two periods ago, which had closed above the upper Bollinger Band. This condition suggests an anticipated bearish reversal.

Stop Loss and Take Profit:

The stop loss for a buy order is set slightly below the low of the current candle, and for a sell order, it is set slightly above the high of the current candle.

The take profit level is determined based on a predefined risk-reward ratio of 1:3. This means the take profit target is set at a distance three times greater than the distance between the entry price and the stop loss.

Risk Management:

The strategy includes an input option to adjust the risk-reward ratio, allowing for flexibility in managing the trade's potential risk versus reward.

Trade Execution:

The strategy automatically plots the buy and sell signals on the chart and executes the trades according to the defined conditions. It also visually indicates the stop loss levels for each trade.

Usage Notes:

This strategy is designed for use in the TradingView platform using Pine Script version 5.

It is important to backtest and paper trade the strategy before using it in live trading to understand its performance characteristics and risk profile.

The strategy should be used as part of a comprehensive trading plan, considering market conditions, trader risk tolerance, and personal trading goals.

Индикаторы и стратегии

Turtle Trading Strategy@lihexieThe full implementation of the Turtle Trading Rules (as distinct from the various truncated versions circulating within the community) is now ready.

This trading strategy script distinguishes itself from all currently publicly available Turtle trading systems on Tradingview by comprehensively embodying the rules for entries, exits, position management, and profit and loss controls.

Market Selection:

Trade in highly liquid markets such as forex, commodity futures, and stock index futures.

Entry Strategies:

Model 1: Buy when the price breaks above the highest point of the last 20 trading days; Sell when the price drops below the lowest point of the last 20 trading days. When an entry opportunity arises, if the previous trade was profitable, skip the current breakout opportunity and refrain from entering.

Model 2: Buy when the price breaks above the highest point of the last 55 trading days; Sell when the price drops below the lowest point of the last 55 trading days.

Position Sizing:

Determine the size of each position based on the price volatility (ATR) to ensure that the risk of each trade does not exceed 2% of the account balance.

Exit Strategies:

1. Use a fixed stop-loss point to limit losses: Close long positions when the price falls below the lowest point of the last 10 trading days.

2. Trailing stop-loss: Once a position is profitable, adjust the stop-loss point to protect profits.

Pyramiding Rules:

Unit Doubling: Increase position size by one unit every time the price moves forward by n (default is 0.5) units of ATR, up to a maximum of 4 units, while also raising the stop-loss point to below the ATR value at the level of additional entries.

海龟交易法则的完整实现(区别于当前社区各种有阉割海龟交易系统代码)

本策略脚本区别于Tradingview目前公开的所有的海龟交易系统,完整的实现了海龟交易法则中入场、出场、仓位管理,止盈止损的规则。

市场选择:

选择流动性高的市场进行交易,如外汇、商品期货和股指期货等。

入市策略:

模式1:当价格突破过去20个交易日的高点时,买入;当价格跌破过去20个交易日的低点时,卖出。当出现入场机会时,如果上一笔交易是盈利的,那么跳过当前突破的机会,不进行入场。

模式2:当价格突破过去55个交易日的高点时,买入;当价格跌破过去55个交易日的低点时,卖出。

头寸规模:

根据价格波动性(ATR)来确定每个头寸的大小, 使每笔交易的风险不超过账户余额的2%。

退出策略:

1. 使用一个固定的止损点来限制损失:当多头头寸的价格跌破过去10个交易日的低点时,平仓止损。

2. 跟踪止损:一旦头寸盈利,移动止损点以保护利润。

加仓规则:

单位加倍:每当价格向前n(默认是0.5)个单位的ATR移动时,就增加一个单位的头寸大小(默认最大头寸数量是4个),同时将止损点提升至加仓点位的ATR值以下。

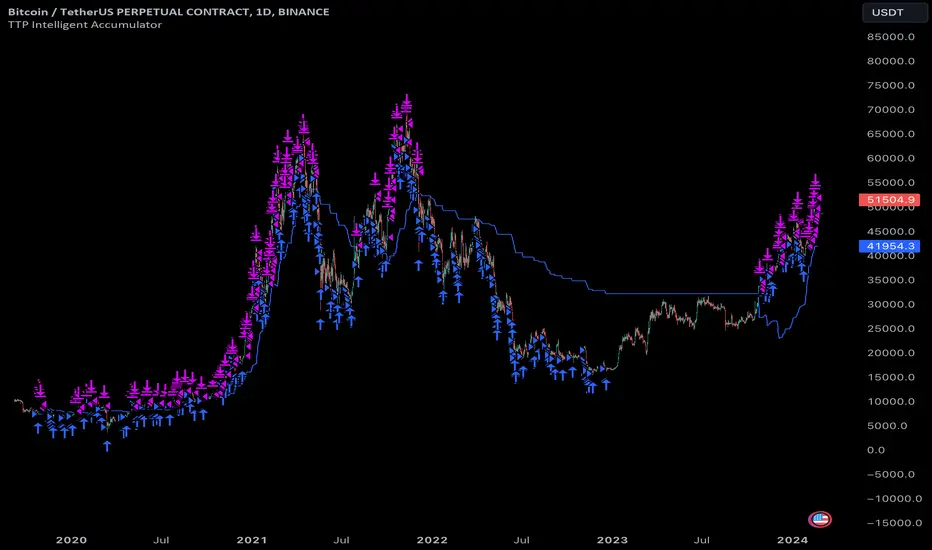

TTP Intelligent AccumulatorThe intelligent accumulator is a proof of concept strategy. A hybrid between a recurring buy and TA-based entries and exits.

Distribute the amount of equity and add to your position as long as the TA condition is valid.

Use the exit TA condition to define your exit strategy.

Decide between adding only into losing positions to average down or take a riskier approach by allowing to add into a winning position as well.

Take full profit or distribute your exit into multiple take profit exists of the same size.

You can also decide if you allow your exit conditions to close your position in a loss or require a minimum take profit %.

The strategy includes a default built-in TA conditions just for showcasing the idea but the final intent of this script is to delegate the TA entries and exists to external sources.

The internal conditions use RSI length 7 crossing below the BB with std 1 for entries and above for exits.

To control the number of orders use the properties from settings:

- adjust the pyramiding

- adjust the percentage of equity

- make sure that pyramiding * % equity equals 100 to prevent over use of equity (unless using leverage)

The script is designed as an alternative to daily or weekly recurring buys but depending on the accuracy of your TA conditions it might prove profitable also in lower timeframes.

The reason the script is named Intelligent is because recurring buy is most commonly used without any decision making: buy no matter what with certain frequency. This strategy seeks to still perform recurring buys but filtering out some of the potential bad entries that can delay unnecessarily seeing the position in profits. The second reason is also securing an exit strategy from the beginning which no recurring buy option offers out-of-the-box.

Long EMA Strategy with Advanced Exit OptionsThis strategy is designed for traders seeking a trend-following system with a focus on precision and adaptability.

**Core Strategy Concept**

The essence of this strategy lies in use of Exponential Moving Averages (EMAs) to identify potential long (buy) positions based on the relative positions of short-term, medium-term, and long-term EMAs. The use of EMAs is a classic yet powerful approach to trend detection, as these indicators smooth out price data over time, emphasizing the direction of recent price movements and potentially signaling the beginning of new trends.

**Customizable Parameters**

- **EMA Periods**: Users can define the periods for three EMAs - long-term, medium-term, and short-term - allowing for a tailored approach to capture trends based on individual trading styles and market conditions.

- **Volatility Filter**: An optional Average True Range (ATR)-based volatility filter can be toggled on or off. When activated, it ensures that trades are only entered when market volatility exceeds a user-defined threshold, aiming to filter out entries during low-volatility periods which are often characterized by indecisive market movements.

