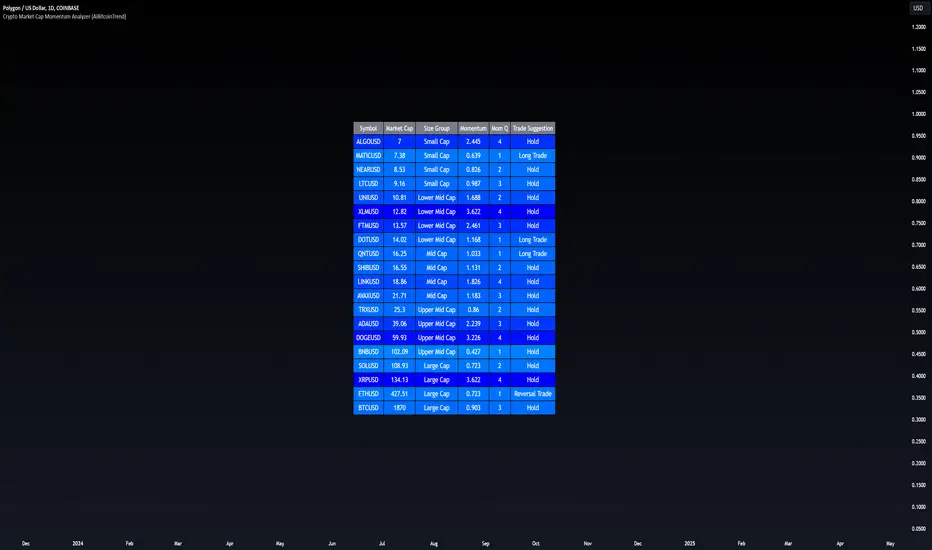

Crypto Market Cap Momentum Analyzer (AiBitcoinTrend)The Crypto Market Cap Momentum Analyzer (AiBitcoinTrend) is a robust tool designed to uncover trading opportunities by blending market cap analysis and momentum dynamics. Inspired by research-backed quantitative strategies, this indicator helps traders identify trend-following and mean-reversion setups in the cryptocurrency market by evaluating recent performance and market cap size.

This indicator classifies cryptocurrencies into market cap quintiles and ranks them based on their 2-week momentum. It then suggests potential trades—whether to go long, anticipate reversals, or simply hold—based on the crypto's market cap group and momentum trends.

👽 How the Indicator Works

👾 Market Cap Classification

The indicator categorizes cryptocurrencies into one of five market cap groups based on user-defined inputs:

Large Cap: Highest market cap tier

Upper Mid Cap: Second highest group

Mid Cap: Middle-tier market caps

Lower Mid Cap: Slightly below the mid-tier

Small Cap: Lowest market cap tier

This classification dynamically adjusts based on the provided market cap data, ensuring that you’re always working with a representative market structure.

👾 Momentum Calculation

By default, the indicator uses a 2-week momentum measure (e.g., a 14-day lookback when set to daily). It compares a cryptocurrency’s current price to its price 14 bars ago, thereby quantifying its short-term performance. Users can adjust the momentum period and rebalance period to capture shorter or longer-term trends depending on their trading style.

👾 Dynamic Ranking and Trade Suggestions

After assigning cryptos to size quintiles, the indicator sorts them by their momentum within each quintile. This two-step process results in:

Long Trade: For smaller market cap groups (Small, Lower Mid, Mid Cap) that have low (bottom-quintile) momentum, anticipating a trend continuation or breakout.

Reversal Trade: For the largest market cap group (Large Cap) that shows low momentum, expecting a mean-reversion back to equilibrium.

Hold: In scenarios where the coin’s momentum doesn’t present a strong contrarian or trend-following signal.

👽 Applications

👾 Trend-Following in Smaller Caps: Identify small or mid-cap cryptos with low momentum that might be poised for a breakout or sustained trend.

👾 Mean-Reversion in Large Caps: Pinpoint large-cap cryptocurrencies experiencing a temporary lull in performance, potentially ripe for a rebound.

👽 Why It Works in Crypto

The cryptocurrency market is heavily driven by retail investor sentiment and volatility. Research shows that:

Small-Cap Cryptos: Tend to experience higher volatility and speculative trends, making them ideal for momentum trades.

Large-Cap Cryptos: Exhibit more predictable behavior, making them suitable for mean-reversion strategies when momentum is low.

This indicator captures these dynamics to give traders a strategic edge in identifying both momentum and reversal opportunities.

👽 Indicator Settings

👾 Rebalance Period: The frequency at which momentum and trade suggestions are recalculated (Daily, Weekly, Monthly).

Shorter Periods (Daily): Fast updates, suitable for short-term trades, but more noise.

Longer Periods (Weekly/Monthly): Smoother signals, ideal for swing trading and more stable trends.

👾 Momentum Period: The lookback period for momentum calculation (default is 14 bars).

Shorter Periods: More responsive but prone to noise.

Longer Periods : Reflects broader trends, reducing sensitivity to short-term fluctuations.

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Волатильность

Median Deviation Suite [InvestorUnknown]The Median Deviation Suite uses a median-based baseline derived from a Double Exponential Moving Average (DEMA) and layers multiple deviation measures around it. By comparing price to these deviation-based ranges, it attempts to identify trends and potential turning points in the market. The indicator also incorporates several deviation types—Average Absolute Deviation (AAD), Median Absolute Deviation (MAD), Standard Deviation (STDEV), and Average True Range (ATR)—allowing traders to visualize different forms of volatility and dispersion. Users should calibrate the settings to suit their specific trading approach, as the default values are not optimized.

Core Components

Median of a DEMA:

The foundation of the indicator is a Median applied to the 7-day DEMA (Double Exponential Moving Average). DEMA aims to reduce lag compared to simple or exponential moving averages. By then taking a median over median_len periods of the DEMA values, the indicator creates a robust and stable central tendency line.

float dema = ta.dema(src, 7)

float median = ta.median(dema, median_len)

Multiple Deviation Measures:

Around this median, the indicator calculates several measures of dispersion:

ATR (Average True Range): A popular volatility measure.

STDEV (Standard Deviation): Measures the spread of price data from its mean.

MAD (Median Absolute Deviation): A robust measure of variability less influenced by outliers.

AAD (Average Absolute Deviation): Similar to MAD, but uses the mean absolute deviation instead of median.

Average of Deviations (avg_dev): The average of the above four measures (ATR, STDEV, MAD, AAD), providing a combined sense of volatility.

Each measure is multiplied by a user-defined multiplier (dev_mul) to scale the width of the bands.

aad = f_aad(src, dev_len, median) * dev_mul

mad = f_mad(src, dev_len, median) * dev_mul

stdev = ta.stdev(src, dev_len) * dev_mul

atr = ta.atr(dev_len) * dev_mul

avg_dev = math.avg(aad, mad, stdev, atr)

Deviation-Based Bands:

The indicator creates multiple upper and lower lines based on each deviation type. For example, using MAD:

float mad_p = median + mad // already multiplied by dev_mul

float mad_m = median - mad

Similar calculations are done for AAD, STDEV, ATR, and the average of these deviations. The indicator then determines the overall upper and lower boundaries by combining these lines:

float upper = f_max4(aad_p, mad_p, stdev_p, atr_p)

float lower = f_min4(aad_m, mad_m, stdev_m, atr_m)

float upper2 = f_min4(aad_p, mad_p, stdev_p, atr_p)

float lower2 = f_max4(aad_m, mad_m, stdev_m, atr_m)

This creates a layered structure of volatility envelopes. Traders can observe which layers price interacts with to gauge trend strength.

Determining Trend

The indicator generates trend signals by assessing where price stands relative to these deviation-based lines. It assigns a trend score by summing individual signals from each deviation measure. For instance, if price crosses above the MAD-based upper line, it contributes a bullish point; crossing below an ATR-based lower line contributes a bearish point.

When the aggregated trend score crosses above zero, it suggests a shift towards a bullish environment; crossing below zero indicates a bearish bias.

