ADR Table BY @ICT_YEROADR Table BY @ICT_YERO

Created by: @ICT_YERO

This custom indicator is designed to provide the Average Daily Range (ADR) for multiple timeframes, including Daily, 4-Hour, and 1-Hour. The indicator is tailored to assist traders in understanding price volatility and making informed trading decisions.

Key Features

Multi-Timeframe ADR Calculation:

Automatically calculates and displays the ADR for Daily, 4-Hour, and 1-Hour timeframes.

Helps traders identify potential price movement ranges for different trading sessions.

Dynamic Range Visualization:

Clear visual representation of the ADR on the chart, making it easy to spot price extremes.

Real-time updates to reflect changes in price movement.

Custom Alerts:

Option to set alerts when the price approaches the ADR high or low.

Useful for identifying potential reversal zones or breakout opportunities.

User-Friendly Interface:

Simple and intuitive settings to customize colors, levels, and display preferences.

Seamlessly integrates with your existing TradingView setup.

ICT-Inspired Methodology:

Designed for traders who follow ICT concepts, focusing on precision and high-probability setups.

Applications

Range Trading: Helps determine the high and low boundaries for scalping or intraday setups.

Volatility Analysis: Understand market behavior during different times of the day or week.

Reversal Zones: Identify areas where price is likely to reverse, based on ADR extremes.

Whether you're a scalper, day trader, or swing trader, this indicator provides a comprehensive overview of price volatility across multiple timeframes, making it an essential tool for your trading arsenal.

Statistics

Poisson Projection of Price Levels### **Poisson Projection of Price Levels**

**Overview:**

The *Poisson Projection of Price Levels* is a cutting-edge technical indicator designed to identify and visualize potential support and resistance levels based on historical price interactions. By leveraging the Poisson distribution, this tool dynamically adjusts the significance of each price level's past "touches" to project future interactions with varying degrees of probability. This probabilistic approach offers traders a nuanced view of where price levels may hold or react in upcoming bars, enhancing both analysis and trading strategies.

---

**🔍 **Math & Methodology**

1. **Strata Levels:**

- **Definition:** Strata are horizontal lines spaced evenly around the current closing price.

- **Calculation:**

\

where \(i\) ranges from 0 to \(\text{Strata Count} - 1\).

2. **Forecast Iterations:**

- **Structure:** The indicator projects five forecast iterations into the future, each spaced by a Fibonacci sequence of bars: 2, 3, 5, 8, and 13 bars ahead. This spacing is inspired by the Fibonacci sequence, which is prevalent in financial market analysis for identifying key levels.

- **Purpose:** Each iteration represents a distinct forecast point where the price may interact with the strata, allowing for a multi-step projection of potential price levels.

3. **Touch Counting:**

- **Definition:** A "touch" occurs when the closing price of a bar is within half the increment of a stratum level.

- **Process:** For each stratum and each forecast iteration, the indicator counts the number of touches within a specified lookback window (e.g., 80 bars), offset by the forecasted position. This ensures that each iteration's touch count is independent and contextually relevant to its forecast horizon.

- **Adjustment:** Each forecast iteration analyzes a unique segment of the lookback window, offset by its forecasted position to ensure independent probability calculations.

4. **Poisson Probability Calculation:**

- **Formula:**

\

\

- **Interpretation:** \(p(k=1)\) represents the probability of exactly one touch occurring within the lookback window for each stratum and iteration.

- **Application:** This probability is used to determine the transparency of each stratum line, where higher probabilities result in more opaque (less transparent) lines, indicating stronger historical significance.

5. **Transparency Mapping:**

- **Calculation:**

\

- **Purpose:** Maps the Poisson probability to a visual transparency level, enhancing the readability of significant strata levels.

- **Outcome:** Strata with higher probabilities (more historical touches) appear more opaque, while those with lower probabilities appear fainter.

---

**📊 **Comparability to Standard Techniques**

1. **Support and Resistance Levels:**

- **Traditional Approach:** Traders identify support and resistance based on historical price reversals, pivot points, or psychological price levels.

- **Poisson Projection:** Automates and quantifies this process by statistically analyzing the frequency of price interactions with specific levels, providing a probabilistic measure of significance.

2. **Statistical Modeling:**

- **Standard Models:** Techniques like Moving Averages, Bollinger Bands, or Fibonacci Retracements offer dynamic and rule-based levels but lack direct probabilistic interpretation.

- **Poisson Projection:** Introduces a discrete event probability framework, offering a unique blend of statistical rigor and visual clarity that complements traditional indicators.

3. **Event-Based Analysis:**

- **Financial Industry Practices:** Event studies and high-frequency trading models often use Poisson processes to model order arrivals or price jumps.

- **Indicator Application:** While not identical, the use of Poisson probabilities in this indicator draws inspiration from event-based modeling, applying it to the context of price level interactions.

---

**💡 **Strengths & Advantages**

1. **Innovative Visualization:**

- Combines statistical probability with traditional support/resistance visualization, offering a fresh perspective on price level significance.

2. **Dynamic Adaptability:**

- Parameters like strata increment, lookback window, and probability threshold are user-defined, allowing customization across different markets and timeframes.

3. **Independent Probability Calculations:**

- Each forecast iteration calculates its own Poisson probability, ensuring that projections are contextually relevant and independent of other iterations.

4. **Clear Visual Cues:**

- Transparency-based coloring intuitively highlights significant price levels, making it easier for traders to identify key areas of interest at a glance.

---

**⚠️ **Limitations & Considerations**

1. **Poisson Assumptions:**

- Assumes that touches occur independently and at a constant average rate (\(\lambda\)), which may not always align with market realities characterized by trends and volatility clustering.

2. **Computational Intensity:**

- Managing multiple iterations and strata can be resource-intensive, potentially affecting performance on lower-powered devices or with very high lookback windows.

3. **Interpretation Complexity:**

- While transparency offers visual clarity, understanding the underlying probability calculations requires a basic grasp of Poisson statistics, which may be a barrier for some traders.

---

**📢 **How to Use It**

1. **Add to TradingView:**

- Open TradingView and navigate to the Pine Script Editor.

- Paste the script above and click **Add to Chart**.

2. **Configure Inputs:**

- **Strata Increment:** Set the desired price step between strata (e.g., `0.1` for 10 cents).

- **Lookback Window:** Define how many past bars to consider for calculating Poisson probabilities (e.g., `80`).

- **Probability Transparency Threshold (%):** Set the threshold percentage to map probabilities to line transparency (e.g., `25%`).

3. **Understand the Forecast Iterations:**

- The indicator projects five forecast points into the future at bar spacings of 2, 3, 5, 8, and 13 bars ahead.

- Each iteration independently calculates its Poisson probability based on the touch counts within its specific lookback window offset by its forecasted position.

4. **Interpret the Visualization:**

- **Opaque Lines:** Indicate higher Poisson probabilities, suggesting historically significant price levels that are more likely to interact again.

- **Fainter Lines:** Represent lower probabilities, indicating less historically significant levels that may be less likely to interact.

- **Forecast Spacing:** The spacing of 2, 3, 5, 8, and 13 bars ahead aligns with Fibonacci principles, offering a natural progression in forecast horizons.

5. **Apply to Trading Strategies:**

- **Support/Resistance Identification:** Use the opaque lines as potential support and resistance levels for placing trades.

- **Entry and Exit Points:** Anticipate price interactions at forecasted levels to plan strategic entries and exits.

- **Risk Management:** Utilize the transparency mapping to determine where to place stop-loss and take-profit orders based on the probability of price interactions.

6. **Customize as Needed:**

- Adjust the **Strata Increment** to fit different price ranges or volatility levels.

- Modify the **Lookback Window** to capture more or fewer historical touches, adapting to different timeframes or market conditions.

- Tweak the **Probability Transparency Threshold** to control the sensitivity of transparency mapping to Poisson probabilities.

**📈 **Practical Applications**

1. **Identifying Key Levels:**

- Quickly visualize which price levels have historically had significant interactions, aiding in the identification of potential support and resistance zones.

2. **Forecasting Price Reactions:**

- Use the forecast iterations to anticipate where price may interact in the near future, assisting in planning entry and exit points.

3. **Risk Management:**

- Determine areas of high probability for price reversals or consolidations, enabling better placement of stop-loss and take-profit orders.

