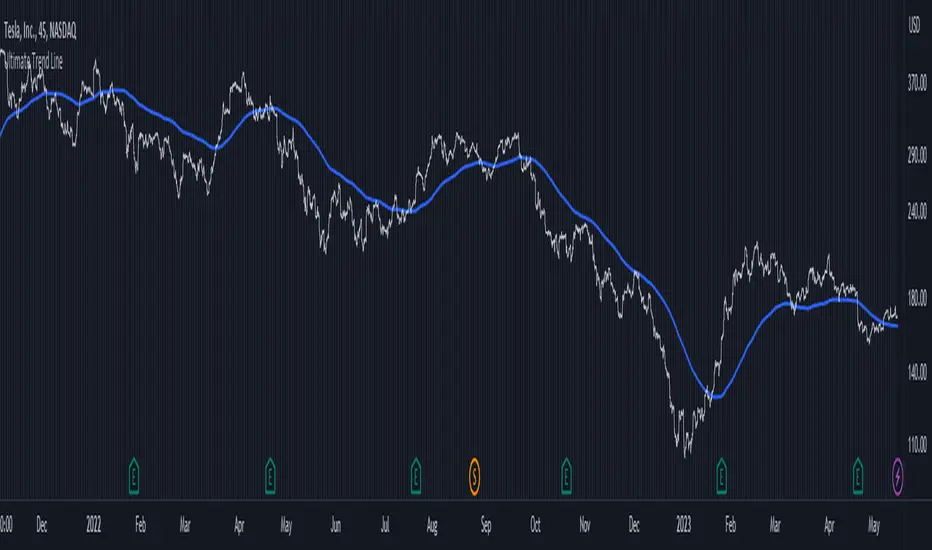

Ultimate Trend LineThe "Ultimate Trend Line" indicator, designed for overlay on financial charts, calculates and plots a global trend line. It works by first allowing users to input several parameters such as different lengths for up to 21 groups, a multiplier that defines the deviation from the linear regression line for calculating the upper and lower bands, and a color for the fill.

Using these inputs, it calculates the upper and lower bands for each length group based on a multiple of the standard deviation from the linear regression line. It then averages these bands to define the global trend line, which is plotted on the graph.

Although the code includes commented-out lines for plotting each individual upper and lower band, the indicator as it stands only displays the overall average trend line. The line's color and linewidth can be adjusted according to user preferences.

This indicator can be effectively used on both logarithmic and linear scales. This versatility allows it to be adaptable to various types of financial charts and trading styles, providing a flexible tool for users to assess and visualize trend patterns across different market conditions and time frames. It maintains its accuracy and relevance, regardless of the scale used, thus making it a comprehensive solution for trend line analysis in diverse scenarios.

It's important to note that the "Ultimate Trend Line" indicator requires a substantial amount of historical data to function properly. If insufficient historical data is available, the indicator may not display accurately or at all. This issue is particularly prevalent when using larger time units, such as weekly or monthly charts, where the available data may not stretch back far enough to satisfy the requirements of the indicator. As such, users should ensure they are operating on a time scale and data set that provides adequate historical depth for the reliable operation of this indicator.

Forecasting

Exponential ADR with Price TargetsThis script is designed to help you analyze price movements in the financial markets by calculating the Average Daily Range (ADR), adjusting it based on exponentiality and generating price targets based on that range.

The ADR represents the average range between the highest and lowest prices of a trading instrument during a specific period. It gives you an idea of how much the price typically moves in a day. In this script, we calculate the ADR using Simple Moving Averages (SMA) of the high and low prices over a certain length of time. You can customize this length according to your preference.

To make the ADR smoother and more responsive to recent price changes, we apply an Exponential Moving Average (EMA) to the ADR values. The EMA places more weight on recent data, giving you a more up-to-date measure of the ADR. The length of the EMA is also adjustable.

Once we have the Exponential ADR, we can generate price targets based on it. Price targets are potential levels where the price may reach in the future. We calculate these targets by adding or subtracting a certain multiple of the Exponential ADR from the current closing price. The multiple is determined by a parameter called the "Target Multiplier." You can adjust this value to control the distance of the price targets from the closing price.

In addition to plotting the Exponential ADR as a histogram on the chart, we create a table that displays the price targets. The table shows three bullish (positive) targets and three bearish (negative) targets. The targets are labeled as "Bull Target" or "Bear Target" followed by a number indicating the target's order. For each target, we display the corresponding price level.

To estimate the potential price levels, we used a formula that takes into account the current closing price and a value called the Exponential Average Daily Range (Exponential ADR). The Exponential ADR represents the average range of price movement over a specific period.

To calculate the price targets, we multiplied the Exponential ADR by a user-defined value called the target multiplier. This target multiplier allows traders to control the distance of the price targets from the current price. The resulting value indicates the desired distance from the current price for each target level.

For bullish targets, we added the calculated value to the current closing price. This suggests potential upward movement in the price. On the other hand, for bearish targets, we subtracted the calculated value from the current closing price. This indicates potential downward movement in the price.

By providing multiple target levels, such as level 1, level 2, and level 3, traders can assess different scenarios and potential price outcomes. These target levels help traders identify possible price levels where they might consider taking profit or adjusting their trading positions.

It's important to note that these price targets are not guaranteed to be reached, but they serve as reference points based on historical price behavior and the Exponential ADR. Traders can use them as part of their overall trading strategy and decision-making process.

Adjust the input parameters according to your desired settings, such as the ADR length, EMA length, target multiplier, table position, and table style. The indicator will then calculate and display the Exponential ADR and price targets on the chart, helping you identify potential levels of support and resistance for your trading decisions.

Matrix Momentum Expansion [IkkeOmar]The indicator consists of several features:

Candlestick chart: The indicator plots a candlestick chart based on the input parameters of the user. The candlesticks are colored blue or orange depending on whether the closing price is above or below the upper and lower bands.

Support and Resistance levels: The indicator also plots support and resistance levels based on the CCI (Commodity Channel Index) of the asset's price. These levels are dynamic and change based on the user's input parameters.

Momentum: The indicator calculates the momentum of the market based on the smoothed and standard deviation of the asset's price. It uses this momentum to calculate upper and lower bands that are plotted on the chart.

Warning signals: The indicator can also be used to identify potential warning signals. When the closing price of the asset moves above the upper band, it could indicate that the market is overbought and a potential reversal could occur. Conversely, when the closing price moves below the lower band, it could indicate that the market is oversold and a potential reversal could occur.

Contractions and expansions in the bands can provide important information to traders about potential price movements.

When the bands contract, it indicates that the market is experiencing low volatility and the price is likely to move sideways. During these periods, traders may look for other signals, such as support and resistance levels or price patterns, to determine potential entry and exit points.

On the other hand, when the bands expand, it indicates that the market is experiencing high volatility and the price is likely to move in a particular direction. Traders can use this information to identify potential trend reversals or continuation patterns. When the upper and lower bands move further apart, it indicates that the trend is becoming stronger, while when they move closer together, it indicates that the trend may be weakening.

When the price moves outside of the bands, it can also provide important information to traders. If the price moves above the upper band, it could indicate that the market is overbought and a potential reversal could occur. Conversely, if the price moves below the lower band, it could indicate that the market is oversold and a potential reversal could occur.

Very important note!

When you see contractions, please understand that it's a wonderful opportunity to pivot into position to catch a good trade because we will see an expansion after!

