Dema Percentile Standard DeviationDema Percentile Standard Deviation

The Dema Percentile Standard Deviation indicator is a robust tool designed to identify and follow trends in financial markets.

How it works?

This code is straightforward and simple:

The price is smoothed using a DEMA (Double Exponential Moving Average).

Percentiles are then calculated on that DEMA.

When the closing price is below the lower percentile, it signals a potential short.

When the closing price is above the upper percentile and the Standard Deviation of the lower percentile, it signals a potential long.

Settings

Dema/Percentile/SD/EMA Length's: Defines the period over which calculations are made.

Dema Source: The source of the price data used in calculations.

Percentiles: Selects the type of percentile used in calculations (options include 60/40, 60/45, 55/40, 55/45). In these settings, 60 and 55 determine percentile for long signals, while 45 and 40 determine percentile for short signals.

Features

Fully Customizable

Fully Customizable: Customize colors to display for long/short signals.

Display Options: Choose to show long/short signals as a background color, as a line on price action, or as trend momentum in a separate window.

EMA for Confluence: An EMA can be used for early entries/exits for added signal confirmation, but it may introduce noise—use with caution!

Built-in Alerts.

Indicator on Diffrent Assets

INDEX:BTCUSD 1D Chart (6 high 56 27 60/45 14)

CRYPTO:SOLUSD 1D Chart (24 open 31 20 60/40 14)

CRYPTO:RUNEUSD 1D Chart (10 close 56 14 60/40 14)

Remember no indicator would on all assets with default setting so FAFO with setting to get your desired signal.

Стандартное отклонение (волатильность)

STANDARD DEVIATION INDICATOR BY WISE TRADERWISE TRADER STANDARD DEVIATION SETUP: The Ultimate Volatility and Trend Analysis Tool

Unlock the power of STANDARD DEVIATIONS like never before with the this indicator, a versatile and comprehensive tool designed for traders who seek deeper insights into market volatility, trend strength, and price action. This advanced indicator simultaneously plots three sets of customizable Deviations, each with unique settings for moving average types, standard deviations, and periods. Whether you’re a swing trader, day trader, or long-term investor, the STANDARD DEVIATION indicator provides a dynamic way to spot potential reversals, breakouts, and trend-following opportunities.

Key Features:

STANDARD DEVIATIONS Configuration : Monitor three different Bollinger Bands at the same time, allowing for multi-timeframe analysis within a single chart.

Customizable Moving Average Types: Choose from SMA, EMA, SMMA (RMA), WMA, and VWMA to calculate the basis of each band according to your preferred method.

Dynamic Standard Deviations: Set different standard deviation multipliers for each band to fine-tune sensitivity for various market conditions.

Visual Clarity: Color-coded bands with adjustable thicknesses provide a clear view of upper and lower boundaries, along with fill backgrounds to highlight price ranges effectively.

Enhanced Trend Detection: Identify potential trend continuation, consolidation, or reversal zones based on the position and interaction of price with the three bands.

Offset Adjustment: Shift the bands forward or backward to analyze future or past price movements more effectively.

Why Use Triple STANDARD DEVIATIONS ?

STANDARD DEVIATIONS are a popular choice among traders for measuring volatility and anticipating potential price movements. This indicator takes STANDARD DEVIATIONS to the next level by allowing you to customize and analyze three distinct bands simultaneously, providing an unparalleled view of market dynamics. Use it to:

Spot Volatility Expansion and Contraction: Track periods of high and low volatility as prices move toward or away from the bands.

Identify Overbought or Oversold Conditions: Monitor when prices reach extreme levels compared to historical volatility to gauge potential reversal points.

Validate Breakouts: Confirm the strength of a breakout when prices move beyond the outer bands.

Optimize Risk Management: Enhance your strategy's risk-reward ratio by dynamically adjusting stop-loss and take-profit levels based on band positions.

Ideal For:

Forex, Stocks, Cryptocurrencies, and Commodities Traders looking to enhance their technical analysis.

Scalpers and Day Traders who need rapid insights into market conditions.

Swing Traders and Long-Term Investors seeking to confirm entry and exit points.

Trend Followers and Mean Reversion Traders interested in combining both strategies for maximum profitability.

Harness the full potential of STANDARD DEVIATIONS with this multi-dimensional approach. The "STANDARD DEVIATIONS " indicator by WISE TRADER will become an essential part of your trading arsenal, helping you make more informed decisions, reduce risks, and seize profitable opportunities.

Who is WISE TRADER ?

Wise Trader is a highly skilled trader who launched his channel in 2020 during the COVID-19 pandemic, quickly building a loyal following. With thousands of paid subscribed members and over 70,000 YouTube subscribers, Wise Trader has become a trusted authority in the trading world. He is known for his ability to navigate significant events, such as the Indian elections and stock market crashes, providing his audience with valuable insights into market movements and volatility. With a deep understanding of macroeconomics and its correlation to global stock markets, Wise Trader shares informed strategies that help traders make better decisions. His content covers technical analysis, trading setups, economic indicators, and market trends, offering a comprehensive approach to understanding financial markets. The channel serves as a go-to resource for traders who want to enhance their skills and stay informed about key market developments.

E9 Bollinger RangeThe E9 Bollinger Range is a technical trading tool that leverages Bollinger Bands to track volatility and price deviations, along with additional trend filtering via EMAs.

The script visually enhances price action with a combination of trend-filtering EMAs, bar colouring for trend direction, signals to indicate potential buy and sell points based on price extension and engulfing patterns.

Here’s a breakdown of its key components:

Bollinger Bands: The strategy plots multiple Bollinger Band deviations to create different price levels. The furthest deviation bands act as warning signs for traders when price extends significantly, signaling potential overbought or oversold conditions.

Bar Colouring: Visual bar colouring is applied to clearly indicate trend direction: green bars for an uptrend and red bars for a downtrend.

EMA Filtering: Two EMAs (50 and 200) are used to help filter out false signals, giving traders a better sense of the underlying trend.

This combination of signals, visual elements, and trend filtering provides traders with a systematic approach to identifying price deviations and taking advantage of market corrections.

Brief History of Bollinger Bands

Bollinger Bands were developed by John Bollinger in the early 1980s as a tool to measure price volatility in financial markets. The bands consist of a moving average (typically 20 periods) with upper and lower bands placed two standard deviations away. These bands expand and contract based on market volatility, offering traders a visual representation of price extremes and potential reversal zones.

John Bollinger’s work revolutionized technical analysis by incorporating volatility into trend detection. His bands remain widely used across markets, including stocks, commodities, and cryptocurrencies. With the ability to highlight overbought and oversold conditions, Bollinger Bands have become a staple in many trading strategies.

Standard Deviation-Based Fibonacci Band by zdmre This indicator is designed to better understand market dynamics by focusing on standard deviation and the Fibonacci sequence. This indicator includes the following components to assist investors in analyzing price movements:

Weighted Moving Average (WMA) : The indicator creates a central band by utilizing the weighted moving average of standard deviation. WMA provides a more current and accurate representation by giving greater weight to recent prices. This central band offers insights into the general trend of the market, helping to identify potential buying and selling opportunities.