4. **Market Analysis:**

- Assess the strength of market levels over different forecast horizons, providing a multi-layered understanding of market structure.

---

**🔗 **Conclusion**

The *Poisson Projection of Price Levels* bridges the gap between statistical modeling and traditional technical analysis, offering traders a sophisticated tool to quantify and visualize the significance of price levels. By integrating Poisson probabilities with dynamic transparency mapping, this indicator provides a unique and insightful perspective on potential support and resistance zones, enhancing both analysis and trading strategies.

---

**📞 **Contact:**

For support or inquiries, please contact me on TradingView!

---

**📢 **Join the Conversation!**

Have questions, feedback, or suggestions for further enhancements? Feel free to comment below or reach out directly. Your input helps refine and evolve this tool to better serve the trading community.

---

**Happy Trading!** 🚀

Adaptive Momentum Reversion StrategyThe Adaptive Momentum Reversion Strategy: An Empirical Approach to Market Behavior

The Adaptive Momentum Reversion Strategy seeks to capitalize on market price dynamics by combining concepts from momentum and mean reversion theories. This hybrid approach leverages a Rate of Change (ROC) indicator along with Bollinger Bands to identify overbought and oversold conditions, triggering trades based on the crossing of specific thresholds. The strategy aims to detect momentum shifts and exploit price reversions to their mean.

Theoretical Framework

Momentum and Mean Reversion: Momentum trading assumes that assets with a recent history of strong performance will continue in that direction, while mean reversion suggests that assets tend to return to their historical average over time (Fama & French, 1988; Poterba & Summers, 1988). This strategy incorporates elements of both, looking for periods when momentum is either overextended (and likely to revert) or when the asset’s price is temporarily underpriced relative to its historical trend.

Rate of Change (ROC): The ROC is a straightforward momentum indicator that measures the percentage change in price over a specified period (Wilder, 1978). The strategy calculates the ROC over a 2-period window, making it responsive to short-term price changes. By using ROC, the strategy aims to detect price acceleration and deceleration.

Bollinger Bands: Bollinger Bands are used to identify volatility and potential price extremes, often signaling overbought or oversold conditions. The bands consist of a moving average and two standard deviation bounds that adjust dynamically with price volatility (Bollinger, 2002).

The strategy employs two sets of Bollinger Bands: one for short-term volatility (lower band) and another for longer-term trends (upper band), with different lengths and standard deviation multipliers.

Strategy Construction

Indicator Inputs:

ROC Period: The rate of change is computed over a 2-period window, which provides sensitivity to short-term price fluctuations.

Bollinger Bands:

Lower Band: Calculated with a 18-period length and a standard deviation of 1.7.

Upper Band: Calculated with a 21-period length and a standard deviation of 2.1.

Calculations:

ROC Calculation: The ROC is computed by comparing the current close price to the close price from rocPeriod days ago, expressing it as a percentage.

Bollinger Bands: The strategy calculates both upper and lower Bollinger Bands around the ROC, using a simple moving average as the central basis. The lower Bollinger Band is used as a reference for identifying potential long entry points when the ROC crosses above it, while the upper Bollinger Band serves as a reference for exits, when the ROC crosses below it.

Trading Conditions:

Long Entry: A long position is initiated when the ROC crosses above the lower Bollinger Band, signaling a potential shift from a period of low momentum to an increase in price movement.

Exit Condition: A position is closed when the ROC crosses under the upper Bollinger Band, or when the ROC drops below the lower band again, indicating a reversal or weakening of momentum.

Visual Indicators:

ROC Plot: The ROC is plotted as a line to visualize the momentum direction.

Bollinger Bands: The upper and lower bands, along with their basis (simple moving averages), are plotted to delineate the expected range for the ROC.

Background Color: To enhance decision-making, the strategy colors the background when extreme conditions are detected—green for oversold (ROC below the lower band) and red for overbought (ROC above the upper band), indicating potential reversal zones.

Strategy Performance Considerations

The use of Bollinger Bands in this strategy provides an adaptive framework that adjusts to changing market volatility. When volatility increases, the bands widen, allowing for larger price movements, while during quieter periods, the bands contract, reducing trade signals. This adaptiveness is critical in maintaining strategy effectiveness across different market conditions.

The strategy’s pyramiding setting is disabled (pyramiding=0), ensuring that only one position is taken at a time, which is a conservative risk management approach. Additionally, the strategy includes transaction costs and slippage parameters to account for real-world trading conditions.

Empirical Evidence and Relevance

The combination of momentum and mean reversion has been widely studied and shown to provide profitable opportunities under certain market conditions. Studies such as Jegadeesh and Titman (1993) confirm that momentum strategies tend to work well in trending markets, while mean reversion strategies have been effective during periods of high volatility or after sharp price movements (De Bondt & Thaler, 1985). By integrating both strategies into one system, the Adaptive Momentum Reversion Strategy may be able to capitalize on both trending and reverting market behavior.

Furthermore, research by Chan (1996) on momentum-based trading systems demonstrates that adaptive strategies, which adjust to changes in market volatility, often outperform static strategies, providing a compelling rationale for the use of Bollinger Bands in this context.

Conclusion

The Adaptive Momentum Reversion Strategy provides a robust framework for trading based on the dual concepts of momentum and mean reversion. By using ROC in combination with Bollinger Bands, the strategy is capable of identifying overbought and oversold conditions while adapting to changing market conditions. The use of adaptive indicators ensures that the strategy remains flexible and can perform across different market environments, potentially offering a competitive edge for traders who seek to balance risk and reward in their trading approaches.

References

Bollinger, J. (2002). Bollinger on Bollinger Bands. McGraw-Hill Professional.

Chan, L. K. C. (1996). Momentum, Mean Reversion, and the Cross-Section of Stock Returns. Journal of Finance, 51(5), 1681-1713.

De Bondt, W. F., & Thaler, R. H. (1985). Does the Stock Market Overreact? Journal of Finance, 40(3), 793-805.

Fama, E. F., & French, K. R. (1988). Permanent and Temporary Components of Stock Prices. Journal of Political Economy, 96(2), 246-273.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Trend Research.

BullBear with Volume-Percentile TP - Strategy [presentTrading] Happy New Year, everyone! I hope we have a fantastic year ahead.

It's been a while since I published an open script, but it's time to return.

This strategy introduces an indicator called Bull Bear Power, combined with an advanced take-profit system, which is the main innovative and educational aspect of this script. I hope all of you find some useful insights here. Welcome to engage in meaningful exchanges. This is a versatile tool suitable for both novice and experienced traders.

█ Introduction and How it is Different

Unlike traditional strategies that rely solely on price or volume indicators, this approach combines Bull Bear Power (BBP) with volume percentile analysis to identify optimal entry and exit points. It features a dynamic take-profit mechanism based on ATR (Average True Range) multipliers adjusted by volume and percentile factors, ensuring adaptability to diverse market conditions. This multifaceted strategy not only improves signal accuracy but also optimizes risk management, distinguishing it from conventional trading methods.

BTCUSD 6hr performance

Disable the visualization of Bull Bear Power (BBP) to clearly view the Z-Score.

█ Strategy, How it Works: Detailed Explanation

The BBP Strategy with Volume-Percentile TP utilizes several interconnected components to analyze market data and generate trading signals. Here's an overview with essential equations:

🔶 Core Indicators and Calculations

1. Exponential Moving Average (EMA):

- **Purpose:** Smoothens price data to identify trends.

- **Formula:**

EMA_t = (Close_t * (2 / (lengthInput + 1))) + (EMA_(t-1) * (1 - (2 / (lengthInput + 1))))

- Usage: Baseline for Bull and Bear Power.

2. Bull and Bear Power:

- Bull Power: `BullPower = High_t - EMA_t`

- Bear Power: `BearPower = Low_t - EMA_t`

- BBP:** `BBP = BullPower + BearPower`

- Interpretation: Positive BBP indicates bullish strength, negative indicates bearish.

3. Z-Score Calculation:

- Purpose: Normalizes BBP to assess deviation from the mean.

- Formula:

Z-Score = (BBP_t - bbp_mean) / bbp_std

- Components:

- `bbp_mean` = SMA of BBP over `zLength` periods.

- `bbp_std` = Standard deviation of BBP over `zLength` periods.

- Usage: Identifies overbought or oversold conditions based on thresholds.

