Стандартное отклонение (волатильность)

Dorsey InertiaThis indicator was originally developed by Donald Dorsey (Stocks & Commodities, V.13:9 (September, 1995): "Refining the Relative Volatility Index").

Inertia is based on Relative Volatility Index (RVI) smoothed using linear regression.

In physics, inertia is the tendency of an object to resist to acceleration. Dorsey chose this name because he believes that trend and inertia are related and that it takes more effort and energy to reverse the direction of a stock or market than to keep it in the same direction. He argues that the volatility is the simplest and most accurate measure of inertia.

When the indicator is below 50, it signals bearish market sentiment and when the indicator is above 50 it signals a bullish trend.

Good luck!

Stiffness IndicatorThis indicator was originally developed by Markos Katsanos (Stocks & Commodities, V.36:12 (November, 2018): "The Stiffness Indicator").

Like and follow for more open source indicators!

Happy Trading!

Ehlers Fisherized Deviation-Scaled OscillatorEhlers Fisherized Deviation-Scaled Oscillator script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 36:11: Probability - Probably A Good Thing To Know).

Ehlers Deviation-Scaled Moving Average (DSMA)Ehlers Deviation-Scaled Moving Average indicator script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 36:8: The Deviation-Scaled Moving Average).

Relative Volatility IndexCorrected Relative Volatility Index. This indicator was originally developed by Donald Dorsey (Stocks & Commodities V.11:6 (253-256): The Relative Volatility Index).

The indicator was revised by Dorsey in 1995 (Stocks & Commodities V.13:09 (388-391): Refining the Relative Volatility Index).

I suggest the refined RVI with optional settings. If you disabled Wilder's Smoothing and Refined RVI you will get the original version of RVI (1993, as built-in).

Also, you can choose an algorithm for calculating Standard Deviation.

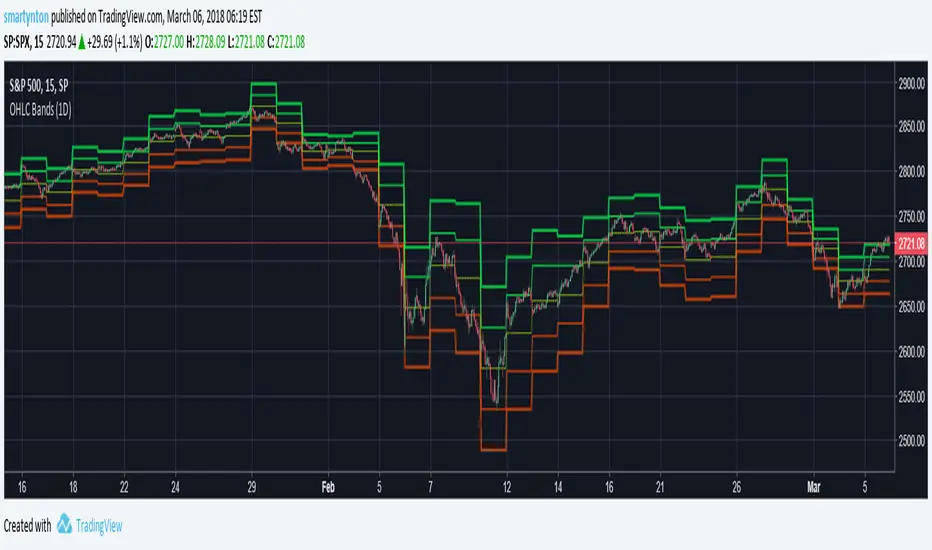

OHLC Daily Resolution BandsShout out to nPE- for the idea.

Bands made with stdev from 10 day OHLC.

Keeps resolution to daily, so you can use bands as daily pivots for day trading.

Upper band 1=yesterday close + 0.5 std(ohlc,10)

Upper band 1=yesterday close + 1 std(ohlc,10)

Mid=yesterday close

Lower band 1=yesterday close - 0.5 std(ohlc,10)

Lower band 2=yesterday close - 1 std(ohlc,1

BBLathe2: Bollinger Band Lathe w/ Elder's Force Index [sclark39]Welcome to the second version of the BBLathe!

This shows Bollinger Bands centered on a horizontal basis, to make it easier to see how volatility is changing and identify squeeze opportunities. By default Bollinger bands are calculated using an exponential moving average and an improved higher precision stdev implementation, but this can be disabled. Version 2 also shows Elder's Force Index as a white histogram, so you can see some volume information to help confirm the power of the bears/bulls. The green/red shadow shows how the Bollinger's basis is changing, and when it is going up there will be a green shadow underneath the basis line (this can be inverted in the settings). There is also price line (yellow) showing the location of the price within the Bollinger Bands.

Use this indicator for trades at your own risk, I made this for fun and it is not a trade recommendation.

That being said, if you like my work please tip me!

ETH: 0xf8E0Ea503B5c833fD4546E7fa2c70EcE42A27C8A

Please comment with feedback and requests!

