Price Filter [AstrideUnicorn]The indicator calculates a fast price filter based on the closing price of the underlying asset. Overall, it is intended to provide a fast, reliable way to detect trend direction and confirm trend strength, using statistical measures of price movements.

The algorithm was adapted from Marcus Schmidberger's (2018) article "High Frequency Trading with the MSCI World ETF". It demeans the price time series using the long-term average and then normalizes it with the long-term standard deviation. The resulting time series is then compared to specified thresholds to determine the trend direction.

HOW TO USE

The indicator surface is colored green if the price is trending upwards and red if the price is trending downwards. If the indicator outline is the opposite color of the indicator surface, it indicates that the price is moving against the trend and the current trend may be losing strength.

If the 'Use threshold' setting is enabled, the indicator will be colored blue if its value is within the range defined by the upper and lower thresholds. This indicates that the price is trending sideways, or that the current trend is losing strength.

SETTNGS

Length - the length of the long-term average used to calculate the price filter. Recommended range 20 - 200. The sensitivity of the indicator increases as the value becomes smaller, allowing it to detect smaller price moves and swings earlier.

Threshold - the threshold value used to detect trend direction.

Use threshold - a boolean (true/false) input that determines whether to use the threshold value for confirmation.

Trend

Slope NormalizerBrief:

This oscillator style indicator takes another indicator as its source and measures the change over time (the slope). It then isolates the positive slope values from the negative slope values to determine a 'normal' slope value for each.

** A 'normal' value of 1.0 is determined by the average slope plus the standard deviation of that slope.

The Scale

This indicator is not perfectly linear. The values are interpolated differently from 0.0 - 1.0 than values greater than 1.0.

From values 0.0 to 1.0 (positive or negative): it means that the value of the slope is less than 'normal' **.

Any value above 1.0 means the current slope is greater than 'normal' **.

A value of 2.0 means the value is the average plus 2x the standard deviation.

A value of 3.0 means the value is the average plus 3x the standard deviation.

A value greater than 4.0 means the value is greater than the average plus 4x the standard deviation.

Because the slope value is normalized, the meaning of these values can remain generally the same for different symbols.

Potential Usage Examples/b]

Using this in conjunction with an SMA or WMA may indicate a change in trend, or a change in trend-strength.

Any values greater than 4 indicate a very strong (and unusual) trend that may not likely be sustainable.

Any values cycling between +1.0 and -1.0 may mean indecision.

A value that is decreasing below 0.5 may predict a change in trend (slope may soon invert).

Musashi_Fractal_Dimension === Musashi-Fractal-Dimension ===

This tool is part of my research on the fractal nature of the markets and understanding the relation between fractal dimension and chaos theory.

To take full advantage of this indicator, you need to incorporate some principles and concepts:

- Traditional Technical Analysis is linear and Euclidean, which makes very difficult its modeling.

- Linear techniques cannot quantify non-linear behavior

- Is it possible to measure accurately a wave or the surface of a mountain with a simple ruler?

- Fractals quantify what Euclidean Geometry can’t, they measure chaos, as they identify order in apparent randomness.

- Remember: Chaos is order disguised as randomness.

- Chaos is the study of unstable aperiodic behavior in deterministic non-linear dynamic systems

- Order and randomness can coexist, allowing predictability.

- There is a reason why Fractal Dimension was invented, we had no way of measuring fractal-based structures.

- Benoit Mandelbrot used to explain it by asking: How do we measure the coast of Great Britain?

- An easy way of getting the need of a dimension in between is looking at the Koch snowflake.

- Market prices tend to seek natural levels of ranges of balance. These levels can be described as attractors and are determinant.

Fractal Dimension Index ('FDI')

Determines the persistence or anti-persistence of a market.

- A persistent market follows a market trend. An anti-persistent market results in substantial volatility around the trend (with a low r2), and is more vulnerable to price reversals

- An easy way to see this is to think that fractal dimension measures what is in between mainstream dimensions. These are:

- One dimension: a line

- Two dimensions: a square

- Three dimensions: a cube.

--> This will hint you that at certain moment, if the market has a Fractal Dimension of 1.25 (which is low), the market is behaving more “line-like”, while if the market has a high Fractal Dimension, it could be interpreted as “square-like”.

- 'FDI' is trend agnostic, which means that doesn't consider trend. This makes it super useful as gives you clean information about the market without trying to include trend stuff.

Question: If we have a game where you must choose between two options.

1. a horizontal line

2. a vertical line.

Each iteration a Horizontal Line or a Square will appear as continuation of a figure. If it that iteration shows a square and you bet vertical you win, same as if it is horizontal and it is a line.

- Wouldn’t be useful to know that Fractal dimension is 1.8? This will hint square. In the markets you can use 'FD' to filter mean-reversal signals like Bollinger bands, stochastics, Regular RSI divergences, etc.

- Wouldn’t be useful to know that Fractal dimension is 1.2? This will hint Line. In the markets you can use 'FD' to confirm trend following strategies like Moving averages, MACD, Hidden RSI divergences.

Calculation method:

Fractal dimension is obtained from the ‘hurst exponent’.

'FDI' = 2 - 'Hurst Exponent'

Musashi version of the Classic 'OG' Fractal Dimension Index ('FDI')

- By default, you get 3 fast 'FDI's (11,12,13) + 1 Slow 'FDI' (21), their interaction gives useful information.