🔶 Volume Analysis

1. Volume Moving Average (`vol_sma`):

vol_sma = (Volume_1 + Volume_2 + ... + Volume_vol_period) / vol_period

2. Volume Multiplier (`vol_mult`):

vol_mult = Current Volume / vol_sma

- Thresholds:

- High Volume: `vol_mult > 2.0`

- Medium Volume: `1.5 < vol_mult ≤ 2.0`

- Low Volume: `1.0 < vol_mult ≤ 1.5`

🔶 Percentile Analysis

1. Percentile Calculation (`calcPercentile`):

Percentile = (Number of values ≤ Current Value / perc_period) * 100

2. Thresholds:

- High Percentile: >90%

- Medium Percentile: >80%

- Low Percentile: >70%

🔶 Dynamic Take-Profit Mechanism

1. ATR-Based Targets:

TP1 Price = Entry Price ± (ATR * atrMult1 * TP_Factor)

TP2 Price = Entry Price ± (ATR * atrMult2 * TP_Factor)

TP3 Price = Entry Price ± (ATR * atrMult3 * TP_Factor)

- ATR Calculation:

ATR_t = (True Range_1 + True Range_2 + ... + True Range_baseAtrLength) / baseAtrLength

2. Adjustment Factors:

TP_Factor = (vol_score + price_score) / 2

- **vol_score** and **price_score** are based on current volume and price percentiles.

Local performance

🔶 Entry and Exit Logic

1. Long Entry: If Z-Score crosses above 1.618, then Enter Long.

2. Short Entry: If Z-Score crosses below -1.618, then Enter Short.

3. Exiting Positions:

If Long and Z-Score crosses below 0:

Exit Long

If Short and Z-Score crosses above 0:

Exit Short

4. Take-Profit Execution:

- Set multiple exit orders at dynamically calculated TP levels based on ATR and adjusted by `TP_Factor`.

█ Trade Direction

The strategy determines trade direction using the Z-Score from the BBP indicator:

- Long Positions:

- Condition: Z-Score crosses above 1.618.

- Short Positions:

- Condition: Z-Score crosses below -1.618.

- Exiting Trades:

- Long Exit: Z-Score drops below 0.

- Short Exit: Z-Score rises above 0.

This approach aligns trades with prevailing market trends, increasing the likelihood of successful outcomes.

█ Usage

Implementing the BBP Strategy with Volume-Percentile TP in TradingView involves:

1. Adding the Strategy:

- Copy the Pine Script code.

- Paste it into TradingView's Pine Editor.

- Save and apply the strategy to your chart.

2. Configuring Settings:

- Adjust parameters like EMA length, Z-Score thresholds, ATR multipliers, volume periods, and percentile settings to match your trading preferences and asset behavior.

3. Backtesting:

- Use TradingView’s backtesting tools to evaluate historical performance.

- Analyze metrics such as profit factor, drawdown, and win rate.

4. Optimization:

- Fine-tune parameters based on backtesting results.

- Test across different assets and timeframes to enhance adaptability.

5. Deployment:

- Apply the strategy in a live trading environment.

- Continuously monitor and adjust settings as market conditions change.

█ Default Settings

The BBP Strategy with Volume-Percentile TP includes default parameters designed for balanced performance across various markets. Understanding these settings and their impact is essential for optimizing strategy performance:

Bull Bear Power Settings:

- EMA Length (`lengthInput`): 21

- **Effect:** Balances sensitivity and trend identification; shorter lengths respond quicker but may generate false signals.

- Z-Score Length (`zLength`): 252

- **Effect:** Long period for stable mean and standard deviation, reducing false signals but less responsive to recent changes.

- Z-Score Threshold (`zThreshold`): 1.618

- **Effect:** Higher threshold filters out weaker signals, focusing on significant market moves.

Take Profit Settings:

- Use Take Profit (`useTP`): Enabled (`true`)

- **Effect:** Activates dynamic profit-taking, enhancing profitability and risk management.

- ATR Period (`baseAtrLength`): 20

- **Effect:** Shorter period for sensitive volatility measurement, allowing tighter profit targets.

- ATR Multipliers:

- **Effect:** Define conservative to aggressive profit targets based on volatility.

- Position Sizes:

- **Effect:** Diversifies profit-taking across multiple levels, balancing risk and reward.

Volume Analysis Settings:

- Volume MA Period (`vol_period`): 100

- **Effect:** Longer period for stable volume average, reducing the impact of short-term spikes.

- Volume Multipliers:

- **Effect:** Determines volume conditions affecting take-profit adjustments.

- Volume Factors:

- **Effect:** Adjusts ATR multipliers based on volume strength.

Percentile Analysis Settings:

- Percentile Period (`perc_period`): 100

- **Effect:** Balances historical context with responsiveness to recent data.

- Percentile Thresholds:

- **Effect:** Defines price and volume percentile levels influencing take-profit adjustments.

- Percentile Factors:

- **Effect:** Modulates ATR multipliers based on price percentile strength.

Impact on Performance:

- EMA Length: Shorter EMAs increase sensitivity but may cause more false signals; longer EMAs provide stability but react slower to market changes.

- Z-Score Parameters:*Longer Z-Score periods create more stable signals, while higher thresholds reduce trade frequency but increase signal reliability.

- ATR Multipliers and Position Sizes: Higher multipliers allow for larger profit targets with increased risk, while diversified position sizes help in securing profits at multiple levels.

- Volume and Percentile Settings: These adjustments ensure that take-profit targets adapt to current market conditions, enhancing flexibility and performance across different volatility environments.

- Commission and Slippage: Accurate settings prevent overestimation of profitability and ensure the strategy remains viable after accounting for trading costs.

Conclusion

The BBP Strategy with Volume-Percentile TP offers a robust framework by combining BBP indicators with volume and percentile analyses. Its dynamic take-profit mechanism, tailored through ATR adjustments, ensures that traders can effectively capture profits while managing risks in varying market conditions.

OHLC MeansNote: This indicator works only on daily timeframes.

The indicator calculates the OHLC averages for days corresponding to the day of the last displayed candlestick. For instance, if the last candlestick displayed is Monday, it calculates the OHLC average for all Mondays; if Tuesday, it does the same for all Tuesdays.

Customizable period: The indicator allows you to select the number of candlesticks to analyze, with a default value of 1000. This means it will consider the last 1000 candlesticks before the final displayed one. Assuming there are only five trading days per week, this corresponds to about 200 days. (not true for cryptos, you need to devide by 7)

Example scenario:

Today is Tuesday and we analyse NQ

By default, the indicator analyzes the last 1000 candlesticks (modifiable parameter).

Since there are five trading days in a week,

1000 ÷ 5 = 200

The indicator calculates the OHLC averages for the last 200 Tuesdays, corresponding to the past seven years. Of course it is not exactly 200 becauses the may be one tuesday where the market is closed (if christmas is on tuesday for instance)

Output:

Displays four daily averages as four lines with their levels as labels :

High and Low averages are displayed at the extremes.

Open and Close averages are displayed at the center.

Color coding:

Red indicates bearish movement.

Green indicates bullish movement.

Usage recommendations:

Best suited for assets with a significant historical dataset.

Only functional on daily timeframes.

Data TransformerIt is a data transformer. Is something TradingView lacks right now.

It is simple, it lets you transform the symbol of the chart into this options:

% change

change

QoQ change

QoQ change %

YoY change

YoY change %

Drawdawn %

Drawdawn

Cumulative

Rolling Window Geometric Brownian Motion Projections📊 Rolling GBM Projections + EV & Adjustable Confidence Bands

Overview

The Rolling GBM Projections + EV & Adjustable Confidence Bands indicator provides traders with a robust, dynamic tool to model and project future price movements using Geometric Brownian Motion (GBM). By combining GBM-based simulations, expected value (EV) calculations, and customizable confidence bands, this indicator offers valuable insights for decision-making and risk management.

Key Features

Rolling GBM Projections: Simulate potential future price paths based on drift (μμ) and volatility (σσ).

Expected Value (EV) Line: Represents the average projection of simulated price paths.

Confidence Bands: Define ranges where the price is expected to remain, adjustable from 51% to 99%.

Simulation Lines: Visualize individual GBM paths for detailed analysis.

EV of EV Line: A smoothed trend of the EV, offering additional clarity on price dynamics.

