Average Low/High Percentage DifferenceThis indicator calculates the Simple Moving Average of the difference in percentage between lows and highs of a candle. This assists in understanding the volatility of an asset. Showing this in percentages is more helpful in crypto.

Историческая волатильность

ADR% - Average Daily Range % by MikeC (AKA TheScrutiniser)This applies a 'corrected' formula to the version created by alpine_trader (which is slightly off). It calculates the Average Daily Range (in percent) over the previous 20 periods and plots it in a chart.

I am grateful to GlinckEastwoot for the 'corrected' formula.

OnTheMoveWith this plot one is able to compare the different % change in the given time frame. It calculates the sma of a given period (defval = 7) for the close/open.

Strategy would be to choose (trade) from one to other asset in order to get higher rates when pumping or lower when dumping.

The Symbol & exchange has to be specified.

defSymbols = BTC, ETH and LINK

defExchange = BINANCE

GBTC Fomo Panic PremiumIt is rumored that GBTC price action leads the Bitcoin market. This indicator compares GBTC fomo/panic levels to the (Binance) BTC spot market. Fomo is measured as large percentage moves of the high price from the min over a look-back period. Panic is measured as large percentage moves of the low price from the max over a look-back period. A prime example of this indicator's usage would be as a sell signal confirmation during the 2020 pre-Thanksgiving panic exhibited on the 1-hour chart while the 20 EMA was still above the 99 SMA.

You can customize the leading and lagging markets and the length of the lookback period. I would love to hear what parameters, markets and timeframes work for you. Maybe there is a way to leave comments, or hit me up on Twitter: @thirdreplicator

May you profit and enjoy.

Volatility Prism [Nic]What is this

The volatility rainbow tracks divergences in a security and its volatility index. This can be used to identify periods of heightened implied (future) risk.

About Volatility

The volatility is calculated by looking at put / call ratios. When VIX goes up it means that puts are outpacing calls. This is a bearish signal.

About Correlation

When the security goes up while the VIX goes up, the divergence on the plot will increase and turn a color. This should be a warning.

Volatility Rainbow

This is a similar indicator, but this one merges all signals into a single line.

IV/HV Ratio's [Nic]IV is implied volatility

HV is historic realized volatility

Seneca teaches that we often suffer more in our minds than in reality, and the same is true with the stock market. This indicator can help identify when people are over paying for implied volatility relative to real volatility . This means that short sellers are over paying for puts and can be squeezed into covering their positions, resulting in a massive rally.

The indicator can track this spread over many time frames, when the short time frame is much higher than the lower time frames, consider it a signal-of-interest.

Divergence Indicator [Nic]This divergence indicator can track the correlation between one or more symbols. I use it to track the divergences between the VIX volatility index, gold, bonds, as well as other market leading indicators.

When using with Vix, lower coefficients can lead to false signals. When in a high vix bear market signals, there is more noise and more false (or missing) signals can occur. Please use with other technical tools.

True Range in %I like to look at volatility in percentage and not in numbers. This is exactly what this script provides. It calculates the true range of a candle in percentage to the current price (for finished candles it uses it's close price).

The script also allows you to compare open and close prices.

2HLA very simple, almost naive strategy, in which you buy on the lowest of the two previous candles and sell at the highest of the two previous candles. You can configure these highest and lowest lenght, in some assets two is too small of a number to make profit. You can also configure to exit the position after X, and I found that 7 (which is a week of working days) is a good number for that.

This is strategy is intended to be used as a swing trade. Your capital needs to be high enough so that it can pay the operaitonal costs, and reach it's target with a reasonable profit.

Since this is a volatility based strategy, assets that are more liquid won't work properly.

Pisani BandsThis indicator is based on Historical Volatility.

It's plot the simple moving average with a upper and a lower band.

The bands are calculated like this:

UpperBand = 20 Simple moving average + 20% * Historical volatility

LowerBand = 20 Simple moving average - 20% * Historical volatility

But, you can change the paramters. I use the 200SMA with 100% of Historical Volatility either.

How to use:

If the price are negociating out of the bands, it's dangerous to trade this stock.

Hope you like it.

Long/Short Margin Ratio for cryptocurrenciesBTCUSDSHORTS and BTCUSDLONGS are like datasets provided by Bitfinex exchange. They record the number of margined for longs and shorts and they are measured in BTC (in case using BTCUSD ).

Margin is Like any loan, the borrower may pay interest while the loan is outstanding, and must eventually pay the loan back.

Red Area: More short margin than long margin.

Green Area: More long margin than short margin.

