Close Combination Lock Style - Visual AppealThis creates a combination style closing price change on each tick.

It has two theme options, one as silver dials for Dark Theme and the other as black dials for White Theme.

We get fixated to watching closing prices on charts and it gets visually daunting. This creates a combination style price change which updates on each tick, which is quite pleasing to the eye.

When new price is above current center line, it shift the above prices showing ▲ arrow, and if new price is lower, it will shift the bottom prices showing ▼ arrow. If there is no change in price between the ticks, it will show =.

Сферы применения Pine

Candles HTF on Heikin Ashi ChartThis script enables calling and/or plotting of traditional Candles sources while loaded on Heikin Ashi charts.

Thanks to @PineCoders for rounding method: www.pinecoders.com

Thanks to @BeeHolder for method to regex normalize syminfo.tickerid.

NOTICE: While this script is meant to be utilized on Heikin Ashi charts it does NOT enable ability to backtest!

NOTICE: For more info on why non standard charts cannot be reliably backtested please see:

NOTICE: This is an example script and not meant to be used as an actual strategy. By using this script or any portion thereof, you acknowledge that you have read and understood that this is for research purposes only and I am not responsible for any financial losses you may incur by using this script!

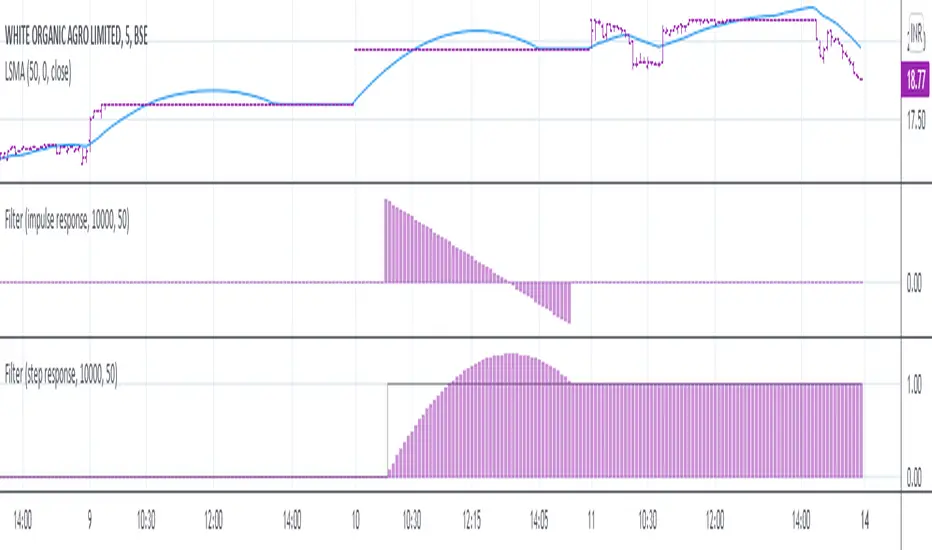

Filter impulse & step responsesA simple utility tool to examine a filter's step & impulse responses.

By default you can see LSMA's responses.

How to use:

1. Insert your filter to "f(input)" function inside the code;

2. Let this tool help you to make your own filters.

I been seeing people dropping snaps with this stuff but NEVER, NO1 actually dropped the tool itself (4 real?).

Well here is it, for you.

Almost forgot, adjust "Position" parameter to make plots seen. Try to zoom out, and +-100

How To Identify Argument Type Of Number Using OverloadsExample overload functions accept loading of _value for types float, int, or string, then positively identifies the actual argument type of that specific loaded _value.

How To Identify Type Of NumberExample function accepts loading of _value for types float, int, or string, then identifies whether the loaded _value is a string number, string, or number.

STRATEGY R18-F-BTCHi, I'm @SenatorVonShaft

Just finished the strategy "STRATEGY R18-F-BTC" for trading on #bitcoin and other cryptocurrencies.

