Swing Counter [theEccentricTrader]█ OVERVIEW

This indicator counts the number of confirmed swing high and swing low scenarios on any given candlestick chart and displays the statistics in a table, which can be repositioned and resized at the user's discretion.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a high price equal to or above the price it opened.

• A red candle is one that closes with a low price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Peak and Trough Prices (Advanced)

• The advanced peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the highest preceding green candle high price, depending on which is higher.

• The advanced trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the lowest preceding red candle low price, depending on which is lower.

Green and Red Peaks and Troughs

• A green peak is one that derives its price from the green candle/s that constitute the swing high.

• A red peak is one that derives its price from the red candle that completes the swing high.

• A green trough is one that derives its price from the green candle that completes the swing low.

• A red trough is one that derives its price from the red candle/s that constitute the swing low.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

█ FEATURES

Inputs

• Start Date

• End Date

• Position

• Text Size

• Show Sample Period

• Show Plots

• Show Lines

Table

The table is colour coded, consists of three columns and nine rows. Blue cells denote neutral scenarios, green cells denote return line uptrend and uptrend scenarios, and red cells denote downtrend and return line downtrend scenarios.

The swing scenarios are listed in the first column with their corresponding total counts to the right, in the second column. The last row in column one, row nine, displays the sample period which can be adjusted or hidden via indicator settings.

Rows three and four in the third column of the table display the total higher peaks and higher troughs as percentages of total peaks and troughs, respectively. Rows five and six in the third column display the total lower peaks and lower troughs as percentages of total peaks and troughs, respectively. And rows seven and eight display the total double-top peaks and double-bottom troughs as percentages of total peaks and troughs, respectively.

Plots

I have added plots as a visual aid to the swing scenarios listed in the table. Green up-arrows with ‘HP’ denote higher peaks, while green up-arrows with ‘HT’ denote higher troughs. Red down-arrows with ‘LP’ denote higher peaks, while red down-arrows with ‘LT’ denote lower troughs. Similarly, blue diamonds with ‘DT’ denote double-top peaks and blue diamonds with ‘DB’ denote double-bottom troughs. These plots can be hidden via indicator settings.

Lines

I have also added green and red trendlines as a further visual aid to the swing scenarios listed in the table. Green lines denote return line uptrends (higher peaks) and uptrends (higher troughs), while red lines denote downtrends (lower peaks) and return line downtrends (lower troughs). These lines can be hidden via indicator settings.

█ HOW TO USE

This indicator is intended for research purposes and strategy development. I hope it will be useful in helping to gain a better understanding of the underlying dynamics at play on any given market and timeframe. It can, for example, give you an idea of any inherent biases such as a greater proportion of higher peaks to lower peaks. Or a greater proportion of higher troughs to lower troughs. Such information can be very useful when conducting top down analysis across multiple timeframes, or considering entry and exit methods.

What I find most fascinating about this logic, is that the number of swing highs and swing lows will always find equilibrium on each new complete wave cycle. If for example the chart begins with a swing high and ends with a swing low there will be an equal number of swing highs to swing lows. If the chart starts with a swing high and ends with a swing high there will be a difference of one between the two total values until another swing low is formed to complete the wave cycle sequence that began at start of the chart. Almost as if it was a fundamental truth of price action, although quite common sensical in many respects. As they say, what goes up must come down.

The objective logic for swing highs and swing lows I hope will form somewhat of a foundational building block for traders, researchers and developers alike. Not only does it facilitate the objective study of swing highs and swing lows it also facilitates that of ranges, trends, double trends, multi-part trends and patterns. The logic can also be used for objective anchor points. Concepts I will introduce and develop further in future publications.

█ LIMITATIONS

Some higher timeframe candles on tickers with larger lookbacks such as the DXY , do not actually contain all the open, high, low and close (OHLC) data at the beginning of the chart. Instead, they use the close price for open, high and low prices. So, while we can determine whether the close price is higher or lower than the preceding close price, there is no way of knowing what actually happened intra-bar for these candles. And by default candles that close at the same price as the open price, will be counted as green. You can avoid this problem by utilising the sample period filter.

The green and red candle calculations are based solely on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with. Alternatively, you can replace the scenarios with your own logic to account for the gap anomalies, if you are feeling up to the challenge.

The sample size will be limited to your Trading View subscription plan. Premium users get 20,000 candles worth of data, pro+ and pro users get 10,000, and basic users get 5,000. If upgrading is currently not an option, you can always keep a rolling tally of the statistics in an excel spreadsheet or something of the like.

█ NOTES

I feel it important to address the mention of advanced peak and trough price logic. While I have introduced the concept, I have not included the logic in my script for a number of reasons. The most pertinent of which being the amount of extra work I would have to do to include it in a public release versus the actual difference it would make to the statistics. Based on my experience, there are actually only a small number of cases where the advanced peak and trough prices are different from the basic peak and trough prices. And with adequate multi-timeframe analysis any high or low prices that are not captured using basic peak and trough price logic on any given time frame, will no doubt be captured on a higher timeframe. See the example below on the 1H FOREXCOM:USDJPY chart (Figure 1), where the basic peak price logic denoted by the indicator plot does not capture what would be the advanced peak price, but on the 2H FOREXCOM:USDJPY chart (Figure 2), the basic peak logic does capture the advanced peak price from the 1H timeframe.

Figure 1.

Figure 2.

█ RAMBLINGS

“Never was there an age that placed economic interests higher than does our own. Never was the need of a scientific foundation for economic affairs felt more generally or more acutely. And never was the ability of practical men to utilize the achievements of science, in all fields of human activity, greater than in our day. If practical men, therefore, rely wholly on their own experience, and disregard our science in its present state of development, it cannot be due to a lack of serious interest or ability on their part. Nor can their disregard be the result of a haughty rejection of the deeper insight a true science would give into the circumstances and relationships determining the outcome of their activity. The cause of such remarkable indifference must not be sought elsewhere than in the present state of our science itself, in the sterility of all past endeavours to find its empirical foundations.” (Menger, 1871, p.45).

█ BIBLIOGRAPHY

Menger, C. (1871) Principles of Economics. Reprint, Auburn, Alabama: Ludwig Von Mises Institute: 2007.