- Fast 'FDI' cross will give you gray or red dots while Slow 'FDI' cross with the slowest of the fast 'FDI's will give white and orange dots. This are great to early spot trend beginnings or trend ends.

- A baseline (purple) is also provided, this is calculated using a 21 period Bollinger bands with 1.618 'SD', once calculated, you just take midpoint, this is the 'TDI's (Traders Dynamic Index) way. The indicator will print purple dots when Slow 'FDI' and baseline crosses, I see them as Short-Term cycle changes.

- Negative slope 'FDI' means trending asset.

- Positive most of the times hints correction, but if it got overextended it might hint a rocket-shot.

TDI Ranges:

- 'FDI' between 1.0≤ 'FDI' ≤1.4 will confirm trend following continuation signals.

- 'FDI' between 1.6≥ 'FDI' ≥2.0 will confirm reversal signals.

- 'FDI' == 1.5 hints a random unpredictable market.

Fractal Attractors

- As you must know, fractals tend orbit certain spots, this are named Attractors, this happens with any fractal behavior. The market of course also shows them, in form of Support & Resistance, Supply Demand, etc. It’s obvious they are there, but now we understand that they’re not linear, as the market is fractal, so simple trendline might not be the best tool to model this.

- I’ve noticed that when the Musashi version of the 'FDI' indicator start making a cluster of multicolor dots, this end up being an attractor, I tend to draw a rectangle as that area as price tend to come back (I still researching here).

Extra useful stuff

- Momentum / speed: Included by checking RSI Study in the indicator properties. This will add two RSI’s (9 and a 7 periods) plus a baseline calculated same way as explained for 'FDI'. This gives accurate short-term trends. It also includes RSI divergences (regular and hidden), deactivate with a simple check in the RSI section of the properties.

- BBWP (Bollinger Bands with Percentile): Efficient way of visualizing volatility as the percentile of Bollinger bands expansion. This line varies color from Iced blue when low volatility and magma red when high. By default, comes with the High vols deactivated for better view of 'FDI' and RSI while all studies are included. DDWP is trend agnostic, just like 'FDI', which make it very clean at providing information.

- Ultra Slow 'FDI': I noticed that while using BBWP and RSI, the indicator gets overcrowded, so there is the possibility of adding only one 'FDI' + its baseline.

Final Note: I’ve shown you few ways of using this indicator, please backtest before using in real trading. As you know trading is more about risk and trade management than the strategy used. This still a work in progress, I really hope you find value out of it. I use it combination with a tool named “Musashi_Katana” (also found in TradingView).

Best!

Musashi

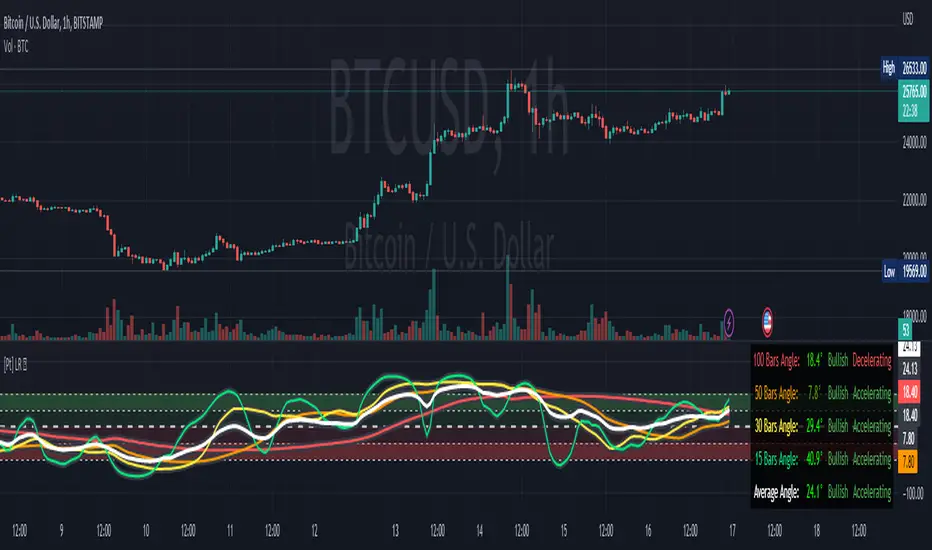

Linear Regression AngleThere are several Linear Regression indicator in the Public Library, but I don't think there is one that converts the Linear Regression (LR) curve into angle in degrees, relative to a set reference frame. Due to the large price range between tickers, creating this indicator isn't as straight forward as I originally thought. For example, given the same time period, a stock that fluctuate in the 10's will have a true linear regression angle dramatically different from a penny stock. Even changing the scale on your chart will affect the "apparent" angle you see on the chart. Hence, this indicator DOES NOT provide the true linear regression angle, but only a relative one based on a defined number of historical bars.

Originality and usefulness

This indicator provides Linear Regression (LR) Angle in degree that may be more easily interpreted by some traders as we are more accustomed to line angles in degree and know how to visualize them.

This script also provides the option to overlay up to four LR curves of different periods, as well as an average curve of the enabled curves. This allows traders to analysis short to long term trends.