Fibonacci Bands : The Fibonacci bands located above and below the central band illustrate potential support and resistance levels for prices. These bands enable investors to pinpoint areas where the price may exhibit indecisiveness. When prices move within these bands, it may be challenging for investors to discern the market's preferred direction.

Indecisiveness Representation : When prices fluctuate between the Fibonacci bands, they may reflect a state of indecisiveness. This condition is critical for identifying potential reversal points and trend changes. Investors can evaluate these periods of indecisiveness to develop suitable buying and selling strategies.

This indicator is designed to assist investors in better analyzing market trends and supporting their decision-making processes. The integration of standard deviation and the Fibonacci sequence offers a new perspective on understanding market movements.

#DYOR

Sinc Bollinger BandsKaiser Windowed Sinc Bollinger Bands Indicator

The Kaiser Windowed Sinc Bollinger Bands indicator combines the advanced filtering capabilities of the Kaiser Windowed Sinc Moving Average with the volatility measurement of Bollinger Bands. This indicator represents a sophisticated approach to trend identification and volatility analysis in financial markets.

Core Components

At the heart of this indicator is the Kaiser Windowed Sinc Moving Average, which utilizes the sinc function as an ideal low-pass filter, windowed by the Kaiser function. This combination allows for precise control over the frequency response of the moving average, effectively separating trend from noise in price data.

The sinc function, representing an ideal low-pass filter, provides the foundation for the moving average calculation. By using the sinc function, analysts can independently control two critical parameters: the cutoff frequency and the number of samples used. The cutoff frequency determines which price movements are considered significant (low frequency) and which are treated as noise (high frequency). The number of samples influences the filter's accuracy and steepness, allowing for a more precise approximation of the ideal low-pass filter without altering its fundamental frequency response characteristics.

The Kaiser window is applied to the sinc function to create a practical, finite-length filter while minimizing unwanted oscillations in the frequency domain. The alpha parameter of the Kaiser window allows users to fine-tune the trade-off between the main-lobe width and side-lobe levels in the frequency response.

Bollinger Bands Implementation

Building upon the Kaiser Windowed Sinc Moving Average, this indicator adds Bollinger Bands to provide a measure of price volatility. The bands are calculated by adding and subtracting a multiple of the standard deviation from the moving average.

Advanced Centered Standard Deviation Calculation

A unique feature of this indicator is its specialized standard deviation calculation for the centered mode. This method employs the Kaiser window to create a smooth deviation that serves as an highly effective envelope, even though it's always based on past data.

The centered standard deviation calculation works as follows:

It determines the effective sample size of the Kaiser window.

The window size is then adjusted to reflect the target sample size.

The source data is offset in the calculation to allow for proper centering.

This approach results in a highly accurate and smooth volatility estimation. The centered standard deviation provides a more refined and responsive measure of price volatility compared to traditional methods, particularly useful for historical analysis and backtesting.

Operational Modes

The indicator offers two operational modes:

Non-Centered (Real-time) Mode: Uses half of the windowed sinc function and a traditional standard deviation calculation. This mode is suitable for real-time analysis and current market conditions.

Centered Mode: Utilizes the full windowed sinc function and the specialized Kaiser window-based standard deviation calculation. While this mode introduces a delay, it offers the most accurate trend and volatility identification for historical analysis.

Customizable Parameters

The Kaiser Windowed Sinc Bollinger Bands indicator provides several key parameters for customization:

Cutoff: Controls the filter's cutoff frequency, determining the divide between trends and noise.

Number of Samples: Sets the number of samples used in the FIR filter calculation, affecting the filter's accuracy and computational complexity.

Alpha: Influences the shape of the Kaiser window, allowing for fine-tuning of the filter's frequency response characteristics.

Standard Deviation Length: Determines the period over which volatility is calculated.

Multiplier: Sets the number of standard deviations used for the Bollinger Bands.

Centered Alpha: Specific to the centered mode, this parameter affects the Kaiser window used in the specialized standard deviation calculation.

Visualization Features

To enhance the analytical value of the indicator, several visualization options are included:

Gradient Coloring: Offers a range of color schemes to represent trend direction and strength for the moving average line.

Glow Effect: An optional visual enhancement for improved line visibility.

Background Fill: Highlights the area between the Bollinger Bands, aiding in volatility visualization.

Applications in Technical Analysis

The Kaiser Windowed Sinc Bollinger Bands indicator is particularly useful for:

Precise trend identification with reduced noise influence

Advanced volatility analysis, especially in the centered mode

Identifying potential overbought and oversold conditions

Recognizing periods of price consolidation and potential breakouts

Compared to traditional Bollinger Bands, this indicator offers superior frequency response characteristics in its moving average and a more refined volatility measurement, especially in centered mode. These features allow for a more nuanced analysis of price trends and volatility patterns across various market conditions and timeframes.

Conclusion

The Kaiser Windowed Sinc Bollinger Bands indicator represents a significant advancement in technical analysis tools. By combining the ideal low-pass filter characteristics of the sinc function, the practical benefits of Kaiser windowing, and an innovative approach to volatility measurement, this indicator provides traders and analysts with a sophisticated instrument for examining price trends and market volatility.

Its implementation in Pine Script contributes to the TradingView community by making advanced signal processing and statistical techniques accessible for experimentation and further development in technical analysis. This indicator serves not only as a practical tool for market analysis but also as an educational resource for those interested in the intersection of signal processing, statistics, and financial markets.

Related:

Fear/Greed Zone Reversals [UAlgo]The "Fear/Greed Zone Reversals " indicator is a custom technical analysis tool designed for TradingView, aimed at identifying potential reversal points in the market based on sentiment zones characterized by fear and greed. This indicator utilizes a combination of moving averages, standard deviations, and price action to detect when the market transitions from extreme fear to greed or vice versa. By identifying these critical turning points, traders can gain insights into potential buy or sell opportunities.

🔶 Key Features

Customizable Moving Averages: The indicator allows users to select from various types of moving averages (SMA, EMA, WMA, VWMA, HMA) for both fear and greed zone calculations, enabling flexible adaptation to different trading strategies.

Fear Zone Settings:

Fear Source: Select the price data point (e.g., close, high, low) used for Fear Zone calculations.

Fear Period: This defines the lookback window for calculating the Fear Zone deviation.

Fear Stdev Period: This sets the period used to calculate the standard deviation of the Fear Zone deviation.

Greed Zone Settings:

Greed Source: Select the price data point (e.g., close, high, low) used for Greed Zone calculations.

Greed Period: This defines the lookback window for calculating the Greed Zone deviation.

Greed Stdev Period: This sets the period used to calculate the standard deviation of the Greed Zone deviation.

