[MAD] Custom Session VWAP BandsOverview

This indicator helps visualize the Volume Weighted Average Price (VWAP) and its associated standard deviation bands over specified time periods, providing traders with a clear understanding of price trends, volatility, and potential support/resistance levels.

Inputs

Deviation

StDev mult 1: Multiplier for the first standard deviation band (Default: 1.0)

StDev mult 2: Multiplier for the second standard deviation band (Default: 2.0)

StDev mult 3: Multiplier for the third standard deviation band (Default: 3.0)

StDev mult 4: Multiplier for the fourth standard deviation band (Default: 4.0)

Line width: Width of the lines for the bands (Default: 2)

Custom Vwap session reset settings

Many different options are considered when a session is going to be reset.

Plot and Fill Options

Enable Fills: Enable/disable filling between bands.

Plot +4: Enable/disable plotting the +4 standard deviation band.

Plot +3: Enable/disable plotting the +3 standard deviation band.

Plot +2: Enable/disable plotting the +2 standard deviation band.

Plot +1: Enable/disable plotting the +1 standard deviation band.

Plot VWAP: Enable/disable plotting the VWAP line.

Plot -1: Enable/disable plotting the -1 standard deviation band.

Plot -2: Enable/disable plotting the -2 standard deviation band.

Plot -3: Enable/disable plotting the -3 standard deviation band.

Plot -4: Enable/disable plotting the -4 standard deviation band.

How to Use the Indicator

Adding the Indicator

Add the indicator to your chart through your trading platform's indicator menu.

Configuring the VWAP Reset

Specify reset intervals based on time, days of the week, or specific dates.

Adjust the time zone if necessary.

Customizing Standard Deviation Bands

Set the multipliers for the standard deviation bands.

Choose line width for better visualization.

Enabling Plots and Fills

Select which bands to display.

Enable or disable fills between the bands.

Practical Application of VWAP Bands

Understanding VWAP

VWAP is a trading benchmark that calculates the average price a security has traded at throughout the day based on volume and price. It is primarily used for intraday trading but can also offer insights during end-of-day reviews.

Using VWAP for Trading

Intraday Trading

Entry and Exit Points: VWAP can help identify optimal buy and sell points. Buy when the price is above VWAP and sell when it's below.

Support and Resistance: VWAP often acts as a dynamic support/resistance level. Prices tend to revert to VWAP, making it a crucial level for intraday traders.

Trend Confirmation

Uptrends and Downtrends: In an uptrend, the price will generally stay above VWAP. Conversely, in a downtrend, it will stay below. Use this to confirm market direction.

Combining with Other Indicators

Moving Averages and Bollinger Bands: Combining VWAP with these indicators can provide a more robust trading signal, confirming trends and potential reversals.

Setting Stop-Loss and Profit Targets

Conservative Stop Orders: Place stop orders at recent lows for pullback trades.

Profit Targets: Use daily highs or Fibonacci extension levels to set profit targets.

Strategies for Using VWAP

Pullback Strategy

Buy during pullbacks to VWAP in an uptrend, and sell during rallies to VWAP in a downtrend.

Breakout Strategy

Look for breakouts above/below VWAP after the market open to capitalize on new trends.

Momentum Trading

Use VWAP to confirm the strength of a trend. Buy when the price is consistently above VWAP and sell when it's consistently below.

Institutional Strategies

Institutional traders use VWAP to execute large orders without causing significant market impact, ensuring trades are made around the average price.

By incorporating these strategies, traders can better understand market dynamics, make informed trading decisions, and manage their risk effectively.

Some setup possibilities

Средневзвешенная цена объёма (VWAP)

Price vs VWAP PerformancePrice vs VWAP Performance (PvVWAP)

This indicator visually displays the deviation between the current price and VWAP (Volume Weighted Average Price), helping you to determine the strength of a trend.

How it Works

VWAP Calculation: Calculates the Volume Weighted Average Price (VWAP) over a specified period.

Standard Deviation Calculation: Calculates the standard deviation of closing prices over the past 20 periods.

Deviation Calculation: Calculates the difference between the current price and VWAP, expressed as a multiple of the standard deviation.

Color Assignment: Changes the color of bars and background based on the magnitude of the deviation.

Green: Very strong uptrend

Light Green: Strong uptrend

Light Gray: No trend

Pinkish Red: Weak downtrend

Red: Very strong downtrend

How to Use

Trend Strength Assessment:

The greater the deviation of the price from VWAP, the stronger the trend is considered to be.

The color of the bars and background provides a visual indication of trend strength.

Entry/Exit Point Reference:

You can enter/exit by aiming for the movement of the price returning to VWAP after a large deviation from VWAP.

Notes

Parameter Settings:

The standard deviation period is 20 periods by default, but can be adjusted as needed.

Avoid Using Alone:

It is recommended to use this indicator in combination with other technical indicators.

F.B_Volume Weighted Average Price MTFThe F.B_Volume Weighted Average Price MTF (VWAP MTF) indicator calculates the volume-weighted average price of a security across different timeframes. The VWAP is a powerful indicator used by both institutional and retail traders to make better trading decisions.

Functionality:

Timeframe:

The indicator allows you to adjust the timeframe for the VWAP calculation via the settings. By default, the timeframe is set to weekly ("W").

Restart at new timeframe:

At each new period in the chosen timeframe, the VWAP calculations are reset, and a new VWAP is calculated.

VWAP Calculation:

The VWAP is calculated by the volume-weighted average of the typical prices (High, Low, and Close) of the security. This calculation takes into account the volume of each transaction to provide an accurate average price.

Visualization:

The VWAP is displayed as a line on the chart, and the color of the line changes depending on the price position relative to the VWAP:

Green: The current closing price is above the VWAP (bullish signal).

Red: The current closing price is below the VWAP (bearish signal).

Options:

Show barcolors:

This option allows you to display the colors of the candles based on their position relative to the VWAP (green for bullish, red for bearish).

Show previous VWAP close:

This option shows the closing value of the VWAP from the previous period to provide historical reference points.

Interpretation:

Bullish Signal:

If the current price is above the VWAP, this indicates that the market trend is upward, which could be considered a buying opportunity.

Bearish Signal:

If the current price is below the VWAP, this indicates that the market trend is downward, which could be considered a selling signal.