// Define Trend scores

var int aad_t = 0

if ta.crossover(src, aad_p)

aad_t := 1

if ta.crossunder(src, aad_m)

aad_t := -1

var int mad_t = 0

if ta.crossover(src, mad_p)

mad_t := 1

if ta.crossunder(src, mad_m)

mad_t := -1

var int stdev_t = 0

if ta.crossover(src, stdev_p)

stdev_t := 1

if ta.crossunder(src, stdev_m)

stdev_t := -1

var int atr_t = 0

if ta.crossover(src, atr_p)

atr_t := 1

if ta.crossunder(src, atr_m)

atr_t := -1

var int adev_t = 0

if ta.crossover(src, adev_p)

adev_t := 1

if ta.crossunder(src, adev_m)

adev_t := -1

int upper_t = src > upper ? 3 : 0

int lower_t = src < lower ? 0 : -3

int upper2_t = src > upper2 ? 1 : 0

int lower2_t = src < lower2 ? 0 : -1

float trend = aad_t + mad_t + stdev_t + atr_t + adev_t + upper_t + lower_t + upper2_t + lower2_t

var float sig = 0

if ta.crossover(trend, 0)

sig := 1

else if ta.crossunder(trend, 0)

sig := -1

Practical Usage and Calibration

Default settings are not optimized: The given parameters serve as a starting point for demonstration. Users should adjust:

median_len: Affects how smooth and lagging the median of the DEMA is.

dev_len and dev_mul: Influence the sensitivity of the deviation measures. Larger multipliers widen the bands, potentially reducing false signals but introducing more lag. Smaller multipliers tighten the bands, producing quicker signals but potentially more whipsaws.

This flexibility allows the trader to tailor the indicator for various markets (stocks, forex, crypto) and time frames.

Backtesting and Performance Metrics

The code integrates with a backtesting library that allows traders to:

Evaluate the strategy historically

Compare the indicator’s signals with a simple buy-and-hold approach

Generate performance metrics (e.g., mean returns, Sharpe Ratio, Sortino Ratio) to assess historical effectiveness.

Disclaimer

No guaranteed results: Historical performance does not guarantee future outcomes. Market conditions can vary widely.

User responsibility: Traders should combine this indicator with other forms of analysis, appropriate risk management, and careful calibration of parameters.

DAILY Supertrend + EMA Crossover with RSI FilterThis strategy is a technical trading approach that combines multiple indicators—Supertrend, Exponential Moving Averages (EMAs), and the Relative Strength Index (RSI)—to identify and manage trades.

Core Components:

1. Exponential Moving Averages (EMAs):

Two EMAs, one with a shorter period (fast) and one with a longer period (slow), are calculated. The idea is to spot when the faster EMA crosses above or below the slower EMA. A fast EMA crossing above the slow EMA often suggests upward momentum, while crossing below suggests downward momentum.

2. Supertrend Indicator:

The Supertrend uses Average True Range (ATR) to establish dynamic support and resistance lines. These lines shift above or below price depending on the prevailing trend. When price is above the Supertrend line, the trend is considered bullish; when below, it’s considered bearish. This helps ensure that the strategy trades only in the direction of the overall trend rather than against it.

3. RSI Filter:

The RSI measures momentum. It helps avoid buying into markets that are already overbought or selling into markets that are oversold. For example, when going long (buying), the strategy only proceeds if the RSI is not too high, and when going short (selling), it only proceeds if the RSI is not too low. This filter is meant to improve the quality of the trades by reducing the chance of entering right before a reversal.

4. Time Filters:

The strategy only triggers entries during user-specified date and time ranges. This is useful if one wants to limit trading activity to certain trading sessions or periods with higher market liquidity.

5. Risk Management via ATR-based Stops and Targets:

Both stop loss and take profit levels are set as multiples of the ATR. ATR measures volatility, so when volatility is higher, both stops and profit targets adjust to give the trade more breathing room. Conversely, when volatility is low, stops and targets tighten. This dynamic approach helps maintain consistent risk management regardless of market conditions.

Overall Logic Flow:

- First, the market conditions are analyzed through EMAs, Supertrend, and RSI.

- When a buy (long) condition is met—meaning the fast EMA crosses above the slow EMA, the trend is bullish according to Supertrend, and RSI is below the specified “overbought” threshold—the strategy initiates or adds to a long position.

- Similarly, when a sell (short) condition is met—meaning the fast EMA crosses below the slow EMA, the trend is bearish, and RSI is above the specified “oversold” threshold—it initiates or adds to a short position.

- Each position is protected by an automatically calculated stop loss and a take profit level based on ATR multiples.

Intended Result:

By blending trend detection, momentum filtering, and volatility-adjusted risk management, the strategy aims to capture moves in the primary trend direction while avoiding entries at excessively stretched prices. Allowing multiple entries can potentially amplify gains in strong trends but also increases exposure, which traders should consider in their risk management approach.

In essence, this strategy tries to ride established trends as indicated by the Supertrend and EMAs, filter out poor-quality entries using RSI, and dynamically manage trade risk through ATR-based stops and targets.

True Amplitude Envelopes (TAE)The True Envelopes indicator is an adaptation of the True Amplitude Envelope (TAE) method, based on the research paper " Improved Estimation of the Amplitude Envelope of Time Domain Signals Using True Envelope Cepstral Smoothing " by Caetano and Rodet. This indicator aims to create an asymmetric price envelope with strong predictive power, closely following the methodology outlined in the paper.

Due to the inherent limitations of Pine Script, the indicator utilizes a Kernel Density Estimator (KDE) in place of the original Cepstral Smoothing technique described in the paper. While this approach was chosen out of necessity rather than superiority, the resulting method is designed to be as effective as possible within the constraints of the Pine environment.

This indicator is ideal for traders seeking an advanced tool to analyze price dynamics, offering insights into potential price movements while working within the practical constraints of Pine Script. Whether used in dynamic mode or with a static setting, the True Envelopes indicator helps in identifying key support and resistance levels, making it a valuable asset in any trading strategy.

Key Features:

Dynamic Mode: The indicator dynamically estimates the fundamental frequency of the price, optimizing the envelope generation process in real-time to capture critical price movements.

High-Pass Filtering: Uses a high-pass filtered signal to identify and smoothly interpolate price peaks, ensuring that the envelope accurately reflects significant price changes.

Kernel Density Estimation: Although implemented as a workaround, the KDE technique allows for flexible and adaptive smoothing of the envelope, aimed at achieving results comparable to the more sophisticated methods described in the original research.

Symmetric and Asymmetric Envelopes: Provides options to select between symmetric and asymmetric envelopes, accommodating various trading strategies and market conditions.

Smoothness Control: Features adjustable smoothness settings, enabling users to balance between responsiveness and the overall smoothness of the envelopes.

The True Envelopes indicator comes with a variety of input settings that allow traders to customize the behavior of the envelopes to match their specific trading needs and market conditions. Understanding each of these settings is crucial for optimizing the indicator's performance.

Main Settings

Source: This is the data series on which the indicator is applied, typically the closing price (close). You can select other price data like open, high, low, or a custom series to base the envelope calculations.

History: This setting determines how much historical data the indicator should consider when calculating the envelopes. A value of 0 will make the indicator process all available data, while a higher value restricts it to the most recent n bars. This can be useful for reducing the computational load or focusing the analysis on recent market behavior.

Iterations: This parameter controls the number of iterations used in the envelope generation algorithm. More iterations will typically result in a smoother envelope, but can also increase computation time. The optimal number of iterations depends on the desired balance between smoothness and responsiveness.

Kernel Style: The smoothing kernel used in the Kernel Density Estimator (KDE). Available options include Sinc, Gaussian, Epanechnikov, Logistic, and Triangular. Each kernel has different properties, affecting how the smoothing is applied. For example, Gaussian provides a smooth, bell-shaped curve, while Epanechnikov is more efficient computationally with a parabolic shape.

Envelope Style: This setting determines whether the envelope should be Static or Dynamic. The Static mode applies a fixed period for the envelope, while the Dynamic mode automatically adjusts the period based on the fundamental frequency of the price data. Dynamic mode is typically more responsive to changing market conditions.

High Q: This option controls the quality factor (Q) of the high-pass filter. Enabling this will increase the Q factor, leading to a sharper cutoff and more precise isolation of high-frequency components, which can help in better identifying significant price peaks.

Symmetric: This setting allows you to choose between symmetric and asymmetric envelopes. Symmetric envelopes maintain an equal distance from the central price line on both sides, while asymmetric envelopes can adjust differently above and below the price line, which might better capture market conditions where upside and downside volatility are not equal.

Smooth Envelopes: When enabled, this setting applies additional smoothing to the envelopes. While this can reduce noise and make the envelopes more visually appealing, it may also decrease their responsiveness to sudden market changes.

Dynamic Settings

Extra Detrend: This setting toggles an additional high-pass filter that can be applied when using a long filter period. The purpose is to further detrend the data, ensuring that the envelope focuses solely on the most recent price oscillations.

Filter Period Multiplier: This multiplier adjusts the period of the high-pass filter dynamically based on the detected fundamental frequency. Increasing this multiplier will lengthen the period, making the filter less sensitive to short-term price fluctuations.

Filter Period (Min) and Filter Period (Max): These settings define the minimum and maximum bounds for the high-pass filter period. They ensure that the filter period stays within a reasonable range, preventing it from becoming too short (and overly sensitive) or too long (and too sluggish).