- **Trailing Stop Loss**: A trailing stop loss mechanism, expressed as a percentage of the highest price achieved since entry, provides a dynamic way to manage risk by allowing profits to run while cutting losses.

- **EMA Exit Condition**: This advanced exit option enables closing positions when the short-term EMA crosses below the medium-term EMA, serving as a signal that the immediate trend may be reversing.

- **Close Below EMA Exit**: An additional exit condition, which is disabled by default, allows positions to be closed if the price closes below a user-selected EMA. This provides an extra layer of flexibility and risk management, catering to traders who prefer to exit positions based on specific EMA thresholds.

**Operational Mechanics**

Upon activation, the strategy evaluates the current price in relation to the set EMAs. A long position is considered when the current price is above the long-term EMA, and the short-term EMA is above the medium-term EMA. This setup aims to identify moments where the price momentum is strong and likely to continue.

The strategy's versatility is further enhanced by its optional settings:

- The **Volatility Filter** adjusts the sensitivity of the strategy to market movements, potentially improving the quality of the entries during volatile market conditions.

The Average True Range (ATR) is a key component of this filter, providing a measure of market volatility by calculating the average range between the high and low prices over a specified number of periods. Here's how you can adjust the volatility filter settings for various market conditions, focusing on filtering out low-volatility markets:

Setting Examples for Volatility Filter

1. High Volatility Markets (e.g., Cryptocurrencies, Certain Forex Pairs):

ATR Periods: 14 (default)

ATR Multiplier: Setting the multiplier to a lower value, such as 1.0 or 1.2, can be beneficial in high-volatility markets. This sensitivity allows the strategy to react to volatility changes more quickly, ensuring that you're entering trades during periods of significant movement.

2. Medium Volatility Markets (e.g., Major Equity Indices, Medium-Volatility Forex Pairs):

ATR Periods: 14 (default)

ATR Multiplier: A multiplier of 1.5 (default) is often suitable for medium volatility markets. It provides a balanced approach, ensuring that the strategy filters out low-volatility conditions without being overly restrictive.

3. Low Volatility Markets (e.g., Some Commodities, Low-Volatility Forex Pairs):

ATR Periods: Increasing the ATR period to 20 or 25 can smooth out the volatility measure, making it less sensitive to short-term fluctuations. This adjustment helps in focusing on more significant trends in inherently stable markets.

ATR Multiplier: Raising the multiplier to 2.0 or even 2.5 increases the threshold for volatility, effectively filtering out low-volatility conditions. This setting ensures that the strategy only triggers trades during periods of relatively higher volatility, which are more likely to result in significant price movements.

How to Use the Volatility Filter for Low-Volatility Markets

For traders specifically interested in filtering out low-volatility markets, the key is to adjust the ATR Multiplier to a higher level. This adjustment increases the threshold required for the market to be considered sufficiently volatile for trade entries. Here's a step-by-step guide:

Adjust the ATR Multiplier: Increase the ATR Multiplier to create a higher volatility threshold. A multiplier of 2.0 to 2.5 is a good starting point for very low-volatility markets.

Fine-Tune the ATR Periods: Consider lengthening the ATR calculation period if you find that the strategy is still entering trades in undesirable low-volatility conditions. A longer period provides a more averaged-out measure of volatility, which might better suit your needs.

Monitor and Adjust: Volatility is not static, and market conditions can change. Regularly review the performance of your strategy in the context of current market volatility and adjust the settings as necessary.

Backtest in Different Conditions: Before applying the strategy live, backtest it across different market conditions with your adjusted settings. This process helps ensure that your approach to filtering low-volatility conditions aligns with your trading objectives and risk tolerance.

By fine-tuning the volatility filter settings according to the specific characteristics of the market you're trading in, you can enhance the performance of this strategy

- The **Trailing Stop Loss** and **EMA Exit Conditions** provide two layers of exit strategies, focusing on capital preservation and profit maximization.

**Visualizations**

For clarity and ease of use, the strategy plots the three EMAs and, if enabled, the ATR threshold on the chart. These visual cues not only aid in decision-making but also help in understanding the market's current trend and volatility state.

**How to Use**

Traders can customize the EMA periods to fit their trading horizon, be it short, medium, or long-term trading. The volatility filter and exit options allow for further customization, making the strategy adaptable to different market conditions and personal risk tolerance levels.

By offering a blend of trend-following principles with advanced risk management features, this strategy aims to cater to a wide range of trading styles, from cautious to aggressive. Its strength lies in its flexibility, allowing traders to fine-tune settings to their specific needs, making it a potentially valuable tool in the arsenal of any trader looking for a disciplined approach to navigating the markets.

Octopus Nest Strategy Hello Fellas,

Hereby, I come up with a popular strategy from YouTube called Octopus Nest Strategy. It is a no repaint, lower timeframe scalping strategy utilizing PSAR, EMA and TTM Squeeze.

The strategy considers these market factors:

PSAR -> Trend

EMA -> Trend

TTM Squeeze -> Momentum and Volatility by incorporating Bollinger Bands and Keltner Channels

Note: As you can see there is a potential improvement by incorporating volume.

What's Different Compared To The Original Strategy?

I added an option which allows users to use the Adaptive PSAR of @loxx, which will hopefully improve results sometimes.

Signals

Enter Long -> source above EMA 100, source crosses above PSAR and TTM Squeeze crosses above 0

Enter Short -> source below EMA 100, source crosses below PSAR and TTM Squeeze crosses below 0

Exit Long and Exit Short are triggered from the risk management. Thus, it will just exit on SL or TP.

Risk Management

"High Low Stop Loss" and "Automatic High Low Take Profit" are used here.

High Low Stop Loss: Utilizes the last high for short and the last low for long to calculate the stop loss level. The last high or low gets multiplied by the user-defined multiplicator and if no recent high or low was found it uses the backup multiplier.

Automatic High Low Take Profit: Utilizes the current stop loss level of "High Low Stop Loss" and gets calculated by the user-defined risk ratio.

Now, follows the bunch of knowledge for the more inexperienced readers.

PSAR: Parabolic Stop And Reverse; Developed by J. Welles Wilders and a classic trend reversal indicator.

The indicator works most effectively in trending markets where large price moves allow traders to capture significant gains. When a security’s price is range-bound, the indicator will constantly be reversing, resulting in multiple low-profit or losing trades.

TTM Squeeze: TTM Squeeze is a volatility and momentum indicator introduced by John Carter of Trade the Markets (now Simpler Trading), which capitalizes on the tendency for price to break out strongly after consolidating in a tight trading range.

The volatility component of the TTM Squeeze indicator measures price compression using Bollinger Bands and Keltner Channels. If the Bollinger Bands are completely enclosed within the Keltner Channels, that indicates a period of very low volatility. This state is known as the squeeze. When the Bollinger Bands expand and move back outside of the Keltner Channel, the squeeze is said to have “fired”: volatility increases and prices are likely to break out of that tight trading range in one direction or the other. The on/off state of the squeeze is shown with small dots on the zero line of the indicator: red dots indicate the squeeze is on, and green dots indicate the squeeze is off.

EMA: Exponential Moving Average; Like a simple moving average, but with exponential weighting of the input data.

Don't forget to check out the settings and keep it up.

Best regards,

simwai

---

Credits to:

@loxx

@Bjorgum

@Greeny

Triple MA HTF strategy - Dynamic SmoothingThe triple MA strategy is a simple but effective method to trade the trend. The advantage of this script over the existing triple MA strategies is that the user can open a lower time frame chart and select higher time frame inputs for different MA types mainting the visibility on the chart. The dynamic smoothing code makes sure the HTF trendlines are not jagged, but a fluid line visiable on the lower time frame chart. The script comes with a MA crossover and crossunder strategy explained below.

