Tops & Bottoms - Day of Week Report█ OVERVIEW

The indicator tracks when the weekly tops and bottoms occur and reports the statistics by the days of the week.

█ CONCEPTS

Not all the days of the week are equal, and the market dynamic can follow through or shift over the trading week. Tops and bottoms are vital when entering a trade, as they will decide if you are catching the train or being straight offside. They are equally crucial when exiting a position, as they will determine if you are closing at the optimal price or seeing your unrealized profits vanish.

This indicator is before all for educational purposes. It aims to make the knowledge available to all traders, facilitate understanding of the various markets, and ultimately get to know your trading pairs by heart (and saving a lot of your time backtesting!).

USDJPY tops and bottoms percentages on any given week.

USDJPY tops and bottoms percentages on up weeks versus down weeks.

█ FEATURES

Custom interval

By default, the indicator uses the weekly interval defined by the symbol (e.g., Monday to Sunday). This option allows you to specify your custom interval.

Weekly interval type filter

Analyze the weekly interval on any weeks, up weeks, or down weeks.

Configurable time range filter

Select the period to report from.

█ NOTES

Trading session

The indicator analyzes the days of the week from the daily chart. The daily trading sessions are defined by the symbol (e.g., 17:00 - 17:00 on EURUSD).

Extended/electronic trading session

The indicator can include the extended hours when activated on the chart, using the 24-hour or 1440-minute timeframe.

█ HOW TO USE

Plot the indicator and navigate on the 1-day or 24-hour timeframe.

Statistics

Blockunity Level Presets (BLP)A simple tool for setting performance targets.

Level Presets (BLP) is a simple tool for setting upside and downside levels relative to the current price of any asset. In this way, you can track which price the asset needs to move towards in order to achieve a defined performance.

How to Use

This indicator is very easy to use, you can set up to 5 upward and downward targets in the parameters.

Elements

The main elements of this tool are upward (default green) and downward (default red) levels.

Settings

Several parameters can be defined in the indicator configuration.

In addition to configuring which performance value to set the level at, you can choose not to display it if you don't need it. For example, here we display only two levels:

You can also choose not to display the labels:

Also concerning labels, you can choose not to display them in currency format, but in numerical format only (for example, if you're viewing a non-USD pair, such as ETHBTC):

Finally, you can modify design elements such as colors, level widths and text size:

How it Works

Here's how upside (_u) and downside (_d) levels are calculated:

source = close

level_1_u = source + (source * (level_1 / 100))

level_1_d = math.max(source - (source * (level_1 / 100)), 0)

Inflation IndicatorThis script provides a great view of Year-over-Year (YoY) inflation rates for key countries.

The inflation data used per default are TradingView Tickers, but you can change them to anything you want from the settings.

There is no calculation in this script, all it does is providing a overview of inflation rates in a single indicator.

Inflation data for the USA, European Union, Australia, Canada, Switzerland, Japan, United Kingdom, and New Zealand (Inflation Symbols editable in the settings)

Customizable static line to indicate a specific threshold value (default: 2.0).

Table displaying country flags, names, and the latest inflation rates.

Country-representative colors for easy identification.

TimeSeriesRecurrencePlotLibrary "TimeSeriesRecurrencePlot"

In descriptive statistics and chaos theory, a recurrence plot (RP) is a plot showing, for each moment i i in time, the times at which the state of a dynamical system returns to the previous state at `i`, i.e., when the phase space trajectory visits roughly the same area in the phase space as at time `j`.

```

A recurrence plot (RP) is a graphical representation used in the analysis of time series data and dynamical systems. It visualizes recurring states or events over time by transforming the original time series into a binary matrix, where each element represents whether two consecutive points are above or below a specified threshold. The resulting Recurrence Plot Matrix reveals patterns, structures, and correlations within the data while providing insights into underlying mechanisms of complex systems.

```

~starling7b

___

Reference:

en.wikipedia.org

github.com

github.com

github.com

github.com

juliadynamics.github.io

distance_matrix(series1, series2, max_freq, norm)

Generate distance matrix between two series.

Parameters:

series1 (float) : Source series 1.

series2 (float) : Source series 2.

max_freq (int) : Maximum frequency to inpect or the size of the generated matrix.

norm (string) : Norm of the distance metric, default=`euclidean`, options=`euclidean`, `manhattan`, `max`.

Returns: Matrix with distance values.

method normalize_distance(M)

Normalizes a matrix within its Min-Max range.

Namespace types: matrix

Parameters:

M (matrix) : Source matrix.

Returns: Normalized matrix.

method threshold(M, threshold)

Updates the matrix with the condition `M(i,j) > threshold ? 1 : 0`.

Namespace types: matrix

Parameters:

M (matrix) : Source matrix.

threshold (float)

Returns: Cross matrix.

rolling_window(a, b, sample_size)

An experimental alternative method to plot a recurrence_plot.

Parameters:

a (array) : Array with data.

b (array) : Array with data.

sample_size (int)

Returns: Recurrence_plot matrix.

Test - Most correlated assetThis is a simple test to find the most and least correlated assets in a list.

TimeSeriesGrammianAngularFieldLibrary "TimeSeriesGrammianAngularField"

provides Grammian angular field and associated utility functions.

___

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

www.researchgate.net

method normalize(data, a, b)

Normalize the series to a optional range, usualy within `(-1, 1)` or `(0, 1)`.

Namespace types: array

Parameters:

data (array) : Sample data to normalize.

a (float) : Minimum target range value, `default=-1.0`.

b (float) : Minimum target range value, `default= 1.0`.

Returns: Normalized array within new range.

___

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

normalize_series(source, length, a, b)

Normalize the series to a optional range, usualy within `(-1, 1)` or `(0, 1)`.\

*Note that this may provide a different result than the array version due to rolling range*.