Bull Bear Correlation Tracker PaneThe Bull Bear Correlation Tracker is a versatile indicator designed to help traders identify the direction and strength of market trends by comparing the price action of multiple assets. It is particularly useful for those who are familiar with the carry trade principle, as it can detect when positively or negatively correlated assets move in favor or against the asset being traded. This indicator can be used for various markets, including crypto and forex, by simply adjusting the default options.

Key features of the Bull Bear Correlation Tracker include:

Multiple methods for determining trend direction: Supertrend, Pivot Point SuperTrend by LonesomeTheBlue, MACD - Zero Cross, and MACD - Grow/Shrink. These methods help traders identify the primary trend direction and potential trade opportunities.

Optional slow trend display for additional insights into market trends, allowing traders to analyze both short-term and long-term trends simultaneously.

Supports up to three symbols, enabling traders to analyze multiple assets simultaneously and better understand their correlation.

Assumed correlation settings to test traders' hypotheses about asset relationships, allowing traders to make informed decisions about potential correlations between different assets.

Customizable correlation period and smoothing settings to fine-tune the indicator's performance, providing traders with the ability to optimize the indicator based on their preferred trading style and market conditions.

Market hours filter to focus on specific trading hours, ensuring that the indicator only displays data during the hours specified.

Customizable color settings for easy visualization of trends, helping traders quickly identify the direction and strength of market trends.

Correlation histogram display to visualize asset relationships, providing traders with a clear visual representation of how different assets are correlated.

This indicator can be used to either force the correlation to be assumed positive or negative if the trader knows the correlation, or to use the actual data calculated between the traded asset and other assets if the correlation is broken often. This flexibility makes the Bull Bear Correlation Tracker suitable for trading various assets, including cryptocurrencies and forex, as well as for traders with different levels of experience.

By utilizing the Bull Bear Correlation Tracker, traders can gain valuable insights into market trends and correlations between different assets, helping them make more informed decisions and improve their trading strategies.

Note: I used back-testing for fine tuning do not base your trades on signals from the testing framework.

Price Action Color Forecast (Expo)█ Overview

The Price Action Color Forecast Indicator , is an innovative trading tool that uses the power of historical price action and candlestick patterns to predict potential future market movements. By analyzing the colors of the candlesticks and identifying specific price action events, this indicator provides traders with valuable insights into future market behavior based on past performance.

█ Calculations

The Price Action Color Forecast Indicator systematically analyzes historical price action events based on the colors of the candlesticks. Upon identifying a current price action coloring event, the indicator searches through its past data to find similar patterns that have happened before. By examining these past events and their outcomes, the indicator projects potential future price movements, offering traders valuable insights into how the market might react to the current price action event.

The indicator prioritizes the analysis of the most recent candlesticks before methodically progressing toward earlier data. This approach ensures that the generated candle forecast is based on the latest market dynamics.

The core functionality of the Price Action Color Forecast Indicator:

Analyzing historical price action events based on the colors of the candlesticks.

Identifying similar events from the past that correspond to the current price action coloring event.

Projecting potential future price action based on the outcomes of past similar events.

█ Example

In this example, we can see that the current price action pattern matches with a similar historical price action pattern that shares the same characteristics regarding candle coloring. The historical outcome is then projected into the future. This helps traders to understand how the past pattern evolved over time.

█ How to use

The indicator provides traders with valuable insights into how the market might react to the current price action event by examining similar historical patterns and projecting potential future price movements.

█ Settings

Candle series

The candle lookback length refers to the number of bars, starting from the current one, that will be examined in order to find a similar event in the past.

Forecast Candles

Number of candles to project into the future.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

hidden & regular rsi divergenceThis is a divergence indicator that draws regular and hidden divergences based on the Zigzag indicator and RSI indicator. There are two degrees of Zigzag. So, in each Zigzag degree, there are two types of regular divergences and one type of hidden divergence.

👉(The logic is written in case of a bearish regular divergence. The opposite will apply for a bullish one.)

Type 1 of regular divergence (Logic 1):

Zigzag has to form a higher high. The highest RSI within both Zigzag legs must form lower highs, but the RSI values which are exactly at the Zigzag highs should not form lower highs.

Type 2 of regular divergence (Logic 2):

Zigzag has to form a higher high. The highest RSI within both Zigzag legs must form lower highs, and the RSI values which are exactly at the Zigzag highs should form lower highs.

👉(The logic is written in case of a bearish hidden divergence. The opposite will apply for a bullish one.)

Zigzag has to form a lower high. The highest RSI within both Zigzag legs must form higher highs.

👉There is also a filter that will be applied to all the divergences. It only shows the divergences whose corresponding RSI value was above/below a level (overbought level/oversold level).

Logic for regular divergences:

Bearish regular divergence's first high's (leftmost) RSI value should be greater than or equal to 70.

Bullish regular divergence's first low's (leftmost) RSI value should be less than or equal to 30.

Logic for hidden divergences:

Bearish hidden divergence's second high's (rightmost) RSI value should be greater than or equal to 70.

Bullish hidden divergence's second low's (rightmost) RSI value should be less than or equal to 30.

👉There is another feature also. This indicator colors the background based on whether the RSI is in a bullish or bearish range.

If it's within 80-60, the background will be colored green (this means that RSI is in a bullish range).

If it's within 40-20, the background will be colored red (this means that RSI is in a bearish range).

Weekly and daily separatorsThis script plots vertical line between each trading week (thick, solid) and smaller lines (dotted) between each trading day. This helps kepping a better overview on the aspect of time on the higher timeframes below 1D. The distance of the lines to the top and bottom of the chart is controlled by your chart settings menu under Appearance -> Margins.

ICT SessionsThis script plots the timewindows of the ICT killzones (for forex) and trading session + makros below the chart. Individual components can be switched of to your liking

ICT MakrosThis script highlights the ICT trading makros and silverbullet timewindows with different background colors on your chart. The drawings are only visible on the timeframe 1min - 5min because they become useless above and i didnt code the logic for below 1min

Simple Moving Average Extrapolation via Monte Carlo (SMAE)In this post, I will dive into my Moving Average Extrapolator, a tool that I created to help traders predict future price movements based on past data. I will discuss the underlying logic, its limitations, and the importance of accounting for delays in the moving average. The following code, my Moving Average Extrapolator, will serve as the basis for our discussion.

The Moving Average Extrapolator uses a simple moving average (SMA) to analyze past price movements and make predictions about future price movements. It uses a Monte Carlo simulation to generate possible future price movements based on historical probabilities.

Let's start by understanding the different components of the code:

The movement_probability function calculates the probability of green and red price movements, where green movements indicate an increase in price, and red movements indicate a decrease in price.

The monte function generates an array of potential price movements using a Monte Carlo simulation.

The sim function uses the generated Monte Carlo array to simulate potential future price movements based on the probabilities calculated earlier.

The draw_lines function draws lines connecting the current price to the extrapolated future price movements.

The extrapolate function calculates the extrapolated future price movements based on the provided source, length, and accuracy.

Limitations of My Moving Average Extrapolator:

Reliance on historical data: My Moving Average Extrapolator relies heavily on historical data to make future price predictions. This can be a limitation, as past performance does not guarantee future results. Market conditions can change, making the extrapolator less reliable in predicting future price movements.

Inherent randomness: The Monte Carlo simulation introduces an element of randomness in the extrapolator's predictions. While this can help in exploring various scenarios, it may not always accurately predict future price movements.

Delay in the moving average: Moving averages inherently have a delay, as they are based on past data. This delay can cause my Moving Average Extrapolator to be less accurate in predicting immediate price movements.

