Liquidation Levels with Liquidity Sweeps/Breakouts [AlgoAlpha]🌊📈 Dive into the depths of market liquidity with "Liquidation Levels with Liquidity Sweeps/Breakouts" - your ultimate tool for navigating the turbulent waters of trading! 🧹💹 Crafted by the wizards at AlgoAlpha, this Pine Script™ masterpiece illuminates the unseen liquidity levels and sweeps, guiding you through the financial seas with insight. 🚀🔍

Key Features:

🕒 Timeframe Flexibility: Customize your analysis with a TimeFrame Multiplier, allowing the indicator to operate on higher timeframes for broader market insight.

💥 Dynamic Volume Threshold: Set your sensitivity to breakouts with the High Volume Threshold, ensuring you catch significant market movements while avoiding fakeouts.

👀 Visibility Controls: Toggle the display of swept liquidity and highlight liquidity breakouts with customizable background colors for clear, actionable insights.

🎨 Custom Appearance: Personalize your chart with bullish, bearish, and breakout colors to match your trading style.

How to Use the Liquidity Levels with Liquidation Sweeps Indicator:

Maximize your trading efficiency with the Liquidity Levels with Liquidation Sweeps Indicator by following these simple steps! 🚀🌟

⚙️ Customize Settings: Access the indicator settings to personalize the TimeFrame Multiplier, High Volume Threshold, and Relative Volume Period. Tailor these settings to match your trading strategy and chart preferences.

👁️ Analyze Liquidity Levels: Monitor the chart for liquidity levels and sweeps. Bullish sweeps are marked with green labels, bearish sweeps with red, and breakouts highlighted by the chart background.

🔔 Set Alerts: Enable alert conditions for liquidity breakouts and sweeps within the indicator's settings. This feature allows you to receive real-time notifications, helping you to act promptly on trading opportunities.

How It Works:

The heart of this indicator lies in its ability to track and highlight liquidity levels derived from swing pivots, and sweeps across multiple timeframes. By calculating relative volume against a user-defined threshold, it identifies strong volume movements indicative of liquidity breakouts, this helps filter out fake-outs. When a liquidity level is breached but not completely mitigated, it's either marked as a bullish or bearish sweep, which come with the option to show an estimate of the number of liquidations during the sweep.

if peakform and peakprinted != 1

aR.push(line.new(bar_index-mult, h.get(1), bar_index+1, h.get(1), color = red))

aRv.push(h.get(1))

peakprinted := 1

if valleyform and valleyprinted != 1

aS.push(line.new(bar_index-mult, l.get(1), bar_index+1, l.get(1), color = green))

aSv.push(l.get(1))

valleyprinted := 1

Объем

Deep Volume [ChartPrime]Deep Volume is an indicator designed to give you high fidelity volume information. It does this by utilizing real time data provided by Tradingview to generate a wide range of metrics. We have included a convenient column chart to visualize the polarity of the volume, and a table to see the real time data. This works by utilizing pine script's varip feature to get information within candles. This is convenient as it allows users to get lower time frame information without the use of ltf functions. The result is seconds level data with out the need to be on a lower time frame chart. As a result, as you increase the time frame of the chart the updates will become slower. This is because Tradingview doesn't update the chart information as frequently on higher time frames as there isn't as much of a need.

This indicator works on real time data so to compensate for this we generate a simulated history based on candle structure. This helps in estimating the state of the moving average before the real time data starts. As a result the estimated history isn't as accurate and should be treated as such. That being said it is nice to have an estimation when the indicator is first loaded onto the chart.

Finally we have included a cumulative volume comparison that shows you how much volume there is compared to the average cumulative volume for the day. This metric utilizes a gradient to help you interpret the information at a glance. Low daily volume is represented with grays by default, while normal volume and greater is represented with a green color by default.

The table is partitioned into two sections; tick data, and average data. On the left you will see color coded information based on the direction of the move. On the left, the information is color coded based on the average movement direction. You can control how much information is displayed in the table within the indicators settings. This is defaulted to 20 but it can be as long or short as you like. Every new candle open the far left of the table you will see a 🗘 symbol and at the start of a new session you will see a 🗓 symbol.

The included metrics are as follows:

Time: This displays the time of the real time data update.

Time Delta: This displays the elapsed time between updates.

Order Size: This is the volume times the price change between updates.

Volume: This is the volume change for the update.

Price Change: This is the change in price since the last update.

Price: This is the price of the asset at the time of the update.

Speed of Tape: This is the average time delta. Use this to see how quickly the market is moving.

Average Order Size: This is the average order size.

Average Volume: This is the average volume

Volume Ratio: This the the ratio of bullish to bearish volume as expressed by a percent. 100% is all bullish within the window and -100% is all bearish within the window.

Average Price Change: This is the average price change within the window.

Sensitivity: This is a volatility metric designed to show you the price change per 1 volume unit.

Relative Sensitivity: This is a volatility metric designed to show you the average price change per average volume.

Enjoy

Multi-Day Rolling VWAP [Intraday]Ideas from Brian Shannon's book "Anchored VWAP"

The Multi-Day Rolling VWAP indicator for intraday timeframes allows you to track the Volume Weighted Average Price (VWAP) over multiple days, specifically for 1-day, 2-day, 3-day, 4-day, and 5-day periods. This indicator beyond the standard daily VWAP provides a broader perspective on price trends and market sentiment.

Features:

- Multi-day VWAPs: Analyze VWAP over several days to observe longer-term price movements.