Envelope Period Multiplier: Similar to the filter period multiplier, this adjusts the period for the envelope generation. It scales the period dynamically to match the detected price cycles, allowing for more precise envelope adjustments.

Envelope Period (Min) and Envelope Period (Max): These settings establish the minimum and maximum bounds for the envelope period, ensuring the envelopes remain adaptive without becoming too reactive or too slow.

Static Settings

Filter Period: In static mode, this setting determines the fixed period for the high-pass filter. A shorter period will make the filter more responsive to price changes, while a longer period will smooth out more of the price data.

Envelope Period: This setting specifies the fixed period used for generating the envelopes in static mode. It directly influences how tightly or loosely the envelopes follow the price action.

TAE Smoothing: This controls the degree of smoothing applied during the TAE process in static mode. Higher smoothing values result in more gradual envelope curves, which can be useful in reducing noise but may also delay the envelope’s response to rapid price movements.

Visual Settings

Top Band Color: This setting allows you to choose the color for the upper band of the envelope. This band represents the resistance level in the price action.

Bottom Band Color: Similar to the top band color, this setting controls the color of the lower band, which represents the support level.

Center Line Color: This is the color of the central price line, often referred to as the carrier. It represents the detrended price around which the envelopes are constructed.

Line Width: This determines the thickness of the plotted lines for the top band, bottom band, and center line. Thicker lines can make the envelopes more visible, especially when overlaid on price data.

Fill Alpha: This controls the transparency level of the shaded area between the top and bottom bands. A lower alpha value will make the fill more transparent, while a higher value will make it more opaque, helping to highlight the envelope more clearly.

The envelopes generated by the True Envelopes indicator are designed to provide a more precise and responsive representation of price action compared to traditional methods like Bollinger Bands or Keltner Channels. The core idea behind this indicator is to create a price envelope that smoothly interpolates the significant peaks in price action, offering a more accurate depiction of support and resistance levels.

One of the critical aspects of this approach is the use of a high-pass filtered signal to identify these peaks. The high-pass filter serves as an effective method of detrending the price data, isolating the rapid fluctuations in price that are often lost in standard trend-following indicators. By filtering out the lower frequency components (i.e., the trend), the high-pass filter reveals the underlying oscillations in the price, which correspond to significant peaks and troughs. These oscillations are crucial for accurately constructing the envelope, as they represent the most responsive elements of the price movement.

The algorithm works by first applying the high-pass filter to the source price data, effectively detrending the series and isolating the high-frequency price changes. This filtered signal is then used to estimate the fundamental frequency of the price movement, which is essential for dynamically adjusting the envelope to current market conditions. By focusing on the peaks identified in the high-pass filtered signal, the algorithm generates an envelope that is both smooth and adaptive, closely following the most significant price changes without overfitting to transient noise.

Compared to traditional envelopes and bands, such as Bollinger Bands and Keltner Channels, the True Envelopes indicator offers several advantages. Bollinger Bands, which are based on standard deviations, and Keltner Channels, which use the average true range (ATR), both tend to react to price volatility but do not necessarily follow the peaks and troughs of the price with precision. As a result, these traditional methods can sometimes lag behind or fail to capture sudden shifts in price momentum, leading to either false signals or missed opportunities.

In contrast, the True Envelopes indicator, by using a high-pass filtered signal and a dynamic period estimation, adapts more quickly to changes in price behavior. The envelopes generated by this method are less prone to the lag that often affects standard deviation or ATR-based bands, and they provide a more accurate representation of the price's immediate oscillations. This can result in better predictive power and more reliable identification of support and resistance levels, making the True Envelopes indicator a valuable tool for traders looking for a more responsive and precise approach to market analysis.

In conclusion, the True Envelopes indicator is a powerful tool that blends advanced theoretical concepts with practical implementation, offering traders a precise and responsive way to analyze price dynamics. By adapting the True Amplitude Envelope (TAE) method through the use of a Kernel Density Estimator (KDE) and high-pass filtering, this indicator effectively captures the most significant price movements, providing a more accurate depiction of support and resistance levels compared to traditional methods like Bollinger Bands and Keltner Channels. The flexible settings allow for extensive customization, ensuring the indicator can be tailored to suit various trading strategies and market conditions.

RSI and Bollinger Bands Screener [deepakks444]Indicator Overview

The indicator is designed to help traders identify potential long signals by combining the Relative Strength Index (RSI) and Bollinger Bands across multiple timeframes. This combination allows traders to leverage the strengths of both indicators to make more informed trading decisions.

Understanding RSI

What is RSI?

The Relative Strength Index (RSI) is a momentum oscillator that measures the speed and change of price movements. Developed by J. Welles Wilder Jr. for stocks and forex trading, the RSI is primarily used to identify overbought or oversold conditions in an asset.

How RSI Works:

Calculation: The RSI is calculated using the average gains and losses over a specified period, typically 14 periods.

Range: The RSI oscillates between 0 and 100.

Interpretation:

Key Features of RSI:

Momentum Indicator: RSI helps identify the momentum of price movements.

Divergences: RSI can show divergences, where the price makes a higher high, but the RSI makes a lower high, indicating potential reversals.

Trend Identification: RSI can also help identify trends. In an uptrend, the RSI tends to stay above 50, and in a downtrend, it tends to stay below 50.

Understanding Bollinger Bands

What is Bollinger Bands?

Bollinger Bands are a type of trading band or envelope plotted two standard deviations (positively and negatively) away from a simple moving average (SMA) of a price. Developed by financial analyst John Bollinger, Bollinger Bands consist of three lines:

Upper Band: SMA + (Standard Deviation × Multiplier)

Middle Band (Basis): SMA

Lower Band: SMA - (Standard Deviation × Multiplier)

How Bollinger Bands Work:

Volatility Measure: Bollinger Bands measure the volatility of the market. When the bands are wide, it indicates high volatility, and when the bands are narrow, it indicates low volatility.

Price Movement: The price tends to revert to the mean (middle band) after touching the upper or lower bands.

Support and Resistance: The upper and lower bands can act as dynamic support and resistance levels.

Key Features of Bollinger Bands:

Volatility Indicator: Bollinger Bands help traders understand the volatility of the market.

Mean Reversion: Prices tend to revert to the mean (middle band) after touching the bands.

Squeeze: A Bollinger Band Squeeze occurs when the bands narrow significantly, indicating low volatility and a potential breakout.

Combining RSI and Bollinger Bands

Strategy Overview:

The strategy aims to identify potential long signals by combining RSI and Bollinger Bands across multiple timeframes. The key conditions are:

RSI Crossing Above 60: The RSI should cross above 60 on the 15-minute timeframe.

RSI Above 60 on Higher Timeframes: The RSI should already be above 60 on the hourly and daily timeframes.

Price Above 20MA or Walking on Upper Bollinger Band: The price should be above the 20-period moving average of the Bollinger Bands or walking on the upper Bollinger Band.

Strategy Details:

RSI Calculation:

Calculate the RSI for the 15-minute, 1-hour, and 1-day timeframes.

Check if the RSI crosses above 60 on the 15-minute timeframe.

Ensure the RSI is above 60 on the 1-hour and 1-day timeframes.

Bollinger Bands Calculation:

Calculate the Bollinger Bands using a 20-period moving average and 2 standard deviations.

Check if the price is above the 20-period moving average or walking on the upper Bollinger Band.

Entry and Exit Signals:

Long Signal: When all the above conditions are met, consider a long entry.

Exit: Exit the trade when the price crosses below the 20-period moving average or the stop-loss is hit.

Example Usage

Setup:

Add the indicator to your TradingView chart.

Configure the inputs as per your requirements.

Monitoring:

Look for the long signal on the chart.

Ensure that the RSI is above 60 on the 15-minute, 1-hour, and 1-day timeframes.

Check that the price is above the 20-period moving average or walking on the upper Bollinger Band.

Trading:

Enter a long position when the criteria are met.

Set a stop-loss below the low of the recent 15-minute candle or based on your risk management rules.

Monitor the trade and exit when the RSI returns below 60 on any of the timeframes or when the price crosses below the 20-period moving average.

House Rules Compliance

No Financial Advice: This strategy is for educational purposes only and should not be construed as financial advice.

Risk Management: Always use proper risk management techniques, including stop-loss orders and position sizing.

Past Performance: Past performance is not indicative of future results. Always conduct your own research and analysis.

TradingView Guidelines: Ensure that any shared scripts or strategies comply with TradingView's terms of service and community guidelines.

