Regime Filter [CHE]About:

A market regime filter is a tool used by traders and investors to identify the current state or "regime" of the market and adjust their investment strategies accordingly. This can involve identifying trends in market behavior, such as bullish or bearish trends, and using that information to make decisions about which assets to buy or sell.

Market regime filters can be based on a variety of factors, including economic indicators, market sentiment, and technical analysis. They are often used in conjunction with other trading strategies and can help traders and investors manage risk and optimize their returns.

It's important to note that market regime filters are not always accurate and can change over time, so it's important for traders and investors to regularly review and update their filters to ensure that they are relevant and effective.

Understanding the use of a regime filter in trading:

The importance of a trading filter cannot be overemphasized. As a matter of fact, the chances of any trading system making consistent returns over the long term depends on it trading in the right market environment — buying when the market is bullish and selling when the market is bearish. Some traders may want to stay out of the market when the conditions are unfavorable.

The heard of this Regime Filter is the well kown Andean Oscillator. The proposed indicator aims to measure the degree of variations of individual up-trends and down-trends in the price, thus allowing to highlight the direction and amplitude of a current trend.

Settings

Length : Determines the significance of the trends degree of variations measured by the indicator.

Signal Length : Moving average period of the signal line.

The regime filter uses the color yellow and blue, yellow stands for bullish and blue for bearish.

In daily use I have found that it makes sense to use it in different timeframes to identify meaningful trends.

best regards and I hope you enjoy this new indicator

Chervolino

Forecasting

Clean ADX with bidirectional Breakout VolumeThe default Average Directional Index (ADX) helps traders determine the strength of a trend, not its actual direction. The Clean ADX helps traders determine the strength of a trend on a longer time, and the possible direction on different timeframes.

The bidirectional Breakout Volume determines both directions of breakout or breakdown volume. When volume is high by comparing the previous volume high over n periods to the current volume or when volume is lower by comparing the previous volume low over n periods to the current volume.

If the current volume exceeds the previous volume high or low, then the indicator columns will turn red or green.

This indicator should make trading easier and improve analysis. Nothing is worse than indicators that give confusingly different signals.

The combination of the first and second indicator therefore makes perfect sense to me and now you are able to find your long or short trends earlier.

I hope you enjoy my new ideas

best regards

Chervolino

Odd_mod Econ CalendarA modification of Economic Calendar Events: FOMC, CPI, and more written by jdehorty . Please send all tips his way as he is maintaining the underlying data for the Calendar and the original concept.

List of changes:

Optimized code, will only run once on initialization now(No random line in middle of screen on bar change)

Legend - Added short names

Legend - Removed header

Legend - Made repositionable with selectable top margins

Legend - Removed data name from legend when it is disabled

Legend - Removed border

Original Description by jdehorty :

This script plots major events from the Economic Calendar that often correspond to major pivot points in various markets. It also includes built-in logic to retroactively adjust larger time intervals (i.e. greater than 1 hour) to be correctly aligned with the interval during which the event occurred.

Events are taken from the Economic Calendar and will be updated periodically at the following library:

EconomicCalendar

The above library can be used to conveniently access date-related data for major Meetings, Releases, and Announcements as integer arrays, which can be used in other indicators. Currently, it has support for the following events:

FOMC Meetings

The FOMC meets eight times a year to determine the course of monetary policy . The FOMC's decisions are based on a review of economic and financial developments and its assessment of the likely effects of these developments on the economic outlook.

FOMC Minutes

The FOMC minutes are released three weeks after each FOMC meeting. The minutes provide a detailed account of the FOMC's discussion of economic and financial developments and its assessment of the likely effects of these developments on the economic outlook.

Producer Price Index (PPI) Releases

The Producer Price Index (PPI) measures changes in the price level of goods and services sold by domestic producers. The PPI is a weighted average of prices of a basket of goods and services, such as transportation, food, and medical care. PPI is a leading indicator of CPI .

Consumer Price Index ( CPI ) Releases

The Consumer Price Index ( CPI ) measures changes in the price level of goods and services purchased by households. The CPI is a weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. CPI is one of the most widely used measures of inflation .