Consolidation VWAP's [QuantVue]Introducing the Consolidation VWAP's Indicator , a powerful tool designed to identify consolidation periods in stock advance and automatically anchor three distinct VWAPs to key points within the consolidation.

Consolidation Period Identification:

The indicator automatically detects periods of consolidation or areas on the chart where a stock's price moves sideways within a defined range. This period can be seen as the market taking a "breather" as it digests the previous gains. Consolidations are important because they often act as a base for the next move, either continuing the previous uptrend or reversing direction.

Consolidation requirements can be customized by the user to match your instrument and timeframe.

Maximum Consolidation Depth

Minimum Consolidation Length

Maximum Consolidation Length

Prior Uptrend Amount

Anchored VWAP, or Anchored Volume-Weighted Average Price, is a technical analysis tool used to determine the average price of a stock weighted by volume, starting from a specific point in time chosen by the analyst.

Unlike traditional VWAP, which starts at the beginning of the trading session, the anchored VWAP allows traders to select any point on the chart, such as a significant event, price low, high, or a breakout, to begin the calculation.

VWAP incorporates price and volume in a weighted average and can be used to identify areas of support and resistance on the chart.

VWAP Anchored to Consolidation High: This VWAP is anchored at the highest price point within the identified consolidation period. It helps traders understand the

average price paid by buyers who entered at the peak of the consolidation.

VWAP Anchored to Consolidation Low: This VWAP is anchored at the lowest price point within the consolidation. It provides insights into the average price paid by

buyers who entered at the lowest point of the consolidation.

VWAP Anchored to Highest Volume in the Consolidation: This VWAP is anchored at the price level with the highest trading volume during the consolidation. It reflects the average price at

which the most trading activity occurred, often indicating a key support or resistance level.

The indicator also allows the trader to see past consolidation areas and previous anchored VWAP's.

Give this indicator a BOOST and COMMENT your thoughts!

We hope you enjoy.

Cheers!

Vwap Z-Score with Signals [UAlgo]The "VWAP Z-Score with Signals " is a technical analysis tool designed to help traders identify potential buy and sell signals based on the Volume Weighted Average Price (VWAP) and its Z-Score. This indicator calculates the VWAP Z-Score to show how far the current price deviates from the VWAP in terms of standard deviations. It highlights overbought and oversold conditions with visual signals, aiding in the identification of potential market reversals. The tool is customizable, allowing users to adjust parameters for their specific trading needs.

🔶 Features

VWAP Z-Score Calculation: Measures the deviation of the current price from the VWAP using standard deviations.

Customizable Parameters: Allows users to set the length of the VWAP Z-Score calculation and define thresholds for overbought and oversold levels.

Reversal Signals: Provides visual signals when the Z-Score crosses the specified thresholds, indicating potential buy or sell opportunities.

🔶 Usage

Extreme Z-Score values (both positive and negative) highlight significant deviations from the VWAP, useful for identifying potential reversal points.

The indicator provides visual signals when the Z-Score crosses predefined thresholds:

A buy signal (🔼) appears when the Z-Score crosses above the lower threshold, suggesting the price may be oversold and a potential upward reversal.

A sell signal (🔽) appears when the Z-Score crosses below the upper threshold, suggesting the price may be overbought and a potential downward reversal.

These signals can help you identify potential entry and exit points in your trading strategy.

🔶 Disclaimer

The "VWAP Z-Score with Signals " indicator is designed for educational purposes and to assist traders in their technical analysis. It does not guarantee profitable trades and should not be considered as financial advice.

Users should conduct their own research and use this indicator in conjunction with other tools and strategies.

Trading involves significant risk, and it is possible to lose more than your initial investment.

VWAP Suite, Session Cloud RevOverview

The VWAP Suite with Standard Deviation Strategy is a comprehensive indicator designed to help traders make informed trading decisions based on the Volume Weighted Average Price (VWAP) and its associated standard deviation bands. This indicator provides multiple VWAP calculations for different timeframes (Session, Day, Week, Month) and incorporates standard deviation bands to identify potential trade entry and exit points.

Components

VWAP Calculation:

Session VWAP: VWAP calculated based on the current trading session.

Day VWAP: VWAP calculated for the daily timeframe.

Week VWAP: VWAP calculated for the weekly timeframe.

Month VWAP: VWAP calculated for the monthly timeframe.

Standard Deviation Bands:

The indicator includes three standard deviation bands (StDev 1, StDev 2, and StDev 3) around the VWAP. These bands help identify the dispersion of price from the VWAP, providing insight into potential overbought or oversold conditions.

Additional VWAP Lines:

VWAP 2: An additional VWAP line with a customizable timeframe (Day, Week, Month).

VWAP 3: Another VWAP line for further analysis with a customizable timeframe (Day, Week, Month).

Strategy Description

The primary strategy implemented in this indicator revolves around the second standard deviation band (StDev 2). The key aspects of this strategy include:

Entry Points:

Long Entry: Consider entering a long position when the price moves below the lower StDev 2 band and then starts to revert back towards the VWAP. This indicates a potential oversold condition.

Short Entry: Consider entering a short position when the price moves above the upper StDev 2 band and then starts to revert back towards the VWAP. This indicates a potential overbought condition.

Exit Points:

Long Exit: Exit the long position when the price moves back up to the VWAP or the upper StDev 1 band, indicating a normalization of the price.

Short Exit: Exit the short position when the price moves back down to the VWAP or the lower StDev 1 band, indicating a normalization of the price.

Risk Management:

Set stop-loss levels slightly beyond the StDev 3 bands to protect against significant adverse price movements.

Use trailing stops to lock in profits as the price moves favorably.

Customization

The VWAP Suite allows for extensive customization, enabling traders to adjust the following settings:

VWAP Mode: Select the timeframe for the primary VWAP calculation (Session, Day, Week, Month).

Line Widths and Colors: Customize the line widths and colors for VWAP and standard deviation bands.

Fill Opacity: Adjust the opacity of the fill between standard deviation bands for better visual clarity.

Additional VWAPs: Enable and customize additional VWAP lines (VWAP 2 and VWAP 3) for further analysis.

