Market Adaptive Stop-LossI realized that the zone changes in the stoploss remained slow, so I couldn't make enough use of the characteristics of technical indicators when opening positions.

This pushed me to keep stop-loss under the influence of a dependent variable.

This script helped me a lot (everget) :

I've redesigned the stop-loss to be affected by intersections.

Therefore, this script is also suitable for adaptive moving averages, fractional periods.

Script features:

1.You can select calculation methods created by using various technical analysis methods from the scripts' settings:

-Moving Average Convergence Divergence ( Macd )

-Stochastic Oscillator ( Stoch )

-Stochastic Relative Strength Index (StochRSI)

-Stochastic Money Flow Index (StochMFI ) (More info : )

-Know Sure Thing ( KST )

-OBV ( On Balance Volume )

-SMA ( Simple Moving Average )

-EMA ( Exponential Moving Average )

-FISHERTRANSFORM ( Fisher Transform )

-AWESOMEOSCILLATOR( Awesome Oscillator )

-PSAR ( Parabolic Stop and Reverse - Parabolic SAR )

-HULLMA( Hull Moving Average )

-VWMA ( Volume Weighted Moving Average )

-RMA (Moving Average using in Relative Strength Index calculations.)

-COG (Center of Gravity )

-ACC-DIST ( Accumulation / Distribution Index )

2 - The region is determined according to the above calculation methods and if it is larger or smaller than the previous stop loss level.

And if the price in the negative zone is lower than the stoploss, it is the exact signal and is shown with more highlighted colors.

And, in the positive zone, where the price is greater than the stoploss, the trade zones are certain.

Shown with more highlighted colors.

If the zones are correct but stop-loss is not suitable for opening positions:

In other words, if the stop-loss is above/under the highest-lowest levels in the positive zone or if the stop loss is located in the lower zone in the negative zone, these zones are shown to be darker and dimmed so that they do not cause false movements.

*** SUMMARY : As a result, you can use this script with support and resistances,and trend lines to get good results.

I hope it helps in your analyzes. Best regards.

Стоп по волатильности

Lancelot vstop intraday trending strategyDear all,

Free strategy again.

I found using 3 volatility stop with different settings could be very helpful when trading an intraday trending market.

With the ATR setting or 5, 10, 15, we can weed out many false break.

Vstop setting is OHLC4.

On the other hand, this strategy also utilize Renko as part of the strategy, so you could say this strategy is mainly an intraday break out trend following strategy.

Works well on BTCUSD XBTUSD, as well as other major liquid alt Pairs.

And lastly,

Save Hong Kong, the revolution of our times.

Alert-QuarryLake Indicator Map - ATR Trend Following Strategy A lot of times I don't like my chart crowding with indicators, thus the reason for creating this script for my strategy QuarryLake.

This script also comes with alert.

Below is the explanation for QuarryLake

I have also updated the script in version 4.

This strategy consists of 3 indicators that I found works quite well together.

Keltner Channel, Waddah Attah Explosion, and Volatility Stop.

You can find WAE here

KC Period = 200

KCATR = 5

Vstop Period = 3

Vstop Mult = 1.5

Long when close > KC, close > Vstop, WAE trendUp

Short when close < KC, close < Vstop, WAE trendDown

Works well on BTCUSD XBTUSD, as well as other major liquid Pair.

Feel free to follow me on Twitter @Lancelot_Auger for more free Alpha.

Please acknowledge my effort by like and follow.

And lastly,

Save Hong Kong, the revolution of our times.

CloudRest ATR based cloudThis is an indicator I have been working on for the past 2 years, developed specifically for cryptocurrency.

It is primarily a trend following indicator with great success and it performs the best in 4hrs to the weekly chart.

There are two components of this indicator.

The baseline from Ichimoku cloud and volatility stop .

baseline period = 26

volatility stop = 1.5ATR, 3

You can view this as the main component of a trend following system but you will need other confirmation indicators to confirm your entry.