Accounting for Delays in the Moving Average:

It is essential to account for the delay in the moving average to improve the accuracy of my Moving Average Extrapolator. I have taken this into account by introducing a delay variable (delay) in the draw_lines function. The delay variable calculates the delay as half the moving average's length and adjusts the time axis accordingly.

This adjustment helps in reducing the lag in the extrapolator's predictions, making it more accurate and useful for traders. However, it is important to note that even with this adjustment, my Moving Average Extrapolator is still subject to the limitations discussed earlier.

Adding Custom Lookback Period to My Moving Average Extrapolator:

To enhance the functionality and adaptability of my Moving Average Extrapolator, I have implemented an option to set a custom lookback period. The lookback period determines how far back in the historical data the Moving Average Extrapolator should start its analysis.

To achieve this, I have included a method to obtain the current bar index and then calculate the starting bar index by subtracting the desired lookback period.

Here's how to implement the custom lookback period in the Moving Average Extrapolator:

Get the current bar index: I use the bar_index built-in variable to get the current bar index, which represents the current position in the historical data.

Set the start index: To set the start index, you can subtract the desired lookback period from the current bar index. In the code, I have defined a user-input number variable, which can be set to the desired lookback period. By default, it is set to 20800. The starting index for the Moving Average Extrapolator's analysis is calculated as bar_index - number.

Here's the relevant code snippet:

number = input.int(20800, "Bar Start")

And to conditionally run the calculations:

if bar_index > number

draw_lines(avg, extrapolate(close, length, 10), length, extrapolate)

By implementing this custom lookback period, users can easily adjust the starting point of the Moving Average Extrapolator based on their preferences and trading strategies. This allows for more flexibility and adaptability to different market scenarios and ensures that the Moving Average Extrapolator remains a valuable tool for traders.

Conclusion:

My Moving Average Extrapolator can be a valuable tool for traders looking to predict future price movements based on historical data. However, it is essential to understand its limitations and the need to account for the delay in the moving average. By considering these factors, traders can make better-informed decisions and use my Moving Average Extrapolator to complement their trading strategies effectively.

BankNifty targets using VIX Version 2Original Idea Credit: Verified Market Waves

Hi,

After watching different videos online on how to get targets of BankNifty & Nifty decided to write this small script using VIX.

Nothing great but I really like the concept of getting high and low targets for the day or weekly or monthly or yearly.

What does the script do

1. We get closing of India Vix & BankNifty and Nifty

2. We get square root of Daily (365 days) | Weekly (52) | Monthly (12) & Yearly (1)

3. We divide India Vix closing with different square root to get a decimal value.

4. We use the derived value from step 3 which is used as % to calculate high and low values on BankNifty close price.

Small explanation via below screen shot to understand how to use it.

As always it comes with source code so you can modify as per your requirement.

Hope it helps 👍

Price Extrapolator with Std DeviationPrice Extrapolator with Deviation Cones - A Powerful Tool for Predicting Future Prices

Subtitle: Discover how this custom indicator can help you forecast potential price movements with greater accuracy, using historical data.

Introduction

Predicting future price movements is always a challenge for traders and investors. However, by using historical data and statistical analysis, it is possible to make educated guesses about the likelihood of certain outcomes. One such tool for predicting future prices is the Price Extrapolator with Standard Deviation Cones. This custom indicator, can help you visualize potential price movements and their associated risks.

In this post, we will explain how the Price Extrapolator with Deviation Cones works, how to adjust its settings to suit your needs, and how to interpret its output. By the end of this article, you should have a better understanding of how this powerful tool can help you make more informed decisions when trading or investing in financial markets.

Understanding the Price Extrapolator with Deviation Cones

The Price Extrapolator with Deviation Cones is a custom indicator that uses historical price data to calculate the average log return and standard deviation of log returns over a specified period. It then uses this information to extrapolate a series of future price points, as well as upper and lower standard deviation bands that form the "deviation cones."

The average log return represents the expected price change, while the standard deviation of log returns provides a measure of the uncertainty or risk associated with the prediction. The deviation cones can help you visualize the range of potential price movements and assess the likelihood of different outcomes.

Configuring the Indicator

To use the Price Extrapolator with Deviation Cones, you will need to configure several input settings:

1. Length: This setting determines the number of historical data points used to calculate the average log return and standard deviation of log returns. A higher value will produce a smoother, less sensitive indicator, while a lower value will make the indicator more responsive to recent price changes.

2. Number of Future Price Points: This setting controls the number of future price points to extrapolate. Increasing this value will extend the deviation cones further into the future.

3. Multiplier: This setting adjusts the tightness of the deviation cones by controlling the standard deviation multiplier. A higher value will result in wider cones, indicating greater uncertainty, while a lower value will produce narrower cones, suggesting more confidence in the prediction.

Interpreting the Output

After configuring the indicator, you will see the following output on your chart:

1. Green Line: This line represents the extrapolated future price points based on the average log return. It provides a central estimate of potential price movements.

2. Red Lines: These lines form the upper and lower bounds of the deviation cones. They represent the range of potential price movements, taking into account the uncertainty associated with the prediction.

When using the Price Extrapolator with Deviation Cones, it is essential to remember that the output is only a prediction based on historical data and should not be taken as a guarantee of future price movements. However, by providing a visual representation of potential price movements and their associated risks, this indicator can help you make more informed decisions when trading or investing in financial markets.

The Extreme Limitations of the Price Extrapolator with Deviation Cones

While the Price Extrapolator with Deviation Cones can be a valuable addition to your trading toolbox, it is essential to recognize its limitations. As with any forecasting tool, it is not infallible and should be used in conjunction with other forms of analysis. In this section, we will discuss the extreme limitations of this indicator and provide insight into how to use it effectively despite these constraints.

1. Reliance on Historical Data

The Price Extrapolator with Deviation Cones relies heavily on historical price data to make its predictions. While this can provide valuable insights into past trends and patterns, it may not accurately predict future price movements in a constantly changing market.

Market conditions can change rapidly, and historical data may not be a reliable indicator of future performance. Economic events, geopolitical tensions, and changes in market sentiment can all influence price movements in ways that may not be captured by historical data alone.

2. Assumption of Lognormal Distribution

The indicator assumes that price returns follow a lognormal distribution, which may not always be the case. Financial markets can exhibit skewness and kurtosis, resulting in distributions that are not symmetrical or normally distributed. This can lead to inaccurate predictions and a false sense of security when relying on the deviation cones.

3. No Consideration of Fundamental Factors

The Price Extrapolator with Deviation Cones is a purely technical analysis tool, meaning it does not take into account fundamental factors that can influence price movements. Changes in company earnings, interest rates, or economic data can significantly impact asset prices and may not be factored into the indicator's predictions.

4. Limited Time Horizon

The indicator only provides predictions for a limited number of future price points, which may not be sufficient for long-term investors or traders with longer holding periods. Additionally, the accuracy of the predictions may decrease as the time horizon extends, due to the compounding effects of uncertainty and the limitations of historical data.

5. Potential for Overfitting

When adjusting the settings of the Price Extrapolator with Deviation Cones, there is a risk of overfitting the model to the historical data. This can result in an indicator that appears to have excellent predictive power on past data but performs poorly on unseen, future data. It is crucial to be cautious when optimizing the settings and use out-of-sample testing to validate the indicator's performance.