VWAP DivergenceThe "VWAP Divergence" indicator leverages the VWAP Rolling indicator available in TradingView's library to analyze price and volume dynamics. This custom indicator calculates a rolling VWAP (Volume Weighted Average Price) and compares it with a Simple Moving Average (SMA) over a specified historical period.

Advantages:

1. Accurate VWAP Calculation: The VWAP Rolling indicator computes a VWAP that dynamically adjusts based on recent price and volume data. VWAP is a vital metric used by traders to understand the average price at which a security has traded, factoring in volume.

2. SMA Comparison: By contrasting the rolling VWAP from the VWAP Rolling indicator with an SMA of the same length, the indicator highlights potential divergences. This comparison can reveal shifts in market sentiment.

3. Divergence Identification: The primary purpose of this indicator is to detect divergences between the rolling VWAP from VWAP Rolling and the SMA. Divergence occurs when the rolling VWAP significantly differs from the SMA, indicating potential changes in market dynamics.

Interpretation:

1. Positive Oscillator Values: A positive oscillator (difference between rolling VWAP and SMA) suggests that the rolling VWAP, derived from the VWAP Rolling indicator, is above the SMA. This could indicate strong buying interest or accumulation.

2. Negative Oscillator Values: Conversely, a negative oscillator value indicates that the rolling VWAP is below the SMA. This might signal selling pressure or distribution.

3. Divergence Signals: Significant divergences between the rolling VWAP (from VWAP Rolling) and SMA can indicate shifts in market sentiment. For instance, a rising rolling VWAP diverging upwards from the SMA might suggest increasing bullish sentiment.

4. Confirmation with Price Movements: Traders often use these divergences alongside price action to confirm potential trend reversals or continuations.

Implementation:

1. Length Parameter: Adjust the Length input to modify the lookback period for computing both the rolling VWAP from VWAP Rolling and the SMA. A longer period provides a broader view of market sentiment, while a shorter period is more sensitive to recent price movements.

2. Visualization: The indicator plots the VWAP SMA Oscillator, which visually represents the difference (oscillator) between the rolling VWAP (from VWAP Rolling) and SMA over time.

3. Zero Line: The zero line (gray line) serves as a reference point. Oscillator values crossing above or below this line can be interpreted as bullish or bearish signals, respectively.

4. Contextual Analysis: Interpret signals from this indicator in conjunction with broader market conditions and other technical indicators to make informed trading decisions.

This indicator, utilizing the VWAP Rolling component, is valuable for traders seeking insights into the relationship between volume-weighted price levels and traditional moving averages, aiding in the identification of potential trading opportunities based on market dynamics.

VWAP RollingThis indicator, referred to here as "VWAP Rolling," is a technical tool designed to provide insight into the average price at which an asset has traded over a specified rolling period, along with bands that can indicate potential overbought or oversold conditions based on standard deviations from this rolling VWAP.

Purpose and Utility:

The indicator's primary purpose is to track the volume-weighted average price (VWAP) over a specified period, typically 20 bars in this script. The VWAP Rolling is particularly useful in assessing the average price level at which a security has been traded over the recent history, incorporating both price and volume data. This can help traders understand the prevailing market price in relation to trading volume.

Advantages:

1. Dynamic Average: Unlike fixed VWAP indicators that calculate over a specific session, the rolling VWAP adapts to recent price and volume changes, offering a more responsive and dynamic average.

2. Volume Sensitivity: By weighting prices by volume, the rolling VWAP gives more importance to periods with higher trading activity, providing a clearer picture of where significant trading has occurred.

3. Standard Deviation Bands: The inclusion of standard deviation bands (configurable as 1x and 2x deviations in this script) around the rolling VWAP adds a layer of analytical depth. These bands can serve as potential areas of support and resistance, highlighting deviations from the mean price.

Singularization and Interpretation:

The VWAP Rolling indicator is singularized by its ability to adapt to changing market conditions, offering a dynamic representation of the average price level influenced by volume. To use and interpret this indicator effectively:

• Rolling VWAP Line: The main line represents the rolling VWAP. When this line trends upwards, it suggests that recent trading has been occurring at higher prices weighted by volume, indicating potential bullish sentiment. Conversely, a downtrend in the rolling VWAP may indicate bearish sentiment.

• Standard Deviation Bands: The upper and lower bands (configurable as 1x and 2x standard deviations from the rolling VWAP) are used to identify potential overbought or oversold conditions. A price crossing above the upper band may indicate overbought conditions, signaling a potential reversal or correction downwards. Conversely, a price crossing below the lower band may suggest oversold conditions, potentially signaling a bounce or reversal upwards.

• Band Interaction: Watch for interactions between price and these bands. Repeated touches or breaches of the bands can provide clues about the strength of the prevailing trend or potential reversals.

Interpretative Insights:

• Trend Confirmation: The direction of the rolling VWAP can confirm or contradict the prevailing price trend. If the price is above the rolling VWAP and the VWAP is rising, it suggests a strong bullish sentiment. Conversely, a falling rolling VWAP with prices below might indicate a bearish trend.

• ean Reversion Signals: Extreme moves beyond the standard deviation bands may signal potential mean reversion. Traders can look for price to revert back towards the rolling VWAP after such deviations.

In summary, the VWAP Rolling indicator offers traders a flexible tool to gauge average price levels and potential deviations, incorporating both price and volume dynamics. Its adaptability and standard deviation bands provide valuable insights into market sentiment and potential trading opportunities.

Triple Anchored Volume Weighted Average Price [JustinPrime]This indicator provides three separate Volume Weighted Average Price (VWAP) calculations, each anchored from different key points on the chart:

High Anchored VWAP: Resets from the highest price reached since the start date.

Low Anchored VWAP: Resets from the lowest price since the start date.

Start Date VWAP: Calculated from the trading data beginning at the user-defined start date.

Features:

Selectable Timeframe: Choose from timeframes like 1 minute, 5 minutes, 15 minutes, 1 hour, daily, and weekly.

Custom Start Date: Set a specific start date for the VWAP calculations.

Source Data: Uses high, low, and close prices (HLC3) for calculations.

How to Use:

Adjust the start date to focus on significant market periods or events.

Differentiate each VWAP with unique colors for clarity.