Conclusion

This strategy combines RSI and Bollinger Bands across multiple timeframes to identify potential long signals. By ensuring that the RSI is above 60 on higher timeframes and that the price is above the 20-period moving average or walking on the upper Bollinger Band, traders can make more informed decisions. Always remember to conduct thorough research and use proper risk management techniques.

BTC/USDT Volume-Based StrategyOverview

There is a distinct difference between the buying pressure exerted by individual investors and the buying pressure of institutional or "whale" traders. Monitoring volume data over a shorter period of time is crucial to distinguish these subtle differences. When whale investors or other significant market players signal price increases, volume often surges noticeably. Indeed, volume often acts as an important leading indicator in market dynamics.

Key Features

This metric, calibrated with a 5-minute Bitcoin spot chart, identifies a significant inflow of trading volume. For every K-plus surge in trading volume, those candles are shown in a green circle.

When a green circle appears, consider active long positions in subsequent declines and continue to accumulate long positions despite temporary price declines. Pay attention to the continuity of the increase in volume before locking in earnings even after the initial bullish wave.

Conversely, it may be wise to reevaluate the long position if the volume is not increasing in parallel and the price is rising. Under these conditions, starting a partial short position may be advantageous until a larger surge in volume reappears.

ATR for Aggregated Bars (2 Bars)Range Bar ATR Indicator: Detailed Description and Usage Guide

This script is a custom indicator designed specifically for Range Bar charts , tailored to help traders understand and navigate market conditions by utilizing the Average True Range (ATR) concept. The indicator adapts the traditional ATR to work effectively with Range Bar charts, where bars have a fixed range rather than being time-based.

How It Works

1. ATR Calculation on Range Bars :

- Unlike time-based charts, Range Bar charts focus on price movement within a fixed range.

- The indicator calculates ATR by pairing consecutive bars, treating every two bars as a single unit . This pairing ensures that the ATR reflects price movement effectively on Range Bar charts.

2. Short and Long Period ATR Values :

- The script displays two ATR values :

- A short-period ATR , calculated over a smaller number of paired bars.

- A long-period ATR , calculated over a larger number of paired bars.

- These values provide a dynamic view of both recent and longer-term market volatility.

Why Use This Indicator?

The primary goal is to provide a meaningful adaptation of the ATR indicator for Range Bar charts, allowing traders to make informed decisions similar to using ATR on traditional time-based charts.

Key Applications

Determine a Better Custom Range :

- Analyze the ATR values to choose an optimal range size for Range Bar charts, ensuring better alignment with market conditions.

Assess Market Volatility :

- Rising volatility : When the short-period ATR value is higher than the long-period value, it signals increasing volatility.

- Decreasing volatility : When the short-period ATR value is lower, it indicates declining volatility.

Risk and Stop Loss Management :

- Use the higher ATR value (e.g., the long-period ATR) to calculate minimum stop loss levels. Multiply the ATR by 1.5 or 2 to set a safe buffer against market fluctuations.

How to Use It

1. Add the script to a Range Bar chart.

2. Configure the short and long ATR periods to suit your trading style and preferences.

3. Observe the displayed ATR values:

- Use these values to analyze market conditions and adapt your strategy accordingly.

4. Apply insights from the ATR values for:

- Determining custom Range Bar settings.

- Evaluating volatility trends.

- Setting effective risk parameters like stop loss levels.

Benefits

- Provides a tailored ATR tool for Range Bar charts, addressing the unique challenges of fixed-range trading.

- Offers both short-term and long-term perspectives on volatility.

- Enhances decision-making for range settings, volatility analysis, and risk management.

This indicator bridges the gap between traditional ATR indicators and the specific needs of Range Bar chart users, making it a versatile tool for traders.

ka66: Candle Range MarkThis is a simple trailing stop loss tool using bar ranges, to be used with some discretion and understanding of basic price action.

Given a configurable percentage value, e.g. 25%:

A bullish bar (close > open) will be marked at the lower 25%

A bearish bar (close < open) will be marked at the upper 25%

The idea is to move your stop loss after each completed bar in the direction of the trade, at the configured percentage value.

If you have an inside bar, or something very close to it, or a doji-type bar, don't trail that, because there is no clarity of what the bar means, we can only wait.

The chart shows an example use, with trailing at 10% of the bar, from the initial stop loss after entry, trailing till we get stopped out. Some things to note:

Because this example focuses on a short trade, we ignore the bullish candles, and keep our trailing stop at the last bearish candle.

We ignore doji-esque candles and inside bars, where the body is in the range of the prior candle. Some definitions of inside bars include the wicks as well. I don't have a strong opinion, and this example is just for illustration. Furthermore, the inside bar will likely be the opposite of the swing bars (e.g. bullish bar in a range of bearish bars), so our stop remains unchanged.

One could use this semi-systematic approach in scalping on any timeframe, for example to maximise gains, adjusting the bar percentage as needed.

Algorithmic Signal AnalyzerMeet Algorithmic Signal Analyzer (ASA) v1: A revolutionary tool that ushers in a new era of clarity and precision for both short-term and long-term market analysis, elevating your strategies to the next level.

ASA is an advanced TradingView indicator designed to filter out noise and enhance signal detection using mathematical models. By processing price movements within defined standard deviation ranges, ASA produces a smoothed analysis based on a Weighted Moving Average (WMA). The Volatility Filter ensures that only relevant price data is retained, removing outliers and improving analytical accuracy.

While ASA provides significant analytical advantages, it’s essential to understand its capabilities in both short-term and long-term use cases. For short-term trading, ASA excels at capturing swift opportunities by highlighting immediate trend changes. Conversely, in long-term trading, it reveals the overall direction of market trends, enabling traders to align their strategies with prevailing conditions.

Despite these benefits, traders must remember that ASA is not designed for precise trade execution systems where accuracy in timing and price levels is critical. Its focus is on analysis rather than order management. The distinction is crucial: ASA helps interpret price action effectively but may not account for real-time market factors such as slippage or execution delays.

Features and Functionality

ASA integrates multiple tools to enhance its analytical capabilities:

Customizable Moving Averages: SMA, EMA, and WMA options allow users to tailor the indicator to their trading style.

Signal Detection: Identifies bullish and bearish trends using the Relative Exponential Moving Average (REMA) and marks potential buy/sell opportunities.

Visual Aids: Color-coded trend lines (green for upward, red for downward) simplify interpretation.

Alert System: Notifications for trend swings and reversals enable timely decision-making.

Notes on Usage

ASA’s effectiveness depends on the context in which it is applied. Traders should carefully consider the trade-offs between analysis and execution.

Results may vary depending on market conditions and chart types. Backtesting with ASA on standard charts provides more reliable insights compared to non-standard chart types.

Short-term use focuses on rapid trend recognition, while long-term application emphasizes understanding broader market movements.

Takeaways

ASA is not a tool for precise trade execution but a powerful aid for interpreting price trends.

For short-term trading, ASA identifies quick opportunities, while for long-term strategies, it highlights trend directions.

Understanding ASA’s limitations and strengths is key to maximizing its utility.

ASA is a robust solution for traders seeking to filter noise, enhance analytical clarity, and align their strategies with market movements, whether for short bursts of activity or sustained trading goals.

[blackcat] L1 Extreme Shadows█ OVERVIEW

The Pine Script provided is an indicator designed to detect market volatility and extreme shadow conditions. It calculates various conditions based on simple moving averages (SMAs) and plots the results to help traders identify potential market extremes. The primary function of the script is to provide visual cues for extreme market conditions without generating explicit trading signals.

█ LOGICAL FRAMEWORK

Structure:

1 — Input Parameters:

• No user-defined input parameters are present in this script.

2 — Calculations:

• Calculate Extreme Shadow: Checks if the differences between certain SMAs and prices exceed predefined thresholds.

• Calculate Buy Extreme Shadow: Extends the logic by incorporating additional SMAs to identify stronger buy signals.

• Calculate Massive Bullish Sell: Detects massive bullish sell conditions using longer-term SMAs.

3 — Plotting:

• The script plots the calculated conditions using distinct colors to differentiate between various types of extreme shadows.

Data Flow:

• The close price is passed through each custom function.

• Each function computes its respective conditions based on specified SMAs and thresholds.

• The computed values are then summed and returned.

• Finally, the aggregated values are plotted on the chart using the plot function.

█ CUSTOM FUNCTIONS

1 — calculate_extreme_shadow(close)

• Purpose: Identify extreme shadow conditions based on 8-period and 14-period SMAs.

• Functionality: Computes the difference between the 8-period SMA and the close price, and the difference between the 14-period SMA and the 4-period SMA, relative to the 6-period SMA. Returns 2 if both conditions exceed 0.04; otherwise, returns 0.

• Parameters: close (price series)

• Return Value: Integer (0 or 2)

2 — calculate_buy_extreme_shadow(close)

• Purpose: Identify more robust buy signals by evaluating multiple SMAs.