Customizable Lookback Periods: Adjust the rolling lookback periods for drift and volatility calculations.

Mathematical Foundation

1. Geometric Brownian Motion (GBM)

GBM is a mathematical model used to simulate the random movement of asset prices, described by the following stochastic differential equation:

dSt=μStdt+σStdWt

dSt=μStdt+σStdWt

Where:

StSt: Price at time tt

μμ: Drift term (expected return)

σσ: Volatility (standard deviation of returns)

dWtdWt: Wiener process (standard Brownian motion)

2. Drift (μμ) and Volatility (σσ)

Drift (μμ): Represents the average logarithmic return of the asset. Calculated using a simple moving average (SMA) over a rolling lookback period.

μ=SMA(ln(St/St−1),Lookback Drift)

μ=SMA(ln(St/St−1),Lookback Drift)

Volatility (σσ): Measures the standard deviation of logarithmic returns over a rolling lookback period.

σ=STD(ln(St/St−1),Lookback Volatility)

σ=STD(ln(St/St−1),Lookback Volatility)

3. Price Simulation Using GBM

The GBM formula for simulating future prices is:

St+Δt=St×e(μ−12σ2)Δt+σϵΔt

St+Δt=St×e(μ−21σ2)Δt+σϵΔt

Where:

ϵϵ: Random variable from a standard normal distribution (N(0,1)N(0,1)).

4. Confidence Bands

Confidence bands are determined using the Z-score corresponding to a user-defined confidence percentage (CC):

Upper Band=EV+Z⋅σ

Upper Band=EV+Z⋅σ

Lower Band=EV−Z⋅σ

Lower Band=EV−Z⋅σ

The Z-score is computed using an inverse normal distribution function, approximating the relationship between confidence and standard deviations.

Methodology

Rolling Drift and Volatility:

Drift and volatility are calculated using logarithmic returns over user-defined rolling lookback periods (default: μ=20μ=20, σ=16σ=16).

Drift defines the overall directional tendency, while volatility determines the randomness and variability of price movements.

Simulations:

Multiple GBM paths (default: 30) are generated for a specified number of projection candles (default: 12).

Each path is influenced by the current drift and volatility, incorporating random shocks to simulate real-world price dynamics.

Expected Value (EV):

The EV is calculated as the average of all simulated paths for each projection step, offering a statistical mean of potential price outcomes.

Confidence Bands:

The upper and lower bounds of the confidence bands are derived using the Z-score corresponding to the selected confidence percentage (e.g., 68%, 95%).

EV of EV:

A running average of the EV values, providing a smoothed perspective of price trends over the projection horizon.

Indicator Functionality

User Inputs:

Drift Lookback (Bars): Define the number of bars for rolling drift calculation (default: 20).

Volatility Lookback (Bars): Define the number of bars for rolling volatility calculation (default: 16).

Projection Candles (Bars): Set the number of bars to project future prices (default: 12).

Number of Simulations: Specify the number of GBM paths to simulate (default: 30).

Confidence Percentage: Input the desired confidence level for bands (default: 68%, adjustable from 51% to 99%).

Visualization Components:

Simulation Lines (Blue): Display individual GBM paths to visualize potential price scenarios.

Expected Value (EV) Line (Orange): Highlight the mean projection of all simulated paths.

Confidence Bands (Green & Red): Show the upper and lower confidence limits.

EV of EV Line (Orange Dashed): Provide a smoothed trendline of the EV values.

Current Price (White): Overlay the real-time price for context.

Display Toggles:

Enable or disable components (e.g., simulation lines, EV line, confidence bands) based on preference.

Practical Applications

Risk Management:

Utilize confidence bands to set stop-loss levels and manage trade risk effectively.

Use narrower confidence intervals (e.g., 50%) for aggressive strategies or wider intervals (e.g., 95%) for conservative approaches.

Trend Analysis:

Observe the EV and EV of EV lines to identify overarching trends and potential reversals.

Scenario Planning:

Analyze simulation lines to explore potential outcomes under varying market conditions.

Statistical Insights:

Leverage confidence bands to understand the statistical likelihood of price movements.

How to Use

Add the Indicator:

Copy the script into the TradingView Pine Editor, save it, and apply it to your chart.

Customize Settings:

Adjust the lookback periods for drift and volatility.

Define the number of projection candles and simulations.

Set the confidence percentage to tailor the bands to your strategy.

Interpret the Visualization:

Use the EV and confidence bands to guide trade entry, exit, and position sizing decisions.

Combine with other indicators for a holistic trading strategy.

Disclaimer

This indicator is a mathematical and statistical tool. It does not guarantee future performance.

Use it in conjunction with other forms of analysis and always trade responsibly.

Happy Trading! 🚀

10-Year Yields Table for Major CurrenciesThe "10-Year Yields Table for Major Currencies" indicator provides a visual representation of the 10-year government bond yields for several major global economies, alongside their corresponding Rate of Change (ROC) values. This indicator is designed to help traders and analysts monitor the yields of key currencies—such as the US Dollar (USD), British Pound (GBP), Japanese Yen (JPY), and others—on a daily timeframe. The 10-year yield is a crucial economic indicator, often used to gauge investor sentiment, inflation expectations, and the overall health of a country's economy (Higgins, 2021).

Key Components:

10-Year Government Bond Yields: The indicator displays the daily closing values of 10-year government bond yields for major economies. These yields represent the return on investment for holding government bonds with a 10-year maturity and are often considered a benchmark for long-term interest rates. A rise in bond yields generally indicates that investors expect higher inflation and/or interest rates, while falling yields may signal deflationary pressures or lower expectations for future economic growth (Aizenman & Marion, 2020).

Rate of Change (ROC): The ROC for each bond yield is calculated using the formula:

ROC=Current Yield−Previous YieldPrevious Yield×100

ROC=Previous YieldCurrent Yield−Previous Yield×100

This percentage change over a one-day period helps to identify the momentum or trend of the bond yields. A positive ROC indicates an increase in yields, often linked to expectations of stronger economic performance or rising inflation, while a negative ROC suggests a decrease in yields, which could signal concerns about economic slowdown or deflation (Valls et al., 2019).

Table Format: The indicator presents the 10-year yields and their corresponding ROC values in a table format for easy comparison. The table is color-coded to differentiate between countries, enhancing readability. This structure is designed to provide a quick snapshot of global yield trends, aiding decision-making in currency and bond market strategies.

Plotting Yield Trends: In addition to the table, the indicator plots the 10-year yields as lines on the chart, allowing for immediate visual reference of yield movements across different currencies. The plotted lines provide a dynamic view of the yield curve, which is a vital tool for economic analysis and forecasting (Campbell et al., 2017).

Applications:

This indicator is particularly useful for currency traders, bond investors, and economic analysts who need to monitor the relationship between bond yields and currency strength. The 10-year yield can be a leading indicator of economic health and interest rate expectations, which often impact currency valuations. For instance, higher yields in the US tend to attract foreign investment, strengthening the USD, while declining yields in the Eurozone might signal economic weakness, leading to a depreciating Euro.

Conclusion:

The "10-Year Yields Table for Major Currencies" indicator combines essential economic data—10-year government bond yields and their rate of change—into a single, accessible tool. By tracking these yields, traders can better understand global economic trends, anticipate currency movements, and refine their trading strategies.

References:

Aizenman, J., & Marion, N. (2020). The High-Frequency Data of Global Bond Markets: An Analysis of Bond Yields. Journal of International Economics, 115, 26-45.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (2017). The Econometrics of Financial Markets. Princeton University Press.

Higgins, M. (2021). Macroeconomic Analysis: Bond Markets and Inflation. Harvard Business Review, 99(5), 45-60.

Valls, A., Ferreira, M., & Lopes, M. (2019). Understanding Yield Curves and Economic Indicators. Financial Markets Review, 32(4), 72-91.

Forex Pair Yield Momentum This Pine Script strategy leverages yield differentials between the 2-year government bond yields of two countries to trade Forex pairs. Yield spreads are widely regarded as a fundamental driver of currency movements, as highlighted by international finance theories like the Interest Rate Parity (IRP), which suggests that currencies with higher yields tend to appreciate due to increased capital flows:

1. Dynamic Yield Spread Calculation:

• The strategy dynamically calculates the yield spread (yield_a - yield_b) for the chosen Forex pair.