Using the Price Extrapolator with Deviation Cones Effectively

Despite these limitations, the Price Extrapolator with Deviation Cones can still be a valuable tool when used correctly. To use this indicator effectively, consider the following tips:

1. Supplement with Other Forms of Analysis: Use the Price Extrapolator with Deviation Cones alongside other technical and fundamental analysis methods to gain a more comprehensive understanding of potential price movements.

2. Diversify your Trading Strategies: Do not rely solely on the Price Extrapolator with Deviation Cones for your trading decisions. Instead, diversify your strategies and consider multiple indicators and methods to reduce the risk of overreliance on a single tool.

3. Be Cautious with Optimized Settings: When adjusting the indicator's settings, be mindful of the risk of overfitting and validate the performance with out-of-sample testing.

4. Keep an Eye on Market Conditions: Stay informed about current market conditions, economic events, and news that may impact your trading decisions. This will help you make more informed decisions when using the Price Extrapolator with Deviation Cones.

In conclusion, the Price Extrapolator with Deviation Cones is a powerful and versatile tool that can aid traders and investors in predicting potential future price movements. However, it is crucial to remember that this indicator has its limitations, which stem from its reliance on historical data, the assumption of lognormal distribution, its disregard for fundamental factors, limited time horizons, and the potential for overfitting. Despite these constraints, when used correctly and in conjunction with other forms of analysis, the Price Extrapolator with Deviation Cones can provide valuable insights and assist in making more informed trading and investing decisions.

By understanding the underlying mechanics of the indicator, adjusting its settings according to your needs, and being aware of its limitations, you can incorporate the Price Extrapolator with Deviation Cones into your trading arsenal effectively. Always remember that no single tool or indicator is infallible, and it is essential to use a diverse range of analysis methods and strategies to navigate the ever-changing financial markets successfully. Happy trading!

Potential Gain/Loss IndicatorThis indicator calculates the gains and losses in percentage based on the highest high (ATH) and lowest low (ATL) of a given period. It takes the period as an input parameter and calculates the ATH and ATL within that period.

The indicator then calculates the potential gains in percentage if the price goes back to the ATH, as well as the potential losses in percentage if the price goes back to the ATL.

A filled area chart is plotted to show the difference between gains and losses (gains - losses) using a stepline, with green color when positive and red color when negative. The coefficient parameter allows for adjusting the scale of the gains and losses.

# Parameters

1. `period` (integer): The period used for calculating the highest high (ATH) and lowest low (ATL) within the given range. The default value is 50, and the user can select any value greater than or equal to 1.

2. `coef` (float): A coefficient to adjust the scale of the gains and losses. The default value is 0.5, and the user can select any value greater than or equal to 0.1.

Fibonacci Retracements & Trend Following Strategy Hello! This code creates a Fibonacci retracement indicator and a trend-following strategy indicator. Trading signals and price reversal targets are also calculated. The overall structure of the code is quite clear and readable. The purpose of the code is to calculate Fibonacci retracement levels and a trend-following indicator, display price levels on a chart, calculate trading signals, and calculate price reversal targets.

In the first section, Fibonacci levels are determined. Four different Fibonacci levels are defined: 0.236, 0.382, 0.618, and 0.786. These levels will be used as retracement levels.

Next, a trend-following indicator is calculated. This indicator calculates the averages of high and low prices over a certain period. This indicator can be used to determine the direction of the trend.

Then, price levels are calculated. These levels are determined by calculating the difference between the highest and lowest prices of the trend-following indicator. These levels are used in the calculation of Fibonacci retracement levels.

Next, Fibonacci levels are calculated. These levels are calculated by multiplying price levels with Fibonacci retracement levels. These levels are displayed on the chart.

Trading signals and price reversal targets are calculated. This can be used to trade using a Fibonacci retracement strategy.

Finally, price reversal targets are displayed as circles on the chart.

Usage Guide: Fibonacci Retracement Indicator and Trend Following Strategy

This indicator is used for calculating Fibonacci retracement levels and a trend following indicator, displaying price levels on the chart, calculating trading signals, and determining price targets for reversals. It is important to understand how the indicator works and what type of trading signals it generates before trading with it.

1.)Fibonacci Retracement Levels

Fibonacci retracement levels are used to measure the retracement levels of a trend on the chart. These levels can be used where traders are looking for a reversal signal in the market.

This indicator uses four different Fibonacci levels, which are 0.236, 0.382, 0.618, and 0.786. These levels will be used as retracement levels.

2.)Trend Following Indicator

The trend following indicator calculates the averages of high and low prices over a specific period. This indicator can be used to determine the direction of the trend. While showing a rising trend, it helps the prices stay high, and when showing a falling trend, it can help the prices stay low.

3.)Price Levels

Price levels are determined by calculating the difference between the highest and lowest prices of the trend following indicator. These levels are used to calculate Fibonacci retracement levels.

4.)Trading Signals and Price Reversal Targets

Trading signals and price reversal targets can be used to trade using a Fibonacci retracement strategy. The indicator can buy at Fibonacci levels where prices are retreating in an uptrend, and sell at Fibonacci levels where prices are retreating in a downtrend.

Price reversal targets are shown on the chart in circles.

5.)Fibonacci Retracement Targets

The Fibonacci retracement targets are shown in circles on the chart. These target price levels are calculated by applying Fibonacci retracement levels to the high and low price ranges. These levels can help determine buy or sell signals.

6.)Buy and Sell Signals

The most important feature of the indicator is to determine buy and sell signals. A buy signal is given when the trend-following indicator falls below one of the Fibonacci retracement levels and the price drops below it. A sell signal is given when the trend-following indicator rises and the price goes above one of the Fibonacci retracement levels.

7.)Target Price Levels

Using the retracement levels can be used to determine potential target price levels. Target price levels are determined based on Fibonacci retracement levels and positions can be closed when these levels are reached.

8.)Examples of Using the Indicator:

a) Buy Signal

If the trend-following indicator drops below the 0.618 Fibonacci retracement level and the price falls below it, a buy signal can be given. The target price level can be between the 0.382 and 0.236 Fibonacci retracement levels.

b) Sell Signal

If the trend-following indicator rises and the price goes above the 0.236 Fibonacci retracement level, a sell signal can be given. The target price level can be between the 0.382 and 0.618 Fibonacci retracement levels.

c) Target Price Levels

When a position is opened, target price levels can be determined based on Fibonacci retracement levels. For example, when opening a buy position, the target price level can be between the 0.382 and 0.236 Fibonacci retracement levels.

The use of the indicator can be made more effective by using it together with other technical analysis tools. In addition, practical experimentation with the use of the indicator in different scenarios can help understand how the indicator works.

Goertzel Browser [Loxx]As the financial markets become increasingly complex and data-driven, traders and analysts must leverage powerful tools to gain insights and make informed decisions. One such tool is the Goertzel Browser indicator, a sophisticated technical analysis indicator that helps identify cyclical patterns in financial data. This powerful tool is capable of detecting cyclical patterns in financial data, helping traders to make better predictions and optimize their trading strategies. With its unique combination of mathematical algorithms and advanced charting capabilities, this indicator has the potential to revolutionize the way we approach financial modeling and trading.

█ Brief Overview of the Goertzel Browser

The Goertzel Browser is a sophisticated technical analysis tool that utilizes the Goertzel algorithm to analyze and visualize cyclical components within a financial time series. By identifying these cycles and their characteristics, the indicator aims to provide valuable insights into the market's underlying price movements, which could potentially be used for making informed trading decisions.