Relative Average Extrapolation [ChartPrime]Relative Average Extrapolation (ChartPrime) is a new take on session averages, like the famous vwap . This indicator leverages patterns in the market by leveraging average-at-time to get a footprint of the average market conditions for the current time. This allows for a great estimate of market conditions throughout the day allowing for predictive forecasting. If we know what the market conditions are at a given time of day we can use this information to make assumptions about future market conditions. This is what allows us to estimate an entire session with fair accuracy. This indicator works on any intra-day time frame and will not work on time frames less than a minute, or time frames that are a day or greater in length. A unique aspect of this indicator is that it allows for analysis of pre and post market sessions independently from regular hours. This results in a cleaner and more usable vwap for each individual session. One drawback of this is that the indicator utilizes an average for the length of a session. Because of this, some after hour sessions will only have a partial estimation. The average and deviation bands will work past the point where it has been extrapolated to in this instance however. On low time frames due to the limited number of data points, the indicator can appear noisy.

Generally crypto doesn't have a consistent footprint making this indicator less suitable in crypto markets. Because of this we have implemented other weighting schemes to allow for more flexibility in the number of use cases for this indicator. Besides volume weighting we have also included time, volatility, and linear (none) weighting. Using any one of these weighting schemes will transform the vwap into a wma, volatility adjusted ma, or a simple moving average. All of the style are still session period and will become longer as the session progresses.

Relative Average Extrapolation (ChartPrime) works by storing data for each time step throughout the day by utilizing a custom indexing system. It takes the a key , ie hour/minute, and transforms it into an array index to stor the current data point in its unique array. From there we can take the current time of day and advance it by one step to retrieve the data point for the next bar index. This allows us to utilize the footprint the extrapolate into the future. We use the relative rate of change for the average, the relative deviation, and relative price position to extrapolate from the current point to the end of the session. This process is fast and effective and possibly easier to use than the built in map feature.

If you have used vwap before you should be familiar with the general settings for this indicator. We have made a point to make it as intuitive for anyone who is already used to using the standard vwap. You can pick the source for the average and adjust/enable the deviation bands multipliers in the settings group. The average period is what determines the number of days to use for the average-at-time. When it is set to 0 it will use all available data. Under "Extrapolation" you will find the settings for the estimation. "Direction Sensitivity" adjusts how sensitive the indicator is to the direction of the vwap. A higher number will allow it to change directions faster, where a lower number will make it more stable throughout the session. Under the "Style" section you will find all of the color and style adjustments to customize the appearance of this indicator.

Relative Average Extrapolation (ChartPrime) is an advanced and customizable session average indicator with the ability to estimate the direction and volatility of intra-day sessions. We hope you will find this script fascinating and useful in your trading and decision making. With its unique take on session weighting and forecasting, we believe it will be a secret weapon for traders for years to come.

Enjoy

VWAP SuiteThis indicator automates the plotting of various timeframe based VWAP Values. This utilizes a different calculation method for the standard deviations bands compared to the native Tradingview AVWAP. While the Tradingview AVWAP indicator calculates the standard devation based on the VWAP variance, this indicator calculates the std dev based on the price sum variance (i.e. the variance of the hlc3, ohlc4, etc. values).

Current timeframes include:

- Daily VWAP with three user configurable standard deviation bands

- Multi-Day VWAP that allows you to plot 2-day to 5-day VWAP

- Weekly VWAP with three user configurable standard deviation bands

- Monthly VWAP with three user configurable standard deviation bands

Some unique aspects of this indicator is that it allows the user to calculate VWAP for only a specific session range if you are only interested in the VWAP when specific participants are active in the market. For example, the default session range only calculates VWAP for the New York RTH session (0930-1600).

If the user wants to compare how the session range chosen varies from the VWAP calculation with ETH you can select the 'Include Extended Trading Hours' check box which will ignore the session range input variable and simply calculate what is exactly on the chart without filtering.

You can also toggle whether the VWAP values show up in the price scale, status line, or both which can limit the amount of clutter that shows up on the chart based upon the user's preferences.

VWAP SpiderThe VWAP Spider indicator enhances the conventional Volume Weighted Average Price (VWAP) analysis by anchoring it to the first candle and incorporating an extensive series of standard deviation (SD) lines, extending up to +8 SDs with additional half-step increments. This configuration provides a more suitable set of lines for identifying support and resistance, distinguishing it from existing VWAP and SD indicators. Its design, featuring color gradients for fills and distinct labels for each line, aims to improve the utility and user experience.

Optimal Timeframes:

It is recommended for use on weekly or monthly resolutions to ensure all price and volume history is included.

Distinctive Features:

The indicator includes a more extensive array of SD lines than typically found in VWAP indicators, enhancing the depth of market analysis.

The visual presentation is optimized with color gradients and clear labeling, facilitating ease of use and integration into trading strategies.

Practical Use of the VWAP Spider:

SD Lines as Support and Resistance : Observe the interactions between the price and the SD lines closely. These can serve as dynamic support and resistance indicators, influencing trading decisions.

Analyzing Historical Price Action : Investigate how the price has historically interacted with the SD lines. Identify which lines have frequently acted as support and resistance in the past, as they will often continue to be revisited.

Strategic Application : Leverage insights from the interactions between price and SD lines to fine-tune entry and exit points. For example, a rebound from an SD line may suggest a strong entry point, while breaching an SD line could indicate a potential exit.

This indicator is freely available and open-source on TradingView for all. It is designed to help traders enhance their market analysis and strategic decision-making.

MultiWAPThe VWAP tracks the average price, giving weight to each candle based upon its' relative volume.

In other words, high-volume candles move the VWAP faster than low-volume candles.

On a good day, market maker:

-Buys the dip

-Pumps past resistance, causing bullish FOMO

-Sells into the bullish FOMO, causing bearish FOMO

-Buys the dip (rinse and repeat)

By default, MultiWAP begins at the first visible bar.

Range low/high - tracks the most recent high/low

Upper VWAP - tracks retail's average buy price (MM is selling)

Lower VWAP - tracks MM's average buy price (MM is buying)

If price closes below the lower VWAP or the range low, the lower VWAP and range low are reset.

If price closes above the upper VWAP or the range high, the upper VWAP and range high are reset.