Moving Averages (MA) Crossover for Entry:

Long Entry: A long entry signal is triggered when the moving average line 1 crosses above the moving average line 2. This crossover indicates a potential shift in market sentiment towards the upside. However, to validate this signal, the strategy checks if the moving average 3 on a higher time frame (eg. 4 hour) is in an upward trend. This additional filter ensures that the trade aligns with the prevailing trend on a broader time scale, increasing the probability of success.

Short Entry: Conversely, a short entry signal occurs when the moving average line 1 crosses below the moving average line 2. This crossover suggests a possible downturn in market momentum. However, for a short trade to be confirmed, the strategy verifies that the moving average 3 on the higher time frame is in a downward trend. This confirmation ensures that the trade is in harmony with the overarching market direction.

Exit from Long Position: The strategy triggers an exit signal from a long position when the moving average line 1 crosses below the moving average line 2. This crossover indicates a potential reversal in the market trend, prompting the trader to close their long position and take profits or minimize losses.

Exit from Short Position: Similarly, an exit signal from a short position occurs when the moving average line 1 crosses above the moving average line 2. This crossover suggests a potential shift in market sentiment towards the upside, prompting the trader to exit their short position and manage their risk accordingly.

Features of the script

This Triple MA Strategy is basically the HTF Trend Filter displayed 3 times on the chart. For more infomation on how the MA with dynamic smoothing is calculated I recommend reading the following script:

For risk management I included a simple script to opt for % of eauity or # of contracts of in the instrument. For explanation on how the risk management settings work I refer to my ealier published script:

The strategy is a simplified example for setting up an entry and exit logic based on multiple moving avarages. Hence the script is meant for educational purposes only.

Crypto MVRV ZScore - Strategy [PresentTrading]█ Introduction and How it is Different

The "Crypto Valuation Extremes: MVRV ZScore - Strategy " represents a cutting-edge approach to cryptocurrency trading, leveraging the Market Value to Realized Value (MVRV) Z-Score. This metric is pivotal for identifying overvalued or undervalued conditions in the crypto market, particularly Bitcoin. It assesses the current market valuation against the realized capitalization, providing insights that are not apparent through conventional analysis.

BTCUSD 6h Long/Short Performance

Local

█ Strategy, How It Works: Detailed Explanation

The strategy leverages the Market Value to Realized Value (MVRV) Z-Score, specifically designed for cryptocurrencies, with a focus on Bitcoin. This metric is crucial for determining whether Bitcoin is currently undervalued or overvalued compared to its historical 'realized' price. Below is an in-depth explanation of the strategy's components and calculations.

🔶Conceptual Foundation

- Market Capitalization (MC): This represents the total dollar market value of Bitcoin's circulating supply. It is calculated as the current price of Bitcoin multiplied by the number of coins in circulation.

- Realized Capitalization (RC): Unlike MC, which values all coins at the current market price, RC is computed by valuing each coin at the price it was last moved or traded. Essentially, it is a summation of the value of all bitcoins, priced at the time they were last transacted.

- MVRV Ratio: This ratio is derived by dividing the Market Capitalization by the Realized Capitalization (The ratio of MC to RC (MVRV Ratio = MC / RC)). A ratio greater than 1 indicates that the current price is higher than the average price at which all bitcoins were purchased, suggesting potential overvaluation. Conversely, a ratio below 1 suggests undervaluation.

🔶 MVRV Z-Score Calculation

The Z-Score is a statistical measure that indicates the number of standard deviations an element is from the mean. For this strategy, the MVRV Z-Score is calculated as follows:

MVRV Z-Score = (MC - RC) / Standard Deviation of (MC - RC)

This formula quantifies Bitcoin's deviation from its 'normal' valuation range, offering insights into market sentiment and potential price reversals.

🔶 Spread Z-Score for Trading Signals

The strategy refines this approach by calculating a 'spread Z-Score', which adjusts the MVRV Z-Score over a specific period (default: 252 days). This is done to smooth out short-term market volatility and focus on longer-term valuation trends. The spread Z-Score is calculated as follows:

Spread Z-Score = (Market Z-Score - MVVR Ratio - SMA of Spread) / Standard Deviation of Spread

Where:

- SMA of Spread is the simple moving average of the spread over the specified period.

- Spread refers to the difference between the Market Z-Score and the MVRV Ratio.

🔶 Trading Signals

- Long Entry Condition: A long (buy) signal is generated when the spread Z-Score crosses above the long entry threshold, indicating that Bitcoin is potentially undervalued.

- Short Entry Condition: A short (sell) signal is triggered when the spread Z-Score falls below the short entry threshold, suggesting overvaluation.

These conditions are based on the premise that extreme deviations from the mean (as indicated by the Z-Score) are likely to revert to the mean over time, presenting opportunities for strategic entry and exit points.

█ Practical Application

Traders use these signals to make informed decisions about opening or closing positions in the Bitcoin market. By quantifying market valuation extremes, the strategy aims to capitalize on the cyclical nature of price movements, identifying high-probability entry and exit points based on historical valuation norms.

█ Trade Direction

A unique feature of this strategy is its configurable trade direction. Users can specify their preference for engaging in long positions, short positions, or both. This flexibility allows traders to tailor the strategy according to their risk tolerance, market outlook, or trading style, making it adaptable to various market conditions and trader objectives.

█ Usage

To implement this strategy, traders should first adjust the input parameters to align with their trading preferences and risk management practices. These parameters include the trade direction, Z-Score calculation period, and the thresholds for long and short entries. Once configured, the strategy automatically generates trading signals based on the calculated spread Z-Score, providing clear indications for potential entry and exit points.

It is advisable for traders to backtest the strategy under different market conditions to validate its effectiveness and adjust the settings as necessary. Continuous monitoring and adjustment are crucial, as market dynamics evolve over time.

█ Default Settings

- Trade Direction: Both (Allows for both long and short positions)

- Z-Score Calculation Period: 252 days (Approximately one trading year, capturing a comprehensive market cycle)

- Long Entry Threshold: 0.382 (Indicative of moderate undervaluation)

- Short Entry Threshold: -0.382 (Signifies moderate overvaluation)

These default settings are designed to balance sensitivity to market valuation extremes with a pragmatic approach to trade execution. They aim to filter out noise and focus on significant market movements, providing a solid foundation for both new and experienced traders looking to exploit the unique insights offered by the MVRV Z-Score in the cryptocurrency market.

Bollinger and Stochastic with Trailing Stop - D.M.P.This trading strategy combines Bollinger Bands and the Stochastic indicator to identify entry opportunities in oversold and overbought conditions in the market. The aim is to capitalize on price rebounds from the extremes defined by the Bollinger Bands, with the confirmation of the Stochastic to maximize the probability of success of the operations.

Indicators Used

- Bollinger Bands Used to measure volatility and define oversold and overbought levels. When the price touches or breaks through the lower band, it indicates a possible oversold condition. Similarly, when it touches or breaks through the upper band, it indicates a possible overbought condition.

- Stochastic: A momentum oscillator that compares the closing price of an asset with its price range over a certain period. Values below 20 indicate oversold, while values above 80 indicate overbought.

Strategy Logic

- Long Entry (Buy): A purchase operation is executed when the price closes below the lower Bollinger band (indicating oversold) and the Stochastic is also in the oversold zone.

- Short Entry (Sell): A sell operation is executed when the price closes above the upper Bollinger band (indicating overbought) and the Stochastic is in the overbought zone.