- Customizable display: Choose which VWAP periods to display on the chart

- Colorize: Choose different colors for each VWAP to easily distinguish between periods.

- Adjustable settings: Change the line thickness and select the price source for VWAP calculations.

- Works with Replay Mode

- Works in any intraday timeframe on any asset with volume and price

Benefits:

- Trend identification: Compare current prices with multi-day rolling VWAPs to spot trends.

- Spot reversals: Look for potential price reversals or support when prices cross VWAP lines.

Up Down Volume Ratio by 3iauThis script considers the total volume within a user specified time frame, and whether price closed higher or lower at the end of each period within that time frame.

EXAMPLE:

* If the time period of interest is 50-periods, the script considers the volume within each of those 50 periods beginning with the most recent closed period.

* SumUpVol = the sum of all volume occurring within only those periods where price closed higher than that of the previous period.

* SumDnVol = the sum of all volume occurring within only those periods where price closed lower than that of the previous period.

* Difference = the difference between SumUpVol and SumDnVol = SumUpVol - SumDnVol

* Total = the sum of SumUpVol and SumDnVol = SumUpVol + SumDnVol

* The plot will present the change in Difference divided by Total = Difference/Total = (SumUpVol - SumDnVol)/(SumUpVol + SumDnVol) occurring within those 50 periods. What will be plotted is the moving average of this value. The user can specify the moving average type and the number of period for which the average is calculated.

* The plot needs to be fitted into a range, for example, +/- 50 (default) or +/-100, by multiplying the result of Difference/Total by a user specified constant. The constant will contain the majority (not all) of the values within +/- the specified value.

* Range = the user specified constant. If Range = 50, the majority of values plotted will be fall within the range +/- 50.

* Therefore, what is plotted is the moving average of Range * Difference / Total.

* When the value = 0, accumulation = distribution over the user specified 50-periods time frame.

* When the value is positive, accumulation > distribution over the user specified 50-periods time frame.

* When the value is negative, distribution > accumulation over the user specified 50-periods time frame.

This plot allows one to see possible accumulation and distribution occurring within a particular stock. The slope of this plot must be considered, and not any single value. The selected constant (“Range” in the example above) does not have an effect on the slope of the plot.

Three values may be plotted at once, for comparison of accumulation or distribution occurring over different time frames. For example, compare Difference / Total calculated over a 50-periods timeframe with 10-periods timeframe, both time frames beginning with the most recent closed period.

In addition to the above, J. Welles Wilder’s Relative Strength Index (RSI) can be plotted over the Difference / Total.

NOTE: this script is not the same as the more commonly used Up/Down Volume Ratio defined as SumUpVol / SumDnVol over a 50-periods time frame, where SumUpVol = the sum of all volume occurring within only those periods where price closed higher than that of the previous period, and SumDnVol = the sum of all volume occurring within only those periods where price closed lower than that of the previous period.

Compare...

Up Down Volume Ratio = SumUpVol / SumDnVol

Up Down Volume Ratio by 3iau = the moving average of Range * (SumUpVol - SumDnVol) / (SumUpVol + SumDnVol)

Kzx | RSI + Div + MACDComponents Description:

Relative Strength Index (RSI):

Purpose: Measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset.

Implementation: The script allows users to set the length of the RSI calculation and defines overbought and oversold levels, which can be visually represented on the chart. Additional features include options to fill and/or color the background of the chart when overbought or oversold levels are reached.

Divergence (Div):

Purpose: Identifies instances where the price of an asset is moving in the opposite direction of a momentum indicator, such as the RSI in this script. Divergences can signal potential trend reversals.

Implementation: The script provides options for users to define the conditions under which divergences are identified, including the source of price tops/bottoms, detection limits, and the maximum lookback period for divergence analysis. It visually highlights these divergences on the chart.

Moving Average Convergence Divergence (MACD):

Purpose: Tracks the relationship between two moving averages of a security's price. The MACD is used to identify trend direction, momentum, and potential reversal points through crossovers.

Implementation: The script calculates the MACD line and its signal line. It plots buy or sell markers based on crossovers between these two lines, indicating potential entry or exit points.

Script Category:

Category: Technical Analysis / Indicators and Strategies

Subcategory: Oscillators (for RSI and MACD) and Trend Analysis (for Divergence)

Usage:

The script is designed for traders and analysts who rely on technical analysis to make informed decisions in the financial markets. By integrating RSI, divergence detection, and MACD analysis into a single script, users can gain a more nuanced understanding of market conditions, potentially improving their trading strategies.

Customization and Visualization:

Users can customize various parameters, including lengths for RSI and MACD, overbought/oversold levels, divergence detection criteria, and visual aspects like colors and marker sizes.

The script provides visual cues directly on the price chart, making it easy to spot potential buy/sell signals, overbought/oversold conditions, and divergences without the need to switch between different indicators.

Cumulative Volume Delta (CVD)█ OVERVIEW

Cumulative Volume Delta (CVD) is a volume-based trading indicator that provides a visual representation of market buying and selling pressure by calculating the difference in traded volumes between the two sides. It uses intrabar information to obtain more precise volume delta information than methods using only the chart's timeframe.

Volume delta is the net difference between Buy Volume and Sell Volume. Positive volume delta indicates that buy volume is more than sell volume, and opposite. So Cumulative Volume Delta (CVD) is a running total/cumulation of volume delta values, where positive VD gets added to the sum and negative VD gets subtracted from the sum.