Consumer Sentiment Index ( CSI ) Releases

The University of Michigan's Consumer Sentiment Index ( CSI ) is a measure of consumer attitudes about the economy. The CSI is based on a monthly survey of U.S. households and reflects the consumers' assessment of present and future economic conditions. The CSI is a leading indicator of consumer spending, which accounts for about two-thirds of U.S. economic activity.

Consumer Confidence Index ( CCI ) Releases

The Consumer Confidence Index is a survey that measures how optimistic or pessimistic consumers are regarding their expected financial situation.

Non-Farm Payroll (NFP) Releases

The Non-Farm Payroll (NFP) is a measure of the change in the number of employed persons, excluding farm workers and government employees. The NFP is a leading indicator of consumer spending, which accounts for about two-thirds of U.S. economic activity.

M0PB (Momentum Pullback)Long/short strategy that identifies extreme readings on the rsi as a *momentum signal*, unlike most RSI strategies the script will look to buy or sell the first pullback in the direction of the extreme RSI reading.

Enters positions on the first pullback to the 5ema(low)/ 5ema(high) and exits at rolling 12 bar high/ low. The rolling high/ low feature means that if the price enters into a prolonged consolidation the profit target will begin to reduce with each new bar. The best trades tend to work within 2-6 bars.

Built for use on 5 min intervals on FX, Indexes, and Crypto. Lower than 5 minute time frames tend to be noisier and mean more commissions and a higher risk of slippage so the suggested timeframe is 5 mins.

Hard stop is X ATR (users can experiment with this) from the position entry price. This can be adjusted in user inputs.

There is a lot of slack left in entries and exits but the overall strategy is fairly robust across timeframes and markets and has between 60%-70% win rate with larger winners.

Signals that occur from economic news volatility are best avoided.

High Impact NewsDo you have a difficult time remembering high-impact news events throughout the trading week? Now there is an indicator that allows the user to put labels directly on their charts at specific times in the future so news events won’t sneak up on the user.

Description

The “High Impact News” TradingView indicator by Infinity Trading gives the user complete control of three labels that can be set to any time and day of the trading week, even in the future. Each label can be displayed at a specific time, on a unique day of the week, and with custom text. Also, each label has a choice of over 20 emojis to display on the chart along with user-defined text. The text color and size can be independently adjusted.

The position of the labels on the chart can be easily moved up or down with 5 built-in presents: Current Week High, Current Day High, Current Price, Current Day Low, and Current Week Low. Additionally, each label has a separate buffer that allows the users to move the label up or down in increments of five. All of these user-controls ensure the labels are exactly where the user wants them on their charts.

Limitations

This indicator displays labels in the future. TradingView sets a limit of 500 bars/candles in the future you can interact on. This TradingView limit means that labels can only be drawn 500 candles in the future on any timeframe. On larger timeframes this is not a problem and one trading week can easily display any labels. But on smaller timeframes labels multiple days in the future will exceed the 500 candle limit. When a label exceeds the 500 candle limit the indicator will have a temporary error. THIS IS NOT A PROBLEM. Simply go back to a higher timeframe or wait until the label is within 500 candles. All of your Settings will be saved! This is just a limit placed by TradingView that cannot be overwritten.

Important Notice

As stated above, this indicator draws labels in the future on your charts. To achieve future labels, this indicator draws labels in the present and shifts them to the right (which is the future) certain number of bars. Please be aware of the following characteristics of this indicator:

Labels will not appear until after midnight EST on Monday of each trading week

Labels will not appear over the weekends

Labels set to “Monday” won’t appear until midnight EST on Monday (or later)

Labels set to “Tuesday” through “Friday” won’t appear until the time specified in the Settings on Monday. For example, a FOMC label set to 2pm EST on Wednesday will not appear on the chart until 2pm EST on Monday

On 1-Hour or 2-Hour charts, please note that labels with a non-hour time will be shifted slightly so they appear on the chart. For example, a label at 8:15 am on the 5-min chart will be adjusted to 8:00 am on the 1-Hour chart so the label will appear

The above characteristics are a result of having to draw the labels at a specified time (of the trading week) and then calculating how many bars it takes to get the label to the correct time in the future.

Bands Bands (BanB)This indicator uses bands to show the trend of other bands.

The middle bands are used to show the price trend and the other bands are for the middle bands.

The Spike and Plunge bands can also act as a sort of "Bollinger Bands" for middle bands, though not exactly.