The primary purpose of this indicator is to:

1. Detect and analyze the dominant cycles present in the price data.

2. Reconstruct and visualize the composite wave based on the detected cycles.

3. Project the composite wave into the future, providing a potential roadmap for upcoming price movements.

To achieve this, the indicator performs several tasks:

1. Detrending the price data: The indicator preprocesses the price data using various detrending techniques, such as Hodrick-Prescott filters, zero-lag moving averages, and linear regression, to remove the underlying trend and focus on the cyclical components.

2. Applying the Goertzel algorithm: The indicator applies the Goertzel algorithm to the detrended price data, identifying the dominant cycles and their characteristics, such as amplitude, phase, and cycle strength.

3. Constructing the composite wave: The indicator reconstructs the composite wave by combining the detected cycles, either by using a user-defined list of cycles or by selecting the top N cycles based on their amplitude or cycle strength.

4. Visualizing the composite wave: The indicator plots the composite wave, using solid lines for the past and dotted lines for the future projections. The color of the lines indicates whether the wave is increasing or decreasing.

5. Displaying cycle information: The indicator provides a table that displays detailed information about the detected cycles, including their rank, period, Bartel's test results, amplitude, and phase.

This indicator is a powerful tool that employs the Goertzel algorithm to analyze and visualize the cyclical components within a financial time series. By providing insights into the underlying price movements and their potential future trajectory, the indicator aims to assist traders in making more informed decisions.

█ What is the Goertzel Algorithm?

The Goertzel algorithm, named after Gerald Goertzel, is a digital signal processing technique that is used to efficiently compute individual terms of the Discrete Fourier Transform (DFT). It was first introduced in 1958, and since then, it has found various applications in the fields of engineering, mathematics, and physics.

The Goertzel algorithm is primarily used to detect specific frequency components within a digital signal, making it particularly useful in applications where only a few frequency components are of interest. The algorithm is computationally efficient, as it requires fewer calculations than the Fast Fourier Transform (FFT) when detecting a small number of frequency components. This efficiency makes the Goertzel algorithm a popular choice in applications such as:

1. Telecommunications: The Goertzel algorithm is used for decoding Dual-Tone Multi-Frequency (DTMF) signals, which are the tones generated when pressing buttons on a telephone keypad. By identifying specific frequency components, the algorithm can accurately determine which button has been pressed.

2. Audio processing: The algorithm can be used to detect specific pitches or harmonics in an audio signal, making it useful in applications like pitch detection and tuning musical instruments.

3. Vibration analysis: In the field of mechanical engineering, the Goertzel algorithm can be applied to analyze vibrations in rotating machinery, helping to identify faulty components or signs of wear.

4. Power system analysis: The algorithm can be used to measure harmonic content in power systems, allowing engineers to assess power quality and detect potential issues.

The Goertzel algorithm is used in these applications because it offers several advantages over other methods, such as the FFT:

1. Computational efficiency: The Goertzel algorithm requires fewer calculations when detecting a small number of frequency components, making it more computationally efficient than the FFT in these cases.

2. Real-time analysis: The algorithm can be implemented in a streaming fashion, allowing for real-time analysis of signals, which is crucial in applications like telecommunications and audio processing.

3. Memory efficiency: The Goertzel algorithm requires less memory than the FFT, as it only computes the frequency components of interest.

4. Precision: The algorithm is less susceptible to numerical errors compared to the FFT, ensuring more accurate results in applications where precision is essential.

The Goertzel algorithm is an efficient digital signal processing technique that is primarily used to detect specific frequency components within a signal. Its computational efficiency, real-time capabilities, and precision make it an attractive choice for various applications, including telecommunications, audio processing, vibration analysis, and power system analysis. The algorithm has been widely adopted since its introduction in 1958 and continues to be an essential tool in the fields of engineering, mathematics, and physics.

█ Goertzel Algorithm in Quantitative Finance: In-Depth Analysis and Applications

The Goertzel algorithm, initially designed for signal processing in telecommunications, has gained significant traction in the financial industry due to its efficient frequency detection capabilities. In quantitative finance, the Goertzel algorithm has been utilized for uncovering hidden market cycles, developing data-driven trading strategies, and optimizing risk management. This section delves deeper into the applications of the Goertzel algorithm in finance, particularly within the context of quantitative trading and analysis.

Unveiling Hidden Market Cycles:

Market cycles are prevalent in financial markets and arise from various factors, such as economic conditions, investor psychology, and market participant behavior. The Goertzel algorithm's ability to detect and isolate specific frequencies in price data helps trader analysts identify hidden market cycles that may otherwise go unnoticed. By examining the amplitude, phase, and periodicity of each cycle, traders can better understand the underlying market structure and dynamics, enabling them to develop more informed and effective trading strategies.

Developing Quantitative Trading Strategies:

The Goertzel algorithm's versatility allows traders to incorporate its insights into a wide range of trading strategies. By identifying the dominant market cycles in a financial instrument's price data, traders can create data-driven strategies that capitalize on the cyclical nature of markets.

For instance, a trader may develop a mean-reversion strategy that takes advantage of the identified cycles. By establishing positions when the price deviates from the predicted cycle, the trader can profit from the subsequent reversion to the cycle's mean. Similarly, a momentum-based strategy could be designed to exploit the persistence of a dominant cycle by entering positions that align with the cycle's direction.

Enhancing Risk Management:

The Goertzel algorithm plays a vital role in risk management for quantitative strategies. By analyzing the cyclical components of a financial instrument's price data, traders can gain insights into the potential risks associated with their trading strategies.

By monitoring the amplitude and phase of dominant cycles, a trader can detect changes in market dynamics that may pose risks to their positions. For example, a sudden increase in amplitude may indicate heightened volatility, prompting the trader to adjust position sizing or employ hedging techniques to protect their portfolio. Additionally, changes in phase alignment could signal a potential shift in market sentiment, necessitating adjustments to the trading strategy.

Expanding Quantitative Toolkits:

Traders can augment the Goertzel algorithm's insights by combining it with other quantitative techniques, creating a more comprehensive and sophisticated analysis framework. For example, machine learning algorithms, such as neural networks or support vector machines, could be trained on features extracted from the Goertzel algorithm to predict future price movements more accurately.

Furthermore, the Goertzel algorithm can be integrated with other technical analysis tools, such as moving averages or oscillators, to enhance their effectiveness. By applying these tools to the identified cycles, traders can generate more robust and reliable trading signals.

The Goertzel algorithm offers invaluable benefits to quantitative finance practitioners by uncovering hidden market cycles, aiding in the development of data-driven trading strategies, and improving risk management. By leveraging the insights provided by the Goertzel algorithm and integrating it with other quantitative techniques, traders can gain a deeper understanding of market dynamics and devise more effective trading strategies.

█ Indicator Inputs

src: This is the source data for the analysis, typically the closing price of the financial instrument.

detrendornot: This input determines the method used for detrending the source data. Detrending is the process of removing the underlying trend from the data to focus on the cyclical components.

The available options are:

hpsmthdt: Detrend using Hodrick-Prescott filter centered moving average.

zlagsmthdt: Detrend using zero-lag moving average centered moving average.

logZlagRegression: Detrend using logarithmic zero-lag linear regression.

hpsmth: Detrend using Hodrick-Prescott filter.

zlagsmth: Detrend using zero-lag moving average.

DT_HPper1 and DT_HPper2: These inputs define the period range for the Hodrick-Prescott filter centered moving average when detrendornot is set to hpsmthdt.

DT_ZLper1 and DT_ZLper2: These inputs define the period range for the zero-lag moving average centered moving average when detrendornot is set to zlagsmthdt.

