lib_plot_objectsLibrary "lib_plot_objects"

library wrapping basic builtin object constructors, to be able to do calculations with points/lines/boxes/triangles/polygons via libraries and on securities. inspired by Trendoscope's ( and ) with added update mechanism to not have to recreate objects on every iteration for continously drawn items, automated xloc selection for coordinates, compatibility check for Points, added Triangle and Polygon types, object reflection via tostring to valid json (logging via webhook)

method assert_same_xloc(a, b, test)

checks two points for compatibility, i.e. having the same xloc

Namespace types: Point

Parameters:

a (Point)

b (Point)

test (Test type from robbatt/lib_unit/6)

method assert_same_xloc(a, b, test)

checks two lines for compatibility, i.e. having the same xloc

Namespace types: Line

Parameters:

a (Line)

b (Line)

test (Test type from robbatt/lib_unit/6)

method or_default(args)

checks args oject for being na, if so, provide a default instead

Namespace types: LineArgs

Parameters:

args (LineArgs)

method or_default(args)

checks args oject for being na, if so, provide a default instead

Namespace types: LabelArgs

Parameters:

args (LabelArgs)

method or_default(args)

checks args oject for being na, if so, provide a default instead

Namespace types: BoxArgs

Parameters:

args (BoxArgs)

method or_default(args)

checks args oject for being na, if so, provide a default instead

Namespace types: BoxTextArgs

Parameters:

args (BoxTextArgs)

method x(point, xloc)

automatically returns the correct x coordinate, based on the point's set xloc

Namespace types: Point

Parameters:

point (Point)

xloc (string)

method tostring(this, date_format)

converts object to json representation

Namespace types: Point

Parameters:

this (Point)

date_format (string)

method tostring(this, date_format)

converts object to json representation

Namespace types: Point

Parameters:

this (Point )

date_format (string)

method tostring(this)

converts object to json representation

Namespace types: LineArgs

Parameters:

this (LineArgs)

method tostring(this, date_format)

converts object to json representation

Namespace types: Line

Parameters:

this (Line)

date_format (string)

method tostring(this)

Namespace types: LabelArgs

Parameters:

this (LabelArgs)

method tostring(this, date_format)

Namespace types: Label

Parameters:

this (Label)

date_format (string)

method tostring(this, date_format)

Namespace types: LineFill

Parameters:

this (LineFill)

date_format (string)

method tostring(this)

Namespace types: BoxArgs

Parameters:

this (BoxArgs)

method tostring(this)

Namespace types: BoxTextArgs

Parameters:

this (BoxTextArgs)

method tostring(this, date_format)

Namespace types: Box

Parameters:

this (Box)

date_format (string)

method tostring(this, date_format)

Namespace types: Triangle

Parameters:

this (Triangle)

date_format (string)

method tostring(this, date_format)

Namespace types: TriangleFill

Parameters:

this (TriangleFill)

date_format (string)

method tostring(this, date_format)

Namespace types: Polygon

Parameters:

this (Polygon)

date_format (string)

method tostring(this, date_format)

Namespace types: PolygonFill

Parameters:

this (PolygonFill)

date_format (string)

method tostring(this, date_format)

Namespace types: Line

Parameters:

this (Line )

date_format (string)

method tostring(this, date_format)

Namespace types: Box

Parameters:

this (Box )

date_format (string)

method tostring(this, date_format)

Namespace types: Triangle

Parameters:

this (Triangle )

date_format (string)

method tostring(this, date_format)

Namespace types: Polygon

Parameters:

this (Polygon )

date_format (string)

method tostring(this, date_format)

Namespace types: PolygonFill

Parameters:

this (PolygonFill )

date_format (string)

method create_center(points)

Namespace types: Point

Parameters:

points (Point )

method create_center(this, other)

Namespace types: Point

Parameters:

this (Point)

other (Point)

method create_center(this)

Namespace types: Line

Parameters:

this (Line)

method create_line(this, other, args)

Namespace types: Point

Parameters:

this (Point)

other (Point)

args (LineArgs)

method create_triangle(this, b, c, args)

Namespace types: Point

Parameters:

this (Point)

b (Point)

c (Point)

args (LineArgs)

method create_triangle(this, c)

Namespace types: Line

Parameters:

this (Line)

c (Point)

method create_box(this, other, txt, args, text_args)

Namespace types: Point

Parameters:

this (Point)

other (Point)

txt (string)

args (BoxArgs)

text_args (BoxTextArgs)

method create_box(this, txt, args, text_args)

Namespace types: Line

Parameters:

this (Line)

txt (string)

args (BoxArgs)

text_args (BoxTextArgs)

method create_polygon(points, args)

Namespace types: Point

Parameters:

points (Point )

args (LineArgs)

method create_polygon(start, others, args)

Namespace types: Point

Parameters:

start (Point)

others (Point )

args (LineArgs)

method create_fill(this, other, fill_color)

Namespace types: Line

Parameters:

this (Line)

other (Line)

fill_color (color)

method create_fill(this, fill_color)

Namespace types: Triangle

Parameters:

this (Triangle)

fill_color (color)

method create_fill(this, fill_color)

Namespace types: Polygon

Parameters:

this (Polygon)

fill_color (color)

method create_label(this, txt, args, tooltip)

Namespace types: Point

Parameters:

this (Point)

txt (string)

args (LabelArgs)

tooltip (string)

method create_label(this, txt, args, tooltip)

Namespace types: Line

Parameters:

this (Line)

txt (string)

args (LabelArgs)

tooltip (string)

method create_label(this, txt, args, tooltip)

Namespace types: Box

Parameters:

this (Box)

txt (string)

args (LabelArgs)

tooltip (string)

method create_label(this, txt, args, tooltip)

Namespace types: Triangle

Parameters:

this (Triangle)

txt (string)

args (LabelArgs)

tooltip (string)

method create_label(this, txt, args, tooltip)

Namespace types: Polygon

Parameters:

this (Polygon)

txt (string)

args (LabelArgs)

tooltip (string)

method update(this, bar_time, bar_idx, price)

Namespace types: Point

Parameters:

this (Point)

bar_time (int)

bar_idx (int)

price (float)

method update(this, update)

Namespace types: Point

Parameters:

this (Point)

update (Point)

method update(this, point)

Namespace types: Label

Parameters:

this (Label)

point (Point)

method update(this, start, end)

Namespace types: Line

Parameters:

this (Line)

start (Point)

end (Point)

method update(this, left_top, right_bottom)

Namespace types: Box

Parameters:

this (Box)

left_top (Point)

right_bottom (Point)

method update(this, a, b, c)

Namespace types: Triangle

Parameters:

this (Triangle)

a (Point)

b (Point)

c (Point)

method update(this, points)

Namespace types: Polygon

Parameters:

this (Polygon)

points (Point )

method delete(this)

Namespace types: Line

Parameters:

this (Line)

method delete(this)

Namespace types: Label

Parameters:

this (Label)

method delete(this)

Namespace types: LineFill

Parameters:

this (LineFill)

method delete(this)

Namespace types: Box

Parameters:

this (Box)

method delete(this)

Namespace types: TriangleFill

Parameters:

this (TriangleFill)

method delete(this)

Namespace types: Triangle

Parameters:

this (Triangle)

method delete(this)

Namespace types: Polygon

Parameters:

this (Polygon)

method delete(this)

Namespace types: PolygonFill

Parameters:

this (PolygonFill)

method delete(this)

Namespace types: Line

Parameters:

this (Line )

method delete(this)

Namespace types: Label

Parameters:

this (Label )

method delete(this)