Furthermore, slope (rate of change) of each LR curves can be toggled. The slope plot can help traders visualize accelerations and decelerations of the LR curves which may help in spotting trend reversals.

Data table provides real time data for each curve.

Example of using slope plot with a 30 bars Linear Regression Angle:

MAGIC MACDMAGIC MACD ( MACD Indicator with Trend Filter and EMA Crossover confirmation and Momentum). This MACD uses Default Trading view MACD

from Technical indicators library and adding a second MACD along with 3 EMA's to detect Trend and confirm MACD Signal.

Eliminates usage of 3different indicators (Default MACD , MACD-2,EMA5, EMA20, EMA50)

Basic IDEA.

Idea is to filter Histogram when price is above or below 50EMA. Similar to QQE -mod oscillator but Has a EMA Filter

1.Take DEFAULT MACD crossover signals with lower period

2.check with a Higher MACD Histogram.

3.Enter upon EMA crossover signal and Histogram confirmation.

Histogram changes to GRAY when price is below EMA 50 or above EMA 50 (Follows Trend)

4.Exit on next Default MACD crossover signal.

Overview :

Moving Average Convergence Divergence Indicator Popularly Known as MACD is widely used. MACD Usually generates a lots of False signals

and noise in Lower Time Frames, making it difficult to enter a trade in sideways market. Divergence is a major issue along with sideways

movement and tangling of MACD and Signal Lines. There is no way to confirm a Default MACD signal, except to switch time frames and

verify.

Magic MACD Can be used to in combination with other signals.

This MACD uses two MACD Signals to verify the signal given by Default MACD . The Histogram Plot shown is of a higher period

MACD (close,5,50,30) values. When a signal is generated on a lower MACD it is verified by the histogram with higher time period.

Technicals Used:

1. Lower MACD-1 values 12,26 and signal-9 (crossover Signals)

2. Higher MACD-2 values 5,50 and signal-30 (Histogram)

3. EMA 50 (Histogram Filter to allow only if price above or below Ema 50)

4. EMA 5 and EMA 20 for crossover confirmation of trend

What's is in this Indicator?

1.Histogram-(higher period 5,50 and 30signal)

2. MACD crossover Signals-(lower period Default MACD setting)

3.Signal Lines-( EMA 5 & 20)

Implemented & Removed in this Indicator

1. Default MACD and Signal Lines are removed completely

2. MACD crossover are taken on lower periods and plotted as signals(Blue Triangle or Red Triangle)

3. Histogram is plotted from a higher Period providing a clear picture with Higher Time period

4. EMA 5 and EMA 20 are used for MACD signal confirmation

How to use?

Up Signal

1. MACD Default (12,26,30) up signals are shown in Blue

2. Wait till the Histogram changes Blue

3. Look for EMA signals crossover near by

Down Signal

1. MACD Default (12,26,30) up signals are shown in Red

2. Wait till the Histogram changes Red

3. Look for EMA signals crossover near by

Do's

Consider only opposite color as signals

1. Red Triangle on Blue Histogram(likely to move down direction)

2. Blue Triangle on Red Histogram (Likely to move up direction)

Don'ts

1.Ignore Blue Signal on Blue Histogram (pull back signals can be used to enter trade if you miss first crossover)

2.Ignore Red Signal on Red Histogram(pull back signals can be used to enter trade if you miss first crossover)

3.Ignore Up and Down signals till Gray or Blacked out area is finished in Histogram

Tips:

1. EMA plot also shows pull back areas along with signals

2.side by side opposite signals shows sides ways movement

3. EMA 5,20 is plotted on MACD Histogram for Additional Benefit

Thanks & Credits

To Tradingview Team for allowing me to use their default MACD version and coding it in to a MAGIC MACD by adding a few lines of code that

makes it more enhanced.

Warning...!

This is purely for Educational purpose only. Not to be used as a stand alone indicator. Usage is at your own Risk. Please get familiar with its working before implementing. Its not a Financial Advice or Suggestion . Any losses or gains is at your own risk.

Trend Finder with Coefficient of VariationCoefficient of variation (“COV”) is a statistical measure used to describe the variability of values within a data set, it’s calculated by taking the standard deviation divided by the mean.

Traditionally, COV is applied to the expected returns of competing investment portfolios. A risk adverse investor prefers to accept a portfolio with a relatively lower COV value.

On the other hand, when applying COV to price charts, the difference is that instead of looking at expected returns, we now treat price as the source of data. We look at price from a moving average perspective. This script purely focuses on price.

What this indicator does:

Firstly, to go over the parameters:

Let ‘n’ be the lookback period for computing COV, and ‘m’ be the period for comparing the ranking of COVs.

Logics in a nutshell:

This program will (A) calculate the COV by dividing the moving standard deviation by moving average over ‘n’ bars, and then (B) illustrate the relationship of how COV at each bar ranks compared to COVs over past ‘m’ bars. We use a color scale (default black and yellow) for visualizing ranking in terms of percentiles. If COV is below its median value, then we assume that price is consolidating.

Hypothesis:

Using COV on top of regular SMA signals should reduce a lot of unwanted noise such as consecutive crossovers during ranging-periods. Traders want volatility, but not too much of it when sniping for entry opportunities (speaking of initial position; need to add to winning positions after, but this is for another topic). For this reason, the median value of COV is suitable as a metric for signals.