As any strategy on TradingView, R18 opens Long/Short positions (with no leverage) on certain price points for assets in the chart. But I intentionally make this strategy for Bitcoin . Strategy is effective with 1h chart and it has %36 winning trade ratio for #bitcoin trade. As strategy uses approximately 1/3 ratio of SL/TP levels, gross profit for 1 year backtest is above %200 (I mean above 3x for only BTC )

Strategy is built on combination of:

- MACD

- RSI

- FIBONACCI levels

- BTCUSDT price itself as indicator (for different crypto assets and BTCUSDTPERP trading. You can select different assets you like for indicator (it's BTCUSDT:Binance by default))

I fine-tuned all levels of indicators above accordingly (it has more than 10 variables that effects strategy itself).

You can find out your own strategy levels by adjusting long/short tp&sl variables as well as initial capital ratio variable.

Reverse option open reverse positions of the strategy

Backtest EngineThis is a simple backtest engine for your trading strategies. The idea behind this script is to make testing new strategies as easy as possible. Parameters such as take profit/stop loss and time period are built into the script and are customisable by the user via the settings interface. The only coding is to set the entry and exit conditions. Users need not touch any code beyond line 30.

For this post, I have used a 50/200 SMA crossover to demonstrate the ease of use for this script.

The features of this script include:

Backtest period start

Number of days until backtest period end

Take profit and stop loss % (via settings)

Programmable long and short entry/exit

Anti duplicate system (for entry conditions that are continuously satisfied, the engine will only make 1 trade until the is exit condition is satisfied).

DISCLAIMER: The strategy in this post is only a placeholder. The TP/SL levels are set to showcase the functionality of the engine and are in no means optimal settings.

Hope this helps! Feel free to ask any questions about the engine and happy coding!

How To Count DecimalsCustom f_nDecimals() function returns precision of decimal numbers of the following forms:

const, input, simple, and series of the following types: float, integer, and string.

Error checking is performed for valid numbers and invalid values return NaN.

NOTICE: This is an example script and not meant to be used as an actual strategy. By using this script or any portion thereof, you acknowledge that you have read and understood that this is for research purposes only and I am not responsible for any financial losses you may incur by using this script!

Oscillator EdgesAnother simple script to be added on top of other indicators. Simply provides a symbol of varying color depending on the value of the oscillator. Allows up to 4 different colors in each direction. Includes alerts conditions. Demonstration is the indicator being applied to the RSI (purple) included in Market Cipher B.

To use, simply add it to your indicator, and choose and oscillator of your choice in the Input Settings. Alternatively, you can just keep it on 'close' and use the built in RSI. Or, you can use the RSI formula on top of something else (if that's your thing).

The names are silly, so I hope this is okay with all of you.

Let me know what you think, and if there are any problems, questions, or concerns!

Percentile Nearest Rank Using Arrays [LuxAlgo]The new array feature is extremely powerful, as it will allow pinescript users to do more complex things, or compute existing calculations more efficiently, it will also be possible to shine some light to some already existing functions, one of them being percentile_nearest_rank .

We have been working on this new feature with our pal alexgrover, and made this script which computes a rolling percentile using the nearest rank method.

Settings

Length: Window of the rolling percentile, determine the number of past data to be used.

Percentage: Return the current value if Percentage % of the data fall below that value, the setting is in a range (0,100).

Src: Input source of the indicator.

Usage

A rolling percentile can have many usages when it comes to technical analysis, this is due to its ability to return the value of three common rolling statistics, the rolling median, which can be obtained using a percentage equal to 50, the rolling maximum, obtained with a percentage equal to 100, and the rolling minimum, obtained with a percentage equal to 0.

When we use our rolling percentile as a rolling median, we can obtain a robust estimation of the underlying trend in the price, while using it as a rolling maximum/minimum can allow us to determine if the market is trending, and at which direction. The rolling maximum/minimum is a rolling statistic used to calculate the well known stochastic oscillator and Donchian channel indicator.

We can also compute rolling quartiles, which can be obtained using a percentage of 25 or 75, with one of 25 returning the lower quartile and 75 the upper quartile.

In blue the upper rolling quartile (%75), in orange the lower rolling quartile (%25), both using a window size of 100.

Details

In order to compute a rolling percentile nearest rank, we must first take the most recent length closing prices, then order them in ascending order, we then return the value of the ordered observations at index (percentage/100*length) - 1 (we use - 1 because our array index starts at 0).