Note: Can only be used with cryptocurrencies that have such dataset within Bitfinex exchange like BTCUSD , ETHUSD , XRPUSD and a few more.

3 Leg Short Strangle BandsDraws 3 leg bands along with safe zone(green lines) based on input

1) Input ATR, Week Day, Current Market Close

2) Input ATR - Previous day 1H Max ATR

3) ADX < 25

4) Input Current Market Close

5) Trading Day - Mon/Tue/Wed/Thu/Fri - Bands distance calculated based on day M/Tu/F 2*(Max ATR), W/Th 1.5(ATR)

6) Safe zone green lines - CMPCls +/- (1.5 * Max ATR)

7) Leg 1 Upper Lower Legs - M/Tu/F - CMPCls +/-(2 * Max ATR), W/Th - CMPCls +/-(1.5 * ATR)

8) Leg 2 & 3 Calculates based on Leg 2 = Leg 1 +/- 100 pts distance, Leg 3 = Leg 2 +/- 100 pts distance'

9) All figures rounded to nearest 100's

10) Safe zone broken exit all positions

This is a popular technic used by Profitable traders on sideway markets for Intraday

One can keep 3K as SL per 1 set of 3 legs for better R:R

NIFTY VIX Bands1) The script takes current INDIA VIX as input Daily time frame for NIFTY

2) Used a Formula VIX Value / Square root of Time Period

3) Change Timeframe input accordingly 1 Year = 1, Monthly = 12, Weekly = 52, Daily = 365

4) based point 2 formula with 1 standard deviation it creates upper & lower range bands

5) This is generally used for option selling by big traders they go and sell above the band strikes

Standard Deviation Volatility HelperHere is a simple Standard Deviation Line based on supply and demand that will help you to find expected move easily. 3 Standart Deviation merged line available. Number of days and adjustable length.

Geometric Brownian Motion BandIf you are an option trader, who are constantly searching opportunities to set up inverse iron condor position or other strategies, you must be familiar in estimating the range induced by Geometric Brownian Motion (GBM), or Lognormal distribution someone may call.

The theory behind is adopted in the Black Scholes Option Pricing model, this assumes the asset price follows the GBM, shown below, and estimates the range where the price will fall into on the specific date and probability.

dS = a dt + v dW

Assuming the drift term is zero, this GBM Band applies the same model and helps you to quickly assess the suitable range to set up your option strategies with simple setting:

Length – number of bars covered

Vol Multiple - the z-score of the probability

Default values of the Length and Vol Multiple are set to 20 bars and 2.0 z-score respectively.

You can find an example how the GMB Band work.

You can also applies this GMB Band like how Bollinger's Band does for swing trade or breakaway trade.

If you find this indicator is useful to you, Star it, Follow, Donate, Like and Share.

Your support is a highly motivation for me.

Historical Volatility Percentile: Price and VolumeThis is an expansion of the Historical Volatility scripts to include both price and volume volatility.

As Tradingview states :

Historical Volatility is a measure of how much price (and now volume ) deviates from its average in a specific time period that can be set. The more price (or/and volume ) fluctuates, the higher the indicator value. Please note it does not measure the direction of price (and volume ) changes, just how volatile price/ volume has become. There are several reasons to care about volatility but it's mainly a risk measure. As volatility increases, so does risk and uncertainty and vice versa. Traders can use the indicator to flag instruments with high volatility which could point to a trend change. It is often used in combination with other signals.

Example options

Example formats

Link back to some other great ideas:

@Cheatcountry with his prolific sharing , what a great inspiration.

@Picte and his inspired idea .

@Balipour and his great script

Comparing this to other significant HVP indicators

Realized Volatility IIR Filters with BandsDISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The following indicator was made for NON LUCRATIVE ACTIVITIES and must remain as is following TradingView's regulations. Use of indicator and their code are published by Invitation Only for work and knowledge sharing. All access granted over it, their use, copy or re-use should mention authorship(s) and origin(s).

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED AS TESTING. The models included in the indicator have been taken from open sources on the web and some of them has been modified by the author, problems could occur at diverse data sceneries.

WHAT'S THIS...?

Work derived by previous own research for study:

This is mainly an INFINITE IMPULSE RESPONSE FILTERING INDICATOR , it's purpose is to catch trend given by the nature of lag given by a VOLATILITY ESTIMATION ALGORITHM as it's coefficient. It provides as well an INFINITE IMPULSE RESPONSE DEVIATION FILTER that uses the same coefficients of the main filter to plot deviation bands as an auxiliary tool.