Supertrend & CCI Strategy ScalpThis strategy is based on 2 Super Trend Indicators along with CCI .

The longer factor length gives you the current trend and the deviation in the short factor length gives us the opportunity to enter in the trade .

CCI indicator is used to determine the overbought and oversold levels.

Setup :

Long : When atrLength1 > close and atrLength2 < close and CCI < -100 we look for long trades as the longer factor length will be bullish .

Short : When atrLength1 < close and atrLength2 > close and CCI > 100 we look for short trades as the longer factor length will be bearish .

Please tune the settings according to your use .

Trade what you see not what you feel .

Please consult with your financial advisor before you deploy any real money for trading .

PresentTrend RMI Synergy - Strategy [presentTrading] █ Introduction and How it is Different

The "PresentTrend RMI Synergy Strategy" is the combined power of the Relative Momentum Index (RMI) and a custom presentTrend indicator. This strategy introduces a multifaceted approach, integrating momentum analysis with trend direction to offer traders a more nuanced and responsive trading mechanism.

BTCUSD 6h L/S Performance

Local

█ Strategy, How It Works: Detailed Explanation

The "PresentTrend RMI Synergy Strategy" intricately combines the Relative Momentum Index (RMI) and a custom SuperTrend indicator to create a powerful tool for traders.

🔶 Relative Momentum Index (RMI)

The RMI is a variation of the Relative Strength Index (RSI), but instead of using price closes against itself, it measures the momentum of up and down movements in price relative to previous prices over a given period. The RMI for a period length `N` is calculated as follows:

RMI = 100 - 100/ (1 + U/D)

where:

- `U` is the average upward price change over `N` periods,

- `D` is the average downward price change over `N` periods.

The RMI oscillates between 0 and 100, with higher values indicating stronger upward momentum and lower values suggesting stronger downward momentum.

RMI = 21

RMI = 42

For more information - RMI Trend Sync - Strategy :

🔶 presentTrend Indicator

The presentTrend indicator combines the Average True Range (ATR) with a moving average to determine trend direction and dynamic support or resistance levels. The presentTrend for a period length `M` and a multiplier `F` is defined as:

- Upper Band: MA + (ATR x F)

- Lower Band: MA - (ATR x F)

where:

- `MA` is the moving average of the close price over `M` periods,

- `ATR` is the Average True Range over the same period,

- `F` is the multiplier to adjust the sensitivity.

The trend direction switches when the price crosses the presentTrend bands, signaling potential entry or exit points.

presentTrend length = 3

presentTrend length = 10

For more information - PresentTrend - Strategy :

🔶 Strategy Logic

Entry Conditions:

- Long Entry: Triggered when the RMI exceeds a threshold, say 60, indicating a strong bullish momentum, and when the price is above the presentTrend, confirming an uptrend.

- Short Entry: Occurs when the RMI drops below a threshold, say 40, showing strong bearish momentum, and the price is below the present trend, indicating a downtrend.

Exit Conditions with Dynamic Trailing Stop:

- Long Exit: Initiated when the price crosses below the lower presentTrend band or when the RMI falls back towards a neutral level, suggesting a weakening of the bullish momentum.

- Short Exit: Executed when the price crosses above the upper presentTrend band or when the RMI rises towards a neutral level, indicating a reduction in bearish momentum.

Equations for Dynamic Trailing Stop:

- For Long Positions: The exit price is set at the lower SuperTrend band once the entry condition is met.

- For Short Positions: The exit price is determined by the upper SuperTrend band post-entry.

These dynamic trailing stops adjust as the market moves, providing a method to lock in profits while allowing room for the position to grow.

This strategy's strength lies in its dual analysis approach, leveraging RMI for momentum insights and presentTrend for trend direction and dynamic stops. This combination offers traders a robust framework to navigate various market conditions, aiming to capture trends early and exit positions strategically to maximize gains and minimize losses.

█ Trade Direction

The strategy provides flexibility in trade direction selection, offering "Long," "Short," or "Both" options to cater to different market conditions and trader preferences. This adaptability ensures that traders can align the strategy with their market outlook, risk tolerance, and trading goals.

█ Usage

To utilize the "PresentTrend RMI Synergy Strategy," traders should input their preferred settings in the Pine Script™ and apply the strategy to their charts. Monitoring RMI for momentum shifts and adjusting positions based on SuperTrend signals can optimize entry and exit points, enhancing potential returns while managing risk.

█ Default Settings

1. RMI Length: 21

The 21-period RMI length strikes a balance between capturing momentum and filtering out market noise, offering a medium-term outlook on market trends.

2. Super Trend Length: 7

A SuperTrend length of 7 periods is chosen for its responsiveness to price movements, providing a dynamic framework for trend identification without excessive sensitivity.

3. Super Trend Multiplier: 4.0

The multiplier of 4.0 for the SuperTrend indicator widens the trend bands, focusing on significant market moves and reducing the impact of minor fluctuations.

---

The "PresentTrend RMI Synergy Strategy" represents a significant step forward in trading strategy development, blending momentum and trend analysis in a unique way. By providing a detailed framework for understanding market dynamics, this strategy empowers traders to make more informed decisions.

PS January Barometer BacktesterPS January Barometer Backtester (PS JBB)

The PS January Barometer Backtester (PS JBB) is a simple strategy designed to test the "January Effect" hypothesis in financial markets. This effect theorizes that stock market performance in January can predict the trend for the rest of the year. The script operates on a monthly timeframe, focusing on capturing and analyzing the price movements in January and their subsequent influence on the market until the end of each year.

User Input:

January Trifecta Selectors

These are user-selectable options allowing traders to incorporate additional criteria into their market analysis.

The Santa Claus Rally refers to a stock market increase typically seen in the last week of December through the first two trading days in January.

The First Five Days Indicator assesses market performance during the initial five days of the year.

Script Operation:

The script automatically detects the start of each year, tracks January's high, and signals entry and exit points for trades based on the strategy's logic. It's an excellent tool for traders and investors looking to explore the January Effect's validity and its potential impact on their trading decisions.

In essence, the "PS January Barometer Backtester" is designed to exploit specific seasonal market trends, particularly focusing on the early part of the year, by analyzing and acting upon defined market movements. This strategy is ideal for traders who focus on yearly cyclical patterns and seek to incorporate historical trends into their trading decisions.

Note: This script is intended for educational and research purposes and should not be construed as financial advice. Always conduct your own due diligence before making trading/investment decisions.

Candle StrategyThis strategy is based candle count number also strategy analysis -

Rules for buy-

1) choose Candle Number(Ex.-47) For Trade

2) Trade Sell if price is above high of day 1st candle that mean direction is upside

3) We are taking stop loss on lowest low of candle since day first candle to trade no.

4) close Trade at last bar of the day

5) Trader Can Choose Trade Direction From input

Rules for Sell-

1) Choose Candle Number(Ex.-47) For Trade

2) Trade Sell if price is below low of day 1st candle that mean direction is downside

3) We are taking stop loss on highest of candle since day first candle to trade no.

4) close Trade at last bar of the day

5) Trader Can Choose Trade Direction From input

Note - this strategy can be also use for static to understand which candle will make low/high of the day high chance Example in bank nifty 5 minutes chart candle no 47 have highest trade

opportunity appear on long side ...this data is small based on 5000 previous bar ...