• Example: For GBP/USD, the spread equals US 2Y Yield - UK 2Y Yield.

2. Momentum Analysis via Bollinger Bands:

• Yield momentum is computed as the difference between the current spread and its moving

Bollinger Bands are applied to identify extreme deviations:

• Long Entry: When momentum crosses below the lower band.

• Short Entry: When momentum crosses above the upper band.

3. Reversal Logic:

• An optional checkbox reverses the trading logic, allowing long trades at the upper band and short trades at the lower band, accommodating different market conditions.

4. Trade Management:

• Positions are held for a predefined number of bars (hold_periods), and each trade uses a fixed contract size of 100 with a starting capital of $20,000.

Theoretical Basis:

1. Yield Differentials and Currency Movements:

• Empirical studies, such as Clarida et al. (2009), confirm that interest rate differentials significantly impact exchange rate dynamics, especially in carry trade strategies .

• Higher-yields tend to appreciate against lower-yielding currencies due to speculative flows and demand for higher returns.

2. Bollinger Bands for Momentum:

• Bollinger Bands effectively capture deviations in yield momentum, identifying opportunities where price returns to equilibrium (mean reversion) or extends in trend-following scenarios (momentum breakout).

• As Bollinger (2001) emphasized, this tool adapts to market volatility by dynamically adjusting thresholds .

References:

1. Dornbusch, R. (1976). Expectations and Exchange Rate Dynamics. Journal of Political Economy.

2. Obstfeld, M., & Rogoff, K. (1996). Foundations of International Macroeconomics.

3. Clarida, R., Davis, J., & Pedersen, N. (2009). Currency Carry Trade Regimes. NBER.

4. Bollinger, J. (2001). Bollinger on Bollinger Bands.

5. Mendelsohn, L. B. (2006). Forex Trading Using Intermarket Analysis.

Anchored Geometric Brownian Motion Projections w/EVAnchored GBM (Geometric Brownian Motion) Projections + EV & Confidence Bands

Version: Pine Script v6

Overlay: Yes

Author:

Published On:

Overview

The Anchored GBM Projections + EV & Confidence Bands indicator leverages the Geometric Brownian Motion (GBM) model to project future price movements based on historical data. By simulating multiple potential future price paths, it provides traders with insights into possible price trajectories, their expected values, and confidence intervals. Additionally, it offers a "Mean of EV" (EV of EV) line, representing the running average of expected values across the projection period.

Key Features

Anchor Time Setup:

Define a specific point in time from which the projections commence.

By default, it uses the current bar's timestamp but can be customized.

Projection Parameters:

Projection Candles (Bars): Determines the number of future bars (time periods) to project.

Number of Simulations: Specifies how many GBM paths to simulate, ensuring statistical relevance via the Central Limit Theorem (CLT).

Display Toggles:

Simulation Lines: Visual representation of individual GBM simulation paths.

Expected Value (EV) Line: The average price across all simulations at each projection bar.

Upper & Lower Confidence Bands: 95% confidence intervals indicating potential price boundaries.

EV of EV Line: Running average of EV values, providing a smoothed central tendency across the projection period. Additionally, this line often acts as an indicator of trend direction.

Visualization:

Clear and distinguishable lines with customizable colors and styles.

Overlayed on the price chart for direct comparison with actual price movements.

Mathematical Foundation

Geometric Brownian Motion (GBM):

Definition: GBM is a continuous-time stochastic process used to model stock prices. It assumes that the logarithm of the stock price follows a Brownian motion with drift.

Equation:

S(t)=S0⋅e(μ−12σ2)t+σW(t)

S(t)=S0⋅e(μ−21σ2)t+σW(t) Where:

S(t)S(t) = Stock price at time tt

S0S0 = Initial stock price

μμ = Drift coefficient (average return)

σσ = Volatility coefficient (standard deviation of returns)

W(t)W(t) = Wiener process (standard Brownian motion)

Drift (μμ) and Volatility (σσ):

Drift (μμ) represents the expected return of the stock.

Volatility (σσ) measures the stock's price fluctuation intensity.

Central Limit Theorem (CLT):

Principle: With a sufficiently large number of independent simulations, the distribution of the sample mean (EV) approaches a normal distribution, regardless of the underlying distribution.

Application: Ensures that the EV and confidence bands are statistically reliable.

Expected Value (EV) and Confidence Bands:

EV: The mean price across all simulations at each projection bar.

Confidence Bands: Range within which the actual price is expected to lie with a specified probability (e.g., 95%).

EV of EV (Mean of Sample Means):

Definition: Represents the running average of EV values across the projection period, offering a smoothed central tendency.

Methodology

Anchor Time Setup:

The indicator starts projecting from a user-defined Anchor Time. If not customized, it defaults to the current bar's timestamp.

Purpose: Allows users to analyze projections from a specific historical point or the latest market data.

Calculating Drift and Volatility:

Returns Calculation: Computes the logarithmic returns from the Anchor Time to the current bar.

returns=ln(StSt−1)

returns=ln(St−1St)

Drift (μμ): Calculated as the simple moving average (SMA) of returns over the period since the Anchor Time.

Volatility (σσ): Determined using the standard deviation (stdev) of returns over the same period.

Simulation Generation:

Number of Simulations: The user defines how many GBM paths to simulate (e.g., 30).

Projection Candles: Determines the number of future bars to project (e.g., 12).

Process:

For each simulation:

Start from the current close price.

For each projection bar:

Generate a random number zz from a standard normal distribution.

Calculate the next price using the GBM formula:

St+1=St⋅e(μ−12σ2)+σz

St+1=St⋅e(μ−21σ2)+σz

Store the projected price in an array.

Expected Value (EV) and Confidence Bands Calculation:

EV Path: At each projection bar, compute the mean of all simulated prices.

Variance and Standard Deviation: Calculate the variance and standard deviation of simulated prices to determine the confidence intervals.

Confidence Bands: Using the standard normal z-score (1.96 for 95% confidence), establish upper and lower bounds:

Upper Band=EV+z⋅σEV

Upper Band=EV+z⋅σEV

Lower Band=EV−z⋅σEV

Lower Band=EV−z⋅σEV

EV of EV (Running Average of EV Values):

Calculation: For each projection bar, compute the average of all EV values up to that bar.

EV of EV =1j+1∑k=0jEV

EV of EV =j+11k=0∑jEV

Visualization: Plotted as a dynamic line reflecting the evolving average EV across the projection period.

Visualization Elements

Simulation Lines:

Appearance: Semi-transparent blue lines representing individual GBM simulation paths.

Purpose: Illustrate a range of possible future price trajectories based on current drift and volatility.

Expected Value (EV) Line:

Appearance: Solid orange line.

Purpose: Shows the average projected price at each future bar across all simulations.

Confidence Bands:

Upper Band: Dashed green line indicating the upper 95% confidence boundary.

Lower Band: Dashed red line indicating the lower 95% confidence boundary.

Purpose: Highlight the range within which the price is statistically expected to remain with 95% confidence.

EV of EV Line:

Appearance: Dashed purple line.

Purpose: Displays the running average of EV values, providing a smoothed trend of the central tendency across the projection period. As the mean of sample means it approximates the population mean (i.e. the trend since the anchor point.)

Current Price:

Appearance: Semi-transparent white line.

Purpose: Serves as a reference point for comparing actual price movements against projected paths.

Usage Instructions

Configuring User Inputs:

Anchor Time:

Set to a specific timestamp to start projections from a historical point or leave it as default to use the current bar's time.

Projection Candles (Bars):

Define the number of future bars to project (e.g., 12). Adjust based on your trading timeframe and analysis needs.

Number of Simulations:

Specify the number of GBM paths to simulate (e.g., 30). Higher numbers yield more accurate EV and confidence bands but may impact performance.

Display Toggles:

Show Simulation Lines: Toggle to display or hide individual GBM simulation paths.

Show Expected Value Line: Toggle to display or hide the EV path.

Show Upper Confidence Band: Toggle to display or hide the upper confidence boundary.

Show Lower Confidence Band: Toggle to display or hide the lower confidence boundary.

Show EV of EV Line: Toggle to display or hide the running average of EV values.

