Nearest Percentile Moving Average BandsWhile coding some filters into another indicator for Long/Short I noticed that ta.nearest.percentile might be the most useful tool in pinescript I've ever encountered.

While percentile_nearest can be used for all kind of things I decided to code moving averages from it and made bands for bottom percentage and top percentage.

The indicator will calculate the top % price of the given bar length.

Example settings:

length: 150

percentile: 99

So when using 99% it will draw a green line when price is moving above the top 1% price of the last 150 candles. It then calculates if the price is below the bottom 1% of the last 150 candles.

Trading use:

Use this indicator to check if the market is leaving normal territory. This signals a breakout move for example the dogecoin pump or the top of the range. I use this indicator to catch bull/bear moves for botting purposes. An other use would be to countertrend trade after the move has ended. With price being in top 1% for a while it is very probable that we see a large correction.

Below example of dogecoin pumps:

Историческая волатильность

SVDThis indicator aims to compare between two charts if trader isn't sure which one is more active and powerful, it does NOT show entries or help your chart analysis directly.

The main features of this indicator is to show vitality and range of any given chart.

Volatility: it calculates the average profit of every swing in the range and the final result will be the chart volatility, which indicate how profitable this chart is.

Range: it calculates the profit of the whole range compared to the total price. (E.g. range bottom is 0.1 and range top is 0.2 the range will be 100%)

Extra: indicator shows the total direction of the chart in term of (STRONG UPTREND, UPTREND, SIDEWAYS, DOWNTREND, STRONG DOWNTREND), if you got (Somthing_wrong) please contact me.

How to use: apply the indicator on different charts that you have chosen and the higher (volatility & range) the more profitable the chart is.

inputs:

Lookback length: how long the range is (how many candles are included).

How intense should the Swing be: how many candles should be counted as a confirmation complete swing.

Show counted Swings: if checked as true, will show the swings counted in the volatility calculation.

For any notes on the indicator to be edited, or for another indicator ideas please comment.

Percentage Range IndicatorThe Percentage Range Indicator is useful for assessing the volatility of pairs for percentage-based grid bots. The higher the percentage range for a given time period, the more trades a grid bot is likely to generate in that period. Conversely, a grid bot can be optimised by using grids that are less than the Percentage Range Indicator value.

I have been using the Percentage Range Indicator based on the one hour time period and 168 periods of smoothing (seven days based on one-hour periods).

Enjoy.

Basic Shannon Entropy & DerivativesThis script performs the basic Shannon entropy on the closing value of the stock. Additionally, it performs the trailing first and second derivatives of the Shannon Entropy, giving you more information about its movement.

You can change the "Source" to be whatever value you like.

Sessions with High/Low DiffThe main purpose of this indicator is to facilitate backtesting, but it may also be useful for traders to easily identify the current

active/open trading sessions on lower-timeframe charts.

This indicator also tracks the session high/low difference and plots it as a label on the last candle of the session once the last

bar of that session has finished printing and a new candle opened. The position and direction of the label is based on the

session open and close - if the session open is greater than the session close (which would equate to the equivalent of a red candle),

the label will be printed UNDER the last candle, and vice versa if the session close is above the session open.

The number printed inside the label is the difference between the session high and the session low, scaled to the minimum tick value of the chart.

Note #1: There is a Pinescript maximum of 500 labels allowed on any chart. While I could have gotten fancy and done some wizardry with label arrays,

I didn't really see a point to it. If labels are enabled for all 4 sessions at the same time, that would still have them available for the past 125

sessions, which would be about 6 months (approx 252 trading days per year, and this would cover 125 of them). If you limit to 2 sessions, you double

your potential look-back to almost a year (250 days out of the 252 average trading days each year), and for a single session, you double it yet again

to just under 2 years.

Note #2: As this indicator tracks open, high, low, and close for each session, it can potentially be enhanced (or forked) to construct "session candles".

I'm not sure what use this would be to anyone, but the pieces are there should someone find a use for it.

While it would be easy to add alerts on sessions opening/closing, I didn't see a purpose or value in that as it would be little more than a

glorified alarm clock. If I get enough demand to add them, I will gladly consider it.

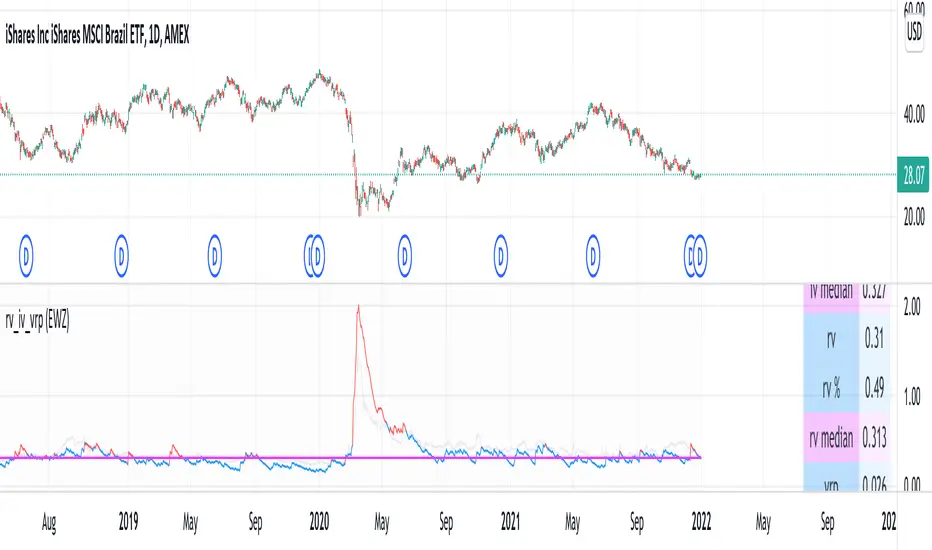

rv_iv_vrpThis script provides realized volatility (rv), implied volatility (iv), and volatility risk premium (vrp) information for each of CBOE's volatility indices. The individual outputs are:

- Blue/red line: the realized volatility. This is an annualized, 20-period moving average estimate of realized volatility--in other words, the variability in the instrument's actual returns. The line is blue when realized volatility is below implied volatility, red otherwise.

- Fuchsia line (opaque): the median of realized volatility. The median is based on all data between the "start" and "end" dates.

- Gray line (transparent): the implied volatility (iv). According to CBOE's volatility methodology, this is similar to a weighted average of out-of-the-money ivs for options with approximately 30 calendar days to expiration. Notice that we compare rv20 to iv30 because there are about twenty trading periods in thirty calendar days.

- Fuchsia line (transparent): the median of implied volatility.

- Lightly shaded gray background: the background between "start" and "end" is shaded a very light gray.

- Table: the table shows the current, percentile, and median values for iv, rv, and vrp. Percentile means the value is greater than "N" percent of all values for that measure.

-----

Volatility risk premium (vrp) is simply the difference between implied and realized volatility. Along with implied and realized volatility, traders interpret this measure in various ways. Some prefer to be buying options when there volatility, implied or realized, reaches absolute levels, or low risk premium, whereas others have the opposite opinion. However, all volatility traders like to look at these measures in relation to their past values, which this script assists with.

By the way, this script is similar to my "vol premia," which provides the vrp data for all of these instruments on one page. However, this script loads faster and lets you see historical data. I recommend viewing the indicator and the corresponding instrument at the same time, to see how volatility reacts to changes in the underlying price.

Portfolio Performance - Effects of RebalancingFunction:

- Can be used to evaluate the performance of a portfolio containing 2 assets over a set time interval

- Shows the % return of the portfolio over the time interval defined by the user

- Includes a threshold rebalancing algorithm to show the effects that rebalancing has on the portfolio over the long term

- Created to evaluate of the performance of portfolios containing different weightings of stocks and bonds over time assuming that the user would rebalance the portfolio when asset weights crossed a threshold

Instructions:

- To be used with dividends adjustments turned on

- Add this script to a symbol. e.g. AMEX:SPY

- Click the chart to define the entry time and the exit time. i.e. the time interval

- Define the initial investment of the portfolio. Default setting is $100,000

- Define the second asset to be included in the portfolio. e.g. BATS:AGG

- The strategy comes pre-populated with a portfolio that has a weight of 80% asset 1 and 20% asset 2. i.e. 80% AMEX:SPY and 20% BATS:AGG if the symbols mentioned above were chosen

- The 7 lines show the weighted % return of each portfolio over the time period defined by the user

- Each line (except the blue) is the return based on a different rebalancing threshold. The default settings are 1%, 2.5%, 5%, 10%, 15%, 20%, 30%

- The blue line is the % return of a portfolio that was made up of 100% asset 1 over the time interval. i.e. 100% AMEX:SPY

- Asset weights and rebalancing thresholds are adjustable via the settings

- Each plot can be turned on and turned off via a tick box in the settings

[BM] SSS 50% Rule EvaluatorSara Strat Sniper 50% Rule Evaluator

█ OVERVIEW

This indicator is based on Sara Strat Sniper's - 50% Rule for trading Outside Bars and helps you to evaluate the historical success rate of that rule.

█ FEATURES

Calculation

• You can choose to evaluate only the current bar to see if it forms an outside bar (success) or not (fail), but you can also choose to include the next bar to see if that one forms a compound outside bar.

• You can enable a start and/or end date to limit the calculation period.

Table

• Show or hide the table with the calculation results.

• Show or hide the calculation details (up/down data).

• Position of the table, opacity, cell width and text size can be customized.

Colors

• Table colors can be customized.

• You can choose to show the inside/outside bars in customizable bar colors.

• You can choose to identify successful/failed/recovered outside bars in customizable background colors.

█ LIMITATIONS

• This script uses a special characteristic of the `security()` function allowing the inspection of intrabars — which is not officially supported by TradingView.

• Intrabar inspection only works on some chart timeframes: 5, 10, 15, 30, 45 and 195 minutes, 1, 2, 3, 4, 5, 6, 7 and 8 hours, 1, 2, 3, 4 and 5 days, 1, 2, 3 and 4 weeks, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11 and 12 months. The script’s code can be modified to run on other resolutions.

• There is a limit to how far back intrabar calculations can be performed, and is dependant on both the intrabar resolution and your subscription (which determines the number of available bars).

ETHE PremiumShows the premium/discount for Grayscale ETHE vs. the fractional amount of ETH per share held.

GBTC PremiumCalculates the historical and current premium/discount for a share of Grayscale GBTC vs. Bitcoin spot price.

Portfolio Performance - 2 AssetsFunction:

- Can be used to evaluate the performance of portfolios containing 2 assets over a set time interval

- Created to evaluate of the performance of portfolios containing different weightings of stocks and bonds over time

- Shows the % return of each portfolio over the time interval defined by the user

- Capable of showing the risk adjusted % return of each portfolio over the time interval defined by the user (setting turned off by default)

Instructions:

- To be used with dividends adjustments turned on

- Add this script to a symbol. e.g. NASDAQ:BND

- Click the chart to define the entry time and the exit time. i.e. the time interval

- Define the second asset to be included in the portfolio. e.g. AMEX:VOO

- The strategy comes pre-populated with 6 portfolios with the most common stock/bond weightings (100% stocks/0% bonds, 80% stocks/20% bonds, 60% stocks/40% bonds, et cetera)

- The 6 lines show the weighted % return of each portfolio over the time period defined by the user

- All asset weights are adjustable via the settings

- Each plot can be turned on and turned off via a tick box in the settings

- There are 6 plots that show the risk adjusted returns of each portfolio (setting turned off by default)

Live off your portofolio (decumulate)This indicator simulates living off your portofolio consisting of a single security or stock such as the SPY etf or even Bitcoin. The simulation starts at a certain point on the chart (which you input as year and month).

Withrawals from the portofolio are made each month according to the yearly withdrawal rate you enter, such as the 4% SWR. The monthly withdrawal income is calculated in USD at the beginning of the retirement period and then adjusted according to the US inflation (CPI) on 01/01 of each year.

The blue graph represents the USD value of the remaining portofolio.

This indicator is meant to be used on daily, weekly or monthly time frame. It may not work properly (and makes little sense to use) on intraday timeframe or larger time frames such as quarterly (3M).

When withdrawing, the indicator considers that fractional stock values can be used (the portofolio value is kept as a float). This may not be true, as most stock brokers currently don't allow this.

It does not explicitly take into account dividends. In order to do this you will have to enable "Adjust for dividends" by clicking on "adj" in the lower right corner of the screen, or by using the indicator on a Total Return (TR) index such as DAX. Unfortunately SPX does not have dividend data, you will have to use the SPY etf (which doesn't have a long history)

Price Action [Morty]This price action indicator uses the higher timeframe SSL channel to identify trends.

The long entry signal is a bullish candlestick pattern when the price retraces to EMA20 in an uptrend.

The short entry signal is a bearish candlestick pattern when the price retraces to the EMA20 in a downrend.

Currently, this indicator shows engulfing patterns, pin bar patterns, 2 bar reversal patterns and harami patterns.

It also shows a volatility squeeze signal when the Bollinger bands is within the Kelter channels.

The buy and sell signal can also be filter by the ADX indicator greater than a threshold.

You can set your stoploss to the previous low/high when you go long/short.

The risk/reward ratio could be 1 to 1.5.

This indicator can be used in any market.

VixFix RVol + EMAThis indicator plots Realised Volatility (measured using VixFix method) against its long-term exponential moving average.

RVol breaking above its EMA = Sell signal

RVol breaking below its EMA = Buy signal

60-day VixFix look back period and 900 day EMA work well for lower volatility tickers (equity ETFs, megacap stocks). Higher volatility tickers could benefit from shorter look back period and EMA.

Outside DayThis strategy is taken from Perry Kaufman's book "Trading System and Methods".

You can enter on the direction of the candle, or opposite to it. I find that the opposite tends to yield better results in volatile assets, allowing a better reward to risk ratio. There is no stop loss in this strategy, only a fixed take profit and a time limitation.

Average Daily RangeRe-Re-upload!

There are a handful of decent Average Daily Range indicators out there.

Often they are built using Pinescript v2 (severely outdated) or have no customization or are "Closed Source"

In this version, you can select two multipliers to display on chart

Primary Mult - Large Green or Red crosses, by default set to 1 or 100% of ADR

Secondary Mult - Small Aqua or Maroon crosses, by default set to 0.5 or 50% of ADR

Cheers,

EFX

Advanced Forex SessionsEssential for ALL Forex Day Traders!

Don't waste your time trading Forex Sessions with little to no volume or volatility!

The Advanced Forex Sessions tool will search through all 4 sessions, tally up the total volume and ticks moved, and show you which session has the most movement.

It will show you the two best sessions on chart and optionally color the background too.

Configure the position & size of the Infographic table as well as custom Forex Session times and colors.

Forex Trading SessionsThere are a million Forex Trading Session indicators out there, but I couldn't find one with all of the following requirements:

1. Automatically show the Sessions that actually affect the current pair (for instance, Tokyo session doesn't matter when trading EURGBP)

2. Editable colors or at the very least no distracting colors

3. Editable times for each exchange session

4. Unique indication of the start of a session vs the end of a session. (Sometimes, I don't notice a background going from Navy Blue to Black)

This indicator has everything I could ever want in a Sessions Tool:

Subdued default colors

Editable colors

Editable session ranges

Obvious, but not obnoxious indication of start and stop

Automatically hide irrelevant Sessions

Cheers. EFX

Bar StatisticsThis script calculates and displays some bar statistics.

For the bar length statistics, it takes every length of upper or lower movements and calculates their average (with SD), median, and max. That way, you can see whether there is a bias in the market or not.

Eg.: If for 10 bars, the market moved 2 up, then 1 down, then 3 up, then 2 down, and 2 up, the average up bars length would be at 2.33, while the average for the down length would be at 1.5, showing that upper movements last longer than down movements.

For the range statistics, it takes the true range of each bar and calculates where the close of the bar is in relation to the true low of it. So if the closing of the bar is at 10.0, the low is at 9.0, and the high is at 10.2, the candle closed in the upper third of the bar. This process is calculated for every bar and for both closing prices and open prices. It is very useful to locate biasses, and they can you a better view of the market, since for most of the time a bar will open on an extreme and close on another extreme.

Eg.: Here on the DJI, we can see that for most of the time, a month opens at the lower third (near the low) and closes at the upper third (near the high). We can also see that it is very difficult for a month to open or close on the middle of the candle, showing how important the first and the last day are for determining the trend of the rest of the month.

myRangestatCalculates the average daily range as well as the standard deviation of the daily range over a given period.

Adding both values gives you a statistical range (bottom to top or top to bottom) in which price can be expected to move.

pricing_tableThis script helps you evaluate the fair value of an option. It poses the question "if I bought or sold an option under these circumstances in the past, would it have expired in the money, or worthless? What would be its expected value, at expiration, if I opened a position at N standard deviations, given the volatility forecast, with M days to expiration at the close of every previous trading day?"

The default (and only) "hv" volatility forecast is based on the assumption that today's volatility will hold for the next M days.

To use this script, only one step is mandatory. You must first select days to expiration. The script will not do anything until this value is changed from the default (-1). These should be CALENDAR days. The script will convert to these to business days for forecasting and valuation, as trading in most contracts occurs over ~250 business days per year.

Adjust any other variables as desired:

model: the volatility forecasting model

window: the number of periods for a lagged model (e.g. hv)

filter: a filter to remove forecasts from the sample

filter type: "none" (do not use the filter), "less than" (keep forecasts when filter < volatility), "greater than" (keep forecasts when filter > volatility)

filter value: a whole number percentage. see example below

discount rate: to discount the expected value to present value

precision: number of decimals in output

trim outliers: omit upper N % of (generally itm) contracts

The theoretical values are based on history. For example, suppose days to expiration is 30. On every bar, the 30 days ago N deviation forecast value is compared to the present price. If the price is above the forecast value, the contract has expired in the money; otherwise, it has expired worthless. The theoretical value is the average of every such sample. The itm probabilities are calculated the same way.

The default (and only) volatility model is a 20 period EWMA derived historical (realized) volatility. Feel free to extend the script by adding your own.

The filter parameters can be used to remove some forecasts from the sample.

Example A:

filter:

filter type: none

filter value:

Default: the filter is not used; all forecasts are included in the the sample.

Example B:

filter: model

filter type: less than

filter value: 50

If the model is "hv", this will remove all forecasts when the historical volatility is greater than fifty.

Example C:

filter: rank

filter type: greater than

filter value: 75

If the model volatility is in the top 25% of the previous year's range, the forecast will be included in the sample apart from "model" there are some common volatility indexes to choose from, such as Nasdaq (VXN), crude oil (OVX), emerging markets (VXFXI), S&P; (VIX) etc.

Refer to the middle-right table to see the current forecast value, its rank among the last 252 days, and the number of business days until

expiration.

NOTE: This script is meant for the daily chart only.

Average Daily Range Fibonacci LevelsThe Average Daily Range is a simple concept, calculated as the difference between daily highs and lows averaged over some period. This indicator uses that range in conjunction with Fibonacci ratios to create zones centered on the day's open that tends to act as areas of support and resistance.

The thicker White lines are the ADR levels; all other lines are the same value adjusted by the various Fibonacci values.

A simpler version of this concept can be seen in my other script, Average Daily Range Zones, which does not include the Fibonacci ratio zones.

Thanks to @Hank Hill for the original idea and TV for the feedback and support on the use of the security() function.

Also thanks to @GoldenCross for the Fibonacci obsession.

Average Daily Range ZonesThe Average Daily Range is a simple concept, calculated as the difference between daily highs and lows averaged over some period. This range is is overlaid and centered on the day's open, and tends to act as areas of support and resistance . This indicator provides two aggregation periods, creating a range that represents volatility in the ADR; a wider spread indicates greater recent volatility , and vice-versa.

Thanks to @Hank Hill for the original idea and ToS script this is based on, and TV for the feedback and support on the use of the security() function.