Disclaimer: market involves significant risks, including complete possible loss of funds. Consequently trading is not suitable for all investors and traders. By increasing leverage risk increases as well.With the demo account you can test any trading strategies you wish in a risk-free environment. Please bear in mind that the results of the transactions of the practice account are virtual, and do not reflect any real profit or loss or a real trading environment, whereas market conditions may affect both the quotation and execution

AI SuperTrend x Pivot Percentile - Strategy [PresentTrading]█ Introduction and How it is Different

The AI SuperTrend x Pivot Percentile strategy is a sophisticated trading approach that integrates AI-driven analysis with traditional technical indicators. Combining the AI SuperTrend with the Pivot Percentile strategy highlights several key advantages:

1. Enhanced Accuracy in Trend Prediction: The AI SuperTrend utilizes K-Nearest Neighbors (KNN) algorithm for trend prediction, improving accuracy by considering historical data patterns. This is complemented by the Pivot Percentile analysis which provides additional context on trend strength.

2. Comprehensive Market Analysis: The integration offers a multi-faceted approach to market analysis, combining AI insights with traditional technical indicators. This dual approach captures a broader range of market dynamics.

BTC 6H L/S Performance

Local

█ Strategy: How it Works - Detailed Explanation

🔶 AI-Enhanced SuperTrend Indicators

1. SuperTrend Calculation:

- The SuperTrend indicator is calculated using a moving average and the Average True Range (ATR). The basic formula is:

- Upper Band = Moving Average + (Multiplier × ATR)

- Lower Band = Moving Average - (Multiplier × ATR)

- The moving average type (SMA, EMA, WMA, RMA, VWMA) and the length of the moving average and ATR are adjustable parameters.

- The direction of the trend is determined based on the position of the closing price in relation to these bands.

2. AI Integration with K-Nearest Neighbors (KNN):

- The KNN algorithm is applied to predict trend direction. It uses historical price data and SuperTrend values to classify the current trend as bullish or bearish.

- The algorithm calculates the 'distance' between the current data point and historical points. The 'k' nearest data points (neighbors) are identified based on this distance.

- A weighted average of these neighbors' trends (bullish or bearish) is calculated to predict the current trend.

For more please check: Multi-TF AI SuperTrend with ADX - Strategy

🔶 Pivot Percentile Analysis

1. Percentile Calculation:

- This involves calculating the percentile ranks for high and low prices over a set of predefined lengths.

- The percentile function is typically defined as:

- Percentile = Value at (P/100) × (N + 1)th position

- Where P is the desired percentile, and N is the number of data points.

2. Trend Strength Evaluation:

- The calculated percentiles for highs and lows are used to determine the strength of bullish and bearish trends.

- For instance, a high percentile rank in the high prices may indicate a strong bullish trend, and vice versa for bearish trends.

For more please check: Pivot Percentile Trend - Strategy

🔶 Strategy Integration

1. Combining SuperTrend and Pivot Percentile:

- The strategy synthesizes the insights from both AI-enhanced SuperTrend and Pivot Percentile analysis.

- It compares the trend direction indicated by the SuperTrend with the strength of the trend as suggested by the Pivot Percentile analysis.

2. Signal Generation:

- A trading signal is generated when both the AI-enhanced SuperTrend and the Pivot Percentile analysis agree on the trend direction.

- For instance, a bullish signal is generated when both the SuperTrend is bullish, and the Pivot Percentile analysis shows strength in bullish trends.

🔶 Risk Management and Filters

- ADX and DMI Filter: The strategy uses the Average Directional Index (ADX) and the Directional Movement Index (DMI) as filters to assess the trend's strength and direction.

- Dynamic Trailing Stop Loss: Based on the SuperTrend indicator, the strategy dynamically adjusts stop-loss levels to manage risk effectively.

This strategy stands out for its ability to combine real-time AI analysis with established technical indicators, offering traders a nuanced and responsive tool for navigating complex market conditions. The equations and algorithms involved are pivotal in accurately identifying market trends and potential trade opportunities.

█ Usage

To effectively use this strategy, traders should:

1. Understand the AI and Pivot Percentile Indicators: A clear grasp of how these indicators work will enable traders to make informed decisions.

2. Interpret the Signals Accurately: The strategy provides bullish, bearish, and neutral signals. Traders should align these signals with their market analysis and trading goals.

3. Monitor Market Conditions: Given that this strategy is sensitive to market dynamics, continuous monitoring is crucial for timely decision-making.

4. Adjust Settings as Needed: Traders should feel free to tweak the input parameters to suit their trading preferences and to respond to changing market conditions.

█Default Settings and Their Impact on Performance

1. Trading Direction (Default: "Both")

Effect: Determines whether the strategy will take long positions, short positions, or both. Adjusting this setting can align the strategy with the trader's market outlook or risk preference.

2. AI Settings (Neighbors: 3, Data Points: 24)

Neighbors: The number of nearest neighbors in the KNN algorithm. A higher number might smooth out noise but could miss subtle, recent changes. A lower number makes the model more sensitive to recent data but may increase noise.

Data Points: Defines the amount of historical data considered. More data points provide a broader context but may dilute recent trends' impact.

3. SuperTrend Settings (Length: 10, Factor: 3.0, MA Source: "WMA")

Length: Affects the sensitivity of the SuperTrend indicator. A longer length results in a smoother, less sensitive indicator, ideal for long-term trends.

Factor: Determines the bandwidth of the SuperTrend. A higher factor creates wider bands, capturing larger price movements but potentially missing short-term signals.

MA Source: The type of moving average used (e.g., WMA - Weighted Moving Average). Different MA types can affect the trend indicator's responsiveness and smoothness.

4. AI Trend Prediction Settings (Price Trend: 10, Prediction Trend: 80)

Price Trend and Prediction Trend Lengths: These settings define the lengths of weighted moving averages for price and SuperTrend, impacting the responsiveness and smoothness of the AI's trend predictions.

5. Pivot Percentile Settings (Length: 10)

Length: Influences the calculation of pivot percentiles. A shorter length makes the percentile more responsive to recent price changes, while a longer length offers a broader view of price trends.

6. ADX and DMI Settings (ADX Length: 14, Time Frame: 'D')

ADX Length: Defines the period for the Average Directional Index calculation. A longer period results in a smoother ADX line.

Time Frame: Sets the time frame for the ADX and DMI calculations, affecting the sensitivity to market changes.

7. Commission, Slippage, and Initial Capital

These settings relate to transaction costs and initial investment, directly impacting net profitability and strategy feasibility.

Four WMA Strategy with TP and SLBasically I read a research paper on how they used different moving averages for long entries and short entries, and it kind of dawned on me that I always used the same one for long entry or exit, or even swing trading. So I smashed this together to see what would happen.

The strategy combines the use of four different WMAs for identifying trade entry points, along with a predefined take profit (TP) and stop loss (SL) for risk management. Here's a detailed description of its features and how it operates:

Main Features

1. **WMAs as the Core Indicator**:

- The strategy uses four WMAs with different lengths. Two WMAs (`longM1` and `longM2`) are used for long entry signals, and the other two (`shortM1` and `shortM2`) for short entry signals.

- The lengths of these WMAs are adjustable through input parameters.

2. **Trade Entry Conditions**:

- A long entry is signaled when the shorter WMA crosses under the longer WMA .

- Conversely, a short entry is signaled when the shorter WMA crosses under the longer WMA.

3. **Take Profit and Stop Loss**:

- The strategy includes a take profit and stop loss mechanism.

- The TP and SL levels are set as a percentage of the entry price, with the percentage values being adjustable through input parameters.

4. **Visual Representation**:

- The WMAs are plotted on the chart for visual aid, each with a distinct color for easy identification.

How It Works

- The strategy continuously monitors the crossing of WMAs to detect potential entry points for long and short positions.

- Upon detecting a long or short condition, it automatically enters a trade and sets the corresponding TP and SL levels based on the current price and the specified percentages.

- The strategy then actively manages the trade, exiting the position when either the TP or SL level is reached.