Namespace types: LineFill

Parameters:

this (LineFill )

method delete(this)

Namespace types: Box

Parameters:

this (Box )

method delete(this)

Namespace types: TriangleFill

Parameters:

this (TriangleFill )

method delete(this)

Namespace types: Polygon

Parameters:

this (Polygon )

method delete(this)

Namespace types: Triangle

Parameters:

this (Triangle )

method delete(this)

Namespace types: PolygonFill

Parameters:

this (PolygonFill )

method draw(this)

Namespace types: Label

Parameters:

this (Label)

method draw(this)

Namespace types: Line

Parameters:

this (Line)

method draw(this)

Namespace types: Box

Parameters:

this (Box)

method draw(this)

Namespace types: Triangle

Parameters:

this (Triangle)

method draw(this)

Namespace types: Polygon

Parameters:

this (Polygon)

method draw(this)

Namespace types: LineFill

Parameters:

this (LineFill)

method draw(this)

Namespace types: TriangleFill

Parameters:

this (TriangleFill)

method draw(this)

Namespace types: PolygonFill

Parameters:

this (PolygonFill)

Point

Fields:

bar_time (series int) : time based x coordinate

bar_idx (series int) : bar index based x coordinate

price (series float) : price based y coordinate

xloc (series string) : To select if x coordinate is represented by bar_idx or bar_time. Possible values: xloc.bar_index and xloc.bar_time. Default is xloc.bar_index.

LabelArgs

Fields:

text_color (series color) : Text color.

bg_color (series color) : Color of the label border and arrow.

text_font_family (series string) : The font family of the text. Optional. The default value is font.family_default. Possible values: font.family_default, font.family_monospace.

yloc (series string) : Possible values are yloc.price, yloc.abovebar, yloc.belowbar. If yloc=yloc.price, y argument specifies the price of the label position. If yloc=yloc.abovebar, label is located above bar. If yloc=yloc.belowbar, label is located below bar. Default is yloc.price.

style (series string) : Label style. Possible values: label.style_none, label.style_xcross, label.style_cross, label.style_triangleup, label.style_triangledown, label.style_flag, label.style_circle, label.style_arrowup, label.style_arrowdown, label.style_label_up, label.style_label_down, label.style_label_left, label.style_label_right, label.style_label_lower_left, label.style_label_lower_right, label.style_label_upper_left, label.style_label_upper_right, label.style_label_center, label.style_square, label.style_diamond, label.style_text_outline. Default is label.style_label_down.

size (series string) : Label size. Possible values: size.auto, size.tiny, size.small, size.normal, size.large, size.huge. Default value is size.normal.

text_align (series string) : Label text alignment. Possible values: text.align_left, text.align_center, text.align_right. Default value is text.align_center.

Label

Fields:

point (Point) : The Label coordinates

txt (series string) : Label text. Default is empty string.

args (LabelArgs) : Wrapper for reusable arguments for label.new()

tooltip (series string) : Hover to see tooltip label.

plot (series label) : The label object to be added and plotted via draw()

LineArgs

Fields:

line_color (series color) : Line color.

style (series string) : Line style. Possible values: line.style_solid, line.style_dotted, line.style_dashed, line.style_arrow_left, line.style_arrow_right, line.style_arrow_both.

width (series int) : Line width in pixels.

extend (series string) : f extend=extend.none, draws segment starting at point (x1, y1) and ending at point (x2, y2). If extend is equal to extend.right or extend.left, draws a ray starting at point (x1, y1) or (x2, y2), respectively. If extend=extend.both, draws a straight line that goes through these points. Default value is extend.none.

Line

Fields:

start (Point) : starting point of the line

end (Point)

args (LineArgs) : Wrapper for reusable arguments for line.new()

plot (series line) : The line object to be added and plotted via draw()

LineFill

Fields:

a (Line) : The first Line object

b (Line) : The second Line object

fill_color (series color) : The color used to fill the space between the lines.

plot (series linefill) : The linefill object to be added and plotted via draw()

BoxArgs

Fields:

border_color (series color) : Color of the four borders. Optional. The default is color.blue.

border_width (series int) : Width of the four borders, in pixels. Optional. The default is 1 pixel.

border_style (series string) : Style of the four borders. Possible values: line.style_solid, line.style_dotted, line.style_dashed. Optional. The default value is line.style_solid.

bg_color (series color) : Background color of the box. Optional. The default is color.blue.

extend (series string) : When extend.none is used, the horizontal borders start at the left border and end at the right border. With extend.left or extend.right, the horizontal borders are extended indefinitely to the left or right of the box, respectively. With extend.both, the horizontal borders are extended on both sides. Optional. The default value is extend.none.

BoxTextArgs

Fields:

text_color (series color) : The color of the text. Optional. The default is color.black.

text_size (series string) : The size of the text. An optional parameter, the default value is size.auto. Possible values: size.auto, size.tiny, size.small, size.normal, size.large, size.huge.

text_halign (series string) : The horizontal alignment of the box's text. Optional. The default value is text.align_center. Possible values: text.align_left, text.align_center, text.align_right.

text_valign (series string) : The vertical alignment of the box's text. Optional. The default value is text.align_center. Possible values: text.align_top, text.align_center, text.align_bottom.

text_wrap (series string) : Defines whether the text is presented in a single line, extending past the width of the box if necessary, or wrapped so every line is no wider than the box itself (and clipped by the bottom border of the box if the height of the resulting wrapped text is higher than the height of the box). Optional. The default value is text.wrap_none. Possible values: text.wrap_none, text.wrap_auto.

text_font_family (series string) : The font family of the text. Optional. The default value is font.family_default. Possible values: font.family_default, font.family_monospace.

Box

Fields:

left_top (Point) : top-left corner of the box

right_bottom (Point) : bottom-right corner of the box

txt (series string) : The text to be displayed inside the box. Optional. The default is empty string.

args (BoxArgs) : Wrapper for reusable arguments for box.new()

text_args (BoxTextArgs)

plot (series box) : The box object to be added and plotted via draw()

Triangle

Fields:

a (Point) : first Corner

b (Point) : second Corner

c (Point) : third Corner

args (LineArgs) : Wrapper for reusable arguments for line.new()

plot_ab (series line) : The line object to be added and plotted via draw()

plot_ac (series line) : The line object to be added and plotted via draw()

plot_bc (series line) : The line object to be added and plotted via draw()

TriangleFill

Fields:

triangle (Triangle) : The Triangle object

fill_color (series color) : The color used to fill the space between the lines.

plot (series linefill) : The linefill object to be added and plotted via draw()

Polygon

Fields:

points (Point ) : array of points that make up the Polygon

center (Point) : Center point of the Polygon, can be used for a label and will be center for PolygonFill

args (LineArgs) : Wrapper for reusable arguments for line.new()

plot (line ) : An array of Lines that form Polygon Border

PolygonFill

Fields:

poly (Polygon) : the Polygon

fill_color (series color) : The color used to fill the space between the lines.

plot_segments (line ) : An array of helper lines to create linefills

plot_fills (linefill ) : An array of linefills that cover the Polygon surface

Techindicator

lib_priceactionLibrary "lib_priceaction"

a library for everything related to price action, starting off with displacements

displacement(len, min_strength, o, c)

calculate if there is a displacement and how strong it is

Parameters:

len (int) : The amount of candles to consider for the deviation

min_strength (float) : The minimum displacement strength to trigger a signal

o (float) : The source series on which calculations are based

c (float) : The source series on which calculations are based

Returns: a tuple of (bool signal, float displacement_strength)