Alert Conditions: Integrated alert conditions notify traders in real-time when a reversal in the fear or greed zone is detected, allowing for timely decision-making.

🔶 Interpreting Indicator

Greed Zone: A Greed Zone is highlighted when the price deviates significantly above the chosen moving average. This suggests market sentiment might be leaning towards greed, potentially indicating a selling opportunity.

Fear Zone Reversal: A Fear Zone is highlighted when the price deviates significantly below the chosen moving average of the selected price source. This suggests market sentiment might be leaning towards fear, potentially indicating a buying opportunity. When the indicator identifies a reversal from a fear zone, it suggests that the market is transitioning from a period of intense selling pressure to a more neutral or potentially bullish state. This is typically indicated by an upward arrow (▲) on the chart, signaling a potential buy opportunity. The fear zone is characterized by high price volatility and overselling, making it a crucial point for traders to consider entering the market.

Greed Zone Reversal: Conversely, a Greed Zone is highlighted when the price deviates significantly above the chosen moving average. This suggests market sentiment might be leaning towards greed, potentially indicating a selling opportunity. When the indicator detects a reversal from a greed zone, it indicates that the market may be moving from an overbought condition back to a more neutral or bearish state. This is marked by a downward arrow (▼) on the chart, suggesting a potential sell opportunity. The greed zone is often associated with overconfidence and high buying activity, which can precede a market correction.

🔶 Why offer multiple moving average types?

By providing various moving average types (SMA, EMA, WMA, VWMA, HMA) , the indicator offers greater flexibility for traders to tailor the indicator to their specific trading strategies and market preferences. Different moving averages react differently to price data and can produce varying signals.

SMA (Simple Moving Average): Provides an equal weighting to all data points within the specified period.

EMA (Exponential Moving Average): Gives more weight to recent data points, making it more responsive to price changes.

WMA (Weighted Moving Average): Allows for custom weighting of data points, providing more flexibility in the calculation.

VWMA (Volume Weighted Moving Average): Considers both price and volume data, giving more weight to periods with higher trading volume.

HMA (Hull Moving Average): A combination of weighted moving averages designed to reduce lag and provide a smoother curve.

Offering multiple options allows traders to:

Experiment: Traders can try different moving averages to see which one produces the most accurate signals for their specific market.

Adapt to different market conditions: Different market conditions may require different moving average types. For example, a fast-moving market might benefit from a faster moving average like an EMA, while a slower-moving market might be better suited to a slower moving average like an SMA.

Personalize: Traders can choose the moving average that best aligns with their personal trading style and risk tolerance.

In essence, providing a variety of moving average types empowers traders to create a more personalized and effective trading experience.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Bias Finder [UAlgo]The "Bias Finder " indicator is a tool designed to help traders identify market bias and trends effectively. This indicator leverages smoothed Heikin Ashi candles and oscillators to provide a clear visual representation of market trends and potential reversals. By utilizing higher timeframes and smoothing techniques, the indicator aims to filter out market noise and offer a more reliable signal for trading decisions.

🔶 Key Features

Heikin Ashi Candles: The indicator uses Heikin Ashi candles, a special type of candlestick that incorporates information from the previous candle to potentially provide smoother visuals and highlight potential trend direction.

Oscillator: The indicator calculates an oscillator based on the difference between the smoothed opening and closing prices of a higher timeframe. This oscillator helps visualize the strength of the bias.

Light Teal: Strong bullish trend.

Dark Teal: Weakening bullish trend.

Light Red: Strong bearish trend.

Dark Red: Weakening bearish trend.

Standard Deviation: The indicator can optionally display upper and lower standard deviation bands based on the Heikin Ashi high and low prices. These bands can help identify potential breakout areas.

Oscillator Period: Adjust the sensitivity of the oscillator.

Higher Timeframe: Select a timeframe for the Heikin Ashi candles and oscillator calculations (must be equal to or greater than the chart's timeframe).

Display Options: Choose whether to display Heikin Ashi candles, market bias fill, standard deviation bands, and HA candle colors based on the bias.

Alerts: Enable/disable specific alerts and customize their messages.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Premarket Std Dev BandsOverview

The Premarket Std Dev Bands indicator is a powerful Pine Script tool designed to help traders gain deeper insights into the premarket session's price movements. This indicator calculates and displays the standard deviation bands for premarket trading, providing valuable information on price volatility and potential support and resistance levels during the premarket hours.

Key Features

Premarket Focus: Specifically designed to analyze price movements during the premarket session, offering unique insights not available with traditional indicators.

Customizable Length: Users can adjust the averaging period for calculating the standard deviation, allowing for tailored analysis based on their trading strategy.

Standard Deviation Bands: Displays both 1 and 2 standard deviation bands, helping traders identify significant price movements and potential reversal points.

Real-Time Updates: Continuously updates the premarket open and close prices, ensuring the bands are accurate and reflective of current market conditions.

How It Works

Premarket Session Identification: The script identifies when the current bar is within the premarket session.

Track Premarket Prices: It tracks the open and close prices during the premarket session.

Calculate Premarket Moves: Once the premarket session ends, it calculates the price movement and stores it in an array.

Compute Averages and Standard Deviation: The script calculates the simple moving average (SMA) and standard deviation of the premarket moves over a specified period.

Plot Standard Deviation Bands: Based on the calculated standard deviation, it plots the 1 and 2 standard deviation bands around the premarket open price.

Usage

To utilize the Premarket Std Dev Bands indicator:

Add the script to your TradingView chart.

Adjust the Length input to set the averaging period for calculating the standard deviation.

Observe the plotted standard deviation bands during the premarket session to identify potential trading opportunities.

Benefits

Enhanced Volatility Analysis: Understand price volatility during the premarket session, which can be crucial for making informed trading decisions.

Support and Resistance Levels: Use the standard deviation bands to identify key support and resistance levels, aiding in better entry and exit points.

Customizable and Flexible: Tailor the averaging period to match your trading style and strategy, making this indicator versatile for various market conditions.

Support/Resistance v2 (ML) KmeanKmean with Standard Deviation Channel

1. Description of Kmean

Kmean (or K-means) is a popular clustering algorithm used to divide data into K groups based on their similarity. In the context of financial markets, Kmean can be applied to find the average price values over a specific period, allowing the identification of major trends and levels of support and resistance.

2. Application in Trading

In trading, Kmean is used to smooth out the price series and determine long-term trends. This helps traders make more informed decisions by avoiding noise and short-term fluctuations. Kmean can serve as a baseline around which other analytical tools, such as channels and bands, are constructed.

3. Description of Standard Deviation (stdev)

Standard deviation (stdev) is a statistical measure that indicates how much the values of data deviate from their mean value. In finance, standard deviation is often used to assess price volatility. A high standard deviation indicates strong price fluctuations, while a low standard deviation indicates stable movements.

4. Combining Kmean and Standard Deviation to Predict Short-Term Price Behavior

Combining Kmean and standard deviation creates a powerful tool for analyzing market conditions. Kmean shows the average price trend, while the standard deviation channels demonstrate the boundaries within which the price can fluctuate. This combination helps traders to:

Identify support and resistance levels.