Drawbacks

- **Overreliance on WMAs**: The strategy heavily relies on WMAs for trade signals. While WMAs are useful for identifying trends, they might not always provide timely entry and exit signals.

- **Market Conditions**: It may not perform well in highly volatile or sideways markets where WMA crossovers could lead to false signals.

- **Risk Management**: The fixed percentage for TP and SL might not be suitable for all market conditions. Traders might need to adjust these values frequently based on market volatility and their risk tolerance.

Apparently I need to emphasize to use brains when using indicators and setting them up to achieve the results you can or want. Also risk of 12% is considered very high so I lowered the numbers to 5%, which tanked the profits, try adjusting them on your own. Check the properties settings for more info on comission and slippage.

Conclusion

The "Four WMA Strategy with TP and SL" is suitable for traders who prefer a moving average-based approach to trading, combined with a straightforward mechanism for risk management through take profit and stop loss. However, like all strategies, it should be used with an understanding of its limitations and ideally tested thoroughly in various market conditions before applying it to live trading.

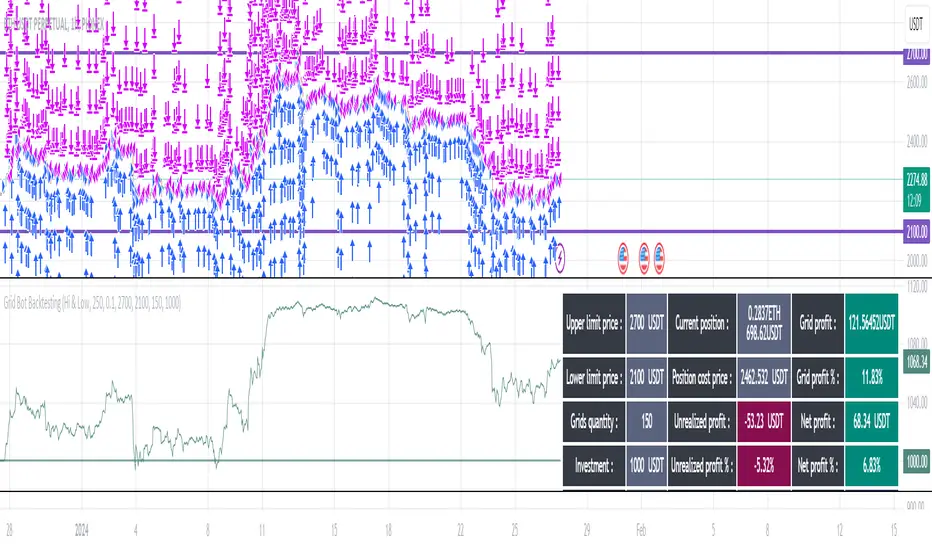

Grid Bot BacktestingBinance, Bybit, Bitget, and other cross-exchange (grid) trading bot backtesting.

Auto bound: Automatically setting upper and lower price bounds.

Manual: Setting upper and lower price bounds manually.

The graph below represents the overall asset changes (initial investment amount + current position profit + grid profit).

Try using backtesting when setting up a grid bot on the exchange!

바이낸스, 바이비트, 비트겟 등 교차거래(그리드) 봇 백테스팅

Auto bound : 자동으로 상,하단 가격 설정

Manual : 직접 상,하단 가격 설정

아래 그래프는 총 자산 변화입니다.(초기투자금액 + 현재 포지션 수익 + 그리드 수익)

거래소에서 그리드 봇 설정할 때 백테스팅 유용하게 써보세요!

Ichimoku Clouds Strategy Long and ShortOverview:

The Ichimoku Clouds Strategy leverages the Ichimoku Kinko Hyo technique to offer traders a range of innovative features, enhancing market analysis and trading efficiency. This strategy is distinct in its combination of standard methodology and advanced customization, making it suitable for both novice and experienced traders.

Unique Features:

Enhanced Interpretation: The strategy introduces weak, neutral, and strong bullish/bearish signals, enabling detailed interpretation of the Ichimoku cloud and direct chart plotting.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Dual Trading Modes: Long and Short modes are available, allowing alignment with market trends.

Flexible Risk Management: Offers three styles in each mode, combining fixed risk management with dynamic indicator states for versatile trade management.

Indicator Line Plotting: Enables plotting of Ichimoku indicator lines on the chart for visual decision-making support.

Methodology:

The strategy utilizes the standard Ichimoku Kinko Hyo model, interpreting indicator values with settings adjustable through a user-friendly menu. This approach is enhanced by TradingView's built-in strategy tester for customization and market selection.

Risk Management:

Our approach to risk management is dynamic and indicator-centric. With data from the last year, we focus on dynamic indicator states interpretations to mitigate manual setting causing human factor biases. Users still have the option to set a fixed stop loss and/or take profit per position using the corresponding parameters in settings, aligning with their risk tolerance.

Backtest Results:

Operating window: Date range of backtests is 2023.01.01 - 2024.01.04. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Maximum Single Position Loss: -6.29%

Maximum Single Profit: 22.32%

Net Profit: +10 901.95 USDT (+109.02%)

Total Trades: 119 (51.26% profitability)

Profit Factor: 1.775

Maximum Accumulated Loss: 4 185.37 USDT (-22.87%)

Average Profit per Trade: 91.67 USDT (+0.7%)

Average Trade Duration: 56 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters. Backtest is calculated using deep backtest option in TradingView built-in strategy tester

How to Use:

Add the script to favorites for easy access.

Apply to the desired chart and timeframe (optimal performance observed on the 1H chart, ForEx or cryptocurrency top-10 coins with quote asset USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Table to filter trades per dayThis script contains a block of code that allows users to filter the total number of trades, loss trades, win trades and win rate per day in a table. This makes it easier to compare which days were profitable and which were not.

Be aware that this script can only be used in strategy scripts. To use the script, open it and copy every line from "START" to "STOP". Then, paste these lines at the very bottom of the strategy script that you want to attach it to.

The user has the ability to adjust the position of the table and customize the size of the text displayed.

If the user sets "Check when the trade:" to "Opened", the script will monitor when the trade opens and add it to the table once it has been closed. If "Check when the trade:" is set to "Closed", the script will track when the trade is closed and add it to the table once it has been closed.

It is recommended to run the script on the "Exchange" setting for more accurate results, even though a "Set the timezone" option is available. This will prevent discrepancies caused by daylight saving time changes.

Please note that the code will only work properly if you choose a daily timeframe or lower.

Turtle Trader StrategyTurtle Trader Strategy :

Introduction :

This strategy is based on the well known « Turtle Trader Strategy », that has proven itself over the years. It sends long and short signals with pyramid orders of up to 5, meaning that the strategy can trigger up to 5 orders in the same direction. Good risk and money management.

It's important to note that the strategy combines 2 systems working together (S1 and S2). Let’s describe the specific features of this strategy.

1/ Position size :

Position size is very important for turtle traders to manage risk properly. This position sizing strategy adapts to market volatility and to account (gains and losses). It’s based on ATR (Average True Range) which can also be called « N ». Its length is per default 20.

ATR(20) = (previous_atr(20)*19 + actual_true_range)/20

The number of units to buy is :

Unit = 1% * account/(ATR(20)*dollar_per_point)

where account is the actual account value and dollar_per_point is the variation in dollar of the asset with a 1 point move.

Depending on your risk aversion, you can increase the percentage of your account, but turtle traders default to 1%. If you trade contracts, units must be rounded down by default.

