WIPFunctionLyaponovLibrary "WIPFunctionLyaponov"

Lyapunov exponents are mathematical measures used to describe the behavior of a system over

time. They are named after Russian mathematician Alexei Lyapunov, who first introduced the concept in the

late 19th century. The exponent is defined as the rate at which a particular function or variable changes

over time, and can be positive, negative, or zero.

Positive exponents indicate that a system tends to grow or expand over time, while negative exponents

indicate that a system tends to shrink or decay. Zero exponents indicate that the system does not change

significantly over time. Lyapunov exponents are used in various fields of science and engineering, including

physics, economics, and biology, to study the long-term behavior of complex systems.

~ generated description from vicuna13b

---

To calculate the Lyapunov Exponent (LE) of a given Time Series, we need to follow these steps:

1. Firstly, you should have access to your data in some format like CSV or Excel file. If not, then you can collect it manually using tools such as stopwatches and measuring tapes.

2. Once the data is collected, clean it up by removing any outliers that may skew results. This step involves checking for inconsistencies within your dataset (e.g., extremely large or small values) and either discarding them entirely or replacing with more reasonable estimates based on surrounding values.

3. Next, you need to determine the dimension of your time series data. In most cases, this will be equal to the number of variables being measured in each observation period (e.g., temperature, humidity, wind speed).

4. Now that we have a clean dataset with known dimensions, we can calculate the LE for our Time Series using the following formula:

λ = log(||M^T * M - I||)/log(||v||)

where:

λ (Lyapunov Exponent) is the quantity that will be calculated.

||...|| denotes an Euclidean norm of a vector or matrix, which essentially means taking the square root of the sum of squares for each element in the vector/matrix.

M represents our Jacobian Matrix whose elements are given by:

J_ij = (∂fj / ∂xj) where fj is the jth variable and xj is the ith component of the initial condition vector x(t). In other words, each element in this matrix represents how much a small change in one variable affects another.

I denotes an identity matrix whose elements are all equal to 1 (or any constant value if you prefer). This term essentially acts as a baseline for comparison purposes since we want our Jacobian Matrix M^T * M to be close to it when the system is stable and far away from it when the system is unstable.

v represents an arbitrary vector whose Euclidean norm ||v|| will serve as a scaling factor in our calculation. The choice of this particular vector does not matter since we are only interested in its magnitude (i.e., length) for purposes of normalization. However, if you want to ensure that your results are accurate and consistent across different datasets or scenarios, it is recommended to use the same initial condition vector x(t) as used earlier when calculating our Jacobian Matrix M.

5. Finally, once we have calculated λ using the formula above, we can interpret its value in terms of stability/instability for our Time Series data:

- If λ < 0, then this indicates that the system is stable (i.e., nearby trajectories will converge towards each other over time).

- On the other hand, if λ > 0, then this implies that the system is unstable (i.e., nearby trajectories will diverge away from one another over time).

~ generated description from airoboros33b

---

Reference:

en.wikipedia.org

www.collimator.ai

blog.abhranil.net

www.researchgate.net

physics.stackexchange.com

---

This is a work in progress, it may contain errors so use with caution.

If you find flaws or suggest something new, please leave a comment bellow.

_measure_function(i)

helper function to get the name of distance function by a index (0 -> 13).\

Functions: SSD, Euclidean, Manhattan, Minkowski, Chebyshev, Correlation, Cosine, Camberra, MAE, MSE, Lorentzian, Intersection, Penrose Shape, Meehl.

Parameters:

i (int)

_test(L)

Helper function to test the output exponents state system and outputs description into a string.

Parameters:

L (float )

estimate(X, initial_distance, distance_function)

Estimate the Lyaponov Exponents for multiple series in a row matrix.

Parameters:

X (map)

initial_distance (float) : Initial distance limit.

distance_function (string) : Name of the distance function to be used, default:`ssd`.

Returns: List of Lyaponov exponents.

max(L)

Maximal Lyaponov Exponent.

Parameters:

L (float ) : List of Lyapunov exponents.

Returns: Highest exponent.

Statistics

Median of Means Estimator Median of Means (MoM) is a measure of central tendency like mean (average) and median. However, it could be a better and robust estimator of central tendency when the data is not normal, asymmetric, have fat tails (like stock price data) and have outliers. The MoM can be used as a robust trend following tool and in other derived indicators.

Median of means (MoM) is calculated as follows, the MoM estimator shuffles the "n" data points and then splits them into k groups of m data points (n= k*m). It then computes the Arithmetic Mean of each group (k). Finally, it calculate the median over the resulting k Arithmetic Means. This technique diminishes the effect that outliers have on the final estimation by splitting the data and only considering the median of the resulting sub-estimations. This preserves the overall trend despite the data shuffle.

Below is an example to illustrate the advantages of MoM

Set A Set B Set C

3 4 4

3 4 4

3 5 5

3 5 5

4 5 5

4 5 5

5 5 5

5 5 5

6 6 8

6 6 8

7 7 10

7 7 15

8 8 40

9 9 50

10 100 100

Median 5 5 5

Mean 5.5 12.1 17.9

MoM 5.7 6.0 17.3

For all three sets the median is the same, though set A and B are the same except for one outlier in set B (100) it skews the mean but the median is resilient. However, in set C the group has several high values despite that the median is not responsive and still give 5 as the central tendency of the group, but the median of means is a value of 17.3 which is very close to the group mean 17.9. In all three cases (set A, B and C) the MoM provides a better snapshot of the central tendency of the group. Note: The MoM is dependent on the way we split the data initially and the value might slightly vary when the randomization is done sevral time and the resulting value can give the confidence interval of the MoM estimator.

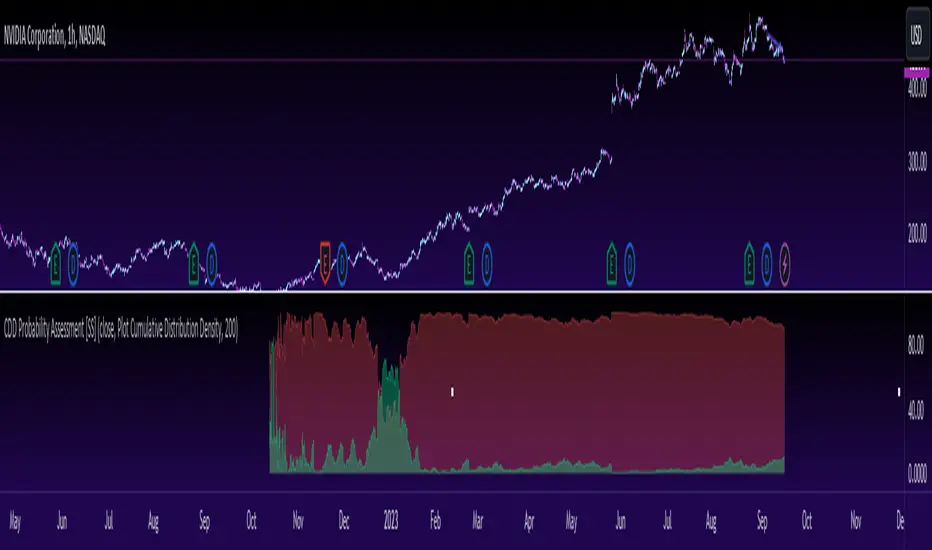

Cumulative Distribution of a Dataset [SS]This is the Cumulative Distribution of a Dataset indicator that also calculates the Kurtosis and Skewness for a selected dataset and determines the normality and distribution type.

What it does, in pragmatic terms?

In the most simplest terms, it calculates the cumulative distribution function (or CDF) of user-defined dataset.

The cumulative distribution function (CDF) is a concept used in statistics and probability to describe how the probability of a random variable taking on a certain value or less is distributed across the entire range of possible values. In simpler terms, you can conceptualize the CDF as this:

Imagine you have a list of data, such as test scores of students in a class. The CDF helps you answer questions like, "What's the probability that a randomly chosen student scored 80 or less on the test?"

Or in our case, say we are in a strong up or downtrend on a stock. The CDF can help us answer questions like "Based on this current xyz trend, what is the probability that a ticker will fall above X price or below Y price".