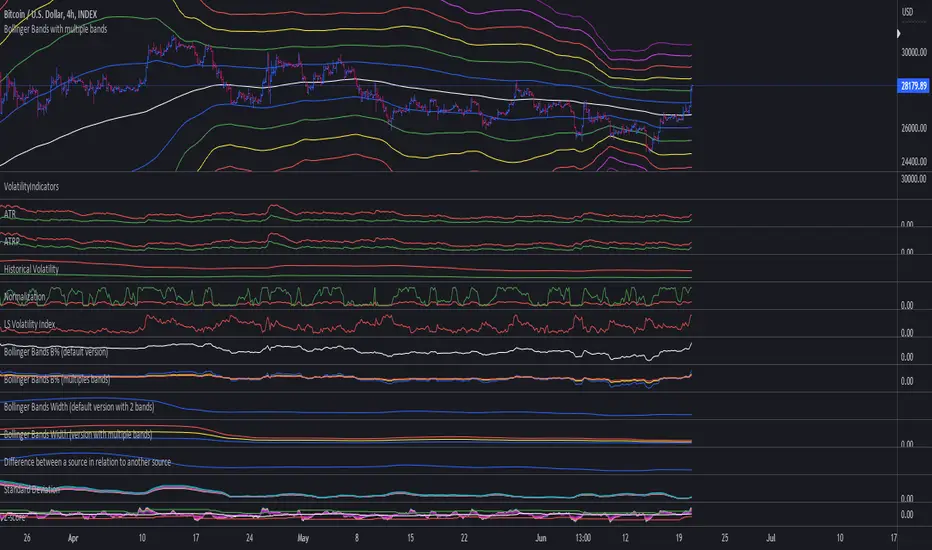

VolatilityIndicatorsLibrary "VolatilityIndicators"

This is a library of Volatility Indicators .

It aims to facilitate the grouping of this category of indicators, and also offer the customized supply of

the parameters and sources, not being restricted to just the closing price.

@Thanks and credits:

1. Dynamic Zones: Leo Zamansky, Ph.D., and David Stendahl

2. Deviation: Karl Pearson (code by TradingView)

3. Variance: Ronald Fisher (code by TradingView)

4. Z-score: Veronique Valcu (code by HPotter)

5. Standard deviation: Ronald Fisher (code by TradingView)

6. ATR (Average True Range): J. Welles Wilder (code by TradingView)

7. ATRP (Average True Range Percent): millerrh

8. Historical Volatility: HPotter

9. Min-Max Scale Normalization: gorx1

10. Mean Normalization: gorx1

11. Standardization: gorx1

12. Scaling to unit length: gorx1

13. LS Volatility Index: Alexandre Wolwacz (Stormer), Fabrício Lorenz, Fábio Figueiredo (Vlad) (code by me)

14. Bollinger Bands: John Bollinger (code by TradingView)

15. Bollinger Bands %: John Bollinger (code by TradingView)

16. Bollinger Bands Width: John Bollinger (code by TradingView)

dev(source, length, anotherSource)

Deviation. Measure the difference between a source in relation to another source

Parameters:

source (float)

length (simple int) : (int) Sequential period to calculate the deviation

anotherSource (float) : (float) Source to compare

Returns: (float) Bollinger Bands Width

variance(src, mean, length, biased, degreesOfFreedom)

Variance. A statistical measurement of the spread between numbers in a data set. More specifically,

variance measures how far each number in the set is from the mean (average), and thus from every other number in the set.

Variance is often depicted by this symbol: σ2. It is used by both analysts and traders to determine volatility and market security.

Parameters:

src (float) : (float) Source to calculate variance

mean (float) : (float) Mean (Moving average)

length (simple int) : (int) The sequential period to calcule the variance (number of values in data set)

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length. Only applies when biased parameter is defined as true.

Returns: (float) Standard deviation

stDev(src, length, mean, biased, degreesOfFreedom)

Measure the Standard deviation from a source in relation to it's moving average.

In this implementation, you pass the average as a parameter, allowing a more personalized calculation.

Parameters:

src (float) : (float) Source to calculate standard deviation

length (simple int) : (int) The sequential period to calcule the standard deviation

mean (float) : (float) Moving average.

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Standard deviation

zscore(src, mean, length, biased, degreesOfFreedom)

Z-Score. A z-score is a statistical measurement that indicates how many standard deviations a data point is from

the mean of a data set. It is also known as a standard score. The formula for calculating a z-score is (x - μ) / σ,

where x is the individual data point, μ is the mean of the data set, and σ is the standard deviation of the data set.

Z-scores are useful in identifying outliers or extreme values in a data set. A positive z-score indicates that the

data point is above the mean, while a negative z-score indicates that the data point is below the mean. A z-score of

0 indicates that the data point is equal to the mean.

Z-scores are often used in hypothesis testing and determining confidence intervals. They can also be used to compare

data sets with different units or scales, as the z-score standardizes the data. Overall, z-scores provide a way to

measure the relative position of a data point in a data

Parameters:

src (float) : (float) Source to calculate z-score

mean (float) : (float) Moving average.

length (simple int) : (int) The sequential period to calcule the standard deviation

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Z-score

atr(source, length)

ATR: Average True Range. Customized version with source parameter.

Parameters:

source (float) : (float) Source

length (simple int) : (int) Length (number of bars back)

Returns: (float) ATR

atrp(length, sourceP)

ATRP (Average True Range Percent)

Parameters:

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

atrp(source, length, sourceP)

ATRP (Average True Range Percent). Customized version with source parameter.

Parameters:

source (float) : (float) Source for ATR

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

historicalVolatility(lengthATR, lengthHist)

Historical Volatility

Parameters:

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

historicalVolatility(source, lengthATR, lengthHist)

Historical Volatility

Parameters:

source (float) : (float) Source for ATR

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

minMaxNormalization(src, numbars)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

minMaxNormalization(src, numbars, minimumLimit, maximumLimit)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

In this implementation, the user explicitly provides the desired minimum (min) and maximum (max) values for the scale,

rather than using the minimum and maximum values from the data.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

minimumLimit (simple float) : (float) Minimum value to scale

maximumLimit (simple float) : (float) Maximum value to scale

Returns: (float) Normalized value

meanNormalization(src, numbars, mean)

Mean Normalization

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

mean (float) : (float) Mean of source

Returns: (float) Normalized value

standardization(src, mean, stDev)

Standardization (Z-score Normalization). How "outside the mean" values relate to the standard deviation (ratio between first and second)

Parameters:

src (float) : (float) Source to normalize

mean (float) : (float) Mean of source

stDev (float) : (float) Standard Deviation

Returns: (float) Normalized value

scalingToUnitLength(src, numbars)

Scaling to unit length

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

lsVolatilityIndex(movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int) : (float) Length for normalization

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

lsVolatilityIndex(sourcePrice, movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

sourcePrice (float) : (float) Source for measure the distance

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int)

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

bollingerBands(src, length, mult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) A tuple of Bollinger Bands, where index 1=basis; 2=basis+dev; 3=basis-dev; and dev=multiplier*stdev

bollingerBands(src, length, aMult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Also, various multipliers can be passed, thus getting more bands (instead of just 2).