I found simple and fast solution how to calculate CVD, so made plain and concise code, here is CVD function :

cvd(_c, _o, _v) =>

var tcvd = 0.0, delta = 0.0

posV = 0.0, negV = 0.0

totUV = 0.0, totDV = 0.0

switch

_c > _o => posV += _v

_c < _o => negV -= _v

_c > nz(_c ) => posV += _v

_c < nz(_c ) => negV -= _v

nz(posV ) > 0 => posV += _v

nz(negV ) < 0 => negV -= _v

totUV += posV

totDV += negV

delta := totUV + totDV

cvd = tcvd + delta

tcvd += delta

cvd

where _c, _o, _v are close, open and volume of intrabar much lower timeframe.

Indicator uses intrabar information to obtain more precise volume delta information than methods using only the chart's timeframe.

Intrabar precision calculation depends on the chart's timeframe:

CVD is good to use together with open interest, volume and price change.

For example if CVD is rising and price makes good move up in short period and volume is rising and open interest makes good move up in short period and before was flat market it is show big chance to pump.

Footprint liteFootprint Lite enables you to monitor volume distribution for the current ticker, offering resolutions as 1 second, segmented by specified price levels with visual representations. Additionally, you have the flexibility to customize the displayed Imbalance price level and the number of consecutive Imbalance level lines.

Here are the input options:

Group Display:

This section allows you to adjust how Footprints are displayed.

"Count show bars": Directly adjusts the display to show the last 'n' bars.

"Display all available bars": Shows all available bars.

Group Row size:

Adjusts the parameters for generating Footprints based on price step size.

"Ticks Per Row": Directly sets the price step, calculated by multiplying the entered value by syminfo.mintick.

"Auto": Enables automatic mode for selecting the "Ticks Per Row" value.

"Max row": Relevant for auto mode, it sets the acceptable number of rows within a bar. The automatic "Ticks Per Row" calculation is based on the first available bar and applied to subsequent bars.

Group Imbalance:

Customizes the display of price levels represented by Imbalance and emphasizes consecutive lines.

"Imbalance Percent": A coefficient expressed as a percentage to determine the Imbalance of price levels, comparing the buy price diagonally to the previous sell price.

"Stacked levels": Sets the minimum number of consecutive Imbalance levels required to draw extended lines.

Alerts:

You can set alerts for various events:

"New imbalance line sell": Alerts on the appearance of a new imbalance line for selling.

"New imbalance line buy": Alerts on the appearance of a new imbalance line for buying.

"Stop past imbalance line sell": Alerts when the previous imbalance line for selling stops, indicating it has reached the range from low to high of the current bar.

"Stop past imbalance line buy": Alerts when the previous imbalance line for buying stops, indicating it is within the range from low to high of the current bar.

"New imbalance buy": Alerts on the appearance of a new or change in the current imbalance level for buying.

"New imbalance sell": Alerts on the appearance of a new or change in the current imbalance level for selling.

Forex Multi-Factor IndicatorMoving Averages (MA):

Two moving averages are plotted on the chart: a fast MA (blue line) and a slow MA (red line).

The fast MA is calculated using a shorter period (10 periods by default), while the slow MA is calculated using a longer period (30 periods by default).

Moving averages help identify trends by smoothing out price fluctuations. When the fast MA crosses above the slow MA, it suggests a bullish trend, and when the fast MA crosses below the slow MA, it suggests a bearish trend.

Relative Strength Index (RSI):

The RSI indicator (orange line) is plotted on a separate axis.

RSI measures the speed and change of price movements and oscillates between 0 and 100.

RSI values above 70 are considered overbought, indicating a potential reversal to the downside, while RSI values below 30 are considered oversold, indicating a potential reversal to the upside.

Volume Moving Average (Volume MA):

The volume moving average (purple line) is plotted on the same axis as the volume.

The volume moving average is calculated over a specified period (20 periods by default).

Volume analysis provides insights into the strength of price movements. When the volume increases along with price movements, it suggests strong conviction from traders.

Buy and Sell Signals:

Buy signals (green triangle) are generated when all of the following conditions are met:

The fast MA crosses above the slow MA (indicating a bullish trend).

The RSI is below the oversold level (indicating potential upward momentum).

The current price is above the fast MA, and the volume is higher than the volume MA (indicating positive volume trend).

Sell signals (red triangle) are generated when all of the following conditions are met:

The fast MA crosses below the slow MA (indicating a bearish trend).

The RSI is above the overbought level (indicating potential downward momentum).

The current price is below the fast MA, and the volume is lower than the volume MA (indicating negative volume trend).

Overall, this multi-factor indicator combines moving averages, RSI, and volume analysis to identify potential buying and selling opportunities in the Forex market. Traders can use the signals generated by this indicator as part of their trading strategy, but it's important to consider other factors such as risk management and market conditions before making trading decisions

Rolling Strategic AVWAPThe Rolling Strategic AVWAP gives you the ability to have the standard AVWAP indicators applied across all charts in all timeframes. There is no manual intervention necessary to keep all the standard VWAPs up to date. This indicator is written so that all weekends and trading holidays are taken into account so you never have any gaps or days where the indicator isn't working.