Predict potential price reversals.

Assess risks and set stop-losses and take-profits.

Should you have any questions about code, please reach me at Tradingview directly.

Hope you find this script helpful!

Vwap Z-Score with Signals [UAlgo]The "VWAP Z-Score with Signals " is a technical analysis tool designed to help traders identify potential buy and sell signals based on the Volume Weighted Average Price (VWAP) and its Z-Score. This indicator calculates the VWAP Z-Score to show how far the current price deviates from the VWAP in terms of standard deviations. It highlights overbought and oversold conditions with visual signals, aiding in the identification of potential market reversals. The tool is customizable, allowing users to adjust parameters for their specific trading needs.

🔶 Features

VWAP Z-Score Calculation: Measures the deviation of the current price from the VWAP using standard deviations.

Customizable Parameters: Allows users to set the length of the VWAP Z-Score calculation and define thresholds for overbought and oversold levels.

Reversal Signals: Provides visual signals when the Z-Score crosses the specified thresholds, indicating potential buy or sell opportunities.

🔶 Usage

Extreme Z-Score values (both positive and negative) highlight significant deviations from the VWAP, useful for identifying potential reversal points.

The indicator provides visual signals when the Z-Score crosses predefined thresholds:

A buy signal (🔼) appears when the Z-Score crosses above the lower threshold, suggesting the price may be oversold and a potential upward reversal.

A sell signal (🔽) appears when the Z-Score crosses below the upper threshold, suggesting the price may be overbought and a potential downward reversal.

These signals can help you identify potential entry and exit points in your trading strategy.

🔶 Disclaimer

The "VWAP Z-Score with Signals " indicator is designed for educational purposes and to assist traders in their technical analysis. It does not guarantee profitable trades and should not be considered as financial advice.

Users should conduct their own research and use this indicator in conjunction with other tools and strategies.

Trading involves significant risk, and it is possible to lose more than your initial investment.

Buy Sell Strategy With Z-Score [TradeDots]The "Buy Sell Strategy With Z-Score" is a trading strategy that harnesses Z-Score statistical metrics to identify potential pricing reversals, for opportunistic buying and selling opportunities.

HOW DOES IT WORK

The strategy operates by calculating the Z-Score of the closing price for each candlestick. This allows us to evaluate how significantly the current price deviates from its typical volatility level.

The strategy first takes the scope of a rolling window, adjusted to the user's preference. This window is used to compute both the standard deviation and mean value. With these values, the strategic model finalizes the Z-Score. This determination is accomplished by subtracting the mean from the closing price and dividing the resulting value by the standard deviation.

This approach provides an estimation of the price's departure from its traditional trajectory, thereby identifying market conditions conducive to an asset being overpriced or underpriced.

APPLICATION

Firstly, it is better to identify a stable trading pair for this technique, such as two stocks with considerable correlation. This is to ensure conformance with the statistical model's assumption of a normal Gaussian distribution model. The ideal performance is theoretically situated within a sideways market devoid of skewness.

Following pair selection, the user should refine the span of the rolling window. A broader window smoothens the mean, more accurately capturing long-term market trends, while potentially enhancing volatility. This refinement results in fewer, yet precise trading signals.

Finally, the user must settle on an optimal Z-Score threshold, which essentially dictates the timing for buy/sell actions when the Z-Score exceeds with thresholds. A positive threshold signifies the price veering away from its mean, triggering a sell signal. Conversely, a negative threshold denotes the price falling below its mean, illustrating an underpriced condition that prompts a buy signal.

Within a normal distribution, a Z-Score of 1 records about 68% of occurrences centered at the mean, while a Z-Score of 2 captures approximately 95% of occurrences.

The 'cool down period' is essentially the number of bars that await before the next signal generation. This feature is employed to dodge the occurrence of multiple signals in a short period.

DEFAULT SETUP

The following is the default setup on EURUSD 1h timeframe

Rolling Window: 80

Z-Score Threshold: 2.8

Signal Cool Down Period: 5

Commission: 0.03%

Initial Capital: $10,000

Equity per Trade: 30%

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

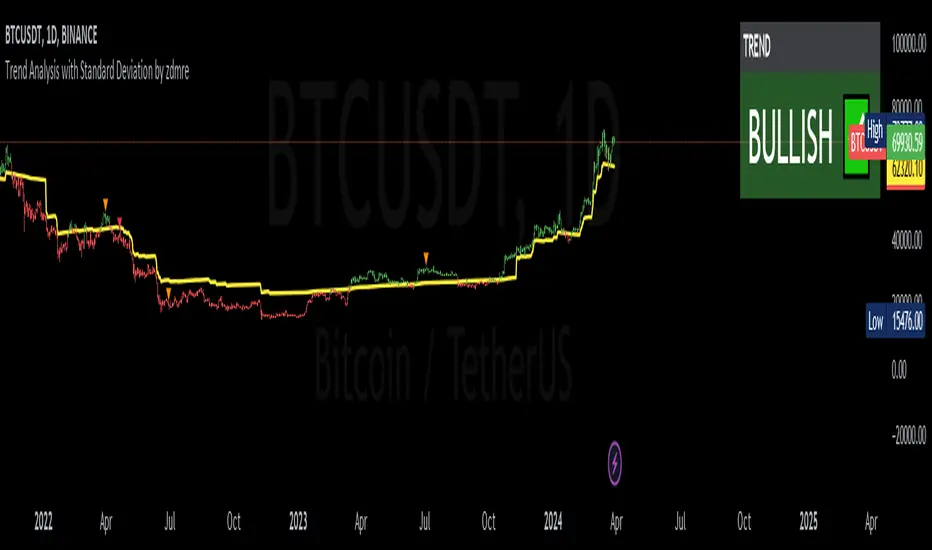

Trend Analysis with Standard Deviation by zdmre This script analyzes trends in financial markets using standard deviation.

The script works by first calculating the standard deviation of a security's price over a specified period of time. The script then uses this standard deviation to identify potential trend reversals.

For example, if the standard deviation of a security's price is high, this could indicate that the security is overvalued and due for a correction. Conversely, if the standard deviation of a security's price is low, this could indicate that the security is undervalued and due for a rally.

The script can be used to analyze any security, including stocks, bonds, and currencies. It can also be used to analyze different time frames, such as daily, weekly, and monthly.

How to Use the Script

To use the script, you will need to specify the following parameters:

Time frame: The time frame you want to analyze.

Standard deviation: The standard deviation you want to use.

Once you have specified these parameters, the script will calculate the standard deviation of the security's price over the specified time frame. The script will then use this standard deviation to identify potential trend reversals.