Applications:

We use the median value of COV to form a decision rule. A signal is generated when COV > median(COV,m), and the direction of trend is determined based on relative position of price with respect to sma(price,n). When the value of COV is increasing, it can also be thought of seeing Bollinger Bands beginning to bulge. When trends begin, this program will plot triangles to signify entry opportunities.

Immediate Trend - VHXIMMEDIATE TREND - VULNERABLE_HUMAN_X

This indicator is used to identify the immediate trend in the market.

When a Short Term High (STH) is engulfed and closed above, we consider that as a bullish trend.

And Similarly, when a Short Term Low (STL) is engulfed and closed below, we consider that as a bullish trend.

STH - A candle that is higher than the one candle towards it's left and one candle towards it's right.

STL - A candle that is lower than the one candle towards it's left and one candle towards it's right.

HOW TO USE:

1. Do not take trades purely based on the immediate trend showcased by the indicator. Rather, use them as confluence with your trading strategy.

2. When you are expecting price to reverse at your point of interest (Denamd/Supply zone), this indicator can help you predict the reversal by showcasing the current trend.

3. Using this indicator you can travel the trend as long as there is a change of trend predicted by this indicator.

M0PB (Momentum Pullback)Long/short strategy that identifies extreme readings on the rsi as a *momentum signal*, unlike most RSI strategies the script will look to buy or sell the first pullback in the direction of the extreme RSI reading.

Enters positions on the first pullback to the 5ema(low)/ 5ema(high) and exits at rolling 12 bar high/ low. The rolling high/ low feature means that if the price enters into a prolonged consolidation the profit target will begin to reduce with each new bar. The best trades tend to work within 2-6 bars.

Built for use on 5 min intervals on FX, Indexes, and Crypto. Lower than 5 minute time frames tend to be noisier and mean more commissions and a higher risk of slippage so the suggested timeframe is 5 mins.

Hard stop is X ATR (users can experiment with this) from the position entry price. This can be adjusted in user inputs.

There is a lot of slack left in entries and exits but the overall strategy is fairly robust across timeframes and markets and has between 60%-70% win rate with larger winners.

Signals that occur from economic news volatility are best avoided.

Gedhusek TrendFibonacciThis indicator is a trend filter based on fibonacci retracement levels

How to read:

- There are three filled zones --> red, yellow and green

- If the price is inside of red zone, there is a downtrend on the market

- If the price is inside the yellow zone, there is a sideways trend on the market

- If the price is inside the green zone, there is a uptrend on the market

- Also, candles are going to have a corresponding color based on the current trend

Calculations of the indicator:

1. Calculate distance between maximal and minimal price over the last "x" bars (choose value for "x" in inputs menu under the "Analysis period")

2. Use this distance for calculating two retracement levels (choose retracement levels in inputs menu)

3. These two retracement levels create an area of what is going to be considered as sideways market

Example:

- Lets say we chose Analysis period of 100, Lower Fibonacci Level as 0.382 and Upper Fibonacci Level as 0.618

- Maximum price over the last 100 bars was of 120 and minimum price was 20. That leaves us with the difference of 100 points

- Now we calculate the fibonacci levels --> 100*0.382 = 38.2 and 100*0.618 = 61.8

- The next step is to add the levels to the lowest price point --> 20 + 38.2 = 58.2 and 20 + 61.8 = 81.8

- And now we have our zones. If the price is going to be below the lower fibonacci level (in this case 58.2), we consider it as a bearish trend. If the price is between those fibonacci levels (58.2 and 81.8), we consider it as a sideways trend. And if the price is above the upper fibonacci level (81.8), we consider it as a bullish trend.

Inputs:

- Analysis period --> number of bars within which the system is going to look for max and min price

- Lower Fibonacci Level --> Choose from options and must be lower or the same as "Upper Fibonacci Level"

- Upper Fibonacci Level --> Choose from options and must be higher or the same as "Lower Fibonacci Level"

- Show Filling --> whether you wish to fill the areas with color

- Change Candle Color --> whether you wish to change the color of candles based on current trend.

[-_-] Volatility Calibrated ATRDescription:

An indicator based on ATR adjusted for volatility of the market. It uses Heikin Ashi data to find short and long opportunities and displays a dynamic stop loss level. Additionally, it has alerts for when the trend changes (which is an entry signal).

How it works:

It works by dynamically calculating the Period for ATR which depends on current volatility level that is calculated by a function that uses Standard Deviation of price. ATR is then smoothed by Weighted Moving Average and multiplied by ATR Factor, resulting in a plot that changes its colour to red when we're in a downtrend and green when in an uptrend. This plot should be used as a dynamic Stop Loss level. Trend change is determined by price crossing the dynamic Stop Loss level. The squared red and green labels appear when the trend changes, and should be used as Entry signals.

Parameters:

- Source -> data used for calculations

- ATR Factor -> higher values produce less noise and longer trends, lower values give more signals

RSItrendRSItrend is a trend indicator based on the standard RSI.

The logic of building the indicator: We build a channel based on the RSI extremes. The exit of the RSI from the channel up is the beginning of the uptrend, the exit of the RSI from the channel down is the beginning of the downtrend. In the downtrend, the candles are colored blue, in the uptrend - orange.