Managing TradingView's Object Limits:

Understanding Limits:

TradingView imposes a limit on the number of graphical objects (e.g., lines) that can be rendered. High values for projection candles and simulations can quickly consume these limits. TradingView appears to only allow a total of 55 candles to be projected, so if you want to see two complete lines, you would have to set the projection length to 27: since 27 * 2 = 54 and 54 < 55.

Optimizing Performance:

Use Toggles: Enable only the necessary visual elements. For instance, disable simulation lines and confidence bands when focusing on the EV and EV of EV lines. You can also use the maximum projection length of 55 with the lower limit confidence band as the only line, visualizing a long horizon for your risk.

Adjust Parameters: Lower the number of projection candles or simulations to stay within object limits without compromising essential insights.

Interpreting the Indicator:

Simulation Lines (Blue):

Represent individual potential future price paths based on GBM. A wider spread indicates higher volatility.

Expected Value (EV) Line (Goldenrod):

Shows the mean projected price at each future bar, providing a central trend.

Confidence Bands (Green & Red):

Indicate the statistical range (95% confidence) within which the price is expected to remain.

EV of EV Line (Dotted Line - Goldenrod):

Reflects the running average of EV values, offering a smoothed perspective of expected price trends over the projection period.

Current Price (White):

Serves as a benchmark for assessing how actual prices compare to projected paths.

Practical Applications

Risk Management:

Confidence Bands: Help in identifying potential support and resistance levels based on statistical confidence intervals.

EV Path: Assists in setting realistic target prices and stop-loss levels aligned with projected expectations.

Trend Analysis:

EV of EV Line: Offers a smoothed trendline, aiding in identifying overarching market directions amidst price volatility. Indicative of the population mean/overall trend of the data since your anchor point.

Scenario Planning:

Simulation Lines: Enable traders to visualize multiple potential outcomes, fostering better decision-making under uncertainty.

Performance Evaluation:

Comparing Actual vs. Projected Prices: Assess how actual price movements align with projected scenarios, refining trading strategies over time.

Mathematical and Statistical Insights

Simulation Integrity:

Independence: Each simulation path is generated independently, ensuring unbiased and diverse projections.

Randomness: Utilizes a Gaussian random number generator to introduce variability in diffusion terms, mimicking real market randomness.

Statistical Reliability:

Central Limit Theorem (CLT): By simulating a sufficient number of paths (e.g., 30), the sample mean (EV) converges to the population mean, ensuring reliable EV and confidence band calculations.

Variance Calculation: Accurate computation of variance from simulation data ensures precise confidence intervals.

Dynamic Projections:

Running Average (EV of EV): Provides a cumulative perspective, allowing traders to observe how the average expectation evolves as the projection progresses.

Customization and Enhancements

Adjustable Parameters:

Tailor the projection length and simulation count to match your trading style and analysis depth.

Visual Customization:

Modify line colors, styles, and transparency to enhance clarity and fit chart aesthetics.

Extended Statistical Metrics:

Future iterations can incorporate additional metrics like median projections, skewness, or alternative confidence intervals.

Dynamic Recalculation:

Implement logic to automatically update projections as new data becomes available, ensuring real-time relevance.

Performance Considerations

Object Count Management:

High simulation counts and extended projection periods can lead to a significant number of graphical objects, potentially slowing down chart performance.

Solution: Utilize display toggles effectively and optimize projection parameters to balance detail with performance.

Computational Efficiency:

The script employs efficient array handling and conditional plotting to minimize unnecessary computations and object creation.

Conclusion

The Anchored GBM Projections + EV & Confidence Bands indicator is a robust tool for traders seeking to forecast potential future price movements using statistical models. By integrating Geometric Brownian Motion simulations with expected value calculations and confidence intervals, it offers a comprehensive view of possible market scenarios. The addition of the "EV of EV" line further enhances analytical depth by providing a running average of expected values, aiding in trend identification and strategic decision-making.

Hope it helps!

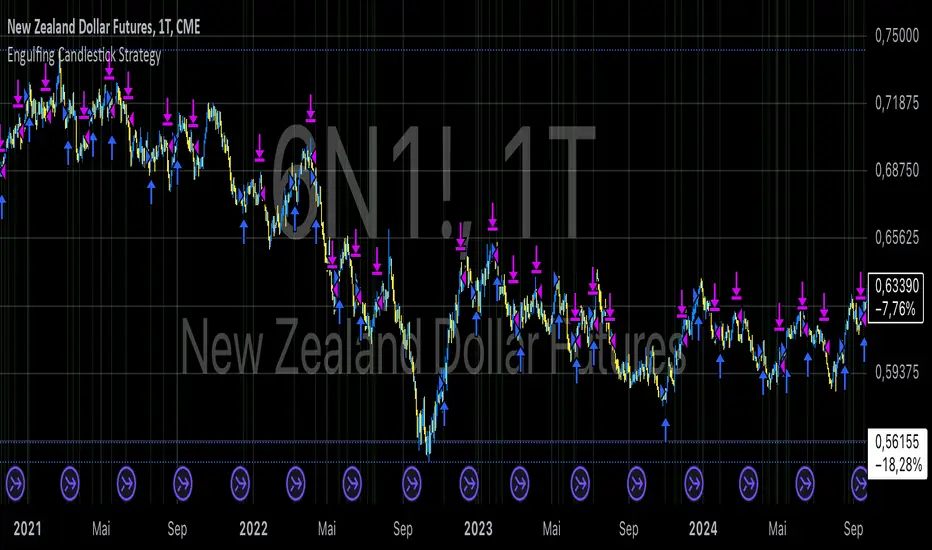

Engulfing Candlestick StrategyEver wondered whether the Bullish or Bearish Engulfing pattern works or has statistical significance? This script is for you. It works across all markets and timeframes.

The Engulfing Candlestick Pattern is a widely used technical analysis pattern that traders use to predict potential price reversals. It consists of two candles: a small candle followed by a larger one that "engulfs" the previous candle. This pattern is considered bullish when it occurs in a downtrend (bullish engulfing) and bearish when it occurs in an uptrend (bearish engulfing).

Statistical Significance of the Engulfing Pattern:

While many traders rely on candlestick patterns for making decisions, research on the statistical significance of these patterns has produced mixed results. A study by Dimitrios K. Koutoupis and K. M. Koutoupis (2014), titled "Testing the Effectiveness of Candlestick Chart Patterns in Forex Markets," indicates that candlestick patterns, including the engulfing pattern, can provide some predictive power, but their success largely depends on the market conditions and timeframe used. The researchers concluded that while some candlestick patterns can be useful, traders must combine them with other indicators or market knowledge to improve their predictive accuracy.

Another study by Brock, Lakonishok, and LeBaron (1992), "Simple Technical Trading Rules and the Stochastic Properties of Stock Returns," explores the profitability of technical indicators, including candlestick patterns, and finds that simple trading rules, such as those based on moving averages or candlestick patterns, can occasionally outperform a random walk in certain market conditions.

However, Jorion (1997), in his work "The Risk of Speculation: The Case of Technical Analysis," warns that the reliability of candlestick patterns, including the engulfing patterns, can vary significantly across different markets and periods. Therefore, it's important to use these patterns as part of a broader trading strategy that includes other risk management techniques and technical indicators.

Application Across Markets:

This script applies to all markets (e.g., stocks, commodities, forex) and timeframes, making it a versatile tool for traders seeking to explore the statistical effectiveness of the bullish and bearish engulfing patterns in their own trading.

Conclusion:

This script allows you to backtest and visualize the effectiveness of the Bullish and Bearish Engulfing patterns across any market and timeframe. While the statistical significance of these patterns may vary, the script provides a clear framework for evaluating their performance in real-time trading conditions. Always remember to combine such patterns with other risk management strategies and indicators to enhance their predictive power.

Daytrading ES Wick Length StrategyThis Pine Script strategy calculates the combined length of upper and lower wicks of candlesticks and uses a customizable moving average (MA) to identify potential long entry points. The strategy compares the total wick length to the MA with an added offset. If the wick length exceeds the offset-adjusted MA, the strategy enters a long position. The position is automatically closed after a user-defined holding period.

Key Features:

1. Calculates the sum of upper and lower wicks for each candlestick.

2. Offers four types of moving averages (SMA, EMA, WMA, VWMA) for analysis.

3. Allows the user to set a customizable MA length and an offset to shift the MA.

4. Automatically exits positions after a specified number of bars.

5. Visualizes the wick length as a histogram and the offset-adjusted MA as a line.

References:

• Candlestick wick analysis: Nison, S. (1991). Japanese Candlestick Charting Techniques.