Statistics

Global GDPThis is the GlobalGDP of the richest and most populous countries

It is measured in USD

The countries included are the same than are included in my Global M2 indicator, as of to be able to compare them side to side.

Candle Counter [theEccentricTrader]█ OVERVIEW

This indicator counts the number of confirmed candle scenarios on any given candlestick chart and displays the statistics in a table, which can be repositioned and resized at the user's discretion.

█ CONCEPTS

Green and Red Candles

A green candle is one that closes with a high price equal to or above the price it opened.

A red candle is one that closes with a low price that is lower than the price it opened.

Upper Candle Trends

A higher high candle is one that closes with a higher high price than the high price of the preceding candle.

A lower high candle is one that closes with a lower high price than the high price of the preceding candle.

A double-top candle is one that closes with a high price that is equal to the high price of the preceding candle.

Lower Candle Trends

A higher low candle is one that closes with a higher low price than the low price of the preceding candle.

A lower low candle is one that closes with a lower low price than the low price of the preceding candle.

A double-bottom candle is one that closes with a low price that is equal to the low price of the preceding candle.

█ FEATURES

Inputs

Start Date

End Date

Position

Text Size

Show Sample Period

Show Plots

Table

The table is colour coded, consists of three columns and twenty-two rows. Blue cells denote all candle scenarios, green cells denote green candle scenarios and red cells denote red candle scenarios.

The candle scenarios are listed in the first column with their corresponding total counts to the right, in the second column. The last row in column one, row twenty-two, displays the sample period which can be adjusted or hidden via indicator settings.

Rows two and three in the third column of the table display the total green and red candles as percentages of total candles. Rows four to nine in column three, coloured blue, display the corresponding candle scenarios as percentages of total candles. Rows ten to fifteen in column three, coloured green, display the corresponding candle scenarios as percentages of total green candles. And lastly, rows sixteen to twenty-one in column three, coloured red, display the corresponding candle scenarios as percentages of total red candles.

Plots

I have added plots as a visual aid to the various candle scenarios listed in the table. Green up-arrows denote higher high candles when above bar and higher low candles when below bar. Red down-arrows denote lower high candles when above bar and lower low candles when below bar. Similarly, blue diamonds when above bar denote double-top candles and when below bar denote double-bottom candles. These plots can also be hidden via indicator settings.

█ HOW TO USE

This indicator is intended for research purposes and strategy development. I hope it will be useful in helping to gain a better understanding of the underlying dynamics at play on any given market and timeframe. It can, for example, give you an idea of any inherent biases such as a greater proportion of green candles to red. Or a greater proportion of higher low green candles to lower low green candles. Such information can be very useful when conducting top down analysis across multiple timeframes, or considering trailing stop loss methods.

What you do with these statistics and how far you decide to take your research is entirely up to you, the possibilities are endless.

This is just the first and most basic in a series of indicators that can be used to study objective price action scenarios and develop a systematic approach to trading.

█ LIMITATIONS

Some higher timeframe candles on tickers with larger lookbacks such as the DXY, do not actually contain all the open, high, low and close (OHLC) data at the beginning of the chart. Instead, they use the close price for open, high and low prices. So, while we can determine whether the close price is higher or lower than the preceding close price, there is no way of knowing what actually happened intra-bar for these candles. And by default candles that close at the same price as the open price, will be counted as green. You can avoid this problem by utilising the sample period filter.

The green and red candle calculations are based solely on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with. Alternatively, you can replace the scenarios with your own logic to account for the gap anomalies, if you are feeling up to the challenge.

It is also worth noting that the sample size will be limited to your Trading View subscription plan. Premium users get 20,000 candles worth of data, pro+ and pro users get 10,000, and basic users get 5,000. If upgrading is currently not an option, you can always keep a rolling tally of the statistics in an excel spreadsheet or something of the like.

Commission-aware Trade LabelsCommission-aware Trade Labels

Description:

This library provides an easy way to visualize take-profit and stop-loss levels on your chart, taking into account trading commissions. The library calculates and displays the net profit or loss, along with other useful information such as risk/reward ratio, shares, and position size.

Features:

Configurable take-profit and stop-loss prices or percentages.

Set entry amount or shares.

Calculates and displays the risk/reward ratio.

Shows net profit or loss, considering trading commissions.

Customizable label appearance.

Usage:

Add the script to your chart.

Create an Order object for take-profit and stop-loss with desired configurations.

Call target_label() and stop_label() methods for each order object.

Example:

target_order = Order.new(take_profit_price=27483, stop_loss_price=28000, shares=0.2)

stop_order = Order.new(stop_loss_price=29000, shares=1)

target_order.target_label()

stop_order.stop_label()

This script is a powerful tool for visualizing your trading strategy's performance and helps you make better-informed decisions by considering trading commissions in your profit and loss calculations.

Library "tradelabels"

entry_price(this)

Parameters:

this : Order object

@return entry_price

take_profit_price(this)

Parameters:

this : Order object

@return take_profit_price

stop_loss_price(this)

Parameters:

this : Order object

@return stop_loss_price

is_long(this)

Parameters:

this : Order object

@return entry_price

is_short(this)

Parameters:

this : Order object

@return entry_price

percent_to_target(this, target)

Parameters:

this : Order object

target : Target price

@return percent

risk_reward(this)

Parameters:

this : Order object

@return risk_reward_ratio

shares(this)

Parameters:

this : Order object

@return shares

position_size(this)

Parameters:

this : Order object

@return position_size

commission_cost(this, target_price)

Parameters:

this : Order object

@return commission_cost

target_price

net_result(this, target_price)

Parameters:

this : Order object

target_price : The target price to calculate net result for (either take_profit_price or stop_loss_price)

@return net_result

create_take_profit_label(this, prefix, size, offset_x, bg_color, text_color)

Parameters:

this

prefix

size

offset_x

bg_color

text_color

create_stop_loss_label(this, prefix, size, offset_x, bg_color, text_color)

Parameters:

this

prefix

size

offset_x

bg_color

text_color

create_entry_label(this, prefix, size, offset_x, bg_color, text_color)

Parameters:

this

prefix

size

offset_x

bg_color

text_color

create_line(this, target_price, line_color, offset_x, line_style, line_width, draw_entry_line)

Parameters:

this

target_price

line_color

offset_x

line_style

line_width

draw_entry_line

Order

Order

Fields:

entry_price : Entry price

stop_loss_price : Stop loss price

stop_loss_percent : Stop loss percent, default 2%

take_profit_price : Take profit price

take_profit_percent : Take profit percent, default 6%

entry_amount : Entry amount, default 5000$

shares : Shares

commission : Commission, default 0.04%

Mason’s Line IndicatorThe Macon Strategy is an idea conceived by Didier Darcet , co-founder of Gavekal Intelligence Software. Inspired by the Water Level, an instrument used by masons to check the horizontality or verticality of a wall. This method aims to measure the psychology of financial markets and determine if the market is balanced or tilting towards an unfavorable side, focusing on the behavioral risk of markets rather than economic or political factors.