• Functionality: Considers the 8-period SMA along with additional SMAs (21, 42, 63, 84, 105) and combines multiple conditions to provide a comprehensive buy signal.

• Parameters: close (price series)

• Return Value: Integer (sum of conditions, ranging from 0 to 14)

3 — calculate_massive_bullish_sell(close)

• Purpose: Detect massive bullish sell conditions using longer-term SMAs.

• Functionality: Evaluates conditions based on the 8-period SMA and longer-term SMAs (88, 44, 22, 11, 5), returning a sum of conditions meeting specified thresholds.

• Parameters: close (price series)

• Return Value: Integer (sum of conditions, ranging from 0 to 10)

█ KEY POINTS AND TECHNIQUES

• Advanced Pine Script Features:

• Multiple Nested Conditions: Uses nested conditions to assess complex market scenarios.

• Combination of Conditions: Combines multiple conditions to provide a more reliable signal.

• Optimization Techniques:

• Thresholds: Employs specific thresholds (0.04 and 0.03) to filter out noise and highlight significant market movements.

• SMA Comparisons: Compares multiple SMAs to identify trends and extreme conditions.

• Unique Approaches:

• Combining Multiple Time Frames: Incorporates multiple time frames to offer a holistic view of the market.

• Visual Distinction: Utilizes different colors and line widths to clearly differentiate between various extreme shadow conditions.

█ EXTENDED KNOWLEDGE AND APPLICATIONS

• Potential Modifications:

• User-Defined Thresholds: Allow users to customize thresholds to align with personal trading strategies.

• Additional Indicators: Integrate other technical indicators like RSI or MACD to improve the detection of extreme market conditions.

• Entry and Exit Signals: Enhance the script to generate clear buy and sell signals based on identified extreme shadow conditions.

• Application Scenarios:

• Volatility Analysis: Analyze market volatility and pinpoint times of extreme price action.

• Trend Following: Pair with trend-following strategies to capitalize on significant market moves.

• Risk Management: Adjust position sizes or stop-loss levels based on detected extreme conditions.

• Related Pine Script Concepts:

• Custom Functions: Demonstrates how to create reusable functions for simplified and organized code.

• Plotting Techniques: Shows effective ways to visualize data using color and styling options.

• Multiple Time Frame Analysis: Highlights the benefits of analyzing multiple time frames for a broader market understanding.

Prediction Based on Linreg & Atr

We created this algorithm with the goal of predicting future prices 📊, specifically where the value of any asset will go in the next 20 periods ⏳. It uses linear regression based on past prices, calculating a slope and an intercept to forecast future behavior 🔮. This prediction is then adjusted according to market volatility, measured by the ATR 📉, and the direction of trend signals, which are based on the MACD and moving averages 📈.

How Does the Linreg & ATR Prediction Work?

1. Trend Calculation and Signals:

o Technical Indicators: We use short- and long-term exponential moving averages (EMA), RSI, MACD, and Bollinger Bands 📊 to assess market direction and sentiment (not visually presented in the script).

o Calculation Functions: These include functions to calculate slope, average, intercept, standard deviation, and Pearson's R, which are crucial for regression analysis 📉.

2. Predicting Future Prices:

o Linear Regression: The algorithm calculates the slope, average, and intercept of past prices to create a regression channel 📈, helping to predict the range of future prices 🔮.

o Standard Deviation and Pearson's R: These metrics determine the strength of the regression 🔍.

3. Adjusting the Prediction:

o The predicted value is adjusted by considering market volatility (ATR 📉) and the direction of trend signals 🔮, ensuring that the prediction is aligned with the current market environment 🌍.

4. Visualization:

o Prediction Lines and Bands: The algorithm plots lines that display the predicted future price along with a prediction range (upper and lower bounds) 📉📈.

5. EMA Cross Signals:

o EMA Conditions and Total Score: A bullish crossover signal is generated when the total score is positive and the short EMA crosses above the long EMA 📈. A bearish crossover signal is generated when the total score is negative and the short EMA crosses below the long EMA 📉.

6. Additional Considerations:

o Multi-Timeframe Regression Channel: The script calculates regression channels for different timeframes (5m, 15m, 30m, 4h) ⏳, helping determine the overall market direction 📊 (not visually presented).

Confidence Interpretation:

• High Confidence (close to 100%): Indicates strong alignment between timeframes with a clear trend (bullish or bearish) 🔥.

• Low Confidence (close to 0%): Shows disagreement or weak signals between timeframes ⚠️.

Confidence complements the interpretation of the prediction range and expected direction 🔮, aiding in decision-making for market entry or exit 🚀.

Español

Creamos este algoritmo con el objetivo de predecir los precios futuros 📊, específicamente hacia dónde irá el valor de cualquier activo en los próximos 20 períodos ⏳. Utiliza regresión lineal basada en los precios pasados, calculando una pendiente y una intersección para prever el comportamiento futuro 🔮. Esta predicción se ajusta según la volatilidad del mercado, medida por el ATR 📉, y la dirección de las señales de tendencia, que se basan en el MACD y las medias móviles 📈.

¿Cómo Funciona la Predicción con Linreg & ATR?

Cálculo de Tendencias y Señales:

Indicadores Técnicos: Usamos medias móviles exponenciales (EMA) a corto y largo plazo, RSI, MACD y Bandas de Bollinger 📊 para evaluar la dirección y el sentimiento del mercado (no presentados visualmente en el script).

Funciones de Cálculo: Incluye funciones para calcular pendiente, media, intersección, desviación estándar y el coeficiente de correlación de Pearson, esenciales para el análisis de regresión 📉.

Predicción de Precios Futuros:

Regresión Lineal: El algoritmo calcula la pendiente, la media y la intersección de los precios pasados para crear un canal de regresión 📈, ayudando a predecir el rango de precios futuros 🔮.

Desviación Estándar y Pearson's R: Estas métricas determinan la fuerza de la regresión 🔍.

Ajuste de la Predicción:

El valor predicho se ajusta considerando la volatilidad del mercado (ATR 📉) y la dirección de las señales de tendencia 🔮, asegurando que la predicción esté alineada con el entorno actual del mercado 🌍.

Visualización:

Líneas y Bandas de Predicción: El algoritmo traza líneas que muestran el precio futuro predicho, junto con un rango de predicción (límites superior e inferior) 📉📈.

Señales de Cruce de EMAs:

Condiciones de EMAs y Puntaje Total: Se genera una señal de cruce alcista cuando el puntaje total es positivo y la EMA corta cruza por encima de la EMA larga 📈. Se genera una señal de cruce bajista cuando el puntaje total es negativo y la EMA corta cruza por debajo de la EMA larga 📉.

Consideraciones Adicionales:

Canal de Regresión Multi-Timeframe: El script calcula canales de regresión para diferentes marcos de tiempo (5m, 15m, 30m, 4h) ⏳, ayudando a determinar la dirección general del mercado 📊 (no presentado visualmente).

Interpretación de la Confianza:

Alta Confianza (cerca del 100%): Indica una fuerte alineación entre los marcos temporales con una tendencia clara (alcista o bajista) 🔥.

Baja Confianza (cerca del 0%): Muestra desacuerdo o señales débiles entre los marcos temporales ⚠️.

La confianza complementa la interpretación del rango de predicción y la dirección esperada 🔮, ayudando en las decisiones de entrada o salida en el mercado 🚀.

The Dragons Maw [inspired by Kioseff Trading]The Dragon's Maw is a playful visualization tool that uses Monte Carlo simulation to create a dragon-like pattern on your chart. Although primarily intended for entertainment, it is also suitable for testing or falsifying the utility of this method's predictions.

What It Does:

- Generates multiple price path simulations that form the shape of a "fire-breathing" effect

- Shows upper and lower boundaries of all simulations as the dragon's "maw"

- Displays the dragon's "eye" and "ear" as a visual indicator of the historical data used

How It Works:

1. The indicator calculates returns from historical price data

2. Using Monte Carlo simulation with either normal distribution or bootstrap sampling, it generates multiple potential price paths

3. These paths are rendered with high transparency to create a fire/smoke effect showing the higher probability regions as denser color

4. It can be observed that the direction of the "fire" is influenced by recent price movement especially when set in relation to the "eye" position which indicates the limit of historical data used for the simulation

Educational Value:

Use the 'Move to the Left' parameter to position the dragon's head at different points in historical data. This feature serves as an excellent demonstration of the limitations of statistical price projections – you'll quickly see how the simulated paths diverge from what actually happened, highlighting why such projections should not be relied upon for trading decisions.

You might find, that it's not at all capable of 'predicting' sudden price movements but rather 'predicts' a continuation of the recent trend.