#DYOR

NormalDistributionFunctionsLibrary "NormalDistributionFunctions"

The NormalDistributionFunctions library encompasses a comprehensive suite of statistical tools for financial market analysis. It provides functions to calculate essential statistical measures such as mean, standard deviation, skewness, and kurtosis, alongside advanced functionalities for computing the probability density function (PDF), cumulative distribution function (CDF), Z-score, and confidence intervals. This library is designed to assist in the assessment of market volatility, distribution characteristics of asset returns, and risk management calculations, making it an invaluable resource for traders and financial analysts.

meanAndStdDev(source, length)

Calculates and returns the mean and standard deviation for a given data series over a specified period.

Parameters:

source (float) : float: The data series to analyze.

length (int) : int: The lookback period for the calculation.

Returns: Returns an array where the first element is the mean and the second element is the standard deviation of the data series for the given period.

skewness(source, mean, stdDev, length)

Calculates and returns skewness for a given data series over a specified period.

Parameters:

source (float) : float: The data series to analyze.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

length (int) : int: The lookback period for the calculation.

Returns: Returns skewness value

kurtosis(source, mean, stdDev, length)

Calculates and returns kurtosis for a given data series over a specified period.

Parameters:

source (float) : float: The data series to analyze.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

length (int) : int: The lookback period for the calculation.

Returns: Returns kurtosis value

pdf(x, mean, stdDev)

pdf: Calculates the probability density function for a given value within a normal distribution.

Parameters:

x (float) : float: The value to evaluate the PDF at.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

Returns: Returns the probability density function value for x.

cdf(x, mean, stdDev)

cdf: Calculates the cumulative distribution function for a given value within a normal distribution.

Parameters:

x (float) : float: The value to evaluate the CDF at.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

Returns: Returns the cumulative distribution function value for x.

confidenceInterval(mean, stdDev, size, confidenceLevel)

Calculates the confidence interval for a data series mean.

Parameters:

mean (float) : float: The mean of the data series.

stdDev (float) : float: The standard deviation of the data series.

size (int) : int: The sample size.

confidenceLevel (float) : float: The confidence level (e.g., 0.95 for 95% confidence).

Returns: Returns the lower and upper bounds of the confidence interval.

Market Activity Risk"Market Activity Risk" (MAR) - Is a dynamic tool designed to structurize the competitive landscape of blockchain transaction blocks, offering traders a strategic edge in anticipating market movements.

By capturing where market participants are actively buying and selling, the MAR indicator provides insights into areas of high competition, allowing traders to make informed decisions and potentially front-run transactions.

At the heart of this tool are blockchain transaction fees , they can represent daily shifts in transaction fee pressures.

By measuring momentum in fees, we can analyze the urgency and competition among traders to have their transactions processed first. This indicator is particularly good at revealing potential support or resistance zones, areas where traders are likely to defend their positions or increase their stakes, thus serving as critical junctures for strategic decision-making.

Key Features:

Adaptable Standard Deviation Settings: Users have the flexibility to adjust the length of the standard deviation and its multipliers, managing the risk bands to their individual risk tolerance.

Color-Coded Risk Levels: The MAR indicator employs an intuitive color scheme, making it easy to interpret the data at a glance.

Multi-Currency Compatibility: While designed with Bitcoin in mind, the MAR indicator is versatile, functioning effectively across various cryptocurrencies including Ethereum, XRP, and several other major altcoins. This broad compatibility ensures that traders across different market segments can leverage the insights provided by this tool.

Customizable Moving Average: The 730-day moving average setting is thoughtfully chosen to reflect the nuances of a typical cryptocurrency cycle, capturing long-term trends and fluctuations. However, recognizing the diverse needs and perspectives of traders, the indicator allows for the moving average period to be modified.

Z-score changeAs a wise man once said that:

1. beginners think in $ change

2. intermediates think in % change

3. pros think in Z change

Here is the "Z-score change" indicator that calculates up/down moves normalized by standard deviation (volatility) displayed as bar chart with 1,2 and 3 stdev levels.

Triple Confirmation Kernel Regression Overlay [QuantraSystems]Kernel Regression Oscillator - Overlay

Introduction

The Kernel Regression Oscillator (ᏦᏒᎧ) represents an advanced tool for traders looking to capitalize on market trends.

This Indicator is valuable in identifying and confirming trend directions, as well as probabilistic and dynamic oversold and overbought zones.

It achieves this through a unique composite approach using three distinct Kernel Regressions combined in an Oscillator.

The additional Chart Overlay Indicator adds confidence to the signal.

Which is this Indicator.

This methodology helps the trader to significantly reduce false signals and offers a more reliable indication of market movements than more widely used indicators can.

Legend

The upper section is the Overlay. It features the Signal Wave to display the current trend.

Its Overbought and Oversold zones start at 50% and end at 100% of the selected Standard Deviation (default σ = 3), which can indicate extremely rare situations which can lead to either a softening momentum in the trend or even a mean reversion situation.

The lower one is the Base Chart.

The Indicator is linked here

It features the Kernel Regression Oscillator to display a composite of three distinct regressions, also displaying current trend.

Its Overbought and Oversold zones start at 50% and end at 100% of the selected Standard Deviation (default σ = 2), which can indicate extremely rare situations.

Case Study

To effectively utilize the ᏦᏒᎧ, traders should use both the additional Overlay and the Base

Chart at the same time. Then focus on capturing the confluence in signals, for example:

If the 𝓢𝓲𝓰𝓷𝓪𝓵 𝓦𝓪𝓿𝓮 on the Overlay and the ᏦᏒᎧ on the Base Chart both reside near the extreme of an Oversold zone the probability is higher than normal that momentum in trend may soften or the token may even experience a reversion soon.

If a bar is characterized by an Oversold Shading in both the Overlay and the Base Chart, then the probability is very high to experience a reversion soon.

In this case the trader may want to look for appropriate entries into a long position, as displayed here.

If a bar is characterized by an Overbought Shading in either Overlay or Base Chart, then the probability is high for momentum weakening or a mean reversion.

In this case the trade may have taken profit and closed his long position, as displayed here.

Please note that we always advise to find more confluence by additional indicators.

Recommended Settings

Swing Trading (1D chart)

Overlay

Bandwith: 45

Width: 2

SD Lookback: 150

SD Multiplier: 2

Base Chart

Bandwith: 45

SD Lookback: 150

SD Multiplier: 2

Fast-paced, Scalping (4min chart)

Overlay

Bandwith: 75

Width: 2

SD Lookback: 150

SD Multiplier: 3

Base Chart

Bandwith: 45

SD Lookback: 150

SD Multiplier: 2

Notes

The Kernel Regression Oscillator on the Base Chart is also sensitive to divergences if that is something you are keen on using.

For maximum confluence, it is recommended to use the indicator both as a chart overlay and in its Base Chart.

Please pay attention to shaded areas with Standard Deviation settings of 2 or 3 at their outer borders, and consider action only with high confidence when both parts of the indicator align on the same signal.

This tool shows its best performance on timeframes lower than 4 hours.

Traders are encouraged to test and determine the most suitable settings for their specific trading strategies and timeframes.