Standard rolling AVWAP indicators:

Daily

2-day

3-day

Week-to-Date

Month-to-Date

Year-to-Date

Additionally I have supplied several custom labeled AVWAP indicators that the user can adjust the date themselves

Custom Fixed AVWAP indicators:

Prior Week-to-Date

Prior Month-to-Date

Prior Year-to-Date

Fed rate decision

Inflation report

GDP report

Jobs report

3 more labeled Custom1-3

These custom locations will allow the user to anchor the VWAP to meaningful dates and times in the market. Often there are large moves due to global macro events that can give the trader an edge by referencing the VWAP to the date and time.

Labels and Display

There are options to turn on and off any of the AVWAPs, as well as turning on and off the display labels below the candles.

VEMA_LTFVEMA indicator is based on lower time frame volume data and it has 3 lines.

20, 50, 100 moving averages of the close price in each candle with the highest volume.

Effectively working fine and hence sharing.

Will Add more information with examples in next update

Open Liquidity Heatmap [BigBeluga]Open Liquidity Heatmap is an indicator designed to display accumulated resting liquidity on the chart.

Unlike any other liquidity heatmap, this aims to accumulate liquidity at specific levels that build up over time, showing larger areas of liquidity.

🔶 FEATURES

The indicator includes the following settings:

Lookback : Used to determine the range calculation of the heatmap.

Leverage : Leverage of the liquidation (Counted as % in price, Example: 4.5 will return a distance from price of 4.5%, indicating any possible resting liquidity in this range).

Levels : Amount of levels to display (Each level is counted as liquidity resting on the chart; fewer levels will return a bigger area of liquidity sitting on the chart).

Mode : Apply a color gradient from the minimum liquidation to the maximum liquidity level. Set the maximum color gradient value (Counted as volume).

Offset : Automatically determine the offset range of the Volume Profiles. Manual offset of the Volume Profiles.

🔶 CALCULATION

for i = 0 to step - 1

float plotter = na

switch i

0 =>

plotter := hs

=>

plotter := hs - diff * ( i )

cls.hm.gnL(plotter)

cls.vp.put(plotter, 0)

We calculate levels like a normal volume profile with steps, from the highest point within the lookback to the lowest one. Each level will contain the corresponding amount of volume that the candle has closed in that range.

As we can see in the image above, we add liquidity each time the distance in % from price is between two levels.

Unlike many liquidity indicators that provide a single candle liquidity heatmap, this aims to add up liquidity (volume) in already present levels.

This can be extremely useful to see which levels are likely to be more liquid and tend to get a bigger reaction to the price.

Imagine it like a range of levels that each time price revisits that area, a new position area is added; we add volume in that area each time price visits that zone. Liquidity builds up in those zones, causing a bigger reaction to the price once the price visits it.

This indicator is not the same as a single candle heatmap like many others. What is a single candle heatmap?

A single candle heatmap is when a level is created on every new candle, coloring the level based on the total volume of it.

This indicator, on the contrary, aims to provide a more specific use by adding up liquidity each time price visits it.

🔶 BASIC DEMOSTRATION

This is a basic demonstration of how we can spot high liquidity points overall using confluence:

We see the POC of the liquidation in a low volume area of the normal volume profile adding up as confluence.

Resistance from the POC Volume Profile suggesting price will go lower.

Major long open liquidity down.

As we can see, price takes out all the long liquidity and right after pumping, indicating that all the major liquidity got taken out.

Some key note to take is that a POC in the liquidation heatmap in a low volume area of the normal Volume Profile add confluence of a possible big reaction in that zone.

In the forex market, we suggest to use a low distance from price (Leverage) while in a crypto market you can use the one that fit the best the current timeframe.

🔶 CONCLUSION

This indicator aims to show open resting liquidity that had built up over time, showing the most amount of liquidation in specific areas in an aggregated way unlike many liquidation heatmap indicators that show single-level liquidation.

🔶 RELATED SCRIPT

RVOL++Overview

RVOL++ is a valuable tool for intraday traders to gauge market participation and anticipate the pace of the market. By understanding the RVOL levels, traders can adjust their strategies and expectations to align with the current market conditions. RVOL is a simple mathematical formula that compares the current volume to a prior lookback period, such as the previous 5 days or previous 10 days. This indicator helps traders understand the level of interest or participation in the market, which in turn can indicate the speed or pace of the market.

How to calculate RVOL at Time

Check if the current time is within the specified time period (e.g., 9:30 AM to 5:00 PM EST).

If it is, calculate the current cumulative volume for that period.

Find the average cumulative volume for the same period over the past X days (where X is the lookback period).

Calculate the RVOL at Time as:

RVOL at Time =(Current Cumulative Volume/Average Cumulative Volume)×100

For more info about calculating RVOL at time please refer to the Tradingview article.

www.tradingview.com

Key Features of RVOL++

Two Session and Daily Modes: In Two Session mode, it calculates RVOL for two distinct trading sessions, while in Daily mode, it calculates RVOL for the entire trading day. Two Session mode helps for instruments like futures, forex, crypto that trade 23+ hours. If you are using an instrument such as a stock like AAPL, if you don't have pre-market/extended hours enabled you will want to use "Daily Mode".

Session Time Settings: The indicator allows users to define the trading session times in Eastern Standard Time (EST) for more accurate RVOL calculations.

Customizable Lookback Period: Users can set the number of days for the lookback period, allowing for flexibility in calculating the average volume at time (RVOL).

Color-Coded RVOL Histogram: The indicator displays a color-coded histogram to visualize RVOL levels. Different colors represent different RVOL ranges, making it easy to identify low, neutral, and high RVOL periods.