There is also an additional rule to reduce the risk if the value of the account falls below the initial capital : in this case and only in this case, account in the unit formula must be replace by :

account = actual_account*actual_account/initial capital

2/ Open a position :

2 systems are working together :

System 1 : Entering a new 20 day breakout

System 2 : Entering a new 55 day breakout

A breakout is a new high or new low. If it’s a new high, we open long position and vice versa if it’s a new low we enter in short position.

We add an additional rule :

System 1 : Breakout is ignored if last long/short position was a winner

System 2 : All signals are taken

This additional rule allows the trader to be in the major trends if the system 1 signal has been skipped. If a signal for system 1 has been skipped, and next candle is also a new 20 day breakout, S1 doesn’t give a signal. We have to wait S2 signal or wait for a candle that doesn’t make a new breakout to reactivate S1.

3/ Pyramid orders :

Turtle Strategy allows us to add extra units to the position if the price moves in our favor. I've configured the strategy to allow up to 5 orders to be added in the same direction. So if the price varies from 0.5*ATR(20) , we add units with the position size formula. Note that the value of account will be replaced by "remaining_account", i.e. the cash remaining in our account after subtracting the value of open positions.

4/ Stop Loss :

We set a stop loss at 1.5*ATR(20) below the entry price for longs and above the entry price for shorts. If pyramid units are added, the stop is increased/decreased by 0.5*ATR(20). Note that if SL is configured for a loss of more than 10%, we set the SL to 10% for the first entry order to avoid big losses. This configuration does not work for pyramid orders as SL moves by 0.5*ATR(20).

5/ Exit signals :

System 1 :

Exit long on a 10 day low

Exit short on a 10 day high

System 2 :

Exit long on a 20 day low

Exit short on a 20 day high

6/ What types of orders are placed ?

To enter in a position, stop orders are placed meaning that we place orders that will be automatically triggered by the signal at the exact breakout price. Stop loss and exit signals are also stop orders. Pyramid orders are market orders which will be triggered at the opening of the next candle to avoid repainting.

PARAMETERS :

Risk % of capital : Percentage used in the position size formula. Default is 1%

ATR period : ATR length used to calculate ATR. Default is 20

Stop ATR : Parameters used to fix stop loss. Default is 1.5 meaning that stop loss will be set at : buy_price - 1.5*ATR(20) for long and buy_price + 1.5*ATR(20) for short. Turtle traders default is 2 but 1.5 is better for cryptocurrency as there is a huge volatility.

S1 Long : System 1 breakout length for long. Default is 20

S2 Long : System 2 breakout length for long. Default is 55

S1 Long Exit : System 1 breakout length to exit long. Default is 10

S2 Long Exit : System 2 breakout length to exit long. Default is 20

S1 Short : System 1 breakout length for short. Default is 15

S2 Short : System 2 breakout length for short. Default is 55

S1 Short Exit : System 1 breakout length to exit short. Default is 7

S2 Short Exit : System 2 breakout length to exit short. Default is 20

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Pyramiding : Number of orders that can be passed in the same direction. Default is 5.

Important : Turtle traders don't trade crypto. For this specific asset type, I modify some parameters such as SL and Short S1 in order to maximize return while limiting drawdown. This strategy is the most optimal on BINANCE:BTCUSD in 1D timeframe with the parameters set per default. If you want to use this strategy for a different crypto please adapt parameters.

NOTE :

It's important to note that the first entry order (long or short) will be the largest. Subsequent pyramid orders will have fewer units than the first order. We've set a maximum SL for the first order of 10%, meaning that you won't lose more than 10% of the value of your first order. However, it is possible to lose more on your pyramid orders, as the SL is increased/decreased by 0.5*ATR(20), which does not secure a loss of more than 10% on your pyramid orders. The risk remains well managed because the value of these orders is less than the value of the first order. Remain vigilant to this small detail and adjust your risk according to your risk aversion.

Enjoy the strategy and don’t forget to take the trade :)

mikul's Ichimoku Cloud Strategy v 2.0This is an Ichimoku cloud (long) strategy with both pump signals and trend signals.

It has both ATR stop loss, trailing percentage stop loss and also ichomoku cloud exit signal.

You can also combine the ATR stop loss and the trailing percentage stop loss with the Ichimoku cloud exit signal and a the take profit percentage.

In this example I use the default ATR stop loss method for taking profit.

10000$ is my initial capital and I risking 10% every trade. Commission is set to 0.075%.

Everything is set to default in this example.

There is also a moving average filter that is available, set to 200 EMA and turned off by default.

Conditions for taking a long position:

Trend Signal:

• Positive cross above the cloud

• Chikou span(lagging span) above price action

• Price above the Cloud

Pump Signal:

• Cloud ahead of you is green

• Price above the cloud

• Positive cross (Doesn’t Matter Where)

• Chikou span(lagging span) above the cloud

Ichimoku cloud exit signals:

• Negative cross

• Chikou span(lagging span) touches the price action

This strategy is totally free as freedom and as in free beer!

I do this for myself, but I like sharing and I want everyone to have the ability to use what I make no matter your economic situation.

If you have any suggestions for this strategy or perhaps any filtering options that could be fun to experiment with, then please leave a comment with your suggestion and maybe I can add it to the next version.

FlexiMA x FlexiST - Strategy [presentTrading]█ Introduction and How it is Different

The FlexiMA x FlexiST Strategy blends two analytical methods - FlexiMA and FlexiST, which are opened in my early post.

- FlexiMA calculates deviations between an indicator source and a dynamic moving average, controlled by a starting factor and increment factor.

- FlexiST, on the other hand, leverages the SuperTrend model, adjusting the Average True Range (ATR) length for a comprehensive trend-following oscillator.

This synergy offers traders a more nuanced and multifaceted tool for market analysis.

BTC 6H L/S Performance

Local

█ Strategy, How It Works: Detailed Explanation

The strategy combines two components: FlexiMA and FlexiST, each utilizing unique methodologies to analyze market trends.

🔶FlexiMA Component:

- Calculates deviations between an indicator source and moving averages of variable lengths.

- Moving average lengths are dynamically adjusted using a starting factor and increment factor.

- Deviations are normalized and analyzed to produce median and standard deviation values, forming the FlexiMA oscillator.

Length indicator (50)

🔶FlexiST Component:

- Uses SuperTrend indicators with varying ATR (Average True Range) lengths.

- Trends are identified based on the position of the indicator source relative to the SuperTrend bands.

- Deviations between the indicator source and SuperTrend values are calculated and normalized.

Starting Factor (5)

🔶Combined Strategy Logic:

- Entry Signals:

- Long Entry: Triggered when median values of both FlexiMA and FlexiST are positive.

- Short Entry: Triggered when median values of both FlexiMA and FlexiST are negative.

- Exit Signals:

- Long Exit: Triggered when median values of FlexiMA or FlexiST turn negative.

- Short Exit: Triggered when median values of FlexiMA or FlexiST turn positive.

This strategic blend of FlexiMA and FlexiST allows for a nuanced analysis of market trends, providing traders with signals based on a comprehensive view of market momentum and trend strength.

█ Trade Direction

The strategy is designed to cater to various trading preferences, offering "Long", "Short", and "Both" options. This flexibility allows traders to align the strategy with their specific market outlook, be it bullish, bearish, or a combination of both.

█ Usage

Traders can effectively utilize the FlexiMA x FlexiST Strategy by first selecting their desired trade direction. The strategy then generates entry signals when the conditions for either the FlexiMA or FlexiST are met, indicating potential entry points in the market. Conversely, exit signals are generated when the conditions for these indicators diverge, thus signaling a potential shift in market trends and suggesting a strategic exit point.

█ Default Settings

1. Indicator Source (HLC3): Provides a balanced and stable price source, reducing the impact of extreme market fluctuations.