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) An array of multiplies used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands, where:

index 1=basis; 2=basis+dev1; 3=basis-dev1; 4=basis+dev2, 5=basis-dev2, 6=basis+dev2, 7=basis-dev2, Nup=basis+devN, Nlow=basis-devN

and dev1, dev2, devN are ```multiplier N * stdev```

bollingerBandsB(src, length, mult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation:

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands %B

bollingerBandsB(src, length, aMult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands %B. The number of results in this array is equal the numbers of multipliers passed via parameter.

bollingerBandsW(src, length, mult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation:

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands Width

bollingerBandsW(src, length, aMult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands Width. The number of results in this array is equal the numbers of multipliers passed via parameter.

dinamicZone(source, sampleLength, pcntAbove, pcntBelow)

Get Dynamic Zones

Parameters:

source (float) : (float) Source

sampleLength (simple int) : (int) Sample Length

pcntAbove (simple float) : (float) Calculates the top of the dynamic zone, considering that the maximum values are above x% of the sample

pcntBelow (simple float) : (float) Calculates the bottom of the dynamic zone, considering that the minimum values are below x% of the sample

Returns: A tuple with 3 series of values: (1) Upper Line of Dynamic Zone;

(2) Lower Line of Dynamic Zone; (3) Center of Dynamic Zone (x = 50%)

Examples:

MyVolatilityBandsLibrary "MyVolatilityBands"

Just a lil' library of volatility bands that I use in some scripts

bollingerbands(src, lkbk, mult, basis)

Bollinger Bands

Parameters:

src (float) : float

lkbk (int) : int

mult (float) : float

basis (float)

Returns: Bollinger Bands

donchianchannels(src, lkbk, band_width)

Donchian Channels

Parameters:

src (float) : float

lkbk (int) : int

band_width (float) : float

Returns: Donchian Channels with an outer band of varying thickness adjusted by the band_width input

doublehalfdonchianchannels(src, lkbk, divisor)

Double Half Donchian Channels

Parameters:

src (float) : float

lkbk (int) : int

divisor (float) : float

Returns: two adjustable bases calculated using Donchian Channels calculation that act as a measure of volatility

PivotLibrary "Pivot"

This library helps you store and manage pivots.

bias(isHigh, isHigher, prevWasHigher)

Helper function to calculate bias.

Parameters:

isHigh (bool) : (bool) Wether the pivot is a pivot high or not.

isHigher (bool) : (bool) Wether the pivot is a higher pivot or not.

@return (bool) The bias (true = bullish, false = bearish, na = neutral).

prevWasHigher (bool)

biasToString(bias)

Parameters:

bias (bool)

biasToColor(bias, theme)

Parameters:

bias (bool)

theme (Theme)

nameString(isHigh, isHigher)

Parameters:

isHigh (bool)

isHigher (bool)

abbrString(isHigh, isHigher)

Parameters:

isHigh (bool)

isHigher (bool)

tooltipString(y, isHigh, isHigher, bias, theme)

Parameters:

y (float)

isHigh (bool)

isHigher (bool)

bias (bool)

theme (Theme)

createLabel(x, y, isHigh, isHigher, prevWasHigher, settings)

Parameters:

x (int)

y (float)

isHigh (bool)

isHigher (bool)

prevWasHigher (bool)

settings (Settings)

new(x, y, isHigh, isHigher, settings)

Parameters:

x (int)

y (float)

isHigh (bool)

isHigher (bool)

settings (Settings)

newArray(size, initialValue)

Parameters:

size (int)

initialValue (Pivot)

method getFirst(this)

Namespace types: Pivot

Parameters:

this (Pivot )

method getLast(this, isHigh)

Namespace types: Pivot

Parameters:

this (Pivot )

isHigh (bool)

method getLastHigh(this)

Namespace types: Pivot

Parameters:

this (Pivot )

method getLastLow(this)

Namespace types: Pivot

Parameters:

this (Pivot )

method getPrev(this, numBack, isHigh)

Namespace types: Pivot

Parameters:

this (Pivot )

numBack (int)

isHigh (bool)

method getPrevHigh(this, numBack)

Namespace types: Pivot

Parameters:

this (Pivot )

numBack (int)

method getPrevLow(this, numBack)

Namespace types: Pivot

Parameters:

this (Pivot )

numBack (int)

method getText(this)

Namespace types: Pivot

Parameters:

this (Pivot)

method setX(this, value)

Namespace types: Pivot

Parameters:

this (Pivot)

value (int)

method setY(this, value)

Namespace types: Pivot

Parameters:

this (Pivot)

value (float)

method setXY(this, x, y)

Namespace types: Pivot

Parameters:

this (Pivot)

x (int)

y (float)

method setBias(this, value)

Namespace types: Pivot

Parameters:

this (Pivot)

value (int)

method setColor(this, value)

Namespace types: Pivot

Parameters:

this (Pivot)

value (color)

method setText(this, value)

Namespace types: Pivot

Parameters:

this (Pivot)

value (string)

method add(this, pivot)

Namespace types: Pivot

Parameters:

this (Pivot )

pivot (Pivot)

method updateLast(this, y, settings)

Namespace types: Pivot

Parameters:

this (Pivot )

y (float)

settings (Settings)

method update(this, y, isHigh, settings)

Namespace types: Pivot

Parameters:

this (Pivot )

y (float)

isHigh (bool)

settings (Settings)

Pivot

Stores Pivot data.

Fields:

x (series int)

y (series float)

isHigh (series bool)

isHigher (series bool)

bias (series bool)

lb (series label)

Theme

Attributes for customizable look and feel.

Fields:

size (series string)

colorDefault (series color)

colorNeutral (series color)

colorBullish (series color)

colorBearish (series color)

colored (series bool)

showTooltips (series bool)

showTooltipName (series bool)

showTooltipValue (series bool)

showTooltipBias (series bool)

Settings

All settings for the pivot.

Fields:

theme (Theme)

MyMovingAveragesLibraryLibrary "MyMovingAveragesLibrary"

alma(src, lkbk, alma_offset, alma_sigma)

ALMA - Arnaud Legoux Moving Average

Parameters:

src (float) : float

lkbk (int) : int

alma_offset (simple float)

alma_sigma (simple float) : float

Returns: moving average

frama(src, lkbk, FC, SC)

FRAMA - Fractal Adaptive Moving Average

Parameters:

src (float) : float

lkbk (int) : int

FC (int) : int

SC (int) : int

Returns: moving average

kama(src, lkbk, kamafastend, kamaslowend)

KAMA - Kaufman Adaptive Moving Average

Parameters:

src (float) : float

lkbk (int) : int

kamafastend (int) : int

kamaslowend (int) : int

Returns: moving average

ema(src, lkbk)

EMA - Exponential Moving Average

Parameters:

src (float) : float

lkbk (simple int) : int

Returns: moving average

dema(src, lkbk)

DEMA - Double Exponential Moving Average

Parameters:

src (float) : float

lkbk (simple int) : int

Returns: moving average

tema(src, lkbk)

TEMA - Triple Exponential Moving Average

Parameters:

src (float) : float

lkbk (simple int) : int

Returns: moving average

hma(src, lkbk)

HMA - Hull Moving Average

Parameters:

src (float) : float

lkbk (simple int) : int

Returns: moving average

jma(src, lkbk, jurik_power, jurik_phase)

JMA - Jurik Moving Average

Parameters:

src (float) : float

lkbk (int) : int

jurik_power (int)

jurik_phase (float)

Returns: moving average

laguerre(src, alpha)

Laguerre Filter

Parameters:

src (float) : float

alpha (float) : float

Returns: moving average

lsma(src, lkbk, lsma_offset)

LSMA - Least Squares Moving Average

Parameters:

src (float) : float

lkbk (simple int) : int

lsma_offset (simple int) : int

Returns: moving average

mcginley(src, lkbk)

McGinley Dynamic

Parameters:

src (float) : float

lkbk (simple int) : int

Returns: moving average

mf(src, lkbk, mf_feedback, mf_beta, mf_z)

