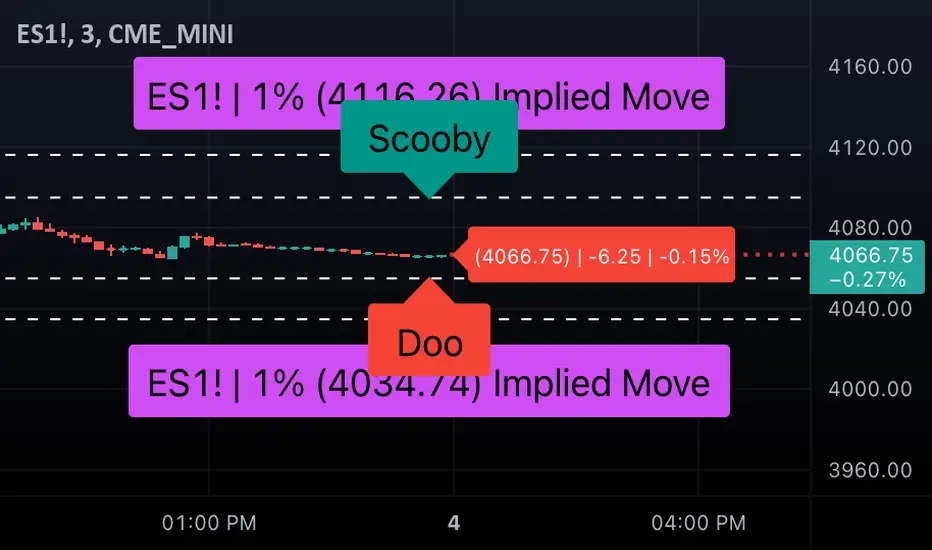

Expected Move by Option's Implied Volatility High Liquidity

This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols with high option liquidity.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options.There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry. This script will display Expected Move data for Symbols within the range of JBL-NOTE in alphabetical order.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

Move

Expected Move by Option's Implied Volatility Symbols: EAT - GBDC

This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols within the range of EAT-GDBC in alphabetical order.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options. There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

Expected Move by Option's Implied Volatility Symbols: CLFD-EARN This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols within the range of CLFD - EARN in alphabetical order.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options. There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

Expected Move by Option's Implied Volatility Symbols: B - CLF

This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols within the range of B - CLF in alphabetical order.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options. There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

Expected Move by Option's Implied Volatility Symbols: A - AZZ

This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols within the range of A - AZZ in alphabetical order.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options. There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

Move Magnitude Visualizer (beta)This experimental visualizer measures all price differences across a range of samples to determine what is normal for a measure of time. Based on whether a recent change in price over time has exceeded the norm, a line is drawn to indicate the magnitude/severity of that move. In short, it attempts to visualize when a move is outside the norm and when it may be risky to join that move.

A thick red line = greater than 3 standard deviations.

An orangish/goldish line = greater than 2 standard deviations.

A thin dotted yellow = greater than 1 standard deviation.

In the end, I've always wanted a tool that gave me a visual warning to when a move is abnormally severe and shouldn't be trusted. RSI and other indicators only work with specific lengths, this attempt to be a deviation detector that isn't bound by length or time-frame.

This is a work in progress, so feedback is appreciated. I don't have a strong idea yet how to properly visualize this data.

It is very compute heavy and some users may experience timeouts. I've done everything I can think of to eliminate redundant computer and to optimize for PineScript.

SPX Expected MoveThis indicator plots the "expected move" of SPX for today's trading session. Expected move is the amount that SPX is predicted to increase or decrease from its current price, based on the current level of implied volatility. The implied volatility in this indicator is computed from the current value of the VIX (or one of several volatility symbols available on Trading view). The computation is done using standard formula. The resulting plots are labeled as 1 and 2 standard deviations. The default values are to use VIX as well as 252 trading days in the years.

Use the square root of (days to expiration, or in this case a fraction of the day remaining) divided but the square root of (252, or number of trading days in a year).

timeRemaining = math.sqrt(DTE) / math.sqrt(252)

Standard deviation move = SPX bar closing price * (VIX/100) * timeRemaining

Implied Move with NASA Ideas & Price LineThis script allows you to customize the Implied Move Percentage and fully customize the way it is shown.

Can be used on any stock that has earnings and works based on the Implied Move (Percent).

Basically, it lets you visualize how the stock moved after reporting earnings and seeing if it reached the implied move or not.

This is helpful as it's important to know what earnings are worth keeping an eye on and which should be avoided.

There is also an added custom text input which was inspired to make from a frogman named NASA.