Within the indicator, you can manually assess a price of interest. Let's say, for NVDA, we want to know the probability NVDA goes above or below $450. We can enter $450 into the indicator and get this result:

Other functions:

Kurtosis and Skewness Functions:

In addition to calculating and plotting the CDF, we can also plot the kurtosis & Skewness.

This can help you look for outlier periods where the distribution of your dataset changed. It can potentially alert you to when a stock is behaving abnormally and when it is more stable and evenly distributed.

Tests of normality

The indicator will use the kurtosis and skewness to determine the normality of the dataset. The indicator is programmed to recognize up to 7 different distribution types and alert you to them and the implications they have in your overall assessment.

e.g. #1 AMC during short squeeze:

e.g. #2: BA during the COVID crash:

Plotting the standardized Z-Score of the Distribution Dataset

You can also standardize the dataset by converting it into Z-Score format:

Plot the raw, CDF results

Two values are plotting, the green and the red. The green represents the probability of a ticker going higher than the current value. The red represents the probability of a ticker going lower than the current value.

Limitations

There are some limitations of the indicator which I think are important to point out. They are:

The indicator cannot tell you timelines, it can only tell you the general probability that data within the dataset will fall above or below a certain value.

The indicator cannot take into account projected periods of consolidation. It is possible a ticker can remain in a consolidation phase for a very long time. This would have the effect of stabilizing the probability in one direction (if there was a lot of downside room, it can normalize the data out so that the extent of the downside probability is mitigated). Thus, its important to use judgement and other methods to assess the likelihood that a stock will pullback or continue up, based on the overall probability.

The indicator is only looking at an individual dataset.

Using this indicator, you have to omit a large amount of data and look at solely a confined dataset. In a way, this actually improves the accuracy, but can also be misleading, depending on the size and strength of the dataset being chosen. It is important to balance your choice of dataset time with such things as:

a) The strength of the uptrend or downtrend.

b) The length of the uptrend or downtrend.

c) The overall performance of the stock leading into the dataset time period

And that is the indicator in a nutshell.

Hopefully you find it helpful and interesting. Feel free to leave questions, comments and suggestions below.

Safe trades everyone and take care!

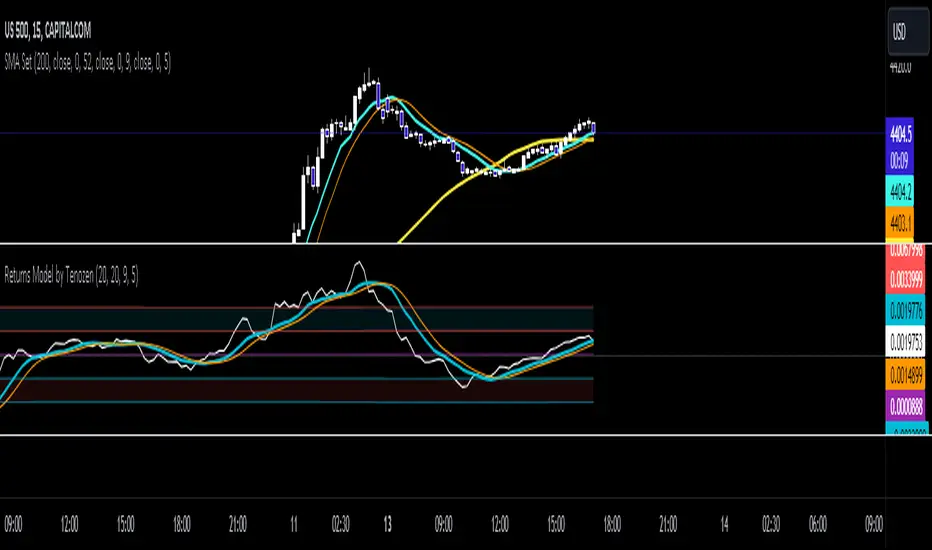

Returns Model by TenozenHey there! I've been diving into the book "Paul Wilmott on Quantitative Finance," and I stumbled upon this cool model for calculating and modeling returns. Basically, it helps us figure out how much a price has changed over a set number of periods—I like to use 20 periods as a default. Once we get that rate of change value, we crunch some numbers to find the standard deviation and mean using all the historical data we have. That's the foundation of this model.

Now, let's talk about how to use it. This model shows us how returns and price behavior are connected. When returns hang out in the +1 to +2 standard deviation range, it usually means returns are about to drop, and vice versa. Often, this leads to corresponding price moves. But here's the thing: sometimes prices don't do what we expect. Why? It's because there's another hidden factor at play—I like to call it "power."

This "power" isn't something we can see directly, but it's there. Basically, when returns are within that standard deviation range, the market faces resistance when trying to move in its preferred direction, whether bullish or bearish. The strength of this "power" determines if the market will snap back to the average or go for a wild ride. It can show up as small price wiggles, big price jumps, or lightning-fast moves. By understanding this "power," we can get a better handle on what the market might do next and avoid getting blindsided. In the meantime, I couldn't explain "power" yet, but In the future, when I've learned enough, I'd love to share the model with you guys!

So... I'm planning to explore and share more models from this book as I learn, even if those pesky math formulas can be tough to crack. I hope you find this indicator as helpful as I do, and if you've got any suggestions or feedback, please feel free to share! Ciao!

TTP PNR filterPNR filter uses the "percentile nearest rank" method to produce signals from any source including oscillator indicators and price bars.

Features:

* Length - how many candles back in time to use for calculating PNR

* % low and high - what range of the spread of values captured will form the PNR band. Use 99&100 to create a band on the 1% highest percentile or 0&1 to create a band in the lowest percentile. It accepts float numbers so you can find very rare occurrences.

* src - by default it will use the close price but PNR filter can be used with any source. It's particularly useful when working with oscillators like RSI, MACD, ADX, etc.

* Signal direction - The indicator will print 1 when the selected conditions are met. Once the PNR band is plotted you can chose from cross over, cross under, above and below conditions to trigger a signal.

* Signal source - the band consists in a % low and % high, this option allows you to pick which band will be used with the "signal direction" parameter.

Example configuration:

1) Select 200 as the length

2) Select % low 0 and % high 1

3) Add RSI to the chart and select it as the source parameter

4) Select signal direction cross over

5) Select signal source % high which corresponds to the 1% band

In this setup you are finding values of RSI that in the past 200 candles have been that low only 1% of the time. With each new candle the calculation window will move as well leaving the oldest candle out.

lib_profileLibrary "lib_profile"

a library with functions to calculate a volume profile for either a set of candles within the current chart, or a single candle from its lower timeframe security data. All you need is to feed the

method delete(this)

deletes this bucket's plot from the chart

Namespace types: Bucket

Parameters:

this (Bucket)

method delete(this)

Namespace types: Profile

Parameters:

this (Profile)

method delete(this)

Namespace types: Bucket

Parameters:

this (Bucket )

method delete(this)

Namespace types: Profile

Parameters:

this (Profile )

method update(this, top, bottom, value, fraction)

updates this bucket's data

Namespace types: Bucket

Parameters:

this (Bucket)

top (float)

bottom (float)

value (float)

fraction (float)

method update(this, tops, bottoms, values)

update this Profile's data (recalculates the whole profile and applies the result to this object) TODO optimisation to calculate this incremental to improve performance in realtime on high resolution

Namespace types: Profile

Parameters:

this (Profile)

tops (float ) : array of range top/high values (either from ltf or chart candles using history() function

bottoms (float ) : array of range bottom/low values (either from ltf or chart candles using history() function

values (float ) : array of range volume/1 values (either from ltf or chart candles using history() function (1s can be used for analysing candles in bucket/price range over time)

method tostring(this)

allows debug print of a bucket

Namespace types: Bucket

Parameters:

this (Bucket)

method draw(this, start_t, start_i, end_t, end_i, args, line_color)

allows drawing a line in a Profile, representing this bucket and it's value + it's value's fraction of the Profile total value

Namespace types: Bucket

Parameters:

this (Bucket)

start_t (int) : the time x coordinate of the line's left end (depends on the Profile box)

start_i (int) : the bar_index x coordinate of the line's left end (depends on the Profile box)

end_t (int) : the time x coordinate of the line's right end (depends on the Profile box)

end_i (int) : the bar_index x coordinate of the line's right end (depends on the Profile box)

args (LineArgs type from robbatt/lib_plot_objects/24) : the default arguments for the line style

line_color (color) : the color override for POC/VAH/VAL lines

method draw(this, forced_width)

draw all components of this Profile (Box, Background, Bucket lines, POC/VAH/VAL overlay levels and labels)

Namespace types: Profile

Parameters:

this (Profile)

forced_width (int) : allows to force width of the Profile Box, overrides the ProfileArgs.default_size and ProfileArgs.extend arguments (default: na)

method init(this)

Namespace types: ProfileArgs

Parameters:

this (ProfileArgs)

method init(this)

Namespace types: Profile

Parameters:

this (Profile)

profile(tops, bottoms, values, resolution, vah_pc, val_pc, bucket_buffer)

split a chart/parent bar into 'resolution' sections, figure out in which section the most volume/time was spent, by analysing a given set of (intra)bars' top/bottom/volume values. Then return price center of the bin with the highest volume, essentially marking the point of control / highest volume (poc) in the chart/parent bar.