Modular Filter

Parameters:

src (float) : float

lkbk (int) : int

mf_feedback (bool) : float

mf_beta (float) : boolean

mf_z (float) : float

Returns: moving average

rdma(src)

RDMA - RexDog Moving Average (RDA, as he calls it)

Parameters:

src (float) : flot

Returns: moving average

sma(src, lkbk)

SMA - Simple Moving Average

Parameters:

src (float) : float

lkbk (int) : int

Returns: moving average

smma(src, lkbk)

SMMA - Smoothed Moving Average (known as RMA in TradingView)

Parameters:

src (float) : float

lkbk (simple int) : int

Returns: moving average

t3(src, lkbk)

T3 Moving Average

Parameters:

src (float) : float

lkbk (simple int) : int

Returns: moving average

tma(src, lkbk)

TMA - Triangular Moving Average

Parameters:

src (float) : float

lkbk (simple int) : int

Returns: moving average

vama(src, lkbk, vol_lkbk)

VAMA - Volatility-Adjusted Moving Average

Parameters:

src (float) : float

lkbk (simple int) : int

vol_lkbk (int) : int

vwma(src, lkbk)

VWMA - Volume-Weighted Moving Average

Parameters:

src (float) : float

lkbk (simple int) : int

Returns: moving average

mf_zlagma(src, lkbk)

Zero-Lag Moving Average

Parameters:

src (float) : float

lkbk (int) : int

Returns: moving average

Absolute ZigZag LibLibrary "Absolute_ZigZag_Lib"

This ZigZag Library is a Bit different. Instead of using percentages or looking more than 1 bar left or right, this Zigzag library calculates pivots by just looking at the current bar highs and lows and the ones of one bar earlier.

This is the most accurate way of calculating pivots and it also eliminates lag.

The library also features a solution for bars that have both a higher high and a higher low like seen below.

You can also use your own colors for the labels and the lines.

You can also quickly select a one-colored theme without changing all colors at once

method isHigherHigh(this)

Checks if current pivot is a higher high

Namespace types: Pivot

Parameters:

this (Pivot) : (Pivot) The object to work with.

@return (bool) True if the pivot is a higher high, false if not.

method isLowerHigh(this)

Checks if current pivot is a lower high

Namespace types: Pivot

Parameters:

this (Pivot) : (Pivot) The object to work with.

@return (bool) True if the pivot is a lower high, false if not.

method isHigherLow(this)

Checks if current pivot is a higher low

Namespace types: Pivot

Parameters:

this (Pivot) : (Pivot) The object to work with.

@return (bool) True if the pivot is a higher low, false if not.

method isLowerLow(this)

Checks if current pivot is a lower low

Namespace types: Pivot

Parameters:

this (Pivot) : (Pivot) The object to work with.

@return (bool) True if the pivot is a lower low, false if not.

method getLastPivotHigh(this)

Gets the last Pivot High

Namespace types: Pivot

Parameters:

this (Pivot ) : (array) The object to work with.

@return (Pivot) The latest Pivot High

method getLastPivotLow(this)

Gets the last Pivot Low

Namespace types: Pivot

Parameters:

this (Pivot ) : (array) The object to work with.

@return (Pivot) The latest Pivot Low

method prev(this, index)

Namespace types: Pivot

Parameters:

this (Pivot )

index (int)

method last(this, throwError)

Namespace types: Pivot

Parameters:

this (Pivot )

throwError (bool)

new(highFirst, theme)

Parameters:

highFirst (bool)

theme (Theme)

getLowerTimeframePeriod()

Theme

Used to create a (color) theme to draw Zigzag

Fields:

colorDefault (series color)

colorNeutral (series color)

colorBullish (series color)

colorBearish (series color)

coloredLines (series bool)

Point

Used to determine a coordination on the chart

Fields:

x (series int)

y (series float)

Pivot

Used to determine pivots on the chart

Fields:

point (Point)

isHigh (series bool)

isHigher (series bool)

ln (series line)

lb (series label)

GeneratorBetaLib:Generator

This library generate levels that could be used inside SNG scripts and strategies. Also uses beta version of SNG Types library

IndicatorsLibrary "Indicators"

this has a calculation for the most used indicators.

macd4C(fastMa, slowMa)

this calculates macd 4c

Parameters:

fastMa (simple int) : is the period for the fast ma. the minimum value is 7

slowMa (simple int) : is the period for the slow ma. the minimum value is 7

Returns: the macd 4c value for the current bar

rsi(rsiSourceInput, rsiLengthInput)

this calculates rsi

Parameters:

rsiSourceInput (float) : is the source for the rsi

rsiLengthInput (simple int) : is the period for the rsi

Returns: the rsi value for the current bar

ao(source, fastPeriod, slowPeriod)

this calculates ao

Parameters:

source (float) : is the source for the ao

fastPeriod (int) : is the period for the fast ma

slowPeriod (int) : is the period for the slow ma

Returns: the ao value for the current bar

kernelAoOscillator(kernelFastLookback, kernelSlowLookback, kernelFastWeight, kernelSlowWeight, kernelFastRegressionStart, kernelSlowRegressionStart, kernelFastSmoothPeriod, kernelSlowSmoothPeriod, kernelFastSmooth, kernelSlowSmooth, source)

this calculates our own kernel ao oscillator which we made

Parameters:

kernelFastLookback (simple int)

kernelSlowLookback (simple int)

kernelFastWeight (simple float)

kernelSlowWeight (simple float)

kernelFastRegressionStart (simple int)

kernelSlowRegressionStart (simple int)

kernelFastSmoothPeriod (int)

kernelSlowSmoothPeriod (int)

kernelFastSmooth (bool)

kernelSlowSmooth (bool)

source (float) : is the source for the ao

Returns: the kernel ao oscillator value for the current bar, the colors for both the fast and slow kernel, the fast & slow kernel

signalLineKernel(lag, h, r, x_0, smoothColors, _src, c_bullish, c_bearish)

Parameters:

lag (int)

h (float)

r (float)

x_0 (int)

smoothColors (bool)

_src (float)

c_bullish (color)

c_bearish (color)

zigzagCalc(Depth, Deviation, Backstep, repaint, Show_zz, line_thick, text_color)

Parameters:

Depth (int)

Deviation (int)

Backstep (int)

repaint (bool)

Show_zz (bool)

line_thick (int)

text_color (color)

RelativeValue█ OVERVIEW

This library is a Pine Script™ programmer's tool offering the ability to compute relative values, which represent comparisons of current data points, such as volume, price, or custom indicators, with their analogous historical data points from corresponding time offsets. This approach can provide insightful perspectives into the intricate dynamics of relative market behavior over time.

█ CONCEPTS

Relative values

In this library, a relative value is a metric that compares a current data point in a time interval to an average of data points with corresponding time offsets across historical periods. Its purpose is to assess the significance of a value by considering the historical context within past time intervals.

For instance, suppose we wanted to calculate relative volume on an hourly chart over five daily periods, and the last chart bar is two hours into the current trading day. In this case, we would compare the current volume to the average of volume in the second hour of trading across five days. We obtain the relative volume value by dividing the current volume by this average.

This form of analysis rests on the hypothesis that substantial discrepancies or aberrations in present market activity relative to historical time intervals might help indicate upcoming changes in market trends.

Cumulative and non-cumulative values

In the context of this library, a cumulative value refers to the cumulative sum of a series since the last occurrence of a specific condition (referred to as `anchor` in the function definitions). Given that relative values depend on time, we use time-based conditions such as the onset of a new hour, day, etc. On the other hand, a non-cumulative value is simply the series value at a specific time without accumulation.