DT_RegZLsmoothPer: This input defines the period for the zero-lag moving average used in logarithmic zero-lag linear regression when detrendornot is set to logZlagRegression.

HPsmoothPer: This input defines the period for the Hodrick-Prescott filter when detrendornot is set to hpsmth.

ZLMAsmoothPer: This input defines the period for the zero-lag moving average when detrendornot is set to zlagsmth.

MaxPer: This input sets the maximum period for the Goertzel algorithm to search for cycles.

squaredAmp: This boolean input determines whether the amplitude should be squared in the Goertzel algorithm.

useAddition: This boolean input determines whether the Goertzel algorithm should use addition for combining the cycles.

useCosine: This boolean input determines whether the Goertzel algorithm should use cosine waves instead of sine waves.

UseCycleStrength: This boolean input determines whether the Goertzel algorithm should compute the cycle strength, which is a normalized measure of the cycle's amplitude.

WindowSizePast and WindowSizeFuture: These inputs define the window size for past and future projections of the composite wave.

FilterBartels: This boolean input determines whether Bartel's test should be applied to filter out non-significant cycles.

BartNoCycles: This input sets the number of cycles to be used in Bartel's test.

BartSmoothPer: This input sets the period for the moving average used in Bartel's test.

BartSigLimit: This input sets the significance limit for Bartel's test, below which cycles are considered insignificant.

SortBartels: This boolean input determines whether the cycles should be sorted by their Bartel's test results.

UseCycleList: This boolean input determines whether a user-defined list of cycles should be used for constructing the composite wave. If set to false, the top N cycles will be used.

Cycle1, Cycle2, Cycle3, Cycle4, and Cycle5: These inputs define the user-defined list of cycles when 'UseCycleList' is set to true. If using a user-defined list, each of these inputs represents the period of a specific cycle to include in the composite wave.

StartAtCycle: This input determines the starting index for selecting the top N cycles when UseCycleList is set to false. This allows you to skip a certain number of cycles from the top before selecting the desired number of cycles.

UseTopCycles: This input sets the number of top cycles to use for constructing the composite wave when UseCycleList is set to false. The cycles are ranked based on their amplitudes or cycle strengths, depending on the UseCycleStrength input.

SubtractNoise: This boolean input determines whether to subtract the noise (remaining cycles) from the composite wave. If set to true, the composite wave will only include the top N cycles specified by UseTopCycles.

█ Exploring Auxiliary Functions

The following functions demonstrate advanced techniques for analyzing financial markets, including zero-lag moving averages, Bartels probability, detrending, and Hodrick-Prescott filtering. This section examines each function in detail, explaining their purpose, methodology, and applications in finance. We will examine how each function contributes to the overall performance and effectiveness of the indicator and how they work together to create a powerful analytical tool.

Zero-Lag Moving Average:

The zero-lag moving average function is designed to minimize the lag typically associated with moving averages. This is achieved through a two-step weighted linear regression process that emphasizes more recent data points. The function calculates a linearly weighted moving average (LWMA) on the input data and then applies another LWMA on the result. By doing this, the function creates a moving average that closely follows the price action, reducing the lag and improving the responsiveness of the indicator.

The zero-lag moving average function is used in the indicator to provide a responsive, low-lag smoothing of the input data. This function helps reduce the noise and fluctuations in the data, making it easier to identify and analyze underlying trends and patterns. By minimizing the lag associated with traditional moving averages, this function allows the indicator to react more quickly to changes in market conditions, providing timely signals and improving the overall effectiveness of the indicator.

Bartels Probability:

The Bartels probability function calculates the probability of a given cycle being significant in a time series. It uses a mathematical test called the Bartels test to assess the significance of cycles detected in the data. The function calculates coefficients for each detected cycle and computes an average amplitude and an expected amplitude. By comparing these values, the Bartels probability is derived, indicating the likelihood of a cycle's significance. This information can help in identifying and analyzing dominant cycles in financial markets.

The Bartels probability function is incorporated into the indicator to assess the significance of detected cycles in the input data. By calculating the Bartels probability for each cycle, the indicator can prioritize the most significant cycles and focus on the market dynamics that are most relevant to the current trading environment. This function enhances the indicator's ability to identify dominant market cycles, improving its predictive power and aiding in the development of effective trading strategies.

Detrend Logarithmic Zero-Lag Regression:

The detrend logarithmic zero-lag regression function is used for detrending data while minimizing lag. It combines a zero-lag moving average with a linear regression detrending method. The function first calculates the zero-lag moving average of the logarithm of input data and then applies a linear regression to remove the trend. By detrending the data, the function isolates the cyclical components, making it easier to analyze and interpret the underlying market dynamics.

The detrend logarithmic zero-lag regression function is used in the indicator to isolate the cyclical components of the input data. By detrending the data, the function enables the indicator to focus on the cyclical movements in the market, making it easier to analyze and interpret market dynamics. This function is essential for identifying cyclical patterns and understanding the interactions between different market cycles, which can inform trading decisions and enhance overall market understanding.

Bartels Cycle Significance Test:

The Bartels cycle significance test is a function that combines the Bartels probability function and the detrend logarithmic zero-lag regression function to assess the significance of detected cycles. The function calculates the Bartels probability for each cycle and stores the results in an array. By analyzing the probability values, traders and analysts can identify the most significant cycles in the data, which can be used to develop trading strategies and improve market understanding.

The Bartels cycle significance test function is integrated into the indicator to provide a comprehensive analysis of the significance of detected cycles. By combining the Bartels probability function and the detrend logarithmic zero-lag regression function, this test evaluates the significance of each cycle and stores the results in an array. The indicator can then use this information to prioritize the most significant cycles and focus on the most relevant market dynamics. This function enhances the indicator's ability to identify and analyze dominant market cycles, providing valuable insights for trading and market analysis.

Hodrick-Prescott Filter:

The Hodrick-Prescott filter is a popular technique used to separate the trend and cyclical components of a time series. The function applies a smoothing parameter to the input data and calculates a smoothed series using a two-sided filter. This smoothed series represents the trend component, which can be subtracted from the original data to obtain the cyclical component. The Hodrick-Prescott filter is commonly used in economics and finance to analyze economic data and financial market trends.

The Hodrick-Prescott filter is incorporated into the indicator to separate the trend and cyclical components of the input data. By applying the filter to the data, the indicator can isolate the trend component, which can be used to analyze long-term market trends and inform trading decisions. Additionally, the cyclical component can be used to identify shorter-term market dynamics and provide insights into potential trading opportunities. The inclusion of the Hodrick-Prescott filter adds another layer of analysis to the indicator, making it more versatile and comprehensive.

Detrending Options: Detrend Centered Moving Average:

The detrend centered moving average function provides different detrending methods, including the Hodrick-Prescott filter and the zero-lag moving average, based on the selected detrending method. The function calculates two sets of smoothed values using the chosen method and subtracts one set from the other to obtain a detrended series. By offering multiple detrending options, this function allows traders and analysts to select the most appropriate method for their specific needs and preferences.

The detrend centered moving average function is integrated into the indicator to provide users with multiple detrending options, including the Hodrick-Prescott filter and the zero-lag moving average. By offering multiple detrending methods, the indicator allows users to customize the analysis to their specific needs and preferences, enhancing the indicator's overall utility and adaptability. This function ensures that the indicator can cater to a wide range of trading styles and objectives, making it a valuable tool for a diverse group of market participants.