It lets you input whatever text you want on whatever price you want.

To summarize, it's basically a Post-It Note that you can add to any price level for any stock.

Alerts can be set if wanted, They can be alerted for the Implied Moves (If the stock price goes Above/ Below the set percentage) and NASA Ideas (if the stock price goes Above/ Below the set price).

There is also an added custom price line which is mostly for having a nonintrusive price line and label.

This price line and label can be switched to show the (Open, High, Low, Close, Extended High, Extended Low, Yesterday's Open, Yesterday's High, Yesterday's Low, and Yesterday's Close).

Strategy Oil Z ScoreObjective is to find forward looking indicators to find good entries into major index's.

In similar vein to my Combo Z Score script I have implemented one looking at oil and oil volatility. Interestingly the script out performs WITHOUT applying the EMA in longer timeframes but under performs in shorter timeframes, for example 2007 vs 2019. Likely due to the bullish nature of the past decade (by and large). You have some options on the underlying included Oil vs OVX (Best), MOVE vs OVX and VIX vs OVX. Oil vs OVX out performs Combo Z Script. Favours Spy over QQQ or derivations (SPXL etc).

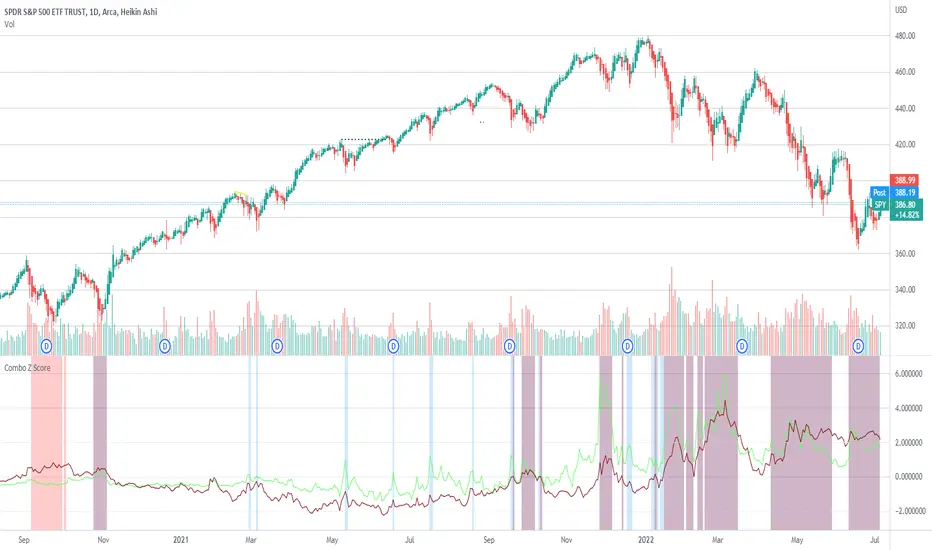

Strategy: Combo Z ScoreStrategy version of Combo Z Score

Objective:

Can we use both VIX and MOVE relationships to indicate movement in the SPY? VIX (forward contract on SPY options) correlations are quite common as forward indicators however MOVE (forward contract on bonds) also provides a slightly different level of insight

Using the Z-Score of VIX vs VVIX and MOVE vs inverted VIX (there is no M of Move so we use inverted Vix as a proxy) we get some helpful indications of potential future moves. Added %B to give us some exposure to momentum. Toggle VIX or MOVE.

If anyone has a better idea of inverted Vix to proxy forward interest in MOVE let me know.

Noticeable delta is that Vix only approach over the back test period is slightly better. Questions would be, what is the structure and nature of the market over the test period and in a bear market would MOVE or combined perform better.

Combo Z ScoreObjective:

Can we use both VIX and MOVE relationships to indicate movement in the SPY? VIX (forward contract on SPY options) correlations are quite common as forward indicators however MOVE (forward contract on bonds) also provides a slightly different level of insight

Using the Z-Score of VIX vs VVIX and MOVE vs inverted VIX (there is no M of Move so we use inverted Vix as a proxy) we get some helpful indications of potential future moves. Added %B to give us some exposure to momentum. Toggle VIX or MOVE.

If anyone has a better idea of inverted Vix to proxy forward interest in MOVE let me know.

Breakeven rectangle overlay for move contractI'm sharing this little script allowing you to display a breakeven rectangle for the move contract after manually writing your parameters (strike price, contract price). In case you are long your breakeven (at expiration) is when the price expire outside the rectangle. In case you are short your breakeven (again at expiration) is when the price is staying inside the rectangle at expiration. You can change multiple personalisation parameters as you wish.

FTX BTC Move Trend [Ryto]

This indicator helps intuitively see the trend between FTX move contract's strike price (Daily or Weekly) and the index price of BTC.

Blue curve: FTX BTC index price.

Red curve: 00:00:00-00:59:59 UTC+00:00 BTC index price TWAP.

Orange curve: 23:00:00-23:59:59 UTC+00:00 BTC index price TWAP.

Grey curve: The strike price of a move contract.

When the blue curve is near the grey curve, that represents the current index price is near to the strike price of a move contract. Cooperate with other indicators and observe the BTC trend also consider move contract price to decide whether to buy or sell.

Note: Should use the timeframe lower than 5 minutes, to ensure the correct TWAP price.

Reference:

- help.ftx.com

- help.ftx.com

- www.tradingview.com

---------------------------------------------------------------------------------------------------------------------------------------------------------------

這個指標適用在觀察 FTX 波動率產品 (日與週波動率合約),可以更直覺的看出 FTX BTC 指數價格與波動率產品行權價的走勢關係。

藍色曲線: BTC 指數價格

紅色曲線: 00:00:00-00:59:59 UTC+00:00 BTC 指數價格之時間加權平均

橘色曲線: 23:00:00-23:59:59 UTC+00:00 BTC 指數價格之時間加權平均

灰色曲線: 波動率產品行權價

當藍色曲線在灰色曲線附近,代表此時指數價格在行權價附近,配合其他指標觀察 BTC 走勢與波動率價格來決定是否買入或賣出波動率。

注意: 需使用時匡為 5 分鐘以下,確保指數價格之時間加權平均計算正確。

參考:

- help.ftx.com

- help.ftx.com (MOVE 合约)

- Pine 腳本時匡限制

MOVE/VXTLT CorrelationMany know of the VIX for equity trading. Yet, many are unaware that there is the same kind of volatility measure for trading bonds, called the MOVE Index.

"The Merrill Lynch Option Volatility Estimate (MOVE) Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options which are weighted on the 2, 5, 10, and 30 year contracts."

With this script one can see the the correlation and divergences between bonds and its volatility measure to make educated decisions in trading or hedging.

The idea of this script comes from NicTheMajestic.

Average Daily Range % | Bigger relative range - better profits.(ENGLISH VERSION BELOW)

Die richtige Auswahl von Instrumenten ist essenziell. Wir können nur dann Profite machen, wenn das Instrument sich bewegt. Bekannte Indikatoren wie der ATR (Average True Range) inkludieren hier ebenfalls Kurslücken. Das ist gut, dennoch wollen wir Volatiltät von einem anderen Standpunkt betrachten. Welche Bewegungen sind also vom Hoch zum Tief möglich gewesen? Verständlicherweise können wir diesen Wert einer kleinen Aktie nicht mit TSLA vergleichen. Aus diesem Grund schauen wir uns die Relation zum Preis an. Somit können wir wirklich Äpfel mit Äpfel vergleichen. Je höher der Wert, desto mehr Range (basierend auf der 20 Tage-Historie und dem jeweiligen Preis). Natürlich funktioniert dieser Indikator auch in anderen Asset-Klassen wie Krypto, Forex etc.

Wichtig: Wende diesen Indikator im Tageschart an!

English version:

Stock selection is pretty important. We can only make decent profits if the underlying stock moves. Well-known indicators like the ATR (Average True Range) also include price gaps here. This is good, nevertheless, we want to look at volatility from another point of view. So, which movements were possible from high to low? Understandably, we cannot compare this value with TSLA for a small share. That's why we look at the relation to price.

The higher the value, the bigger the range (based on the 20-day history and the respective price).

Important: Use this indicator on a daily timeframe!

Cheers,

WirmachenTrader®

Demand & Supply Zone - Muthu SThis indicator marks Demand and Supply Zone on the chart based on various inputs. It also marks Boring candle in Blue colour & Explosive Candle in Black colour.

Prior knowledge of Demand and Supply Zone is mandatory to use this indicator effectively.

Kindly do your own math (based on your experience & knowledge) to identify the zones along with this indicator.

Boring & Explosive Candle - Muthu SThis Indicator marks Explosive candle (Black) and Boring Candle (Blue) on the chart based on various inputs like ATR Range, Legout Strength etc.

Explosive Candle - Muthu SThis Indicator marks Explosive Candle on the chart based on various inputs like ATR Range, Legout Strength etc.

AEONDRIFT {Expected Ranges}Expected Ranges base on AEONDRIFT implementation of Standard Deviation bands.

Note: In no way is this intended as a financial/investment/trading advice. You are responsible for your own investment/trade decisions.

Please PM me for access information.