Features:

- Adjustable number of simulations (affects detail of the "fire" effect)

- Moveable dragon head (can be positioned at different points in price history)

- Customizable colors for the maw boundaries and fire effect

- Optional scale display for price levels

Note: This indicator is inspired by KioseffTrading's original work, with added features for visualization and positioning. While it uses statistical methods, it should be viewed as an artistic interpretation of price movement rather than a predictive tool.

Settings Guide:

- Upper/Lower Limit: Colors for the dragon's maw boundaries

- Fire Color: Color and transparency of the simulation paths

- Look Back: How far back to calculate the dragon's eye position

- Much Fire: Controls the density of simulation paths

- Length: Determines how far forward the simulation extends

The chart shows a clean view of the indicator's output, with the dragon's eye (o), ear, maw boundaries, and fire effect clearly visible on the right side of the chart by default.

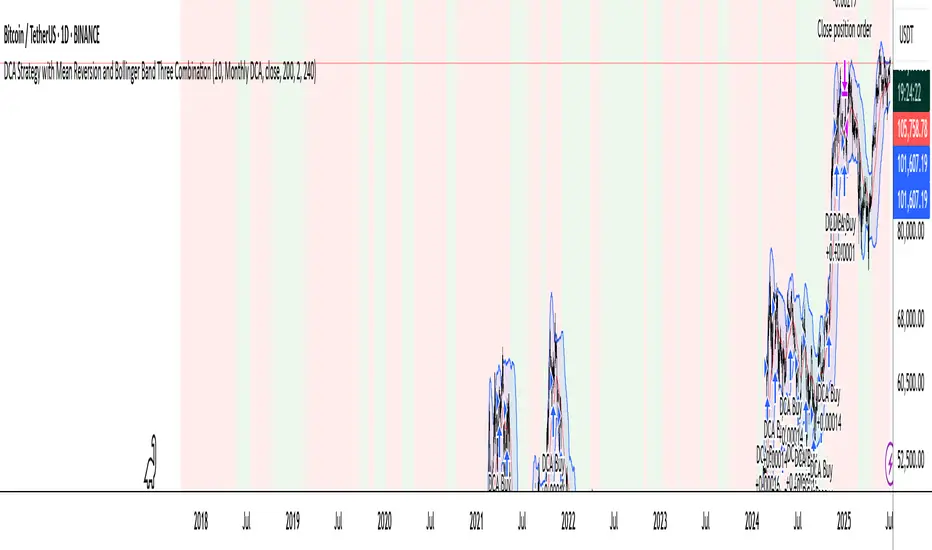

Overnight Effect High Volatility Crypto (AiBitcoinTrend)👽 Overview of the Strategy

This strategy leverages the overnight effect in the cryptocurrency market, specifically targeting the two-hour window from 21:00 UTC to 23:00 UTC. The strategy is designed to be applied only during periods of high volatility, which is determined using historical volatility data. This approach, inspired by research from Padyšák and Vojtko (2022), aims to capitalize on statistically significant return patterns observed during these hours.

Deep Backtesting with a High Volatility Filter

Deep Backtesting without a High Volatility Filter

👽 How the Strategy Works

Volatility Calculation:

Each day at 00:00 UTC, the strategy calculates the 30-day historical volatility of crypto returns (typically Bitcoin). The historical volatility is the standard deviation of the log returns over the past 30 days, representing the market's recent volatility level.

Median Volatility Benchmark:

The median of the 30-day historical volatility is calculated over a 365-day period (one year). This median acts as a benchmark to classify each day as either:

👾 High Volatility: When the current 30-day volatility exceeds the median volatility.

👾 Low Volatility: When the current 30-day volatility is below the median.

Trading Rule:

If the day is classified as a High Volatility Day, the strategy executes the following trades:

👾 Buy at 21:00 UTC.

👾 Sell at 23:00 UTC.

Trade Execution Details:

The strategy uses a 0.02% fee per trade.

Each trade is executed with 25% of the available capital. This allocation helps manage risk while allowing for compounding returns.

Rationale:

The returns during the 22:00 and 23:00 UTC hours have been found to be statistically significant during high volatility periods. The overnight effect is believed to drive this phenomenon due to the asynchronous closing hours of global financial markets. This creates unique trading opportunities in the cryptocurrency market, where exchanges remain open 24/7.

👽 Market Context and Global Time Zone Impact

👾 Why 21:00 to 23:00 UTC?

During this window, major traditional financial markets are closed:

NYSE (New York) closes at 21:00 UTC.

London and European markets are closed during these hours.

Asian markets (Tokyo, Hong Kong, etc.) open later, leaving this window largely unaffected by traditional trading flows.

This global market inactivity creates a period where significant moves can occur in the cryptocurrency market, particularly during high volatility.

👽 Strategy Parameters

Volatility Period: 30 days.

The lookback period for calculating historical volatility.

Median Period: 365 days.

The lookback period for calculating the median volatility benchmark.

Entry Time: 21:00 UTC.

Adjust this to your local time if necessary (e.g., 16:00 in New York, 22:00 in Stockholm).

Exit Time: 23:00 UTC.

Adjust this to your local time if necessary (e.g., 18:00 in New York, 00:00 midnight in Stockholm).

👽 Benefits of the Strategy

Seasonality Effect:

The strategy captures consistent patterns driven by the overnight effect and high volatility periods.

Risk Reduction:

Since trades are executed during a specific window and only on high volatility days, the strategy helps mitigate exposure to broader market risk.

Simplicity and Efficiency:

The strategy is moderately complex, making it accessible for traders while offering significant returns.

Global Applicability:

Suitable for traders worldwide, with clear guidelines on adjusting for local time zones.

👽 Considerations

Market Conditions: The strategy works best in a high-volatility environment.

Execution: Requires precise timing to enter and exit trades at the specified hours.

Time Zone Adjustments: Ensure you convert UTC times accurately based on your location to execute trades at the correct local times.

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

VWAP Trend with Standard Deviation & MidlinesThis indicator is a sophisticated VWAP (Volume Weighted Average Price) tool with multiple features:

Core Functionality:

1. Calculates a primary VWAP line that changes color based on trend direction (green when rising, red when falling)

2. Creates multiple standard deviation bands around the VWAP at customizable distances

3. Resets calculations at either:

- New York session start time (configurable, default 9:30 AM)

- Daily start time

- Can be hidden on daily/weekly/monthly timeframes if desired

Band Structure:

- Band 1 (innermost): ±1 standard deviation

- Band 2 (middle): ±2 standard deviations

- Band 3 (outermost): ±3 standard deviations

- Midlines at 0.5σ intervals between bands

- All bands can be individually enabled/disabled

Customization Options:

1. Band calculation modes:

- Standard Deviation based

- Percentage based

2. Visual settings:

- Customizable colors for all elements

- Adjustable line widths

- Optional labels with configurable size

- Optional extension lines

- Label position adjustment

3. Source data selection (default: HLC3 - High, Low, Close average)

Common Uses:

- Identifying potential support/resistance levels

- Measuring price volatility

- Spotting mean reversion opportunities

- Trading range analysis

- Trend direction confirmation

The indicator essentially creates a dynamic support/resistance structure that adapts to market volatility and volume, making it useful for both intraday and swing trading strategies.

300-Candle Weighted Average Zones w/50 EMA SignalsThis indicator is designed to deliver a more nuanced view of price dynamics by combining a custom, weighted price average with a volatility-based zone and a trend filter (in this case, a 50-period exponential moving average). The core concept revolves around capturing the overall price level over a relatively large lookback window (300 candles) but with an intentional bias toward recent market activity (the most recent 20 candles), thereby offering a balance between long-term context and short-term responsiveness. By smoothing this weighted average and establishing a “zone” of standard deviation bands around it, the indicator provides a refined visualization of both average price and its recent volatility envelope. Traders can then look for confluence with a standard trend filter, such as the 50 EMA, to identify meaningful crossover signals that may represent trend shifts or opportunities for entry and exit.

What the Indicator Does:

Weighted Price Average:

Instead of using a simple or exponential moving average, this indicator calculates a custom weighted average price over the past 300 candles. Most historical candles receive a base weight of 1.0, but the most recent 20 candles are assigned a higher weight (for example, a weight of 2.0). This weighting scheme ensures that the calculation is not simply a static lookback average; it actively emphasizes current market conditions. The effect is to generate an average line that is more sensitive to the most recent price swings while still maintaining the historical context of the previous 280 candles.

Smoothing of the Weighted Average:

Once the raw weighted average is computed, an exponential smoothing function (EMA) is applied to reduce noise and produce a cleaner, more stable average line. This smoothing helps traders avoid reacting prematurely to minor price fluctuations. By stabilizing the average line, traders can more confidently identify actual shifts in market direction.