Resets are indicated by the dots. Resetting either VWAP moves it close to last price, making it easy to breach again.

A down-trend that lasts many bars will produce a string of green dots. When the accumulation phase ends, price pulls away from the lower VWAP, so it stops resetting. The ABSENCE of green dots tells you that we're in the markup phase/up-trend.

An up-trend that lasts many bars will produce a string of red dots. When the distribution phase ends, price pulls away from the upper VWAP, so it stops resetting. The ABSENCE of red dots tells you that we're in the markdown phase/down-trend.

By default, the net result is two VWAP's that automatically anchor themselves to the most recent, significant, and visible, high and low.

Usage:

For any timeframe, I recommend starting zoomed way out. Find the last green dot and drop an "Anchored VWAP" there. Now, zoom in until that candle is no longer visible. Find the last green dot and drop an anchored VWAP there. Continue doing so until you notice the lower VWAP getting reset to basically the same place.

This works the same, in reverse, during down-trends.

Multi-Day Rolling VWAP [Intraday]Ideas from Brian Shannon's book "Anchored VWAP"

The Multi-Day Rolling VWAP indicator for intraday timeframes allows you to track the Volume Weighted Average Price (VWAP) over multiple days, specifically for 1-day, 2-day, 3-day, 4-day, and 5-day periods. This indicator beyond the standard daily VWAP provides a broader perspective on price trends and market sentiment.

Features:

- Multi-day VWAPs: Analyze VWAP over several days to observe longer-term price movements.

- Customizable display: Choose which VWAP periods to display on the chart

- Colorize: Choose different colors for each VWAP to easily distinguish between periods.

- Adjustable settings: Change the line thickness and select the price source for VWAP calculations.

- Works with Replay Mode

- Works in any intraday timeframe on any asset with volume and price

Benefits:

- Trend identification: Compare current prices with multi-day rolling VWAPs to spot trends.

- Spot reversals: Look for potential price reversals or support when prices cross VWAP lines.

Rolling Strategic AVWAPThe Rolling Strategic AVWAP gives you the ability to have the standard AVWAP indicators applied across all charts in all timeframes. There is no manual intervention necessary to keep all the standard VWAPs up to date. This indicator is written so that all weekends and trading holidays are taken into account so you never have any gaps or days where the indicator isn't working.

Standard rolling AVWAP indicators:

Daily

2-day

3-day

Week-to-Date

Month-to-Date

Year-to-Date

Additionally I have supplied several custom labeled AVWAP indicators that the user can adjust the date themselves

Custom Fixed AVWAP indicators:

Prior Week-to-Date

Prior Month-to-Date

Prior Year-to-Date

Fed rate decision

Inflation report

GDP report

Jobs report

3 more labeled Custom1-3

These custom locations will allow the user to anchor the VWAP to meaningful dates and times in the market. Often there are large moves due to global macro events that can give the trader an edge by referencing the VWAP to the date and time.

Labels and Display

There are options to turn on and off any of the AVWAPs, as well as turning on and off the display labels below the candles.

VWAP 8EMA Crossover Scalping IndicatorWhy?

Everybody, especially in Indian context, from 9:15 AM to 3:30 PM, wants to trade in BankNifty.

And even 15m is Too Big timeframe for The Great Indian Options buyers. Everyone knows how potentially BankNifty (& FinNifty on Tuesday and Sensex on Friday) can show dance within 15m.

So there always been an overarching longing among traders to have something in shorter timeframes. And this 5m timeframe, looks like a universally (sic) accepted Standard Timeframe for Indian Options traders.

So here is this.

What?

The time we are publishing this public indicator Indian market (Nifty) is in ATH at ~22200.

In any such super trending market it's always good to wait for a dip and then in suitable time, enter the trade in the direction of the larger trend. The reversal trading systems, in such a situation, proves to be ineffective.

Of course there are time when market is sideways and keeps on oscillating between +/2 standard deviation of the 20 SMA. In such a situation the reversal play works perfectly. But not so in such a trending market.

So the question comes up - after a dip what's the right point to enter.

Hence comes the importance of such a crossover based trading system.

In this indicator, it's a well-known technique (nothing originally from ours, it's taken from social media, exact one we forgot) to find out the 8EMA and VWAP crossover.

So we learned from social media, practice in our daily trading a bit, actuate it and now publishing it.

A few salient points

It does not make sense to jump into the trade just on the crossover (or crossunder).

So we added some more sugar to it, e.g. we check the color the candle. Also the next candle if crosses and closes above (or below) the breakout candle's high/low.

The polarity (color) of both the alert (breakout/breakdown) and confirmation candle to be same (green for crossover, red from crossunder).

Of course, it does provider BUY and SELL alerts separately.

These all we have found out doing backtesting and forward testing with 1/2 lots and saw this sort of approaches works.

Hence all of these are added to this script.

Nomenclature

Here green line is the 8EMA and the red line is the VWAP.

Also there is a black dotted line. That's 50 EMA. It's to show you the trend.

The recent trade is shown in the top right of the chart as green (for buy) or red (for sell) with SL and 1:1 target.

How to trade using this system?

This is roughly we have found the best possible use of this indicator.

Lets explain with a bullish BUY positive crossover (means 8EMA is crossing over the daily VWAP)

Keep timeframe as 5m

Check the direction/slope of the black dotted line (50 EMA). If it's upwards, only take bullish positions.

Open the chart which has the VWAP. (e.g. FinNifty spot or MidcapNifty spot does not have vwap). So in those cases Future is the way to go.

Wait for a breakout crossover and let the indicator gives a green, triangular UP arrow.

Draw a horizontal line to the close of that candle for next few (say 6 candles i.e. 30m) candles.

Wait for the price first to retest the 8EMA or even better the VWAP (or near to the 8EMA, VWAP)

Let the price moves and closes above the horizontal line drawn in the 4th step.

Take a bullish trade, keeping VWAP as the SL and 1:1 as the target.

Additionally, Options buyer can consult ADX also to see if the ADX is more than 25 and moving up for the bullish trade. (This has to be added seperately in the chart, it's not a part of the indicator).

Mention

The concept we have taken from some social media. Forget exactly where we heard this first time. We just coded it with some additional steps.