----- HOW TO USE IT -----

Zoom out in the 30 minute chart. Use 15 minute chart to pinpoint your entries.

Use with price-action trading and with indicators showing overbought & oversold levels.

The numbers below correlate with the numbers in the chart.

1) Price hits the Middle Spike line. The "ARL" bands hit the Bottom Spike line. This is a good indication that price will proceed under the Bottom Spike line.

2) Price hits the Bottom Plunge line. The "ARL" bands hit the Middle Plunge line. This is a good indication that price will proceed above the Middle Plunge line.

3) Notice how price spikes up near the Spike lines but doesn't touch. Notice how the Plunge lines have a strong pull downwards. This shows a continued down trend.

4) The same pattern as numbers 2 & 3 reoccur. This time, however, the proceeding price spike is substantially lower.

5) The price and middle bands finally bounce off the Top Plunge line and starts to get closer to the Spike bands.

6) Price and middle bands finally touch the Bottom Spike line and the Spike Bands and the Plunge Bands come closer together.

7) Narrowing Spike and Plunge Bands show a sideways market. Notice number 1, the bands are far apart -- more volatility is present.

Middle Bands:

The bottom, blue lines are fairly accurate dip-rebounds on the 30 minute chart. Use level indicators to find reversing trends (e.g., RSI, Stoch, etc.).

Price action hovering in between the blue lines and around the center indicate a low volatility market or a consolidating market.

----- HOW THIS INDICATOR IS ORIGINAL; WHAT IT DOES AND HOW IT DOES IT -----

This indicator has an original, unique ability to view the trend of bands in a substantially larger overview when zoomed out.

Normally, one would have to switch to higher time frames to get a sense of a larger market trend.

However, doing so will change any bands indicator to accommodate the new price action in relation to the new time frame.

To avoid this, the middle bands are placed in between two bands to see the trend of the bands that show the trend of price action.

----- VERSION -----

The "ARL Bands" in this indicator are NOT the same as the "ARL Bands" indicator.

They are "ARLs" set in an entirely different context, format, and amount and so does not constitute as a different version of "ARL Bands".

The "ARL Bands" indicator only has 4 lines and can be adjusted to any level. They are mainly focused on rebounds at desired levels.

The 13 "ARLs" here cannot be adjusted and are mainly focused on anticipating/calculating probabilities of peak and dip rebounds.

If any discrepancy should arise, let it be stated here that the "ARLs" in this indicator are considered to be a forked codebase to conserve the functionality of "ARL Bands".

This is proven by the differences described underneath "VERSION", which is located 7 lines above.

Key Points of Adjoining Median (KPAM)This indicator shows more reliable overbought & oversold levels buy combing 3 different level-indicators (i.e., indicators showing overbought/oversold levels).

A median is created by adjoining two of them and then it is assisted by a third one.

This reduces noise in calculating entries when using level indicators.

Note: The extra indicator shown is "Bands Bands (BanB)"

----- HOW TO USE IT -----

Use with price-action trading and with indicators showing the overall trend.

See notes in chart for more explanation.

The high and low levels of the RSI are within a range of 2 & -2 respectively.

The high and low levels for the median range from 4 & -4 respectively.

The Discordance shows how certain the level of the median is.

For example, if a part of the Discordance touches a low level while the median is at a higher level, then it usually indicates that the median is about to reverse.

The more Discordance that is visible, the less certain the current trend of the median is.

----- HOW THIS INDICATOR IS ORIGINAL; WHAT IT DOES AND HOW IT DOES IT -----

This indicator has an original, unique ability to reduce noise when comparing overbought and oversold levels.

It does this by first adjoining the Stochastic and the Stochastic RSI. Second, it creates a median from the two.

Third, the median is compared to the RSI on the same scale to assist in deciding where the median is at in relation to itself.

It shows whether the median lows and highs are near overbought or oversold levels.

----- VERSION -----

This is not a variant of the Stochastic, Stochastic RSI, and/or the RSI.

The focus is on the median that is created by an adjoining of the Stochastic and Stochastic RSI.

The Stochastic and Stochastic RSI are needed in order to obtain and plot the Median and the Discordance.

The RSI is plotted on the same scale to serve as the comparison needed to evaluate the Median levels with more visual accuracy.

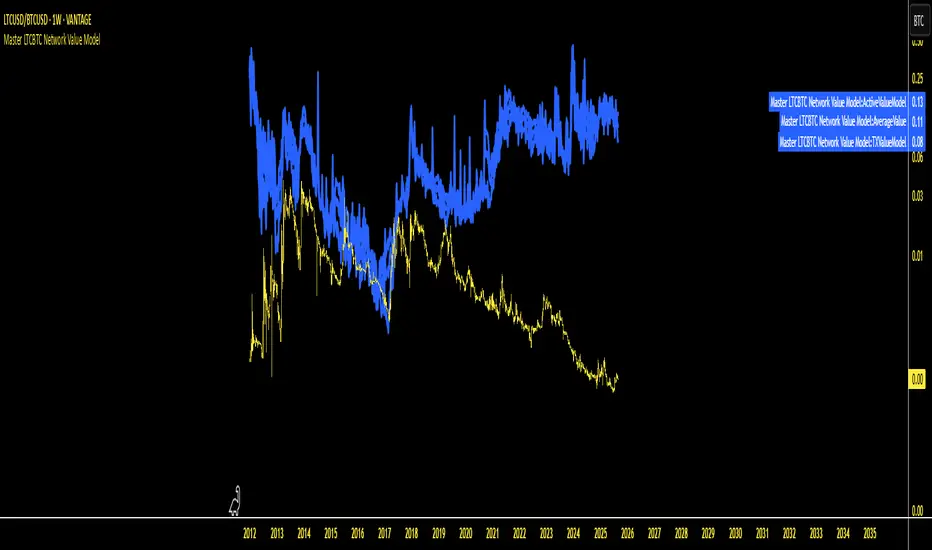

Master LTCBTC Network Value ModelThe Master LTCBTC Network Value Model takes the following 6 network values for Litecoin. It compares them to Bitcoin's network values to determine a "fair" value based on Litecoin's network usage compared to Bitcoin's.

Please apply on an LTCBTC chart. Use Black Background to view.

This also includes an average of the 6 network metrics and is colored white with a slightly large line width.

New Addresses

Total Addresses

Active Addresses

Total Volume USD

Transaction Count

# of Retail

Master Litecoin Network Value ModelThe Master Litecoin Network Value Model takes the following 6 network values for Litecoin. It compares them to Bitcoin's network values to determine a "fair" value based on Litecoin's network usage compared to Bitcoin's.

Please apply on an LTCUSD chart

This also includes an average of the 6 network metrics and is colored white with a slightly large line width.

New Addresses

Total Addresses

Active Addresses

Total Volume USD

Transaction Count

# of Retail

Average Daily Range Expansion Remaindeer for DaytradingThis indicator shows how much will the price need to go to fill its Average Daily Range based on the last 5 days (before today).

5-day ADR is used in concepts by ICT, Poltoratskiy and number of others.

Generally speaking, we would like to enter when there is a lot of room for price movement.

Outer lines are a full expansion. If the price moves only upside from the opening bell, it will reach as far.

Inner lines are a remaining expansion required to hit ADR. If the price initially moves in one direction and then reverses, this drip is substracted. This is more important metric!

Quantum Vector AlertsIts the part 2 of Multiple Indicators 50EMA Cross Alerts.

Its more suitable for the seconds chart. Beside, you can use it in higher timeframe.

The input bars length is the sample size that the code will use to trigger all alert. 20 mean 20 bar after the current candle.

When you activate volume alert you can select an amount of volume that when volume cross it you will be notified. The volume of every bar is displayed in the screener below volume.

In the section percentage vector counting the script do the sum of the red vector and green vector and give a ratio. In bullish vector count percentage for alert, you can select the percentage difference that you want to receive an alert. If your sample have 3 red vectors and 7 green vectors you will receive an alert saying that there is an imbalance of 70% showing more green vectors.

You can select a variant of percentage vector. The variant will do a summation of volume. If 1 vector candle is the size of the 3 other vector, they will have the same ponderation.

Normal alert counting count the number of vectors in the bars length. You can count the red and green candle only or add the blue and violet.

Bullish vector count will show a notification when the number of green candle will appear on the chart in the selected length. The same process is valid for bearish vector count. For example, if you want 3 bullish candle in 20 bar. You select bars length 20 and bullish vector count 3.