Parameters:

tops (float ) : array of range top/high values (either from ltf or chart candles using history() function

bottoms (float ) : array of range bottom/low values (either from ltf or chart candles using history() function

values (float ) : array of range volume/1 values (either from ltf or chart candles using history() function (1s can be used for analysing candles in bucket/price range over time)

resolution (int) : amount of buckets/price ranges to sort the candle data into (analyse how much volume / time was spent in a certain bucket/price range) (default: 25)

vah_pc (float) : a threshold percentage (of values' total) for the top end of the value area (default: 80)

val_pc (float) : a threshold percentage (of values' total) for the bottom end of the value area (default: 20)

bucket_buffer (Bucket ) : optional buffer of empty Buckets to fill, if omitted a new one is created and returned. The buffer length must match the resolution

Returns: poc (price level), vah (price level), val (price level), poc_index (idx in buckets), vah_index (idx in buckets), val_index (idx in buckets), buckets (filled buffer or new)

create_profile(start_idx, tops, bottoms, values, resolution, vah_pc, val_pc, args)

split a chart/parent bar into 'resolution' sections, figure out in which section the most volume/time was spent, by analysing a given set of (intra)bars' top/bottom/volume values. Then return price center of the bin with the highest volume, essentially marking the point of control / highest volume (poc) in the chart/parent bar.

Parameters:

start_idx (int) : the bar_index at which the Profile should start drawing

tops (float ) : array of range top/high values (either from ltf or chart candles using history() function

bottoms (float ) : array of range bottom/low values (either from ltf or chart candles using history() function

values (float ) : array of range volume/1 values (either from ltf or chart candles using history() function (1s can be used for analysing candles in bucket/price range over time)

resolution (int) : amount of buckets/price ranges to sort the candle data into (analyse how much volume / time was spent in a certain bucket/price range) (default: 25)

vah_pc (float) : a threshold percentage (of values' total) for the top end of the value area (default: 80)

val_pc (float) : a threshold percentage (of values' total) for the bottom end of the value area (default: 20)

args (ProfileArgs)

Returns: poc (price level), vah (price level), val (price level), poc_index (idx in buckets), vah_index (idx in buckets), val_index (idx in buckets), buckets (filled buffer or new)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (int)

len (int)

offset (int)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (float)

len (int)

offset (int)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (bool)

len (int)

offset (int)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (string)

len (int)

offset (int)

Bucket

Fields:

idx (series int) : the index of this Bucket within the Profile starting with 0 for the lowest Bucket at the bottom of the Profile

value (series float) : the value of this Bucket, can be volume or time, for using time pass and array of 1s to the update function

top (series float) : the top of this Bucket's price range (for calculation)

btm (series float) : the bottom of this Bucket's price range (for calculation)

center (series float) : the center of this Bucket's price range (for plotting)

fraction (series float) : the fraction this Bucket's value is compared to the total of the Profile

plot_bucket_line (Line type from robbatt/lib_plot_objects/24) : the line that resembles this bucket and it's valeu in the Profile

ProfileArgs

Fields:

show_poc (series bool) : whether to plot a POC line across the Profile Box (default: true)

show_profile (series bool) : whether to plot a line for each Bucket in the Profile Box, indicating the value per Bucket (Price range), e.g. volume that occured in a certain time and price range (default: false)

show_va (series bool) : whether to plot a VAH/VAL line across the Profile Box (default: false)

show_va_fill (series bool) : whether to fill the 'value' area between VAH/VAL line (default: false)

show_background (series bool) : whether to fill the Profile Box with a background color (default: false)

show_labels (series bool) : whether to add labels to the right end of the POC/VAH/VAL line (default: false)

show_price_levels (series bool) : whether add price values to the labels to the right end of the POC/VAH/VAL line (default: false)

extend (series bool) : whether extend the Profile Box to the current candle (default: false)

default_size (series int) : the default min. width of the Profile Box (default: 30)

args_poc_line (LineArgs type from robbatt/lib_plot_objects/24) : arguments for the poc line plot

args_va_line (LineArgs type from robbatt/lib_plot_objects/24) : arguments for the va line plot

args_poc_label (LabelArgs type from robbatt/lib_plot_objects/24) : arguments for the poc label plot

args_va_label (LabelArgs type from robbatt/lib_plot_objects/24) : arguments for the va label plot

args_profile_line (LineArgs type from robbatt/lib_plot_objects/24) : arguments for the Bucket line plots

args_profile_bg (BoxArgs type from robbatt/lib_plot_objects/24)

va_fill_color (series color) : color for the va area fill plot

Profile

Fields:

start (series int) : left x coordinate for the Profile Box

end (series int) : right x coordinate for the Profile Box

resolution (series int) : the amount of buckets/price ranges the Profile will dissect the data into

vah_threshold_pc (series float) : the percentage of the total data value to mark the upper threshold for the main value area

val_threshold_pc (series float) : the percentage of the total data value to mark the lower threshold for the main value area

args (ProfileArgs) : the style arguments for the Profile Box

h (series float) : the highest price of the data

l (series float) : the lowest price of the data

total (series float) : the total data value (e.g. volume of all candles, or just one each to analyse candle distribution over time)

buckets (Bucket ) : the Bucket objects holding the data for each price range bucket

poc_bucket_index (series int) : the Bucket index in buckets, that holds the poc Bucket

vah_bucket_index (series int) : the Bucket index in buckets, that holds the vah Bucket

val_bucket_index (series int) : the Bucket index in buckets, that holds the val Bucket

poc (series float) : the according price level marking the Point Of Control

vah (series float) : the according price level marking the Value Area High

val (series float) : the according price level marking the Value Area Low

plot_poc (Line type from robbatt/lib_plot_objects/24)

plot_vah (Line type from robbatt/lib_plot_objects/24)

plot_val (Line type from robbatt/lib_plot_objects/24)

plot_poc_label (Label type from robbatt/lib_plot_objects/24)

plot_vah_label (Label type from robbatt/lib_plot_objects/24)

plot_val_label (Label type from robbatt/lib_plot_objects/24)

plot_va_fill (LineFill type from robbatt/lib_plot_objects/24)

plot_profile_bg (Box type from robbatt/lib_plot_objects/24)

Percentile Based Trend StrengthThe "Percentile Based Trend Strength" (PBTS) calculates trend strength based on percentile values of high and low prices for various length periods and then identifies the current trend as either Bullish, Bearish, or N/A (No Trend). Here's a step-by-step explanation of the code:

Percentile Calculations:

For each specified length period (13, 21, 34, 55, 89, and 144 - Fibonacci numbers), the code calculates the 75th percentile of high prices (e.g., percentile_13H) and the 25th percentile of low prices (e.g., percentile_13L). These percentiles represent levels that prices need to exceed or fall below to indicate a strong trend.

Calculate Highest High and Lowest Low:

The highest high (75th percentile high price of longest length) and lowest low (25th percentile low price of longest length) for the longest length period (144) are calculated as highest_high and lowest_low. These values represent threshold price levels .