RVOL Ranges**: The indicator defines RVOL ranges as follows:

40 - 80: Low RVOL (Red/Yellow)

80 - 120: Neutral RVOL (Blue/Cyan)

120+: High RVOL (Green-Lime)

Low RVOL Environment

Expect slow market movement with limited opportunities.

Focus on A+ setups and be selective.

Use tighter stops, size down, and adjust trading goals.

Neutral RVOL Environment

Expect a more normalized trading pace with frequent rotations.

Lean on structure and incorporate other trading tools.

Use normal sizing and stop management.

High RVOL Environment

Expect the best opportunities for range expansion and rotations.

Be more relaxed about overtrading but stay focused on structure.

Start with smaller initial size and build up to a full position.

VWAP 8EMA Crossover Scalping IndicatorWhy?

Everybody, especially in Indian context, from 9:15 AM to 3:30 PM, wants to trade in BankNifty.

And even 15m is Too Big timeframe for The Great Indian Options buyers. Everyone knows how potentially BankNifty (& FinNifty on Tuesday and Sensex on Friday) can show dance within 15m.

So there always been an overarching longing among traders to have something in shorter timeframes. And this 5m timeframe, looks like a universally (sic) accepted Standard Timeframe for Indian Options traders.

So here is this.

What?

The time we are publishing this public indicator Indian market (Nifty) is in ATH at ~22200.

In any such super trending market it's always good to wait for a dip and then in suitable time, enter the trade in the direction of the larger trend. The reversal trading systems, in such a situation, proves to be ineffective.

Of course there are time when market is sideways and keeps on oscillating between +/2 standard deviation of the 20 SMA. In such a situation the reversal play works perfectly. But not so in such a trending market.

So the question comes up - after a dip what's the right point to enter.

Hence comes the importance of such a crossover based trading system.

In this indicator, it's a well-known technique (nothing originally from ours, it's taken from social media, exact one we forgot) to find out the 8EMA and VWAP crossover.

So we learned from social media, practice in our daily trading a bit, actuate it and now publishing it.

A few salient points

It does not make sense to jump into the trade just on the crossover (or crossunder).

So we added some more sugar to it, e.g. we check the color the candle. Also the next candle if crosses and closes above (or below) the breakout candle's high/low.

The polarity (color) of both the alert (breakout/breakdown) and confirmation candle to be same (green for crossover, red from crossunder).

Of course, it does provider BUY and SELL alerts separately.

These all we have found out doing backtesting and forward testing with 1/2 lots and saw this sort of approaches works.

Hence all of these are added to this script.

Nomenclature

Here green line is the 8EMA and the red line is the VWAP.

Also there is a black dotted line. That's 50 EMA. It's to show you the trend.

The recent trade is shown in the top right of the chart as green (for buy) or red (for sell) with SL and 1:1 target.

How to trade using this system?

This is roughly we have found the best possible use of this indicator.

Lets explain with a bullish BUY positive crossover (means 8EMA is crossing over the daily VWAP)

Keep timeframe as 5m

Check the direction/slope of the black dotted line (50 EMA). If it's upwards, only take bullish positions.

Open the chart which has the VWAP. (e.g. FinNifty spot or MidcapNifty spot does not have vwap). So in those cases Future is the way to go.

Wait for a breakout crossover and let the indicator gives a green, triangular UP arrow.

Draw a horizontal line to the close of that candle for next few (say 6 candles i.e. 30m) candles.

Wait for the price first to retest the 8EMA or even better the VWAP (or near to the 8EMA, VWAP)

Let the price moves and closes above the horizontal line drawn in the 4th step.

Take a bullish trade, keeping VWAP as the SL and 1:1 as the target.

Additionally, Options buyer can consult ADX also to see if the ADX is more than 25 and moving up for the bullish trade. (This has to be added seperately in the chart, it's not a part of the indicator).

Mention

The concept we have taken from some social media. Forget exactly where we heard this first time. We just coded it with some additional steps.

Statutory Disclaimer

There is no silver bullet / holy grail in trading. Nothing works 100% time. One has to be careful about the loss (s)he can bear in case of the trade goes against.

We, as the author of this script, is not responsible for any trading or position decision one is taken based on the outcome of this.

It is our sole discretion to change, add, delete the portion or withdraw the whole script without any prior notice or intimation.

In Indian Context: We are not SEBI registered.

Fusion Traders - RSI Overbought/Oversold + Divergence IndicatorFusion Traders - RSI Overbought/Oversold + Divergence Indicator - new version

This indicator has lots of various add ons.

RSI overbought / oversold with changeable inputs

Divergence indicator

DESCRIPTION:

This script combines the Relative Strength Index ( RSI ), Moving Average and Divergence indicator to make a better decision when to enter or exit a trade.

- The Moving Average line (MA) has been made hidden by default but enhanced with an RSIMA cloud.

- When the RSI is above the selected MA it turns into green and when the RSI is below the select MA it turns into red.

- When the RSI is moving into the Overbought or Oversold area, some highlighted areas will appear.

- When some divergences or hidden divergences are detected an extra indication will be highlighted.

- When the divergence appear in the Overbought or Oversold area the more weight it give to make a decision.

- The same colour pallet has been used as the default candlestick colours so it looks familiar.

HOW TO USE:

The prerequisite is that we have some knowledge about the Elliot Wave Theory, the Fibonacci Retracement and the Fibonacci Extension tools.

We are hoping you like this indicator and added to your favourite indicators. If you have any question then comment below, and I'll do my best to help.