Possible use of the indicator:

I recommend using it with heiken ashi

On small timeframes, you can trade using extremes that are easy to determine by the indicator, as shown in the example given.

On the higher timeframes above the day, you can simply buy an orange bar, sell a blue one. Add a few money management techniques and make a profit.

Gedhusek UltraTrendThis indicator serves a purpose of a trend recognizer. It is able to tell you whether the market is bullish, bearish or if the price goes sideways.

Process of determining the trend:

- The indicator uses 3 moving averages to determine the trend

- For each of these averages, there is calculated value change over a certain period. So, if the value of Moving average was 100 and now it is 110, the change is going to be +10

- After these calculations are done, all three of these values are summed up into one

- Based on this value we can determine whether the overall sentiment is bullish or bearish (if the value is larger than 0, the sentiment is bullish and if it is bellow 0, it is bearish)

- One more metric is used when determining the overall trend, and that is the ATR indicator. This indicator represents a certain movement threshold that has to be surpassed in order to have a valid trend

- So all of this can be summed up into this -> if the summed up value of the value shift of 3 moving averages over certain period is larger than ATR value for certain period, the trend is considered as bullish and if this summed up value is lower than ATR value *-1, the trend is considered as bearish. In case the summed value is smaller than ATR value and larger than ATR value *-1, there is no trend.

-----------------------------------------------------------------------------------------

How to use the Indicator:

- The indicator should be used as a tool for giving you a generic feel about the current trend

- It is not a signal providing system

- It can be adjusted for any trading style by changing the Periods in input menu. (As the values are lower, it will give you more short time trend and vice versa)

- It is a great tool to combine with any trend following strategy

-----------------------------------------------------------------------------------------

Which markets and TimeFrame:

- The UltraTrend Indicator works on all of the markets and all of the TF

- I usually use it on 15min and 1H TF, but that is solely my preference

-----------------------------------------------------------------------------------------

Inputs:

First Period = Period of the first MA

Second Period = Period of the second MA

Third Period = Period of the third MA

ATR Period = Period of the ATR

Ticker vs IndexI was exploring a simple idea how I can visualize the ticker performance against the underlying Index (or any other ticker) performance.

how it works:

When the line is moving up (blue zone), the ticker is performing better than the underlying index (e.g. SPX)(configurable).

When the line is moving down (red zone), the ticker is performing worse than the underlying index.

How to use it:

Use as confirmation always in conjunction with other (main) indicators, avoid "buy" when indicator is in the red zone

Also, crossing over the zero line is often an indication for an upcoming upward move

Try to different SMA length - default is 20 but 10 was often showing better results

(No financial advise, for testing purposes only)

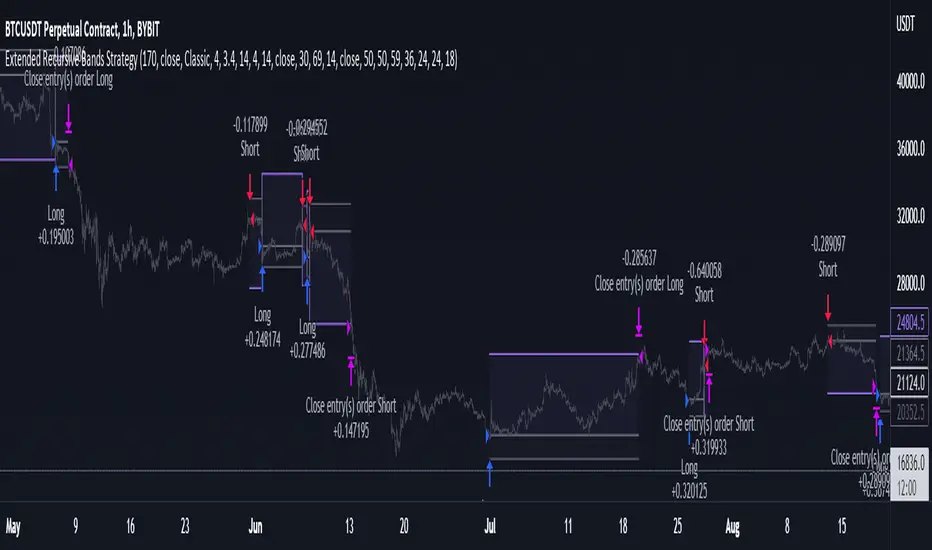

Extended Recursive Bands StrategyThe original indicator was created by alexgrover .

All credit goes to alexgrover for creating the indicator that this strategy uses.

This strategy was posted because there were multiple requests for it, and no strategy based on this indicator exists yet.

The Recursive Bands Indicator, an indicator specially created to be extremely efficient, I think you already know that calculation time is extra important in algorithmic trading, and this is the principal motivation for the creation of the proposed indicator. Originally described in Alex's paper "Pierrefeu, Alex (2019): Recursive Bands - A New Indicator For Technical Analysis", the indicator framework has been widely used in his previous uploaded indicators, however it would have been a shame to not upload it, however user experience being a major concern for me, I decided to add extra options, which explain the term "extended".

The Indicator

The indicator displays one upper and one lower band, every common usages applied to bands indicators such as support/resistance , breakout, trailing stop, etc, can also be applied to this one. Length controls how reactive the bands are, higher values will make the bands cross the price less often.