The auxiliary functions functions discussed in this section demonstrate the power and versatility of mathematical techniques in analyzing financial markets. By understanding and implementing these functions, traders and analysts can gain valuable insights into market dynamics, improve their trading strategies, and make more informed decisions. The combination of zero-lag moving averages, Bartels probability, detrending methods, and the Hodrick-Prescott filter provides a comprehensive toolkit for analyzing and interpreting financial data. The integration of advanced functions in a financial indicator creates a powerful and versatile analytical tool that can provide valuable insights into financial markets. By combining the zero-lag moving average,

█ In-Depth Analysis of the Goertzel Browser Code

The Goertzel Browser code is an implementation of the Goertzel Algorithm, an efficient technique to perform spectral analysis on a signal. The code is designed to detect and analyze dominant cycles within a given financial market data set. This section will provide an extremely detailed explanation of the code, its structure, functions, and intended purpose.

Function signature and input parameters:

The Goertzel Browser function accepts numerous input parameters for customization, including source data (src), the current bar (forBar), sample size (samplesize), period (per), squared amplitude flag (squaredAmp), addition flag (useAddition), cosine flag (useCosine), cycle strength flag (UseCycleStrength), past and future window sizes (WindowSizePast, WindowSizeFuture), Bartels filter flag (FilterBartels), Bartels-related parameters (BartNoCycles, BartSmoothPer, BartSigLimit), sorting flag (SortBartels), and output buffers (goeWorkPast, goeWorkFuture, cyclebuffer, amplitudebuffer, phasebuffer, cycleBartelsBuffer).

Initializing variables and arrays:

The code initializes several float arrays (goeWork1, goeWork2, goeWork3, goeWork4) with the same length as twice the period (2 * per). These arrays store intermediate results during the execution of the algorithm.

Preprocessing input data:

The input data (src) undergoes preprocessing to remove linear trends. This step enhances the algorithm's ability to focus on cyclical components in the data. The linear trend is calculated by finding the slope between the first and last values of the input data within the sample.

Iterative calculation of Goertzel coefficients:

The core of the Goertzel Browser algorithm lies in the iterative calculation of Goertzel coefficients for each frequency bin. These coefficients represent the spectral content of the input data at different frequencies. The code iterates through the range of frequencies, calculating the Goertzel coefficients using a nested loop structure.

Cycle strength computation:

The code calculates the cycle strength based on the Goertzel coefficients. This is an optional step, controlled by the UseCycleStrength flag. The cycle strength provides information on the relative influence of each cycle on the data per bar, considering both amplitude and cycle length. The algorithm computes the cycle strength either by squaring the amplitude (controlled by squaredAmp flag) or using the actual amplitude values.

Phase calculation:

The Goertzel Browser code computes the phase of each cycle, which represents the position of the cycle within the input data. The phase is calculated using the arctangent function (math.atan) based on the ratio of the imaginary and real components of the Goertzel coefficients.

Peak detection and cycle extraction:

The algorithm performs peak detection on the computed amplitudes or cycle strengths to identify dominant cycles. It stores the detected cycles in the cyclebuffer array, along with their corresponding amplitudes and phases in the amplitudebuffer and phasebuffer arrays, respectively.

Sorting cycles by amplitude or cycle strength:

The code sorts the detected cycles based on their amplitude or cycle strength in descending order. This allows the algorithm to prioritize cycles with the most significant impact on the input data.

Bartels cycle significance test:

If the FilterBartels flag is set, the code performs a Bartels cycle significance test on the detected cycles. This test determines the statistical significance of each cycle and filters out the insignificant cycles. The significant cycles are stored in the cycleBartelsBuffer array. If the SortBartels flag is set, the code sorts the significant cycles based on their Bartels significance values.

Waveform calculation:

The Goertzel Browser code calculates the waveform of the significant cycles for both past and future time windows. The past and future windows are defined by the WindowSizePast and WindowSizeFuture parameters, respectively. The algorithm uses either cosine or sine functions (controlled by the useCosine flag) to calculate the waveforms for each cycle. The useAddition flag determines whether the waveforms should be added or subtracted.

Storing waveforms in matrices:

The calculated waveforms for each cycle are stored in two matrices - goeWorkPast and goeWorkFuture. These matrices hold the waveforms for the past and future time windows, respectively. Each row in the matrices represents a time window position, and each column corresponds to a cycle.

Returning the number of cycles:

The Goertzel Browser function returns the total number of detected cycles (number_of_cycles) after processing the input data. This information can be used to further analyze the results or to visualize the detected cycles.

The Goertzel Browser code is a comprehensive implementation of the Goertzel Algorithm, specifically designed for detecting and analyzing dominant cycles within financial market data. The code offers a high level of customization, allowing users to fine-tune the algorithm based on their specific needs. The Goertzel Browser's combination of preprocessing, iterative calculations, cycle extraction, sorting, significance testing, and waveform calculation makes it a powerful tool for understanding cyclical components in financial data.

█ Generating and Visualizing Composite Waveform

The indicator calculates and visualizes the composite waveform for both past and future time windows based on the detected cycles. Here's a detailed explanation of this process:

Updating WindowSizePast and WindowSizeFuture:

The WindowSizePast and WindowSizeFuture are updated to ensure they are at least twice the MaxPer (maximum period).

Initializing matrices and arrays:

Two matrices, goeWorkPast and goeWorkFuture, are initialized to store the Goertzel results for past and future time windows. Multiple arrays are also initialized to store cycle, amplitude, phase, and Bartels information.

Preparing the source data (srcVal) array:

The source data is copied into an array, srcVal, and detrended using one of the selected methods (hpsmthdt, zlagsmthdt, logZlagRegression, hpsmth, or zlagsmth).

Goertzel function call:

The Goertzel function is called to analyze the detrended source data and extract cycle information. The output, number_of_cycles, contains the number of detected cycles.

Initializing arrays for past and future waveforms:

Three arrays, epgoertzel, goertzel, and goertzelFuture, are initialized to store the endpoint Goertzel, non-endpoint Goertzel, and future Goertzel projections, respectively.

Calculating composite waveform for past bars (goertzel array):

The past composite waveform is calculated by summing the selected cycles (either from the user-defined cycle list or the top cycles) and optionally subtracting the noise component.

Calculating composite waveform for future bars (goertzelFuture array):

The future composite waveform is calculated in a similar way as the past composite waveform.

Drawing past composite waveform (pvlines):

The past composite waveform is drawn on the chart using solid lines. The color of the lines is determined by the direction of the waveform (green for upward, red for downward).

Drawing future composite waveform (fvlines):

The future composite waveform is drawn on the chart using dotted lines. The color of the lines is determined by the direction of the waveform (fuchsia for upward, yellow for downward).

Displaying cycle information in a table (table3):

A table is created to display the cycle information, including the rank, period, Bartel value, amplitude (or cycle strength), and phase of each detected cycle.

Filling the table with cycle information:

The indicator iterates through the detected cycles and retrieves the relevant information (period, amplitude, phase, and Bartel value) from the corresponding arrays. It then fills the table with this information, displaying the values up to six decimal places.

To summarize, this indicator generates a composite waveform based on the detected cycles in the financial data. It calculates the composite waveforms for both past and future time windows and visualizes them on the chart using colored lines. Additionally, it displays detailed cycle information in a table, including the rank, period, Bartel value, amplitude (or cycle strength), and phase of each detected cycle.