The given Filter based indicator provides my own Multi Volatility-Estimators Function with only 3 models:

ELASTIC VOLUME WEIGHTED VOLATILITY : This is a Modified Daigler & Padungsaksawasdi "Volume Weighted Volatility" as on DOI: 10.1504/IJBAAF.2018.089423 but with Elastic Volume Weighted Moving Average instead of VWAP (intraday) for faster (but inaccurate) calculation. A future version is planned on the way using intra-bar inspection for intraday timeframe as described in original paper.

GARMAN & KLASS / YANG-ZANG EXTENSION : As one of the best range based (OHLC) with open gaps inclusion in a single bar.

PETER MARTIN'S ULCER INDEX : This is a better approach to measure realized volatility than standard deviation of log returns given it's proven convex risk metric for DrawDowns as shown in Chekhlov et al. (2005) . Regarding this particular model, I take a different approach to use it as coefficient feed: Given that the UI only takes in consideration DrawDawns, I code myself the inverse of this to compute Draw-Ups as well and use both of them to filter minimums volatility levels in order to create a SLOW version of the IIR filter, and maximums of both to calculate as FAST variation. This approach can be used as a better proxy instead of any other common moving average given that with NO COMPOUND IN TIME AT ALL (N=1) or only using as long as N=3 bars of compund, the filter can catch a trend easily, making the indicator nearly a NON PARAMETRIC FILTER.

NOTES:

This version DO NOT INCLUDE ALERTS.

This version DO NOT INCLUDE STRATEGY: ALL Feedback welcome.

DERIVED WORK:

Incremental calculation of weighted mean and variance by Tony Finch (fanf2@cam. ac .uk) (dot@dotat.at), 2009.

Volume weighted volatility: empirical evidence for a new realised volatility measure by Chaiyuth Padungsaksawasdi & Robert T. Daigler, 2018.

Basic DSP Tips & Trics by TradingView user @alexgrover

CHEERS!

@XeL_Arjona 2020.

Bitcoin Implied VolatilityThis simple script collects data from FTX:BVOLUSD to plot BTC’s implied volatility as a standalone indicator instead of a chart.

Implied volatility is used to gauge future volatility and often used in options trading.

SPY Expected Move by VIXThis indicator shows 1 and 2 standard deviation price move from the VWAP based on VIX. Implied Volatility (IV) is being used extensively in the Option world to project the Expected Move for the underlying instrument. VIX is used as a proxy for SPY's IV for 30 days.

This indicator is meaningful only for SPY but can be used in any other instrument which has a strong correlation to SPY.

Historical Volatility Percentile + SMAHistorical Volatility Percentile tells you the percentage of the days from the past year (252 trading days) that have lower volatility than the current volatility.

I included a simple moving average as a signal line to show you how volatile the stock is at the moment.

I have included simple colors to let you know when to enter or exit a position.

Buy when price higher than EMA & historical volatility higher than SMA

Sell when price lower than EMA & historical volatility higher than SMA

Please let me know if you would like me to publish any other indicators! I always love to hear from you guys.

Volatility SkewThis indicator measure the historical skew of actual volatility for an individual security. It measure the volatility of up moves versus down moves over the period and gives a ratio. When the indicator is greater than one, it indicators that volatility is greater to the upside, when it is below 1 it indicates that volatility is skewed to the downside.

This is not comparable to the SKEW index, since that measures the implied volatility across option strikes, rather than using historical volatility.

Moving Average Adaptive FilterThe Moving Avg Adaptive Filter (MAAF) was authored by Perry Kaufman in the Stocks and Commodities Magazine 03/1998

This is a volatility based indicator so when this indicator goes up, sell in the direction of how that stock is going. In other words go short when it is rising and the stock price is below the ema or go long when it is rising and the stock price is above the ema. Lower volatility means it is trading sideways or the current price action is about to reverse.

Send me a message and let me know what other indicators you would like to see!

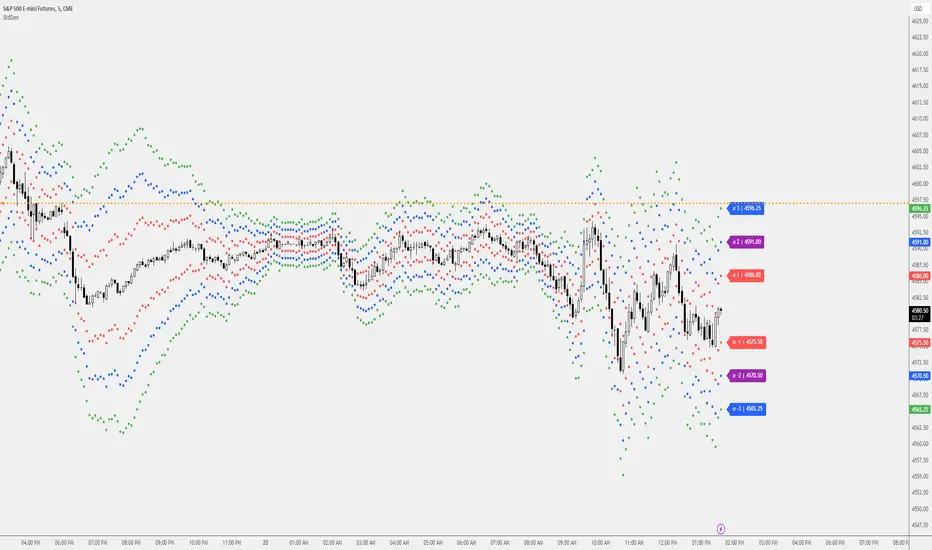

Standard Deviation Measurement ToolIf you like the script please come back and leave me a comment or find me on the interwebs. I get notified you "liked" it... but I have no idea if you actually use it. So, let me know =)

The script uses the open price as the mean and calculates the standard deviation from the open price on a per candle basis

- Goal: -

To establish a mean based on the Open Price and calculate the standard deviation.

The reason for this is if the Open is the mean, then the Standard deviation implies a standardized distance a given candle can be expected to travel

from the open price

- Edge: -

If you know that there is a 68%/95%/99.7% probability that price will NOT move more than

One Standard Deviation/Two Standard Deviations/Three Standard Deviations from the open price respectively

you can set reasonable price targets that relate to those probabilities in a given timeframe.

e.g. if you're on a 1h chart and your target is 3.5% from the open price, but 1 standard deviation of the hourly candle is equal to 0.78%.

You can make assumptions on either:

- The reasonableness of your target

or

- The holding period likely required for the trade.

Also, Standard Deviation is a function of volatility and this tool provides a unique mechanism for measuring volatility as well on a candle by candle basis

- Customization Options-

- Set 3 independent upper and lower standard deviations.

- Each set of standard deviations are on a switch so you can show 1, 2, or 3 sets of standard deviations

- You can set the distribution width

- Though it's not recommended, you can change the mean source.

- There is a switch to show the standard deviation on only the real-time bar or real-time and historical bars.

- How I Think About This Script -

This strategy is predicated the same principle as Bollinger Bands: the reality that 68% of all data points will fall within one standard deviation of the mean, 96% of all data points will fall within two standard deviations, and 98% of al data points will fall within 3 standard deviations. By understanding the standard deviation, you can possibly infer an edge by understanding the probabilistic range price will be bound to the limits of standard deviation rules according to their probabilistic outcomes for the single candle on any given timeframe. Bollinger Bands are designed to provide this information with the mean being a 20-period moving average and this indicator.

This indicator is designed to provide standard deviation information with the mean being based on the distance price travels away from the open of individual candles in the lookback period.

If you use a strategy where you enter on major candle closes, this can be useful to set targets for those entries based on the intended hold period or at least add/remove validity to other target metrics.

Example:

Your target is at the 1.618 Fibonacci level and your confirmation triggers on the 4h candle close (H4 if that's your thing lol). You set up the indicator based on the standard deviation of price movement in 4h candles over the last week.

Let's say the indicator shows that the 1.618 Fibonacci level is 3 standard deviations away.

This being the case this statistically indicates that within the next 4 hours, you have a very low probability of achieving your target (>2%). This doesn't invalidate your target, but it does indicate a low probability of achieving it in the next 4hrs. With this information, you can infer that you are either going to be (a) really lucky (b) in this trade for a lot longer than 4hrs or (c) your target is unrealistic given your intended hold period.

You can develop a more probabilistically favorable hold period calculation by looking at the standard deviation on a higher time frame (e.g. 1d-1w).

Bonus feature: You'll find that the 2 and 3 standard deviations will often "cluster" and these clusters often provide future S/R levels. That's a pretty sweet feature no one things to look for. But, try it. Find a cluster of 2nd and 3rd stdevs that are in somewhat of a horizontal pattern (usually the result of a range) and you'll find that to be a good s/r area. Even better if you use the 3.2 standard deviation, you'll find that is a fantastic breakout signal!

Summary

So, you can use it for target setting, a confluence test, a reasonableness test, or just a measurement tool.

This was the first TV script I ever wrong.. Got taken down. But, I've re-released it because there are other TV scripts that attempt to do this but are completely wrong.

Please be careful about using other people's scripts. Always validate the math of the script before you use it if possible.

Stay safe out there and I hope all your dreams come true.