The strategy examines the satisfaction and frustration of investors based on the distance between the low and high points of the market over a period of one year. Investor satisfaction is influenced by the current price of the index and the path taken to reach that price. The distance to the low point provides satisfaction, while the distance to the high point generates frustration. The balance between the two dictates investors’ desire to hold or sell their positions.

To refine the strategy, it is important to consider the opinion of a group of investors rather than just one individual. The members of a hypothetical investor club invest successively throughout the past year. The overall satisfaction of the market on a given day is a democratic expression of all participants.

If the overall satisfaction is below 50%, investors are frustrated and sell their positions. If it is above, they are satisfied and hold their positions. The position of the group of investors relative to the high and low points represents the position of the air bubble in the water level. Market performance is measured day by day based on participant satisfaction or dissatisfaction.

In conclusion, memory, emotions, and decision-making ability are closely linked, and their interaction influences investment decisions. The Macon Strategy highlights the importance of the behavioral dimension in understanding financial market dynamics. By studying investor behavior through this strategy, it is possible to better anticipate market trends and make more informed investment decisions.

Presentation of the Mason’s Line Indicator:

The main strategy of this indicator is to measure the average satisfaction of investors based on the position of an imaginary air bubble in a tube delimited by the market’s highs and lows over a given period. After calculating the satisfaction level, it is then normalized between 0 and 1, and a moving average can be used to visualize trends.

Key features:

Calculation of highs and lows over a user-defined period.

Determination of the position of the air bubble in the tube based on the closing price.

Calculation of the average satisfaction of investors over a selected period.

Normalization of the average satisfaction between 0 and 1.

Visualization of normalized or non-normalized average satisfaction levels, as well as their corresponding moving averages.

User parameters:

Period for min and max (days) : Sets the period over which highs and lows will be calculated (1 to 365 days).

Period for average satisfaction (days) : Determines the period over which the average satisfaction of investors will be calculated (1 to 365 days).

Period for SMA : Sets the period of the simple moving average used to smooth the data (1 to 1000 days).

Bubble_value : Adjustment of the air bubble value, ranging from 0 to 1, in increments of 0.025.

Normalized average satisfaction : Option to choose whether to display the normalized or non-normalized average satisfaction.

Please note that the Mason’s Line Indicator is not a guarantee of future market performance and should be used in conjunction with proper risk management. Always ensure that you have a thorough understanding of the indicator’s methodology and its limitations before making any investment decisions. Additionally, past performance is not indicative of future results.

Kimchi Premium watchThis indicator provides easy-to-see Kimchi premium information.

It provides three pieces of information.

1. Current premium

2. The highest value of the premium over the last 240 candlesticks in the current timeframe.

3. The highest value of the premium over the last 240 candlesticks in the current timeframe.

I think this script is a very simple indicator.

It is usually recommended to get value in a large time frame.

The basic operation formula is as follows.

premium(percent) = ( BTC KRW - ( BTC USDT x USD KRW ) / ( BTC USDT x USDT USD x USD KRW )) x 100

Thank you.

Сoncentrated Market Maker Strategy by oxowlConcentrated Market Maker Strategy by oxowl. This script plots an upper and lower bound for liquidity provision, and checks for rebalancing conditions. It also includes alert conditions for when the price crosses the upper or lower bounds.

Here's an overview of the script:

It defines the input parameters: liquidity range percentage, rebalance frequency in minutes, and minimum trade size in assets.

It calculates the upper and lower bounds for liquidity provision based on the liquidity range percentage.

It initializes variables for the last rebalance time and price.

It defines a rebalance condition based on the frequency and current price within the specified range.

If the rebalance condition is met, it updates the last rebalance time and price.

It plots the upper and lower bounds on the chart as lines and adds price labels for both bounds.

It defines alert conditions for when the price crosses the upper or lower bounds.

Finally, it creates alert conditions with appropriate messages for when the price crosses the upper or lower bounds.

Concentrated liquidity is a concept often used in decentralized finance (DeFi) market-making strategies. It allows liquidity providers (LPs) to focus their liquidity within a specific price range, rather than across the entire price curve. Using an indicator with concentrated liquidity can offer several advantages:

Increased capital efficiency: Concentrated liquidity allows LPs to allocate their capital within a narrower price range. This means that the same amount of capital can generate more significant price impact and potentially higher returns compared to providing liquidity across a broader range.

Customized risk exposure: LPs can choose the price range they feel most comfortable with, allowing them to better manage their risk exposure. By selecting a range based on their market outlook, they can optimize their positions to maximize potential returns.

Adaptive strategies: Indicators that support concentrated liquidity can help traders adapt their strategies based on market conditions. For example, they can choose to provide liquidity around a stable price range during low-volatility periods or adjust their range when market conditions change.

To continue integrating this script into your trading strategy, follow these steps:

Import the script into your TradingView account. Navigate to the Pine editor, paste the code, and save it as a new script.

Apply the indicator to a trading pair chart. You can customize the input parameters (liquidity range percentage, rebalance frequency, and minimum trade size) based on your preferences and risk tolerance.

Set alerts for when the price crosses the upper or lower bounds. This will notify you when it's time to take action, such as adding or removing liquidity, or rebalancing your position.

Monitor the performance of your strategy over time. Adjust the input parameters as needed to optimize your returns and manage risk effectively.

(Optional) Integrate the script with a trading bot or automation platform. If you're using an API-based trading solution, you can incorporate the logic and conditions from the script into your bot's algorithm to automate the process of providing concentrated liquidity and rebalancing your positions.