Volatility Zone via Standard Deviation Bands:

To contextualize how far price can deviate from this weighted average, the indicator uses standard deviation. Standard deviation is a statistical measure of volatility—how spread out the price values are around the mean. By adding and subtracting one standard deviation from the smoothed weighted average, the indicator plots an upper band and a lower band, creating a zone or channel. The area between these bands is filled, often with a semi-transparent color, highlighting a volatility corridor within which price and the EMA might oscillate.

This zone is invaluable in visualizing “normal” price behavior. When the 50 EMA line and the weighted average line are both within this volatility zone, it indicates that the market’s short- to mid-term trend and its average pricing are aligned well within typical volatility bounds.

Incorporation of a 50-Period EMA:

The inclusion of a commonly used trend filter, the 50 EMA, adds another layer of context to the analysis. The 50 EMA, being a widely recognized moving average length, is often considered a baseline for intermediate trend bias. It reacts faster than a long-term average (like a 200 EMA) but is still stable enough to filter out the market “chop” seen in very short-term averages.

By overlaying the 50 EMA on this custom weighted average and the surrounding volatility zone, the trader gains a dual-dimensional perspective:

Trend Direction: If the 50 EMA is generally above the weighted average, the short-term trend is gaining bullish momentum; if it’s below, the short-term trend has a bearish tilt.

Volatility Normalization: The bands, constructed from standard deviations, provide a sense of whether the price and the 50 EMA are operating within a statistically “normal” range. If the EMA crosses the weighted average within this zone, it signals a potential trend initiation or meaningful shift, as opposed to a random price spike outside normal volatility boundaries.

Why a Trader Would Want to Use This Indicator:

Contextualized Price Level:

Standard MAs may not fully incorporate the most recent price dynamics in a large lookback window. By weighting the most recent candles more heavily, this indicator ensures that the trader is always anchored to what the market is currently doing, not just what it did 100 or 200 candles ago.

Reduced Whipsaw with Smoothing:

The smoothed weighted average line reduces noise, helping traders filter out inconsequential price movements. This makes it easier to spot genuine changes in trend or sentiment.

Visual Volatility Gauge:

The standard deviation bands create a visual representation of “normal” price movement. Traders can quickly assess if a breakout or breakdown is statistically significant or just another oscillation within the expected volatility range.

Clear Trade Signals with Confirmation:

By integrating the 50 EMA and designing signals that trigger only when the 50 EMA crosses above or below the weighted average while inside the zone, the indicator provides a refined entry/exit criterion. This avoids chasing breakouts that occur in abnormal volatility conditions and focuses on those crossovers likely to have staying power.

How to Use It in an Example Strategy:

Imagine you are a swing trader looking to identify medium-term trend changes. You apply this indicator to a chart of a popular currency pair or a leading tech stock. Over the past few days, the 50 EMA has been meandering around the weighted average line, both confined within the standard deviation zone.

Bullish Example:

Suddenly, the 50 EMA crosses decisively above the weighted average line while both are still hovering within the volatility zone. This might be your cue: you interpret this crossover as the 50 EMA acknowledging the recent upward shift in price dynamics that the weighted average has highlighted. Since it occurred inside the normal volatility range, it’s less likely to be a head-fake. You place a long position, setting an initial stop just below the lower band to protect against volatility.

If the price continues to rise and the EMA stays above the average, you have confirmation to hold the trade. As the price moves higher, the weighted average may follow, reinforcing your bullish stance.

Bearish Example:

On the flip side, if the 50 EMA crosses below the weighted average line within the zone, it suggests a subtle but meaningful change in trend direction to the downside. You might short the asset, placing your protective stop just above the upper band, expecting that the statistically “normal” level of volatility will contain the price action. If the price does break above those bands later, it’s a sign your trade may not work out as planned.

Other Indicators for Confluence:

To strengthen the reliability of the signals generated by this weighted average zone approach, traders may want to combine it with other technical studies:

Volume Indicators (e.g., Volume Profile, OBV):

Confirm that the trend crossover inside the volatility zone is supported by volume. For instance, an uptrend crossover combined with increasing On-Balance Volume (OBV) or volume spikes on up candles signals stronger buying pressure behind the price action.

Momentum Oscillators (e.g., RSI, Stochastics):

Before taking a crossover signal, check if the RSI is above 50 and rising for bullish entries, or if the Stochastics have turned down from overbought levels for bearish entries. Momentum confirmation can help ensure that the trend change is not just an isolated random event.

Market Structure Tools (e.g., Pivot Points, Swing High/Low Analysis):

Identify if the crossover event coincides with a break of a previous pivot high or low. A bullish crossover inside the zone aligned with a break above a recent swing high adds further strength to your conviction. Conversely, a bearish crossover confirmed by a breakdown below a previous swing low can make a short trade setup more compelling.

Volume-Weighted Average Price (VWAP):

Comparing where the weighted average zone lies relative to VWAP can provide institutional insight. If the bullish crossover happens while the price is also holding above VWAP, it can mean that the average participant in the market is in profit and that the trend is likely supported by strong hands.

This indicator serves as a tool to balance long-term perspective, short-term adaptability, and volatility normalization. It can be a valuable addition to a trader’s toolkit, offering enhanced clarity and precision in detecting meaningful shifts in trend, especially when combined with other technical indicators and robust risk management principles.

Implied Leverage Ratio Between Current Symbol and BTCThis script calculates and visualizes the implied leverage ratio between the current symbol and Bitcoin (BTC). The implied leverage ratio is computed by comparing the cumulative price changes of the two symbols over a defined number of candles. The results provide insights into how the current symbol performs relative to BTC in terms of bullish (upward) and bearish (downward) movements.

Features

Cumulative Up and Down Ratios:

The script calculates the cumulative price increase (up) and decrease (down) ratios for both the current symbol and BTC. These ratios are based on the percentage changes relative to each candle's opening price.

Implied Leverage Ratio:

For bullish movements, the cumulative up ratio of the current symbol is divided by BTC's cumulative up ratio.

For bearish movements, the cumulative down ratio of the current symbol is divided by BTC's cumulative down ratio.

These values reflect the implied leverage of the current symbol relative to BTC in both directions.

Customizable Comparison Symbol:

By default, the script compares the current symbol to BINANCE:BTCUSDT. However, you can specify any other symbol to tailor the analysis.

Interactive Visualization:

Green Line: Represents the ratio of cumulative up movements (current symbol vs. BTC).

Red Line: Represents the ratio of cumulative down movements (current symbol vs. BTC).

A horizontal zero line is included for reference, ensuring the chart always starts from zero.

How to Use

Add this script to your chart from the Pine Editor or the public library.

Customize the number of candles (t) to define the period over which cumulative changes are calculated.

If desired, replace the comparison symbol with another asset in the input settings.

Analyze the green and red lines to identify relative strength and implied leverage trends.

Who Can Benefit

Traders and Analysts: Gain insights into the relative performance of altcoins, stocks, or other instruments against BTC.

Leverage Seekers: Identify assets with higher or lower implied leverage compared to Bitcoin.

Market Comparisons: Understand how various assets react to market movements relative to BTC.

This tool is particularly useful for identifying potential outperformers or underperformers relative to Bitcoin and can guide strategic decisions in trading pairs or market analysis.

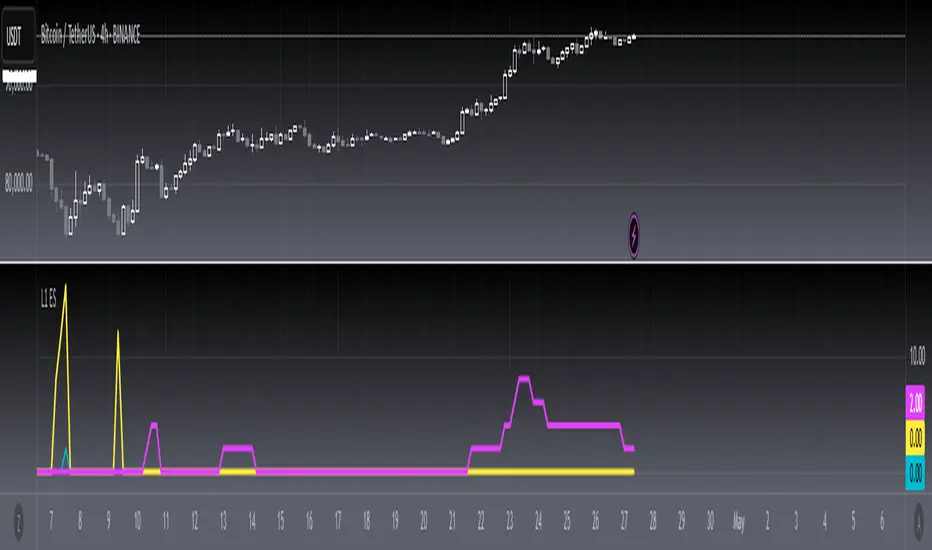

[blackcat] L1 Banker Move█ OVERVIEW

The Pine Script is an indicator designed to analyze market signals for institutional and short-term investors. It calculates and plots three main signals: Institutional Signal, Institutional Build, and Short-Term Investor Signal. The script uses a combination of price, volume, and moving average data to generate these signals, which can help traders identify potential buying or selling opportunities.