Calculating relative values

Four main functions coordinate together to compute the relative values: `maintainArray()`, `calcAverageByTime()`, `calcCumulativeSeries()`, and `averageAtTime()`. These functions are underpinned by a `collectedData` user-defined type (UDT), which stores data collected since the last reset of the timeframe along with their corresponding timestamps. The relative values are calculated using the following procedure:

1. The `averageAtTime()` function invokes the process leveraging all four of the methods and acts as the main driver of the calculations. For each bar, this function adds the current bar's source and corresponding time value to a `collectedData` object.

2. Within the `averageAtTime()` function, the `maintainArray()` function is called at the start of each anchor period. It adds a new `collectedData` object to the array and ensures the array size does not exceed the predefined `maxSize` by removing the oldest element when necessary. This method plays an essential role in limiting memory usage and ensuring only relevant data over the desired number of periods is in the calculation window.

3. Next, the `calcAverageByTime()` function calculates the average value of elements within the `data` field for each `collectedData` object that corresponds to the same time offset from each anchor condition. This method accounts for cases where the current index of a `collectedData` object exceeds the last index of any past objects by using the last available values instead.

4. For cumulative calculations, the `averageAtTime()` function utilizes the `isCumulative` boolean parameter. If true, the `calcCumulativeSeries()` function will track the running total of the source data from the last bar where the anchor condition was met, providing a cumulative sum of the source values from one anchor point to the next.

To summarize, the `averageAtTime()` function continually stores values with their corresponding times in a `collectedData` object for each bar in the anchor period. When the anchor resets, this object is added to a larger array. The array's size is limited by the specified number of periods to be averaged. To correlate data across these periods, time indexing is employed, enabling the function to compare corresponding points across multiple periods.

█ USING THIS LIBRARY

The library simplifies the complex process of calculating relative values through its intuitive functions. Follow the steps below to use this library in your scripts.

Step 1: Import the library and declare inputs

Import the library and declare variables based on the user's input. These can include the timeframe for each period, the number of time intervals to include in the average, and whether the calculation uses cumulative values. For example:

//@version=5

import TradingView/RelativeValue/1 as TVrv

indicator("Relative Range Demo")

string resetTimeInput = input.timeframe("D")

int lengthInput = input.int(5, "No. of periods")

Step 2: Define the anchor condition

With these inputs declared, create a condition to define the start of a new period (anchor). For this, we use the change in the time value from the input timeframe:

bool anchor = timeframe.change(resetTimeInput)

Step 3: Calculate the average

At this point, one can calculate the average of a value's history at the time offset from the anchor over a number of periods using the `averageAtTime()` function. In this example, we use True Range (TR) as the `source` and set `isCumulative` to false:

float pastRange = TVrv.averageAtTime(ta.tr, lengthInput, anchor, false)

Step 4: Display the data

You can visualize the results by plotting the returned series. These lines display the non-cumulative TR alongside the average value over `lengthInput` periods for relative comparison:

plot(pastRange, "Past True Range Avg", color.new(chart.bg_color, 70), 1, plot.style_columns)

plot(ta.tr, "True Range", close >= open ? color.new(color.teal, 50) : color.new(color.red, 50), 1, plot.style_columns)

This example will display two overlapping series of columns. The green and red columns depict the current TR on each bar, and the light gray columns show the average over a defined number of periods, e.g., the default inputs on an hourly chart will show the average value at the hour over the past five days. This comparative analysis aids in determining whether the range of a bar aligns with its typical historical values or if it's an outlier.

█ NOTES

• The foundational concept of this library was derived from our initial Relative Volume at Time script. This library's logic significantly boosts its performance. Keep an eye out for a forthcoming updated version of the indicator. The demonstration code included in the library emulates a streamlined version of the indicator utilizing the library functions.

• Key efficiencies in the data management are realized through array.binary_search_leftmost() , which offers a performance improvement in comparison to its loop-dependent counterpart.

• This library's architecture utilizes user-defined types (UDTs) to create custom objects which are the equivalent of variables containing multiple parts, each able to hold independent values of different types . The recently added feature was announced in this blog post.

• To enhance readability, the code substitutes array functions with equivalent methods .

Look first. Then leap.

█ FUNCTIONS

This library contains the following functions:

calcCumulativeSeries(source, anchor)

Calculates the cumulative sum of `source` since the last bar where `anchor` was `true`.

Parameters:

source (series float) : Source used for the calculation.

anchor (series bool) : The condition that triggers the reset of the calculation. The calculation is reset when `anchor` evaluates to `true`, and continues using the values accumulated since the previous reset when `anchor` is `false`.

Returns: (float) The cumulative sum of `source`.

averageAtTime(source, length, anchor, isCumulative)

Calculates the average of all `source` values that share the same time difference from the `anchor` as the current bar for the most recent `length` bars.

Parameters:

source (series float) : Source used for the calculation.

length (simple int) : The number of reset periods to consider for the average calculation of historical data.

anchor (series bool) : The condition that triggers the reset of the average calculation. The calculation is reset when `anchor` evaluates to `true`, and continues using the values accumulated since the previous reset when `anchor` is `false`.

isCumulative (simple bool) : If `true`, `source` values are accumulated until the next time `anchor` is `true`. Optional. The default is `true`.

Returns: (float) The average of the source series at the specified time difference.

AoDivergenceLibrary_Library "AoDivergenceLibrary_"

this has functions which calculate and plot divergences which are used for ao divergences. essentially, this finds divergences by using the ao divergence logic. this logic has been used in "AO Hid & Reg Div with LC & Kernel".

regBullDivergence(swingLow, osc, colour)

Parameters:

swingLow (bool)

osc (float)

colour (color)

regBearDivergence(swingHigh, osc, colour)

Parameters:

swingHigh (bool)

osc (float)

colour (color)

hidBullDivergence(swingHigh, osc, colour)

Parameters:

swingHigh (bool)

osc (float)

colour (color)

hidBearDivergence(swingHigh, osc, colour)

Parameters:

swingHigh (bool)

osc (float)

colour (color)

HelperTALibrary "HelperTA"

This library contains useful technical indicators that I use regularly in my charts.

`stockRSI` is not mine, but included because used often and referenced by internal functions.

`DCO` is a normalisation of the donchian channels; the price relative to the donchian channels, on a range.

`MarketCycle` is a weighted aggregate of RSI, Stochastic RSI & DCO (demo on the chart)

stockRSI(src, K, D, rsiPeriod, stochPeriod)

stockRSI

Parameters:

src (float)

K (int)

D (int)

rsiPeriod (simple int)

stochPeriod (int)

Returns:

DCO(price, donchianPeriod, smaPeriod)

DCO

Parameters:

price (float)

donchianPeriod (int)

smaPeriod (int)

Returns:

MarketCycle(donchianPrice, rsiPrice, srsiPrice, donchianPeriod, donchianSmoothing, rsiPeriod, rsiSmoothing, srsiPeriod, srsiSmoothing, srsiK, srsiD, rsiWeight, srsiWeight, dcoWeight)

MarketCycle

Parameters:

donchianPrice (float)

rsiPrice (float)

srsiPrice (float)

donchianPeriod (simple int)

donchianSmoothing (simple int)

rsiPeriod (simple int)

rsiSmoothing (int)

srsiPeriod (simple int)

srsiSmoothing (simple int)

srsiK (simple int)

srsiD (simple int)

rsiWeight (simple float)

srsiWeight (simple float)

dcoWeight (simple float)