The trend following functionality is indicated through the "𝓢𝓲𝓰𝓷𝓪𝓵 𝓦𝓪𝓿𝓮" Line, with optional "Up" and "Down" arrows to denote trend directions only (toggle “Show Trend Signals”).

Methodology

The Kernel Regression Oscillator takes three distinct kernel regression functions,

used at similar weight, in order to calculate a balanced and smooth composite of the regressions. Part of it are:

The Epanechnikov Kernel Regression: Known for its efficiency in smoothing data by assigning less weight to data points further away from the target point than closer data points, effectively reducing variance.

The Wave Kernel Regression: Similarly assigning weight to the data points based on distance, it captures repetitive and thus wave-like patterns within the data to smoothen out and reduce the effect of underlying cyclical trends.

The Logistic Kernel Regression: This uses the logistic function in order to assign weights by probability distribution on the distance between data points and target points. It thus avoids both bias and variance to a certain level.

kernel(source, bandwidth, kernel_type) =>

switch kernel_type

"Epanechnikov" => math.abs(source) <= 1 ? 0.75 * (1 - math.pow(source, 2)) : 0.0

"Logistic" => 1/math.exp(source + 2 + math.exp(-source))

"Wave" => math.abs(source) <= 1 ? (1 - math.abs(source)) * math.cos(math.pi * source) : 0.

kernelRegression(src, bandwidth, kernel_type) =>

sumWeightedY = 0.

sumKernels = 0.

for i = 0 to bandwidth - 1

base = i*i/math.pow(bandwidth, 2)

kernel = kernel(base, 1, kernel_type)

sumWeightedY += kernel * src

sumKernels += kernel

(src - sumWeightedY/sumKernels)/src

// Triple Confirmations

Ep = kernelRegression(source, bandwidth, 'Epanechnikov' )

Lo = kernelRegression(source, bandwidth, 'Logistic' )

Wa = kernelRegression(source, bandwidth, 'Wave' )

By combining these regressions in an unbiased average, we follow our principle of achieving confluence for a signal or a decision, by stacking several edges to increase the probability that we are correct.

// Average

AV = math.avg(Ep, Lo, Wa)

The Standard Deviation bands take defined parameters from the user, in this case sigma of ideally between 2 to 3,

to help the indicator detect extremely improbable conditions and thus take an inversely probable signal from it to forward to the user.

The parameter settings and also the visualizations allow for ample customizations by the trader. The indicator comes with default and recommended settings.

For questions or recommendations, please feel free to seek contact in the comments.

Volatility ZigZagIt calculates and plots zigzag lines based on volatility and price movements. It has various inputs for customization, allowing you to adjust parameters like source data, length, deviation, line styling, and labeling options.

The indicator identifies pivot points in the price movement, drawing lines between these pivots based on the deviation from certain price levels or volatility measures.

The script labels various data points at the ZigZag pivot points on the chart. These labels provide information about different aspects of the price movement and volume around these pivot points. Here's a breakdown of what gets labeled:

Price Change: Indicates the absolute and average percentage change between the two pivot points. It displays the absolute or relative change in price as a percentage. Additionally, the average absolute price increase or the average rate of increase can also be labeled.

Volume: Shows the total volume and average volume between the two pivot points.

Number of Bars: Indicates the number of bars between the current and the last pivot point.

Reversal Price: Displays the price of the reversal point (the previous pivot).

Z-ScoreThe "Z-Score" indicator is a unique and powerful tool designed to help traders identify overbought and oversold conditions in the market. Below is an explanation of its features, usefulness, and what makes it special:

Features:

Z-Score Calculation: The indicator calculates the Z-Score, a statistical measure that represents how far the current price is from the moving average (MA) in terms of standard deviations. It helps identify extreme price movements.

Customizable Parameters: Traders can adjust key parameters such as the Z-Score threshold, the type of MA (e.g., SMA, EMA), and the length of the moving average to suit their trading preferences.

Signal Options: The indicator offers flexibility in terms of signaling. Traders can choose whether to trigger signals when the Z-Score crosses the specified threshold or when it moves away from the threshold.

Visual Signals : Z-Score conditions are represented visually on the chart with color-coded background highlights. Overbought conditions are marked with a red background, while oversold conditions are indicated with a green background.

Information Table: A dynamic information table displays essential details, including the MA type, MA length, MA value, standard deviation, current price, and Z-Score. This information table helps traders make informed decisions.

Usefulness:

Overbought and Oversold Signals: Z-Score is particularly valuable for identifying overbought and oversold market conditions. Traders can use this information to potentially enter or exit positions.

Statistical Analysis: The Z-Score provides a statistical measure of price deviation, offering a data-driven approach to market analysis.

Customization: Traders can customize the indicator to match their trading strategies and preferences, enhancing its adaptability to different trading styles.

Visual Clarity: The visual signals make it easy for traders to quickly spot potential trade opportunities on the price chart.

In summary, the Z-Score indicator is a valuable tool for traders looking to incorporate statistical analysis into their trading strategies. Its customizability, visual signals, and unique statistical approach make it an exceptional choice for identifying overbought and oversold market conditions and potential trading opportunities.

Z-Score - AsymmetrikZ-Score-Asymmetrik User Manual

Introduction

The Z-Score Indicator is a powerful tool used in technical analysis to measure how far a data point is from the mean value of a dataset, measured in terms of standard deviations. This indicator helps traders identify potential overbought or oversold conditions in the market.

This user manual provides a comprehensive guide on how to use the Z-Score Indicator in TradingView.

0. Quickstart

- Set the thresholds based on your asset (number of standard deviations that you consider being extreme for this asset / timeframe).

- Red background indicates a possible overbought situation, green background an oversold one.

- The color and direction of the Z-Score Line acts as a confirmation of the trend reversal.

1. Indicator Overview

The Z-Score Indicator, also known as the Z-Score Oscillator, is designed to display the Z-Score of a selected financial instrument on your TradingView chart. The Z-Score measures how many standard deviations an asset's price is from its mean (average) price over a specified period.

The indicator consists of the following components:

- Z-Score Line: This line represents the Z-Score value and is displayed on the indicator panel.

- Background Color: The background color of the indicator panel changes based on user-defined thresholds.

2. Inputs

The indicator provides several customizable inputs to tailor it to your specific trading preferences:

- Number of Periods: This input allows you to define the number of periods over which the Z-Score will be calculated. A longer period will provide a smoother Z-Score line but may be less responsive to recent price changes.

- Z-Score Low Threshold: Sets the lower threshold value for the Z-Score. When the Z-Score crosses below this threshold, the background color of the indicator panel changes accordingly.

- Z-Score High Threshold: Sets the upper threshold value for the Z-Score. When the Z-Score crosses above this threshold, the background color of the indicator panel changes accordingly.

3. How to Use the Indicator

Here are the steps to use the Z-Score Indicator:

- Adjust Parameters: Modify the indicator's inputs as needed. You can change the number of periods for the Z-Score calculation and set your desired low and high thresholds.