FEATURES:

• You can show/hide the RSI .

• You can show/hide the MA.

• You can show/hide the lRSIMA cloud.

• You can show/hide the Stoch RSI cloud.

• You can show/hide and adjust the Overbought and Oversold zones.

• You can show/hide and adjust the Overbought Extended and Oversold Extended zones.

• You can show/hide the Overbought and Oversold highlighted zones.

HOW TO GET ACCESS TO THE SCRIPT:

• Favorite the script and add it to your chart.

Herrick Payoff Index @shrilssThis indicator combines elements of price action, volume, and open interest to provide insights into market strength and potential trend reversals. This script calculates the Herrick Payoff Index (HPI) based on a modified formula that incorporates volume and open interest adjustments.

The HPI is derived from comparing the current day's mean price to the previous day's mean price, factoring in volume and open interest changes. By analyzing these factors, the indicator aims to gauge the effectiveness of market participants' positions.

Key Features:

- HPI Calculation: The HPI value is calculated using the formula: ((M - My) * C * V) * (1 + |OI - OI | / min(OI, OI )), where M represents the mean price for the current day, My represents the mean price for the previous day, C is a constant (set to 1), V is the volume, and OI is the open interest. This adjusted calculation accounts for changes in volume and open interest, providing a more nuanced view of market dynamics.

- Moving Averages: The script also includes two Exponential Moving Averages (EMAs) of the HPI values, allowing traders to identify trends and potential reversal points. Users can customize the length of these moving averages to suit their trading strategies.

- Visual Signals: The indicator visually represents the HPI values and their relationship to the moving averages. When the HPI value is above the shorter-term EMA, it suggests bullish momentum, while values below indicate bearish sentiment.

CVI Tops/Bottoms Detector [AstroHub]

Welcome to the realm of precision trading with the CVI Tops/Bottoms Detector by AstroHub. Crafted with a keen eye on market dynamics, this indicator stands as a reliable tool for identifying potential trend reversals and market turning points.

Key Features of the Indicator:

The CVI Tops/Bottoms Detector, developed by AstroHub, is a powerful tool designed to detect tops and bottoms in the market. Its calculations are based on sound mathematical principles, ensuring accurate identification of bullish and bearish signals. 🔍

Calculation Period and Thresholds:

Calculation Period: Adjust the "Period" parameter to tailor the indicator to different timeframes.

Thresholds: Set the "Bullish Threshold" and "Bearish Threshold" to determine the sensitivity of the indicator to potential market shifts.

CVI Calculation:

The indicator calculates the Current Volume Index (CVI) by considering the difference between the closing price and the smoothed average, normalized by volatility. This innovative approach provides a clear view of market sentiment.

Visual Signals and Alerts:

Bullish and Bearish Signals: Clearly defined signals are represented by diamond shapes on the chart, accompanied by color-coded indications.

Gradient Colors: Gradient colors add a visual dimension to the signals, making it easier to interpret market trends.

Connecting Lines: Lines connect signals, offering a visual guide for understanding the flow of the market.

Symbol Transparency:

Customize the transparency of the underlying symbol to ensure clarity in signal visualization.

User-Friendly Customization:

Flexible Coloring: Tailor the colors of bullish and bearish signals to match your preferences.

Line Colors: Adjust line colors to enhance visibility.

Alerts: Receive timely alerts when a new bullish or bearish signal is detected.

Usage Example:

Open the indicator settings.

Adjust the "Period" to match your desired timeframe.

Fine-tune the "Bullish" and "Bearish Thresholds" based on your risk tolerance.

Experiment with customizing colors and transparency to suit your visual preferences.

Alerts for Proactive Trading:

Activate alerts to stay informed about potential bullish or bearish market opportunities. 🚨

By integrating the CVI Tops/Bottoms Detector into your trading toolkit, you gain a powerful ally in navigating the dynamic landscape of financial markets. 🌐💹

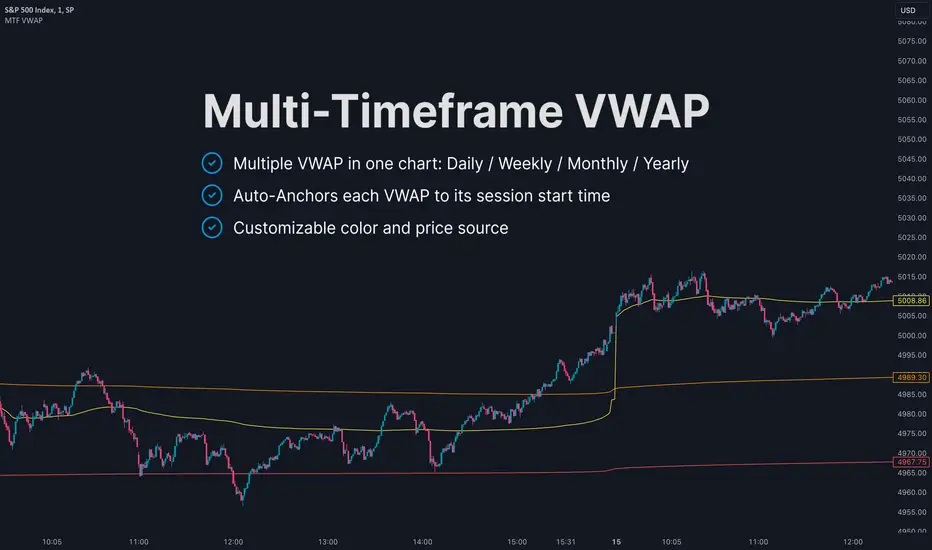

MTF VWAPThis indicator is an enhanced version of the traditional VWAP, providing traders with multiple timeframe views, automatic session anchoring, and customization options for optimized technical analysis.