Returns:

CurrentlyPositionIndicatorLibrary "CurrentlyPositionIndicator"

Currently position indicator

run(_index, _price, _stoploss, _high, _low, _side, _is_entered, _colors, _position_left, _box_width)

Currently positions indicator

Parameters:

_index (int) : entry index

_price (float) : entry price

_stoploss (float) : stoploss price

_high (float) : range high

_low (float) : range low

_side (int)

_is_entered (bool) : is entered

_colors (color ) : color array

_position_left (int) : Left position

_box_width (int) : box's width

Returns: TODO: add what function returns

BankNifty_CSMLibrary "BankNifty_CSM"

TODO: add library description here

getLtp_N_Chang(openPrice, closePrice, highPrice, hl2Price, lowPrice, hlc3Price, bankNiftyClose)

Parameters:

openPrice (float)

closePrice (float)

highPrice (float)

hl2Price (float)

lowPrice (float)

hlc3Price (float)

bankNiftyClose (float)

ka66: lib/MovingAveragesLibrary "MovingAverages"

Exotic or Interesting Moving Averages Collection. Just the one right now!

alphaConfigurableEma(src, alpha, nSmooth)

Calculates a variation of the EMA by specifying a custom alpha value.

Parameters:

src (float) : a float series to get the EMA for, e.g. close, hlc3, etc.

alpha (float) : a value between 0 (ideally greater, to get any MA!) and 1. Closer

to one makes it more responsive, and choppier.

nSmooth (int) : Just applies the same alpha and EMA to the last Alpha-EMA output.

A value between 0 and 10 (just keeping a a reasonable bound). The idea is

you can first use a reasonably high alpha, then smooth it out. Default 0,

no further smoothing.

Returns: MA series.

bands(src, multiplier)

Calculates fixed bands around a series, can be any series, though the intent

here is for MA series.

Parameters:

src (float) : a float series.

multiplier (float) : a value greater than or equal to 0 (ideally greater, to get any MA!),

determines the width of the bands. Start with small float values, or it may go

beyond the scale, e.g. 0.005.

Returns: a 2-tuple of (upBand, downBand)

Spider_PlotIntroduction:

Spider charts, also known as radar charts or web charts, are a powerful data visualization tool that can display multiple variables in a circular format. They are particularly useful when you want to compare different data sets or evaluate the performance of a single data set across multiple dimensions. In this blog post, we will dive into the world of spider charts, explore their benefits, and demonstrate how you can create your own spider chart using the Spider_Plot library.

Why Spider Charts are Cool:

Spider charts have a unique visual appeal that sets them apart from other chart types. They allow you to display complex data in a compact, easy-to-understand format, making them perfect for situations where you need to convey a lot of information in a limited space. Some of the key benefits of spider charts include:

Multi-dimensional analysis: Spider charts can display multiple variables at once, making them ideal for analyzing relationships between different data sets or examining a single data set across multiple dimensions.

Easy comparison: By displaying data in a circular format, spider charts make it simple to compare different data points, identify trends, and spot potential issues.

Versatility: Spider charts can be used for a wide range of applications, from business and finance to sports and health. They are particularly useful for situations where you need to analyze performance or make comparisons between different entities.

Creating Your Own Spider Chart with the Spider_Plot Library:

The Spider_Plot library is a user-friendly, easy-to-use tool that allows you to create stunning spider charts with minimal effort. To get started, you'll need to import the Spider_Plot library:

import peacefulLizard50262/Spider_Plot/1

With the library imported, you can now create your own spider chart. The first step is to normalize your data. Normalizing ensures that all data points fall within the 0 to 1 range, which is important for creating a visually balanced spider chart.

The Spider_Plot library provides the data_normalize function to help you normalize your data. This function accepts several parameters, including the normalization style ("All Time", "Range", or "Custom"), length of the range, outlier level, lookback period for standard deviation, and minimum and maximum values for the "Custom" normalization style.

Once you have normalized your data, you can create an array of your data points using the array.from function. This array will be used as input for the draw_spider_plot function, which is responsible for drawing the spider plot on your chart.

The draw_spider_plot function accepts an array of float values (the normalized data points), an array of background colors for each sector, a color for the axes, and a scaling factor.

Example Usage:

Here's an example script that demonstrates how to create a spider chart using the Spider_Plot library:

oc = data_normalize(ta.ema(math.abs(open - close), 20), "Range", 20)

// Create an array of your data points

data = array.from(tr, rsi, stoch, dev, tr, oc, tr)

// Define colors for each sector

colors = array.from(color.new(color.red, 90), color.new(color.blue, 90), color.new(color.green, 90), color.new(color.orange, 90), color.new(color.purple, 90), color.new(color.purple, 90), color.new(color.purple, 90))

// Draw the spider plot on your chart

draw_spider_plot(data, colors, color.gray, 100)

In this example, we have first normalized six different data points (rsi, source, stoch, dev, tr, and oc) using the data_normalize function. Next, we create an array of these normalized data points and define an array of colors for each sector of the spider chart. Finally, we call the draw_spider_plot function to draw the spider chart on our chart.

Conclusion:

Spider charts are a versatile and visually appealing tool for analyzing and comparing multi-dimensional data. With the Spider_Plot library, you can easily create your own spider charts and unlock valuable insights from your data. Just remember to normalize your data and create an array of data points before calling the draw_spider_plot function. Happy charting!

Library "Spider_Plot"

data_normalize(data, style, length, outlier_level, dev_lookback, min, max)

data_normalize(data, string style, int length, float outlier_level, simple int dev_lookback, float min, float max)

Parameters:

data (float) : float , A float value to normalize.

style (string) : string , The normalization style: "All Time", "Range", or "Custom".

length (int) : int , The length of the range for "Range" normalization style.

outlier_level (float) : float , The outlier level to exclude from calculations.

dev_lookback (simple int) : int , The lookback period for calculating the standard deviation.

min (float) : float , The minimum value for the "Custom" normalization style.

max (float) : float , The maximum value for the "Custom" normalization style.

Returns: array , The normalized float value.

draw_spider_plot(values, bg_colors, axes_color, scale)

draw_spider_plot(array values, array bg_colors, color axes_color, float scale)

Parameters:

values (float ) : array , An array of float values to plot in the spider plot.

bg_colors (color ) : array , An array of background colors for each sector in the spider plot.

axes_color (color) : color , The color of the axes in the spider plot. Default: color.gray

scale (float) : float , A scaling factor for the spider plot. Default: 10

Returns: void , Draws the spider plot on the chart.

ReversalChartPatternLibraryLibrary "ReversalChartPatternLibrary"

User Defined Types and Methods for reversal chart patterns - Double Top, Double Bottom, Triple Top, Triple Bottom, Cup and Handle, Inverted Cup and Handle, Head and Shoulders, Inverse Head and Shoulders

method delete(this)

Deletes the drawing components of ReversalChartPatternDrawing object

Namespace types: ReversalChartPatternDrawing

Parameters:

this (ReversalChartPatternDrawing) : ReversalChartPatternDrawing object

Returns: current ReversalChartPatternDrawing object

method delete(this)

Deletes the drawing components of ReversalChartPattern object. In turn calls the delete of ReversalChartPatternDrawing

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: current ReversalChartPattern object

method lpush(this, obj, limit, deleteOld)

Array push with limited number of items in the array. Old items are deleted when new one comes and exceeds the limit

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern ) : array object

obj (ReversalChartPattern) : ReversalChartPattern object which need to be pushed to the array

limit (int) : max items on the array. Default is 10

deleteOld (bool) : If set to true, also deletes the drawing objects. If not, the drawing objects are kept but the pattern object is removed from array. Default is false.

Returns: current ReversalChartPattern object

method draw(this)

Draws the components of ReversalChartPatternDrawing

Namespace types: ReversalChartPatternDrawing

Parameters:

this (ReversalChartPatternDrawing) : ReversalChartPatternDrawing object

Returns: current ReversalChartPatternDrawing object

method draw(this)

Draws the components of ReversalChartPatternDrawing within the ReversalChartPattern object.

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: current ReversalChartPattern object

method scan(zigzag, patterns, errorPercent, shoulderStart, shoulderEnd)

Scans zigzag for ReversalChartPattern occurences

Namespace types: zg.Zigzag

Parameters:

zigzag (Zigzag type from HeWhoMustNotBeNamed/ZigzagTypes/2) : ZigzagTypes.Zigzag object having array of zigzag pivots and other information on each pivots

patterns (ReversalChartPattern ) : Existing patterns array. Used for validating duplicates

errorPercent (float) : Error threshold for considering ratios. Default is 13

shoulderStart (float) : Starting range of shoulder ratio. Used for identifying shoulders, handles and necklines

shoulderEnd (float) : Ending range of shoulder ratio. Used for identifying shoulders, handles and necklines

Returns: int pattern type

method createPattern(zigzag, patternType, patternColor, riskAdjustment)

Create Pattern from ZigzagTypes.Zigzag object

Namespace types: zg.Zigzag

Parameters:

zigzag (Zigzag type from HeWhoMustNotBeNamed/ZigzagTypes/2) : ZigzagTypes.Zigzag object having array of zigzag pivots and other information on each pivots

patternType (int) : Type of pattern being created. 1 - Double Tap, 2 - Triple Tap, 3 - Cup and Handle, 4 - Head and Shoulders

patternColor (color) : Color in which the patterns are drawn

riskAdjustment (float) : Used for calculating stops

Returns: ReversalChartPattern object created

method getName(this)

get pattern name of ReversalChartPattern object

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: string name of the pattern

method getDescription(this)

get consolidated description of ReversalChartPattern object

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: string consolidated description

method init(this)

initializes the ReversalChartPattern object and creates sub object types

Namespace types: ReversalChartPattern

Parameters:

this (ReversalChartPattern) : ReversalChartPattern object

Returns: ReversalChartPattern current object

ReversalChartPatternDrawing

Type which holds the drawing objects for Reversal Chart Pattern Types

Fields:

patternLines (Line type from HeWhoMustNotBeNamed/DrawingTypes/1) : array of Line objects representing pattern

entry (Line type from HeWhoMustNotBeNamed/DrawingTypes/1) : Entry price Line

target (Line type from HeWhoMustNotBeNamed/DrawingTypes/1) : Target price Line

patternLabel (Label type from HeWhoMustNotBeNamed/DrawingTypes/1)

ReversalChartPattern

Reversal Chart Pattern master type which holds the pattern components, drawings and trade details

Fields:

pivots (Pivot type from HeWhoMustNotBeNamed/ZigzagTypes/2) : Array of Zigzag Pivots forming the pattern

patternType (series int) : Defines the main type of pattern 1 - Double Tap, 1 - Triple Tap, 3 - Cup and Handle, 4 - Head and Shoulders

patternColor (series color) : Color in which the pattern will be drawn on chart

riskAdjustment (series float) : Percentage adjustment of risk. Used for setting stops

drawing (ReversalChartPatternDrawing) : ReversalChartPatternDrawing object which holds the drawing components

trade (Trade type from HeWhoMustNotBeNamed/TradeTracker/1) : TradeTracker.Trade object holding trade components

TradeTrackerLibrary "TradeTracker"

Simple Library for tracking trades

method track(this)

tracks trade when called on every bar

Namespace types: Trade

Parameters:

this (Trade) : Trade object

Returns: current Trade object

Trade

Has the constituents to track trades generated by any method.

Fields:

id (series int)

direction (series int) : Trade direction. Positive values for long and negative values for short trades

initialEntry (series float) : Initial entry price. This value will not change even if the entry is changed in the lifecycle of the trade

entry (series float) : Updated entry price. Allows variations to initial calculated entry. Useful in cases of trailing entry.

initialStop (series float) : Initial stop. Similar to initial entry, this is the first calculated stop for the lifecycle of trade.

stop (series float) : Trailing Stop. If there is no trailing, the value will be same as that of initial trade

targets (float ) : array of target values.

startBar (series int) : bar index of starting bar. Set by default when object is created. No need to alter this after that.

endBar (series int) : bar index of last bar in trade. Set by tracker on each execution

startTime (series int) : time of the start bar. Set by default when object is created. No need to alter this after that.

endTime (series int) : time of the ending bar. Updated by tracking method.

status (series int) : Integer parameter to track the status of the trade

retest (series bool) : Boolean parameter to notify if there was retest of the entry price

peacefulIndicatorsWe are delighted to present the PeacefulIndicators library, a modest yet powerful collection of custom technical indicators created to enhance your trading analysis. The library features an array of practical tools, including MACD with Dynamic Length, Stochastic RSI with ATR Stop Loss, Bollinger Bands with RSI Divergence, and more.

The PeacefulIndicators library offers the following functions:

macdDynamicLength: An adaptive version of the classic MACD indicator, which adjusts the lengths of the moving averages based on the dominant cycle period, providing a more responsive signal.

rsiDivergence: A unique implementation of RSI Divergence detection that identifies potential bullish and bearish divergences using a combination of RSI and linear regression.

trendReversalDetection: A helpful tool for detecting trend reversals using the Rate of Change (ROC) and Moving Averages, offering valuable insights into possible market shifts.

volume_flow_oscillator: A custom oscillator that combines price movement strength and volume to provide a unique perspective on market dynamics.

weighted_volatility_oscillator: Another custom oscillator that factors in price volatility and volume to deliver a comprehensive view of market fluctuations.

rvo: The Relative Volume Oscillator highlights changes in volume relative to historical averages, helping to identify potential breakouts or reversals.

acb: The Adaptive Channel Breakout indicator combines a moving average with an adjustable volatility multiplier to create dynamic channels, useful for identifying potential trend shifts.

We hope this library proves to be a valuable addition to your trading toolbox.

Library "peacefulIndicators"

A custom library of technical indicators for trading analysis, including MACD with Dynamic Length, Stochastic RSI with ATR Stop Loss, Bollinger Bands with RSI Divergence, and more.

macdDynamicLength(src, shortLen, longLen, signalLen, dynLow, dynHigh)

Moving Average Convergence Divergence with Dynamic Length

Parameters:

src (float) : Series to use

shortLen (int) : Shorter moving average length

longLen (int) : Longer moving average length

signalLen (int) : Signal line length

dynLow (int) : Lower bound for the dynamic length

dynHigh (int) : Upper bound for the dynamic length

Returns: tuple of MACD line and Signal line

Computes MACD using lengths adapted based on the dominant cycle period

rsiDivergence(src, rsiLen, divThreshold, linRegLength)

RSI Divergence Detection

Parameters:

src (float) : Series to use

rsiLen (simple int) : Length for RSI calculation

divThreshold (float) : Divergence threshold for RSI

linRegLength (int) : Length for linear regression calculation

Returns: tuple of RSI Divergence (positive, negative)

Computes RSI Divergence detection that identifies bullish (positive) and bearish (negative) divergences

trendReversalDetection(src, rocLength, maLength, maType)

Trend Reversal Detection (TRD)

Parameters:

src (float) : Series to use