Feel free to modify the script for your own system.

Feel free to follow me on twitter @Lancelot_Auger

I will be posting more content in the future, stay tuned.

And lastly,

Free hong kong, the revolution of our time!

ATR ChannelsATR Channels help you to identify where to place your stop-loss or trailing stop-loss based on price volatility, according to the Average True Range (ATR).

Volatility Stop trading with risk managementQuick coding of a trading system based on the Volatility Stop (VStop) indicator. In addition to that I added the possibility to calculate the position size based on the amount that you want to risk. Beware, this is the amount you want to risk per trade. The total draw-down might be higher, as you can have multiple loosing trades.

IFTS+TS Strategy OverlayInverse Fisher transform on stochastic with Hull MA and Donchian Channels with oversell/overbuy levels and dynamic trailing stop

Options:

Fixed trailing stop

Dynamic, based on ATR trailing stop

Re-enter after trailing stop

Includes Hull MA

Hull MA filtration for re-entering after trailing stop

Donchian channels, with overbuy/oversell levels

No repaints

Volatility System by Wilder [LucF]The Volatility System was created by J. Welles Wilder, Jr. It first appeared in his seminal masterpiece, "New Concepts in Technical Trading Systems" (1978). He describes the system on pp.23-26, in the chapter discussing the first presentation ever of the "Volatility Index", built using a novel way of calculating a value representing volatility that he named Average True Range (ATR). The latter stuck.

The system is a pure reversal system (it is always either long or short). One of its characteristics is that its stop strategy moves up and down during a trade, widening the gap from price when volatility (ATR) increases. Because of this, this strategy can suffer large drawdowns and is not for the faint of heart.

The strategy uses a length (n) to calculate an ATR. ATR(n) is then multiplied by a factor to calculate the Average Range Constant (ARC). The ARC is then added to the lowest close n bars back to form the high Stop and Reverse points (SAR), and subtracted from the highest close n bars back to calculate the low SAR. Reversals occur when price closes above the high SAR or below the low SAR.

The system is best suited to higher time frames: 12H and above. Its performance depends heavily on calibration of the length and ARC factor. Wilder proposes a length of 7 and a factor between 2.8 to 3.1. My summary tests at 12H, 1D and 3D on stocks and cryptos yield better results with values of approximately 9-10/1.8-2.5 for cryptos and 9-10/3.0-4.0 for stocks. Small changes in the values will sometimes yield large variations in results, which I don’t particularly like because it tends to imply fragility, whereas I’d expect more robustness from a system with such simple rules. Additionally, backtests at 1D on cryptos provide so little data that no solid conclusions can be drawn from them.

All in all, the system is not very useful in my opinion; I publish it more for completeness, since as far as I can tell, it did not exist on this platform before. I also publish it out of respect for Wilder’s work. His book laid the foundation for many of the building blocks used by system designers, even today. In less than a hundred pages he presented RSI, ATR, DMI, ADXR and the Parabolic SAR indicators, some of which have become built-in functions in programming languages. This is a colossal feat and has not been repeated. Wilder is a monument.

Some lesser-known facts about his book:

It sells for the exact same price it cost in 1978: 65$,

The book has always been published by Wilder himself,

The layout hasn’t changed in 40 years,

He sells >35K copies/year.

Gotta love the guy.

The strategy is shown here on BTC /USD with settings of 12/1.8 (the defaults are 9/1.8). It shows the system under its best light. Other markets will most not reproduce such results. Also, the drawdown is as scary as the results are impressive.

Features

The code is written as a strategy but can easily be converted to an indicator if you want to use the alerts it can produce. Instructions are in the code.

You can change the length and ARC factor.

You can choose to trade only long or short positions.

You can choose to display the SARs (the stops) in multiple ways.

You can show trigger markers.

A date range can be defined.

3 alerts: reversals (both long and short), longs, shorts. Remember that for the moment, strategies cannot generate alerts in TradingView, so the strategy must be converted to an indicator in order to make the alerts available.