These alerts are suitable to the hybrid system. Thanks to our teacher Trader Reality and to all the member that contribute to this great discord community.

dmn's ICT ToolkitThis is my quality of life indicator for forex trading using the methods and concepts of ICT.

The idea is to automate marking up important price levels and times of the day instead of doing it manually every day.

Killzones

Marks the most volatile times of the day on the chart, during which the intraday high/low usually takes place.

Particularly impactful when there's news released during these times.

London Open (02:00-05:00 EST)

New York Open (08:30-11:00 EST)

London Close (10:00-11:30 EST)

True Day delineation

Vertical line at the start of the "true day" (00:00 EST), start of the algorithmic trading day and aids in visualizing the intraday direction.

New York midnight price level

Noteworthy price level at the start of the "true day".

This price level is referenced by the interbank trading algorithms during the day. Buy below it on bullish days, sell above it on bearish days.

Daily open price level

Reference level for optimal trade entries. Buy below it on bullish days, sell above it on bearish days.

Central Banks Dealers Range (CBDR) (14:00-20:00 EST) &

Central Banks Dealers Flout (CBDF) (15:00-24:00 EST) &

Asian Range (AR) (20:00-24:00 EST)

The standard deviation lines available are used to make predictions for short-term future highs/lows when the CBDR and AR are smaller than 40 pips.

Trade them by looking for 5/15min key levels that converge with the projection levels.

X days Average Daily Range (ADR)

Default to 5 days back, gives an idea of how much movement to expect intraday when the ADR high/low is converging with CBDR/CBDF/AR standard deviations.

Current Daily Range (CDR)

Used for comparison against the ADR to help determine if there's enough intraday range left to enter a trade.

Dynamically changes color based on percentage of the ADR. Green below 50% of ADR, orange between 50 and 100%, red when CDR exceeds ADR.

All of the above are used in conjunction with each other and higher timeframe levels of importance to find entries and target.

Note: Preferably use New York's time zone for your charts.

Divergence Strength OscillatorDetects divergence before it has formed a valid divergent pivot, across multiple indicators. After publishing my Strength of Divergence Across Multiple Indicators script, it seemed there were a lot of people who wanted to see the divergence signals before the divergent pivots were actually confirmed. Everyone complains about indicators repainting, yet in the next breath they complain about not wanting to wait for a signal to be confirmed before it appears on their chart! No matter how many times you ask, you can't have your cake and eat it too.

While this isn't exactly cake, it's as close as you're gonna get. This oscillator will calculate the strength of divergence as it forms on any bar that could potentially be a pivot point (e.g. for a pivot low, the preceding bars must be higher than it) and track the net (bullish - bearish) value.

For example:

PLEASE NOTE that this is not intended to be a "Buy" or "Sell" signal, and it would be foolish to use it as such. The purpose of this script is to show you potential divergences as early as possible, so that you have more time to plan and evaluate confluent signals, etc.

The Divergence Strength Calculation:

The total divergence strength value is the sum of the divergence strengths of all indicators for which divergence was detected at a given bar. Each indicator's individual divergence strength is comprised of two basic components: (1) |ΔPrice| - the magnitude of the change in price over the divergence period (pivot-to-pivot), and (2) |ΔIndicator| - the magnitude of the change in indicator value over the divergence period.

Because different indicators' scales and volatility can vary greatly, the Δ values are expressed in terms of standard deviation to ensure that the values are meaningful and equitable across all indicators and assets/instruments/currency pairs, etc:

|ΔIndicator| = |indicator_value_1 - indicator_value_2| / 2 * StDev(indicator_series,100)

Based on work for my Strength of Divergence Across Multiple Indicators script:

Movement Polarization (MoP)This shows the negative or positive charge of price movement and volume .

The "Polarization" shows how much negativity or positivity the movement of the price and volume have.

IMPORTANT:

Use with crypto currencies only is highly recommended.

If the volume in a currency is not visible, adjust the "Factor" number higher in the "Inputs" tab.

Adjust it until there is a balance between the vertical spread of the volume and polarization.

There will be a noticeable jump in the scale of the indicator if it is set too high.

The "Factor" is scaled at a baseline for SHIB prices. Any lower price scales than SHIB's will not show the volume .