2. Indicator Lengths (20 for FlexiMA, 10 for FlexiST): Longer FlexiMA length smooths out short-term fluctuations, while shorter FlexiST length allows for quicker response to market changes.

3. Starting Factors (1.0 for FlexiMA, 0.618 for FlexiST): Balanced start for FlexiMA and a harmonized approach for FlexiST, resonating with natural market cycles.

4. Increment Factors (1.0 for FlexiMA, 0.382 for FlexiST): FlexiMA captures a wide range of market behaviors, while FlexiST provides a gradual transition to capture finer trend shifts.

5. Normalization Methods ('None'): Uses raw deviations, suitable for markets where absolute price movements are more significant.

6. Trade Direction ('Both'): Allows strategy to consider both long and short opportunities, ideal for versatile market engagement.

*More details:

1. FlexiMA

2. FlexiST

5 ema strategyThis Strategy is based of Subhashish Pani's (power of stocks) 5 EMA Strategy.strategy used for sell in 5 minutes and for buy in 15 minutes ..

Rules for this strategy ..

Sell signal -

1) if price is above 5 Ema and not touching Ema use as alert candle..

2) if price break low of alert candle strategy open trade ..

3) if price move more upside low of alert candle keep change into next candle ..

4) input we can select number of trade per day .as rule should take only 4 signal should execute

5) stop loss is fixed highest high of last 2 candle and take profit is input multiply of stop loss

buy signal-

1) if price is below 5 Ema and not touching Ema use as alert candle..

2) if price break high of alert candle strategy open trade ..

3) if price move more downside high of alert candle keep change into next candle ..

4) input we can select number of trade per day .as rule should take only 4 signal should execute

5) stop loss is fixed lowest low of last 2 candle and take profit is input multiply of stop loss

notes -input can be selected which side should take signal either buy or sell side ...number of trade can be adjusted ..

Disclaimer -Traders can use this script as a starting point for further customization or as a reference for developing their own trading strategies. It's important to note that past performance is not indicative of future results, and thorough testing and validation are recommended before deploying any trading strategy.

CCI based support and resistance strategy

WARNING:

Commissions and slippage has not been considered! Don’t take it easy adding commissions and slippage could turns a fake-profitable strategy to a real disaster.

We consider account size as 10k and we enter 1000 for each trade.

Less than 100 trades is too small sample community and it’s not reliable, Also the performance of the past do not guarantee future performance. This result was handpicked by author and will differ by other timeframes, instruments and settings.

*PLEASE SHARE YOUR SETTINGS THAT WORK WITH THE COMMUNITY.

Introduction:

The CCI-based dynamic support and resistance is a "Bands and Channels" kind of indicator consisting an upper and lower band. This is a strategy which uses CCI-based (Made by me) indicator to execute trades.

SL and TP are calculated based on max ATR during last selected time period. You can edit strategy settings using "Ksl", "Ktp" and the other button for time period. “KSL” and “KTP” are 2.5 and 5 by default.

Bands are calculated regarding CCI previous high and low pivot. CCI length, right pivot length and left pivot length are 50.

A dynamic support and resistance has been calculated using last upper-cci minus a buffer and last lower-cci plus the buffer. The buffer is 10.

If "Trend matter?" button is on you can detect trend by color of the upper and lower line. Green is bullish and red is bearish! "Trend matter?" is on.

The "show mid?" button makes mid line visible, which is average of upper and lower lines, visible. The button is not active by default.

Reaction to the support could be a buy signal while a reaction to the resistance could interpreted as a sell signal.

How this strategy work?

Donald Lambert, a technical analyst, created the CCI, or Commodity Channel Index, which he first published in 1980. CCI is calculated regarding CCI can be used both as trend-detector or an oscillator. As an oscillator most traders believe in static predefined levels. Overbought and oversold candles which are clear in the chart could be used as sell and buy signals.

During my trading career I’ve noticed that there might be some reversal points for the CCI. I believe CCI could have to potential to reverse more from lately reversal point. Of course, just like other trading strategies we are talking about probabilities. We do not expect a win trade each time.

On price chart

Now this the question! What price should the instrument reach that CCI turns to be equal to our reversing aim for CCI? Imagine we have found last important bearish reversal of CCI in 200. Now, if we need the CCI to be 200 what price should we wait for?

How to calculate?

This is the CCI formula:

CCI = (Typical Price - SMA of TP) / (0.015 x Mean Deviation)

Where, Typical Price (TP) = (High + Low + Close)/3

For probable reversing points, high and low pivots of 50 bars have been used.

So we do have an Upper CCI and a Lower CCI. They are valid until the next pivot is available.

By relocating factors in CCI formula you can reach the “Typical Price”.

“

Typical Price = CCI (0.015 * Mean Deviation) + SMA of TP

So we could have a Support or Resistance by replacing CCI with Upper and Lower CCI.

A buy signal is valid if the trend is bullish (or “trend matter” is off) and lowest low of last 2 candles is lower than support and close is greater than both support and open.

A Sell signal is produced in opposite situation.

There are 2+1 options for trend!

Trend matter box is on by default, which means we’ll just open trades in direction of the trend. It’s available to turn it off.

Other 2 options are cross and slope. Cross calculated by comparing fast SMA and slow SMA. The slope one differentiate slow SMA to last “n” one.

Considering last day and today highest ATR as the ATR to calculating SL and TP is our unique technique.

Hulk Grid Algorithm V2 - The Quant ScienceIt's the latest proprietary grid algorithm developed by our team. This software represents a clearer and more comprehensive modernization of the deprecated Hulk Grid Algorithm. In this new release, we have optimized the source code architecture and investment logic, which we will describe in detail below.

Overview

Hulk Grid Algorithm V2 is designed to optimize returns in sideways market conditions. In this scenario, the algorithm divides purchases with long orders at each level of the grid. Unlike a typical grid algorithm, this version applies an anti-martingale model to mitigate volatility and optimize the average entry price. Starting from the lower level, the purchase quantity is increased at each new subsequent level until reaching the upper level. The initial quantity of the first order is fixed at 0.50% of the initial capital. With each new order, the initial quantity is multiplied by a value equal to the current grid level (where 1 is the lower level and 10 is the upper level).

Example: Let's say we have an initial capital of $10,000. The initial capital for the first order would be $50 * 1 = $50, for the second order $50 * 2 = $100, for the third order $50 * 3 = $150, and so on until reaching the upper level.

All previously opened orders are closed using a percentage-based stop-loss and take-profit, calculated based on the extremes of the grid.

Set Up

As mentioned earlier, the user's goal is to analyze this strategy in markets with a lack of trend, also known as sideways markets. After identifying a price range within which the asset tends to move, the user can choose to create the grid by placing the starting price at the center of the range. This way, they can consider trading the asset, if the backtesting generates a return greater than the Buy & Hold return.

Grid Configuration

To create the grid, it's sufficient to choose the starting price during the launch phase. This level will be the center of the grid from which the upper and lower levels will be calculated. The grid levels are computed using an arithmetic method, adding and subtracting a configurable fixed amount from the user interface (Grid Step $).

Example: Let's imagine choosing 1000 as the starting price and 50 as the Grid Step ($). The upper levels will be 1000, 1050, 1100, 1150, 1200. The lower levels will be 950, 900, 850, 800, and 750.

Markets

This software can be used in all markets: stocks, indices, commodities, cryptocurrencies, ETFs, Forex, etc.

Application

With this backtesting software, is possible to analyze the strategy and search for markets where it can generate better performance than Buy & Hold returns. There are no alerts or automatic investment mechanisms, and currently, the strategy can only be executed manually.

Design

Is possible to modify the grid style and customize colors by accessing the Properties section of the user interface.