In order to provide more flexibility for the user alexgrover added the option to use various methods for the calculation of the indicator, therefore the indicator can use the average true range , standard deviation, average high-low range, and one totally exclusive method specially designed for this indicator.

Added logic:

We have implemented a logic that checks whether the bands have been following in the same direction for a set amount of bars. This logic must be true before it can enter trades. This is completely new code that was written by us entirely, and it makes a huge difference on strategy performance.

Strategy Long conditions:

1 — Price low is below the the lower band.

2 — The lower band keeps increasing in value until the 'lookback' setting amount of bars is reached.

Strategy Short conditions:

1 — Price high is above the upper band.

2 — The upper band keeps decreasing in value until the 'lookback' setting amount of bars is reached.

Strategy Properties:

We have set a default commission of 0.06% because these are Bybit's fees. The strategy uses an order size of 10% of equity, since drawdown is very low like this. We also use a 10 tick slippage to keep results realistic and account for this. All other settings were left as default apart from initial capital, just to decrease the size of the numbers.

True Accumulation/Distribution (TG fork)An accumulation/distribution indicator that works better against gaps and with trend coloring.

Accumulation/Distribution was developed by Marc Chaikin to provide insight into strength of a trend by measuring flow of buy and sell volume .

The fact that A/D only factors current period's range for calculating the volume multiplier causes problem with price gaps. They are ignored or even misinterpreted.

True Accumulation/Distribution solves the problem by using True Range instead of only relying on current period's high and low.

Most of the time, True A/D reverts to producing the same values as the original A/D. The difference between True A/D and original A/D can be better seen when a gap has occurred, True A/D has handles it better than Accumulation/Distribution which a bearish close in period's range cause it to misinterpret the strong buy pressure as sell volume

The Moving Average Cloud is simply the filling between the moving average and the True A/D. This feature was inspired by D7R ACC/DIST closed-source indicator, kudos to D7R for making such neat visual indicators (but unfortunately all closed source!).

This indicator was made to extend the original work by adding MTF support and a moving average cloud and coloring.

If you like this indicator, please show the original author RezzaHmt some love:

Musashi_Katana=== Musashi-Katana ===

This tool was designed to fit my particular trading style and personal theories about the "Alchemy of the markets" and ''Harmonic Structure'.

Context

When following a Technical approach to to surf the markets, there are teachings that must be understood before reaching a confort-zone, this usually happen the possible worst way by constant experimentation, it hurts.

Here few technical hints:

- Align High timeframes with lower timeframes:

This simple concept relax a lot complexity of finding of a trend bias. Musashi-Katana allows you to use technical indicator corresponding to specific timeframes, like daily weekly or yearly. They wont change when you change the chart's timeframe, its very useful as you know where you're standing in the long term, Its quite relaxing.

- Use volume:

The constant usage of volume will allow you to sync with the market's breathing. This shows you the mass of money flowing into and out of the market, is key if you want to understand momentum. This tool can help here, as it have multi-period vwaps. You can use yearly, monthly for swing trading, and even weekly if you enjoy scalping.

Useful stuff:

- You have access to baselines, AMA and Kijun-sen with the possibility of adding ATR bands.

- AMAs come as two lines strategies for different approaches, fast medium or slow.

- You can experiment with normal and multi timeframe moving averages and other trend tools.

Final Note

If used correctly Musashi-Katana is a very powerful tool, which makes no sense as there is no correct usage. Don't add everything at the same time, experiment, combine stuff, every market is different.

Backtest every possible strategy before using it, see what works and doesn't. This gives you a lot of peace, specially while you're at the tip of the spear surfing the markets

--> I personally use this in combination with 'Musashi_Slasher (Mometum+Volatility)', as it gives me volatility and momentum in a very precise way.

Band of Filtered RS by Mustafa ÖZVERBand of Filtered RS by Mustafa ÖZVER

This code shows a range (max-min values) price may get if we get strong movements. These values is based on RSI (Relative Strange Index). And also these are calculated using RSI, if we get trades to make rsi is equal to 25 (or rsi down limit) or 75 (rsi up limit) or any value you set, how much will price value get? This code calculate these and shows these to you on graph.

This price are between these band limits because we expect cross reaction to hard movements on price.

For scalping, we can use these values as

long signal when price under down limit,

short signal when price over up limit,

But only these values can not guarantee good results for trading. BE CAREFUL

Adaptive Fisherized Trend Intensity Index Introduction

Here, I modified the script "Trend Intensity Index" (TII) of @everyget.

TTI was developed by M.H. Pee, who also published other trend analysis indicators like the Trend Trigger/Continuation Factor

It helps to determine how strong the current trend is.

The stronger the trend, the higher the chance the price may continue moving in the current direction.

Features

Adaptive mode (based on Ehlers dominant cycle determination) => automatically determines the length

Inverse Fisher Transform => gives sharper signals

Customizable MA Types => discover the impact of different ma bases

Hann Window and NET smoothing => state-of-the-art smoothing

Trend Visualization => shows you the up/down/side trend

Usage

This indicator here offers a perfect trend filtering system. It is capable of up/down/side trend detection.

There are a lot of trend indicators which don't respect sidetrends, which makes this indicator pretty useful.