- Interpret the Indicator: Observe the Z-Score line on the indicator panel. It fluctuates above and below zero. Pay attention to the background color changes when the Z-Score crosses your specified thresholds.

4. Interpreting the Indicator

- Z-Score Line: The Z-Score line represents the current Z-Score value. When it is above zero, it suggests that the asset's price is above the mean, indicating potential overvaluation. When below zero, it suggests undervaluation.

- Background Color: The background color of the indicator panel changes based on the Z-Score's position relative to the specified thresholds. Green indicates the Z-Score is below the low threshold (potential undervaluation), while red indicates it is above the high threshold (potential overvaluation).

- Z-Score Line Color: The color of the Z-Score line shows that the Z-Score is trending up compared to its moving average. This can be used as a validation of the background color.

5. Customization Options

You can customize the Z-Score Indicator in the following ways:

- Adjust Inputs: Modify the number of periods and the Z-Score thresholds.

- Change Line and Background Colors: You can customize the colors of the Z-Score line and background by editing the indicator's script.

6. Troubleshooting

If you encounter any issues while using the Z-Score Indicator, make sure to check the following:

- Ensure that the indicator is applied correctly to your chart.

- Verify that the indicator's inputs match your intended settings.

- Contact me for more support if needed

7. Conclusion

The Z-Score Indicator is a valuable tool for traders and investors to identify potential overbought and oversold conditions in the market. By understanding how the Z-Score works and customizing it to your preferences, you can integrate it into your trading strategy to make informed decisions.

Remember that trading involves risk, and it's essential to combine technical indicators like the Z-Score with other analysis methods and risk management strategies for successful trading.

Momentum ChannelbandsThe "Momentum Channelbands" is indicator that measures and displays an asset's momentum. It includes options to calculate Bollinger Bands and Donchian Channels around the momentum. Users can customize settings for a comprehensive view of momentum-related insights. This tool helps assess trend strength, identify overbought/oversold conditions, and pinpoint highs/lows. It should be used alongside other indicators due to potential lag and false signals.

dharmatech : Standard Deviation ChannelDESCRIPTION

Based on version by leojez.

Adds a 3rd standard deviation level.

Twice as fast as original version.

Refactored and simplified source code.

HOW TO USE

Load your chart

Adjust the timeframe and zoom of the chart so that the trend you're interested in is in view.

Add the indicator

Use the measuring tool to measure the number of bars from the start of the trend to the latest candle.

Open settings for the indicator.

Set the length value to the number of bars that you noted.

Advanced Weighted Residual Arbitrage AnalyzerThe Advanced Weighted Residual Arbitrage Analyzer is a sophisticated tool designed for traders aiming to exploit price deviations between various asset pairs. By examining the differences in normalized price relations and their weighted residuals, this indicator provides insights into potential arbitrage opportunities in the market.

Key Features:

Multiple Relation Analysis: Analyze up to five different asset relations simultaneously, offering a comprehensive view of potential arbitrage setups.

Normalization Functions: Choose from a variety of normalization techniques like SMA, EMA, WMA, and HMA to ensure accurate comparisons between different price series.

Dynamic Weighting: Residuals are weighted based on their correlation, ensuring that stronger correlations have a more pronounced impact on the analysis. Weighting can be adjusted using several functions including square, sigmoid, and logistic.

Regression Flexibility: Incorporate linear, polynomial, or robust regression to calculate residuals, tailoring the analysis to different market conditions.

Customizable Display: Decide which plots to display for clarity and focus, including normalized relations, weighted residuals, and the difference between the screen relation and the average weighted residual.

Usage Guidelines:

Configure the asset pairs you wish to analyze using the Symbol Relations group in the settings.

Adjust the normalization, volatility, regression, and weighting functions based on your preference and the specific characteristics of the asset pairs.

Monitor the weighted residuals for deviations from the mean. Larger deviations suggest stronger arbitrage opportunities.

Use the difference plot (between the screen relation and average weighted residual) as a quick visual cue for potential trade setups. When this plot deviates significantly from zero, it indicates a possible arbitrage opportunity.

Regularly update and adjust the parameters to account for changing market conditions and ensure the most accurate analysis.

In the Advanced Weighted Residual Arbitrage Analyzer , the value set in Alert Threshold plays a crucial role in delineating a normalized band. This band serves as a guide to identify significant deviations and potential trading opportunities.

When we observe the plots of the green line and the purple line, the Alert Threshold provides a boundary for these plots. The following points explain the significance:

Breach of the Band: When either the green or purple line crosses above or below the Alert Threshold , it indicates a significant deviation from the mean. This breach can be interpreted as a potential trading signal, suggesting a possible arbitrage opportunity.

Convergence to the Mean: If the green line converges with the purple line , it denotes that the price relation has reverted to its mean. This convergence typically suggests that the arbitrage opportunity has been exhausted, and the market dynamics are returning to equilibrium.

Trade Execution: A trader can consider entering a trade when the lines breach the Alert Threshold . The return of the green line to align closely with the purple line can be seen as a signal to exit the trade, capitalizing on the reversion to the mean.

By monitoring these plots in conjunction with the Alert Threshold , traders can gain insights into market imbalances and exploit potential arbitrage opportunities. The convergence and divergence of these lines, relative to the normalized band, serve as valuable visual cues for trade initiation and termination.

When you're analyzing relations between two symbols (for instance, BINANCE:SANDUSDT/BINANCE:NEARUSDT ), you're essentially looking at the price relationship between the two underlying assets. This relationship provides insights into potential imbalances between the assets, which arbitrage traders can exploit.

Breach of the Lower Band: If the purple line touches or crosses below the lower Alert Threshold , it indicates that the first symbol (in our example, SANDUSDT ) is undervalued relative to the second symbol ( NEARUSDT ). In practical terms:

Action: You would consider buying the first symbol ( SANDUSDT ) and selling the second symbol ( NEARUSDT ).

Rationale: The expectation is that the price of the first symbol will rise, or the price of the second symbol will fall, or both, thereby converging back to their historical mean relationship.

Breach of the Upper Band: Conversely, if the difference plot touches or crosses above the upper Alert Threshold , it suggests that the first symbol is overvalued compared to the second. This implies:

Action: You'd consider selling the first symbol ( SANDUSDT ) and buying the second symbol ( NEARUSDT ).

Rationale: The anticipation here is that the price of the first symbol will decrease, or the price of the second will increase, or both, bringing the relationship back to its historical average.

Convergence to the Mean: As mentioned earlier, when the green line aligns closely with the purple line, it's an indication that the assets have returned to their typical price relationship. This serves as a signal for traders to consider closing out their positions, locking in the gains from the arbitrage opportunity.

It's important to note that when you're trading based on symbol relations, you're essentially betting on the relative performance of the two assets. This strategy, often referred to as "pairs trading," seeks to capitalize on price imbalances between related financial instruments. By taking opposing positions in the two symbols, traders aim to profit from the eventual reversion of the price difference to the mean.