Remember that no strategy is foolproof, and past performance is not indicative of future results. Always exercise caution when trading and carefully consider your risk tolerance.

Linear Regress on Price And VolumeLinear regression is a statistical method used to model the relationship between a dependent variable and one or more independent variables. It assumes a linear relationship between the dependent variable and the independent variable(s) and attempts to fit a straight line that best describes the relationship.

In the context of predicting the price of a stock based on the volume, we can use linear regression to build a model that relates the price of the stock (dependent variable) to the volume (independent variable). The idea is to use lookback period to predict future prices based on the volume.

To build this indicator, we start by collecting data on the price of the stock and the volume over a selected of time or by default 21 days. We then plot the data on a scatter plot with the volume on the x-axis and the price on the y-axis. If there is a clear pattern in the data, we can fit a straight line to the data using a method called least squares regression. The line represents the best linear approximation of the relationship between the price and the volume.

Once we have the line, we can use it to make predictions. For example, if we observe a certain volume, we can use the line to estimate the corresponding price.

It's worth noting that linear regression assumes a linear relationship between the variables. In reality, the relationship between the price and the volume may be more complex, and other factors may also influence the price of the stock. Therefore, while linear regression can be a useful tool, it should be used in conjunction with other methods and should be interpreted with caution.

Bitwise, Encode, DecodeLibrary "Bitwise, Encode, Decode"

Bitwise, Encode, Decode, and more Library

docs()

Hover-Over Documentation for inside Text Editor

bAnd(a, b)

Returns the bitwise AND of two integers

Parameters:

a : `int` - The first integer

b : `int` - The second integer

Returns: `int` - The bitwise AND of the two integers

bOr(a, b)

Performs a bitwise OR operation on two integers.

Parameters:

a : `int` - The first integer.

b : `int` - The second integer.

Returns: `int` - The result of the bitwise OR operation.

bXor(a, b)

Performs a bitwise Xor operation on two integers.

Parameters:

a : `int` - The first integer.

b : `int` - The second integer.

Returns: `int` - The result of the bitwise Xor operation.

bNot(n)

Performs a bitwise NOT operation on an integer.

Parameters:

n : `int` - The integer to perform the bitwise NOT operation on.

Returns: `int` - The result of the bitwise NOT operation.

bShiftLeft(n, step)

Performs a bitwise left shift operation on an integer.

Parameters:

n : `int` - The integer to perform the bitwise left shift operation on.

step : `int` - The number of positions to shift the bits to the left.

Returns: `int` - The result of the bitwise left shift operation.

bShiftRight(n, step)

Performs a bitwise right shift operation on an integer.

Parameters:

n : `int` - The integer to perform the bitwise right shift operation on.

step : `int` - The number of bits to shift by.

Returns: `int` - The result of the bitwise right shift operation.

bRotateLeft(n, step)

Performs a bitwise right shift operation on an integer.

Parameters:

n : `int` - The int to perform the bitwise Left rotation on the bits.

step : `int` - The number of bits to shift by.

Returns: `int`- The result of the bitwise right shift operation.

bRotateRight(n, step)

Performs a bitwise right shift operation on an integer.

Parameters:

n : `int` - The int to perform the bitwise Right rotation on the bits.

step : `int` - The number of bits to shift by.

Returns: `int` - The result of the bitwise right shift operation.

bSetCheck(n, pos)

Checks if the bit at the given position is set to 1.

Parameters:

n : `int` - The integer to check.

pos : `int` - The position of the bit to check.

Returns: `bool` - True if the bit is set to 1, False otherwise.

bClear(n, pos)

Clears a particular bit of an integer (changes from 1 to 0) passes if bit at pos is 0.

Parameters:

n : `int` - The integer to clear a bit from.

pos : `int` - The zero-based index of the bit to clear.

Returns: `int` - The result of clearing the specified bit.

bFlip0s(n)

Flips all 0 bits in the number to 1.

Parameters:

n : `int` - The integer to flip the bits of.

Returns: `int` - The result of flipping all 0 bits in the number.

bFlip1s(n)

Flips all 1 bits in the number to 0.

Parameters:

n : `int` - The integer to flip the bits of.

Returns: `int` - The result of flipping all 1 bits in the number.

bFlipAll(n)

Flips all bits in the number.

Parameters:

n : `int` - The integer to flip the bits of.

Returns: `int` - The result of flipping all bits in the number.

bSet(n, pos, newBit)

Changes the value of the bit at the given position.

Parameters:

n : `int` - The integer to modify.

pos : `int` - The position of the bit to change.

newBit : `int` - na = flips bit at pos reguardless 1 or 0 | The new value of the bit (0 or 1).

Returns: `int` - The modified integer.

changeDigit(n, pos, newDigit)

Changes the value of the digit at the given position.

Parameters:

n : `int` - The integer to modify.

pos : `int` - The position of the digit to change.

newDigit : `int` - The new value of the digit (0-9).

Returns: `int` - The modified integer.

bSwap(n, i, j)

Switch the position of 2 bits of an int

Parameters:

n : `int` - int to manipulate

i : `int` - bit pos to switch with j

j : `int` - bit pos to switch with i

Returns: `int` - new int with bits switched

bPalindrome(n)

Checks to see if the binary form is a Palindrome (reads the same left to right and vice versa)

Parameters:

n : `int` - int to check

Returns: `bool` - result of check

bEven(n)

Checks if n is Even

Parameters:

n : `int` - The integer to check.

Returns: `bool` - result.

bOdd(n)

checks if n is Even if not even Odd

Parameters:

n : `int` - The integer to check.

Returns: `bool` - result.

bPowerOfTwo(n)

Checks if n is a Power of 2.

Parameters:

n : `int` - number to check.

Returns: `bool` - result.

bCount(n, to_count)

Counts the number of bits that are equal to 1 in an integer.

Parameters:

n : `int` - The integer to count the bits in.

to_count `string` - the bits to count

Returns: `int` - The number of bits that are equal to 1 in n.

GCD(a, b)

Finds the greatest common divisor (GCD) of two numbers.

Parameters:

a : `int` - The first number.

b : `int` - The second number.

Returns: `int` - The GCD of a and b.

LCM(a, b)

Finds the least common multiple (LCM) of two integers.

Parameters:

a : `int` - The first integer.

b : `int` - The second integer.