Parameters:

source (float) : Series to normalize.

length (int) : Number of bars to sample the range.

a (float) : Minimum target range value, `default=-1.0`.

b (float) : Minimum target range value, `default= 1.0`.

Returns: Normalized series within new range.

method polar(data)

Turns a normalized sample array into polar coordinates.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Converted array into polar coordinates.

polar_series(source)

Turns a normalized series into polar coordinates.

Parameters:

source (float) : Source series.

Returns: Converted series into polar coordinates.

method gasf(data)

Gramian Angular Summation Field *`GASF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GASF`* values.

method gasf_id(data)

Trig. identity of Gramian Angular Summation Field *`GASF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GASF`* values.

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

method gadf(data)

Gramian Angular Difference Field *`GADF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GADF`* values.

method gadf_id(data)

Trig. identity of Gramian Angular Difference Field *`GADF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GADF`* values.

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

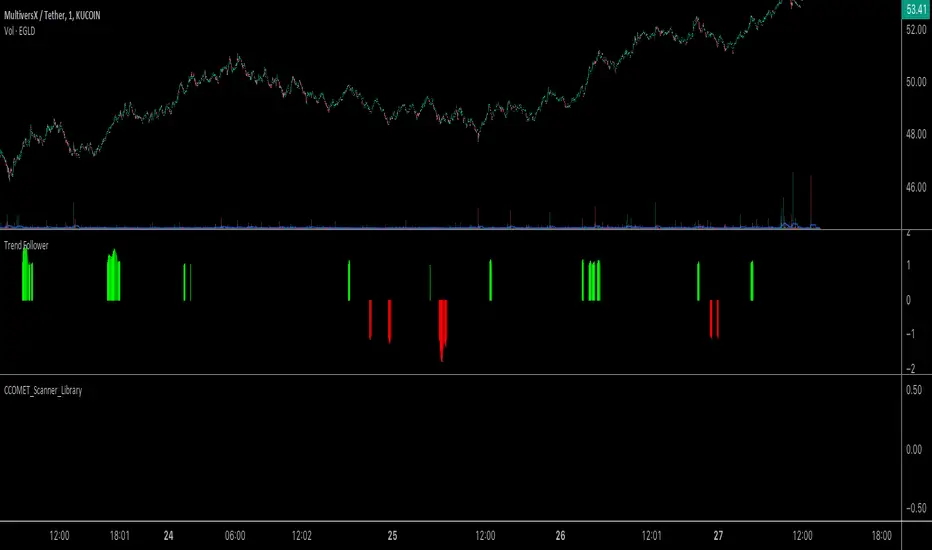

CCOMET_Scanner_LibraryLibrary "CCOMET_Scanner_Library"

- A Trader's Edge (ATE)_Library was created to assist in constructing CCOMET Scanners

Loc_tIDs_Col(_string, _firstLocation)

TickerIDs: You must form this single tickerID input string exactly as described in the scripts info panel (little gray 'i' that

is circled at the end of the settings in the settings/input panel that you can hover your cursor over this 'i' to read the

details of that particular input). IF the string is formed correctly then it will break up this single string parameter into

a total of 40 separate strings which will be all of the tickerIDs that the script is using in your CCOMET Scanner.

Locations: This function is used when there's a desire to print an assets ALERT LABELS. A set Location on the scale is assigned to each asset.

This is created so that if a lot of alerts are triggered, they will stay relatively visible and not overlap each other.

If you set your '_firstLocation' parameter as 1, since there are a max of 40 assets that can be scanned, the 1st asset's location

is assigned the value in the '_firstLocation' parameter, the 2nd asset's location is the (1st asset's location+1)...and so on.

Parameters:

_string (simple string) : (string)

A maximum of 40 Tickers (ALL joined as 1 string for the input parameter) that is formulated EXACTLY as described

within the tooltips of the TickerID inputs in my CCOMET Scanner scripts:

assets = input.text_area(tIDset1, title="TickerID (MUST READ TOOLTIP)", tooltip="Accepts 40 TICKERID's for each

copy of the script on the chart. TEXT FORMATTING RULES FOR TICKERID'S:

(1) To exclude the EXCHANGE NAME in the Labels, de-select the next input option.

(2) MUST have a space (' ') AFTER each TickerID.

(3) Capitalization in the Labels will match cap of these TickerID's.

(4) If your asset has a BaseCurrency & QuoteCurrency (ie. ADAUSDT ) BUT you ONLY want Labels

to show BaseCurrency(ie.'ADA'), include a FORWARD SLASH ('/') between the Base & Quote (ie.'ADA/USDT')", display=display.none)

_firstLocation (simple int) : (simple int)

Optional (starts at 1 if no parameter added).

Location that you want the first asset to print its label if is triggered to do so.

ie. loc2=loc1+1, loc3=loc2+1, etc.

Returns: Returns 40 output variables in the tuple (ie. between the ' ') with the TickerIDs, 40 variables for the locations for alert labels, and 40 Colors for labels/plots

TickeridForLabelsAndSecurity(_ticker, _includeExchange)

This function accepts the TickerID Name as its parameter and produces a single string that will be used in all of your labels.

Parameters:

_ticker (simple string) : (string)

For this parameter, input the varible named '_coin' from your 'f_main()' function for this parameter. It is the raw

Ticker ID name that will be processed.

_includeExchange (simple bool) : (bool)

Optional (if parameter not included in function it defaults to false ).

Used to determine if the Exchange name will be included in all labels/triggers/alerts.

Returns: ( )

Returns 2 output variables:

1st ('_securityTickerid') is to be used in the 'request.security()' function as this string will contain everything

TV needs to pull the correct assets data.

2nd ('lblTicker') is to be used in all of the labels in your CCOMET Scanner as it will only contain what you want your labels

to show as determined by how the tickerID is formulated in the CCOMET Scanner's input.

InvalID_LblSz(_barCnt, _close, _securityTickerid, _invalidArray, _tablePosition, _stackVertical, _lblSzRfrnce)

INVALID TICKERIDs: This is to add a table in the middle right of your chart that prints all the TickerID's that were either not formulated

correctly in the '_source' input or that is not a valid symbol and should be changed.

LABEL SIZES: This function sizes your Alert Trigger Labels according to the amount of Printed Bars the chart has printed within

a set time period, while also keeping in mind the smallest relative reference size you input in the 'lblSzRfrnceInput'

parameter of this function. A HIGHER % of Printed Bars(aka...more trades occurring for that asset on the exchange),

the LARGER the Name Label will print, potentially showing you the better opportunities on the exchange to avoid

exchange manipulation liquidations.

*** SHOULD NOT be used as size of labels that are your asset Name Labels next to each asset's Line Plot...

if your CCOMET Scanner includes these as you want these to be the same size for every asset so the larger ones dont cover the

smaller ones if the plots are all close to each other ***

Parameters:

_barCnt (float) : (float)

Get the 1st variable('barCnt') from the Security function's tuple and input it as this functions 1st input

parameter which will directly affect the size of the 2nd output variable ('alertTrigLabel') that is also outputted by this function.

_close (float) : (float)

Put your 'close' variable named '_close' from the security function here.

_securityTickerid (string) : (string)

Throughout the entire charts updates, if a '_close' value is never registered then the logic counts the asset as INVALID.

This will be the 1st TickerID variable (named _securityTickerid) outputted from the tuple of the TickeridForLabels()

function above this one.

_invalidArray (array) : (array string)

Input the array from the original script that houses all of the invalidArray strings.

_tablePosition (simple string) : (string)

Optional (if parameter not included, it defaults to position.middle_right). Location on the chart you want the table printed.

Possible strings include: position.top_center, position.top_left, position.top_right, position.middle_center,

position.middle_left, position.middle_right, position.bottom_center, position.bottom_left, position.bottom_right.

_stackVertical (simple bool) : (bool)

Optional (if parameter not included, it defaults to true). All of the assets that are counted as INVALID will be

created in a list. If you want this list to be prited as a column then input 'true' here, otherwise they will all be in a row.

_lblSzRfrnce (string) : (string)

Optional (if parameter not included, it defaults to size.small). This will be the size of the variable outputted

by this function named 'assetNameLabel' BUT also affects the size of the output variable 'alertTrigLabel' as it uses this parameter's size

as the smallest size for 'alertTrigLabel' then uses the '_barCnt' parameter to determine the next sizes up depending on the "_barCnt" value.

Returns: ( )

Returns 2 variables:

1st output variable ('AssetNameLabel') is assigned to the size of the 'lblSzRfrnceInput' parameter.

2nd output variable('alertTrigLabel') can be of variying sizes depending on the 'barCnt' parameter...BUT the smallest

size possible for the 2nd output variable ('alertTrigLabel') will be the size set in the 'lblSzRfrnceInput' parameter.

PrintedBarCount(_time, _barCntLength, _barCntPercentMin)

The Printed BarCount Filter looks back a User Defined amount of minutes and calculates the % of bars that have printed

out of the TOTAL amount of bars that COULD HAVE been printed within the same amount of time.

Parameters:

_time (int) : (int)

The time associated with the chart of the particular asset that is being screened at that point.

_barCntLength (int) : (int)

The amount of time (IN MINUTES) that you want the logic to look back at to calculate the % of bars that have actually

printed in the span of time you input into this parameter.

_barCntPercentMin (int) : (int)

The minimum % of Printed Bars of the asset being screened has to be GREATER than the value set in this parameter

for the output variable 'bc_gtg' to be true.

Returns: ( )

Returns 2 outputs:

1st is the % of Printed Bars that have printed within the within the span of time you input in the '_barCntLength' parameter.

2nd is true/false according to if the Printed BarCount % is above the threshold that you input into the '_barCntPercentMin' parameter.

Volume Footprint Voids [BigBeluga]Volume Footprint Voids is a unique tool that uses lower timeframe calculation to plot different styles of single candle POC.

This indicator is very powerful for scalping and finding very precise entry and exits, spotting potential trapped traders, and more.

Unlike many other volume profiles, this aims to plot single candle profiles as well as their own footprints.

🔶 FEATURES

The script includes the following settings:

Windows: Plotting style and calculations

Coloring modes

Display modes

lower-timeframe calculations

🔶 CALCULATION

In the image above we can see how the script calculates each level position that will serve as a calculation process to see how much volume/closes there are within the levels.

In the image above, we can have a more clear example of how we count each candle close.

We use the prior screenshot as an example, after setting each level we will use the lower-timeframe input to measure the amount of closes within the ranges.

Depending on the lot size, the box will be larger or smaller, usually the POC will always have the highest box size.

NOTE: Size is the starting point, always from the low of the candle.

To find more voids, select a closer LTF to the current one you're using.

To find fewer voids, select a timeframe away from your current one.

Due to Pine Script limitations, we are only able to plot a certain amount of footprints, and we can't plot the whole history chart.

POC will be the largest block displayed, indicating the time point of control

Gray areas are closes above the average

Black are Void or imbalance that price will fill in the future, like FVG

The image above shows an incorrect size input that will lead to bad calculations, while on the other side, a correct size input that will lead to a clear vision and better calculation.

🔶 WINDOWS

The "▲▼" Mode will display delta buyers and delta sellers coloring with voids as black.

It also offers a gradient mode for a beautier visualization

The "Total Volume" mode will display the net volume within the lot size (closes within the levels).

This is useful to spot possible highest net volume within the same highest lot size.

The "POC + Gaps" will show both POC and Gaps as the highest block while all the rest will be considered as the smaller block.

This is useful to see where the highest lot were and if there are higher or lower imbalances within the candle

The last option "Gaps" will simply display the gaps as the highest block, while the POC as the lowest block.

This is useful to have a better view of the gaps areas

🔶 EXAMPLE

This is one of the most basic examples of how this script can be used. POC at the bottom creating a strong support area as price holds and creates higher voids gap that price fills while rising.

🔶 SETTINGS

Users have full control over the script, from colors to choosing the lower-timeframe inputs to disabling the lot size.

Drawdown % (with SMA)This script, titled "Drawdown % (with SMA)" and designed for Pine Script version 5

offers a sophisticated tool for traders to monitor drawdown percentages, a crucial metric in assessing investment risks. The script calculates the drawdown as the percentage decrease from the all-time high value of the selected financial instrument.

Portfolio Management [TrendX_]Portfolio Management is a powerful tool that helps you create and manage your own portfolio of stocks, based on your risk and return preferences.

*** Note: You should select the appropriate index for each stock as the benchmark to compare your portfolio’s performance.

*** Note: You should apply the indicator to the same chart as the benchmark, so that it can capture the historical trends of all the 10 stocks in your portfolio.

USAGE

Analyze your portfolio’s return factor, which shows the compound annual growth rate (CAGR) of each stock and the portfolio as a whole, as well as the weight of each stock in the portfolio.

The Weighting approach contains 2 options, Equal and Growth-based method:

Customize your portfolio by selecting up to 10 stocks from a wide range of markets and sectors:

Compare your portfolio’s performance with a benchmark of your choice, which is the S&P500 by default setting.

Evaluate your portfolio’s risk factor, which includes the capital asset pricing model (CAPM), the portfolio beta, and the Sharpe ratio of both the portfolio and the benchmark:

- CAPM is a model that calculates the expected return of the portfolio based on its risk and the risk-free rate of return.

- Portfolio beta is a measure of how sensitive the portfolio is to the movements of the benchmark. A beta of 1 means the portfolio moves in sync with the benchmark, a beta of less than 1 means the portfolio is less volatile than the benchmark, and a beta of more than 1 means the portfolio is more volatile than the benchmark.

- Sharpe ratio measures how much excess return the portfolio generates per unit of risk. It is calculated by subtracting the risk-free rate of return from the portfolio’s return, and dividing by the portfolio’s standard deviation. A higher Sharpe ratio means the portfolio has a better risk-adjusted return. A Sharpe ratio of more than 1 is considered good, a Sharpe ratio of more than 2 is considered very good, and a Sharpe ratio of more than 3 is considered excellent .

Adjust your portfolio’s rebalancing strategy, which determines when and how to change the weight of each stock in the portfolio to optimize your return and risk objectives. The tool also suggests a default hedging-stock asset, which is the US dollar interpreted through the dollar index (DXY):

- The dollar index is a measure of the value of the US dollar relative to a basket of other major currencies. It is often used as a proxy for the global economic sentiment and the demand for safe-haven assets. A rising dollar index means the US dollar is strengthening, which may indicate a bearish outlook for the stock market. A falling dollar index means the US dollar is weakening, which may indicate a bullish outlook for the stock market.

- The rebalancing strategy suggest increasing the weight of the hedging-stock asset when the dollar index is under positive supertrend condition, and decreasing the weight of the hedging-stock asset when the dollar index is in the downward supertrend. This way, you can hedge against the adverse effects of the stock market fluctuations on your portfolio, simply you can just cash out at the suggested hedging weight.

CONCLUSION

Investors can gain a deeper insight into their portfolio’s performance, risk, and potential, and make informed decisions to achieve their financial goals with confidence and ease.

DISCLAIMER

The results achieved in the past are not all reliable sources of what will happen in the future. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur.

Therefore, you should always exercise caution and judgment when making decisions based on past performance.

Qullamaggie ADR and Volatility and Price Change IndicatorElevate your trading strategy with Qullamaggie ADR, a dynamic indicator inspired by the Kristjan Qullamaggie trading approach. Gain a deeper understanding of market dynamics, daily price movements, and potential turning points.

Key Features:

Qullamaggie ADR: Assess market volatility through the QullaADR, offering customizable time intervals (5, 10, 15, 20 days) to adapt to various trading styles.

Today's Change: Monitor price changes relative to the low of the current trading day, providing valuable intraday insights.

PrevDay price differentials from the previous day's low, aiding in the identification of potential trend reversals.

Track the percentage change from the opening price, offering a snapshot of intraday market sentiment.

Percent from 10-day SMA: Visualize the percentage difference between the closing price and a 10-day Simple Moving Average (SMA), a key trend-following indicator.

Usage:

Utilize QullaADR to set realistic profit targets and stop-loss levels based on current market conditions.

Identify potential trend shifts by observing changes from the previous day's low with Today's QullaChange.

Incorporate QullaPercent from 10-day SMA for trend confirmation and well-informed trading decisions.

Strategy Inspiration:

QullaADR draws inspiration from the Kristjan Qullamaggie trading strategy, aiming to complement your trading toolkit and enhance decision-making.

Disclaimer:

Trading involves risk, and past performance is not indicative of future results. Use this indicator as a supplementary tool within a comprehensive trading strategy.

Version: 1.0

Sessions [TradingFinder] New York, London, Tokyo & Sydney ForexTiming is one of the influential factors in a trader's position. This indicator categorizes transactions into three sessions (Asia, Europe, and America). Five significant trading cities (New York, London, Frankfurt, Tokyo, and Sydney) are selectable.

I recommend using the tool on a 5-minute time frame, but it is usable on all time frames.

Settings:

• Trading sessions: Display or hide each trading session as needed.

• Color: Change the color of each box.

• Session time intervals: The default is based on the main working hours for each time interval and can be adjusted.

• Information table: Delete or display additional information table.

Information Table:

• Trading sessions

• Opening and closing times of each trading session

How to Use:

Initiating trading sessions involves entering with increased liquidity, and the market usually experiences significant movements. Many trading strategies are based on "time" and "session openings." This tool empowers traders to focus intensely on each time interval.

These trading sessions are crucial for all Forex, stock, and index traders:

The total price ceiling and floor in the Asia session (Tokyo and Sydney) are crucial for traders in the European session.

The European session starts with Frankfurt, and an hour later, London begins, collectively forming the European session.

The dashboard provides additional information, displaying hours based on UTC.

Customization options are considered in all sections so that everyone can apply their own settings.

Important: Default times are the most accurate for each region, and in most indicators, this time is not correctly selected. Therefore, the level of influence and time intervals are specified at the beginning of each session. If you are using another indicator, match its default time to the announced time and share the results with me in the comments.

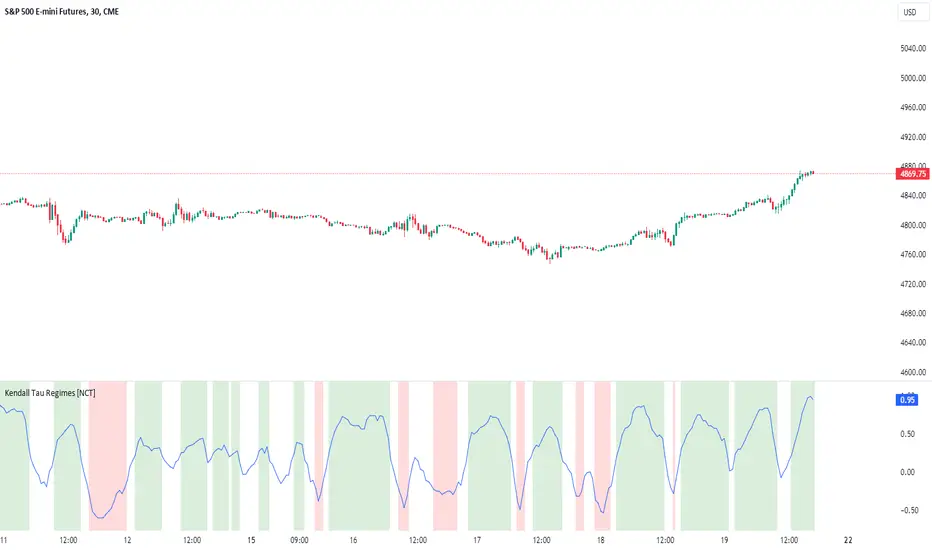

Kendall's Tau Correlation Regimes [NariCapitalTrading]The "Kendall's Tau Correlation Regimes" indicator is designed to analyze price data and determine market regimes based on Kendall's Tau correlation coefficient. It provides insight into the strength and direction of the correlation between two data series: close price and a selected moving average.

User Inputs:

Period: Defines the lookback period for calculating Kendall's Tau correlation. It can be adjusted using the input slider, with a minimum value of 1.

Threshold: Sets the threshold for identifying bullish and bearish market regimes. The user can adjust this value within the range of 0.1 to 1.0 with step increments of 0.1.

MA Type: Allows users to select the type of moving average to be used in the correlation calculation. Options include Simple Moving Average (SMA), Exponential Moving Average (EMA), and Hull Moving Average (HMA).

Kendall's Tau Correlation Calculation:

Calculates Kendall's Tau correlation coefficient between the closing price and the selected moving average.

Kendall's Tau measures the strength and direction of the ordinal association between two data series. It assesses whether the data pairs are in the same order or not.

The calculation involves counting concordant and discordant pairs of data points and then computing the coefficient.

Market Regime Identification:

Based on the threshold defined by the user, the indicator identifies two market regimes: bullish and bearish.

A regime is considered bullish when the Kendall's Tau correlation coefficient is greater than the threshold.

A regime is considered bearish when the Kendall's Tau correlation coefficient is less than the negative of the threshold.

Plotting:

The indicator plots the calculated Kendall's Tau correlation coefficient as a blue line on a separate indicator pane.

It also highlights bullish regimes with a green background and bearish regimes with a red background.

Conclusion:

The "Kendall's Tau Correlation Regimes" indicator provides traders with a visual aid for assessing market regimes based on the strength of correlation between price and a selected moving average.

Disclaimer: This indicator is for educational and informational purposes only.

Least Median of Squares Regression | ymxbThe Least Median of Squares (LMedS) is a robust statistical method predominantly used in the context of regression analysis. This technique is designed to fit a model to a dataset in a way that is resistant to outliers. Developed as an alternative to more traditional methods like Ordinary Least Squares (OLS) regression, LMedS is distinguished by its focus on minimizing the median of the squares of the residuals rather than their mean. Residuals are the differences between observed and predicted values.

The key advantage of LMedS is its robustness against outliers. In contrast to methods that minimize the mean squared residuals, the median is less influenced by extreme values, making LMedS more reliable in datasets where outliers are present. This is particularly useful in linear regression, where it identifies the line that minimizes the median of the squared residuals, ensuring that the line is not overly influenced by anomalies.

STATISTICAL PROPERTIES

A critical feature of the LMedS method is its robustness, particularly its resilience to outliers. The method boasts a high breakdown point, which is a measure of an estimator's capacity to handle outliers. In the context of LMedS, this breakdown point is approximately 50%, indicating that it can tolerate corruption of up to half of the input data points without a significant degradation in accuracy. This robustness makes LMedS particularly valuable in real-world data analysis scenarios, where outliers are common and can severely skew the results of less robust methods.

Rousseeuw, Peter J.. “Least Median of Squares Regression.” Journal of the American Statistical Association 79 (1984): 871-880.

The LMedS estimator is also characterized by its equivariance under linear transformations of the response variable. This means that whether you transform the data first and then apply LMedS, or apply LMedS first and then transform the data, the end result remains consistent. However, it's important to note that LMedS is not equivariant under affine transformations of both the predictor and response variables.

ALGORITHM

The algorithm randomly selects pairs of points, calculates the slope (m) and intercept (b) of the line, and then evaluates the median squared deviation (mr2) from this line. The line minimizing this median squared deviation is considered the best fit.

DISCLAIMER

In the LMedS approach, a subset of the data is randomly selected to compute potential models (e.g., lines in linear regression). The method then evaluates these models based on the median of the squared residuals. Since the selection of data points is random, different runs may select different subsets, leading to variability in the computed models.

Autocorrelation Candles [SS]Hey everyone, this is the Autocorrelation Candles indicator!

I have formulated it in a way that is similar to the TD 9 candle counting indicators, only instead of TD, its using a lagged autocorrelation of previous candle over a 14 period look back.

It operates similar to trend correlations (for example, my Trend Correlation Oscillator Indicator), however instead of correlating to time, it correlates to itself (autoregression). The theory being, as the autoregression correlation increases and the market becomes too "trendy", we are due for a reversal.

The indicator will display the current lagged correlation of each candle below it. When we approach a period of previous reversal, it will change the colour to orange. When we reach a very high autocorrelation (0.94 or greater), it will turn red and signal a potential reversal to the upside or downside:

Uses:

I will reference this on the larger timeframes (Daily, weekly and 4 hour) about a couple times a week or after a major trend day to see where we are.

You can use this on the smaller timeframes as well, it will work just fine.

Customizations:

I have been listening and learning my lesson, I have made the ability to customize the base text colour to black or white depending on your theme use! SO if you have white theme, you can change to black and vice versa.

As well, if you don't want labels on every candle, in the settings menu there is an option to limit the labels to a desired amount. You select the max amount and it will adjust.

You can also adjust the size of the labels between tiny, medium, and large.

Conclusion

And that's the indicator! Despite being fairly simple in concept, I have been working away on it for a bit with some logistic issues that I finally got sorted.

Hopefully, you enjoy,

Leave your questions below!

Safe trades everyone!

Advanced Volume Analytics and Distribution IndicatorThe Advanced Volume Analytics and Distribution Indicator is a sophisticated tool designed for financial analysts and traders who seek in-depth insights into market volume dynamics. This Pine Script-based indicator is a comprehensive solution, offering a rich set of features that analyze volume data using various statistical methods and theories. It's tailored for those who require a deeper understanding of market movements and volume distribution.

Key Features:

Volume Distribution Analysis: Utilizes standard deviation and mean calculations to analyze the distribution of trading volume. Employs z-scores to measure the standard deviations of volume from its mean, offering insights into volume anomalies.

Bell Curve Modeling: Constructs a bell curve (normal distribution) based on volume data, enabling users to visualize and assess the distribution of volume in a standard statistical format.

Provides a z-score based bell curve, offering a normalized view of volume deviations.

Exponential Smoothing: Applies exponential smoothing to volume data, giving more weight to recent observations. This feature is crucial for analyzing trending behaviors in volume data.

Stress Metric Calculation: Introduces a unique 'stress' metric, calculated using a custom formula. This metric is designed to evaluate the volatility or variability in the volume data over a specified period.

Central Limit Theorem (CLT) Mean Estimation: Implements CLT for estimating the mean of volume data. The CLT states that the distribution of sample means approximates a normal distribution as the sample size becomes larger.

Variance Point Estimation: Calculates the variance of volume data, providing insights into its variability and consistency over time.

Chi-Squared Test (Commented): Although not active in the initial release, the script includes a framework for a Chi-Squared Test to compare observed and expected volume frequencies, offering potential for future statistical comparisons.

Percentile Calculations and Convolution: Performs percentile calculations on volume data and employs convolution to these percentiles, enabling a more nuanced analysis of volume distribution.

Customizability: Users can input various parameters like anchor period, degrees of freedom, and smoothing preferences, making the tool adaptable to different analysis needs.

Visualization and Plotting: Features multiple plots for easy visualization of volume metrics, including stress, bell curves, point estimators, and smoothed data.

Theoretical Foundations:

This indicator is grounded in established statistical theories and methods, including the Central Limit Theorem, Chi-Squared Test (for future implementations), and convolution techniques. These foundations ensure that the indicator not only provides practical insights but also maintains a high standard of statistical rigor.

Intended Users:

This indicator is ideal for technical analysts, traders, and financial professionals who require a deep and statistically sound understanding of market volume behavior.

Release Notes:

This tool is designed a theoretical test of established statistical models and requires familiarity with Pine Script for customization. Future updates may include activation and expansion of the Chi-Squared Test functionality and additional statistical modules based on user feedback. It should be noted that it is advisable to use a logarithmic-inverted scale; when combined, these scales can provide a unique perspective that neither could offer alone. This combination might be particularly useful in highlighting exponential growth or decay trends, or in cases where the most significant data points are in the lower range of the dataset.

Notes of Stress Calculations:

The "stress metric" in the script is a custom-designed feature intended to measure the level of variability or volatility in the volume data over a given time period. This metric is calculated using a novel approach with concepts similar to those used in the field of engineering , particularly in stress analysis and finite element analysis (FEA).

Segmentation of Time Frame:

The script divides the given time frame (timeFrame) into smaller segments based on a specified number of units (units). This segmentation essentially breaks down the entire period into smaller, more manageable intervals for analysis. For each segment, the script calculates a 'stress' value. This involves iterating through each segment and performing calculations based on the source data (src), the default src is the volume data.

Calculation per Segment:

For each segment, the script identifies two points: the starting point (x1) and the ending point (x2). It then retrieves the corresponding values of the source data at these points (y1 and y2).

It calculates the difference in the x-axis (delta_x, the length of the segment) and the difference in the y-axis (delta_y, the change in volume over that segment).

Stress Calculation:

The script then calculates the 'stress' for each segment as the ratio of delta_y to delta_x. This ratio gives a measure of how much the volume has changed per unit of time within each segment. The stress values for each segment are then summed up to provide a cumulative measure of stress over the entire time frame.

The stress metric is essentially a measure of the volatility or variability in volume data. High stress values indicate larger changes in volume over shorter periods, suggesting more volatile market conditions. For traders and analysts, understanding the level of volatility is crucial. It can inform decision-making processes, risk management strategies, and provide insights into market sentiment. By comparing stress levels across different time frames or different securities, analysts can gain insights into relative market dynamics.

Blockunity Drawdown Visualizer (BDV)Monitor the drawdown (value of the drop between the highest and lowest points) of assets and act accordingly to reduce your risk.

Introducing BDV, the incredibly intuitive metric that visualizes asset drawdowns in the most visually appealing manner. With its color gradient display, BDV allows you to instantly grasp the state of retracement from the asset’s highest price level. But that’s not all – you have the option to display the oscillator’s colorization directly on your chart, enhancing your analysis even further.

The Idea

The goal is to provide the community with the best and most complete tool for visualizing the Drawdown of any asset.

How to Use

Very simple to use, the indicator takes the form of an oscillator, with colors ranging from red to green depending on the Drawdown level. A table summarizes several key data points.

Elements

On the oscillator, you'll find a line with a color gradient showing the asset's Drawdown. The flatter line represents the Max Drawdown (the lowest value reached).

In addition, the table summarizes several data:

The asset's All Time High (ATH).

Current Drawdown.

The Max Drawdown that has been reached.

Settings

First of all, you can activate a "Bar Color" in the settings (You must also uncheck "Borders" and "Wick" in your Chart Settings):

You can display Fibonacci levels on the oscillator. You'll see that levels can be relevant to drawdown. The color of the levels is also configurable.

In the calculation parameters, you can first choose between taking the High of the candles or the Close. By default this is Close, but if you change the parameter to High, the indication next to ATH in the table will change, and you'll see that the values in the table will be affected.

The second calculation parameter (Start Date) lets you modify the effective start date of the ATH, which will affect the drawdown level. Here's an example:

How it Works

First, we calculate the ATH:

var bdv_top = bdv_source

bdv_top := na(bdv_top ) ? bdv_source : math.max(bdv_source, bdv_top )

Then the drawdown is calculated as follows:

bdv = ((bdv_source / bdv_top) * 100) - 100

Then the max drawdown :

bdv_max = bdv

bdv_max := na(bdv_max ) ? bdv : math.min(bdv, bdv_max )

Hodl Calculation v1.0I have developed an indicator that calculates the value of our currency if we had periodically bought any stock or cryptocurrency on any exchange. I believe many individuals would be interested in computing such values.

You can customize the start and end times, choose the amount of currency to be used for each deal, and select from two frequency options.

The first option involves specific intervals, such as hourly, every three days, or bi-weekly.

The second option allows purchases at specific dates or times, like every 15th of the month at 12:00 PM, every Monday at 11:00 AM, or every day at 6:00 AM.

After selecting the frequency, the indicator performs calculations and presents statistical information in a table.

The summarized data includes frequency value, total selected period duration, number of deals, total quantity, total cost, current value, and profit/loss status.

IBIT Premium to CoinbaseThe BTC ETF premium indicator for TradingView is a specialized tool designed to measure and visualize the premium or discount of the iShares Bitcoin Trust (IBIT), an investment vehicle that holds Bitcoin, relative to the actual price of Bitcoin on the Coinbase exchange. This indicator can be particularly insightful for traders interested in the BTC securities market and those analyzing the demand for Bitcoin as reflected by institutional investment products.

#### Description:

The BTC ETF premium indicator in TradingView leverages an advanced Pine Script algorithm to calculate the premium (or discount) percentage of IBIT compared to the spot price of Bitcoin (BTC/USD) on Coinbase. The premium is a critical insight that reflects market sentiment and potentially arbitrage opportunities between the trust's share price and the underlying cryptocurrency asset.

Here's how the indicator works:

1. **Calculation Methodology:**

- **Implied Bitcoin Price of IBIT:** We determine the implied price of Bitcoin within IBIT by dividing the IBIT closing price by the known ratio of Bitcoin per share.

- **IBIT Premium to Coinbase:** The percentage premium is then calculated as:

$$\text{IBIT Premium} = \frac{(\text{Implied Bitcoin Price of IBIT } - \text{Actual Bitcoin Price on Coinbase})}{\text{Actual Bitcoin Price on Coinbase}} \times 100$$

- This calculation is performed using the closing prices on a per-minute basis to ensure timely and accurate analysis.

2. **Visualization:** The indicator plots the premium as a step line chart, making it easy to visualize changes over time. A dynamic label accompanies the plot, displaying the implied Bitcoin price, the actual percentage premium or discount, and whether the premium is trending up or down compared to the previous day's value.

3. **Usage Scenario:** Traders can use this indicator to monitor the live premium 24/7 and analyze how it behaves during different market conditions, including when the equity market, where IBIT is traded, is closed.

#### Additional Features:

- **Color-Coding:** The premium is color-coded in green when positive (premium) and in red when negative (discount), aiding quick visual assessment.

- **Zero-Line Reference:** A horizontal line is drawn at zero to easily identify when IBIT is trading at par with the spot price of Bitcoin.

- **Real-Time Label Updates:** The label updates in real time with the latest premium/discount information and includes an arrow to signify the trend direction.

#### Access and Usage:

The indicator can be favorited or added to your TradingView charts. You are also welcome to use the source code as a foundation for further customization to suit your trading strategies.

#### Notes:

Please consider that the IBIT has specific trading hours, and the indicator can show live changes even when its market is closed, which might lead to discrepancies from official static data. For best performance, use this indicator alongside the IBIT candlestick chart on TradingView.

GBTC Premium to CoinbaseThe BTC ETF premium indicator for TradingView is a specialized tool designed to measure and visualize the premium or discount of the Grayscale Bitcoin Trust (GBTC), an investment vehicle that holds Bitcoin, relative to the actual price of Bitcoin on the Coinbase exchange. This indicator can be particularly insightful for traders interested in the BTC securities market and those analyzing the demand for Bitcoin as reflected by institutional investment products.

#### Description:

The BTC ETF premium indicator in TradingView leverages an advanced Pine Script algorithm to calculate the premium (or discount) percentage of GBTC compared to the spot price of Bitcoin (BTC/USD) on Coinbase. The premium is a critical insight that reflects market sentiment and potentially arbitrage opportunities between the trust's share price and the underlying cryptocurrency asset.

Here's how the indicator works:

1. **Calculation Methodology:**

- **Implied Bitcoin Price of GBTC:** We determine the implied price of Bitcoin within GBTC by dividing the GBTC closing price by the known ratio of Bitcoin per share.

- **GBTC Premium to Coinbase:** The percentage premium is then calculated as:

$$\text{GBTC Premium} = \frac{(\text{Implied Bitcoin Price of GBTC} - \text{Actual Bitcoin Price on Coinbase})}{\text{Actual Bitcoin Price on Coinbase}} \times 100$$

- This calculation is performed using the closing prices on a per-minute basis to ensure timely and accurate analysis.

2. **Visualization:** The indicator plots the premium as a step line chart, making it easy to visualize changes over time. A dynamic label accompanies the plot, displaying the implied Bitcoin price, the actual percentage premium or discount, and whether the premium is trending up or down compared to the previous day's value.

3. **Usage Scenario:** Traders can use this indicator to monitor the live premium 24/7 and analyze how it behaves during different market conditions, including when the equity market, where GBTC is traded, is closed.

#### Additional Features:

- **Color-Coding:** The premium is color-coded in green when positive (premium) and in red when negative (discount), aiding quick visual assessment.

- **Zero-Line Reference:** A horizontal line is drawn at zero to easily identify when GBTC is trading at par with the spot price of Bitcoin.

- **Real-Time Label Updates:** The label updates in real time with the latest premium/discount information and includes an arrow to signify the trend direction.

#### Access and Usage:

The indicator can be favorited or added to your TradingView charts. You are also welcome to use the source code as a foundation for further customization to suit your trading strategies.

#### Notes:

Please consider that the GBTC has specific trading hours, and the indicator can show live changes even when its market is closed, which might lead to discrepancies from official static data. For best performance, use this indicator alongside the GBTC candlestick chart on TradingView.

TabulateTabulate statistics from up to 10 symbols and display in a table format

you can choose to display up to 20 periods data points back in time

Symbol and description

Select a symbol and provide a description for it, this would be used as the label on the left column

Highlighting options

Color based on value increase/decrease

Colors the value green if it has increased from previous value, or red if it has decreased

Color based on positive/negative value

Stat will be colored accordingly green if positive, red if negative

Table value formatting

Allows you to change how the values are formatted for easy viewing

if 0.000% is selected, the source will be replaced by the following formula (close - open)/open

table text color should be changed to "Color based on positive/negative value"

NOTE: symbols that hold only monthly values would need to be placed in a chart with real time data to show the latest period.

Trended CVD [Mxwll]Hey!

This indicator "Trended CVD" categorizes price movement by trend (using zig zag) and calculates cumulative volume delta for the entirety of the price move.

Features

CVD calculated for the trend

CVD divergences are distinguished (uptrend and falling CVD / downtrend and rising CVD)

CVD output normalized to scale with chart, and is plotted alongside the trend

Can be used for trend confirmation (CVD trend correlating with price trend)

All regular zig-zag features available

What constitutes a trend is customizable. Can locate small, medium, large price trends with detailed user-input settings.

How-To Use Trended CVD

The image above shows one of two primary uses for the indicator.

In the left-half of the image, price is downtrending simultaneously with CVD; thereby, CVD is confirming the downtrend.

The right-half of the image shows price uptrending simultaneously with CVD; CVD is confirming the uptrend.

This information can be used to classify the "strength" of the price move, and decide to trade with it or against it.

The image above shows the second primary use for the indicator.

A slight price decrease transpires while CVD increases - CVD diverging upwards from the price trend.

This information can be used to classify the strength of the downtrend, and decide to trade against it, or abstain from trading with it.

The image above shows, subsequent to divergence, price failed to sustain "meaningful" downwards movement.

Labels oriented at the final pivot of a trend show the cumulative volume delta for the entirety of the price move (distinguishable by the superimposed zig zag line).

That's really it! A more complex concept integrated with a simple output.

Thank you!

BTC ETF VolumesVolume

This script plots the trading volume of all BTC spot ETFs as well as the aggregate volume. Works on any chart and any timeframe.

Indicators

The volume of every ETF is plotted in a different color, with the total column adding up to the aggregate volume.

If you have price and indicator labels enabled you will also see individual ETF volume on your price scale on the right hand side.

If more BTC ETFs get launched I will add them.