Key Features:

1. Multiple Timeframes, One View : Visualize Daily, Weekly, Monthly, and Yearly VWAP calculations simultaneously on a single chart.

2. Automatic Anchoring : The indicator intelligently auto-anchors each VWAP calculation to the start of its respective session. This ensures accurate readings and streamlines your analysis by eliminating the need for manual adjustments.

3. Customizability : Tailor the appearance of the indicator with fully customizable colors and the ability to select your preferred price source (e.g., high, low, close, hlc3, hlcc4, or a custom one).

VSA Volume Spread AnalysisVolume Spread Analysis with Trend Direction is an indicator designed to Identify trend based volume spread.

Volume

Spread

Trend

This is a very simple yet powerful to identify Trend and corresponding volume Breakout. Unlike other Volume Indicators this indicator detects Breakout along with trend direction. One can detect the Early breakout in volume using this indicator. The Buy or Sell Signal is based on zero crossing of the Histogram.

Trend direction is confirmed using the MA of the Histogram which is similar to the Volume MA on volume indicator. One can enter a trade using the indicator when Trend direction and histogram are in same direction. Entry is done when ever histogram crosses the Trend MA line.

Fake entries can be eliminated by changing the indicator to higher Timeframe.

Spread is determined using the difference in open and close of the candle

Volume change is determined using the ratio of change of volume to previous volume

EMA 10 is used to determine the Spread and multiplied by volume change so the

PRICE(ema10), Volume, Spread(close-open) are merged to one indicator.

Direction changes when ever difference of VSA is positive or negative.

VWAP Bands @shrilssVWAP Bands Integrates VWAP with standard deviation bands to provide traders with insights into potential support and resistance levels based on volume dynamics. VWAP is a key metric used by institutional traders to gauge the average price a security has traded at throughout the trading day, taking into account both price and volume.

This script calculates the VWAP for each trading session and overlays it on the price chart as a solid line. Additionally, it plots multiple standard deviation bands around the VWAP to indicate potential areas of price extension or contraction. These bands are derived from multiplying the standard deviation of price by predetermined factors, offering traders a visual representation of potential price ranges.

Timely Opening Range Breakout Strategy [TORB] (Zeiierman)█ Overview

The Timely Opening Range Breakout (TORB) indicator builds upon the classic Open Range Breakout (ORB) concept. The ORB strategy is a popular trading setup used to identify trades around the opening range of an asset. It's based on the idea that the first few minutes (15-60 minutes) of trading often set the tone for the rest of the day, with breakouts above or below the opening range signifying potential trends.

TORB refines the concept by stating that a trade is only valid if there is sufficient market activity. This means a breakout beyond the upper or lower range is only of interest during the most active trading hours, as defined by PMMV (Per-Minute Mean Volume)

█ How It Works

ORB

The indicator works by first defining a session's opening range based on user-specified settings, including the session's start and end times and the applicable time zone. During this session, it calculates the high and low price points, which form the basis for identifying potential breakout levels.

PMMV

PMMV (Per-Minute Mean Volume) provides a snapshot of the market's activity level at each minute of the trading day. PMMV is calculated by averaging the trading volume in a one-minute interval over a specified number of trading days. This script uses the average volume over the last N periods to determine the PMMV value. This average volume provides a smoother representation of volume activity compared to using a single volume value. It considers the volume over a broader timeframe, filtering out short-term fluctuations and potentially offering a more reliable indicator of underlying market activity.

TORB

TORB works by integrating the Opening Range Breakout (ORB) highs and lows with the Per-Minute Mean Volume (PMMV) metric to assess the validity of breakouts. The objective is to identify breakouts from the opening high and low levels during periods of heightened market activity, as indicated by PMMV.

█ How to Use

To effectively utilize the Timely Opening Range Breakout (TORB) strategy, follow these steps:

Identify Active Hours: Employ PMMV to pinpoint periods of peak activity within the trading day.

Apply Basic ORB Rules: If the price surpasses the upper range (resistance), buy; if it breaches the lower range (support), sell.

Breakouts

The TORB strategy identifies breakout signals when the price moves beyond the established range, supported by volume exceeding a set threshold. This technique aims to eliminate false signals, focusing on price movements during high market activity.

█ Settings

Session

Trading Session: Customize the trading session's start and end times.

Volume

Volume analysis is integral to the TORB strategy, as it uses volume data to confirm the strength and validity of breakout signals.

Period: Sets the number of periods (or bars) to calculate the average volume, which is then used to assess market activity level.

Sensitivity and Significance: Adjusts how responsive the volume analysis is to changes in trading volume. By adjusting the sensitivity, traders can decide how much emphasis to place on volume spikes, potentially reducing false breakouts and focusing on those supported by significant trading activity.

Breakout Threshold

This setting establishes a criterion to identify when the price movement is significant enough.

Threshold: Traders set a threshold level to identify high market activity. If the PMMV is greater than or equal to this threshold, it indicates significant market activity.