Multi Fib Volatility StopA 7-band overlapping Fibonacci volatility stop. Select the start and multiplier and 6 increasing fibonacci bands will be overlayed to suggest areas of high probability buy/ sell opportunities.

ATR SL Visualization (on chart)This indicator plots 2 sets of dots (and lines) based on your chosen ATR multiplier (Average True Range).

Generally, when trading on the daily timeframe a good rule of thumb is to use the ATR * 1.5 (the default setting of this indicator).

I created this indicator to quickly test other indicators but I also find it helpful in live trading.

How to use this indicator:

Your trade system provides an entry signal. The red dot (can be connected line in options) would be used as the stop loss for either a long or short.

Then the dot on the other side would be your first 1:1 target.

The blue line is the same ATR multiplier as a target (default but can be modified).

Using an additional tool like the horizontal ray can be helpful to see the exact location the SL might be hit or where the target might hit.

When drawing your ray ensure you’re using the right entry candle.

For instance, in a long scenario you would typically be entering a trade after your signal candle closes. So draw the ray at the point in price on the next candle for both stop loss and target.

Also use these dots (lines) as guides provides an easy way to plot SL and targets if you want to use the Long or Short tool.

For my trade systems I don’t use price targets (I exit when structure or indicators reveal to exit) but I do find it helpful to graph when testing. When something moves in my favor either the ATR or the ATR * 1.5 I take profit and typically move up my stop loss to break even or trailing.

The other strategy that could be possible but have not tested is as long as the SL is making a new high moving up a hard stop to the ATR SL each day the trade goes in your favor.

This should be obvious but if you want to use just the true ATR edit the multiplier to be 1.0

Multi Timeframe Rolling Bitmex Liquidation LevelsTrack Bitmex liquidations levels in real-time with a rolling VWMA or VWAP basis.

Allows the input of a different time frame if you wish.

Gann Square Of 9 LevelsThis script uses the last hlc3 value of 1H, 4H, D and/or W and rotates it 360º up/down with four increments of 90º to find out potential support and resistance areas. Can be used as a dynamic support & resistance tool or just to gauge how overbought/oversold the market is. Special thanks to @Nv56 for his assistance in writing this script.

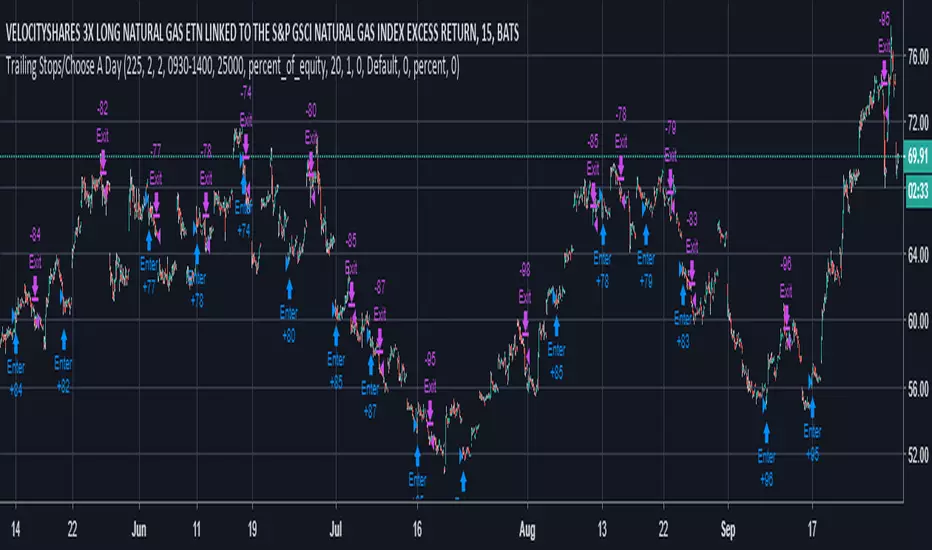

Trailing Stops/Choose a Day of the WeekThis would be my second ever published strategy. It is almost the same as my first ever published script . I've been working primarily on UGAZ and DGAZ .

