Market Relative Candle Ratio ComparatorIntroducing the Market Relative Candle Ratio Comparator, a visually captivating script that eases the way you compare two financial assets, such as cryptocurrencies and market indices. Leveraging a distinctive calculation method based on percentage changes and their averages, this tool presents a crystal-clear view of how your chosen assets perform in relation to each other, both for individual candles and over a range of previous candles.

Tailoring the script to your preferences is a walk in the park, as it allows you to easily adjust input symbols, moving average lengths, and other parameters to match your analytical approach. The visually arresting column chart it creates employs vivid red and green colors to underscore the differences between the two assets on each candle. Simultaneously, the lower-opacity columns depict the accumulated differences over a specified lookback period. This vibrant blend of colors and opacities results in a dynamic visual experience, enabling you to better grasp market trends relative to each other.

The reverse bool input is a handy feature that lets you invert the effect of the input symbol (DXY by default) in the comparison. When you set the reverse input to true, the script multiplies the calculated DXY percentage change by -1, effectively reversing the comparison. This is particularly useful when examining assets with an inverse relationship or when you'd like to analyze the input symbol's impact in the opposite direction.

For instance, if the input symbol represents a market index that generally moves in the opposite direction of the selected cryptocurrency, enabling the reverse input will help you better visualize and understand the relationship between the two assets by inverting the input symbol's effect on the comparison.

In the accompanying chart, you can observe the comparison of Bitcoin's movement relative to the Dollar, Gold, Bonds, and the S&P 500. The indicator reveals that in the last day, Bitcoin outperformed Bonds, Gold, and the Dollar but not the S&P 500!

Statistics

Arbitrage SpreadThis indicator helps to find spreads between cryptocurrencies, assess their correlation, spread, z score and atr z score.

The graphs are plotted as a percentage. Because of the limitation in pine tradingview for 5000 bars a period was introduced (after which a new starting point of the graph construction will be started), if you want it can be disabled

The multiplier parameter affects only the construction of the joint diagram on which z score and atr z score are calculated (construction of the diagram is done by dividing one pair by another and multiplying by the multiplier parameter) is shown with a red line

To create a notification you have to specify the data for parameters other than zero which you want to monitor. For parameters z score and atr z score data are counted in both directions

The data can be tracked via the data window

Link to image of the data window prnt.sc

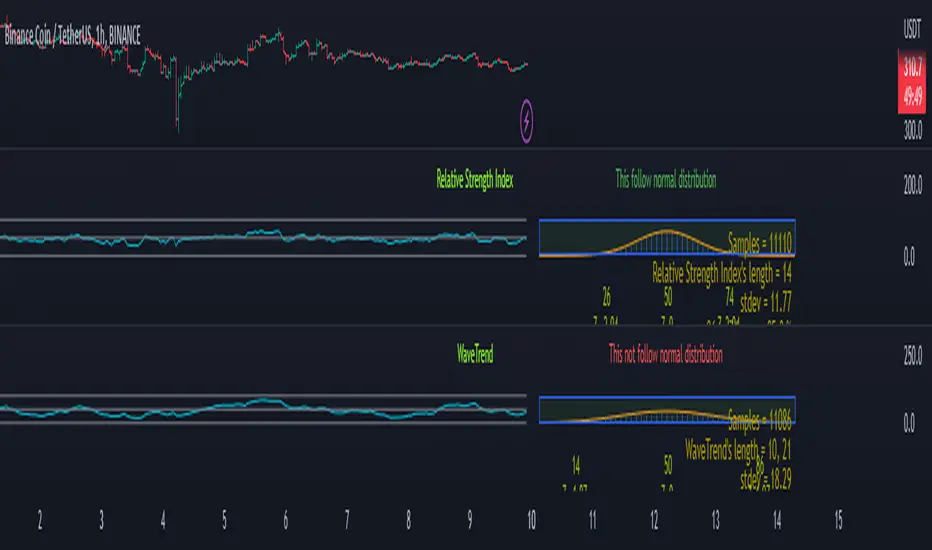

Oscillator: Which follows Normal Distribution?When doing machine learning using oscillators, it would be better if the oscillators were normally distributed.

So I analyzed the distribution of oscillators.

The value of the oscillator was divided into 50 groups each from 0 to 100.

ex) if rsi value is 45.43 -> group_44, 58.23 -> group_58

Ocscillators : RSI, Stoch, MFI, WT, RVI, etc....

Caution: The normal distribution was verified through an empirical formula.

[MiV] MA Screener v1.0In my trading I stick to the following strategy: I buy an asset above the 100/200 moving average and then sell it.

The most problematic thing in all this is to look for assets that are above the 100 or 200 moving average, and to assess how "far" the price is from that moving average.

In fact, to solve this problem I created this indicator.

It works with 30 different assets and displays the state of its two moving averages, whether the price is higher or not, and how much higher the price is from that level.

Multiple Moving Average ToolkitFeatures Overview:

Multiple Moving Averages: The script allows you to plot up to five different Moving Averages (MAs) on your chart at the same time. You can choose the type of MA (EMA, SMA, HMA, WMA, DEMA, VWMA, VWAP) and the length of each one.

Color Ribbon: You can turn the MAs into a color ribbon by selecting the "Turn into Color Ribbon?" option. This will make the area between the MAs colored and can help you identify trends more easily.

MA Value Table: You can draw a table on your chart that displays the current values of each MA, whether the trend is bullish or bearish along with the length of the MAs. The current ATR value is also shown in the last cell of the table. You can choose the location of the table (Top Left, Top Right, Bottom Left, Bottom Right) and the transparency of the background color.

Crosses: The script can detect when two MAs cross over each other (1st MA crosses 5th MA and vice versa), indicating a potential trend reversal. It will plot crosses on the chart at the point of the crossover and give an alert if the "Bullish Cross Detected" or "Bearish Cross Detected" condition is met.

How to use:

Once the script is added to your chart, you can customize the settings to fit your preferences. You can choose the type and length of each MA, whether to turn them into a color ribbon, whether to plot crosses, and whether to draw the MA Value Table.

The MA Value Table can be moved to a different location on the chart by selecting the "Location of Table" option and choosing Top Left, Top Right, Bottom Left, or Bottom Right.

Watch for MA crossovers and alerts to identify potential trend reversals. The script can help you identify bullish and bearish trends by color-coding the area between the MAs and displaying the current values of each MA in the table.

Breakdown of the script:

User Inputs

The first section of the script defines several user inputs that allows you to customize the indicator. These include options for turning the MAs into a color ribbon, plotting crosses when there is a bullish or bearish cross of the MAs, drawing a table of the MA values, and setting the transparency of the ribbon. You can also select the location of the MA value table and customize the settings for each individual MA.

Moving Average Calculation

The script defines a function called "getMA" that calculates the moving average for a given type and length. The function uses a switch statement to determine which type of moving average to use, such as an exponential moving average (EMA), simple moving average (SMA), Hull moving average (HMA), weighted moving average (WMA), double exponential moving average (DEMA), volume-weighted moving average (VWMA), or volume-weighted average price (VWAP).

The script then calls this function to calculate the values of up to five different MAs, depending on the user input. The ATR (average true range) is also calculated using the TA library.

Color Filter and Cross Detection

The script sets a color filter based on the relationship between the MAs. If the shorter-term MAs are above the longer-term MAs, the filter is set to green to indicate a bullish trend, and if the shorter-term MAs are below the longer-term MAs, the filter is set to red to indicate a bearish trend. You can adjust the transparency of the ribbon to make it more or less visible.

The script also detects when there is a bullish or bearish cross of the MAs and can generate alerts to notify you.

MA Plotting

The script plots up to five MAs on the chart, depending on the user input. The MAs are plotted as lines with different colors and thicknesses, and you can choose to turn them into a color ribbon if desired.

Cross Plotting

The script plots crosses on the chart when there is a bullish or bearish cross of the MAs. The crosses are plotted as X shapes at the location of the cross and are color-coded to indicate the direction of the cross.

MA Value Table

Finally, the script draws a table of the MA values on the chart, displaying the values of each MA as well as the current trend and the ATR. You can customize the location of the table, and the table is colored to match the color filter of the MAs.

Feel free to message me or comment on the post with any questions or issues!

Much more to come!

Thanks for reading, enjoy!

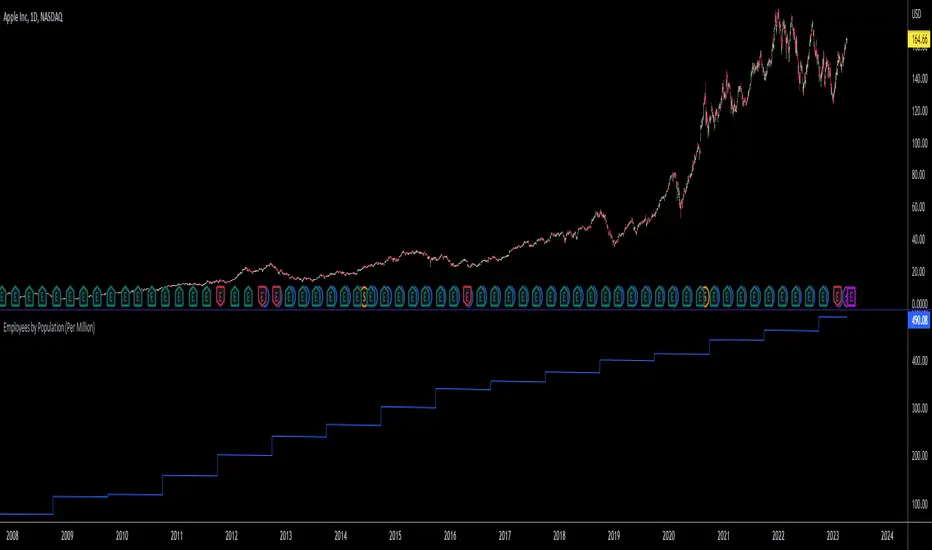

Employees by Population (Per Million)This script measures the number of employees a company has per million people in the US population, either by total or employed population.

*Backtesting System ⚉ OVERVIEW ⚉

One of the best Systems for Backtesting your Strategies.

Incredibly flexible, simple, fast and feature-rich system — will solve most of your queries without much effort.

Many systems for setting StopLoss, TakeProfit, Risk Management and advanced Filters.

All you need to do is plug in your indicator and start Backtesting .

I intentionally left the option to use my System on Full Power before you load your indicator into it.

The system uses the built-in simple and popular moving average crossover signal for this purpose. (EMA 50 & 200).

Also Highly Recommend that you Fully use ALL of the features of this system so that you understand how they work before you ask questions.

Also tried to leave TIPS for each feature everywhere, read Tips, activate them and see how they work.

But before you use this system, I Recommend you to read the following description in Full.

—————— How to connect your indicator in 2 steps:

Adapt your indicator by adding only 2 lines of code and then connect it to this Backtesting System.

Step 1 — Create your connector, For doing so:

• 1 — Find or create in your indicator where are the conditions printing the Long-Buy and Short-Sell signals.

• 2 — Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator wether it's a MACD, RSI , Pivots, or whatever indicator with Clear Buy and Sell conditions.

//@version=5

indicator('Moving Average Cross', overlay = true)

MA200 = ta.𝚎𝚖𝚊(close, 200)

MA50 = ta.𝚎𝚖𝚊(close, 50)

// Generate Buy and Sell conditions

buy = ta.crossover (MA200, MA50)

sell = ta.crossunder (MA200, MA50)

plot(MA200, color=color.green)

plot(MA50 , color=color.red )

bgcolor(color = buy ? color.green : sell ? color.red : na, title='SIGNALS')

// ———————————————— SIGNAL FOR SYSTEM ————————————————

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, title='🔌Connector🔌', display = display.none)

// —————— 🔥 The Backtesting System expects the value to be exactly +1 for the 𝚋𝚞𝚕𝚕𝚒𝚜𝚑 signal, and -1 for the 𝚋𝚎𝚊𝚛𝚒𝚜𝚑 signal

Basically, I identified my Buy & Sell conditions in the code and added this at the bottom of my indicator code

Now you can connect your indicator to the Backtesting System using the Step 2

Step 2 — Connect the connector

• 1 — Add your updated indicator to a TradingView chart and Add the Backtesting System as well to the SAME chart

• 2 — Open the Backtesting System settings and in the External Source field select your 🔌Connector🔌 (which comes from your indicator)

_______________________________

⚉ MAIN SETTINGS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

𝐄𝐱𝐭𝐞𝐫𝐧𝐚𝐥 𝐒𝐨𝐮𝐫𝐜𝐞 — Select your indicator. Add your indicator by following the 2 steps described above and select it in the menu. To familiarize yourself with the system until you select your indicator, you will have an in-built strategy of crossing the two moving EMA's of 50 and 200.

Long Deals — Enable/Disable Long Deals.

Short Deals — Enable/Disable Short Deals.

Wait End Deal — Enable/Disable waiting for a trade to close at Stop Loss/Take Profit. Until the trade closes on the Stop Loss or Take Profit, no new trade will open.

Reverse Deals — To force the opening of a trade in the opposite direction.

ReEntry Deal — Automatically open the same new deal after the deal is closed.

ReOpen Deal — Reopen the trade if the same signal is received. For example, if you are already in the long and a new signal is received in the long, the trade will reopen. * Does not work if Wait End Deal is enabled.

𝐓𝐚𝐤𝐞 𝐏𝐫𝐨𝐟𝐢𝐭:

None — Disables take profit. Useful if you only want to use dynamic stoplosses such as MA, Fast-Trailing, ATR Trail.

FIXED % — Fixed take profit in percent.

FIXED $ — Fixed Take in Money.

ATR — Fixed Take based on ATR.

R:R — Fixed Take based on the size of your stop loss. For example, if your stop is 10% and R:R=1, then the Take would be 10%. R:R=3 Take would be 30%, etc.

HH / LL — Fixed Take based on the previous maximum/minimum (extremum).

𝐒𝐭𝐨𝐩 𝐋𝐨𝐬𝐬:

None — Disables Stop Loss. Useful if you want to work without a stop loss. *Be careful if Wait End Deal is enabled, the trade may not close for a long time until it reaches the Take.

FIXED % — Fixed Stop in percent.

FIXED $ — Fixed Stop in Money.

TRAILING — Dynamic Trailing Stop like on the stock exchanges.

FAST TRAIL — Dynamic Fast Trailing Stop moves immediately in profit and stays in place if the price stands still or the price moves in loss.

ATR — Fixed Stop based on the ATR.

ATR TRAIL — Dynamic Trailing Stop based on the ATR.

LO / HI — A Fixed Stop based on the last Maximum/Minimum extemum. Allows you to place a stop just behind or above the low/high candle.

MA — Dynamic Stop based on selected Moving Average. * You will have 8 types of MA (EMA, SMA, HMA, etc.) to choose from, but you can easily add dozens of other MAs, which makes this type of stop incredibly flexible.

Add % — If true, then with the "𝗦𝘁𝗼𝗽 %" parameter you can add percentages to any of the current SL. Can be especially useful when using Stop - 𝗔𝗧𝗥 or 𝗠𝗔 or 𝗟𝗢/𝗛𝗜. For example with 𝗟𝗢/𝗛𝗜 to put a stop for the last High/Low and add 0.5% additional Stoploss.

Fixed R:R — If the stop loss is Dynamic (Trailing or MA) then if R:R true can also be made Dynamic * Use it carefully, the function is experimental.

_________________________________________

⚉ TAKE PROFIT LEVELS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

A unique method of constructing intermediate Take Profit Levels will allow you to select up to 5 intermediate Take Profit Levels and one intermediate Stop Loss.

Intermediate Take Profit Levels are perfectly calculated into 5 equal parts in the form of levels from the entry point to the final Take Profit target.

All you need to do is to choose the necessary levels for fixing and how much you want to fix at each level as a percentage. For example, TP 3 will always be exactly between the entry point and the Take Profit target. And the value of TP 3 = 50 will close 50% of the amount of the remaining size of the position.

Note: all intermediate SL/TP are closed from the remaining position amount and not from the initial position size, as TV does by default.

SL 0 Position — works in the same way as TP 1-5 but it's Stop. With this parameter you can set the position where the intermediate stop will be set.

Breakeven on TP — When activated, it allows you to put the stop loss at Breakeven after the selected TP is reached. For this function to work as it should - you need to activate an intermediate Take. For example, if TP 3 is activated and Breakeven on TP = 3, then after the price reaches this level, the Stop loss will go to Breakeven.

* This function will not work with Dynamic Stoplosses, because it simply does not make sense.

CoolDown # Bars — When activated, allows you to add a delay before a new trade is opened. A new trade after CoolDown will not be opened until # bars pass and a new signal appears.

_____________________________

⚉ TIME FILTERS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

Powerful time filter code that allows you to filter data based on specific time zones, dates, and session days. This code is ideal for those who need to analyze data from different time zones and weed out irrelevant data.

With Time Filter, you can easily set the starting and ending time zones by which you want to filter the data.

You can also set a start and end date for your data and choose which days of the week to include in the analysis. In addition, you can specify start and end times for a specific session, allowing you to focus your analysis on specific time periods.

_________________________________

⚉ SIGNAL FILTERS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

Signal Filters — allows you to easily customize and optimize your trading strategies based on 10 filters.

Each filter is designed to help you weed out inaccurate signals to minimize your risks.

Let's take a look at their features:

__________________________________

⚉ RISK MANAGEMENT ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

Risk management tools that allow you to set the maximum number of losing trades in a row, a limit on the number of trades per day or week and other filters.

Loss Streak — Set Max number of consecutive loss trades.

Win Streak — Max Winning Streak Length.

Row Loss InDay — Max of consecutive days with a loss in a row.

DrawDown % — Max DrawDown (in % of strategy equity).

InDay Loss % — Set Max Intraday Loss.

Daily Trades — Limit the number of MAX trades per day.

Weekly Trades — Limit the number of MAX trades per week.

* 🡅 I would Not Recommend using these functions without understanding how they work.

Order Size — Position Size

• NONE — Use the default position size settings in Tab "Properties".

• EQUITY — The amount of the allowed position as a percentage of the initial capital.

• Use Net Profit — On/Off the use of profit in the following trades. *Only works if the type is EQUITY.

• SIZE — The size of the allowed position in monetary terms.

• Contracts — The size of the allowed position in the contracts. 1 Сontract = Сurrent price.

________________

⚉ NOTES ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

It is important to note that I have never worked with Backtesting and the functions associated with them before.

It took me about a month of slow work to build this system.

I want to say Big Thanks:

• The PineScripters🌲 group, the guys suggested how to implement some features. Especially @allanster

• Thanks to all those people who share their developments for free on TV and not only.

• I also thank myself for not giving up and finishing the project, and not trying to monetize the system by selling it. * Although I really want the money :)

I tried hard to make it as fast and convenient as possible for everyone who will use my code.

That's why I didn't use any libraries and dozens of heavy functions, and I managed to fit in 8+-functions for the whole code.

Absolutely every block of code I tried to make full-fledged modular, that it was easy to import/edit for myself (you).

I have abused the Ternary Pine operator a little (a lot) so that the code was as compact as possible.

Nevertheless, I tried very hard to keep my code very understandable even for beginners.

At last I managed to write 500 lines of code, making it one of the fastest and most feature-rich systems out there.

I hope everyone enjoys my work.

Put comments and write likes.

HarmonicPatternTrackingLibrary "HarmonicPatternTracking"

Library contains few data structures and methods for tracking harmonic pattern trades via pinescript.

method draw(this)

Creates and draws HarmonicDrawing object for given HarmonicPattern

Namespace types: HarmonicPattern

Parameters:

this (HarmonicPattern) : HarmonicPattern object

Returns: current HarmonicPattern object

method addTrade(this)

calculates HarmonicTrade and sets trade object for HarmonicPattern

Namespace types: HarmonicPattern

Parameters:

this (HarmonicPattern) : HarmonicPattern object

Returns: bool true if pattern trades are valid, false otherwise

method delete(this)

Deletes drawing objects of HarmonicDrawing

Namespace types: HarmonicDrawing

Parameters:

this (HarmonicDrawing) : HarmonicDrawing object

Returns: current HarmonicDrawing object

method delete(this)

Deletes drawings of harmonic pattern

Namespace types: HarmonicPattern

Parameters:

this (HarmonicPattern) : HarmonicPattern object

Returns: current HarmonicPattern object

HarmonicDrawing

Drawing objects of Harmonic Pattern

Fields:

xa (series line) : xa line

ab (series line) : ab line

bc (series line) : bc line

cd (series line) : cd line

xb (series line) : xb line

bd (series line) : bd line

ac (series line) : ac line

xd (series line) : xd line

x (series label) : label for pivot x

a (series label) : label for pivot a

b (series label) : label for pivot b

c (series label) : label for pivot c

d (series label) : label for pivot d

xabRatio (series label) : label for XAB Ratio

abcRatio (series label) : label for ABC Ratio

bcdRatio (series label) : label for BCD Ratio

xadRatio (series label) : label for XAD Ratio

HarmonicTrade

Trade tracking parameters of Harmonic Patterns

Fields:

initialEntry (series float) : initial entry when pattern first formed.

entry (series float) : trailed entry price.

initialStop (series float) : initial stop when trade first entered.

stop (series float) : current stop updated as per trailing rules.

target1 (series float) : First target value

target2 (series float) : Second target value

target3 (series float) : Third target value

target4 (series float) : Fourth target value

status (series int) : Trade status referenced as integer

retouch (series bool) : Flag to show if the price retouched after entry

HarmonicProperties

Display and trade calculation properties for Harmonic Patterns

Fields:

fillMajorTriangles (series bool) : Display property used for using linefill for harmonic major triangles

fillMinorTriangles (series bool) : Display property used for using linefill for harmonic minor triangles

majorFillTransparency (series int) : transparency setting for major triangles

minorFillTransparency (series int) : transparency setting for minor triangles

showXABCD (series bool) : Display XABCD pivot labels

lblSizePivots (series string) : Pivot label size

showRatios (series bool) : Display Ratio labels

useLogScaleForScan (series bool) : Use log scale to determine fib ratios for pattern scanning

useLogScaleForTargets (series bool) : Use log scale to determine fib ratios for target calculation

base (series string) : base on which calculation of stop/targets are made.

entryRatio (series float) : fib ratio to calculate entry

stopRatio (series float) : fib ratio to calculate initial stop

target1Ratio (series float) : fib ratio to calculate first target

target2Ratio (series float) : fib ratio to calculate second target

target3Ratio (series float) : fib ratio to calculate third target

target4Ratio (series float) : fib ratio to calculate fourth target

HarmonicPattern

Harmonic pattern object to track entire pattern trade life cycle

Fields:

id (series int) : Pattern Id

dir (series int) : pattern direction

x (series float) : X Pivot

a (series float) : A Pivot

b (series float) : B Pivot

c (series float) : C Pivot

d (series float) : D Pivot

xBar (series int) : Bar index of X Pivot

aBar (series int) : Bar index of A Pivot

bBar (series int) : Bar index of B Pivot

cBar (series int) : Bar index of C Pivot

dBar (series int) : Bar index of D Pivot

przStart (series float) : Start of PRZ range

przEnd (series float) : End of PRZ range

patterns (bool ) : array representing the patterns

patternLabel (series string) : string representation of list of patterns

patternColor (series color) : color assigned to pattern

properties (HarmonicProperties) : HarmonicProperties object containing display and calculation properties

trade (HarmonicTrade) : HarmonicTrade object to track trades

drawing (HarmonicDrawing) : HarmonicDrawing object to manage drawings

Double Candle Trend Counter [theEccentricTrader]█ OVERVIEW

This indicator counts the number of confirmed double candle trend scenarios on any given candlestick chart and displays the statistics in a table, which can be repositioned and resized at the user's discretion.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Upper Candle Trends

• A higher high candle is one that closes with a higher high price than the high price of the preceding candle.

• A lower high candle is one that closes with a lower high price than the high price of the preceding candle.

• A double-top candle is one that closes with a high price that is equal to the high price of the preceding candle.

Lower Candle Trends

• A higher low candle is one that closes with a higher low price than the low price of the preceding candle.

• A lower low candle is one that closes with a lower low price than the low price of the preceding candle.

• A double-bottom candle is one that closes with a low price that is equal to the low price of the preceding candle.

Muti-Part Upper and Lower Candle Trends

• A multi-part higher high trend begins with the formation of a new higher high and continues until a new lower high ends the trend.

• A multi-part lower high trend begins with the formation of a new lower high and continues until a new higher high ends the trend.

• A multi-part higher low trend begins with the formation of a new higher low and continues until a new lower low ends the trend.

• A multi-part lower low trend begins with the formation of a new lower low and continues until a new higher low ends the trend.

Double Candle Trends

• A double uptrend candle trend is formed when a candle closes with both a higher high and a higher low.

• A double downtrend candle trend is formed when a candle closes with both a lower high and a lower low.

Multi-Part Double Candle Trends

• A multi-part double uptrend candle trend begins with the formation of a new double uptrend candle trend and continues until a new lower high or lower low ends the trend.

• A multi-part double downtrend candle trend begins with the formation of a new double downtrend candle trend and continues until a new higher high or higher low ends the trend.

█ FEATURES

Inputs

• Start Date

• End Date

• Position

• Text Size

• Show Plots

Table

The table is colour coded, consists of seven columns and, as many as, thirty-two rows. Blue cells denote the multi-part trend scenarios, green cells denote the corresponding double uptrend candle trend scenarios and red cells denote the corresponding double downtrend candle trend scenarios.

The multi-part double candle trend scenarios are listed in the first column with their corresponding total counts to the right, in the second and fifth columns. The last row in column one, displays the sample period which can be adjusted or hidden via indicator settings.

The third and sixth columns display the double candle trend scenarios as percentages of total 1-part double candle trends. And columns four and seven display the total double candle trend scenarios as percentages of the last, or preceding double candle trend part. For example 4-part double uptrend candle trends as percentages of 3-part double uptrend candle trends.

Plots

I have added plots as a visual aid to the double candle trend scenarios. Green up-arrows, with the number of the trend part, denote double uptrend candle trends. Red down-arrows, with the number of the trend part, denote double downtrend candle trends.

█ HOW TO USE

This indicator is intended for research purposes, strategy development and strategy optimisation. I hope it will be useful in helping to gain a better understanding of the underlying dynamics at play on any given market and timeframe.

It can, for example, give you an idea of whether the current double candle trend will continue or fail, based on the current trend scenario and what has happened in the past under similar circumstances. Such information can be useful when conducting top down analysis across multiple timeframes and making strategic decisions.

What you do with these statistics and how far you decide to take your research is entirely up to you, the possibilities are endless.

█ LIMITATIONS

Some higher timeframe candles on tickers with larger lookbacks such as the DXY , do not actually contain all the open, high, low and close (OHLC) data at the beginning of the chart. Instead, they use the close price for open, high and low prices. So, while we can determine whether the close price is higher or lower than the preceding close price, there is no way of knowing what actually happened intra-bar for these candles. And by default candles that close at the same price as the open price, will be counted as green. You can avoid this problem by utilising the sample period filter.

It is also worth noting that the sample size will be limited to your Trading View subscription plan. Premium users get 20,000 candles worth of data, pro+ and pro users get 10,000, and basic users get 5,000. If upgrading is currently not an option, you can always keep a rolling tally of the statistics in an excel spreadsheet or something of the like.

Statistics: High & Low timings of custom session; 1yr historyGet statistics of the Session High and Session Low timings for any custom session; based on around 1yr of data.

//Purpose:

-To get data on the 'time of day' tendencies of an asset.

-Narrow in on a custom defined session and get statistics on that session.

//Notes:

-Input times are always in New York time (but changing the timezone after setting WILL adust both table stats and background highlight correctly.

-For particularly long sessions, make sure text size is set to 'tiny' (very long vertical table), or adjust table to display horizontally.

-You'll notice most assets show higher readings around NY equities open (9:30am NY time). Other assets will have 'hot-spots' at other times too.

-Timings represent the beginning of a 15m candle. i.e. reading for 15:45 represents a high occurring between 15:45 and 1600.

-Premium users should get 20k bars => around 1year's worth of data on a 15minute chart. Days of history is displayed in the top left corner of the table.

//Limitations

-only designed and working on 15minute timeframe (to gather a full year of meaningful/comparable % stats, need 15minute 'buckets' of time.

-sessions cannot cross through midnight, or start at midnight (00:15 is ok). 00:15 >> 23:45 is the max session length. On BTC, same applies but 01:00 instead of midnight (all in NY time).

-if your session crosses through 'dead time' (e.g. 17:00-18:00 S&P NY time); table will correctly omit these non-existent candles, but it will add on the missing hour before the start time.

//Cautionary note:

-Since markets are not uncommonly in a trending state when your defined session starts or ends, the high/low timings % readings for start and end of session may be misleadingly high. Try to look for unusually high readings that are not at the start/end of your session.

Wheat (ZW1!) 15min chart; Table displayed vertically:

Nasdaq (NQ1!) 15m chart; Table displayed horizontally and with smaller text to view a very long custom session:

Upper and Lower Candle Trend Counter [theEccentricTrader]█ OVERVIEW

This indicator counts the number of confirmed upper and lower candle trend scenarios on any given candlestick chart and displays the statistics in a table, which can be repositioned and resized at the user's discretion.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Upper Candle Trends

• A higher high candle is one that closes with a higher high price than the high price of the preceding candle.

• A lower high candle is one that closes with a lower high price than the high price of the preceding candle.

• A double-top candle is one that closes with a high price that is equal to the high price of the preceding candle.

Lower Candle Trends

• A higher low candle is one that closes with a higher low price than the low price of the preceding candle.

• A lower low candle is one that closes with a lower low price than the low price of the preceding candle.

• A double-bottom candle is one that closes with a low price that is equal to the low price of the preceding candle.

Muti-Part Upper and Lower Candle Trends

• A multi-part higher high trend begins with the formation of a new higher high and continues until a new lower high ends the trend.

• A multi-part lower high trend begins with the formation of a new lower high and continues until a new higher high ends the trend.

• A multi-part higher low trend begins with the formation of a new higher low and continues until a new lower low ends the trend.

• A multi-part lower low trend begins with the formation of a new lower low and continues until a new higher low ends the trend.

█ FEATURES

Inputs

• Start Date

• End Date

• Position

• Text Size

Table

The table is colour coded, consists of seven columns and, as many as, sixty-two rows. Blue cells denote the multi-part trend scenarios, green cells denote the corresponding upper candle trend scenarios and red cells denote the corresponding lower candle trend scenarios.

The multi-part candle trend scenarios are listed in the first column with their corresponding total counts to the right, in the second and fifth columns. The last row in column one, displays the sample period which can be adjusted or hidden via indicator settings.

The third and sixth columns display the candle trend scenarios as percentages of total 1-part candle trends. And columns four and seven display the total candle trend scenarios as percentages of the last, or preceding candle trend part. For example 4-part higher high trends as a percentages of 3-part higher high trends. This offers more insight into what might happen next at any given point in time.

Plots

For a visual aid to this indicator please use in conjunction with my Upper Candle Trends and Lower Candle Trends indicators which can both be found on my profile page under scripts, or in community scripts under the same names.

Green up-arrows, with the number of the trend part, denote higher high trends when above bar and higher low trends when below bar. Red down-arrows, with the number of the trend part, denote lower high trends when above bar and lower low trends when below bar.

█ HOW TO USE

This is intended for research purposes, strategy development and strategy optimisation. I hope it will be useful in helping to gain a better understanding of the underlying dynamics at play on any given market and timeframe.

It can, for example, give you an idea of whether the current upper or lower candle trend will continue or fail, based on the current trend scenario and what has happened in the past under similar circumstances. Such information can be useful when conducting top down analysis across multiple timeframes and making strategic decisions.

What you do with these statistics and how far you decide to take your research is entirely up to you, the possibilities are endless.

█ LIMITATIONS

Some higher timeframe candles on tickers with larger lookbacks such as the DXY , do not actually contain all the open, high, low and close (OHLC) data at the beginning of the chart. Instead, they use the close price for open, high and low prices. So, while we can determine whether the close price is higher or lower than the preceding close price, there is no way of knowing what actually happened intra-bar for these candles. And by default candles that close at the same price as the open price, will be counted as green. You can avoid this problem by utilising the sample period filter.

It is also worth noting that the sample size will be limited to your Trading View subscription plan. Premium users get 20,000 candles worth of data, pro+ and pro users get 10,000, and basic users get 5,000. If upgrading is currently not an option, you can always keep a rolling tally of the statistics in an excel spreadsheet or something of the like.

Double Trend Counter [theEccentricTrader]█ OVERVIEW

This indicator counts the number of confirmed double trend scenarios on any given candlestick chart and displays the statistics in a table, which can be repositioned and resized at the user's discretion.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

Muti-Part Upper and Lower Trends

• A multi-part return line uptrend begins with the formation of a new return line uptrend and continues until a new downtrend ends the trend.

• A multi-part downtrend begins with the formation of a new downtrend and continues until a new return line uptrend ends the trend.

• A multi-part uptrend begins with the formation of a new uptrend and continues until a new return line downtrend ends the trend.

• A multi-part return line downtrend begins with the formation of a new return line downtrend and continues until a new uptrend ends the trend.

Double Trends

• A double uptrend is formed when the current trough price is higher than the preceding trough price and the current peak price is higher than the preceding peak price.

• A double downtrend is formed when the current peak price is lower than the preceding peak price and the current trough price is lower than the preceding trough price.

Muti-Part Double Trends

• A multi-part double uptrend begins with the formation of a new uptrend that proceeds a new return line uptrend, and continues until a new downtrend or return line downtrend ends the trend.

• A multi-part double downtrend begins with the formation of a new downtrend that proceeds a new return line downtrend, and continues until a new uptrend or return line uptrend ends the trend.

█ FEATURES

Inputs

• Start Date

• End Date

• Position

• Text Size

Table

The table is colour coded, consists of seven columns and, as many as, fifteen rows. Blue cells denote the multi-part trend scenarios, green cells denote the corresponding double uptrend scenarios and red cells denote the corresponding double downtrend scenarios.

The double trend scenarios are listed in the first column with their corresponding total counts to the right, in the second and fifth columns. The last row in column one, displays the sample period which can be adjusted or hidden via indicator settings.

The third and sixth columns display the double trend scenarios as percentages of total 1-part double trends. And columns four and seven display the total double trend scenarios as percentages of the last, or preceding double trend part. For example, 4-part double trends as percentages of 3-part double trends and so on.

Plots

For a visual aid to this indicator please use in conjunction with my Double Trends indicator which can be found on my profile page under scripts, or in community scripts under the same name.

Green up-arrows, with the number of the double trend part, denote double uptrends. Red down-arrows, with the number of the double trend part, denote double downtrends.

█ HOW TO USE

This indicator is intended for research purposes, strategy development and strategy optimisation. I hope it will be useful in helping to gain a better understanding of the underlying dynamics at play on any given market and timeframe.

It can, for example, give you an idea of whether the current double trend will continue or fail, based on the current double trend scenario and what has happened in the past under similar circumstances. Such information can be very useful when conducting top down analysis across multiple timeframes and making strategic decisions.

What you do with these statistics and how far you decide to take your research is entirely up to you, the possibilities are endless.

█ LIMITATIONS

Some higher timeframe candles on tickers with larger lookbacks such as the DXY , do not actually contain all the open, high, low and close (OHLC) data at the beginning of the chart. Instead, they use the close price for open, high and low prices. So, while we can determine whether the close price is higher or lower than the preceding close price, there is no way of knowing what actually happened intra-bar for these candles. And by default candles that close at the same price as the open price, will be counted as green. You can avoid this problem by utilising the sample period filter.

The green and red candle calculations are based solely on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with. Alternatively, you can replace the scenarios with your own logic to account for the gap anomalies, if you are feeling up to the challenge.

It is also worth noting that the sample size will be limited to your Trading View subscription plan. Premium users get 20,000 candles worth of data, pro+ and pro users get 10,000, and basic users get 5,000. If upgrading is currently not an option, you can always keep a rolling tally of the statistics in an excel spreadsheet or something of the like.

Rangemeter [theEccentricTrader]█ OVERVIEW

This indicator simply displays candle and peak to trough ranges in points or pips, depending on the symbol type, in a table, which can be repositioned and resized at the user's discretion.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Open Green and Red Candles

• An open green candle is one that has a close price equal to or above the price it opened, but has not yet closed to confirm the condition.

• An open red candle is one that has a close price lower than the price it opened, but has not yet closed to confirm the condition.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Range

The range is simply the difference between the current peak and current trough prices, generally expressed in terms of points or pips.

Open Range

An open range is here defined as one that is forming but has not yet completed. For example, a swing low that has an open green candle proceeding a red candle or series of red candles. Or a swing high that has an open red candle proceeding a green candle or series of green candles.

The table will only display the open range under the aforementioned circumstances, otherwise it will display the current, or previous, range.

█ FEATURES

Inputs

• Show Candle Ranges

• Show Largest and Smallest Candle Ranges

• Average Candle Range Lookback

• Show Ranges

• Show Largest and Smallest Ranges

• Average Range Lookback

• Position

• Text Size

█ HOW TO USE

The indicator can be used for strategy filtering and development, gauging current market conditions versus historic and helping to make more informed discretionary trading decisions. It can also be used like my Wavemeter indicator to objectively set the angle and projection ratio for my Fan Projections and Parallel Projections indicators.

█ LIMITATIONS

Some higher timeframe candles on tickers with larger lookbacks such as the DXY , do not actually contain all the open, high, low and close (OHLC) data at the beginning of the chart. Instead, they use the close price for open, high and low prices. So, while we can determine whether the close price is higher or lower than the preceding close price, there is no way of knowing what actually happened intra-bar for these candles. And by default candles that close at the same price as the open price, will be counted as green. You can avoid this problem by ensuring the lookback for the average range does not reach as far back as the start of the chart. If you are unsure about the candle count you can use my Candle Counter indicator to find out how many candles are displayed on the chart.

The green and red candle calculations are based solely on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with. Alternatively, you can replace the scenarios with your own logic to account for the gap anomalies, if you are feeling up to the challenge.

It is also worth noting that the lookback will be limited to your Trading View subscription plan. Premium users get 20,000 candles worth of data, pro+ and pro users get 10,000, and basic users get 5,000.

Opening Hour/Closing Hour Indices Statistics: high/low times; 5mVery specific indicator designed for 5min timeframe, to show the statistical timings of the highs and lows of Opening hour (9:30-10am) and Closing hour (3pm-4pm) NY time

~~Shown here on SPX 5min chart. Works all variants of the US indices. SPX and SPY typically show more days of history (non-extended session =>> more bars).

//Purpose:

-To get statistics on the timings of the high and low of the opening hour and the high & low of the closing hour.

//Design & Limitations:

- Designed for the 5minute chart ONLY . Need a sweet spot of 'bucket' size for the statistics: to allow meaningful comparison between times.

-Will also display on 1min chart but NOT the statistics panel, only the realtime data (today's opening hour/ closing hour timings).

-Can be slow to load depending on server load at the time. This is becasue of the multiple usage of looping array functions. Please be patient when loading or changing settings.

//User inputs:

-Standard formatting options: highlight color, table text color. Toggle on/off independently

-Decimal % percision (default = 0, i.e. 23%. If set to 1 => 22.8%)

-Show statistics: Show Opening hour statistics, Show Closing hour statistics

//Notes:

-Days of history shown at top of table; this is the size of the dataset. i.e. 254 here (254 trading days) =>> 254 opening hour highs, 254 closing hour lows etc.

--to illustrate with the above: 18% of those 254 closing hour highs occured on the 15:00 5min candle (i.e. between 15:00 and 15:05).

-SPY or SPX offer the largest history/dataset (circa 254 trading days).

-Note that the final timing in each hour is 10:25am and 15:55pm respectively: this is because the 10:25am 5min candle essentially ends at 10:30am =>> we properly captures the opening hour this way

-Pro+ users will get less data history than Premium users (half as much, due to 10k vs 20k bars history limit).

OHLC📕 LIBRARY OHLC

🔷 Introduction

This library is a custom library designed to work with real-time bars. It allows to easily calculate OHLC values for any source.

Personally, I use this library to accurately display the highest and lowest values on visual indicators such as my progress bars.

🔷 How to Use

◼ 1. Import the OHLC library into your TradingView script:

import cryptolinx/OHLC/1

- or -

Instead of the library namespace, you can define a custom namespace as alias.

import cryptolinx/OHLC/1 as src

◼ 2. Create a new OHLC source using the `new()` function.

varip mySrc = OHLC.new() // It is required to use the `varip` keyword to init your ``

- or -

If you has set up an alias before.

varip mySrc = src.new()

===

In that case, your `` needs to be `na`, define your object like that

varip mySrc = na

◼ 3. Call the `hydrateOHLC()` method on your OHLC source to update its values:

Basic

float rsi = ta.rsi(close, 14)

mySrc.hydrateOHLC(rsi)

- or -

Inline

rsi = ta.rsi(close, 14).hydrateOHLC(mySrc)

◼ 4. The data is accessible under their corresponding names.

mySrc.open

mySrc.high

mySrc.low

mySrc.close

🔷 Note: This library only works with real-time bars and will not work with historical bars.

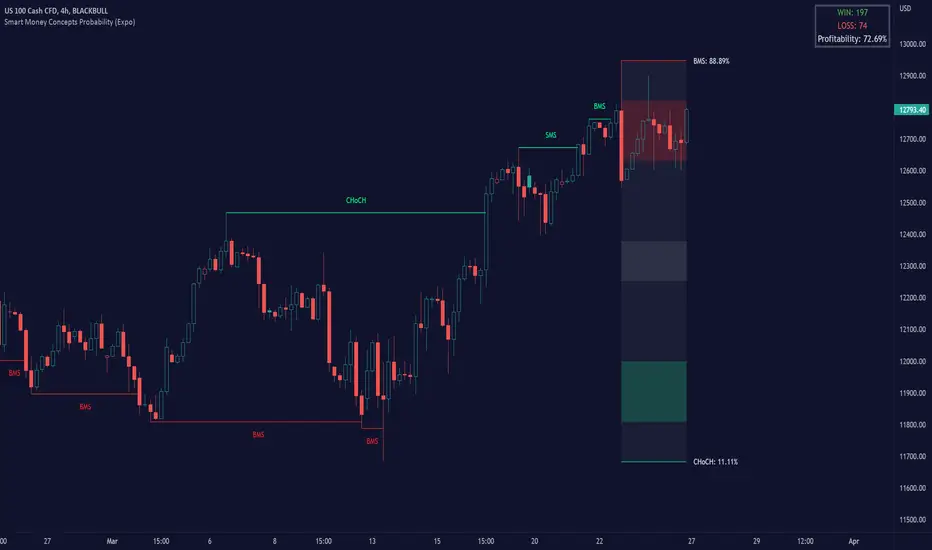

Smart Money Concepts Probability (Expo)█ Overview

The Smart Money Concept Probability (Expo) is an indicator developed to track the actions of institutional investors, commonly known as "smart money." This tool calculates the likelihood of smart money being actively engaged in buying or selling within the market, referred to as the "smart money order flow."

The indicator measures the probability of three key events: Change of Character ( CHoCH ), Shift in Market Structure ( SMS ), and Break of Structure ( BMS ). These probabilities are displayed as percentages alongside their respective levels, providing a straightforward and immediate understanding of the likelihood of smart money order flow.

Finally, the backtested results are shown in a table, which gives traders an understanding of the historical performance of the current order flow direction.

█ Calculations

The algorithm individually computes the likelihood of the events ( CHoCH , SMS , and BMS ). A positive score is assigned for events where the price successfully breaks through the level with the highest probability, and a negative score when the price fails to do so. By doing so, the algorithm determines the probability of each event occurring and calculates the total profitability derived from all the events.

█ Example

In this case, we have an 85% probability that the price will break above the upper range and make a new Break Of Structure and only a 16.36% probability that the price will break below the lower range and make a Change Of Character.

█ Settings

The Structure Period sets the pivot period to use when calculating the market structure.

The Structure Response sets how responsive the market structure should be. A low value returns a more responsive structure. A high value returns a less responsive structure.

█ How to use

This indicator is a perfect tool for anyone that wants to understand the probability of a Change of Character ( CHoCH ), Shift in Market Structure ( SMS ), and Break of Structure ( BMS )

The insights provided by this tool help traders gain an understanding of the smart money order flow direction, which can be used to determine the market trend.

█ Any Alert function call

An alert is sent when the price breaks the upper or lower range, and you can select what should be included in the alert. You can enable the following options:

Ticker ID

Timeframe

Probability percentage

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

NIFTY USDNifty in terms of USD value over time.

Nifty 50 index of Indian Stock Market, in terms of US Dollar terms at that specific time.

MarkovChainLibrary "MarkovChain"

Generic Markov Chain type functions.

---

A Markov chain or Markov process is a stochastic model describing a sequence of possible events in which the

probability of each event depends only on the state attained in the previous event.

---

reference:

Understanding Markov Chains, Examples and Applications. Second Edition. Book by Nicolas Privault.

en.wikipedia.org

www.geeksforgeeks.org

towardsdatascience.com

github.com

stats.stackexchange.com

timeseriesreasoning.com

www.ris-ai.com

github.com

gist.github.com

github.com

gist.github.com

writings.stephenwolfram.com

kevingal.com

towardsdatascience.com

spedygiorgio.github.io

github.com

www.projectrhea.org

method to_string(this)

Translate a Markov Chain object to a string format.

Namespace types: MC

Parameters:

this (MC) : `MC` . Markov Chain object.

Returns: string

method to_table(this, position, text_color, text_size)

Namespace types: MC

Parameters:

this (MC)

position (string)

text_color (color)

text_size (string)

method create_transition_matrix(this)

Namespace types: MC

Parameters:

this (MC)

method generate_transition_matrix(this)

Namespace types: MC

Parameters:

this (MC)

new_chain(states, name)

Parameters:

states (state )

name (string)

from_data(data, name)

Parameters:

data (string )

name (string)

method probability_at_step(this, target_step)

Namespace types: MC

Parameters:

this (MC)

target_step (int)

method state_at_step(this, start_state, target_state, target_step)

Namespace types: MC

Parameters:

this (MC)

start_state (int)

target_state (int)

target_step (int)

method forward(this, obs)

Namespace types: HMC

Parameters:

this (HMC)

obs (int )

method backward(this, obs)

Namespace types: HMC

Parameters:

this (HMC)

obs (int )

method viterbi(this, observations)

Namespace types: HMC

Parameters:

this (HMC)

observations (int )

method baumwelch(this, observations)

Namespace types: HMC

Parameters:

this (HMC)

observations (int )

Node

Target node.

Fields:

index (series int) : . Key index of the node.

probability (series float) : . Probability rate of activation.

state

State reference.

Fields:

name (series string) : . Name of the state.

index (series int) : . Key index of the state.

target_nodes (Node ) : . List of index references and probabilities to target states.

MC

Markov Chain reference object.

Fields:

name (series string) : . Name of the chain.

states (state ) : . List of state nodes and its name, index, targets and transition probabilities.

size (series int) : . Number of unique states

transitions (matrix) : . Transition matrix

HMC

Hidden Markov Chain reference object.

Fields:

name (series string) : . Name of thehidden chain.

states_hidden (state ) : . List of state nodes and its name, index, targets and transition probabilities.

states_obs (state ) : . List of state nodes and its name, index, targets and transition probabilities.

transitions (matrix) : . Transition matrix

emissions (matrix) : . Emission matrix

initial_distribution (float )

FunctionProbabilityViterbiLibrary "FunctionProbabilityViterbi"

The Viterbi Algorithm calculates the most likely sequence of hidden states *(called Viterbi path)*

that results in a sequence of observed events.

viterbi(observations, transitions, emissions, initial_distribution)

Calculate most probable path in a Markov model.

Parameters:

observations (int ) : array . Observation states data.

transitions (matrix) : matrix . Transition probability table, (HxH, H:Hidden states).

emissions (matrix) : matrix . Emission probability table, (OxH, O:Observed states).

initial_distribution (float ) : array . Initial probability distribution for the hidden states.

Returns: array. Most probable path.

FunctionBaumWelchLibrary "FunctionBaumWelch"

Baum-Welch Algorithm, also known as Forward-Backward Algorithm, uses the well known EM algorithm

to find the maximum likelihood estimate of the parameters of a hidden Markov model given a set of observed

feature vectors.

---

### Function List:

> `forward (array pi, matrix a, matrix b, array obs)`

> `forward (array pi, matrix a, matrix b, array obs, bool scaling)`

> `backward (matrix a, matrix b, array obs)`

> `backward (matrix a, matrix b, array obs, array c)`

> `baumwelch (array observations, int nstates)`

> `baumwelch (array observations, array pi, matrix a, matrix b)`

---

### Reference:

> en.wikipedia.org

> github.com

> en.wikipedia.org

> www.rdocumentation.org

> www.rdocumentation.org

forward(pi, a, b, obs)

Computes forward probabilities for state `X` up to observation at time `k`, is defined as the

probability of observing sequence of observations `e_1 ... e_k` and that the state at time `k` is `X`.

Parameters:

pi (float ) : Initial probabilities.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing

states given a state matrix is size (M x M) where M is number of states.

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. Given

state matrix is size (M x O) where M is number of states and O is number of different

possible observations.

obs (int ) : List with actual state observation data.

Returns: - `matrix _alpha`: Forward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first

dimension refers to the state and the second dimension to time.

forward(pi, a, b, obs, scaling)

Computes forward probabilities for state `X` up to observation at time `k`, is defined as the

probability of observing sequence of observations `e_1 ... e_k` and that the state at time `k` is `X`.

Parameters:

pi (float ) : Initial probabilities.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing

states given a state matrix is size (M x M) where M is number of states.

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. Given

state matrix is size (M x O) where M is number of states and O is number of different

possible observations.

obs (int ) : List with actual state observation data.

scaling (bool) : Normalize `alpha` scale.

Returns: - #### Tuple with:

> - `matrix _alpha`: Forward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first

dimension refers to the state and the second dimension to time.

> - `array _c`: Array with normalization scale.

backward(a, b, obs)

Computes backward probabilities for state `X` and observation at time `k`, is defined as the probability of observing the sequence of observations `e_k+1, ... , e_n` under the condition that the state at time `k` is `X`.

Parameters:

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

obs (int ) : Array with actual state observation data.

Returns: - `matrix _beta`: Backward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first dimension refers to the state and the second dimension to time.

backward(a, b, obs, c)

Computes backward probabilities for state `X` and observation at time `k`, is defined as the probability of observing the sequence of observations `e_k+1, ... , e_n` under the condition that the state at time `k` is `X`.

Parameters:

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

obs (int ) : Array with actual state observation data.

c (float ) : Array with Normalization scaling coefficients.

Returns: - `matrix _beta`: Backward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first dimension refers to the state and the second dimension to time.

baumwelch(observations, nstates)

**(Random Initialization)** Baum–Welch algorithm is a special case of the expectation–maximization algorithm used to find the

unknown parameters of a hidden Markov model (HMM). It makes use of the forward-backward algorithm

to compute the statistics for the expectation step.

Parameters:

observations (int ) : List of observed states.

nstates (int)

Returns: - #### Tuple with:

> - `array _pi`: Initial probability distribution.

> - `matrix _a`: Transition probability matrix.

> - `matrix _b`: Emission probability matrix.

---

requires: `import RicardoSantos/WIPTensor/2 as Tensor`

baumwelch(observations, pi, a, b)

Baum–Welch algorithm is a special case of the expectation–maximization algorithm used to find the

unknown parameters of a hidden Markov model (HMM). It makes use of the forward-backward algorithm

to compute the statistics for the expectation step.

Parameters:

observations (int ) : List of observed states.

pi (float ) : Initial probaility distribution.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

Returns: - #### Tuple with:

> - `array _pi`: Initial probability distribution.

> - `matrix _a`: Transition probability matrix.

> - `matrix _b`: Emission probability matrix.

---

requires: `import RicardoSantos/WIPTensor/2 as Tensor`

MyLibraryLibrary "MyLibrary"

TODO: add library description here

fun(x)

TODO: add function description here

Parameters:

x (float) : TODO: add parameter x description here

Returns: TODO: add what function returns

Leveraged Share Conversion IndicatorHello everyone,

Releasing my leveraged share conversion indicator.

I noticed that the option traders have all the fun and resources but the share traders don't really have many resources in terms of adjusting or profits on leveraged and inverse shares. So, I decided to change that this this indicator!

What it does:

In a nut shell, the calculator converts one share to the price of another through the use of a regression based analysis.

There are multiple pre-stored libraries available in the indicator, including IWM, SPY, BTC and QQQ.

However, if the ticker you want to convert is not in one of the pre-defined libraries, you can select "Use Alternative Ticker" and indicate the stock you wish to convert.

Using Libraries:

If the conversion you want is available in one of the libraries, simply select the conversion you would like. For example, if you want to convert SPY to SPXU, select that conversion. The indicator will then launch up the conversion results which it will display in a dashboard to the right and will also display the plotted conversion on a chart (see imagine below:

In the dashboard, the indicator will show you:

a) The conversion result: This is the most likely price based on the analysis

b) The standard error: This is the degree of error within the conversion. This is the basis of the upper and lower bands. In statistics, we can add and subtract the standard error from the likely result to get the "Upper" and "Lower" Confidence levels of assessment. This is just a fancy way of saying the range in which our predicted result will fall. So, for example, in the image above it shows you the price of SPXU is assessed to be around 16$ based on SPY's price. The standard error range is 15-17. This means that, the majority of the time, based on this SPY close price, SPXU should fall between 15-17$ with the most likely result being the 16$ range.

Why is there error?

Because leveraged shares have an inherent decay in them. The degree of decay can be captured utilizing the standard error. So at any given time, the small changes in price fluctuations caused by the fact that the share is leveraged can be assessed and displayed using standard error measurements.

c) The current correlation: This is important! Because if the stocks are not strongly correlated, it tells you there is a problem. In general, a perfect correlation is 1 or -1 (perfectly negative correlation or inverse correlation) and a bad correlation is anything under 0.5 or -0.5. So, for an INVERSE leveraged share, you would expect the correlation to read a negative value. Ideally -1. Because the inverse share is doing the opposite of the underlying (if the underlying goes up, the inverse goes down and vice versa). For a non-inverse leveraged share, the correlation should read a positive value. As the underlying goes up, so too does the leveraged.

Manual Conversion using Library:

If you are using a pre-defined library but want to convert a manual close price, simply select "Enable manual conversion" at the bottom of the settings and then type in the manual close price. If you are converting SPY to SPXU, type in the manual close price of SPY to get the result in SPXU and vice versa.

Using an Alternative Ticker:

If the ticker you want is not available in a pre-defined library (i.e. UDOW, BOIL, APPU, TSLL, etc.), simply select "Use Alternative Ticker" in the settings menu. When you select this, make sure your chart is set to the dominant chart. The "Dominant chart" is the chart of the underlying. So, if you want TSLA to TSLL, be sure you have the TSLA chart open and then set your Alternative Ticker to TSLL or TSLQ.

The process of using an Alternative Ticker remains the same. If you wish to enter a manual close price, simply select "Enable Manual Conversion".

Special Considerations:

The indicator uses 1 hour candles. Thus, please leave your dominant chart set on the 1 hour time frame to avoid confusing the indicator.

The lookback period of the manual conversion is 10, 1 hour candles. As such, the results should not be used to make longer term predictions (i.e. anything over 6 months is pushing the capabilities of a manual conversion but fair game for the pre-defined library conversions which use more longer-term data).

You can technically use the indicator to make assessments between 2 separate equities. For example, the relationship between QQQ and ARKK, SPY and DIA, IWM and SPY, etc. If there is a good enough correlation, you can use it to make predictions of the opposing ticker. For example, if DIA goes to 340, what would SPY likely do? And vice versa.

As always, I have prepared a tutorial and getting started video for your reference:

As always, let me know your questions and requests/recommendations for the indicator below. This indicator is my final reference indicator in my 3 part reference indicator release. I will be going back over the feedback to make improvements based on the suggestions I have received. So please feel free to leave any suggestions here and I will take them into consideration for improvement!

Thank you for checking this out and as always, safe trades!

Trend Counter [theEccentricTrader]█ OVERVIEW

This indicator counts the number of confirmed trend scenarios on any given candlestick chart and displays the statistics in a table, which can be repositioned and resized at the user's discretion.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a high price equal to or above the price it opened.

• A red candle is one that closes with a low price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

Muti-Part Upper and Lower Trends

• A multi-part return line uptrend begins with the formation of a new return line uptrend, or higher peak, and continues until a new downtrend, or lower peak, completes the trend.

• A multi-part downtrend begins with the formation of a new downtrend, or lower peak, and continues until a new return line uptrend, or higher peak, completes the trend.

• A multi-part uptrend begins with the formation of a new uptrend, or higher trough, and continues until a new return line downtrend, or lower trough, completes the trend.

• A multi-part return line downtrend begins with the formation of a new return line downtrend, or lower trough, and continues until a new uptrend, or higher trough, completes the trend.

█ FEATURES

Inputs

Start Date

End Date

Position

Text Size

Show Sample Period

Table

The table is colour coded, consists of seven columns and, as many as, forty-one rows. Blue cells denote the multi-part trend scenarios, green cells denote the corresponding return line uptrend and uptrend scenarios and red cells denote the corresponding downtrend and return line downtrend scenarios.

The trend scenarios are listed in the first column with their corresponding total counts to the right, in the second and fifth columns. The last row in column one, displays the sample period which can be adjusted or hidden via indicator settings.

The third and sixth columns display the trend scenarios as percentage of total 1-part trends. And columns four and seven display the total trend scenarios as percentages of the, last, or preceding trend part. For example 4-part trends as a percentages of 3-part trends. This offers more insight into what might happen next at any given point in time.

Plots

For a visual aid to this indicator please use in conjunction with my Return Line Uptrends, Downtrends, Uptrends and Return Line Downtrends indicators which can all be found on my profile page under scripts, or in community scripts under the same names. Unfortunately, I could not fit all the plots with the correct offsets into one script so I had to make a separate indicator for each trend type. I decided against labels as this would limit the visual data points to 500.

Green up-arrows, with the number of the trend part, denote return line uptrends and uptrends. Red down-arrows, with the number of the trend part, denote downtrends and return line downtrends.

█ HOW TO USE

This is intended for research purposes, strategy development and strategy optimisation. I hope it will be useful in helping to gain a better understanding of the underlying dynamics at play on any given market and timeframe.

It can, for example, give you an idea of whether the current trend will continue or fail, based on the current trend scenario and what has happened in the past under similar circumstances. Such information can be very useful when conducting top down analysis across multiple timeframes and making strategic decisions.

What you do with these statistics and how far you decide to take your research is entirely up to you, the possibilities are endless.

█ LIMITATIONS

Some higher timeframe candles on tickers with larger lookbacks such as the DXY , do not actually contain all the open, high, low and close (OHLC) data at the beginning of the chart. Instead, they use the close price for open, high and low prices. So, while we can determine whether the close price is higher or lower than the preceding close price, there is no way of knowing what actually happened intra-bar for these candles. And by default candles that close at the same price as the open price, will be counted as green. You can avoid this problem by utilising the sample period filter.