Setting the correct threshold is key to balancing sensitivity and specificity. Too low of a threshold may lead to many false positives, while too high of a threshold might filter out potentially profitable breakouts. This setting helps in pinpointing when market activity indicates a strong move, thereby aligning trade entries with moments of heightened market momentum.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

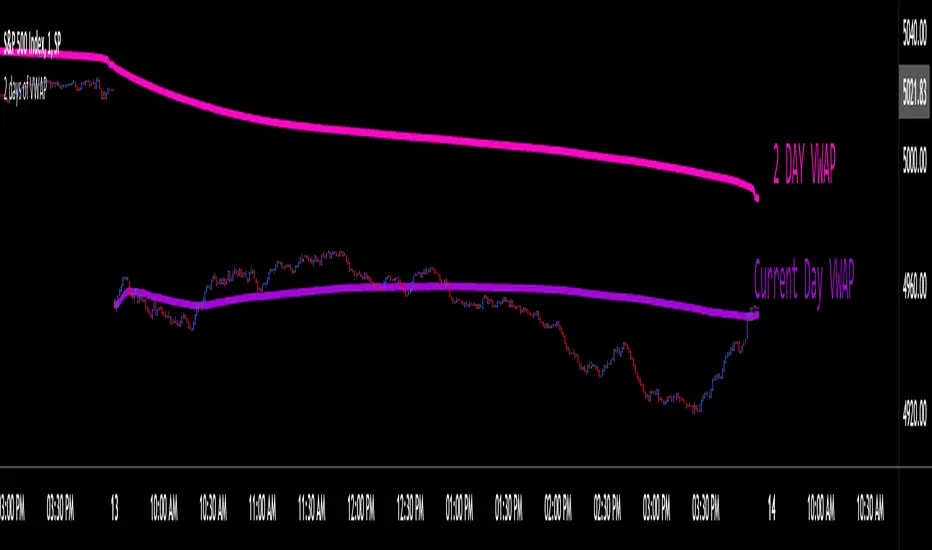

VWAP_CURRENT_YESTERDAY

The "VWAP CURRENT YESTERDAY" is a Pine Script designed for TradingView that automatically calculates and plots the Volume Weighted Average Price (VWAP) for the current day, the previous day.

Dynamic VWAP Calculation:

Automatically generates VWAPs for 1 day and 2 day.

User-Friendly Customization:

Through input options, users can easily toggle the visibility of each VWAP line, adjust colors, and set line thicknesses to their preference.

Configuration Options

1. VWAP Source:

Choose the price source for VWAP calculation. Default is the typical price (`hlc3` - the average of high, low, and close).

2. VWAP Lines:

Toggle the display for Today's VWAP, Yesterday's VWAP, and the VWAP from 2 days ago.

Customize colors and thickness for each VWAP line for clear visual distinction.

3. VWAP Labels:

Configure label sizes and positions to ensure that VWAP values are easily identifiable on the chart.

How It Works:

- The script calculates the sum of price multiplied by volume (`vwapsum`) and the sum of volumes (`volumesum`) for the specified periods.

- It utilizes an impulse function to reset calculations at the start of each new session or custom date, ensuring accurate and relevant VWAP values .

- Final VWAP values are plotted as lines on the chart, with optional labels for current and 2-day VWAPs for quick reference.

Customization Guide:

- To activate or deactivate specific VWAP lines, navigate to the 'VWAP Lines' section in the script's settings and toggle the respective options.

- Adjust the color and thickness of each VWAP line under the same section to match your charting preferences.

- Label settings, including size and offset, can be customized in the 'VWAP Labels' section, allowing for personalized label positioning and readability.

Volume inspectorThe "Volume inspector" is designed to provide a deep dive into the volume dynamics within a given larger timeframe by dissecting the positive and negative volume of candles from a lower timeframe. This analysis helps in understanding how the volume within a single candle is composed, whether it leans towards buying or selling pressure. The indicator sums up the positive and negative volumes to present the net volume in columns, offering a clear visual representation of the market's buying or selling intensity at a glance.

Additionally, it features an area between two Exponential Moving Averages (EMAs) to gauge the prevailing trend direction. A green spread between the EMAs signals strong buying pressure, with the width of the area indicating the strength of this pressure. Conversely, a red area points to selling pressure, warning users to exercise caution — it advises against buying the asset when the spread is narrow or red, suggesting weak buying momentum or strong selling momentum.

The tool recommends using daily candles as the primary timeframe for a broad market overview, with the following configurations for the lower timeframe analysis:

5 minutes for highly liquid and voluminous assets,

15 or 30 minutes for assets with lower volume to ensure accuracy without excessive market noise.

It's important to note that this indicator does not predict future market movements but rather analyzes the current behavior of the asset, making it a valuable tool for traders looking to understand immediate market sentiment and trend strength.

Asset capital flows - multi-timeframeIndicator for use on the any timeframe to show net capital flows into an asset of your choosing, to allow the user to track potential buy and selling pressure.

Net volume is derived from lower timeframe data (5 minute chart by default for daily timeframe) and multiplied by the average price for the same LTF period (defined by the mean of the high, low + close values). This gives the net capital inflow or outflow for the asset per bar. The cumulative sum of all previous bars is also calculated each period/day and available to be plotted as a line chart.

This might be preferred to other similar indicators as it uses low time frame bars to calculate the up/down volumes and price, thus accuracy is improved.

It should be borne in mind that the values of capital flows displayed are specific to the asset and the volume/price feed origin (ie the listed exchange used), and thus correlated with the total underlying flows, but there are other external factors influencing the volume/price data feed beyond the buy/sell volume of the specified exchange (such as spot and futures trading on other locations/exchanges)