█ LOGICAL FRAMEWORK

The script is structured into several main sections:

1 — Input Parameters

The script does not explicitly define any input parameters, relying on default values for calculations.

2 — Custom Functions

• reference_value(values, length) : Retrieves the first non-NA value from a specified number of past values.

• calculate_institutional_and_short_term_signals(low, close, open, volume) : Calculates the institutional and short-term investor signals based on price, volume, and moving average data.

3 — Calculations

• Price and Volume Metrics: The script calculates various smoothed price changes, lowest and highest values over different periods, and volume-weighted prices.

• Moving Averages: It computes simple moving averages (SMA) and exponential moving averages (EMA) for different periods.

• RSI Calculation: The script calculates a custom RSI for different periods.

• Signal Generation: It generates the institutional and short-term investor signals based on the calculated metrics.

4 — Plotting

The script plots the three main signals on the chart using the plot function.

The flow of data and logic is as follows:

• The reference_value function is used to find reference values for calculations.

• The calculate_institutional_and_short_term_signals function performs the core calculations and returns the institutional and short-term investor signals.

• The main script calls this function and plots the results.

█ CUSTOM FUNCTIONS

1 — reference_value(values, length)

• Purpose : Retrieves the first non-NA value from a specified number of past values.

• Parameters :

• values: An array of values.

• length: The number of past values to consider.

• Return Value : The first non-NA value found or na if no valid value is found.

• Functionality : Iterates through the specified number of past values and returns the first non-NA value.

2 — calculate_institutional_and_short_term_signals(low, close, open, volume)

• Purpose : Calculates the institutional and short-term investor signals based on price, volume, and moving average data.

• Parameters :

• low: Low price series.

• close: Close price series.

• open: Open price series.

• volume: Volume series.

• Return Values :

• institutional_signal: The institutional signal.

• institutional_build: The institutional build signal.

• short_term_investor_signal: The short-term investor signal.

• Functionality :

• Computes various price and volume metrics.

• Calculates moving averages and volume-weighted prices.

• Generates the institutional and short-term investor signals based on these metrics.

█ KEY POINTS AND TECHNIQUES

1 — Advanced Pine Script Features

• Custom Functions: The script defines and uses custom functions to encapsulate complex logic.

• Conditional Statements: Extensive use of iff and if statements to control the flow of calculations.

• Looping Constructs: The for loop in reference_value function to iterate through past values.

• Exponential Moving Averages (EMA): Used to smooth out price and signal changes.

• Volume-Weighted Price (VWP): Calculated to factor in volume in price analysis.

• Custom RSI Calculation: A custom RSI formula is used, which differs from the standard RSI calculation.

2 — Optimization Techniques

• Efficient Data Handling: The reference_value function efficiently finds the first non-NA value without unnecessary computations.

• Smoothed Signals: Using EMAs to smooth out noisy signals for better trend identification.

3 — Unique Approaches

• Combination of Metrics: The script combines multiple metrics (price, volume, moving averages, and custom RSI) to generate comprehensive signals.

• Institutional Build Signal: A unique approach to detect institutional activity by comparing current price levels with historical lows and smoothed price changes.

█ EXTENDED KNOWLEDGE AND APPLICATIONS

1 — Potential Modifications

• Input Parameters: Add input parameters to allow users to customize the lengths and thresholds used in the calculations.

• Strategy Version: Convert the indicator into a strategy by adding buy/sell signals based on the generated signals.

• Additional Indicators: Integrate other technical indicators (e.g., MACD, Bollinger Bands) to enhance the signal generation process.

2 — Similar Trading Scenarios

• Institutional Activity Analysis: Use similar techniques to analyze institutional activity in other markets or assets.

• Volume Analysis: Apply the volume-weighted price and volume analysis to identify significant price movements.

• Multi-Timeframe Analysis: Extend the script to analyze signals across multiple timeframes for a more robust trading strategy.

3 — Related Pine Script Concepts

• Pine Script Functions: Understanding how to define and use custom functions effectively.

• Conditional Logic: Mastering the use of iff and if statements for complex logic.

• Looping Constructs: Familiarity with for loops for iterating through data.

• Moving Averages: Knowledge of different types of moving averages and their applications.

• Volume Analysis: Techniques for incorporating volume data into price analysis.

Shannon Entropy Volatility AnalyzerThis algorithm aims to measure market uncertainty or volatility using a Shannon entropy-based approach. 🔄📊

Entropy is a measure of disorder or unpredictability, and here we use it to evaluate the structure of price returns within a defined range of periods (window length). 🧩⏳ Thus, the goal is to detect changes to identify conditions of high or low volatility. 🔍⚡

What we seek with Shannon's formula in this algorithm is to measure market uncertainty or volatility through dynamic entropy. This measure helps us understand how unpredictable price behavior is over a given period, which is key to making informed decisions. 📈🧠

Through this formula, we calculate the level of disorder or dispersion in price returns based on their probability of occurrence, enabling us to identify moments of high or low volatility. 💡💥

Shannon Entropy Calculation 📏

• Uses probabilities to measure uncertainty in returns. 🎲

• Entropy is normalized on a scale of 0 to 100, where:

o High Entropy: Unpredictable movements (high uncertainty). ⚠️💥

•

o Low Entropy: Structured movements (low uncertainty). 📉🔒

•

• With probabilities, we measure the level of dispersion or unpredictability of returns using Shannon's entropy formula. 📊🔍

________________________________________

Indicator Usefulness 🛠️

• Identify High Volatility: When the market is unpredictable, the indicator signals "High Uncertainty." ⚡🔮

• Detect Market Stability: When the market is more predictable and structured, the indicator highlights "Low Uncertainty." 🔒🧘♂️

• Neutral Zones: Helps monitor markets without extreme conditions, enabling safer entry or exit opportunities. ⚖️🚶♂️

________________________________________

Uncertainty Zones 🌀

1. High Uncertainty: When entropy exceeds the upper threshold. 🚨🔺

2. Low Uncertainty: When entropy is below the lower threshold. 🔻💡

3. Neutral: When entropy lies between both thresholds. ⚖️🔄

________________________________________

What We Aim to Achieve with the Formula in Practice 🎯

1. Detection of Volatile Moments: Shannon’s formula helps us identify when the market is unpredictable. This is a good moment to take additional precautions, such as reducing position size or avoiding trading during high volatility phases. ⚠️📉

2. Trading Opportunities in Stable Markets: With low entropy, we can identify when the market is more predictable, favoring trend or momentum strategies with a higher chance of success. 🚀📈

3. Optimization of Risk Management: By measuring market volatility in real-time, we can adjust entry and exit strategies, tailoring risk based on the level of uncertainty detected. 🔄⚖️

________________________________________

We hope this makes it easy to interpret and use. If you have any questions or comments, please feel free to reach out to us! 📬😊

Custom EMA (v4) [MacroGlide]Custom EMA (v4) is an easy-to-use tool designed for traders who want a clear and reliable way to analyze market trends. By using multiple Exponential Moving Averages (EMAs), this indicator helps you visualize the market's direction and momentum in a straightforward way. Whether you're tracking short-term movements or looking for long-term patterns, Custom EMA makes it simple to spot trends and trading opportunities.

Key Features:

• Multi-EMA System: Plots up to four EMAs on the chart with customizable lengths and colors, providing flexibility to analyze trends over different timeframes.

• Dynamic Trend Cloud: A visually intuitive cloud is generated between the fastest and slowest EMA. The cloud changes color based on market trends:

• Green Cloud: Indicates a bullish trend when shorter EMAs are above longer EMAs.

• Red Cloud: Indicates a bearish trend when shorter EMAs are below longer EMAs.

• Highlighting Zones: Background shading helps distinguish bullish and bearish conditions, further clarifying the prevailing trend in the market.

How to Use:

• Add the Indicator: Load the indicator onto your chart and customize the EMA lengths to suit your trading style.

• Interpret the Cloud: Observe the color of the trend cloud to identify bullish (green) or bearish (red) market conditions.