Trend Strength Conditions:

The code calculates various conditions to determine trend strength. For each percentile value and each length period, it checks if the percentile value is greater than the highest high (trendBull) or less than the lowest low (trendBear). These conditions are used to assess the strength of the bullish and bearish trends.

Count Bull and Count Bear:

The countBull and countBear variables count the number of bullish and bearish conditions met, respectively. These counts help evaluate trend strength.

Weak Bull and Weak Bear Count:

The code calculates the number of weak bullish and bearish conditions. Weak conditions occur when a percentile value falls within the range defined by the highest high and lowest low but doesn't meet the strong trend criteria.

Bull Strength and Bear Strength:

bullStrength and bearStrength are calculated based on the counts of bullish, bearish, weak bullish, and weak bearish conditions. These values represent the overall strength of the bullish and bearish trends.

Strong Bull and Bear Conditions:

These conditions occur when the 75th percentile of high prices (for bull conditions) or the 25th percentile of low prices (for bear conditions) exceeds or falls below the highest high or lowest low, respectively, for the specified length period.

Strong bull conditions indicate a strong upward trend, while strong bear conditions indicate a strong downward trend.

Strong conditions are indicative of more significant price movements and are considered as primary signals of trend strength.

Weak Bull and Bear Conditions:

Weak bull and bear conditions are more nuanced. They occur when the 75th percentile of high prices (for weak bull conditions) or the 25th percentile of low prices (for weak bear conditions) falls within the range defined by the highest high and lowest low for the specified length period.

In other words, prices are not strong enough to reach the extreme levels represented by the highest high or lowest low, but they still exhibit some bullish or bearish tendencies within that range.

Weak conditions suggest a less robust trend. They may indicate that while there is some bias toward a bullish or bearish trend, it is not as strong or decisive as in the case of strong conditions.

Current Trend Identification:

The current trend is determined by comparing bullStrength and bearStrength. If bullStrength is greater, it's considered a Bull trend; if bearStrength is greater, it's a Bear trend. If they are equal, the trend is identified as N/A (No Trend).

Displaying Trend Information:

The code creates a table to display the current trend, reversal probability (strength), count of bullish and bearish conditions, weak bullish and weak bearish counts, and colors the text accordingly.

Plotting Percentiles:

Finally, the code plots the percentile lines for visualization, with 20% transparency. It also plots the highest high and lowest low lines (75th and 25th percentile of the longest length 144) using their original colors.

In summary, this indicator calculates trend strength based on percentile levels of high and low prices for different length periods. It then counts the number of bullish and bearish conditions, factors in weak conditions, and compares the strengths to identify the current trend as Bullish, Bearish, or No Trend. It provides a table with trend information and visualizes percentile lines on the chart.

Strategy Gaussian Anomaly DerivativeConcept behind this Strategy :

Considering a normal "buy/sell" situation, an asset would be bought in average at the median price following a Gaussian like concept. A higher or lower average trend would significate that the current perceived value is respectively higher or lower than the current median price, which mean that the buyers are evaluating the price underpriced or overpriced.

This behaviour would be even more relevent depending on its derivative evolution.

Therefore, this Strategy setup is based on this Gaussian like concept anomaly of average close positionning compare to high-low average derivative, such as the derivative of the following ploted basic signal : 1-(high+low)/(2*close).

This Strategy can actually be used like a trend change and continuation strength indicator aswell.

In the Setup Signal part :

You can define the filtering of the basis signal "1-(high+low)/(2*close)" on EMA or SMA as you wish.

You can define the corresponding period and the threathold as a mutiply of the average 1/3 of all time value of the basis signal.

You can define the SMA filtering period of the Derivative signal and the corresponding threathold on the same mutiply of the average 1/3 of all time value of the derivative.

In the Setup Strategy part :

You can set up your strategy assesment based on Long and/or Short. You can also define the considered period.

The most successful tuned strategies I did were based on the derivative indicator with periods on the basis signal and the derivative under 30, can be 1 to 3 of te derivative and 7 to 21 for the basis signal. The threathold depends on the asset volatility aswell, 1 is usually the most efficient but 0 to 10 can be relevent depending on the situation I met. You can find an example of tuning for this strategy based on Kering's case hereafter.

I hoping that you will enjoy using this Strategy, don't hesitate to comment, to question, to correct or complete it ! I would be very curious about similar famous approaches that would have already been made.

Thank to you !

Paytience DistributionPaytience Distribution Indicator User Guide

Overview:

The Paytience Distribution indicator is designed to visualize the distribution of any chosen data source. By default, it visualizes the distribution of a built-in Relative Strength Index (RSI). This guide provides details on its functionality and settings.

Distribution Explanation:

A distribution in statistics and data analysis represents the way values or a set of data are spread out or distributed over a range. The distribution can show where values are concentrated, values are absent or infrequent, or any other patterns. Visualizing distributions helps users understand underlying patterns and tendencies in the data.

Settings and Parameters:

Main Settings:

Window Size

- Description: This dictates the amount of data used to calculate the distribution.

- Options: A whole number (integer).

- Tooltip: A window size of 0 means it uses all the available data.

Scale

- Description: Adjusts the height of the distribution visualization.

- Options: Any integer between 20 and 499.

Round Source

- Description: Rounds the chosen data source to a specified number of decimal places.

- Options: Any whole number (integer).

Minimum Value

- Description: Specifies the minimum value you wish to account for in the distribution.

- Options: Any integer from 0 to 100.

- Tooltip: 0 being the lowest and 100 being the highest.

Smoothing

- Description: Applies a smoothing function to the distribution visualization to simplify its appearance.

- Options: Any integer between 1 and 20.

Include 0

- Description: Dictates whether zero should be included in the distribution visualization.

- Options: True (include) or False (exclude).

Standard Deviation

- Description: Enables the visualization of standard deviation, which measures the amount of variation or dispersion in the chosen data set.

- Tooltip: This is best suited for a source that has a vaguely Gaussian (bell-curved) distribution.

- Options: True (enable) or False (disable).

Color Options

- High Color and Low Color: Specifies colors for high and low data points.

- Standard Deviation Color: Designates a color for the standard deviation lines.

Example Settings:

Example Usage RSI

- Description: Enables the use of RSI as the data source.

- Options: True (enable) or False (disable).

RSI Length

- Description: Determines the period over which the RSI is calculated.

- Options: Any integer greater than 1.

Using an External Source:

To visualize the distribution of an external source:

Select the "Move to" option in the dropdown menu for the Paytience Distribution indicator on your chart.

Set it to the existing panel where your external data source is placed.

Navigate to "Pin to Scale" and pin the indicator to the same scale as your external source.

Indicator Logic and Functions:

Sinc Function: Used in signal processing, the sinc function ensures the elimination of aliasing effects.

Sinc Filter: A filtering mechanism which uses sinc function to provide estimates on the data.

Weighted Mean & Standard Deviation: These are statistical measures used to capture the central tendency and variability in the data, respectively.

Output and Visualization:

The indicator visualizes the distribution as a series of colored boxes, with the intensity of the color indicating the frequency of the data points in that range. Additionally, lines representing the standard deviation from the mean can be displayed if the "Standard Deviation" setting is enabled.

The example RSI, if enabled, is plotted along with its common threshold lines at 70 (upper) and 30 (lower).

Understanding the Paytience Distribution Indicator

1. What is a Distribution?

A distribution represents the spread of data points across different values, showing how frequently each value occurs. For instance, if you're looking at a stock's closing prices over a month, you may find that the stock closed most frequently around $100, occasionally around $105, and rarely around $110. Graphically visualizing this distribution can help you see the central tendencies, variability, and shape of your data distribution. This visualization can be essential in determining key trading points, understanding volatility, and getting an overview of the market sentiment.

2. The Rounding Mechanism

Every asset and dataset is unique. Some assets, especially cryptocurrencies or forex pairs, might have values that go up to many decimal places. Rounding these values is essential to generate a more readable and manageable distribution.

Why is Rounding Needed? If every unique value from a high-precision dataset was treated distinctly, the resulting distribution would be sparse and less informative. By rounding off, the values are grouped, making the distribution more consolidated and understandable.

Adjusting Rounding: The `Round Source` input allows users to determine the number of decimal places they'd like to consider. If you're working with an asset with many decimal places, adjust this setting to get a meaningful distribution. If the rounding is set too low for high precision assets, the distribution could lose its utility.

3. Standard Deviation and Oscillators

Standard deviation is a measure of the amount of variation or dispersion of a set of values. In the context of this indicator:

Use with Oscillators: When using oscillators like RSI, the standard deviation can provide insights into the oscillator's range. This means you can determine how much the oscillator typically deviates from its average value.

Setting Bounds: By understanding this deviation, traders can better set reasonable upper and lower bounds, identifying overbought or oversold conditions in relation to the oscillator's historical behavior.

4. Resampling

Resampling is the process of adjusting the time frame or value buckets of your data. In the context of this indicator, resampling ensures that the distribution is manageable and visually informative.

Resample Size vs. Window Size: The `Resample Resolution` dictates the number of bins or buckets the distribution will be divided into. On the other hand, the `Window Size` determines how much of the recent data will be considered. It's crucial to ensure that the resample size is smaller than the window size, or else the distribution will not accurately reflect the data's behavior.

Why Use Resampling? Especially for price-based sources, setting the window size around 500 (instead of 0) ensures that the distribution doesn't become too overloaded with data. When set to 0, the window size uses all available data, which may not always provide an actionable insight.

5. Uneven Sample Bins and Gaps

You might notice that the width of sample bins in the distribution is not uniform, and there can be gaps.

Reason for Uneven Widths: This happens because the indicator uses a 'resampled' distribution. The width represents the range of values in each bin, which might not be constant across bins. Some value ranges might have more data points, while others might have fewer.

Gaps in Distribution: Sometimes, there might be no data points in certain value ranges, leading to gaps in the distribution. These gaps are not flaws but indicate ranges where no values were observed.

In conclusion, the Paytience Distribution indicator offers a robust mechanism to visualize the distribution of data from various sources. By understanding its intricacies, users can make better-informed trading decisions based on the distribution and behavior of their chosen data source.

Bursa Malaysia Index SeriesBursa Malaysia Index Series. The index computation is as follows:-

Current aggregate Market Capitalisation/Base Aggregate Market Capitalisation x 100.

The Bursa Malaysia Index Series is calculated and disseminated on a real-time basis at 60-second intervals during Bursa’s trading hours.

Label_Trades Enter your trade information to display on chartThis indicator is an overlay for your main chart. It will display your trade entry and trade close positions on your chart.

After you place the indicator on you shart you will need to enter the trade information that you want to display.

You can open thte input setting by clicking on the gear sprocket that appears when you hover your mouse over the indicator name. There are 7 seting you will want to fill in.

Date and Time Bought

Date and Time Sold

Trade Lot Size

Select whether the trades was 'long' or 'short'

The price for buying the Trade

The price for selling the Trade

On the third tab

The code is straightforward. Using a conditional based on whtehr the trade was 'long' or 'short' determines where the labels will be placed and whether they show a long trade or short trade. It also displays a tool tip when you hover over the label. The tooltip will display the number of lots bought or sold and the price.

The lable.new() function is the meat of the indicator. I will go over a line to explainthe options available.

Pinscript manual(www.tradingview.com)

The function parameters can be called out as in the example above or the values can be placed comma seperated. If you do the latter you must enter the parameters in order. I like anming the parameters as I place them so I can easily see what I did.

label.new(

x=t_bot, // x is the time the transaction occured

y=na, // y is the for the y-axis it is not used here so 'na' tells pinescript to ignore the parameter

xloc=xloc.bar_time, // x_loc is specifying that x is a time value

yloc=yloc.belowbar, // y-loc specifies to place the label under the bar. There are other locations to use. See language reference ((www.tradingview.com)

style=label.style_triangleup, // This parameter selects the lable style. There are many other style to use, see the manual.

color=color.green, // the Label fill color

size=size.small, // the label size

tooltip=str.tostring(lot_size) + " lots bought at $" + str.tostring(bot_val)) // Some parameters are tricky. This one needs to be a string but we are using an integer value(lot_size) and a float value(bol_val). They are all concatenated via the "+" sign. In oorder to do this the numeric values need to be cast or converted into strings. The string function str.tostring() does this.

Z-Score Based Momentum Zones with Advanced Volatility ChannelsThe indicator "Z-Score Based Momentum Zones with Advanced Volatility Channels" combines various technical analysis components, including volatility, price changes, and volume correction, to calculate Z-Scores and determine momentum zones and provide a visual representation of price movements and volatility based on multi timeframe highest high and lowest low values.

Note: THIS IS A IMPROVEMNT OF "Multi Time Frame Composite Bands" INDICATOR OF MINE WITH MORE EMPHASIS ON MOMENTUM ZONES CALULATED BASED ON Z-SCORES

Input Options

look_back_length: This input specifies the look-back period for calculating intraday volatility. correction It is set to a default value of 5.

lookback_period: This input sets the look-back period for calculating relative price change. The default value is 5.

zscore_period: This input determines the look-back period for calculating the Z-Score. The default value is 500.

avgZscore_length: This input defines the length of the momentum block used in calculations, with a default value of 14.

include_vc: This is a boolean input that, if set to true, enables volume correction in the calculations. By default, it is set to false.

1. Volatility Bands (Composite High and Low):

Composite High and Low: These are calculated by combining different moving averages of the high prices (high) and low prices (low). Specifically:

a_high and a_low are calculated as the average of the highest (ta.highest) and lowest (ta.lowest) high and low prices over various look-back periods (5, 8, 13, 21, 34) to capture short and long-term trends.

b_high and b_low are calculated as the simple moving average (SMA) of the high and low prices over different look-back periods (5, 8, 13) to smooth out the trends.

high_c and low_c are obtained by averaging a_high with b_high and a_low with b_low respectively.

IDV Correction Calulation : In this script the Intraday Volatility (IDV) is calculated as the simple moving average (SMA) of the daily high-low price range divided by the closing price. This measures how much the price fluctuates in a given period.

Composite High and Low with Volatility: The final c_high and c_low values are obtained by adjusting high_c and low_c with the calculated intraday volatility (IDV). These values are used to create the "Composite High" and "Composite Low" plots.

Composite High and Low with Volatility Correction: The final c_high and c_low values are obtained by adjusting high_c and low_c with the calculated intraday volatility (IDV). These values are used to create the "Composite High" and "Composite Low" plots.

2. Momentum Blocks Based on Z-Score:

Relative Price Change (RPC):

The Relative Price Change (rpdev) is calculated as the difference between the current high-low-close average (hlc3) and the previous simple moving average (psma_hlc3) of the same quantity. This measures the change in price over time.

Additionally, std_hlc3 is calculated as the standard deviation of the hlc3 values over a specified look-back period. The standard deviation quantifies the dispersion or volatility in the price data.

The rpdev is then divided by the std_hlc3 to normalize the price change by the volatility. This normalization ensures that the price change is expressed in terms of standard deviations, which is a common practice in quantitative analysis.

Essentially, the rpdev represents how many standard deviations the current price is away from the previous moving average.

Volume Correction (VC): If the include_vc input is set to true, volume correction is applied by dividing the trading volume by the previous simple moving average of the volume (psma_volume). This accounts for changes in trading activity.

Volume Corrected Relative Price Change (VCRPD): The vcrpd is calculated by multiplying the rpdev by the volume correction factor (vc). This incorporates both price changes and volume data.

Z-Scores: The Z-scores are calculated by taking the difference between the vcrpd and the mean (mean_vcrpd) and then dividing it by the standard deviation (stddev_vcrpd). Z-scores measure how many standard deviations a value is away from the mean. They help identify whether a value is unusually high or low compared to its historical distribution.

Momentum Blocks: The "Momentum Blocks" are essentially derived from the Z-scores (avgZScore). The script assigns different colors to the "Fill Area" based on predefined Z-score ranges. These colored areas represent different momentum zones:

Positive Z-scores indicate bullish momentum, and different shades of green are used to fill the area.

Negative Z-scores indicate bearish momentum, and different shades of red are used.

Z-scores near zero (between -0.25 and 0.25) suggest neutrality, and a yellow color is used.

Robust Bollinger Bands with Trend StrengthThe "Robust Bollinger Bands with Trend Strength" indicator is a technical analysis tool designed assess price volatility, identify potential trading opportunities, and gauge trend strength. It combines several robust statistical methods and percentile-based calculations to provide valuable information about price movements with Improved Resilience to Noise while mitigating the impact of outliers and non-normality in price data.

Here's a breakdown of how this indicator works and the information it provides:

Bollinger Bands Calculation: Similar to traditional Bollinger Bands, this indicator calculates the upper and lower bands that envelop the median (centerline) of the price data. These bands represent the potential upper and lower boundaries of price movements.

Robust Statistics: Instead of using standard deviation, this indicator employs robust statistical measures to calculate the bands (spread). Specifically, it uses the Interquartile Range (IQR), which is the range between the 25th percentile (low price) and the 75th percentile (high price). Robust statistics are less affected by extreme values (outliers) and data distributions that may not be perfectly normal. This makes the bands more resistant to unusual price spikes.

Median as Centerline: The indicator utilizes the median of the chosen price source (either HLC3 or VWMA) as the central reference point for the bands. The median is less affected by outliers than the mean (average), making it a robust choice. This can help identify the center of price action, which is useful for understanding whether prices are trending or ranging.

Trend Strength Assessment: The indicator goes beyond the standard Bollinger Bands by incorporating a measure of trend strength. It uses a robust rank-based correlation coefficient to assess the relationship between the price source and the bar index (time). This correlation coefficient, calculated over a specified length, helps determine whether a trend is strong, positive (uptrend), negative (down trend), or non-existent and weak. When the rank-based correlation coefficient shifts it indicates exhaustion of a prevailing trend. Trend Strength" indicator is designed to provide statistically valid information about trend strength while minimizing the impact of outliers and data distribution characteristics. The parameter choices, including a length of 14 and a correlation threshold of +/-0.7, considered to offer meaningful insights into market conditions and statistical validity (p-value ,0.05 statistically significant). The use of rank-based correlation is a robust alternative to traditional Pearson correlation, especially in the context of financial markets.

Trend Fill: Based on the robust rank-based correlation coefficient, the indicator fills the area between the upper and lower Bollinger Bands with different colors to visually represent the trend strength. For example, it may use green for an uptrend, red for a down trend, and a neutral color for a weak or ranging market. This visual representation can help traders quickly identify potential trend opportunities. In addition the middle line also informs about the overall trend direction of the median.

Cross Correlation [Kioseff Trading]Hello!

This script "Cross Correlation" calculates up to ~10,000 lag-symbol pair cross correlation values simultaneously!

Cross correlation calculation for 20 symbols simultaneously

+/- Lag Range is theoretically infinite (configurable min/max)

Practically, calculate up to 10000 lag-symbol pairs

Results can be sorted by greatest absolute difference or greatest sum

Ability to "isolate" the symbol on your chart and check for cross correlation against a list of symbols

Script defaults to stock pairs when on a stock, Forex pairs when on a Forex pair, crypto when on a crypto coin, futures when on a futures contract.

A custom symbol list can be used for cross correlation checking

Can check any number of available historical data points for cross correlation

Practical Assessment

Ideally, we can calculate cross correlation to determine if, in a list of assets, any of the assets frequently lead or lag one another.

Example

Say we are comparing the log returns for the previous 10 days for SPY and XLU.

*A single time-interval corresponds to the timeframe of your chart i.e. 1-minute chart = 1-minute time interval. We're using days for this example.

(Example Results)

A lag value (k) +/-3 is used.

The cross correlation (normalized) for k = +3 is -0.787

The cross correlation (normalized) for k = -3 is 0.216

A positive "k" value indicates the correlation when Asset A (SPY) leads Asset B (XLU)

A negative "k" value indicates the correlation when Asset B (XLU) leads Asset A (SPY)

A normalized cross correlation of -0.787 for k = +3 indicates an "adequately strong" negative relationship when SPY leads XLU by 3 days.

When SPY increases or decreases - XLU frequently moves in the opposite direction 3 days later.

A cross correlation value of 0.216 at k = −3 indicates a "weak" positive correlation when XLU leads SPY by 3 days.

There's a slight tendency for SPY to move in the same direction as XLU 3 days later.

After the cross-correlation score is normalized it will fall between -1 and 1.

A cross-correlation score of 1 indicates a perfect directional relationship between asset A and asset B at the corresponding lag (k).

A cross correlation of -1 indicates a perfect inverse relationship between asset A and asset B at the corresponding lag (k).

A cross correlation of 0 indicates no correlation at the corresponding lag (k).

The image above shows the primary usage for the script!

The image above further explains the data points located in the table!

The image above shows the script "isolating" the symbol on my chart and checking the cross correlation between the symbol and a list of symbols!

Wrapping Up

With this information, hopefully you can find some meaningful lead-lag relationships amongst assets!

Thank you for checking this out (:

Z-Score Support & Resistance [SS}Hello everyone,

This is the Z-Score Support and Resistance (S/R) indicator.

How it works:

The trouble with most indicators and strategies that rely on distributions is that they are constantly moving targets.

To combat this, what I have done is anchored the assessment of the normal distribution to the period open price and dropped the data from the current day.

This provides us with a static assessment of the current distribution and static target levels.

It then plots out an assessment of what would be neutral (0 Standard Deviations) all the way up to +3 Standard Deviations and all the way down to -3 Standard Deviations.

It can plot out this assessment on any timeframe, from the minutes to the months to the years, simply select which desired timeframe you want in the settings menu (default is 9 which seems to work well for most generic tickers and indicies).

The indicator will also count the number of times a ticker has closed within each designated period. To do this, please make sure that you have the assessment timeframe opened on the chart. So if you want to look at the instances on the daily timeframe, ensure you have the daily timeframe opened. If you want to look on the monthly, ensure you have the monthly opened, etc. (See below):

How to Use:

To use the indicator, its pretty simple.

Simply select the desired timeframe you want to use as S/R and use it!

You can adjust the period lookback from the defaulted 9 period based on:

a) The degree of normality in the dataset (you can use a kurtosis indicator to help you ascertain this); or

b) The back-test results of closes within a desired range.

For the later, you can see an example below:

This is TSLA with a 9 period lookback:

We can see that 50% of closes are happening within 0.5 and -0.5 standard deviations. If we extend this to a 15 period lookback:

Now over 60% of closes are happening in this area.

Why does this matter? Well, because now we know our prime short and long entries (see below):

The green arrows represent prime long setups and the red prime short setups.

This is because we know, 61% of the time the ticker will close between 0.5 and -0.5 standard deviations, so we can trade the ticker back to this area.

Further instructions:

Because it is somewhat of a complex indicator, I have done a tutorial video that I will link below here:

And that is the indicator my friends! Hopefully you enjoy :-).

As always, leave your comments and suggestions / Questions below!

Safe trades!

VWMA/SMA Delta Volatility (Statistical Anomaly Detector)The "VWMA/SMA Delta Volatility (Statistical Anomaly Detector)" indicator is a tool designed to detect and visualize volatility in a financial market's price data. The indicator calculates the difference (delta) between two moving averages (VWMA/SMA) and uses statistical analysis to identify anomalies or extreme price movements. Here's a breakdown of its components:

Hypothesis:

The hypothesis behind this indicator is that extreme price movements or anomalies in the market can be detected by analyzing the difference between two moving averages and comparing it to a statistically derived normal distribution. When the MA delta (the difference between two MAs: VWMA/SMA) exceeds a certain threshold based on standard deviation and the Z-score coefficient, it may indicate increased market volatility or potential trading opportunities.

Calculation of MA Delta:

The indicator calculates the MA delta by subtracting a simple moving average (SMA) from a volume-weighted moving average (VWMA) of a selected price source. This calculation represents the difference in the market's short-term and long-term trends.

Statistical Analysis:

To detect anomalies, the indicator performs statistical analysis on the MA delta. It calculates a moving average (MA) of the MA delta and its standard deviation over a specified sample size. This MA acts as a baseline, and the standard deviation is used to measure how much the MA delta deviates from the mean.