VolatilityIndicatorsLibrary "VolatilityIndicators"

This is a library of Volatility Indicators .

It aims to facilitate the grouping of this category of indicators, and also offer the customized supply of

the parameters and sources, not being restricted to just the closing price.

@Thanks and credits:

1. Dynamic Zones: Leo Zamansky, Ph.D., and David Stendahl

2. Deviation: Karl Pearson (code by TradingView)

3. Variance: Ronald Fisher (code by TradingView)

4. Z-score: Veronique Valcu (code by HPotter)

5. Standard deviation: Ronald Fisher (code by TradingView)

6. ATR (Average True Range): J. Welles Wilder (code by TradingView)

7. ATRP (Average True Range Percent): millerrh

8. Historical Volatility: HPotter

9. Min-Max Scale Normalization: gorx1

10. Mean Normalization: gorx1

11. Standardization: gorx1

12. Scaling to unit length: gorx1

13. LS Volatility Index: Alexandre Wolwacz (Stormer), Fabrício Lorenz, Fábio Figueiredo (Vlad) (code by me)

14. Bollinger Bands: John Bollinger (code by TradingView)

15. Bollinger Bands %: John Bollinger (code by TradingView)

16. Bollinger Bands Width: John Bollinger (code by TradingView)

dev(source, length, anotherSource)

Deviation. Measure the difference between a source in relation to another source

Parameters:

source (float)

length (simple int) : (int) Sequential period to calculate the deviation

anotherSource (float) : (float) Source to compare

Returns: (float) Bollinger Bands Width

variance(src, mean, length, biased, degreesOfFreedom)

Variance. A statistical measurement of the spread between numbers in a data set. More specifically,

variance measures how far each number in the set is from the mean (average), and thus from every other number in the set.

Variance is often depicted by this symbol: σ2. It is used by both analysts and traders to determine volatility and market security.

Parameters:

src (float) : (float) Source to calculate variance

mean (float) : (float) Mean (Moving average)

length (simple int) : (int) The sequential period to calcule the variance (number of values in data set)

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length. Only applies when biased parameter is defined as true.

Returns: (float) Standard deviation

stDev(src, length, mean, biased, degreesOfFreedom)

Measure the Standard deviation from a source in relation to it's moving average.

In this implementation, you pass the average as a parameter, allowing a more personalized calculation.

Parameters:

src (float) : (float) Source to calculate standard deviation

length (simple int) : (int) The sequential period to calcule the standard deviation

mean (float) : (float) Moving average.

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Standard deviation

zscore(src, mean, length, biased, degreesOfFreedom)

Z-Score. A z-score is a statistical measurement that indicates how many standard deviations a data point is from

the mean of a data set. It is also known as a standard score. The formula for calculating a z-score is (x - μ) / σ,

where x is the individual data point, μ is the mean of the data set, and σ is the standard deviation of the data set.

Z-scores are useful in identifying outliers or extreme values in a data set. A positive z-score indicates that the

data point is above the mean, while a negative z-score indicates that the data point is below the mean. A z-score of

0 indicates that the data point is equal to the mean.

Z-scores are often used in hypothesis testing and determining confidence intervals. They can also be used to compare

data sets with different units or scales, as the z-score standardizes the data. Overall, z-scores provide a way to

measure the relative position of a data point in a data

Parameters:

src (float) : (float) Source to calculate z-score

mean (float) : (float) Moving average.

length (simple int) : (int) The sequential period to calcule the standard deviation

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Z-score

atr(source, length)

ATR: Average True Range. Customized version with source parameter.

Parameters:

source (float) : (float) Source

length (simple int) : (int) Length (number of bars back)

Returns: (float) ATR

atrp(length, sourceP)

ATRP (Average True Range Percent)

Parameters:

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

atrp(source, length, sourceP)

ATRP (Average True Range Percent). Customized version with source parameter.

Parameters:

source (float) : (float) Source for ATR

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

historicalVolatility(lengthATR, lengthHist)

Historical Volatility

Parameters:

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

historicalVolatility(source, lengthATR, lengthHist)

Historical Volatility

Parameters:

source (float) : (float) Source for ATR

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

minMaxNormalization(src, numbars)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

minMaxNormalization(src, numbars, minimumLimit, maximumLimit)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

In this implementation, the user explicitly provides the desired minimum (min) and maximum (max) values for the scale,

rather than using the minimum and maximum values from the data.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

minimumLimit (simple float) : (float) Minimum value to scale

maximumLimit (simple float) : (float) Maximum value to scale

Returns: (float) Normalized value

meanNormalization(src, numbars, mean)

Mean Normalization

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

mean (float) : (float) Mean of source

Returns: (float) Normalized value

standardization(src, mean, stDev)

Standardization (Z-score Normalization). How "outside the mean" values relate to the standard deviation (ratio between first and second)

Parameters:

src (float) : (float) Source to normalize

mean (float) : (float) Mean of source

stDev (float) : (float) Standard Deviation

Returns: (float) Normalized value

scalingToUnitLength(src, numbars)

Scaling to unit length

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

lsVolatilityIndex(movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int) : (float) Length for normalization

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

lsVolatilityIndex(sourcePrice, movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

sourcePrice (float) : (float) Source for measure the distance

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int)

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

bollingerBands(src, length, mult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) A tuple of Bollinger Bands, where index 1=basis; 2=basis+dev; 3=basis-dev; and dev=multiplier*stdev

bollingerBands(src, length, aMult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Also, various multipliers can be passed, thus getting more bands (instead of just 2).

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) An array of multiplies used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands, where:

index 1=basis; 2=basis+dev1; 3=basis-dev1; 4=basis+dev2, 5=basis-dev2, 6=basis+dev2, 7=basis-dev2, Nup=basis+devN, Nlow=basis-devN

and dev1, dev2, devN are ```multiplier N * stdev```

bollingerBandsB(src, length, mult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation:

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands %B

bollingerBandsB(src, length, aMult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands %B. The number of results in this array is equal the numbers of multipliers passed via parameter.

bollingerBandsW(src, length, mult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation:

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands Width

bollingerBandsW(src, length, aMult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands Width. The number of results in this array is equal the numbers of multipliers passed via parameter.

dinamicZone(source, sampleLength, pcntAbove, pcntBelow)

Get Dynamic Zones

Parameters:

source (float) : (float) Source

sampleLength (simple int) : (int) Sample Length

pcntAbove (simple float) : (float) Calculates the top of the dynamic zone, considering that the maximum values are above x% of the sample

pcntBelow (simple float) : (float) Calculates the bottom of the dynamic zone, considering that the minimum values are below x% of the sample

Returns: A tuple with 3 series of values: (1) Upper Line of Dynamic Zone;

(2) Lower Line of Dynamic Zone; (3) Center of Dynamic Zone (x = 50%)

Examples: