Symbol CorrelationThe "Symbol Correlation" indicator calculates and displays the correlation between the chosen symbol's price and another selected source over a specified period. It also includes a moving average (SMA) of this correlation to provide a smoothed view of the relationship.

Why SMA and Table Display ?

The inclusion of SMA (Simple Moving Average) with adjustable length (SMA Length) enhances the indicator's utility by smoothing out short-term fluctuations in correlation, allowing for clearer trend identification. The SMA helps to visualize the underlying trend in correlation, making it easier to spot changes and patterns over time.

The table display of the correlation SMA value offers a concise summary of this trend. By showcasing the current correlation SMA alongside its historical values, traders can quickly gauge the relationship's strength relative to previous periods.

Interpreting the Indicator:

1. Correlation Values: The primary plot shows the raw correlation values between the symbol's price and the specified source. A value of 1 indicates a perfect positive correlation, -1 signifies a perfect negative correlation, and 0 suggests no linear relationship.

2. Correlation SMA: The SMA line represents the average correlation over a defined period (SMA Length). Rising SMA values indicate strengthening correlation trends, while declining values suggest weakening correlations.

3. Choosing SMA Length: Traders can adjust the SMA Length parameter to tailor the moving average to their specific analysis horizon. Shorter SMA lengths react quickly to price changes but may be more volatile, while longer SMA lengths smooth out noise but respond slower to recent changes.

In summary, the "Symbol Correlation" indicator is a valuable tool for assessing the evolving relationship between a symbol's price and an external source. Its use of SMA and tabular presentation facilitates a nuanced understanding of correlation trends, aiding traders in making informed decisions based on market dynamics.

Statistics

Tweet/X Post Timestamp - By LeviathanThis script allows you to generate visual timestamps of X/Twitter posts directly on your chart, highlighting the precise moment an X post/tweet was made. All you have to do is copy and paste the post URL.

◽️ Use Cases:

- News Trading: Traders can use this indicator to visually align market price actions with news or announcements made on X (formerly Twitter), aiding in the analysis of news impact on market volatility.

- Behavioral Analysis: Traders studying the influence of social media on price can use the timestamps to track correlations between specific posts and market reactions.

- Proof of Predictions: Traders can use this indicator to timestamp their market forecasts shared on X (formerly Twitter), providing a visual record of their predictions relative to actual market movements. This feature allows for transparent verification of the timing and accuracy of their analyses

◽️ Process of Timestamp Calculation

The calculation of the timestamp from a tweet ID involves the following steps:

Extracting the Post ID:

The script first parses the input URL provided by the user to extract the unique ID of the tweet or X post. This ID is embedded in the URL and is crucial for determining the exact posting time.

Calculating the Timestamp:

The post ID undergoes a mathematical transformation known as a right shift by 22 bits. This operation aligns the ID's timestamp to a base reference time used by the platform.

Adding Base Offset:

The result from the right shift is then added to a base offset timestamp (1288834974657 ms, the epoch used by Twitter/X). This converts the processed ID into a UNIX timestamp reflecting the exact moment the post was made.

Date-Time Conversion:

The UNIX timestamp is further broken down into conventional date and time components (year, month, day, hour, minute, second) using calculations that account for leap years and varying days per month.

Label Placement:

Based on user settings, labels displaying the timestamp, username, and other optional information such as price changes or pivot points are dynamically placed on the chart at the bar corresponding to the timestamp.

Bayesian Bias OscillatorWhat is a Bayes Estimator?

Bayesian estimation, or Bayesian inference, is a statistical method for estimating unknown parameters of a probability distribution based on observed data and prior knowledge about those parameters. At first , you will need a prior probability distribution, which is a prior belief about the distribution of the parameter that you are interested in estimating. This distribution represents your initial beliefs or knowledge about the parameter value before observing any data. Second , you need a likelihood function, which represents the probability of observing the data given different values of the parameter. This function quantifies how well different parameter values explain the observed data. Then , you will need a posterior probability distribution by combining the prior distribution and the likelihood function to obtain the posterior distribution of the parameter. The posterior distribution represents the updated belief about the parameter value after observing the data.

Bayesian Bias Oscillator

This tool calculates the Bayes bias of returns, which are directional probabilities that provide insight on the "trend" of the market or the directional bias of returns. It comes with two outputs: the default one, which is the Z-Score of the Bayes Bias, and the regular raw probability, which can be switched on in the settings of the indicator.

The Z-Score output value doesn't tell you the probability, but it does tell you how much of a standard deviation the value is from the mean. It uses both probabilities, the probability of a positive return and the probability of a negative return, which is just (1 - probability of a positive return).

The probability output value shows you the raw probability of a positive return vs. the probability of a negative return. The probability is the value of each line plotted (blue is the probability of a positive return, and purple is the probability of a negative return).

regressionsLibrary "regressions"

This library computes least square regression models for polynomials of any form for a given data set of x and y values.

fit(X, y, reg_type, degrees)

Takes a list of X and y values and the degrees of the polynomial and returns a least square regression for the given polynomial on the dataset.

Parameters:

X (array) : (float ) X inputs for regression fit.

y (array) : (float ) y outputs for regression fit.

reg_type (string) : (string) The type of regression. If passing value for degrees use reg.type_custom

degrees (array) : (int ) The degrees of the polynomial which will be fit to the data. ex: passing array.from(0, 3) would be a polynomial of form c1x^0 + c2x^3 where c2 and c1 will be coefficients of the best fitting polynomial.

Returns: (regression) returns a regression with the best fitting coefficients for the selecected polynomial

regress(reg, x)

Regress one x input.

Parameters:

reg (regression) : (regression) The fitted regression which the y_pred will be calulated with.

x (float) : (float) The input value cooresponding to the y_pred.

Returns: (float) The best fit y value for the given x input and regression.

predict(reg, X)

Predict a new set of X values with a fitted regression. -1 is one bar ahead of the realtime

Parameters:

reg (regression) : (regression) The fitted regression which the y_pred will be calulated with.

X (array)

Returns: (float ) The best fit y values for the given x input and regression.

generate_points(reg, x, y, left_index, right_index)

Takes a regression object and creates chart points which can be used for plotting visuals like lines and labels.

Parameters:

reg (regression) : (regression) Regression which has been fitted to a data set.

x (array) : (float ) x values which coorispond to passed y values

y (array) : (float ) y values which coorispond to passed x values

left_index (int) : (int) The offset of the bar farthest to the realtime bar should be larger than left_index value.

right_index (int) : (int) The offset of the bar closest to the realtime bar should be less than right_index value.

Returns: (chart.point ) Returns an array of chart points

plot_reg(reg, x, y, left_index, right_index, curved, close, line_color, line_width)

Simple plotting function for regression for more custom plotting use generate_points() to create points then create your own plotting function.

Parameters:

reg (regression) : (regression) Regression which has been fitted to a data set.

x (array)

y (array)

left_index (int) : (int) The offset of the bar farthest to the realtime bar should be larger than left_index value.

right_index (int) : (int) The offset of the bar closest to the realtime bar should be less than right_index value.

curved (bool) : (bool) If the polyline is curved or not.

close (bool) : (bool) If true the polyline will be closed.

line_color (color) : (color) The color of the line.

line_width (int) : (int) The width of the line.

Returns: (polyline) The polyline for the regression.

series_to_list(src, left_index, right_index)

Convert a series to a list. Creates a list of all the cooresponding source values

from left_index to right_index. This should be called at the highest scope for consistency.

Parameters:

src (float) : (float ) The source the list will be comprised of.

left_index (int) : (float ) The left most bar (farthest back historical bar) which the cooresponding source value will be taken for.

right_index (int) : (float ) The right most bar closest to the realtime bar which the cooresponding source value will be taken for.

Returns: (float ) An array of size left_index-right_index

range_list(start, stop, step)

Creates an from the start value to the stop value.

Parameters:

start (int) : (float ) The true y values.

stop (int) : (float ) The predicted y values.

step (int) : (int) Positive integer. The spacing between the values. ex: start=1, stop=6, step=2:

Returns: (float ) An array of size stop-start

regression

Fields:

coeffs (array__float)

degrees (array__float)

type_linear (series__string)

type_quadratic (series__string)

type_cubic (series__string)

type_custom (series__string)

_squared_error (series__float)

X (array__float)

Momentum ProfileProfile market behavior in horizontal zones

Profile Sidebar

Buckets pointing rightward indicate upward security movement in the lookahead window at that level, and buckets pointing leftward indicate downward movement in the lookahead window.

Green profile buckets indicate the security's behavior following an uptrend in the lookbehind window. Conversely, Red profile buckets show security's behavior following a downtrend in the lookbehind window. Yellow profile buckets show behavior following sideways movement.

Buckets length corelates with the amount of movement measured in that direction at that level.

Inputs

Length determines how many bars back are considered for the calculation. On most securities, this can be increased to just above 4000 without issues.

Rows determines the number of buckets that the securities range is divided into.

You can increase or decrease the threshold for which moves are considered sideways with the sideways_filter input: higher means more moves are considered sideways.

The lookbehind input determines the lookbehind window. Specifically, how many bars back are considered when determining whether a data point is considered green (uptrend), red (downtrend), or yellow (no significant trend).

The lookahead input determines how many bars after the current bar are considered when determining the length and direction of each bucket (leftward for downward moves, rightward for upward moves).

Profile_width and Profile_spacing are cosmetic choices.

Intrabar support is not current supported.

Region Highlighting

Regions highlighted green saw an upward move in the lookahead window for both lookbehind downtrends and uptrends. In other words, both red and green profile buckets pointed rightward.

Regions highlighted red saw a downward move in the lookahead window both for lookbehind downtrends and uptrends.

Regions highlighted brown indicate a reversal region: uptrends were followed by downtrends, and vice versa. These regions often indicate a chop range or sometimes support/resistance levels. On the profile, this means that green buckets pointed left, and red buckets pointed right.

Regions highlighted purple indicate that whatever direction the security was moving, it continued that way. On the profile, this means that green buckets pointed right, and red buckets pointed left in that region.

sVPSA - standardized Volume Price Spread AnalysisDear Analysts and Traders,

I want to introduce my new indicator - sVPSA - standardized Volume Price Spread Analysis. For me, this script is helpfully in Technical Analysis mainly with Wyckoff and VSA methodologies. Maybe You are in circle of people who used my previous script - normalized Volume Price Spread Analysis. I work with him a lot of time, but I come to a conclusion that I can do better...

Theory concept...

What is a big volume? How big was this spread? It was extreme high or just high? How to do an answer for this and a lot other questions related to this subject? My thoughts was directed to statistics. In my first script I used to x/max normalized data. It was good, but susceptible for high deviation events. So, I choose standardization method with smaller sensitivity on violent events - z-Score standardization Description of z-Score formula:

Z = (x-mean)/standard deviation

Probability of event are descriptive by probability density function - The Normal Distribution.

en.wikipedia.org

en.Wikipedia.org

This is base of script methodology, let’s go deeper in indicator.

X axis is time, date. Y axis is standard deviation. Narrow bar represent price spread, wide one is volume. Colors are corresponding to deviation, blue < sigma, green > sigma, red > 2*sigma and fuchsia > 3*sigma. Appearance is full editable.

Data collection starts from left to right. There is two possibilities to use, constans number of bars or visible data range, also indicator permit to overscore linear regression from data. There is a possibility to set an alert.

Short introduction how put an interpretation on visualized data.

For this example I used constans value of data collection, 52 bars. So, from left I see great, fuchsia volume bar with low spread. This record respond Celsius withdrawals pause. This is bar with the biggest volume on presented chart, more than four sigmas. Spread value is near one sigma. I should consider this via one of Wyckoffs laws - effort vs result. I see a three bars in turn, they tenor tells me that bear market is possible near end. Accumulation structure near new year, spring test and bullish momentum bar near march are approval of this idea. Next high spread bars have volume near mean value. Effort is low but result is great. Interesting is last bar, with -2,8 deviation of volume. I see the lowest volume value on chart, so he’s deviation is strong to negative side. This script require a little of practise and can be a potent tool in Technical Analysis.

If You have a concept how to improve my script or You experience bug, please, send me feedback.

I hope that You consider my work as useful.

I wish You great trades and faultless analysis.

CatTheTrader

Nadaraya-Watson Probability [Yosiet]The script calculates and displays probability bands around price movements, offering insights into potential market trends.

Setting Up the Script

Window Size: Determines the length of the window for the Nadaraya-Watson estimation. A larger window smooths the data more but might lag current market conditions.

Bandwidth: Controls the bandwidth for the kernel regression, affecting the smoothness of the probability bands.

Reading the Data Table

The script dynamically updates a table positioned at the bottom right of your chart, providing real-time insights into market probabilities. Here's how to interpret the table:

Table Columns: The table is organized into three columns:

Up: Indicates the probability or relative change percentage for the upper band.

Down: Indicates the probability or relative change percentage for the lower band.

Table Rows: There are two main rows of interest:

P%: Shows the price change percentage difference between the bands and the closing price. A positive value in the "Up" column suggests the upper band is above the current close, indicating potential upward momentum. Conversely, a negative value in the "Down" column suggests downward momentum.

R%: Displays the relative inner change percentage difference between the bands, offering a measure of the market's volatility or stability within the bands.

Utilizing the Insights

Market Trends: A widening gap between the "Up" and "Down" percentages in the "P%" row might indicate increasing market volatility. Traders can use this information to adjust their risk management strategies accordingly.

Entry and Exit Points: The "R%" row provides insights into the relative position of the current price within the probability bands. Traders might consider positions closer to the lower band as potential entry points and positions near the upper band as exit points or take-profit levels.

Conclusion

The Nadaraya-Watson Probability script offers a sophisticated tool for traders looking to incorporate statistical analysis into their trading strategy. By understanding and utilizing the data presented in the script's table, traders can gain insights into market trends and volatility, aiding in decision-making processes. Remember, no indicator is foolproof; always consider multiple data sources and analyses when making trading decisions.

Lot Size Calculator - Acero FXENGLISH DESCRIPTION:

Easy get your lot size (by Acero FX)

---------------------------

We use this transaction sizes:

Forex = 1

XAUUSD = 0.001

US100, US30 or other index = 10

---------------------------

Automatic Information for calculations:

Currency used: USD

Instrument: Detected Automatically

---------------------------

Manual Inputs:

Choose your Balance amount in "Tamaño de Cuenta"

Choose your Risk Type in "Tipo de Riesgo" between Percentage or Amount

Choose your method to calculate your Lot Size in "Calcular Usando..." between Pips or Entry and SL price

---------------------------

Table Shows:

Title: Lot Size Calc 5.0 - Acero FX

Instrument: .................

Lot Size: ..............

Entry Price: .............

Stop Loss Price: .............

Pips: ...............

Risk ($): ...............

Risk (%): ............

Transaction Size: ..............

---------------------------

Important Disclaimers:

-Minor pairs may have some differences between other calculators.

-JPY pairs use USDJPY open price of the day

DESCRIPCIÓN EN ESPAÑOL

Calcula fácilmente tu lote (Diseñado por Acero FX)

---------------------

Usamos estos tamaños de transacción:

Forex = 1

XAUUSD = 0,001

US100, US30 u otros índices = 10

---------------------

Información automática para cálculos:

Moneda utilizada: USD

Instrumento: Detectado automáticamente

---------------------

Entradas manuales:

Elige el monto de tu Saldo en "Tamaño de Cuenta"

Elige el Tipo de Riesgo en "Tipo de Riesgo" entre Porcentaje o Monto

Elige el método para calcular el tamaño de stu lote en "Calcular Usando..." entre Pips o Entrada y precio SL

---------------------

La tabla muestra:

Título: Calc. Tamaño de Lote 5.0 - Acero FX

Instrumento: .................

Lotaje: ..............

Entrada: .............

Stop Loss: .............

Pips: .................

Riesgo ($): .................

Riesgo (%): ............

Tamaño del contrato (tamaño de la transacción): .................

---------------------

Descargos de responsabilidad importantes:

-Los pares menores pueden tener algunas diferencias entre otras calculadoras.

-Los pares JPY utilizan el precio de apertura del día USDJPY

Gaussian Price Filter [BackQuant]Gaussian Price Filter

Overview and History of the Gaussian Transformation

The Gaussian transformation, often associated with the Gaussian (normal) distribution, is a mathematical function characteristically prominent in statistics and probability theory. The bell-shaped curve of the Gaussian function, expressing the normal distribution, is ubiquitously employed in various scientific and engineering disciplines, including financial market analysis. This transformation's core utility in trading and economic forecasting is derived from its efficacy in smoothing data series and highlighting underlying trends, which are pivotal for making strategic trading decisions.

The Gaussian filter, specifically, is a type of data-smoothing algorithm that mitigates the random "noise" of market price data, thus enhancing the visibility of crucial trend changes and patterns. Historically, this concept was adapted from fields such as signal processing and image editing, where precise extraction of useful information from noisy environments is critical.

1. What is a Gaussian Transformation?

A Gaussian transformation involves the application of a Gaussian function to a set of data points. The function is applied as a filter in the context of trading algorithms to smooth time series data, which helps in identifying the intrinsic trends obscured by market volatility. The transformation is characterized by its parameter, sigma (σ), representing the standard deviation, which determines the width of the Gaussian bell curve. The breadth of this curve impacts the degree of smoothing: a wider curve (higher sigma value) results in more smoothing, beneficial for longer-term trend analysis.

2. Filtering Price with Gaussian Transformation and its Benefits

In the provided Script, the Gaussian transformation is utilized to filter price data. The filtering process involves convolving the price data with Gaussian weights, which are calculated based on the chosen length (the number of data points considered) and sigma. This convolution process smooths out short-term fluctuations and highlights longer-term movements, facilitating a clearer analysis of market trends.

Benefits:

Reduces noise: It filters out minor price movements and random fluctuations, which are often misleading.

Enhances trend recognition: By smoothing the data, it becomes easier to identify significant trends and reversals.

Improves decision-making: Traders can make more informed decisions by focusing on substantive, smoothed data rather than reacting to random noise.

3. Potential Limitations and Issues

While Gaussian filters are highly effective in smoothing data, they are not without limitations:

Lag introduction: Like all moving averages, the Gaussian filter introduces a lag between the actual price movements and the output signal, which can delay decision-making.

Feature blurring: Over-smoothing might obscure significant price movements, especially if a large sigma is used.

Parameter sensitivity: The choice of length and sigma significantly affects the output, requiring optimization and backtesting to determine the best settings for specific market conditions.

4. Extending Gaussian Filters to Other Indicators

The methodology used to filter price data with a Gaussian filter can similarly be applied to other technical indicators, such as RSI (Relative Strength Index) or MACD (Moving Average Convergence Divergence). By smoothing these indicators, traders can reduce false signals and enhance the reliability of the indicators' outputs, leading to potentially more accurate signals and better timing for entering or exiting trades.

5. Application in Trading

In trading, the Gaussian Price Filter can be strategically used to:

Spot trend reversals: Smoothed price data can more clearly indicate when a trend is starting to change, which is crucial for catching reversals early.

Define entry and exit points: The filtered data points can help in setting more precise entry and exit thresholds, minimizing the risk and maximizing the potential return.

Filter other data streams: Apply the Gaussian filter on volume or open interest data to identify significant changes in market dynamics.

6. Functionality of the Script

The script is designed to:

Calculate Gaussian weights (f_gaussianWeights function): Generates the weights used for the Gaussian kernel based on the provided length and sigma.

Apply the Gaussian filter (f_applyGaussianFilter function): Uses the weights to compute the smoothed price data.

Conditional Trend Detection and Coloring: Determines the trend direction based on the filtered price and colors the price bars on the chart to visually represent the trend.

7. Specific Actions of This Code

The Pine Script provided by BackQuant executes several specific actions:

Input Handling: It allows users to specify the source data (src), kernel length, and sigma directly in the chart settings.

Weight Calculation and Normalization: Computes the Gaussian weights and normalizes them to ensure their sum equals one, which maintains the original data scale.

Filter Application: Applies the normalized Gaussian kernel to the price data to produce a smoothed output.

Trend Identification and Visualization: Identifies whether the market is trending upwards or downwards based on the smoothed data and colors the bars green (up) or red (down) to indicate the trend direction.

US CPIIntroducing "US CPI" Indicator

The "US CPI" indicator, based on the Consumer Price Index (CPI) of the United States, is a valuable tool for analyzing inflation trends in the U.S. economy. This indicator is derived from official data provided by the U.S. Bureau of Labor Statistics (BLS) and is widely recognized as a key measure of inflationary pressures.

What is CPI?

The Consumer Price Index (CPI) is a measure that examines the average change in prices paid by consumers for a basket of goods and services over time. It is an essential economic indicator used to gauge inflationary trends and assess changes in the cost of living.

How is "US CPI" Calculated?

The "US CPI" indicator in this script retrieves CPI data from the Federal Reserve Economic Data (FRED) using the FRED:CPIAUCSL symbol. It calculates the rate of change in CPI over a specified period (typically 12 months) and applies technical analysis tools like moving averages (SMA and EMA) for trend analysis and smoothing.

Why Use "US CPI" Indicator?

1. Inflation Analysis: Monitoring CPI trends provides insights into the rate of inflation, which is crucial for understanding the overall economic health and potential impact on monetary policy.

2. Policy Implications: Changes in CPI influence decisions by policymakers, central banks, and investors regarding interest rates, fiscal policies, and asset allocation.

3. Market Sentiment: CPI data often impacts market sentiment, influencing trading strategies across various asset classes including currencies, bonds, and equities.

Key Features:

1. Customizable Smoothing: The indicator allows users to apply exponential moving average (EMA) smoothing to CPI data for clearer trend identification.

2. Visual Representation: The plotted line visually represents the inflation rate based on CPI data, helping traders and analysts assess inflationary pressures at a glance.

Sources and Data Integrity:

The CPI data used in this indicator is sourced directly from FRED, ensuring reliability and accuracy. The script incorporates robust security protocols to handle data requests and maintain data integrity in a trading environment.

In conclusion, the "US CPI" indicator offers a comprehensive view of inflation dynamics in the U.S. economy, providing traders, economists, and policymakers with valuable insights for informed decision-making and risk management.

Disclaimer: This indicator and accompanying analysis are for informational purposes only and should not be construed as financial advice. Users are encouraged to conduct their own research and consult with professional advisors before making investment decisions.

RSI AcceleratorThe Relative Strength Index (RSI) is like a fitness tracker for the underlying time series. It measures how overbought or oversold an asset is, which is kinda like saying how tired or energized it is.

When the RSI goes too high, it suggests the asset might be tired and due for a rest, so it could be a sign it's gonna drop. On the flip side, when the RSI goes too low, it's like the asset is pumped up and ready to go, so it might be a sign it's gonna bounce back up. Basically, it helps traders figure out if a stock is worn out or revved up, which can be handy for making decisions about buying or selling.

The RSI Accelerator takes the difference between a short-term RSI(5) and a longer-term RSI(14) to detect short-term movements. When the short-term RSI rises more than the long-term RSI, it typically refers to a short-term upside acceleration.

The conditions of the signals through the RSI Accelerator are as follows:

* A bullish signal is generated whenever the Accelerator surpasses -20 after having been below it.

* A bearish signal is generated whenever the Accelerator breaks 20 after having been above it.

ATH Distance HeatmapThe "ATH Distance Heatmap" is a powerful visualization tool designed for traders and investors who seek to quickly assess the relative performance of assets against their All-Time Highs (ATH). By mapping the percentage distance of current prices from their historical peaks, this script provides a unique perspective on market sentiment, potential recovery opportunities, and overvaluation risks.

Key Features:

Visual Clarity: Utilize a color-coded heatmap to instantly recognize which assets are near or far from their ATHs. Colors transition smoothly from cool to warm tones, indicating smaller to larger distances respectively.

Real-Time Updates: The script updates dynamically with live market data, ensuring you have the most current information at your fingertips.

Versatile Application: Whether you're tracking stocks, cryptocurrencies, commodities, or indices, the "ATH Distance Heatmap" adapts to a wide array of assets, making it a versatile tool for your trading arsenal.

Insightful Analysis: Beyond mere visualization, this tool can help identify potential buying opportunities in assets that are significantly below their ATHs, or highlight caution for those nearing their peaks.

How to Use:

Configure Your Assets: Start by selecting the assets you wish to track. The script can be customized to monitor a broad market range or a specific segment.

Interpret the Colors: Use the color gradient to gauge the distance of each asset from its ATH. Cooler colors indicate assets closer to their ATH, while warmer colors highlight those further away.

Ideal for:

Traders looking for a quick visual guide to market trends and asset performance.

Investors aiming to capitalize on recovery opportunities or to evaluate entry and exit points.

Market analysts interested in a concise overview of asset health relative to historical performance.

Index Generator [By MUQWISHI]▋ INTRODUCTION :

The “Index Generator” simplifies the process of building a custom market index, allowing investors to enter a list of preferred holdings from global securities. It aims to serve as an approach for tracking performance, conducting research, and analyzing specific aspects of the global market. The output will include an index value, a table of holdings, and chart plotting, providing a deeper understanding of historical movement.

_______________________

▋ OVERVIEW:

The image can be taken as an example of building a custom index. I created this index and named it “My Oil & Gas Index”. The index comprises several global energy companies. Essentially, the indicator weights each company by collecting the number of shares and then computes the market capitalization before sorting them as seen in the table.

_______________________

▋ OUTPUTS:

The output can be divided into 3 sections:

1. Index Title (Name & Value).

2. Index Holdings.

3. Index Chart.

1. Index Title , displays the index name at the top, and at the bottom, it shows the index value, along with the daily change in points and percentage.

2. Index Holdings , displays list the holding securities inside a table that contains the ticker, price, daily change %, market cap, and weight %. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

3. Index Chart , display a plot of the historical movement of the index in the form of a bar, candle, or line chart.

_______________________

▋ INDICATOR SETTINGS:

(1) Naming the index.

(2) Entering a currency. To unite all securities in one currency.

(3) Table location on the chart.

(4) Table’s cells size.

(5) Table’s colors.

(6) Sorting table. By securities’ (Market Cap, Change%, Price, or Ticker Alphabetical) order.

(7) Plotting formation (Candle, Bar, or Line)

(8) To show/hide any indicator’s components.

(9) There are 34 fields where user can fill them with symbols.

Please let me know if you have any questions.

Evolving RThe "Evolving R" script is a script that allows to calculate a dynamic reward-to-risk ratio at any given point of time during the trade. Its fundamentals are based on Tom Dante's concept of an evolving reward-to-risk. The script requires a user to input their preferred stop loss price and the target price for a specific asset, and calculates the ratio between two differences: (a) the absolute difference between the target price and the current price and (b) the absolute difference between the stop loss price and the current price.

The output of the script displays the ratio discussed as a value called "Evolving R" in the table. In order to use it successfully, the user of the script has to input:

(a) Stop loss price for the asset

(b) Target price for the asset

Theoretically, as long as the evolving R value holds above or equal to 0.25, the trade is worth holding. However, if the evolving R value drops below 0.25, the table turns red and signifies that such a trade possesses more risk than there is a reward remaining: this alerts the user to possibly take profits prematurely without risking their unrealized gains for a minor amount of additional gain.

The graphics of the script are represented by green and red areas: the green area indicates the area between the current price and the target price, while the red area shows the distance between the current price and the stop loss price. This visual representation allows users to understand the relative reward-to-risk ratio graphically in addition to the given evolving R value output.

The script is used for any type of trading: whether trend-trading or in a ranging market, it doesn't suggest a user which market conditions they should use.

FunctionDiscreteCosineTransformLibrary "FunctionDiscreteCosineTransform"

Discrete Cosine Transform (DCT)

The Discrete Cosine Transform (DCT) is a mathematical algorithm that converts a series of samples of a signal, typically in the time domain, into another domain called the frequency or spectral domain. It's commonly used for data compression and image/video coding applications such as JPEG and MPEG standards.

The DCT works by multiplying the input sequence with specific cosine functions that are pre-defined and then summing up these products to obtain a new series of values, which represent the frequency components of the original signal. The main advantage of the DCT over other transforms like Fourier Transform is its ability to handle non-stationary signals (i.e., signals with varying statistical properties) more effectively due to its localized basis functions.

In simple terms, the DCT can be thought of as a way to break down an image or video into different frequency components and then compress them without losing too much information. This compression technique is essential for efficient transmission and storage of digital media files over the internet or on devices with limited memory capacity.

~Mixtral4x7b

___

Reference:

lcamtuf.substack.com

dct(data, len)

Discrete Cosine Transform.

Parameters:

data (array) : Data source.

len (int) : Length of the sampling window.

Returns: List with frequency domain transformed information.

dct(data, len)

Discrete Cosine Transform.

Parameters:

data (float) : Data source.

len (int) : Length of the sampling window.

Returns: List with frequency domain transformed information.

idct(data, len)

Inverse Discrete Cosine Transform.

Parameters:

data (array) : Data source.

len (int) : Length of the sampling window.

Returns: List with time domain transformed information.

idct(data, len)

Inverse Discrete Cosine Transform.

Parameters:

data (float) : Data source.

len (int) : Length of the sampling window.

Returns: List with time domain transformed information.

Kalman Hull Supertrend [BackQuant]Kalman Hull Supertrend

At its core, this indicator uses a Kalman filter of price, put inside of a hull moving average function (replacing the weighted moving averages) and then using that as a price source for the supertrend instead of the normal hl2 (high+low/2).

Therefore, making it more adaptive to price and also sensitive to recent price action.

PLEASE Read the following, knowing what an indicator does at its core before adding it into a system is pivotal. The core concepts can allow you to include it in a logical and sound manner.

1. What is a Kalman Filter

The Kalman Filter is an algorithm renowned for its efficiency in estimating the states of a linear dynamic system amidst noisy data. It excels in real-time data processing, making it indispensable in fields requiring precise and adaptive filtering, such as aerospace, robotics, and financial market analysis. By leveraging its predictive capabilities, traders can significantly enhance their market analysis, particularly in estimating price movements more accurately.

If you would like this on its own, with a more in-depth description please see our Kalman Price Filter.

2. Hull Moving Average (HMA) and Its Core Calculation

The Hull Moving Average (HMA) improves on traditional moving averages by combining the Weighted Moving Average's (WMA) smoothness and reduced lag. Its core calculation involves taking the WMA of the data set and doubling it, then subtracting the WMA of the full period, followed by applying another WMA on the result over the square root of the period's length. This methodology yields a smoother and more responsive moving average, particularly useful for identifying market trends more rapidly.

3. Combining Kalman Filter with HMA

The innovative combination of the Kalman Filter with the Hull Moving Average (KHMA) offers a unique approach to smoothing price data. By applying the Kalman Filter to the price source before its incorporation into the HMA formula, we enhance the adaptiveness and responsiveness of the moving average. This adaptive smoothing method reduces noise more effectively and adjusts more swiftly to price changes, providing traders with clearer signals for market entries or exits.

The calculation is like so:

KHMA(_src, _length) =>

f_kalman(2 * f_kalman(_src, _length / 2) - f_kalman(_src, _length), math.round(math.sqrt(_length)))

4. Integration with Supertrend

Incorporating this adaptive price smoothing technique into the Supertrend indicator further enhances its efficiency. The Supertrend, known for its proficiency in identifying the prevailing market trend and providing clear buy or sell signals, becomes even more powerful with an adaptive price source. This integration allows the Supertrend to adjust more dynamically to market changes, offering traders more accurate and timely trading signals.

5. Application in a Trading System

In a trading system, the Kalman Hull Supertrend indicator can serve as a critical component for identifying market trends and generating signals for potential entry and exit points. Its adaptiveness and sensitivity to price changes make it particularly useful for traders looking to minimize lag in signal generation and improve the accuracy of their market trend analysis. Whether used as a standalone tool or in conjunction with other indicators, its dynamic nature can significantly enhance trading strategies.

6. Core Calculations and Benefits

The core of this indicator lies in its sophisticated filtering and averaging techniques, starting with the Kalman Filter's predictive adjustments, followed by the adaptive smoothing of the Hull Moving Average, and culminating in the trend-detecting capabilities of the Supertrend. This multi-layered approach not only reduces market noise but also adapts to market volatility more effectively. Benefits include improved signal accuracy, reduced lag, and the ability to discern trend changes more promptly, offering traders a competitive edge.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

QuarterCandlesChanges candle color when close is within the top 25% or bottom 25% of candle range (High - Low) on the last candle update.

Due to limitations of barcolor command, I'd suggest that you turn OFF the candle borders (chart settings--> right click on chart --> settings -->symbol and uncheck the border option) to ensure that the bar color is easily identifiable.

Inflation CorrelationHeyo fellas,

In today’s dynamic economic landscape, understanding the relationship of market prices to other economical factors like inflation rate is crucial. The Inflation Correlation Indicator is designed to provide traders with a clear visualization of this relationship. By correlating average inflation rates from selected countries with market closing prices, this indicator offers a unique perspective on potential market movements influenced by inflationary trends.

Features:

Country Selection: Choose from the European Union (EU), Germany (DE), or the United States (US) to tailor the correlation analysis to your specific market interest.

Correlation Length Customization: Adjust the correlation length to refine the sensitivity of the indicator to recent inflation data.

Visual Clarity: The correlation histogram changes color based on the direction of the correlation, providing an intuitive understanding of the inflation correlation.

Whether you’re a fundamental analyst seeking to incorporate macroeconomic indicators into your strategy or a trader looking for an edge in inflation-sensitive markets, the Inflation Correlation Indicator is an indispensable tool in your TradingView arsenal.

Thanks for checking this out!

Best regards,

simwai

LSMA Z-Score [BackQuant]LSMA Z-Score

Main Features and Use in the Trading Strategy

- The indicator normalizes the LSMA into a detrended Z-Score, creating an oscillator with standard deviation levels to indicate trend strength.

- Adaptive coloring highlights the rate of change and potential reversals, with different colors for positive and negative changes above and below the midline.

- Extreme levels with adaptive coloring indicate the probability of a reversion, providing strategic entry or exit points.

- Alert conditions for crossing the midline or significant shifts in trend direction enhance its utility within a trading strategy.

1. What is an LSMA?

The Least Squares Moving Average (LSMA) is a technical indicator that smoothens price data to help identify trends. It uses the least squares regression method to fit a straight line through the selected price points over a specified period. This approach minimizes the sum of the squares of the distances between the line and the price points, providing a more statistically grounded moving average that can adapt more smoothly to price changes.

2. What is a Z-Score?

A Z-Score is a statistical measurement that describes a value's relationship to the mean of a group of values, measured in terms of standard deviations from the mean. If a Z-Score is 0, it indicates that the data point's score is identical to the mean score. A Z-Score helps in understanding if a data point is typical for a given data set or if it is atypical. In finance, a Z-Score is often used to measure how far a piece of data is from the average of a set, which can be helpful in identifying outliers or unusual data points.

3. Why Turning LSMA into a Z-Score is Innovative and Its Benefits

Converting LSMA into a Z-Score is innovative because it combines the trend identification capabilities of the LSMA with the statistical significance testing of Z-Scores. This transformation normalizes the LSMA, creating a detrended oscillator that oscillates around a mean (zero line), with standard deviation levels to show trend strength. This method offers several benefits:

Enhanced Trend Detection:

- By normalizing the LSMA, traders can more easily identify when the price is deviating significantly from its trend, which can signal potential trading opportunities.

Standardization:

- The Z-Score transformation allows for comparisons across different assets or time frames, as the score is standardized.

Objective Measurement of Trend Strength:

- The use of standard deviation levels provides an objective measure of trend strength and volatility.

4. How It Can Be Used in the Context of a Trading System

This indicator can serve as a versatile tool within a trading system for a range of things:

Trend Confirmation:

- A positive Z-Score can confirm an uptrend, while a negative Z-Score can confirm a downtrend, providing traders with signals to enter or exit trades.

Oversold/Overbought Conditions:

- Extreme Z-Score levels can indicate overbought or oversold conditions, suggesting potential reversals or pullbacks.

Volatility Assessment:

- The standard deviation levels can help traders assess market volatility, with wider bands indicating higher volatility.

5. How It Can Be Used for Trend Following

For trend following strategies, this indicator can be particularly useful:

Trend Strength Indicator:

- By monitoring the Z-Score's distance from zero, traders can gauge the strength of the current trend, with larger absolute values indicating stronger trends.

Directional Bias:

- Positive Z-Scores can be used to establish a bullish bias, while negative Z-Scores can establish a bearish bias, guiding trend following entries and exits.

Color-Coding for Trend Changes :

- The adaptive coloring of the indicator based on the rate of change and extreme levels provides visual cues for potential trend reversals or continuations.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

This is using the Midline Crossover:

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Fractional Differentiation█ Description

This Pine Script indicator implements fractional differentiation, a mathematical operation that extends the concept of differentiation to non-integer orders. Fractional differentiation is particularly significant in financial analysis, as it enables analysts to uncover underlying patterns in price series that are not evident with traditional integer-order differentiation. The motivation behind fractional differencing lies in its ability to balance the trade-off between retaining data/feature memory and ensuring stationarity.

█ Significance

Fractional differentiation offers a nuanced view of market data, allowing for the adjustment of the differentiation order to balance between signal clarity and noise reduction. This is especially useful in financial markets, where the choice of differentiation order can highlight long-term trends or short-term price movements without completely smoothing out the valuable market noise.

█ Approximations Used

The implementation relies on the Gamma function for the computation of coefficients in the fractional differentiation formula. Given the complexity of the Gamma function, this script uses an approximation method based on the Lanczos approximation for the logarithm of the Gamma function, as detailed in "An Analysis Of The Lanczos Gamma Approximation" by Glendon Ralph Pugh (2004). This approximation strikes a balance between computational efficiency and accuracy, making it suitable for real-time market analysis in Pine Script.

█ Limitations

While this script opens new avenues for market analysis, it comes with inherent limitations:

- The approximation of the Gamma function, although accurate, is not exact. The precision of the fractional differentiation result may vary slightly, especially for higher-order differentiations.

- The script's performance is subject to Pine Script's execution environment, with a default loop limit set to 100 iterations for practicality. Users might need to adjust this limit based on their specific use case, balancing between computational load and the desired depth of historical data analysis.

█ Credits

This script makes use of the `MathSpecialFunctionsGamma` library, authored by Ricardo Santos . This library provides essential mathematical functions, including an approximation of the Gamma function, which is crucial for the fractional differentiation calculation.

I also extend my sincere gratitude to

Dr. Marcos López de Prado for his seminal work, Advances in Financial Machine Learning (2018). Dr. López de Prado's insights have significantly influenced our approach to developing sophisticated analytical tools.

Dr. Ernie Chan for his freely and generously sharing valuable insights via discourse on quantitative trading strategies through his talks and publications.

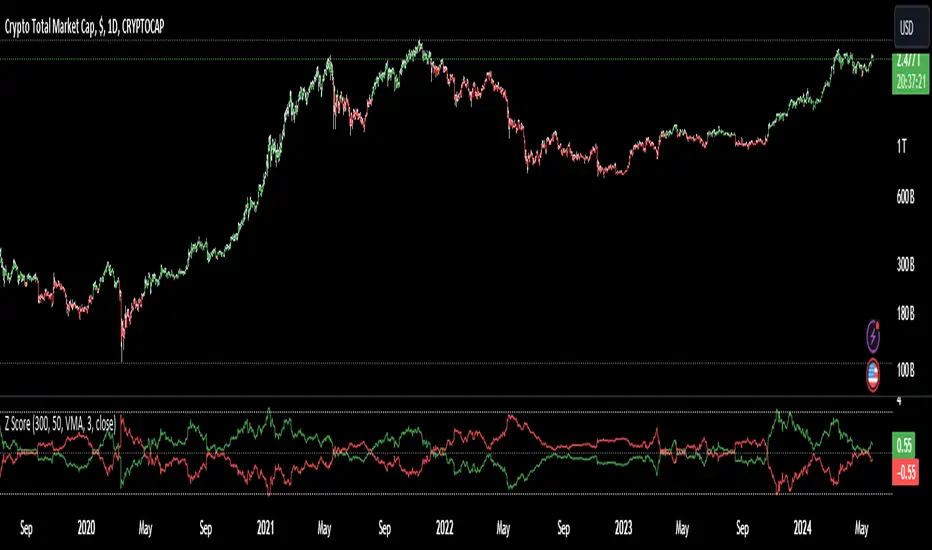

Z Score & Trend FollowingIntroduction:

The Z Score & Trend Following indicator is a tool used in financial markets to assess the standard deviation of a data point from its mean value over a specified period. It calculates the Z score, which is a measure of how many standard deviations an element is from the mean. This indicator also incorporates trend-following characteristics, allowing traders to visualize trends based on the Z score.

Indicator Parameters:

Standard Deviation Length: Determines the length of the standard deviation calculation.

Average Length: Specifies the length of the moving average used for the mean calculation.

Calculation Type: Allows users to choose between different types of moving averages (SMA, EMA, WMA, VMA, TMA).

Standard Deviations: Sets the number of standard deviations to be used for trend analysis.

Bar Color: Option to enable or disable bar coloring based on trend conditions.

Calculations:

Z Score Calculation: The Z score is calculated as the difference between the source data point and the moving average divided by the standard deviation.

zscore = (src - (getMA(src, length))) / ta.stdev(src, slength)

Plots:

Z Score Plot: Plots the Z score values, typically in green.

Inverted Z Score Plot: Plots the inverted Z score values (multiplied by -1), typically in red.

Lines:

Zero Line: A horizontal dotted line indicating zero.

Upper Threshold Line: A dotted line representing the upper threshold defined by the number of standard deviations.

Lower Threshold Line: A dotted line representing the lower threshold defined by the negative number of standard deviations.

Bar Color:

The bar color changes based on the Z score values and the predefined standard deviation thresholds. Green bars indicate values above the upper threshold, red bars indicate values below the lower threshold, lime bars indicate positive Z scores, and maroon bars indicate negative Z scores. Neutral values are represented by black bars.

Conclusion:

The Z Score & Trend Following indicator combines the statistical concept of Z score with trend-following characteristics to provide traders with insights into market trends and potential reversal points. By visualizing Z scores alongside trend analysis, traders can make more informed decisions regarding market entry and exit points.

AWR - Chris - V3Calculates the AWR based on Dr. Coles formula. Takes the last 12 weeks (not including the current one) highs and lows, adds them and then divides by twelve, give the average weekly range. Then takes the AWR and show the playing field based on the high and low of the current weekly candle. Must be used on the weekly chart to get the data needed then manually plot your lines on the required charts.

Bitcoin Regression Price BoundariesTLDR

DCA into BTC at or below the blue line. DCA out of BTC when price approaches the red line. There's a setting to toggle the future extrapolation off/on.

INTRODUCTION

Regression analysis is a fundamental and powerful data science tool, when applied CORRECTLY . All Bitcoin regressions I've seen (Rainbow Log, Stock-to-flow, and non-linear models), have glaring flaws ... Namely, that they have huge drift from one cycle to the next.

Presented here, is a canonical application of this statistical tool. "Canonical" meaning that any trained analyst applying the established methodology, would arrive at the same result. We model 3 lines:

Upper price boundary (red) - Predicted the April 2021 top to within 1%

Lower price boundary (green)- Predicted the Dec 2022 bottom within 10%

Non-bubble best fit line (blue) - Last update was performed on Feb 28 2024.

NOTE: The red/green lines were calculated using solely data from BEFORE 2021.

"I'M INTRUIGED, BUT WHAT EXACTLY IS REGRESSION ANALYSIS?"

Quite simply, it attempts to draw a best-fit line over some set of data. As you can imagine, there are endless forms of equations that we might try. So we need objective means of determining which equations are better than others. This is where statistical rigor is crucial.

We check p-values to ensure that a proposed model is better than chance. When comparing two different equations, we check R-squared and Residual Standard Error, to determine which equation is modeling the data better. We check residuals to ensure the equation is sufficiently complex to model all the available signal. We check adjusted R-squared to ensure the equation is not *overly* complex and merely modeling random noise.

While most people probably won't entirely understand the above paragraph, there's enough key terminology in for the intellectually curious to research.

DIVING DEEPER INTO THE 3 REGRESSION LINES ABOVE

WARNING! THIS IS TECHNICAL, AND VERY ABBREVIATED

We prefer a linear regression, as the statistical checks it allows are convenient and powerful. However, the BTCUSD dataset is decidedly non-linear. Thus, we must log transform both the x-axis and y-axis. At the end of this process, we'll use e^ to transform back to natural scale.

Plotting the log transformed data reveals a crucial visual insight. The best fit line for the blowoff tops is different than for the lower price boundary. This is why other models have failed. They attempt to model ALL the data with just one equation. This causes drift in both the upper and lower boundaries. Here we calculate these boundaries as separate equations.

Upper Boundary (in red) = e^(3.24*ln(x)-15.8)

Lower Boundary (green) = e^(0.602*ln^2(x) - 4.78*ln(x) + 7.17)

Non-Bubble best fit (blue) = e^(0.633*ln^2(x) - 5.09*ln(x) +8.12)

* (x) = The number of days since July 18 2010

Anyone familiar with Bitcoin, knows it goes in cycles where price goes stratospheric, typically measured in months; and then a lengthy cool-off period measured in years. The non-bubble best fit line methodically removes the extreme upward deviations until the residuals have the closest statistical semblance to normal data (bell curve shaped data).

Whereas the upper/lower boundary only gets re-calculated in hindsight (well after a blowoff or capitulation occur), the Non-Bubble line changes ever so slightly with each new datapoint. The last update to this line was made on Feb 28, 2024.

ENOUGH NERD TALK! HOW CAN I APPLY THIS?

In the simplest terms, anything below the blue line is a statistical buying opportunity. The closer you approach the green line (the lower boundary) the more statistically strong that opportunity is. As price approaches the red line, is a growing statistical likelyhood/danger of an imminent blowoff top.

So a wise trader would DCA (dollar cost average) into Bitcoin below the blue line; and would DCA out of Bitcoin as it approaches the red line. Historically, you may or may not have a large time-window during points of maximum opportunity. So be vigilant! Anything within 10-20% of the boundary should be regarded as extreme opportunity.

Note: You can toggle the future extrapolation of these lines in the settings (default on).

CLOSING REMARKS

Keep in mind this is a pure statistical analysis. It's likely that this model is probing a complex, real economic process underlying the Bitcoin price. Statistical models like this are most accurate during steady state conditions, where the prevailing fundamentals are stable. (The astute observer will note, that the regression boundaries held despite the economic disruption of 2020).

Thus, it cannot be understated: Should some drastic fundamental change occur in the underlying economic landscape of cryptocurrency, Bitcoin itself, or the broader economy, this model could drastically deviate, and become significantly less accurate.

Furthermore, the upper/lower boundaries cross in the year 2037. THIS MODEL WILL EVENTUALLY BREAK DOWN. But for now, given that Bitcoin price moves on the order of 2000% from bottom to top, it's truly remarkable that, using SOLELY pre-2021 data, this model was able to nail the top/bottom within 10%.