A lot of traders use trend-following trading systems.

A trader will usually make his/her entry in the market during a strong trend and ride it, until the TII provides an indication of a reversal.

For mean-revertive trading systems, you could use TII to just trade in side trend.

A lot of mean-revertive signal emitters like Bollinger Bands or RSI work most of the times better in side trend.

Furthermore, every timeframe could be used, but higher timeframes have more impact because trends are stronger there.

Signals

Green zone (Top) => Etablished bullish trend

"Peachy" Zone (Middle) => Sidetrend/flat market

Red Zone (Bottom) => Etablished bearish trend

Enjoy guys!

(Let me know your opinions!)

--

Credits to:

@blackcat1402

@DasanC

@cheatcountry

@everget

Trend & atr day & calcHi!

Why for what and how in this script?

At the time of publication the script consists of three modules, it may increase in the future.

1. Bottom left corner : daytime ATR module

(idea and basis of the author's script - ???)

- The size of the daily ATR based on 14 bars;

- intraday ATR progress;

- colour indication of the progress status, for easier visual perception (green < 70%, yellow 70-90 and red over 90% of ATR)

By evaluating the progress of the daily ATR, it is possible to suggest and expedient to enter/exit/hold a trade.

2. Top right: trend module

The trend is calculated based on Bill Williams' alligator indicator

- trend status on specified timeframes for the current ticker;

- colour indication for visual perception (green - growing trend, yellow - alligator is sleeping, red - downtrend)

Do not forget that the alligator is based on moving averages with the resulting consequences.

Its purpose is to assess the state of the trend on other ticker TFs, without additional actions (switching to another screen or TF)

3. In the bottom left corner - risk and position calculator

(based on an idea of the risk calculator by @andrei.bunulu)

It helps to determine the advisability of entering the trade and also what size position to enter into the trade, within money management strategy chosen.

- The calculator works in two directions: long deal and short deal (short deal calculation is enabled by check-box in settings)

- two calculation methods:

a. based on the set stop loss % (default is 0.3%), in this mode the stop and takeout level is automatically calculated (default is 1 / 3).

b. by entering the desired price levels (entry, stop and take profit points)

To make this work correctly please do not forget to choose the type of calculation (% or price) in the settings, and the currency symbol (for visual representation in the results).

The calculator can take into account the set commissions and spreads.

When hovering over the module - tooltips are displayed.

Each module can be enabled / disabled in the settings.

The size and arrangement of the modules is made for joint use with the script - "Abnormal Bar".

/// а по-русски это так ///

Привет!

Зачем для чего и как в этом скрипте?

На момент публикации скрипт состоит из трех модулей, возможно в будущем увеличится.

1. В левом нижнем углу : модуль дневного ATR

(идея и основа скрипт автора - ???)

- размер дневной ATR на основании 14 баров;

- прогресс ATR внутри дня;

- цветовая индикация состояния прогресса, для более простого визуального восприятия (зеленый < 70%, желтый 70-90 и красный более 90% ATR)

Оценивая прогресс дневного ATR, можно предположить и целесообразности входа / выхода / удержания из сделки.

2. В правом верхнем углу: модуль тренда

Тренд рассчитывается на основе индикатора - аллигатор Билла Вильямса

- состояние тренда на указанных таймфреймах для текущего тикера;

- цветовая индикация для визуального восприятия (зеленый - растущий тренд, желтый - аллигатор спит, красный - нисходящий тренд)

Не забываем, что аллигатор построен на основе скользящих средних с вытекающими последствиями.

Назначение - оценить состояние тренда на других ТФ тикера, без дополнительных действий (переключения на другой экран или ТФ)

3. В нижнем левом углу - калькулятор рисков и позиции

(на основе идеи калькулятора аuthor: @andrei.bunulu)

Помогает определить целесообразность входа в сделку, а также каким размером позиции входить в сделку, в рамках выбранной стратегии мани менеджмента.

- калькулятор работает в два направления: длинная и короткая сделка (расчет по короткой включается в настройках чек-боксом)

- два варианта расчета:

а. на основании установленного % стоп лосса (по-умолчанию 0,3%), при этом режиме происходит автоматический расчет уровня стопа и тейка (по умолчанию 1 / 3).

b. путем ввода данных желаемых уровней цены (точки входа, стопа и тейк профита)

Для корректной работы не забываем в настройках выбирать тип расчета (% или цена), а также символ валюты (для визуального отображения в итогах).

Калькулятор может учитывать установленный размер комиссий и спреда.

При наведении на модуль - отображаются подсказки.

Каждый модуль можно включить / выключить в настройках.

Размер и расположение модулей сделано для совместного использования со скриптом - "Abnormal Bar"

MTM - Momentum IndicatorMTM - Momentum

Description

The Momentum indicator is a speed of movement indicator that is designed to identify the speed (or strength) of price movement. This indicator compares the current close price to the close price N bars ago and also displays a moving average of this difference.

Category

Momentum Indicators

Parameters

N ( Default: 6 Min: 1 Max: 100 )

N1 ( Default: 6 Min: 1 Max: 100 )

Chart Script

MTM : CLOSE-REF(CLOSE,N);

MTMMA : MA(MTM,N1)

www.edgerater.com

Generalized Bollinger Bands %B And Bandwidth (Tartigradia)Bollinger Band is simply a representation of the rolling average of price and its standard deviation around the average (called the "basis").

This indicator generalizes the Bollinger Band by implementing many different equations to calculate the Bollinger Bands beyond the standard deviation and sma, and then plot the %B (where the current price falls inside the Bollinger Band), Bandwidth (size of the Bollinger Band) as well as the Bollinger Band itself and a reproduction of the OHLC price candles in a separate pane.

Whereas other Bollinger Bands indicators often just change the basis but not the stdev calculation, the correct way to change the basis is to also change it inside the stdev calculation.

Advanced features such as temporal discounting (ie, newer bars can have more weights), median absolute deviation and multiple sigma bands (eg, 3-sigma) are available.

Up to 3 different Bollinger Bands can be displayed, and the background can be highlighted when price is overbought/oversold (beyond the Bollinger Band of choice). Tip: BB3, which is the bollinger band with standard deviation of 3, which represents 99% of observed values in the lookback period, is a good choice to highlight overbought/oversold conditions.

Three "Sentiment Bars" are provided to see at a glance the sentiments on the price action relative to the Bollinger Bands as reflected by the %B value.

Usage:

Use the %B as a measure of sentiment: bullish if > 0.5, bearish if < 0.5. You can use the Sentiment Bars at the bottom for a quick reference: aqua if bullish, red if bearish, gray if undefined (too close to the middle line).

Use the bandwidth as a measure of volatility: higher is more volatile, lower is less.

When overbought, it can be a good time to sell/short. Use a higher Bollinger Band Multiplier such as 3 or more to reduce false positives.

When oversold, it can be a good time to buy/long. Use a higher Bollinger Band Multiplier such as 3 or more to reduce false positives.

Consider setting a much tighter lookback period of 4 as recommended in backtested works (en.wikipedia.org), use zlma instead of sma, and finally set a higher timeframe for the Bollinger Bands than the one you are currently studying. Then, the Bollinger Bands can help in detecting overbought and oversold regions (price going "out of bands").

Note that I tried to automate the setting of a higher timeframe, but for some reason the output is different when I manually do it using request.security() than when it's in indicator(timeframe=""). If someone has any suggestion as to why it happens, please let me know! (You can try it for yourself by uncommenting the auto_timeframe parameter line).

Change of VolatilityOVERVIEW

The Change of Volatility indicator is a technical indicator that gauges the amount of volatility currently present in the market. The purpose of this indicator is to filter out with-trend signals during ranging/non-trending/consolidating conditions.

CONCEPTS

This indicator assists traders in capitalizing on the assumption that trends are more likely to start during periods of high volatility compared to periods of low volatility . This is because high volatility indicates that there are bigger players currently in the market, which is necessary to begin a sustained trending move.

So, to determine whether the current volatility in the market is low, the indicator will grey out all the areas on the chart whose short term standard deviation of volatility is lower than the long term standard deviation of volatility.

If the short term standard deviation of volatility is above the long term standard deviation of volatility, the current volatility in the market is considered high. This would the ideal time to enter a trending trade due to the assumption that trends are more likely to start during these high-volatility periods.

HOW DO I READ THIS INDICATOR

When the histogram is grey, don't take any trend trades since the current volatility is less than the usual volatility experienced in the market.

When the histogram is green, take all valid with-trend trades since the current volatility is greater than the usual volatility experienced in the market.

Q-TrendQ-Trend is an multipurpose indicatorm that can be used for swing- and trend-trading equally on any timeframe (non-volatile markets are better for this thing).

Settings:

Trend period - used to calculate trend line in the special moments(will explain below);

ATR Multiplier - changes sensitivity. The higher the multiplier = the more sensitive it is.

Also option to smooth source data (helps get cleaner signals, as always).

How to use?

Signals are given on the chart. Also ou can use trend line as S/R line.

The idea behind:

Terms:

SRС = Source

TL = trend line;

MP = ATR multiplier;

ATR = ATR :)

TL = (highest of source P-bars back + lowest of source P-bars back) / 2

Epsilon = MP * ATR

I was thinking for a week about combining volatility and relation between highest and lowest price point. That why I called indicator Q-Trend = Quantitative Trend , as I was trying to think about price in a mathematical way.

Okay, time to go philosophical:

1) TL is shows good price trend, but as it is slow enough and not enough informative, we need add additional conditions to produce signals.

2) Okay, so what can we add as conditions? We need to take volatility into account, as it is crucial in the moments of market uncertainty. So let's use ATR (Average True Range) somehow. My idea is that if SRC breaks TL + ATR , then it means that there will be upmove and we update our TL . Analogically for SRC breaking TL - ATR (breaks are crosses of TL +- ATR lines) .

Conclusion:

- if SRC breaks TL + ATR , it is a BUY signal and update of trend line;

- if SRC breaks TL - ATR , it is a SELL signal and update of trend line;

I think that such indicator already exisits on TradingView, as I've already saw something similar, but long ago, so please don't report, if such thing already exists.

But if not, then I hope, that you will gain some profits with Q-Trend :)

I will continue my work on this thing, so stay tuned.

Trade with your own risks and have your profits!

Wish you all the best!

- Tarasenko Fyodor