Bollinger Bands + 2 MA (Exponential)Basic Bollinger Bands implementation, with the option to use an exponential moving average and a more accurate stdev function than the builtin. This also includes two extra MA lines which can be tuned as you like, to reduce the number of indicators needed (the bollinger basis is also a moving average, so in total you get 3MA out of this indicator). This draws an inner/outer envelope which can be tuned, by default it is set to 1-2STDEV.

This uses the same same improvement to stdev as my other bollinger indicator:

See more info about the bultin stdev here:

OHLC Volatility Estimators by @Xel_arjonaDISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The embedded code and ideas within this work are FREELY AND PUBLICLY available on the Web for NON LUCRATIVE ACTIVITIES and must remain as is by Creative-Commons as TradingView's regulations. Any use, copy or re-use of this code should mention it's origin as it's authorship.

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED AS DEBUGING CODE The models included in the function have been taken from openly sources on the web so they could have some errors as in the calculation scheme and/or in it's programatic scheme. Debugging are welcome.

WHAT'S THIS?

Here's a full collection of candle based (compressed tick) Volatility Estimators given as a function, openly available for free, it can print IMPLIED VOLATILITY by an external symbol ticker like INDEX:VIX.

Models included in the volatility calculation function:

CLOSE TO CLOSE: This is the classic estimator by rule, sometimes referred as HISTORICAL VOLATILITY and is the must common, accepted and widely used out there. Is based on traditional Standard Deviation method derived from the logarithm return of current close from yesterday's.

ELASTIC WEIGHTED MOVING AVERAGE: This estimator has been used by RiskMetriks®. It's calculation is based on an ElasticWeightedMovingAverage Standard Deviation method derived from the logarithm return of current close from yesterday's. It can be viewed or named as an EXPONENTIAL HISTORICAL VOLATILITY model.

PARKINSON'S: The Parkinson number, or High Low Range Volatility, developed by the physicist, Michael Parkinson, in 1980 aims to estimate the Volatility of returns for a random walk using the high and low in any particular period. IVolatility.com calculates daily Parkinson values. Prices are observed on a fixed time interval. n=10, 20, 30, 60, 90, 120, 150, 180 days.

ROGERS-SATCHELL: The Rogers-Satchell function is a volatility estimator that outperforms other estimators when the underlying follows a Geometric Brownian Motion (GBM) with a drift (historical data mean returns different from zero). As a result, it provides a better volatility estimation when the underlying is trending. However, this Rogers-Satchell estimator does not account for jumps in price (Gaps). It assumes no opening jump. The function uses the open, close, high, and low price series in its calculation and it has only one parameter, which is the period to use to estimate the volatility.

YANG-ZHANG: Yang and Zhang were the first to derive an historical volatility estimator that has a minimum estimation error, is independent of the drift, and independent of opening gaps. This estimator is maximally 14 times more efficient than the close-to-close estimator.

LOGARITHMIC GARMAN-KLASS: The former is a pinescript transcript of the model defined as in iVolatility . The metric used is a combination of the overnight, high/low and open/close range. Such a volatility metric is a more efficient measure of the degree of volatility during a given day. This metric is always positive.

ELASTIC WEIGHTED MOVING AVG with STDDEV BANDSImported from Stock & Commodities February 2017 month’s Traders’ Tips issue , from Vitali Apirine’s article in this issue, “Exponential Standard Deviation Bands.” Here, we present the February 2017 Traders’ Tips code with possible implementations in various software.

Volume (D)EMAA simple yet configurable indicator that shows recent traffic volumes.

The time period is specified as weeks/days/hours/minutes, not as bars.

Set the volume period to non-zero if you want to use a generalized double EMA instead of plain.

The "ratio" option will show the size of the current volume compared to the average volume as computed for the specified time period; say hello to fat tails and goodby to "standard" and "normal" and "average". With the "together" option, it compares the current volume to the both sides together (buy+sell), otherwise it compares it to just its respective side.

Volume (D)EMAA simple yet configurable indicator that shows recent traffic volumes.

The time period is specified as weeks/days/hours/minutes, not as bars.

Set the volume period to non-zero if you want to use a generalized double EMA instead of plain.

The ratio option will show the size of the current volume compared to the volume in the specified time period (expect to see something very non-Gaussian, say goodby to trusting your ATR and stddev, and say hello to fat tails.) With the "together" option, it compares the current volume to the both sides together (buy+sell), otherwise it compares it to just its own.

Standard Error Bands by @XeL_arjonaStandard Error Bands - Code by @XeL_arjona

Original implementation by:

Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

Version 1

For a quick and publicly open explanation of this Statistical indicator, you can refer at Here!

Extract from the former URL:

Standard Error bands are quite different than Bollinger's. First, they are bands constructed around a linear regression curve. Second, the bands are based on two standard errors above and below this regression line. The error bands measure the standard error of the estimate around the linear regression line. Therefore, as a price series follows the course of the regression line the bands will narrow, showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands.