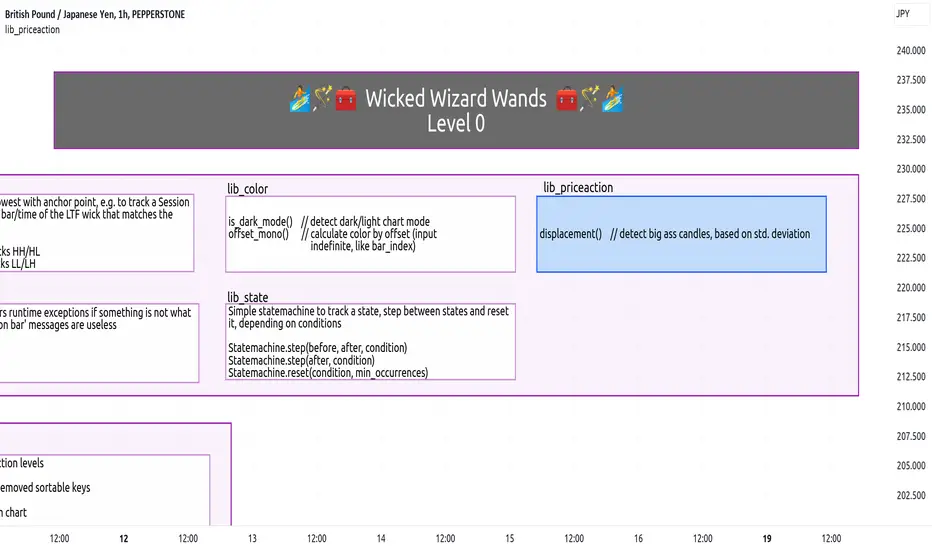

lib_priceactionLibrary "lib_priceaction"

a library for everything related to price action, starting off with displacements

displacement(len, min_strength, o, c)

calculate if there is a displacement and how strong it is

Parameters:

len (int) : The amount of candles to consider for the deviation

min_strength (float) : The minimum displacement strength to trigger a signal

o (float) : The source series on which calculations are based

c (float) : The source series on which calculations are based

Returns: a tuple of (bool signal, float displacement_strength)

Statistics

Overgeared Library Economic Calendar-----------------------------------------------------------

Base on script -> jdehorty/EconomicCalendar

Very Big Thanks to jdehorty/EconomicCalendar

-----------------------------------------------------------

Trend Correlation HeatmapHello everyone!

I am excited to release my trend correlation heatmap, or trend heatmap for short.

Per usual, I think its important to explain the theory before we get into the use of the indicator, so let's get into the theory!

The theory:

So what is a correlation?

Correlation is the relationship one variable has to another. Correlations are the basis of everything I do as a quantitative trader. From the correlation between the same variables (i.e. autocorrelation), the correlation between other variables (i.e. VIX and SPY, SPY High and SPY Low, DXY and ES1! close, etc.) and, as well, the correlation between price and time (time series correlation).

This may sound very familiar to you, especially if you are a user, observer or follower of my ideas and/or indicators. Ninety-five percent of my indicators are a function of one of those three things. Whether it be a time series based indicator (i.e.my time series indicator), whether it be autocorrelation (my autoregressive cloud indicator or my autocorrelation oscillator) or whether it be regressive in nature (i.e. my SPY Volume weighted close, or even my expected move which uses averages in lieu of regressive approaches but is foundational in regression principles. Or even my VIX oscillator which relies on the premise of correlations between tickers.) So correlation is extremely important to me and while its true I am more of a regression trader than anything, I would argue that I am more of a correlation trader, because correlations are the backbone of how I develop math models of stocks.

What I am trying to stress here is the importance of correlations. They really truly are foundational to any type of quantitative analysis for stocks. And as such, understanding the current relationship a stock has to time is pivotal for any meaningful analysis to be conducted.

So what is correlation to time and what does it tell us?

Correlation to time, otherwise known and commonly referred to as "Time Series", is the relationship a ticker's price has to the passing of time. It is displayed in the traditional Pearson Correlation Coefficient or R value and can be any value from -1 (strong negative relationship, i.e. a strong downtrend) to + 1 (i.e. a strong positive relationship, i.e. a strong uptrend). The higher or lower the value the stronger the up or downtrend is.

As such, correlation to time tells us two very important things. These are:

a) The direction of the stock; and

b) The strength of the trend.

Let's take a look at an example:

Above we have a chart of QQQ. We can see a trendline that seems to fit well. The questions we ask as traders are:

1. What is the likelihood QQQ breaks down from this trendline?

2. What is the likelihood QQQ continues up?

3. What is the likelihood QQQ does a false breakdown?

There are numerous mathematical approaches we can take to answer these questions. For example, 1 and 2 can be answered by use of a Cumulative Distribution Density analysis (CDDA) or even a linear or loglinear regression analysis and 3 can be answered, more or less, with a linear regression analysis and standard error ascertainment, or even just a general comparison using a data science approach (such as cosine similarity or Manhattan distance).

But, the reality is, all 3 of these questions can be visualized, at least in some way, by simply looking at the correlation to time. Let's look at this chart again, this time with the correlation heatmap applied:

If we look at the indicator we can see some pivotal things. These are:

1. We have 4, very strong uptrends that span both higher AND lower timeframes. We have a strong uptrend of 0.96 on the 5 minute, 50 candle period. We have a strong uptrend at the 300 candle lookback period on the 1 minute, we have a strong uptrend on the 100 day lookback on the daily timeframe period and we have a strong uptrend on the 5 minute on the 500 candle lookback period.

2. By comparison, we have 3 downtrends, all of which have correlations less than the 4 uptrends. All of the downtrends have a correlation above -0.8 (which we would want lower than -0.8 to be very strong), and all of the uptrends are greater than + 0.80.

3. We can also see that the uptrends are not confined to the smaller timeframes. We have multiple uptrends on multiple timeframes and both short term (50 to 100 candles) and long term (up to 500 candles).

4. The overall trend is strengthening to the upside manifested by a positive Max Change and a Positive Min change (to be discussed later more in-depth).

With this, we can see that QQQ is actually very strong and likely will continue at least some upside. If we let this play out:

We continued up, had one test and then bounced.

Now, I want to specify, this indicator is not a panacea for all trading. And in relation to the 3 questions posed, they are best answered, at least quantitatively, not only by correlation but also by the aforementioned methods (CDDA, etc.) but correlation will help you get a feel for the strength or weakness present with a stock.

What are some tangible applications of the indicator?

For me, this indicator is used in many ways. Let me outline some ways I generally apply this indicator in my day and swing trading:

1. Gauging the strength of the stock: The indictor tells you the most prevalent behavior of the stock. Are there more downtrends than uptrends present? Are the downtrends present on the larger timeframes vs uptrends on the shorter indicating a possible bullish reversal? or vice versa? Are the trends strengthening or weakening? All of these things can be visualized with the indicator.

2. Setting parameters for other indicators: If you trade EMAs or SMAs, you may have a "one size fits all" approach. However, its actually better to adjust your EMA or SMA length to the actual trend itself. Take a look at this:

This is QQQ on the 1 hour with the 200 EMA with 200 standard deviation bands added. If we look at the heatmap, we can see, yes indeed 200 has a fairly strong uptrend correlation of 0.70. But the strongest hourly uptrend is actually at 400 candles, with a correlation of 0.91. So what happens if we change the EMA length and standard deviation to 400? This:

The exact areas are circled and colour coded. You can see, the 400 offers more of a better reference point of supports and resistances as well as a better overall trend fit. And this is why I never advocate for getting married to a specific EMA. If you are an EMA 200 lover or 21 or 51, know that these are not always the best depending on the trend and situation.

Components of the indicator:

Ah okay, now for the boring stuff. Let's go over the functionality of the indicator. I tried to keep it simple, so it is pretty straight forward. If we open the menu here are our options:

We have the ability to toggle whichever timeframes we want. We also have the ability to toggle on or off the legend that displays the colour codes and the Max and Min highest change.

Max and Min highest change: The max and min highest change simply display the change in correlation over the previous 14 candles. An increasing Max change means that the Max trend is strengthening. If we see an increasing Max change and an increasing Min change (the Min correlation is moving up), this means the stock is bullish. Why? Because the min (i.e. ideally a big negative number) is going up closer to the positives. Therefore, the downtrend is weakening.

If we see both the Max and Min declining (red), that means the uptrend is weakening and downtrend is strengthening. Here are some examples:

Final Thoughts:

And that is the indicator and the theory behind the indicator.

In a nutshell, to summarize, the indicator simply tracks the correlation of a ticker to time on multiple timeframes. This will allow you to make judgements about strength, sentiment and also help you adjust which tools and timeframes you are using to perform your analyses.

As well, to make the indicator more user friendly, I tried to make the colours distinctively different. I was going to do different shades but it was a little difficult to visualize. As such, I have included a toggle-able legend with a breakdown of the colour codes!

That's it my friends, I hope you find it useful!

Safe trades and leave your questions, comments and feedback below!

Price Delta HeatmapThe Price Delta Heatmap is an indicator designed to visualize the price changes of an asset over time. It helps traders identify and analyze significant price movements and potential volatility. The indicator calculates the price delta, which is the difference between the current close price and the previous close price. It then categorizes the price deltas into different color ranges to create a heatmap-like display on the chart.

The indicator uses user-defined thresholds to determine the color ranges. These thresholds represent the minimum price change required for a specific color to be assigned. The thresholds are adjustable to accommodate different asset classes and trading strategies. Positive price deltas are associated with bullish movements, while negative price deltas represent bearish movements.

The indicator plots bars color-coded according to the price delta range it falls into. The color ranges can be customized to match personal preferences or specific trading strategies. Additionally, the indicator includes signal shapes below the bars to highlight significant positive or negative price deltas. Traders can adjust the threshold values based on their preferred sensitivity to price changes. Higher threshold values may filter out minor price movements and focus on more significant shifts, while lower threshold values will capture even minor fluctuations.

****The default settings have the thresholds set to levels of 100, 50, 20, 10, 0, -10, -20, -50, and -100. These numbers are well-suited for assets such as Ethereum or Bitcoin which are larger in price than an asset that has a price of $1.50, for example. To compensate, adjust the thresholds in the settings to reflect the price delta on the desired asset. All coloration and horizontal line plots will adjust to reflect these changes.****

Traders can interpret the Price Delta Heatmap as follows:

-- Bright green bars indicate the highest positive price deltas, suggesting strong bullish price movements.

-- Green bars represent positive price deltas above the third threshold, indicating significant bullish price changes.

-- Olive bars indicate positive price deltas above the second threshold, suggesting moderate bullish price movements.

-- Yellow bars represent positive price deltas above the lowest threshold, indicating minor bullish price changes. This color is reflected on the negative side as well. Yellow bars below zero indicate negative price deltas below the lowest threshold, suggesting minor bearish price changes.

-- White bars represent zero price deltas, indicating no significant price movement.

-- Orange bars represent negative price deltas below the second threshold, indicating moderate bearish price movements.

-- Red bars indicate negative price deltas below the third threshold, suggesting significant bearish price changes.

-- Maroon bars represent the lowest negative price deltas, indicating strong bearish price movements.

The coloration of the Price Delta line itself is determined by the line's relation to the second positive and second negative thresholds (default +/- 20) - if the line is above the second positive threshold, the line is colored lime (and is reflected in a lime arrow at the bottom of the indicator); if the line is below the second negative threshold, the line is colored fuchsia (also reflected as an arrow); if the line is between thresholds, it is colored aqua.

The Price Delta Heatmap can be used in various trading strategies and applications. Some potential use cases include:

-- Trend identification : The indicator helps traders identify periods of high volatility and potential trend reversals.

-- Volatility analysis : By observing the color changes in the heatmap, traders can gauge the volatility of an asset and adjust their risk management strategies accordingly.

-- Confirmation tool : The indicator can be used as a confirmation tool alongside other technical indicators, such as trend-following indicators or oscillators.

-- Breakout trading : Traders can look for price delta bars of a specific color range to identify potential breakout opportunities.

However, it's important to note that the Price Delta Heatmap has certain limitations. These include:

-- Lagging nature : The indicator relies on historical price data, which means it may not provide real-time insights into price movements.

-- Sensitivity to thresholds : The choice of threshold values affects the indicator's sensitivity and may vary depending on the asset being traded. It requires experimentation and adjustment to find optimal values.

-- Market conditions : The indicator's effectiveness may vary depending on market conditions, such as low liquidity or sudden news events.

Traders should consider using the Price Delta Heatmap in conjunction with other technical analysis tools and incorporate risk management strategies to enhance their trading decisions.

Currency Conversion ChartReleasing this utility indicator I made for myself and thought others may find it helpful.

It is a simple currency conversion indicator. I personally trade both the TSX and the NYSE and hold both CAD and USD. As such, when I take positions in either or, I like to track how the currency I hold is affecting my position.

What the indicator does:

So, as indicated above, it converts a ticker's candlestick chart into the designated currency. You can either manually set the currency exchange rate, or search the currency exchange chart on Tradingview and it will auto-convert:

Purple arrow: The purple arrow points to the auto-input. You can search the currency you want to convert and it will automatically apply the conversion. It defaults to USD to CAD, but you can do USD to JPY, AUD to CAD, whatever currency you want provided it is available on tradingview. Alternatively, you can select manual conversion and input the manual conversion rate to apply.

Green Arrow: The green arrow refers to the conversion type. The indicator will default to static auto. This will pull the previous daily close. As currency trades at all hours, real-time is not advisable because the currency is in constant flux. Static will provide more stable results. However, you can toggle between the two. You can also just toggle Manual conversion.

Yellow arrow and red arrow: These pertain to position management. The indicator will display the change in the currency price over the designated amount of days. If you want to know how much the currency has changed in price over the last 7 or 20 days, simply put that value in the change input.

When you click manage position, you can fill out the position size variable and put the number of days you have had the position in the change parameter. This is the cost of your position. It can be options or shares. It will then adjust your position cost for the current change in the currency based on the number of days you have held it.

The indicator can be viewed on any timeframe and you can see how the conversion price compares to the listed price.

And that's basically the indicator! Its a simple utility indicator and hopefully some people will find use from it like I do!

Safe trades everyone, take care.

Perp/Spot % SpreadTo be used on BINANCE USDT PERPETUAL charts.

Automatically pulls the equivalent Binance Spot pair and plots the Spread of the Close in % terms( Value of 1 means 1% difference from Perp price)

-Positive value means Spot is trading x% ABOVE the PERP

-Negative value means Spot is trading x% UNDER the PERP

Autocorrelation OscillatorReleasing the autocorrelation oscillator.

NOTE! Please be sure to read the description. This is a theoretical indicator and its important to understand the theory behind its use.

About the indicator:

Before getting into the indicator and its functionality, its important to discuss the theoretical underpinnings of the indicator.

The autocorrelation oscillator operates on two theories of market behaviour that go hand in hand. Those theories are the market efficiency theory and the random walk theory (or hypothesis ).

Market efficiency theory: The market efficiency theory or "Efficient Market Hypothesis (EMH)" postulates that all available information is reflected in a ticker's price almost instantaneously and thus it is impossible for an investor or trader to get ahead of the market because we cannot respond to the speed that the market responds. Of course, there are many holes in this theory, the most notable being that the market is a function of humans. Absent humans and their technological integrations into the market, the market would cease to react at all. But that's besides the point. This is a widely accepted theory and one in which I can mathematically observe through statistical tests. The truth behind this theory is the market is efficient for responding to evolving economic and financial information, likely owning to huge amounts of computer and algorithmic integration into trading, and thus the market is more efficient than the average person is capable (absent computerized algorithms and integration) of ascertaining nuanced financial and economic circumstances. By the time we the people can appraise information, the market has already acted on it. And that is the main premise of the EMH.

The next theory is the Random Walk Theory or Hypothesis (RWH). This builds on the EMH and essentially postulates that the market reacts so quickly to price in current circumstances that it is too random for people to truly exploit and benefit from.

The result of these two theories is two-fold and can be summarized as such:

a) The market behaves in a chaotic fashion that is seemingly random and is incapable of being predicted effectively; and

b) The market is more efficient than a person in incorporating key fundamental information, contributing to the high degree of seemingly random behaviour.

So, how does this help us?

It is said, because of the EMH and the RWH, the only way to truly exploit the market for profit is by:

a) Buying and holding and investing under the bias that stocks will eventually rise in value; or

b) For short term trading, exploiting the pricing anomalies within the data.

So how do we exploit pricing anomalies within the data?

Well, in my own research on market efficiency and behaviour, I have identified many ways of figuring out some anomalies. One of the most effective ways is by looking at simple correlation of lagged values, or autocorrelation for short.

What is autocorrelation and how to use it in relation to EMH and RWH?

Autocorrelation refers to the correlative relationship among the values in a series. Put simply, its the relationship of the same variable over time. For example, if we wanted to look at the auto-correlation of a ticker's high price, we would take, say, 5 to 7 previous high prices and correlate them with the current high price in a series dataset. If the EMH and RWH are true, the correlation among all the variables should have an average less than 0.5 or greater than -0.5. This would indicate true randomness in the dataset and thus an efficient market.

However, if the average of all of the sum's of these correlations are greater than or equal to 0.5 or less than or equal to -0.5, that indicates there is a high degree of autocorrelation and thus the EMH ad RWH is being invalidated as the market is not operating efficiently. This is an anomaly and this anomaly can be exploited.

So how do we exploit it?

Well, when the EMH and RWH hypothesis is being invalidated, we can expect what I coin as a "Regression to Chaos" i.e. the market will revert back to an efficient equilibrium state. So if we have a high correlation of the lagged variables and a strong uptrend or downtrend correlation, we can expect an inefficient market to correct back to an efficient market (i.e. have a reversal from the current trend).

So how does the indicator work?

The indicator measures the lagged correlation of the previous 5 highs and lows of a ticker. A high correlation among all of the highs and lows that exceeds 0.8 would be an invalidation of the EMH and RWH and thus signal a correction to come (i.e. a Regression to Chaos).

The indicator will display this by changing colour. Red for a bearish reversal and green for a bullish. Let's take a look below using the ticker MSFT:

Above we can see the indicator identifying observed inefficiencies within the MSFT ticker on the 1 minute timeframe. The green vertical lines correspond to potential bullish reversals as a result of bearish inefficiencies, the red correspond to bearish reversals as a result of bullish inefficiencies.

You can see these lead to reversals within the ticker.

Components of the indicator:

In the chart above we see the following that are being indicated by arrows:

Red Arrows: Show the identified inefficiencies. Red for bullish inefficiencies (i.e. bearish reversal), green for bearish inefficiencies (i.e. bullish reversal)

Yellow Arrow: The lagged variable chart. This will display the current correlation among all the lagged variables the indicator is assessing.

Teal arrow: Displays the current strength of the trend by correlating the trend to time. A strong negative value (i.e. a value less than or equal to -0.5) indicates a strong downtrend, a strong positive value indicates the inverse.

You can unselect the data-tables in the settings menu if you just want to view the correlation line itself. This part of the indicator is customizable. You can also define the lookback period; however, it is strongly recommended to leave it at 14 as this maintains the use of this indicator as an oscillator.

And that is the indicator! Let me know your comments, questions and feedback below.

Safe trades everyone!

Default Strategy Template© CN_FX-999

Coded By Christian Nataliano

First Coded In 14/06/2023

Last Edited In 22/06/2023

This Is A Default Strategy Template That Can Make Your Strategy Scripts More Organized With The Benefit Of Having The Same Layouts & Not Needing To Copy Over The Common Codes Such As Displaying Backtest Results, Opening & Closing Trades, Pine Connector Capabilities And A Clean User Input Interface. This Is A Blank Strategy Script So Feel Free To Use It As Your Default Template For Your Future Strategies.

Credits To Some Of The Custom Code In The Scripts To © ZenAndTheArtOfTrading, Especially The Table Data Plotting

CNTLibraryLibrary "CNTLibrary"

Custom Functions To Help Code In Pinescript V5

Coded By Christian Nataliano

First Coded In 10/06/2023

Last Edited In 22/06/2023

Huge Shout Out To © ZenAndTheArtOfTrading and his ZenLibrary V5, Some Of The Custom Functions Were Heavily Inspired By Matt's Work & His Pine Script Mastery Course

Another Shout Out To The TradingView's Team Library ta V5

//====================================================================================================================================================

// Custom Indicator Functions

//====================================================================================================================================================

GetKAMA(KAMA_lenght, Fast_KAMA, Slow_KAMA)

Calculates An Adaptive Moving Average Based On Perry J Kaufman's Calculations

Parameters:

KAMA_lenght (int) : Is The KAMA Lenght

Fast_KAMA (int) : Is The KAMA's Fastes Moving Average

Slow_KAMA (int) : Is The KAMA's Slowest Moving Average

Returns: Float Of The KAMA's Current Calculations

GetMovingAverage(Source, Lenght, Type)

Get Custom Moving Averages Values

Parameters:

Source (float) : Of The Moving Average, Defval = close

Lenght (simple int) : Of The Moving Average, Defval = 50

Type (string) : Of The Moving Average, Defval = Exponential Moving Average

Returns: The Moving Average Calculation Based On Its Given Source, Lenght & Calculation Type (Please Call Function On Global Scope)

GetDecimals()

Calculates how many decimals are on the quote price of the current market © ZenAndTheArtOfTrading

Returns: The current decimal places on the market quote price

Truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places © ZenAndTheArtOfTrading

Parameters:

number (float)

decimalPlaces (simple float)

Returns: The given number truncated to the given decimalPlaces

ToWhole(number)

Converts pips into whole numbers © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

ToPips(number)

Converts whole numbers back into pips © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

GetPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period © ZenAndTheArtOfTrading

Parameters:

value1 (float)

value2 (float)

lookback (int)

BarsAboveMA(lookback, ma)

Counts how many candles are above the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are above the MA

BarsBelowMA(lookback, ma)

Counts how many candles are below the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are below the EMA

BarsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many times price recently crossed the EMA

GetPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count) © ZenAndTheArtOfTrading

Parameters:

lookback (int)

direction (int)

Returns: The bar count of how many candles have retraced over the given lookback & direction

GetSwingHigh(Lookback, SwingType)

Check If Price Has Made A Recent Swing High

Parameters:

Lookback (int) : Is For The Swing High Lookback Period, Defval = 7

SwingType (int) : Is For The Swing High Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing High

GetSwingLow(Lookback, SwingType)

Check If Price Has Made A Recent Swing Low

Parameters:

Lookback (int) : Is For The Swing Low Lookback Period, Defval = 7

SwingType (int) : Is For The Swing Low Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing Low

//====================================================================================================================================================

// Custom Risk Management Functions

//====================================================================================================================================================

CalculateStopLossLevel(OrderType, Entry, StopLoss)

Calculate StopLoss Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLoss (float) : Is The Custom StopLoss Distance, Defval = 2x ATR Below Close

Returns: Float - The StopLoss Level In Actual Price As A

CalculateStopLossDistance(OrderType, Entry, StopLoss)

Calculate StopLoss Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

StopLoss (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The StopLoss Value In Pips

CalculateTakeProfitLevel(OrderType, Entry, StopLossDistance, RiskReward)

Calculate TakeProfit Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLossDistance (float)

RiskReward (float)

Returns: Float - The TakeProfit Level In Actual Price

CalculateTakeProfitDistance(OrderType, Entry, TakeProfit)

Get TakeProfit Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

TakeProfit (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The TakeProfit Value In Pips

CalculateConversionCurrency(AccountCurrency, SymbolCurrency, BaseCurrency)

Get The Conversion Currecny Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

AccountCurrency (simple string) : Is For The Account Currency Used

SymbolCurrency (simple string) : Is For The Current Symbol Currency (Front Symbol)

BaseCurrency (simple string) : Is For The Current Symbol Base Currency (Back Symbol)

Returns: Tuple Of A Bollean (Convert The Currency ?) And A String (Converted Currency)

CalculateConversionRate(ConvertCurrency, ConversionRate)

Get The Conversion Rate Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

ConvertCurrency (bool) : Is To Check If The Current Symbol Needs To Be Converted Or Not

ConversionRate (float) : Is The Quoted Price Of The Conversion Currency (Input The request.security Function Here)

Returns: Float Price Of Conversion Rate (If In The Same Currency Than Return Value Will Be 1.0)

LotSize(LotSizeSimple, Balance, Risk, SLDistance, ConversionRate)

Get Current Lot Size

Parameters:

LotSizeSimple (bool) : Is To Toggle Lot Sizing Calculation (Simple Is Good Enough For Stocks & Crypto, Whilst Complex Is For Forex)

Balance (float) : Is For The Current Account Balance To Calculate The Lot Sizing Based Off

Risk (float) : Is For The Current Risk Per Trade To Calculate The Lot Sizing Based Off

SLDistance (float) : Is The Current Position StopLoss Distance From Its Entry Price

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - Position Size In Units

ToLots(Units)

Converts Units To Lots

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots

ToUnits(Lots)

Converts Lots To Units

Parameters:

Lots (float) : Is For How Many Lots Need To Be Converted Into Units (Minimun 0.01 Units)

Returns: Int - Position Size In Units

ToLotsInUnits(Units)

Converts Units To Lots Than Back To Units

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots That Were Rounded To Units

ATRTrail(OrderType, SourceType, ATRPeriod, ATRMultiplyer, SwingLookback)

Calculate ATR Trailing Stop

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

SourceType (int) : Is To Determine Where To Calculate The ATR Trailing From, Defval = close

ATRPeriod (simple int) : Is To Change Its ATR Period, Defval = 20

ATRMultiplyer (float) : Is To Change Its ATR Trailing Distance, Defval = 1

SwingLookback (int) : Is To Change Its Swing HiLo Lookback (Only From Source Type 5), Defval = 7

Returns: Float - Number Of The Current ATR Trailing

DangerZone(WinRate, AvgRRR, Filter)

Calculate Danger Zone Of A Given Strategy

Parameters:

WinRate (float) : Is The Strategy WinRate

AvgRRR (float) : Is The Strategy Avg RRR

Filter (float) : Is The Minimum Profit It Needs To Be Out Of BE Zone, Defval = 3

Returns: Int - Value, 1 If Out Of Danger Zone, 0 If BE, -1 If In Danger Zone

IsQuestionableTrades(TradeTP, TradeSL)

Checks For Questionable Trades (Which Are Trades That Its TP & SL Level Got Hit At The Same Candle)

Parameters:

TradeTP (float) : Is The Trade In Question Take Profit Level

TradeSL (float) : Is The Trade In Question Stop Loss Level

Returns: Bool - True If The Last Trade Was A "Questionable Trade"

//====================================================================================================================================================

// Custom Strategy Functions

//====================================================================================================================================================

OpenLong(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Long Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Long"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Long Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

OpenShort(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Short Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Short"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Short Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

TP_SLExit(FromID, TPLevel, SLLevel, PercentageClose, Comment, CommentValue)

Exits Based On Predetermined TP & SL Levels

Parameters:

FromID (string) : Is The Trade ID That The TP & SL Levels Be Palced

TPLevel (float) : Is The Take Profit Level

SLLevel (float) : Is The StopLoss Level

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

CloseLong(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Long Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Long"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

CloseShort(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Short Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Short"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

BrokerCheck(Broker)

Checks Traded Broker With Current Loaded Chart Broker

Parameters:

Broker (string) : Is The Current Broker That Is Traded

Returns: Bool - True If Current Traded Broker Is Same As Loaded Chart Broker

OpenPC(LicenseID, OrderType, UseLimit, LimitPrice, SymbolPrefix, Symbol, SymbolSuffix, Risk, SL, TP, OrderComment, Spread)

Compiles Given Parameters Into An Alert String Format To Open Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Open

UseLimit (bool) : Is If We Want To Enter The Position At Exactly The Previous Closing Price

LimitPrice (float) : Is The Limit Price Of The Trade (Only For Pending Orders)

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Risk (float) : Is The Trade Risk Per Trade / Fixed Lot Sizing

SL (float) : Is The Trade SL In Price / In Pips

TP (float) : Is The Trade TP In Price / In Pips

OrderComment (string) : Is The Executed Trade Comment

Spread (float) : is The Maximum Spread For Execution

Returns: String - Pine Connector Order Syntax Alert Message

ClosePC(LicenseID, OrderType, SymbolPrefix, Symbol, SymbolSuffix)

Compiles Given Parameters Into An Alert String Format To Close Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Close

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Returns: String - Pine Connector Order Syntax Alert Message

//====================================================================================================================================================

// Custom Backtesting Calculation Functions

//====================================================================================================================================================

CalculatePNL(EntryPrice, ExitPrice, LotSize, ConversionRate)

Calculates Trade PNL Based On Entry, Eixt & Lot Size

Parameters:

EntryPrice (float) : Is The Trade Entry

ExitPrice (float) : Is The Trade Exit

LotSize (float) : Is The Trade Sizing

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - The Current Trade PNL

UpdateBalance(PrevBalance, PNL)

Updates The Previous Ginve Balance To The Next PNL

Parameters:

PrevBalance (float) : Is The Previous Balance To Be Updated

PNL (float) : Is The Current Trade PNL To Be Added

Returns: Float - The Current Updated PNL

CalculateSlpComm(PNL, MaxRate)

Calculates Random Slippage & Commisions Fees Based On The Parameters

Parameters:

PNL (float) : Is The Current Trade PNL

MaxRate (float) : Is The Upper Limit (In Percentage) Of The Randomized Fee

Returns: Float - A Percentage Fee Of The Current Trade PNL

UpdateDD(MaxBalance, Balance)

Calculates & Updates The DD Based On Its Given Parameters

Parameters:

MaxBalance (float) : Is The Maximum Balance Ever Recorded

Balance (float) : Is The Current Account Balance

Returns: Float - The Current Strategy DD

CalculateWR(TotalTrades, LongID, ShortID)

Calculate The Total, Long & Short Trades Win Rate

Parameters:

TotalTrades (int) : Are The Current Total Trades That The Strategy Has Taken

LongID (string) : Is The Order ID Of The Long Trades Of The Strategy

ShortID (string) : Is The Order ID Of The Short Trades Of The Strategy

Returns: Tuple Of Long WR%, Short WR%, Total WR%, Total Winning Trades, Total Losing Trades, Total Long Trades & Total Short Trades

CalculateAvgRRR(WinTrades, LossTrades)

Calculates The Overall Strategy Avg Risk Reward Ratio

Parameters:

WinTrades (int) : Are The Strategy Winning Trades

LossTrades (int) : Are The Strategy Losing Trades

Returns: Float - The Average RRR Values

CAGR(StartTime, StartPrice, EndTime, EndPrice)

Calculates The CAGR Over The Given Time Period © TradingView

Parameters:

StartTime (int) : Is The Starting Time Of The Calculation

StartPrice (float) : Is The Starting Price Of The Calculation

EndTime (int) : Is The Ending Time Of The Calculation

EndPrice (float) : Is The Ending Price Of The Calculation

Returns: Float - The CAGR Values

//====================================================================================================================================================

// Custom Plot Functions

//====================================================================================================================================================

EditLabels(LabelID, X1, Y1, Text, Color, TextColor, EditCondition, DeleteCondition)

Edit / Delete Labels

Parameters:

LabelID (label) : Is The ID Of The Selected Label

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

Text (string) : Is The Text Than Wants To Be Written In The Label

Color (color) : Is The Color Value Change Of The Label Text

TextColor (color)

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

EditLine(LineID, X1, Y1, X2, Y2, Color, EditCondition, DeleteCondition)

Edit / Delete Lines

Parameters:

LineID (line) : Is The ID Of The Selected Line

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

X2 (int) : Is The X2 Coordinate IN BARINDEX Xloc

Y2 (float) : Is The Y2 Coordinate IN PRICE Yloc

Color (color) : Is The Color Value Change Of The Line

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

//====================================================================================================================================================

// Custom Display Functions (Using Tables)

//====================================================================================================================================================

FillTable(TableID, Column, Row, Title, Value, BgColor, TextColor, ToolTip)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

Column (int) : Is The Current Column Of The Table That Wants To Be Edited

Row (int) : Is The Current Row Of The Table That Wants To Be Edited

Title (string) : Is The String Title Of The Current Cell Table

Value (string) : Is The String Value Of The Current Cell Table

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

ToolTip (string) : Is The ToolTip Of The Current Cell In The Table

Returns: Void

DisplayBTResults(TableID, BgColor, TextColor, StartingBalance, Balance, DollarReturn, TotalPips, MaxDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

StartingBalance (float) : Is The Account Starting Balance

Balance (float)

DollarReturn (float) : Is The Account Dollar Reture

TotalPips (float) : Is The Total Pips Gained / loss

MaxDD (float) : Is The Maximum Drawdown Over The Backtesting Period

Returns: Void

DisplayBTResultsV2(TableID, BgColor, TextColor, TotalWR, QTCount, LongWR, ShortWR, InitialCapital, CumProfit, CumFee, AvgRRR, MaxDD, CAGR, MeanDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

TotalWR (float) : Is The Strategy Total WR In %

QTCount (int) : Is The Strategy Questionable Trades Count

LongWR (float) : Is The Strategy Total WR In %

ShortWR (float) : Is The Strategy Total WR In %

InitialCapital (float) : Is The Strategy Initial Starting Capital

CumProfit (float) : Is The Strategy Ending Cumulative Profit

CumFee (float) : Is The Strategy Ending Cumulative Fee (Based On Randomized Fee Assumptions)

AvgRRR (float) : Is The Strategy Average Risk Reward Ratio

MaxDD (float) : Is The Strategy Maximum DrawDown In Its Backtesting Period

CAGR (float) : Is The Strategy Compounded Average GRowth In %

MeanDD (float) : Is The Strategy Mean / Average Drawdown In The Backtesting Period

Returns: Void

//====================================================================================================================================================

// Custom Pattern Detection Functions

//====================================================================================================================================================

BullFib(priceLow, priceHigh, fibRatio)

Calculates A Bullish Fibonacci Value (From Swing Low To High) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

BearFib(priceLow, priceHigh, fibRatio)

Calculates A Bearish Fibonacci Value (From Swing High To Low) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

GetBodySize()

Gets The Current Candle Body Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN POINTS

GetTopWickSize()

Gets The Current Candle Top Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Top Wick Size IN POINTS

GetBottomWickSize()

Gets The Current Candle Bottom Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Bottom Wick Size IN POINTS

GetBodyPercent()

Gets The Current Candle Body Size As A Percentage Of Its Entire Size Including Its Wicks © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN PERCENTAGE

GetTopWickPercent()

Gets The Current Top Wick Size As A Percentage Of Its Entire Body Size

Returns: Float - The Current Candle Top Wick Size IN PERCENTAGE

GetBottomWickPercent()

Gets The Current Bottom Wick Size As A Percentage Of Its Entire Bodu Size

Returns: Float - The Current Candle Bottom Size IN PERCENTAGE

BullishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Engulfing Candle

BearishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bearish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Engulfing Candle

Hammer(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Star(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Doji(MaxWickSize, MaxBodySize, DojiType, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Doji Candle

Parameters:

MaxWickSize (float) : To Specify The Maximum Lenght Of Its Upper & Lower Wick, Defval = 2

MaxBodySize (float) : To Specify The Maximum Lenght Of Its Candle Body IN PERCENT, Defval = 0.05

DojiType (int)

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Doji Candle

BullishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Harami Candle

BearishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Harami Candle

//====================================================================================================================================================

// Custom Time Functions

//====================================================================================================================================================

BarInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls within the given time session

BarOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls outside the given time session

DateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range © ZenAndTheArtOfTrading

Parameters:

startTime (int)

endTime (int)

Returns: A boolean - true if the current bar falls within the given dates

DayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze © ZenAndTheArtOfTrading

Parameters:

monday (bool)

tuesday (bool)

wednesday (bool)

thursday (bool)

friday (bool)

saturday (bool)

sunday (bool)

Returns: A boolean - true if the current bar's day is one of the given days

AUSSess()

Checks If The Current Australian Forex Session In Running

Returns: Bool - True If Currently The Australian Session Is Running

ASIASess()

Checks If The Current Asian Forex Session In Running

Returns: Bool - True If Currently The Asian Session Is Running

EURSess()

Checks If The Current European Forex Session In Running

Returns: Bool - True If Currently The European Session Is Running

USSess()

Checks If The Current US Forex Session In Running

Returns: Bool - True If Currently The US Session Is Running

UNIXToDate(Time, ConversionType, TimeZone)

Converts UNIX Time To Datetime

Parameters:

Time (int) : Is The UNIX Time Input

ConversionType (int) : Is The Datetime Output Format, Defval = DD-MM-YYYY

TimeZone (string) : Is To Convert The Outputed Datetime Into The Specified Time Zone, Defval = Exchange Time Zone

Returns: String - String Of Datetime

Regression Candle Conversion IndicatorHey everyone!

I got a pseudo-request a while ago for something like this, essentially the ability to track where another ticker would fall based on an alternative ticker.

I did create my ticker correlation reference indicator which directly looks at the correlation between 2 tickers. However, this is an indicator that operates on the same principle but is more pragmatic for trading.

What does it do?

Well, in keeping with the theme of what I call my indicators, this has a title that explains exactly what it does, "Regression Candle Conversion Indicator" or "RCCI" for short. It uses simple regression to convert one ticker to another. So while you are tracking one indicator, you can see where the expected value should fall on the other.

Applications?

The big application of this for me is being able to track where SPY/QQQ or IWM is falling during overnight trading sessions. Extended trading hours close at 8 pm NYSE time. After that, you have to guess where futures prices will put the ETF version of it. This indicator will allow you to track where, theoretically, the underlying ETF ticker will fall based on the current trading behaviour.

Some other applications are just the ability to track how similar or dissimilar one stock is to the other. For example, if we wanted to trade, say, Boeing using shares of DFEN or ITA (a defence specific ETF), here is what we get:

In the chart above we can see BA as the primary chart and ITA as the RCCI converted chart. We will see 2 major things that should cause us concern.

First, there is a really poor correlation between the two tickers. This indicates that ITA may not produce the best exposure if I am directly looking for Boeing exposure.

Second, there is a wide standard error. this means that the results that the RCCI is providing may be skewed up to +/- 2 points (as indicated by the standard error chart).

Let's take a look at BA and DFEN:

In the above, we can see that the correlation is not great, but the standard error is quite low.

This means that, while this may not be the best ticker for Boeing exposure, the RCCI is able to confidently calculate the ticker within +/- 0.50 cents based on BA's underlying data.

However, its important to note that it is not advisable to really rely on these results if the correlation is less than + 0.5 or greater than -0.5.

Let's take a look at a few more examples:

Above we have BA (NYSE) vs BA (NEO TSX CAD Hedged). We can see the strong relationship and high confidence calculations.

And some others:

SPX (primary) and ES1! (secondary):

RTY and IWM:

ES1! and SPY:

Customizations:

As you can see above, it is pretty straight forward. There are 3 options:

Lookback Length: Determines the length of assessment for correlation and the regression assessment.

Manual Ticker Input: The indicator will pull the data from your current chart and compare it against a manually selected indicator. You must tell the indicator which ticker you are comparing against.

Data Table: This will show you the data table which contains the standard error assessment and the correlation assessment. These are determined by your lookback length. The lookback length is defaulted to 500.

And that's the indicator! It's pretty straight forward. Hopefully you find it helpful, especially if you track futures during overnight sessions.

Leave your comments/questions and feedback below.

Thanks for checking it out!

Risk ManagementLibrary "RiskManagement"

This library keeps your money in check, and is used for testing and later on webhook-applications too. It has four volatility functions and two of them can be used to calculate a Stop-Loss, like Average True Range. It also can calculate Position Size, and the Risk Reward Ratio. But those calculations don't take leverage into account.

position_size(portfolio, risk, entry, stop_loss, use_leverage, qty_as_integer)

This function calculates the definite amount of contracts/shares/units you should use to buy or sell. This value can used by `strategy.entry(qty)` for example.

Parameters:

portfolio (float) : This is the total amount of the currency you own, and is also used by strategy.initial_capital, for example. The amount is needed to calculate the maximum risk you are willing to take per trade.

risk (float) : This is the percentage of your Portfolio you willing to loose on a single trade. Possible values are between 0.1 and 100%. Same usecase with strategy(default_qty_type=strategy.percent_of_equity,default_qty_value=100), except its calculation the risk only.

entry (float) : This is the limit-/market-price for the investment. In other words: The price per contract/share/unit you willing to buy or sell.

stop_loss (float) : This is the limit-/market-price when to exit the trade, to minimize your losses.

use_leverage (bool) : This value is optional. When not used or when set to false then this function will let you invest your portfolio at max.

qty_as_integer (bool) : This value is optional. When set to true this function will return a value used with integers. The largest integer less than or equal to the given number. Because some Broker/Exchanges let you trade hole contracts/shares/units only.

Returns: float

position_size_currency(portfolio, risk, entry, stop_loss)

This function calculates the definite amount of currency you should use when going long or short.

Parameters:

portfolio (float) : This is the total amount of the currency you own, and is also used by strategy.initial_capital, for example. The amount is needed to calculate the maximum risk you are willing to take per trade.

risk (float) : This is the percentage of your Portfolio you willing to loose on a single trade. For example: 1 is 100% and 0,01 is 1%. Default amount is 0.02 (2%).

entry (float) : This is the limit-/market-price for the current investment. In other words: The price per contract/share/units you willing to buy or sell.

stop_loss (float) : This is the limit-/market-price when to exit the trade, to minimize your losses.

Returns: float

rrr(entry, stop_loss, take_profit)

This function calculates the Risk Reward Ratio. Common values are between 1.5 and 2.0 and you should not go lower except for very few special cases.

Parameters:

entry (float) : This is the limit-/market-price for the investment. In other words: The price per contract/share/unit you willing to buy or sell.

stop_loss (float) : This is the limit-/market-price when to exit the trade, to minimize your losses.

take_profit (float) : This is the limit-/market-price when to take profits.

Returns: float

change_in_price(length)

This function calculates the difference between price now and close price of the candle 'n' bars before that. If prices are very volatile but closed where they began, then this method would show zero volatility. Over many calculations, this method returns a reasonable measure of volatility, but will always be lower than those using the highs and lows.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

maximum_price_fluctuation(length)

This function measures volatility over most recent candles, which could be used as an estimate of risk. It may also be effective as the basis for a stop-loss or take-profit, like the ATR but it ignores the frequency of directional changes within the time interval. In other words: The difference between the highest high and lowest low over 'n' bars.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

absolute_price_changes(length)

This function measures volatility over most recent close prices. This is excellent for comparing volatility. It includes both frequency and magnitude. In other words: Sum of differences between second to last close price and last close price as absolute value for 'n' bars.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

annualized_volatility(length)

This function measures volatility over most recent close prices. Its the standard deviation of close over the past 'n' periods, times the square root of the number of periods in a year.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

Total ReturnThis script calculates a Total Return index for stocks that shows the total performance of a stock, incorporating returns from both the share price and dividends.

To understand this, consider the situation where you invest in a 5% div stock and hold the position for 10 years. Assume at the end of 10 years, the price has gone up by 50%. A price chart will then show a 50% return, but in reality the investor has also received 50% of the initial investment in dividends, making his total return substantially more. Exactly how much more depends on whether the investor reinvested the dividends in the stock, or just held them as cash. If the former, his total return will be well over 100%; in the latter, his total return will be 100% exactly.

There are 2 input options:

- Dividend type: allows the user to choose "gross" or "net". Note that most stocks will have a "gross" data series whereas many will not have a "net" series.

- Reinvestment: allows the user to choose whether dividends should be reinvested in the stock ("Yes") or held in cash ("No").

Total return formula:

- With reinvestment: log((today's closing price + dividends paid today) / (yesterday's closing price))

- Without reinvestment: log(today's closing price / yesterday's closing price) + log (dividends paid thus far / first closing price)

Linear Correlation Coefficient W/ MAs and Significance TestsThis Linear CC takes into account the log-normal distribution of stock prices and performs Pearson correlation on that data set. It also smoothens the results into an easy to read oscillator, and performs a two-tail t-test on the correlation coefficient data (with a = 0.05) to determine the significance of the coefficients. Significant results are shown in a solid yellow color while insignificant results are shown in a dark yellow color (you can eyeball this with a normal LCC by looking at results around -0.5 to +0.5).

Two MAs are provided as well for a quick trend analysis. You can reduce the lookback period, but it defaults to 31 for the sake of statistical standards.

ASG Delta %This utility script provides a convenient way to calculate the percentage gain or drop of a token's price within a user-defined date range. It eliminates the need for manual measurement on individual charts, saving time and effort.

The script is particularly valuable when integrated into a daily token scanning routine for watchlists. By comparing the significant gains or drops among different tokens, traders can identify potential trading opportunities.

Simply select the desired date range, and the script will identify the highest and lowest price points achieved during that period. It then shows a visual representation in the form of a bullish or bearish box, displaying the percentage change (delta %). If the current price falls within the box's upper and lower bounds, additional percentage information can be shown in either the 'normal' or 'reverse' mode.

For instance, if a token experiences a -52.35% drop, enabling the 'Reverse' setting will reveal a potential 109.86% gain (from the low), or a 76.02% gain (from current price) or a potential drop of -16.5% (from current price) etc.. Having these basic statistics available, without having to manually chart them, especially during prolonged bear or bull markets, enables traders to make informed decisions and position themselves for more profitable trades.

I hope you find this script valuable. Your comments and recommendations are welcome as they will help improve the script's functionality further.

The Z-score The Z-score, also known as the standard score, is a statistical measurement that describes a value's relationship to the mean of a group of values. It's measured in terms of standard deviations from the mean. If a Z-score is 0, it indicates that the data point's score is identical to the mean score. Z-scores may be positive or negative, with a positive value indicating the score is above the mean and a negative score indicating it is below the mean.

The concept of Z-score was introduced by statistician Carl Friedrich Gauss as part of his "method of the least squares," which was an important step in the development of the normal distribution and Z-score tables. It's a key concept in statistics and is used in various statistical tests.

In financial analysis, Z-scores are used to determine whether a data point is usual or unusual. You can think of it as a measure of how many standard deviations an element is from the mean. For instance, a Z-score of 1.0 would denote a value that is one standard deviation from the mean. Z-scores are also used to predict probabilities, with Z-scores having a distribution that is expected to be normal.

In trading, a Z-score is used to determine how often a trading system may produce a string of winners or losers. It can help a trader to understand whether the losses or profits they see are something that the system would most likely produce, or if it's a once in a blue moon situation. This helps traders make decisions about when to start or stop a system.

I just wanted to play a bit with the Z-score I guess.

Feel free to share your findings if you discover additional applications for this strategy or identify timeframes where it appears to perform more optimally.

How it works:

This strategy is based on a statistical concept called Z-score, which measures the number of standard deviations a data point is from the mean. In other words, it helps determine how unusual or usual a data point is.

In the context of this strategy, Z-score is applied to a 10-period EMA (Exponential Moving Average) of Heikin-Ashi candlestick close prices. The Z-score is calculated over a look-back period of 25 bars.

The EMA of the Z-score is then calculated over a 20-bar period, and the upper and lower thresholds (bounds for buy and sell signals) are defined using the 90th and 10th percentiles of this EMA score.

Long positions are taken when the Z-score crosses above the lower threshold or crosses above the mid-line (50th percentile). An additional long entry is made when the Z-score crosses above the highest value the EMA has been in the past 100 periods.

Short positions are initiated when the EMA crosses below the upper threshold, lower threshold or the highest value the EMA has been in the past 100 periods.

Positions are closed when opposing entry conditions are met, for example, a long position is closed when the short entry condition is true, and vice versa.

Set your desired start date for the strategy. This can be modified in the timestamp("YYYY MM DD") function at the top of the script.

Machine Learning : Torben's Moving Median KNN BandsWhat is Median Filtering ?

Median filtering is a non-linear digital filtering technique, often used to remove noise from an image or signal. Such noise reduction is a typical pre-processing step to improve the results of later processing (for example, edge detection on an image). Median filtering is very widely used in digital image processing because, under certain conditions, it preserves edges while removing noise (but see the discussion below), also having applications in signal processing.

The main idea of the median filter is to run through the signal entry by entry, replacing each entry with the median of neighboring entries. The pattern of neighbors is called the "window", which slides, entry by entry, over the entire signal. For one-dimensional signals, the most obvious window is just the first few preceding and following entries, whereas for two-dimensional (or higher-dimensional) data the window must include all entries within a given radius or ellipsoidal region (i.e. the median filter is not a separable filter).

The median filter works by taking the median of all the pixels in a neighborhood around the current pixel. The median is the middle value in a sorted list of numbers. This means that the median filter is not sensitive to the order of the pixels in the neighborhood, and it is not affected by outliers (very high or very low values).

The median filter is a very effective way to remove noise from images. It can remove both salt and pepper noise (random white and black pixels) and Gaussian noise (randomly distributed pixels with a Gaussian distribution). The median filter is also very good at preserving edges, which is why it is often used as a pre-processing step for edge detection.

However, the median filter can also blur images. This is because the median filter replaces each pixel with the value of the median of its neighbors. This can cause the edges of objects in the image to be smoothed out. The amount of blurring depends on the size of the window used by the median filter. A larger window will blur more than a smaller window.

The median filter is a very versatile tool that can be used for a variety of tasks in image processing. It is a good choice for removing noise and preserving edges, but it can also blur images. The best way to use the median filter is to experiment with different window sizes to find the setting that produces the desired results.

What is this Indicator ?

K-nearest neighbors (KNN) is a simple, non-parametric machine learning algorithm that can be used for both classification and regression tasks. The basic idea behind KNN is to find the K most similar data points to a new data point and then use the labels of those K data points to predict the label of the new data point.

Torben's moving median is a variation of the median filter that is used to remove noise from images. The median filter works by replacing each pixel in an image with the median of its neighbors. Torben's moving median works in a similar way, but it also averages the values of the neighbors. This helps to reduce the amount of blurring that can occur with the median filter.

KNN over Torben's moving median is a hybrid algorithm that combines the strengths of both KNN and Torben's moving median. KNN is able to learn the underlying distribution of the data, while Torben's moving median is able to remove noise from the data. This combination can lead to better performance than either algorithm on its own.

To implement KNN over Torben's moving median, we first need to choose a value for K. The value of K controls how many neighbors are used to predict the label of a new data point. A larger value of K will make the algorithm more robust to noise, but it will also make the algorithm less sensitive to local variations in the data.

Once we have chosen a value for K, we need to train the algorithm on a dataset of labeled data points. The training dataset will be used to learn the underlying distribution of the data.

Once the algorithm is trained, we can use it to predict the labels of new data points. To do this, we first need to find the K most similar data points to the new data point. We can then use the labels of those K data points to predict the label of the new data point.

KNN over Torben's moving median is a simple, yet powerful algorithm that can be used for a variety of tasks. It is particularly well-suited for tasks where the data is noisy or where the underlying distribution of the data is unknown.

Here are some of the advantages of using KNN over Torben's moving median:

KNN is able to learn the underlying distribution of the data.

KNN is robust to noise.

KNN is not sensitive to local variations in the data.

Here are some of the disadvantages of using KNN over Torben's moving median:

KNN can be computationally expensive for large datasets.

KNN can be sensitive to the choice of K.

KNN can be slow to train.

Ratio To Average - The Quant ScienceRatio To Average - The Quant Science is a quantitative indicator that calculates the percentage ratio of the market price in relation to a reference average. The indicator allows the calculation of the ratio using four different types of averages: SMA, EMA, WMA, and HMA. The ratio is represented by a series of histograms that highlight periods when the ratio is positive (in green) and periods when the ratio is negative (in red).

What is the Ratio to Average?

The Ratio to Average is a measure that tracks the price movements with one of its averages, calculating how much the price is above or below its own average, in percentage terms.

USER INTERFACE

Lenght: it adjusts the number of bars to include in the calculation of the average.

Moving Average: it allows you to choose the type of average to use.

Color Up/Color Down : it allows you to choose the color of the indicator for positive and negative ratios.

Currency ConverterWhat it is?

It's a Currency converter/Exchange rate Viewer.

How it works?

You put the main currency and the other currency in setting then it will show the converted rate in chart.

Daily data infoThis indicator can:

- Indicate on which day of the week created the High or Low

- Based on the bars you set, sum the times in which (The day of the week you want to test makes the Weekly High or Low)

- Has the option to Sum or calculate the %

Position Size Calculator (EzAlgo)Upon adding the indicator to the chart, you will be prompted to place entry price lines, stop loss price line, and multiple take profit price lines by clicking at the desired price level on the chart.

Section Summaries