• Moving averages: Brock, W., Lakonishok, J., & LeBaron, B. (1992). “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns”. Journal of Finance.

This strategy is suitable for identifying candlesticks with significant volatility and long wicks, which can indicate potential trend reversals or continuations.

Up Gap Strategy with DelayThis strategy, titled “Up Gap Strategy with Delay,” is based on identifying up gaps in the price action of an asset. A gap is defined as the percentage difference between the current bar’s open price and the previous bar’s close price. The strategy triggers a long position if the gap exceeds a user-defined threshold and includes a delay period before entering the position. After entering, the position is held for a set number of periods before being closed.

Key Features:

1. Gap Threshold: The strategy defines an up gap when the gap size exceeds a specified threshold (in percentage terms). The gap threshold is an input parameter that allows customization based on the user’s preference.

2. Delay Period: After the gap occurs, the strategy waits for a delay period before initiating a long position. This delay can help mitigate any short-term volatility that might occur immediately after the gap.

3. Holding Period: Once the position is entered, it is held for a user-defined number of periods (holdingPeriods). This is to capture the potential post-gap trend continuation, as gaps often indicate strong directional momentum.

4. Gap Plotting: The strategy visually plots up gaps on the chart by placing a green label beneath the bar where the gap condition is met. Additionally, the background color turns green to highlight up-gap occurrences.

5. Exit Condition: The position is exited after the defined holding period. The strategy ensures that the position is closed after this time, regardless of whether the price is in profit or loss.

Scientific Background:

The gap theory has been widely studied in financial literature and is based on the premise that gaps in price often represent areas of significant support or resistance. According to research by Kaufman (2002), gaps in price action can be indicators of future price direction, particularly when they occur after a period of consolidation or a trend reversal. Moreover, Gaps and their Implications in Technical Analysis (Murphy, 1999) highlights that gaps can reflect imbalances between supply and demand, leading to high momentum and potential price continuation or reversal.

In trading strategies, utilizing gaps with specific conditions, such as delay and holding periods, can enhance the ability to capture significant price moves. The strategy’s delay period helps avoid potential market noise immediately after the gap, while the holding period seeks to capitalize on the price continuation that often follows gap formation.

This methodology aligns with momentum-based strategies, which rely on the persistence of trends in financial markets. Several studies, including Jegadeesh & Titman (1993), have documented the existence of momentum effects in stock prices, where past price movements can be predictive of future returns.

Conclusion:

This strategy incorporates gap detection and momentum principles, supported by empirical research in technical analysis, to attempt to capitalize on price movements following significant gaps. By waiting for a delay period and holding the position for a specified time, it aims to mitigate the risk associated with early volatility while maximizing the potential for sustained price moves.

Statistical Trend Analysis (Scatterplot) [BigBeluga]Statistical Trend Analysis (Scatterplot) provides a unique perspective on market dynamics by combining the statistical concept of z-scores with scatterplot visualization to assess price momentum and potential trend shifts.

🧿 What is Z-Score?

Definition: A z-score is a statistical measure that quantifies how far a data point is from the mean, expressed in terms of standard deviations.

In this Indicator:

A high positive z-score indicates the price is significantly above the average.

A low negative z-score indicates the price is significantly below the average.

The indicator also calculates the rate of change of the z-score, helping identify momentum shifts in the market.

🧿 Key Features:

Scatterplot Visualization:

Displays data points of z-score and its change across four quadrants.

Quadrants help interpret market conditions:

Upper Right (Strong Bullish Momentum): Most data points here signal an ongoing uptrend.

Upper Left (Weakening Momentum): Data points here may indicate a potential market shift or ranging market.

Lower Left (Strong Bearish Momentum): Indicates a dominant downtrend.

Lower Right (Trend Shift to Bullish/Ranging): Suggests weakening bearish momentum or an emerging uptrend.

Color-Coded Candles:

Candles are dynamically colored based on the z-score, providing a visual cue about the price's deviation from the mean.

Z-Score Time Series:

A line plot of z-scores over time shows price deviation trends.

A gray histogram displays the rate of change of the z-score, highlighting momentum shifts.

🧿 Usage:

Use the scatterplot and quadrant gauges to understand the current market momentum and potential shifts.

Monitor the z-score line plot to identify overbought/oversold conditions.

Utilize the gray histogram to detect momentum reversals and trend strength.

This tool is ideal for traders who rely on statistical insights to confirm trends, detect potential reversals, and assess market momentum visually and quantitatively.

ROE BandROE Band shows the return on net profit from shareholders' equity and the formula for decomposition

ROE = ROA x CSL x CEL

ROE Band consists of 5 parts:

1. ROE (TTM) is the 12-month ROE calculation in "green"

2. Return on Equity (ROE) is the current quarterly net profit / the average of the beginning and ending periods of shareholders' equity in "yellow"

3. Return on Assets (ROA) is the current quarterly NOPAT (net profit before tax) / the average of the beginning and ending periods of total assets in "blue"

4. Capital structure leverage (CSL) is a financial measure that compares a company's debt to its total capital. It is calculated by taking the average of the beginning and ending periods of total assets / the average of the beginning and ending periods of shareholders' equity. The higher the CSL, the more deb, in. "red"

5. Common earnings leverage (CEL) is the proportion of net profit and NOPAT (net profit before tax), where a lower CEL means more tax, in "orange"

The "😱" emoji represents the value if it increases by more than or decreases by less than 20%, e.g.

- ROE(TTM), ROE, ROA, CEL is decreasing

- CSL is increasing

The "🔥" emoji represents the value if it increases by more than or decreases, e.g.

- ROE(TTM), ROE, ROA, CEL is increasing

- CSL is decreasing

RSI Trend [MacroGlide]The RSI Trend indicator is a versatile and intuitive tool designed for traders who want to enhance their market analysis with visual clarity. By combining Stochastic RSI with moving averages, this indicator offers a dynamic view of market momentum and trends. Whether you're a beginner or an experienced trader, this tool simplifies identifying key market conditions and trading opportunities.

Key Features:

• Stochastic RSI-Based Calculations: Incorporates Stochastic RSI to provide a nuanced view of overbought and oversold conditions, enhancing standard RSI analysis.

• Dynamic Moving Averages: Includes two customizable moving averages (MA1 and MA2) based on smoothed Stochastic RSI, offering flexibility to align with your trading strategy.

• Candle Color Coding: Automatically colors candles on the chart:

• Blue: When the faster moving average (MA2) is above the slower one (MA1), signaling bullish momentum.

• Orange: When the faster moving average is below the slower one, indicating bearish momentum.

• Integrated Scaling: The indicator dynamically adjusts with the chart's scale, ensuring seamless visualization regardless of zoom level.

How to Use:

• Add the Indicator: Apply the indicator to your chart from the TradingView library.

• Interpret Candle Colors: Use the color-coded candles to quickly identify bullish (blue) and bearish (orange) phases.

• Customize to Suit Your Needs: Adjust the lengths of the moving averages and the Stochastic RSI parameters to better fit your trading style and timeframe.

• Combine with Other Tools: Pair this indicator with trendlines, volume analysis, or support and resistance levels for a comprehensive trading approach.

Methodology:

The indicator utilizes Stochastic RSI, a derivative of the standard RSI, to measure momentum more precisely. By applying smoothing and calculating moving averages, the tool identifies shifts in market trends. These trends are visually represented through candle color changes, making it easy to spot transitions between bullish and bearish phases at a glance.

Originality and Usefulness:

What sets this indicator apart is its seamless integration of Stochastic RSI and moving averages with real-time candle coloring. The result is a visually intuitive tool that adapts dynamically to chart scaling, offering clarity without clutter.

Charts:

When applied, the indicator plots two moving averages alongside color-coded candles. The combination of visual cues and trend logic helps traders easily interpret market momentum and make informed decisions.

Enjoy the game!

Smooth RSI [MarktQuant]This indicator combines elements of the Relative Strength Index (RSI) and Rate of Change (RoC) to provide a smoother and potentially more insightful view of market momentum and price movement. The Smooth RSI calculates RSI values across four price points (high, open, low, close) to average them, offering a less volatile RSI signal. Additionally, it incorporates a Rate of Change for trend confirmation, enhancing the decision-making process for trade entries and exits.