█ Enhancing the Goertzel Algorithm-Based Script for Financial Modeling and Trading

The Goertzel algorithm-based script for detecting dominant cycles in financial data is a powerful tool for financial modeling and trading. It provides valuable insights into the past behavior of these cycles and potential future impact. However, as with any algorithm, there is always room for improvement. This section discusses potential enhancements to the existing script to make it even more robust and versatile for financial modeling, general trading, advanced trading, and high-frequency finance trading.

Enhancements for Financial Modeling

Data preprocessing: One way to improve the script's performance for financial modeling is to introduce more advanced data preprocessing techniques. This could include removing outliers, handling missing data, and normalizing the data to ensure consistent and accurate results.

Additional detrending and smoothing methods: Incorporating more sophisticated detrending and smoothing techniques, such as wavelet transform or empirical mode decomposition, can help improve the script's ability to accurately identify cycles and trends in the data.

Machine learning integration: Integrating machine learning techniques, such as artificial neural networks or support vector machines, can help enhance the script's predictive capabilities, leading to more accurate financial models.

Enhancements for General and Advanced Trading

Customizable indicator integration: Allowing users to integrate their own technical indicators can help improve the script's effectiveness for both general and advanced trading. By enabling the combination of the dominant cycle information with other technical analysis tools, traders can develop more comprehensive trading strategies.

Risk management and position sizing: Incorporating risk management and position sizing functionality into the script can help traders better manage their trades and control potential losses. This can be achieved by calculating the optimal position size based on the user's risk tolerance and account size.

Multi-timeframe analysis: Enhancing the script to perform multi-timeframe analysis can provide traders with a more holistic view of market trends and cycles. By identifying dominant cycles on different timeframes, traders can gain insights into the potential confluence of cycles and make better-informed trading decisions.

Enhancements for High-Frequency Finance Trading

Algorithm optimization: To ensure the script's suitability for high-frequency finance trading, optimizing the algorithm for faster execution is crucial. This can be achieved by employing efficient data structures and refining the calculation methods to minimize computational complexity.

Real-time data streaming: Integrating real-time data streaming capabilities into the script can help high-frequency traders react to market changes more quickly. By continuously updating the cycle information based on real-time market data, traders can adapt their strategies accordingly and capitalize on short-term market fluctuations.

Order execution and trade management: To fully leverage the script's capabilities for high-frequency trading, implementing functionality for automated order execution and trade management is essential. This can include features such as stop-loss and take-profit orders, trailing stops, and automated trade exit strategies.

While the existing Goertzel algorithm-based script is a valuable tool for detecting dominant cycles in financial data, there are several potential enhancements that can make it even more powerful for financial modeling, general trading, advanced trading, and high-frequency finance trading. By incorporating these improvements, the script can become a more versatile and effective tool for traders and financial analysts alike.

█ Understanding the Limitations of the Goertzel Algorithm

While the Goertzel algorithm-based script for detecting dominant cycles in financial data provides valuable insights, it is important to be aware of its limitations and drawbacks. Some of the key drawbacks of this indicator are:

Lagging nature:

As with many other technical indicators, the Goertzel algorithm-based script can suffer from lagging effects, meaning that it may not immediately react to real-time market changes. This lag can lead to late entries and exits, potentially resulting in reduced profitability or increased losses.

Parameter sensitivity:

The performance of the script can be sensitive to the chosen parameters, such as the detrending methods, smoothing techniques, and cycle detection settings. Improper parameter selection may lead to inaccurate cycle detection or increased false signals, which can negatively impact trading performance.

Complexity:

The Goertzel algorithm itself is relatively complex, making it difficult for novice traders or those unfamiliar with the concept of cycle analysis to fully understand and effectively utilize the script. This complexity can also make it challenging to optimize the script for specific trading styles or market conditions.

Overfitting risk:

As with any data-driven approach, there is a risk of overfitting when using the Goertzel algorithm-based script. Overfitting occurs when a model becomes too specific to the historical data it was trained on, leading to poor performance on new, unseen data. This can result in misleading signals and reduced trading performance.

No guarantee of future performance: While the script can provide insights into past cycles and potential future trends, it is important to remember that past performance does not guarantee future results. Market conditions can change, and relying solely on the script's predictions without considering other factors may lead to poor trading decisions.

Limited applicability: The Goertzel algorithm-based script may not be suitable for all markets, trading styles, or timeframes. Its effectiveness in detecting cycles may be limited in certain market conditions, such as during periods of extreme volatility or low liquidity.

While the Goertzel algorithm-based script offers valuable insights into dominant cycles in financial data, it is essential to consider its drawbacks and limitations when incorporating it into a trading strategy. Traders should always use the script in conjunction with other technical and fundamental analysis tools, as well as proper risk management, to make well-informed trading decisions.

█ Interpreting Results

The Goertzel Browser indicator can be interpreted by analyzing the plotted lines and the table presented alongside them. The indicator plots two lines: past and future composite waves. The past composite wave represents the composite wave of the past price data, and the future composite wave represents the projected composite wave for the next period.

The past composite wave line displays a solid line, with green indicating a bullish trend and red indicating a bearish trend. On the other hand, the future composite wave line is a dotted line with fuchsia indicating a bullish trend and yellow indicating a bearish trend.

The table presented alongside the indicator shows the top cycles with their corresponding rank, period, Bartels, amplitude or cycle strength, and phase. The amplitude is a measure of the strength of the cycle, while the phase is the position of the cycle within the data series.

Interpreting the Goertzel Browser indicator involves identifying the trend of the past and future composite wave lines and matching them with the corresponding bullish or bearish color. Additionally, traders can identify the top cycles with the highest amplitude or cycle strength and utilize them in conjunction with other technical indicators and fundamental analysis for trading decisions.

This indicator is considered a repainting indicator because the value of the indicator is calculated based on the past price data. As new price data becomes available, the indicator's value is recalculated, potentially causing the indicator's past values to change. This can create a false impression of the indicator's performance, as it may appear to have provided a profitable trading signal in the past when, in fact, that signal did not exist at the time.

The Goertzel indicator is also non-endpointed, meaning that it is not calculated up to the current bar or candle. Instead, it uses a fixed amount of historical data to calculate its values, which can make it difficult to use for real-time trading decisions. For example, if the indicator uses 100 bars of historical data to make its calculations, it cannot provide a signal until the current bar has closed and become part of the historical data. This can result in missed trading opportunities or delayed signals.

█ Conclusion

The Goertzel Browser indicator is a powerful tool for identifying and analyzing cyclical patterns in financial markets. Its ability to detect multiple cycles of varying frequencies and strengths make it a valuable addition to any trader's technical analysis toolkit. However, it is important to keep in mind that the Goertzel Browser indicator should be used in conjunction with other technical analysis tools and fundamental analysis to achieve the best results. With continued refinement and development, the Goertzel Browser indicator has the potential to become a highly effective tool for financial modeling, general trading, advanced trading, and high-frequency finance trading. Its accuracy and versatility make it a promising candidate for further research and development.

█ Footnotes

What is the Bartels Test for Cycle Significance?

The Bartels Cycle Significance Test is a statistical method that determines whether the peaks and troughs of a time series are statistically significant. The test is named after its inventor, George Bartels, who developed it in the mid-20th century.

The Bartels test is designed to analyze the cyclical components of a time series, which can help traders and analysts identify trends and cycles in financial markets. The test calculates a Bartels statistic, which measures the degree of non-randomness or autocorrelation in the time series.

The Bartels statistic is calculated by first splitting the time series into two halves and calculating the range of the peaks and troughs in each half. The test then compares these ranges using a t-test, which measures the significance of the difference between the two ranges.