Delta Normalization:

The MA delta, lower filter, and upper filter are normalized using a function that scales them to a specific range, typically from -100 to 100. Normalization helps in comparing these values on a consistent scale and enhances their visual representation.

Visual Representation:

The indicator visualizes the results through histograms and channels:

The histogram bars represent the normalized MA delta. Red bars indicate negative and below-lower-filter values, green bars indicate positive and above-upper-filter values, and silver bars indicate values within the normal range.

It also displays a Z-score channel, which represents the upper and lower filters after normalization. This channel helps traders identify price levels that are statistically significant and potentially indicative of market volatility.

In summary, the "MA Delta Volatility (Statistical Anomaly Detector)" indicator aims to help traders identify abnormal price movements in the market by analyzing the difference between two moving averages and applying statistical measures. It can be a valuable tool for traders looking to spot potential opportunities during periods of increased volatility or to identify potential market anomalies.

Trade Warehouse (SPOT trades)Hello there!

Let's imagine You are trading SPOT, buy more and more every new dump, but bear market is not going to stop... and your first trade was 3 YEARS AGO!!!

Can't believe it is true.

The problem is - exchanges allow You to see only new trades last 6 months(Binance). But I want to see all of them! How do I know AVG Price?

This script is my solution. Just use it to track and store your trade, so You can see AVG without uploading old trades everytime and using calculator.

Script description:

Here You can see the "Trade" type of variable. Python script using Pandas converts trades from .csv file into string type that You can input as trade(price, pair, amount, date..). After it uppends to the trades_array and pushed into the loop.

If trade date is more than current cundle - it pushes new trade to other arrays such a "pair", "avg_tot" etc. to comput it later.

If trade was buy - it increase invested capital and owned amount, opposite for sell and recomputs AVG price.

Since script has at least 1 trade it starts to plot AVG price.

There are 2 AVG price:

1. For total invested counting(You can get negative value if traded successful)

2. Current AVG price since last 0 currency amount(there is dust value to set how many usd we take as dust)

Table represents all assets statistics

Just upload your trades only 1 time, use script to convert it into pine code, and use as indicator. This script allow You to see ALL trades from oldest to the newest.

github.com/Arivadis/...w_Tradings_warehouse

If this script helped You - press Star (on GitHub) Like (on TradingView)

Warning -

Does not include free/earn/withdraw/deposit counting. Only Buy and Sell =>

This script has no idea about your side currency deposits, so if You got Your BTC or EUR or .. from another wallet and sold later - it can break your statistical data. Add this transfer manually(see examples inside script).

Use my github manual to get this script workin.

Installing takes around 3 minutes and contains 3-5 steps

[GTH decimals heatmap] (wide screen advised)Preface

I share my personal general view on indicators below; skip ahead to the Description below if you are not interested.

It is my personal conviction that most - if not all - indicators rely mainly on trader's belief that they work, and in a feedback system like free markets they might become a self-fulfilling prophecy as a result, if (!) a big part of the traders believes in it, because some famous trader releases an indicator, or such person's public statement goes viral.

One of those voodoo indicators is the famous "follow-through day". There is zero statistical evidence for its validity, beyond the validity of a statement like "If it's bright at day it's usually the sun shining". The uselessness was proven exactly on its inventor's YT channel, Investors Business Daily. According to the examiner, its inventor William J. O'Neil himself could not explain the values used for this indicator. It might have been an incidental observation at some point without general validity. A.k.a "curve fitting". Still, it's being used by many today.

Another one of those indicators is the three points reversal on the S&P 500 Volatility Index (VIX) which allegedly might potentially maybe indicate a possible shift in trend. Both indicators share an immediately problematic feature: They use absolute values. Nothing is ever absolute in a highly subjective and emotionally driven game like the markets where a lot of money can be made and lost.

Most indicators can not produce additional information since they can only re-pack price/volume action. Many times an interpretion of the distance between price and a moving average and/or the slope of a moving average deliver very similar - if not better - results than MACD, RSI etc., especially with standard settings, the origin of which are usually unknown (always a warning sign). Very few indicators can deliver information which is otherwise hard to quantify, e. g. market noise (Kaufman's Efficiency Ratio or Price Density) or volatility, standard deviation etc.

It is common knowledge that trading the markets is a game of probability. No indicator works all the time (or at all, see above). In order to make decisions based on any indicator, the probability for its validity and the conditions under which validity seemed to have occurred, must be known. Otherwise it is just coffee grounds reading under the illusion of adding to the edge, when in fact it is only adding to the trees, making it even harder to see the forest.

Description

A common belief is that whole or half-dollar prices tend to be attraction points in price action, so a number of traders include those into decision making. But are they really...?

Spoiler Alert:

Generally, it is safe to say that for the big majority of stocks there is very thin evidence for it. It depends vastly on the asset, the timeframe used and the market period (pre/post/main trading times). If at all, there seems to be an above random but still thin evidence for whole prices being significant attraction points. Interesting/surprising patterns are visible on many stocks/timeframes/session periods, though.

The screenshot shows TSLA, 30m timeframe, two heatmaps added. The top one shows pre/post-market data only, the bottom one main market data only. The cyan fields indicate the strongest occurrence, the dark blue fields indicate the weakest occurrence of open/high/low/close prices at the respective decimal. The red field indicates the current/last price decimal.

Clearly, TSLA displays a strong pre-market attraction for .00, followed by .33 and .67 and .50. This pattern of thirds seems to be a unique feature of TSLA. In the main trading session it is being diluted by a more random distribution.

Other interesting equities to examine:

SPY: No significant pattern on any timeframe!

META: Generally weak patterns on all timeframes, but interestingly on the 1D there is evidence for less randomness on O and H, more on L and most on C.

AAPL: 1D, foggy attraction areas around .35 and .12. Whole price is no attraction area at all! Very weak attraction around .73.

AMD: Strong pattern on D, W, M, attraction areas around 1/16th intervals. No patterns on lower timeframes.

AMZN: Significant differences between pre/post and main session. Strong 1/16th pattern below D in pre/post.

TAOP: Strong 1/5th pattern on all timeframes.

Read the tool tips and go explore!

Candle Tick SizeHello everyone!

I dont think it exists, I couldnt find it any way I searched, maybe it is part of a bigger indicator. This is a really basic code, all it does, it shows the tick/pip size of the candles forming. You can adjust on how many candles should it show. Also because the code counts the point size of the candles from high to low, you can adjust that how many ticks are in one point, like for ES and NQ 4 ticks to a point, which is the basic setting. It helps me with entrys when I calculate the contract size so my risk/reward stays pretty much the same depending on the candle size for my entrys.

Multi-Asset Performance [Spaghetti] - By LeviathanThis indicator visualizes the cumulative percentage changes or returns of 30 symbols over a given period and offers a unique set of tools and data analytics for deeper insight into the performance of different assets.

Multi Asset Performance indicator (also called “Spaghetti”) makes it easy to monitor the changes in Price, Open Interest, and On Balance Volume across multiple assets simultaneously, distinguish assets that are overperforming or underperforming, observe the relative strength of different assets or currencies, use it as a tool for identifying mean reversion opportunities and even for constructing pairs trading strategies, detect "risk-on" or "risk-off" periods, evaluate statistical relationships between assets through metrics like correlation and beta, construct hedging strategies, trade rotations and much more.

Start by selecting a time period (e.g., 1 DAY) to set the interval for when data is reset. This will provide insight into how price, open interest, and on-balance volume change over your chosen period. In the settings, asset selection is fully customizable, allowing you to create three groups of up to 30 tickers each. These tickers can be displayed in a variety of styles and colors. Additional script settings offer a range of options, including smoothing values with a Simple Moving Average (SMA), highlighting the top or bottom performers, plotting the group mean, applying heatmap/gradient coloring, generating a table with calculations like beta, correlation, and RSI, creating a profile to show asset distribution around the mean, and much more.