Returns: `int` - The LCM of a and b.

aLCM(nums)

Finds the LCM of an array of integers.

Parameters:

nums : `int ` - The list of integers.

Returns: `int` - The LCM of the integers in nums.

adjustedLCM(nums, LCM)

adjust an array of integers to Least Common Multiple (LCM)

Parameters:

nums : `int ` - The first integer

LCM : `int` - The second integer

Returns: `int ` - array of ints with LCM

charAt(str, pos)

gets a Char at a given position.

Parameters:

str : `string` - string to pull char from.

pos : `int` - pos to get char from string (left to right index).

Returns: `string` - char from pos of string or "" if pos is not within index range

decimalToBinary(num)

Converts a decimal number to binary

Parameters:

num : `int` - The decimal number to convert to binary

Returns: `string` - The binary representation of the decimal number

decimalToBinary(num, to_binary_int)

Converts a decimal number to binary

Parameters:

num : `int` - The decimal number to convert to binary

to_binary_int : `bool` - bool to convert to int or to string (true for int, false for string)

Returns: `string` - The binary representation of the decimal number

binaryToDecimal(binary)

Converts a binary number to decimal

Parameters:

binary : `string` - The binary number to convert to decimal

Returns: `int` - The decimal representation of the binary number

decimal_len(n)

way of finding decimal length using arithmetic

Parameters:

n `float` - floating decimal point to get length of.

Returns: `int` - number of decimal places

int_len(n)

way of finding number length using arithmetic

Parameters:

n : `int`- value to find length of number

Returns: `int` - lenth of nunber i.e. 23 == 2

float_decimal_to_whole(n)

Converts a float decimal number to an integer `0.365 to 365`.

Parameters:

n : `string` - The decimal number represented as a string.

Returns: `int` - The integer obtained by removing the decimal point and leading zeroes from s.

fractional_part(x)

Returns the fractional part of a float.

Parameters:

x : `float` - The float to get the fractional part of.

Returns: `float` - The fractional part of the float.

form_decimal(a, b, zero_fix)

helper to form 2 ints into 1 float seperated by the decimal

Parameters:

a : `int` - a int

b : `int` - b int

zero_fix : `bool` - fix for trailing zeros being truncated when converting to float

Returns: ` ` - float = float decimal of ints | string = string version of b for future use to ref length

bEncode(n1, n2)

Encodes two numbers into one using bit OR. (fastest)

Parameters:

n1 : `int` - The first number to Encodes.

n2 : `int` - The second number to Encodes.

Returns: `int` - The result of combining the two numbers using bit OR.

bDecode(n)

Decodes an integer created by the bCombine function.(fastest)

Parameters:

n : `int` - The integer to decode.

Returns: ` ` - A tuple containing the two decoded components of the integer.

Encode(a, b)

Encodes by seperating ints into left and right of decimal float

Parameters:

a : `int` - a int

b : `int` - b int

Returns: `float` - new float of encoded ints one on left of decimal point one on right

Decode(encoded)

Decodes float of 2 ints seperated by decimal point

Parameters:

encoded : `float` - the encoded float value

Returns: ` ` - tuple of the 2 ints from encoded float

encode_heavy(a, b)

Encodes by combining numbers and tracking size in the

decimal of a floating number (slowest)

Parameters:

a : `int` - a int

b : `int` - b int

Returns: `float` - new decimal of encoded ints

decode_heavy(encoded)

Decodes encoded float that tracks size of ints in float decimal

Parameters:

encoded : `float` - encoded float

Returns: ` ` - tuple of decoded ints

decimal of float (slowest)

Parameters:

encoded : `float` - the encoded float value

Returns: ` ` - tuple of the 2 ints from encoded float

Bitwise, Encode, Decode Docs

In the documentation you may notice the word decimal

not used as normal this is because when referring to

binary a decimal number is a number that

can be represented with base 10 numbers 0-9

(the wiki below explains better)

A rule of thumb for the two integers being

encoded it to keep both numbers

less than 65535 this is because anything lower uses 16 bits or less

this will maintain 100% accuracy when decoding

although it is possible to do numbers up to 2147483645 with

this library doesnt seem useful enough

to explain or demonstrate.

The functions provided work within this 32-bit range,

where the highest number is all 1s and

the lowest number is all 0s. These functions were created

to overcome the lack of built-in bitwise functions in Pinescript.

By combining two integers into a single number,

the code can access both values i.e when

indexing only one array index

for a matrices row/column, thus improving execution time.

This technique can be applied to various coding

scenarios to enhance performance.

Bitwise functions are a way to use integers in binary form

that can be used to speed up several different processes

most languages have operators to perform these function such as

`<<, >>, &, ^, |, ~`

en.wikipedia.org

Spot vs Derivative PremiumDifference between spot and derivative prices. With this indicator you can get an idea on how strong the market is.

Turtle Trading Risk Adjusted Position Size CalculatorTurtle Trading Risk Adjusted Position Size Calculator

Hello Traders !

Turtle Trading Risk Adjustment Calculator (inspired by the Turtle Traders Position sizing methods) aims to objectively help day traders allocate the appropriate position size per trade by scaling different instruments by their risk, as measured by their volatility via the ATR (default - Average of 14 period True Range). By doing so This volatility-based position sizing method normalizes risk across different asset classes.

Understanding The formula

Formula U normalizes positions sizes among any non FX asset, by representing a standard unit of risk as a fraction of volatility adjusted by a risk coefficient (note higher risk coeff values (high uncertainty) will lead to lower trade capital allocation i.e lower position size - Varying the risk coefficient is relevant in expressing uncertainty) and scaled to ones trading account size relative to 1 contract of the asset to be traded, This is referred to as the Dollar volatility, formula D.

Dollar volatility is a bit confusing but in essence it is simply a factor of the asset price such that quantity sums to ones Trading account balance or how many times larger ones trading account is than the assets current market price, or more formally The amount of value a $1 change in the contract would impact your trading account given you are current trading all you account equity.

Formula TVPP is my own adaptation of the Turtle Trading Position Sizing formulas and the standard value per pip formula adjusted for volatility, this iteration has the same logic as stated above although the formulas vary.

Hope this is Useful, Wishing you Luck in your Trading Journey - u got this !!

Futures/Spot Ratiowhat is Futures /Spot Ratio?

Although futures and spot markets are separate markets, they are correlated. arbitrage bots allow this gap to be closed. But arbitrage bots also have their limits. so there are always slight differences between futures and spot markets. By analyzing these differences, the movements of the players in the market can be interpreted and important information about the price can be obtained. Futures /Spot Ratio is a tool that facilitates this analysis.

what it does?

it compresses the ratio between two selected spot and futures trading pairs between 0 and 100. its purpose is to facilitate use and interpretation. it also passes a regression (Colorful Regression) through the middle of the data for the same purpose.

about Colorful Regression:

how it does it?

it uses this formula:

how to use it?

use it to understand whether the market is priced with spot trades or leveraged positions. A value of 50 is the breakeven point where the ratio of the spot and leveraged markets are equal. Values above 50 indicate excess of long positions in the market, values below 50 indicate excess of short positions. I have explained how to interpret these ratios with examples below.

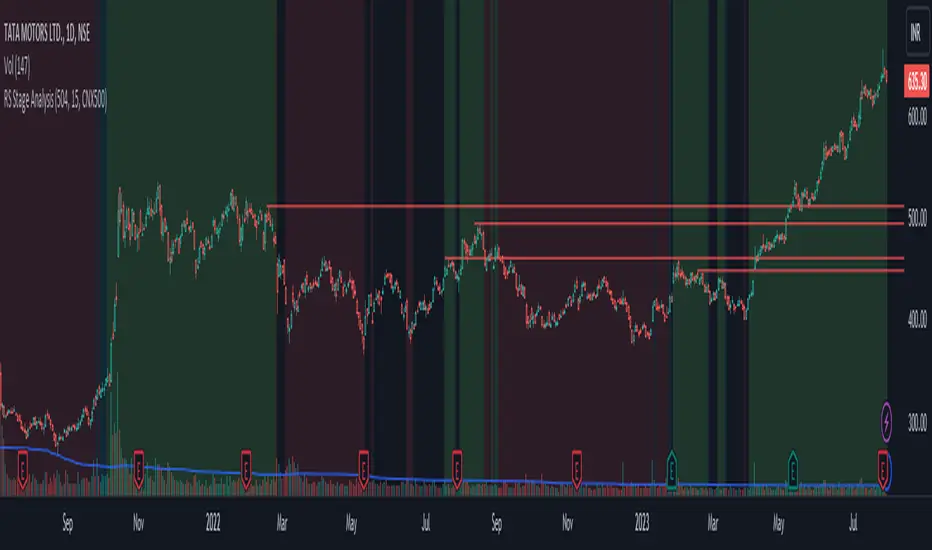

RS Stage AnalysisThis script trying to detect different lifecycle of stock / Stages.

There is mainly 4 stages of stocks.

1) stage 1 - Accumulation = color = aqua

2) stage 2 - Advancing = color = green

3) stage 3 - Distribution = color = yellow

4) stage 4 - Declining = color = red

At some point the condition i wrote wont detect any stage.

XLY/XLP RatioThe XLY/XLP ratio is a financial indicator that measures the ratio between the two ETFs (Exchange Traded Funds) Consumer Discretionary Select Sector SPDR Fund (XLY) and Consumer Staples Select Sector SPDR Fund (XLP). This ratio is often used by traders and investors as a measure of the relative success of companies in the consumer goods and consumer services sectors.

A higher XLY/XLP ratio indicates that consumer confidence is higher and people are more willing to spend their money on non-essential items, such as entertainment or luxury goods (discretionary spending). A lower XLY/XLP ratio, on the other hand, indicates that consumer confidence is lower and people are more willing to spend their money on essential items like food and household items (staple spending).

The interpretation of the XLY/XLP ratio depends on the current market situation and the analysis of the economic and political factors that may influence consumption. If the XLY/XLP ratio rises, it could be an indication of a growing economy and increasing consumer sentiment. However, if it falls, it could be an indication of a weakening economy or declining consumer confidence.

It is important to note that the XLY/XLP indicator should not be used as the sole indicator to make trading decisions. It is advisable to also consider other indicators, such as technical and fundamental analysis, before making a decision.

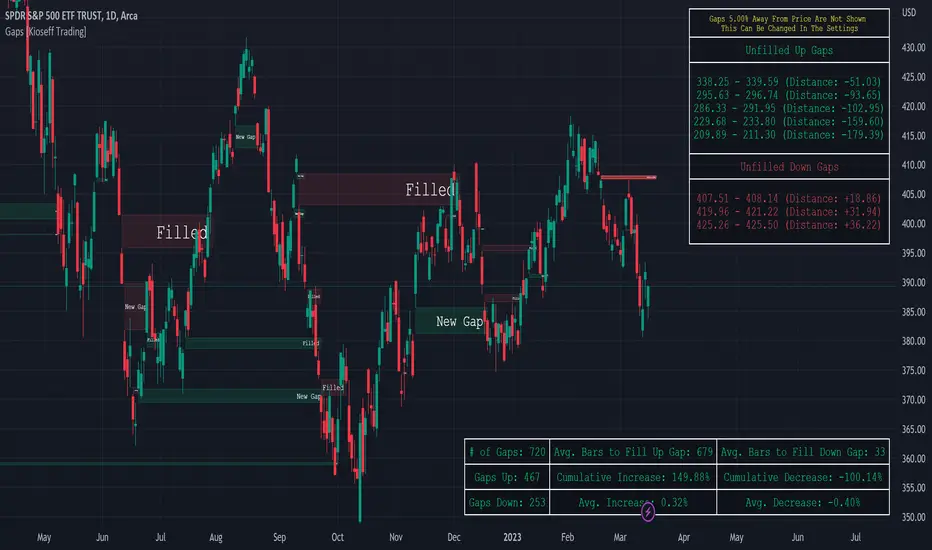

Gaps [Kioseff Trading]Hello!

This script "Gaps" is a continuation and improvement on a subset indicator included in the "Quartile Volume; Volume Aggregation; US Range Bars; Gaps)" script!

As advised by @thebearfib, the "Gaps" indicator is now standalone!

Features

Stat: Avg. Bars to Fill Up Gap

Stat: Avg. Bars to Fill Down Gap

Stat: Cumulative Up Gap % Increase

Stat: Cumulative Down Gap % Increase

Stat: Avg Up Gap % Increase

Stat: Avg Down Gap % Decrease

Nearest Unfilled Up Gaps and Down Gaps Displayed in Table

% Price Move Requirement, Including Dollar Amount, for Nearest Unfilled Gaps to Fill

Gaps Marked on Chart, Including Partially Filled Gaps and The % Amount a Partially Filled Gap Has Been Violated

Gaps Chart

The image above shows the data tables included in the indicator!

Settings

The image above shows various settings for the indicator!

The image above shows how partially filled gaps are marked using the default settings.

Exceeded price areas are shaded darker; however, by selecting the "No Partially Filled Gaps" option, the indicator will treat partially filled gaps differently.

The image above shows alternative behavior! Instead of the gap changing color it narrows in size.

The image above shows the indicator's behavior when selecting to show gap data in labels.

Therefore, when a gap is small and the box text is imperceptible, you can select to show the data in a label.

Additionally, you can select to display a "Gaps Chart".

The image above shows this feature enabled. The gaps chart shows the sequence of price gaps for the asset as candlesticks.

Thank you for checking this out; if you'd like other features included please let me know!

Highest/Lowest value since X time ago, various indicatorsThis script will count the bars back since the last time the current bar indicator value was either this low or this high.

It will provide the time in either, seconds, minutes, hours, days, weeks, months, or years.

please note:

There are currently no alerts setup for this script.

the length options only apply to the sources that have the "(MA)" in their name.

There is a horizontal line display issue which corrects once you adjust the amount of sources you want to use.

Once you select the amount of sources you would like to use, align the indicator so the horizontal lines match up with the table lines.

If find any bugs in the script, let me know.

Price Data LabelThis indicator gives you the ability to see historical data for each bar on the chart by simply hovering over the high of the bar, similar to the functionality of MarketSmith.

Data for each bar includes:

Open

High

Low

Close + Change

Percentage Change

Closing Range

Volume

Volume Percent based on 50 day average

Distance to 4 selectable moving averages

Example of stats on a historical bar:

* Note this only works on the last 500 historical bars. If you use bar replay it will work with 500 historical bars from the last bar.

* If you have multiple indicators on your chart, in order to see the data you will need to use visual order to bring to front. This can be done by clicking the three dots next to the indicator name and selecting visual order.

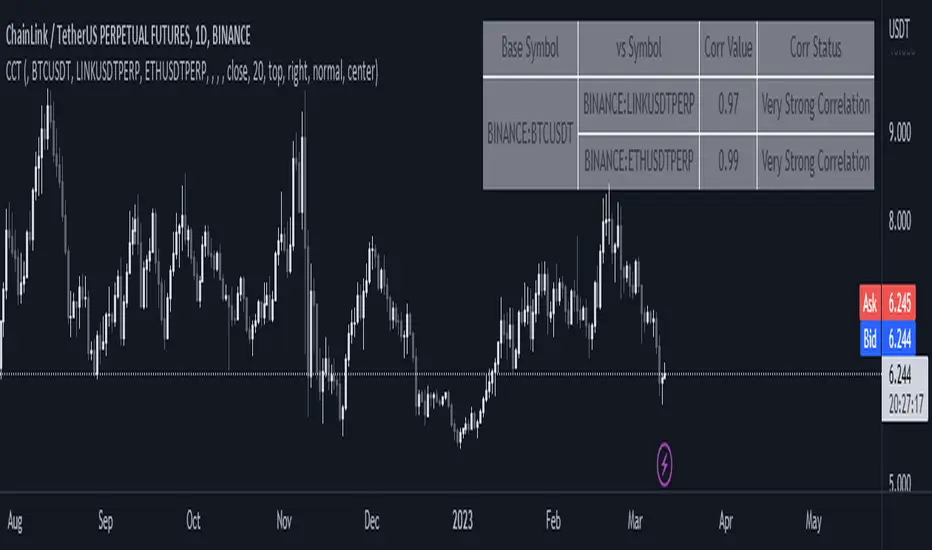

Correlation Coefficient TableThis is a sample PineSript code implementation using Correlation Coefficient. It uses the ta.correlation library of Pinescript and calculates the correlation based on user input length. The results are then plotted on a table. The corr value displays the actual correlation coefficient value while the Corr Status displays the interpretation of the correlation coefficient values.

The script takes the following input

Source Symbol - This is the base symbol which will be used in calculating correlation coefficient. In my case, since i am looking more often on crypto. I defaulted it to BTCUSDT

Symbol 1 - Symbol 5 - These are the coins that will be compared to our base symbol for correlation.

Source - You can select on which price source you want to be calculated. By default this is set to candle close price.

Length - The number of price bar to look back and retrieve correlation coefficient. Set to 20 bars by default.

Table Settings - Since the correlation coefficient are displayed on a table. An option to customize the table settings are presented.

The Correlation Status column was based on this Interpretation:

For more information, read this article www.tradingview.com

Global (World) Monetary Supply M2 (measured in USD)This is the Global Monetary Supply M2 of the richest and most populous countries that have info from at least 2008

It is measured in USD (converting the M2 of each of the countries respective currencies and virtually converting them into USD)

This is less than the global liquidity as it does not include the countries' assets in other currencies (on their balance sheets), it only focuses on the monetary supply of each of the countries own currencies.

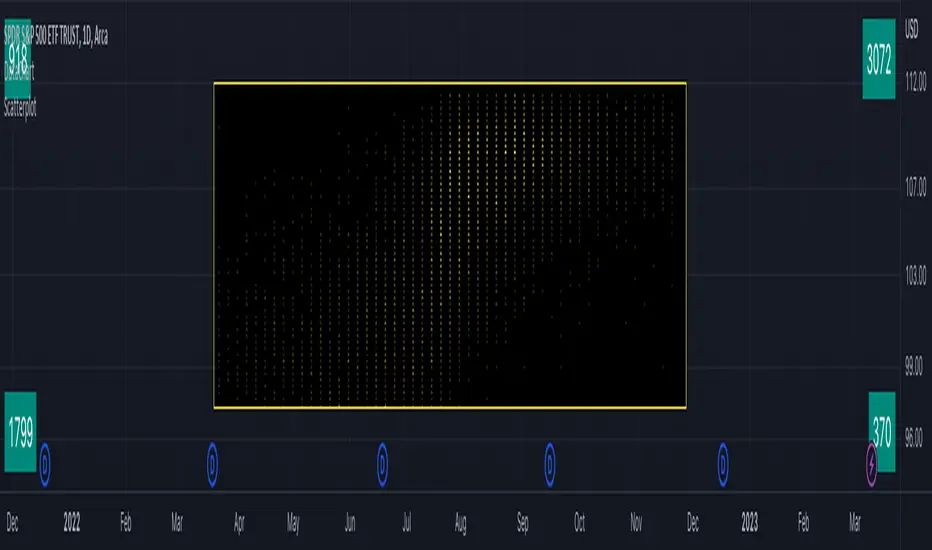

DataChartLibrary "DataChart"

Library to plot scatterplot or heatmaps for your own set of data samples

draw(this)

draw contents of the chart object

Parameters:

this : Chart object

Returns: current chart object

init(this)

Initialize Chart object.

Parameters:

this : Chart object to be initialized

Returns: current chart object

addSample(this, sample, trigger)

Add sample data to chart using Sample object

Parameters:

this : Chart object

sample : Sample object containing sample x and y values to be plotted

trigger : Samples are added to chart only if trigger is set to true. Default value is true

Returns: current chart object

addSample(this, x, y, trigger)

Add sample data to chart using x and y values

Parameters:

this : Chart object

x : x value of sample data

y : y value of sample data

trigger : Samples are added to chart only if trigger is set to true. Default value is true

Returns: current chart object

addPriceSample(this, priceSampleData, config)

Add price sample data - special type of sample designed to measure price displacements of events

Parameters:

this : Chart object

priceSampleData : PriceSampleData object containing event driven displacement data of x and y

config : PriceSampleConfig object containing configurations for deriving x and y from priceSampleData

Returns: current chart object

Sample

Sample data for chart

Fields:

xValue : x value of the sample data

yValue : y value of the sample data

ChartProperties

Properties of plotting chart

Fields:

title : Title of the chart

suffix : Suffix for values. It can be used to reference 10X or 4% etc. Used only if format is not format.percent

matrixSize : size of the matrix used for plotting

chartType : Can be either scatterplot or heatmap. Default is scatterplot

outliersStart : Indicates the percentile of data to filter out from the starting point to get rid of outliers

outliersEnd : Indicates the percentile of data to filter out from the ending point to get rid of outliers.

backgroundColor

plotColor : color of plots on the chart. Default is color.yellow. Only used for scatterplot type

heatmapColor : color of heatmaps on the chart. Default is color.red. Only used for heatmap type

borderColor : border color of the chart table. Default is color.yellow.

plotSize : size of scatter plots. Default is size.large

format : data representation format in tooltips. Use mintick.percent if measuring any data in terms of percent. Else, use format.mintick

showCounters : display counters which shows totals on each quadrants. These are single cell tables at the corners displaying number of occurences on each quadrant.

showTitle : display title at the top center. Uses the title string set in the properties

counterBackground : background color of counter table cells. Default is color.teal

counterTextColor : text color of counter table cells. Default is color.white

counterTextSize : size of counter table cells. Default is size.large

titleBackground : background color of chart title. Default is color.maroon

titleTextColor : text color of the chart title. Default is color.white

titleTextSize : text size of the title cell. Default is size.large

addOutliersToBorder : If set, instead of removing the outliers, it will be added to the border cells.

useCommonScale : Use common scale for both x and y. If not selected, different scales are calculated based on range of x and y values from samples. Default is set to false.

plotchar : scatter plot character. Default is set to ascii bullet.

ChartDrawing

Chart drawing objects collection

Fields:

properties : ChartProperties object which determines the type and characteristics of chart being plotted

titleTable : table containing title of the chart.

mainTable : table containing plots or heatmaps.

quadrantTables : Array of tables containing counters of all 4 quandrants

Chart

Chart type which contains all the information of chart being plotted

Fields:

properties : ChartProperties object which determines the type and characteristics of chart being plotted

samples : Array of Sample objects collected over period of time for plotting on chart.

displacements : Array containing displacement values. Both x and y values

displacementX : Array containing only X displacement values.

displacementY : Array containing only Y displacement values.

drawing : ChartDrawing object which contains all the drawing elements

PriceSampleConfig

Configs used for adding specific type of samples called PriceSamples

Fields:

duration : impact duration for which price displacement samples are calculated.

useAtrReference : Default is true. If set to true, price is measured in terms of Atr. Else is measured in terms of percentage of price.

atrLength : atrLength to be used for measuring the price based on ATR. Used only if useAtrReference is set to true.

PriceSampleData

Special type of sample called price sample. Can be used instead of basic Sample type

Fields:

trigger : consider sample only if trigger is set to true. Default is true.

source : Price source. Default is close

highSource : High price source. Default is high

lowSource : Low price source. Default is low

tr : True range value. Default is ta.tr

Global Monetary Supply M2 Vs the Global GDP This indicator compares the Global (world) Monetary Supply (measured in USD) compared to the Global GDP.

This can be useful to measure the "money printing speed" of the world compare to the "world gdp growth", the higher the slope (angle of growth) the more money printing.

It includes the exact same countries of the Global M2 indicator (done by me), to make fair the comparison, which has the richest and most populous countries so to have a clear overview.

There tough a few very populated countries excluded, the details can be found on the Global M2 indicator script and reason for exclusion.

Enjoy!

Feature ScalingLibrary "Feature_Scaling"

FS: This library helps you scale your data to certain ranges or standarize, normalize, unit scale or min-max scale your data in your prefered way. Mostly used for normalization purposes.

minmaxscale(source, min, max, length)

minmaxscale: Min-max normalization scales your data to set minimum and maximum range

Parameters:

source

min

max

length

Returns: res: Data scaled to the set minimum and maximum range

meanscale(source, length)

meanscale: Mean normalization of your data

Parameters:

source

length

Returns: res: Mean normalization result of the source

standarize(source, length, biased)

standarize: Standarization of your data

Parameters:

source

length

biased

Returns: res: Standarized data

unitlength(source, length)

unitlength: Scales your data into overall unit length

Parameters:

source

length

Returns: res: Your data scaled to the unit length