Features:

Multi-RSI Calculation: RSI is computed for high, open, low, and close prices, then averaged to reduce noise.

Trend Confirmation with RoC: Uses the Rate of Change to validate the RSI signals, coloring bars based on the trend direction.

Visual Signals:

Bar colors change based on combined RSI and RoC signals.

Green for bullish signals (RSI above 50 and positive RoC).

Red for bearish signals (RSI below 50 and negative RoC).

Horizontal lines at 30, 50, and 70 to denote overbought, neutral, and oversold conditions.

Customizable Display:

Option to show/hide RSI plot or RoC plot for cleaner charts.

Candle plot overlay option to visualize current price action alongside the indicator.

Inputs:

RSI Length: Default 28. Adjusts the lookback period for RSI calculation.

RoC Length: Default 28. Sets the period for the Rate of Change calculation.

Plot Settings:

Show RSI - Toggle RSI plot visibility.

Show RoC - Toggle RoC plot visibility.

Usage:

Long signals are indicated when the average RSI is above 50 and the RoC is positive.

Short signals are suggested when the average RSI falls below 50 with a negative RoC.

The color coding helps visually confirm trends at a glance.

Notes:

This indicator is best used in conjunction with other analysis methods to confirm signals.

Adjust the length parameters based on your trading timeframe for optimal results.

Disclaimer:

This indicator does not guarantee trading success; use it as part of a comprehensive trading strategy. Always conduct your own analysis before making trading decisions.

Market Correlation AnalysisMarket Correlation Analysis is an indicator that measures the correlation of any two instruments.

To express price changes in a way that is comparable, this indicator uses a percentage of the ATR as a unit.

User Inputs:

Other Symbol - the symbol which we want to compare with the symbol of the main chart.

ATR for Price Movement Normalisation - I recommend high values to get the ATR more stable across time - if the ATR drastically changes, the indicator will register that as a price movement, because the unit in which price movements are measured itself changed by a lot. However, with higher values the ATR is stable and, in my opinion, more reliable than simply a percentage change of the current price.

Correlation Length - this is the number of bars for which the correlation coefficient will be calculated.

About The Indicator:

Market Correlation Analysis expresses the price changes of both instruments in question on the same histogram.

By default, the price changes that represent the instrument of the main chart are expressed with thinner bars of stronger colour, while the price changes that represent the other instrument are expressed with much thicker bars, which are of more pale colour.

The correlation coefficient is not expressed on the histogram, as it has a different scale. Therefore, it is only showed as a number.

I hope this indicator can make it easier to understand just how much two instruments have been similar to one another over a certain period of time. The possibility to see the correlation for any given time frame can give information that very specific to any trading style.

Enhanced Price Z-Score OscillatorThe Enhanced Price Z-Score Oscillator by tkarolak is a powerful tool that transforms raw price data into an easy-to-understand statistical visualization using Z-Score-derived candlesticks. Simply put, it shows how far prices stray from their average in terms of standard deviations (Z-Scores), helping traders identify when prices are unusually high (overbought) or unusually low (oversold).

The indicator’s default feature displays Z-Score Candlesticks, where each candle reflects the statistical “distance” of the open, high, low, and close prices from their average. This creates a visual map of market extremes and potential reversal points. For added flexibility, you can also switch to Z-Score line plots based on either Close prices or OHLC4 averages.

With clear threshold lines (±2σ and ±3σ) marking moderate and extreme price deviations, and color-coded zones to highlight overbought and oversold areas, the oscillator simplifies complex statistical concepts into actionable trading insights.

Temporary Help Services Jobs - Trend Allocation StrategyThis strategy is designed to capitalize on the economic trends represented by the Temporary Help Services (TEMPHELPS) index, which is published by the Federal Reserve Economic Data (FRED). Temporary Help Services Jobs are often regarded as a leading indicator of labor market conditions, as changes in temporary employment levels frequently precede broader employment trends.

Methodology:

Data Source: The strategy uses the FRED dataset TEMPHELPS for monthly data on temporary help services.

Trend Definition:

Uptrend: When the current month's value is greater than the previous month's value.

Downtrend: When the current month's value is less than the previous month's value.

Entry Condition: A long position is opened when an uptrend is detected, provided no position is currently held.

Exit Condition: The long position is closed when a downtrend is detected.

Scientific Basis:

The TEMPHELPS index serves as a leading economic indicator, as noted in studies analyzing labor market cyclicality (e.g., Katz & Krueger, 1999). Temporary employment is often considered a proxy for broader economic conditions, particularly in predicting recessions or recoveries. Incorporating this index into trading strategies allows for aligning trades with potential macroeconomic shifts, as suggested by research on employment trends and market performance (Autor, 2001; Valetta & Bengali, 2013).

Usage:

This strategy is best suited for long-term investors or macroeconomic trend followers who wish to leverage labor market signals for equity or futures trading. It operates exclusively on end-of-month data, ensuring minimal transaction costs and noise.

Option Time ValueThis TradingView script calculates and visualizes the time value of an option (Call or Put) based on its market price and intrinsic value. The time value represents the premium paid for the option above its intrinsic value, and it is a key metric for analyzing the cost of holding an option.

This script is suitable for traders analyzing options on indices or stocks, such as the NIFTY 50, and supports both Call and Put options. By dynamically extracting the strike price and option type from the input symbol, it adapts seamlessly to the selected instrument.

Key Features:

Dynamic Instrument Selection:

Users can input the underlying asset (e.g., NSE:NIFTY) and the specific option instrument (e.g., NSE:NIFTY250327C24000 for a Call or NSE:NIFTY250327P24000 for a Put).

Automatic Option Type Detection:

The script detects whether the option is a Call or a Put by parsing the input symbol for the characters "C" (Call) or "P" (Put).

Dynamic Strike Price Extraction:

The strike price is dynamically extracted from the input option symbol, eliminating the need for hardcoding and reducing user errors.

Key Metrics Plotted:

Time Value: The premium paid above the intrinsic value, plotted in blue.

Intrinsic Value: The calculated intrinsic value of the option, plotted in green.

Seamless Integration:

Designed for ease of use and integration into existing TradingView setups.

Automatically adjusts to the timeframe and pricing data of the selected instruments.

McClellan A-D Volume Integration ModelThe strategy integrates the McClellan A-D Oscillator with an adjustment based on the Advance/Decline (A-D) volume data. The McClellan Oscillator is calculated by taking the difference between the short-term and long-term exponential moving averages (EMAs) of the A-D line. This strategy introduces an enhancement where the A-D volume (the difference between the advancing and declining volume) is factored in to adjust the oscillator value.

Inputs:

• ema_short_length: The length for the short-term EMA of the A-D line.

• ema_long_length: The length for the long-term EMA of the A-D line.

• osc_threshold_long: The threshold below which the oscillator must drop for an entry signal to trigger.

• exit_periods: The number of periods after which the position is closed.

• Data Sources:

• ad_advance and ad_decline are the data sources for advancing and declining issues, respectively.

• vol_advance and vol_decline are the volume data for the advancing and declining issues. If volume data is unavailable, it defaults to na (Not Available), and the fallback logic ensures that the strategy continues to function.

McClellan Oscillator with Volume Adjustment:

• The A-D line is calculated by subtracting the declining issues from the advancing issues. Then, the volume difference is applied to this line, creating a “weighted” A-D line.

• The short and long EMAs are calculated for the weighted A-D line to generate the McClellan Oscillator.

Entry Condition:

• The strategy looks for a reversal signal, where the oscillator falls below the threshold and then rises above it again. The condition is designed to trigger a long position when this reversal happens.

Exit Condition:

• The position is closed after a set number of periods (exit_periods) have passed since the entry.

Plotting:

• The McClellan Oscillator and the threshold are plotted on the chart for visual reference.

• Entry and exit signals are highlighted with background colors to make the signals more visible.

Scientific Background:

The McClellan A-D Oscillator is a popular market breadth indicator developed by Sherman and Marian McClellan. It is used to gauge the underlying strength of a market by analyzing the difference between the number of advancing and declining stocks. The oscillator is typically calculated using exponential moving averages (EMAs) of the A-D line, with the idea being that crossovers of these EMAs indicate potential changes in the market’s direction.