Statutory Disclaimer

There is no silver bullet / holy grail in trading. Nothing works 100% time. One has to be careful about the loss (s)he can bear in case of the trade goes against.

We, as the author of this script, is not responsible for any trading or position decision one is taken based on the outcome of this.

It is our sole discretion to change, add, delete the portion or withdraw the whole script without any prior notice or intimation.

In Indian Context: We are not SEBI registered.

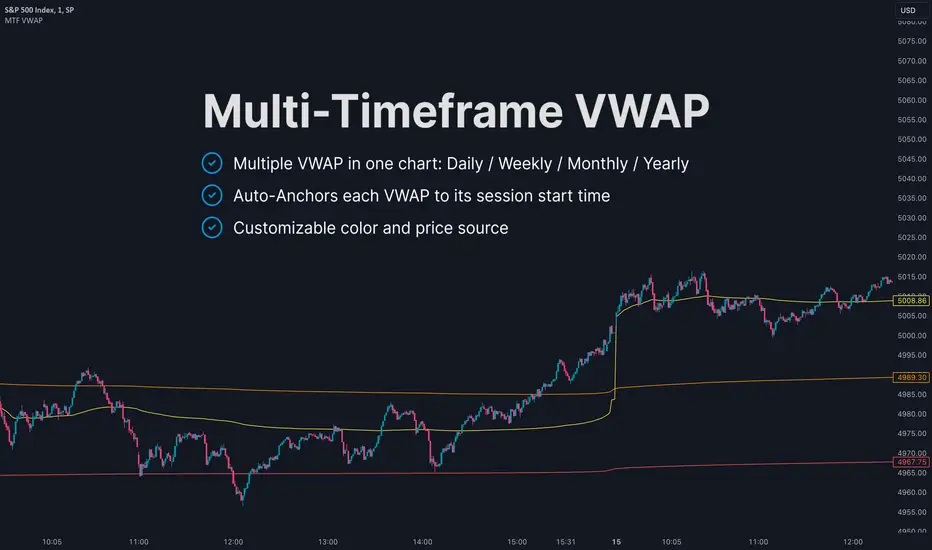

MTF VWAPThis indicator is an enhanced version of the traditional VWAP, providing traders with multiple timeframe views, automatic session anchoring, and customization options for optimized technical analysis.

Key Features:

1. Multiple Timeframes, One View : Visualize Daily, Weekly, Monthly, and Yearly VWAP calculations simultaneously on a single chart.

2. Automatic Anchoring : The indicator intelligently auto-anchors each VWAP calculation to the start of its respective session. This ensures accurate readings and streamlines your analysis by eliminating the need for manual adjustments.

3. Customizability : Tailor the appearance of the indicator with fully customizable colors and the ability to select your preferred price source (e.g., high, low, close, hlc3, hlcc4, or a custom one).

VWAP Bands @shrilssVWAP Bands Integrates VWAP with standard deviation bands to provide traders with insights into potential support and resistance levels based on volume dynamics. VWAP is a key metric used by institutional traders to gauge the average price a security has traded at throughout the trading day, taking into account both price and volume.

This script calculates the VWAP for each trading session and overlays it on the price chart as a solid line. Additionally, it plots multiple standard deviation bands around the VWAP to indicate potential areas of price extension or contraction. These bands are derived from multiplying the standard deviation of price by predetermined factors, offering traders a visual representation of potential price ranges.

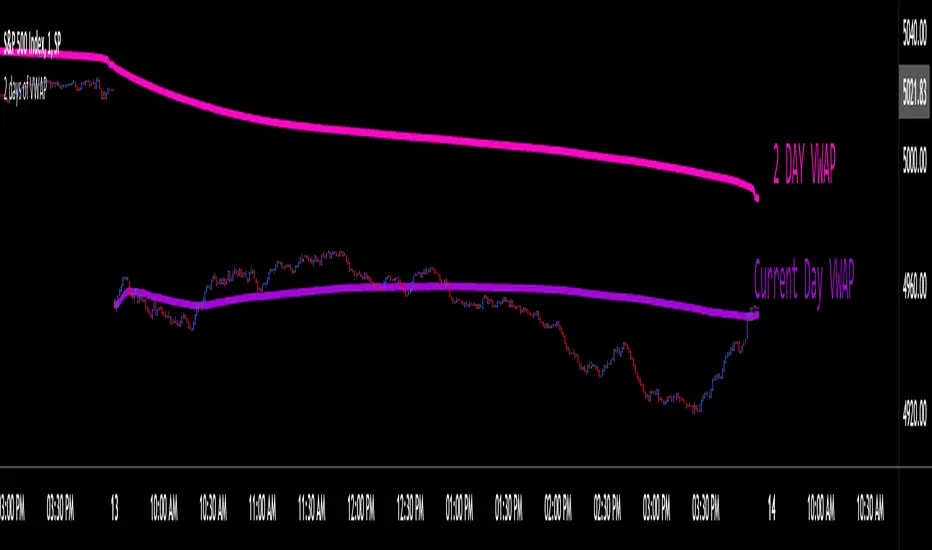

VWAP_CURRENT_YESTERDAY

The "VWAP CURRENT YESTERDAY" is a Pine Script designed for TradingView that automatically calculates and plots the Volume Weighted Average Price (VWAP) for the current day, the previous day.

Dynamic VWAP Calculation:

Automatically generates VWAPs for 1 day and 2 day.

User-Friendly Customization:

Through input options, users can easily toggle the visibility of each VWAP line, adjust colors, and set line thicknesses to their preference.

Configuration Options

1. VWAP Source:

Choose the price source for VWAP calculation. Default is the typical price (`hlc3` - the average of high, low, and close).

2. VWAP Lines:

Toggle the display for Today's VWAP, Yesterday's VWAP, and the VWAP from 2 days ago.

Customize colors and thickness for each VWAP line for clear visual distinction.

3. VWAP Labels:

Configure label sizes and positions to ensure that VWAP values are easily identifiable on the chart.

How It Works:

- The script calculates the sum of price multiplied by volume (`vwapsum`) and the sum of volumes (`volumesum`) for the specified periods.

- It utilizes an impulse function to reset calculations at the start of each new session or custom date, ensuring accurate and relevant VWAP values .