This is basically a statistical trade. It buys every morning near market open (or by choosing a "time constraint"), then immediately places a trailing stop at a specified amount in ticks (if used on UGAZ a tick = $0.01, if used on NG at tick = $0.001). I've found between 2% and 3% works well for the trailing stop (ie. if UGAZ = $75, a 3% trailing stop = $2.25)

-----What is different from my first strategy?------

You can test the trailing stop strategy one 1 day of the week. Days of the week are assigned numbers. Sunday=1, Monday=2, Tuesday=3 and so on. Just choose a number that correlates to the day of the week you want to test. The Trailing stop may go past that day, that's a good thing if it's making money.

-- Go long/Short is just that, it will buy shares/contracts or short them.

-- Trades per day. This may not be a good choice, when left on "2", it will trade once per day. If set above 2 and there is time left for another trade, an order will enter on the open of the next candle. I'm am still working on ideas for this.

-- Time constraints. When you select this check box, the strategy will limit an entry to the time specified below the "Use Time Constraints" check box. An Exit order will still continue past this window of time until it is stopped out.

---- very important ----

Due to decay, leveraged ETFs will give false results if the price gets far out of range. For example, your ETF is trading around $20 and you choose a 1 hour chart, it may back test back to a time before a reverse split. If the price gets to be too large, like $200, or $1200, the movement on the chart creates false indication of profit/loss.

--- Most important. ---

Do not trade off this strategy, you may lose lots of money. This is for educational use only.

Good luck

A/D Levelsuses reversal candles to determine accumulation and distribution candles

remembers the last reversal candle and draws a support or resistance line at the reversal level

does a barcolor if the price breaks support/resistance

similar to the hoffman a/d breakout indicator but there is no trend detection components

Trailing Stops Only - For Leveraged ETFs (UGAZ/DGAZ)Looking for Statistical trades that work. This one seems to work on some Leveraged ETFs with a lot of noise like UGAZ/DGAZ. It can also be used on Futures Contracts, but be sure to change up the type of investment from % of equity to contracts. Also one point I'm trying to make with this strategy is the trades are best made in the morning around market open. When used with Contracts, be sure to make use of the time settings. It will limit buying between the hours set. Selling will occur at any time the trailing stop is triggered.

This Strategy is best used on 5min or 15min charts.

!!!! very important !!!!

Due to decay, leveraged ETFs will give false results if the price gets far out of range. For example, your ETF is trading around $20 and you choose a 1 hour chart, it may back test back to a time before a reverse split. If the price gets to be too large, like $200, or $1200, the movement on the chart creates false indication of profit/loss.

Most important. Do not trade off this strategy, you may lose lots of money. This is for educational use only.

TRBTrue Range Bands; the 'Supertrend', also known as a volatility stop, using a 14 period length and 3x multiplier.

VMA's (T=1h, 2h, 4h, 8h)Plots four VMA's (Variable/Volatility Moving Average) in multiple static resolutions (1h, 2h, 4h, 8h), ideal for support/resistance/stops on predictably trending symbols like BTCUSD.

Example:

BitMex Trailing Stop StrategyThis script is designed for those who want to use BitMex's trailing stop. It's not meant to be used as entry exits, but rather to get an idea of how wide the trailing stop needs to be. I suggest you backtest with different values. The script can also be integrated into an existing strategy which does give entry/exits to act as its stop loss.

Simple Trailing Buy & Stop StrategyAllows you to backtest a simple percentage based trailing stop, with a trailing buy. Experiment with different percentages on different timeframes for different charts.

For BTCUSD, on daily 4.3% stop and 1.9% buy works well, while on 4hr a 1.5% stop and 1.9% buy works best.

Please comment with any other combos that work well for you on different markets or timeframes.