One of the most important script tools is the screener table, which can display:

🔸 Percentage Change (Represents the return or the percentage increase or decrease in Price/OI/OBV over the current selected period)

🔸 Beta (Represents the sensitivity or responsiveness of asset's returns to the returns of a benchmark/mean. A beta of 1 means the asset moves in tandem with the market. A beta greater than 1 indicates the asset is more volatile than the market, while a beta less than 1 indicates the asset is less volatile. For example, a beta of 1.5 means the asset typically moves 150% as much as the benchmark. If the benchmark goes up 1%, the asset is expected to go up 1.5%, and vice versa.)

🔸 Correlation (Describes the strength and direction of a linear relationship between the asset and the mean. Correlation coefficients range from -1 to +1. A correlation of +1 means that two variables are perfectly positively correlated; as one goes up, the other will go up in exact proportion. A correlation of -1 means they are perfectly negatively correlated; as one goes up, the other will go down in exact proportion. A correlation of 0 means that there is no linear relationship between the variables. For example, a correlation of 0.5 between Asset A and Asset B would suggest that when Asset A moves, Asset B tends to move in the same direction, but not perfectly in tandem.)

🔸 RSI (Measures the speed and change of price movements and is used to identify overbought or oversold conditions of each asset. The RSI ranges from 0 to 100 and is typically used with a time period of 14. Generally, an RSI above 70 indicates that an asset may be overbought, while RSI below 30 signals that an asset may be oversold.)

⚙️ Settings Overview:

◽️ Period

Periodic inputs (e.g. daily, monthly, etc.) determine when the values are reset to zero and begin accumulating again until the period is over. This visualizes the net change in the data over each period. The input "Visible Range" is auto-adjustable as it starts the accumulation at the leftmost bar on your chart, displaying the net change in your chart's visible range. There's also the "Timestamp" option, which allows you to select a specific point in time from where the values are accumulated. The timestamp anchor can be dragged to a desired bar via Tradingview's interactive option. Timestamp is particularly useful when looking for outperformers/underperformers after a market-wide move. The input positioned next to the period selection determines the timeframe on which the data is based. It's best to leave it at default (Chart Timeframe) unless you want to check the higher timeframe structure of the data.

◽️ Data

The first input in this section determines the data that will be displayed. You can choose between Price, OI, and OBV. The second input lets you select which one out of the three asset groups should be displayed. The symbols in the asset group can be modified in the bottom section of the indicator settings.

◽️ Appearance

You can choose to plot the data in the form of lines, circles, areas, and columns. The colors can be selected by choosing one of the six pre-prepared color palettes.

◽️ Labeling

This input allows you to show/hide the labels and select their appearance and size. You can choose between Label (colored pointed label), Label and Line (colored pointed label with a line that connects it to the plot), or Text Label (colored text).

◽️ Smoothing

If selected, this option will smooth the values using a Simple Moving Average (SMA) with a custom length. This is used to reduce noise and improve the visibility of plotted data.

◽️ Highlight

If selected, this option will highlight the top and bottom N (custom number) plots, while shading the others. This makes the symbols with extreme values stand out from the rest.

◽️ Group Mean

This input allows you to select the data that will be considered as the group mean. You can choose between Group Average (the average value of all assets in the group) or First Ticker (the value of the ticker that is positioned first on the group's list). The mean is then used in calculations such as correlation (as the second variable) and beta (as a benchmark). You can also choose to plot the mean by clicking on the checkbox.

◽️ Profile

If selected, the script will generate a vertical volume profile-like display with 10 zones/nodes, visualizing the distribution of assets below and above the mean. This makes it easy to see how many or what percentage of assets are outperforming or underperforming the mean.

◽️ Gradient

If selected, this option will color the plots with a gradient based on the proximity of the value to the upper extreme, zero, and lower extreme.

◽️ Table

This section includes several settings for the table's appearance and the data displayed in it. The "Reference Length" input determines the number of bars back that are used for calculating correlation and beta, while "RSI Length" determines the length used for calculating the Relative Strength Index. You can choose the data that should be displayed in the table by using the checkboxes.

◽️ Asset Groups

This section allows you to modify the symbols that have been selected to be a part of the 3 asset groups. If you want to change a symbol, you can simply click on the field and type the ticker of another one. You can also show/hide a specific asset by using the checkbox next to the field.

Pro Bollinger Bands CalculatorThe "Pro Bollinger Bands Calculator" indicator joins our suite of custom trading tools, which includes the "Pro Supertrend Calculator", the "Pro RSI Calculator" and the "Pro Momentum Calculator."

Expanding on this series, the "Pro Bollinger Bands Calculator" is tailored to offer traders deeper insights into market dynamics by harnessing the power of the Bollinger Bands indicator.

Its core mission remains unchanged: to scrutinize historical price data and provide informed predictions about future price movements, with a specific focus on detecting potential bullish (green) or bearish (red) candlestick patterns.

1. Bollinger Bands Calculation:

The indicator kicks off by computing the Bollinger Bands, a well-known volatility indicator. It calculates two pivotal Bollinger Bands parameters:

- Bollinger Bands Length: This parameter sets the lookback period for Bollinger Bands calculations.

- Bollinger Bands Deviation: It determines the deviation multiplier for the upper and lower bands, typically set at 2.0.

2. Visualizing Bollinger Bands:

The Bollinger Bands derived from the calculations are skillfully plotted on the price chart:

- Red Line: Represents the upper Bollinger Band during bearish trends, suggesting potential price declines.

- Teal Line: Represents the lower Bollinger Band in bullish market conditions, signaling the possibility of price increases.

3.Analyzing Consecutive Candlesticks:

The indicator's core functionality revolves around tracking consecutive candlestick patterns based on their relationship with the Bollinger Bands lines. To be considered for analysis, a candlestick must consistently close either above (green candles) or below (red candles) the Bollinger Bands lines for multiple consecutive periods.

4. Labeling and Enumeration:

To convey the count of consecutive candles displaying consistent trend behavior, the indicator meticulously assigns labels to the price chart. The position of these labels varies depending on the direction of the trend, appearing either below (for bullish patterns) or above (for bearish patterns) the candlesticks. The label colors match the candle colors: green labels for bullish candles and red labels for bearish ones.

5. Tabular Data Presentation:

The indicator complements its graphical analysis with a customizable table that prominently displays comprehensive statistical insights. Key data points within the table encompass:

- Consecutive Candles: The count of consecutive candles displaying consistent trend characteristics.

- Candles Above Upper BB: The number of candles closing above the upper Bollinger Band during the consecutive period.

- Candles Below Lower BB: The number of candles closing below the lower Bollinger Band during the consecutive period.

- Upcoming Green Candle: An estimated probability of the next candlestick being bullish, derived from historical data.

- Upcoming Red Candle: An estimated probability of the next candlestick being bearish, also based on historical data.

6. Custom Configuration:

To cater to diverse trading strategies and preferences, the indicator offers extensive customization options. Traders can fine-tune parameters such as Bollinger Bands length, upper and lower band deviations, label and table placement, and table size to align with their unique trading approaches.

The Next Pivot [Kioseff Trading]Hello!

This script "The Next Pivot" uses various similarity measures to compare historical price sequences to the current price sequence!

Features

Find the most similar price sequence up to 100 bars from the current bar

Forecast price path up to 250 bars

Forecast ZigZag up to 250 bars

Spearmen

Pearson

Absolute Difference

Cosine Similarity

Mean Squared Error

Kendall

Forecasted linear regression channel

The image above shows/explains some of the indicator's capabilities!

The image above highlights the projected zig zag (pivots) pattern!

Colors are customizable (:

Additionally, you can plot a forecasted LinReg channel.

Should load times permit it, the script can search all bar history for a correlating sequence. This won't always be possible, contingent on the forecast length, correlation length, and the number of bars on the chart.

Reasonable Assessment

The script uses various similarity measures to find the "most similar" price sequence to what's currently happening. Once found, the subsequent price move (to the most similar sequence) is recorded and projected forward.

So,

1: Script finds most similar price sequence

2: Script takes what happened after and projects forward

While this may be useful, the projection is simply the reaction to a possible one-off "similarity" to what's currently happening. Random fluctuations are likely and, if occurring, similarities between the current price sequence and the "most similar" sequence are plausibly coincidental.