- Final VWAP values are plotted as lines on the chart, with optional labels for current and 2-day VWAPs for quick reference.

Customization Guide:

- To activate or deactivate specific VWAP lines, navigate to the 'VWAP Lines' section in the script's settings and toggle the respective options.

- Adjust the color and thickness of each VWAP line under the same section to match your charting preferences.

- Label settings, including size and offset, can be customized in the 'VWAP Labels' section, allowing for personalized label positioning and readability.

Multi VWAP from Gaps [MW]Multi VWAP from Gaps

Introduction

The Multi VWAP from Gaps tool extends the concept of using the Anchored Volume Weighted Average Price, popularized by its founder, Brian Shannon, founder of AlphaTrends. It creates automatic AVWAPS for anchor points originating at the biggest gaps of the week, month, quarter and year. Currently, most standard VWAP tools allow users to place custom anchored VWAPs, but the routine of doing this for every equity being watched can become cumbersome. This tool makes that process multi-times easier. Considering that large gaps can represent a shift in market structure, this tool provides unique and immediate insight into how past daily price gaps can and have affected price action.

Settings

LABEL SETTINGS

Show Biggest Gap of Week | Month | Quarter : Toggle labels that identify the location of the biggest gaps for the selected time period.

Show Big Labels : Toggle labels from showing the date and gap size to just showing a single letter (W/M/Q/Y) designating the time period that the gap is from.

Hide All Labels : Turn labels off and on.

MAX VWAP LINES

Max Weekly | Monthly | Quarterly | Yearly Lines : How many VWAP lines, starting from today, should be shown for the specified time period. Max: 5

SHOW VWAP LINES

Show Weekly | Monthly | Quarterly | Yearly Lines : This feature allows you to remove lines for the specified time period.

Calculations

This indicator does not provide buy or sell signals. It is simply the VWAP calculated starting from an “anchor point”, or start time. It is calculated by the summation of Price x Volume / Volume for the period starting at the anchor point.

How to Interpret

According to Brian Shannon, VWAP is an objective measure of what the average trader has paid for a particular equity over a given period, and is the value that large institutional investors frequently use as a trade signal. Therefore, by definition, when the price is above an AVWAP, buyers are in control for that period of time. Likewise, if the price is below the AVWAP, sellers are in control for that period of time.

VWAPs that coincide with important events, such as FOMC meetings, CPI reports, earnings reports, have added significance. In many cases, these events can cause gaps to happen in day-to-day price movement, and can affect market structure going forward.

Practically speaking, price action can tend to change direction when a significant VWAP is hit, voiding buy and sell signals. Like moving averages, this indicator can show, in real-time, how a buy or sell signal should be interpreted. A significant AVWAP line is a point of interest, and can serve as strong support or resistance, because large institutions may be using those values for entries or exits. For a great analysis of how to use AVWAP, visit the AlphaTrends channel on Youtube here or you can buy Brian Shannon’s “Anchored VWAP” book on Amazon.

Other Usage Notes and Limitations

It's important for traders to be aware of the limitations of any indicator and to use them as part of a broader, well-rounded trading strategy that includes risk management, fundamental analysis, and other tools that can help with reducing false signals, determining trend direction, and providing additional confirmation for a trade decision. Diversifying strategies and not relying solely on one type of indicator or analysis can help mitigate some of these risks.

Additionally, in order to build the VWAP calculations, past data is needed that may not be available on shorter timeframes. The workaround is that for some longer-term VWAP lines on shorter timeframes, you may see less than the total of lines that you selected in settings. This is particularly the case with quarterly VWAP lines on the 5 minute timeframe for some equities.

Acknowledgements

This script uses the MarketHolidays library by @Protervus. Also, for debugging, the JavaScript-style Debug Console by @algotraderdev was invaluable. Special thanks to @antsmuzic for helping review and debug the script. And, of course, without Brian Shannon's books, videos, and interviews, this indicator would would not have happened.

Multi-Time AVWAP_BEARConcept

Collaboration Highlight:

This was a collaboration with @Chart_School and @KioseffTrading Thank you to both, along with Ricardo Santos for his awesome library we used.

Overview

See how you view different time frame charts with one indicator and little to no adjustment.

Innovation:

The concept of using Anchored VWAP (AVWAP) with time events is a powerful technique in trading and technical analysis. Anchored VWAP differs from the traditional Volume Weighted Average Price (VWAP) by allowing traders to select a specific starting point or "anchor," from which the VWAP calculation begins. This approach is particularly useful for assessing price movements in relation to significant market events or specific periods of interest.

Utility and Flexibility:

Explaining the flexibility in turning on and off different time slices without much adjustment showcases a user-friendly design.

Key Uses and Benefits

Comparative Performance:

Anchoring the VWAP at the start of different time frames (e.g., weekly, monthly, quarterly) enables traders to compare the current price performance against previous periods. This comparison can highlight trends or shifts in trading momentum relative to past activity.

Support and Resistance Levels:

AVWAP lines can act as dynamic support and resistance levels. When anchored to significant time events, these levels gain additional relevance as they reflect the market's valuation of an asset since a notable point in time. Traders often watch for price interactions with these levels to make informed trading decisions.

Risk Management:

Anchored VWAP can serve as a benchmark for setting stop-loss orders or profit targets. By considering the price's relation to the AVWAP of a specific period or after a key event, traders can define exit points that are aligned with market-generated information.

Trend Confirmation: The direction and stability of the price relative to an anchored VWAP can indicate the strength of a trend. If the price consistently remains above an AVWAP anchored at a bullish event (or below for a bearish event), it may confirm the trend's continuation.

Further Reading

Educational Resource:

Becuase we are using Volume with a relation to price AVWAP is very powerful to show data that cannot be eye balled on its own. Brian Shannon's book "Maximum Trading Gains With Anchored VWAP - The Perfect Combination of Price, Time & Volume", is an excellent guide to best practices on how to use AVWAP to your advatage while trading. His book goes into depth about the best way to use this indicator to its fullest potencial.

Tips for Using This Indicator

Weekly / Monthly / Quarterly Settings:

All the settings for the lower timeframe charts are similar. Here is an example of seeing a Weekly AVWAP for 6 weeks, showing:

1. The start of the 6-week AVWAP is using a High Low Close source for the first candle of the 6 weeks.

2. The lines are colored "Red" for the AVWAPs.

3. The line thickness is "1".

Yearly Settings

Simlair to the other settings with the Yearly we give you a couple more options along with 3 years to toggle on and off. The idea was to allow the user to see which AVWAP most effected by price and quickly toggle them on and off to unclutter their chart.

Watch for how and if the labels over lap and choose the one you feel is most in play. In Shannon's Book he talks about "Hand off's" and "Pinches". These concepts are easy to spot with being able to see all the Major Time Events, then simply toggle off the one you dont need.

A great benefit to how we coded this script you can buzz through a watch list without having to re-adjust the Anchor points. This will save you time if following a basket of symbols and show coorlations in the overall market.

Secret Feature

When looking at these becuase the user doesn't need to hand plot the anchor points and we are fouced on major time slices, I encourge you to use the Trading View "Bar Replay" Feature. You think that you are missing a high or low AVWAP but what is happening is the indicator is re-plotting a level that is super hard to see, then you will see the hand-offs like Shannon discusses in his book. This blew me away while we were discussing it post development.

Conclusion

There are so many uses of how to use VWAP and therories on its best practice. We are only using "TIME EVENTS". For more ways to use AVWAP, I would encourge you to also handplot them with Trading View's new "Anchored VWAP", as seen in the standard toolbar.

Using your ideas along with this indicator i think its a powerful combination.

Also Check Out: allanster's - Anchored VWAP Pinch & Handoff, Intervals, and Signals

He has a great AVWAP script that incorporates many AVWAP ideas.

VWAP LEVELS [PRO]32 VWAP levels with labels and a table to help you identify quickly where current price is in relation to your favorite VWAP pivot levels. To help reduce cognitive load, 4 colors are used to show you where price is in relation to a VWAP level as well as the strength of that respective level. Ultimately, VWAP can be an invaluable source of support and resistance; in other words you'll often see price bounce off of a level (whether price is increasing or decreasing) once or multiple times and that could be an indication of a price's direction. Another way that you could utilize this indicator is to use it in confluence with other popular signals, such as an EMA crossover. Many traders will wait till a bar's close on the 5m or 10m time frame above a VWAP level (developing 1D VWAP would be a popular choice) before making a decision on a potential trade especially if price is rising above the 1D VWAP *and* there's been a recent 100 EMA cross UP of the 200 EMA. These are 2 bullish signals that you could look for before possibly entering in to a trade.

I've made this indicator extremely customizable:

⚡Each VWAP level has 2 labels: 1 "at level" and 1 "at right", each label and price can be disabled

⚡Each VWAP label has its own input for label padding. The "at right" label padding input allows you to zoom in and out of a chart without the labels moving along their respective axis. However, the "at level" label padding input doesn't work the same way once you move the label out of the "0" input. The label will move slightly when you zoom in and out

⚡Both "current" and "previous" VWAP levels have their own plot style that can be changed from circles, crosses and lines

⚡Significant figures input allows you to round a price up or down

⚡A price line that allows you to identify where price is in relation to a VWAP level

⚡A table that's color coded the same way as the labels. The labels and table cells change to 1 of 4 colors when "OC Check Mode" is enabled. This theory examines if the VWAP from the Open is above or below the VWAP from Close and if price is above or below normal VWAP (HLC3). This way we have 4 states:

Red = Strong Downtrend

Light Red = Weak Downtrend

Light = Weak Uptrend

Green = Strong Uptrend

Something to keep in mind: At the start of a new year, week or month, some levels will converge and they'll eventually diverge slowly or quickly depending on the level and/or time frame. You could add a few labels "at level" to show which levels are converging at the time. Since we're at the beginning of a new year, you'll see current month, 2 month, 3 month etc converge in to one level.

🙏Thanks to (c)MartinWeb for the inspiration behind this indicator.

🙏Thanks to (c)SimpleCryptoLife for the libraries and code to help create the labels.

Rolling VWAP [QuantraSystems]Rolling VWAP

Introduction

The Rolling VWAP (R͜͡oll-VWAP) indicator modernizes the traditional VWAP by recalculating continuously on a rolling window, making it adept at pinpointing market trends and breakout points.

Its dual functionality includes both the dynamic rolling VWAP and a customizable anchored VWAP, enhanced by color-coded visual cues, thereby offering traders valuable flexibility and insight for their market analysis.

Legend

In the Image you can see the BTCUSD 1D Chart with the R͜͡oll-VWAP overlay.

You can see the individually activatable Standard Deviation (SD) Bands and the main VWAP Line.

It also features a Trend Signal which is deactivated by default and can be enabled if required.

Furthermore you can find the coloring of the VWAP line to represent the Trend.

In this case the trend itself is defined as:

Close being greater than the VWAP line -> Uptrend

Close below the VWAP line -> Downtrend

Notes

The R͜͡oll-VWAP can be used in a variety of ways.

Volatility adjusted expected range

This aims to identify in which range the asset is likely to move - according to the historical values the SD Bands are calculated and thus their according probabilities displayed.

Trend analysis

Trending above or below the VWAP shows up or down trends accordingly.

S/R Levels

Based on the probability distribution the 2. SD often works as a Resistance level and either mid line or 1. SD lines can act as S/R levels

Unsustainable levels

Based on the probability distributions a SD level of beyond 2.5, especially 3 and higher is hit very seldom and highly unsustainable.

This can either mean a mean reversion state or a momentum slowdown is necessary to get back to a sustainable level.

Please note that we always advise to find more confluence by additional indicators.

Traders are encouraged to test and determine the most suitable settings for their specific trading strategies and timeframes.

Methodology

The R͜͡oll-VWAP is based on the inbuilt TV VWAP.

It expands upon the limitations of having an anchored timeframe and thus a limited data set that is being reset constantly.

Instead we have integrated a rolling nature that continuously calculates the VWAP over a customizable lookback.

To also keep the base utility it is possible to use the anchored timeframes as well.

Furthermore the visualization has been improved and we added the coloring of the main VWAP line according to the Trend as stated above.

The applicable Trend signals are also part of that.

The parameter settings and also the visualizations allow for ample customizations by the trader.

For questions or recommendations, please feel free to seek contact in the comments.