Version:

This is a forked codebase to conserve the functionality of "RSI TV". The "RSI TV" focuses only on the RSI trend, this focuses on price and volume movement.

As such, there is no need for the MA of the RSI. Also, the TV Line from the "RSI TV" is used to show polarization of movement in this context.

The Trend Veracity line from the "RSI TV" has a broad scope in verifying different, particular trends, not just the RSI trend.

The RSI, volume, and polarization are all conveniently placed within the same scale to facilitate longer-term trading with price action. See also: "RSI TV" .

How this indicator is original; what it does, and how it does it:

This indicator has an original, unique ability to give the volume a further-projecting forecast.

The MoP does this by placing the volume on a vertical scale. It then compares it to a polarization level.

This gives 3 reference points: 1) Past data of volume, 2) volume vertical thresholds, and 3) polarization levels.

The volume by itself has no reference but its own past data. This gives a short-sighted forecast.

How to use it:

Useful with a trend finding indicator and price-action trading. See notes in picture above (scroll chart left to see first note).

Extra indicator shown in chart is an adjusted "ARL Bands" .

1) A condensing of volume and polarization usually means that an uptrend will soon turn.

2) A widening of volume and polarization usually means that a downtrend will soon turn.

3) A weak uptrend is indicated when volume falls while low, positive polarization also falls.

4) A growing uptrend is indicated when volume and positive polarization grow together.

5) Overlapping volume and positive polarization usually signifies oncoming peaks.

Tilson Bull-Bear-MarkerThe Tilson Bull-Bear marker is using 2 Tilson moving averages and their divergence to identify bull and bear trends and reversals (potential entry or exit points).

How to use it:

Fast T3 (thick line) above thin line / solid blue fill color = ongoing bull trend

Slow T3 (thin line) above thick line / solid red fill color = ongoing bear trend

Shrinking or expanding divergence between the lines = trend is getting hotter or cooling down

Fast T3 (thick line) changes color from blue to red = potential trend reversal from bullish to bearish

Fast T3 (thick line) changes color from red to blue = potential trend reversal from bearish to bullish

(No financial advise, for testing purposes only)

Big Whale Purchases and SalesBig Whale Purchases and Sales - plots big whale transactions on your chart!

People that hold more than 1% of a crypto currencies circulating supply are considered whales and have a huge influence on price, not just because they can move the market with their huge transactions, but also because other traders often track their wallets and follow their example. Taking a look at whale holdings, one can see why whale worship is so common in crypto: While Bitcoin has a relatively low whale concentration, many of the Top 100 Cryptocurrencies have whales control 60% or more of their circulating supply.

Integrating IntoTheBlock data, this script plots the transactions of these whales and, in strategy mode, copy trades them.

Features:

Strategy Mode: Switches the script between an indicator and a strategy.

Standard Deviations: The number of Standard Deviations that a transaction needs to surpass to be considered worth plotting. Setting this to 0 will show all whale transactions, higher settings will only show the biggest transactions.

Blockchain: The Chain on which Whale activity is tracked.

ATR Table 2.0ATR Table 2.0

This script was created in order to display a table that "calculates" how far the price can go on the current day .

The script is a table with 3 lines that calculates:

First Line - Day TR: The True Range of the current day ( - , including an Opening GAP if it exists);

Second Line - 10 Day ATR: The Average True Range of the asset (including Opening GAPs) for the last 10 days;

Third LIne - Range Consumed: How much of the 10 Day ATR it was consumed on the current day.

Example of how to use the information on the table and the understanding of it's purpose:

1) Supose you are day trading an asset that, during the last 10 days, have moved around $1.00 a day - This is the 10 Day ATR.

2) On this day, after 2 hours of the opening market, the price have already moved $0.50 (supose that it has moved $0.30 up and $0.35 down from the close of the prior day and the price is now near the close of the prior day).

3) In this situation, knowing that the price often moves around $1.00 a day, and knowing that it already moved $0.65 ($0.30 up and $0.35 down based on the close of the prior day), you may pay attention when the price breaksthrough the max or the min of the day, cause it can still move $0.35 in that direction ($1.00 - $0.65).

----------------------------------------------

ATR Table 2.0

Esse script foi criado para disponibilizar uma tabela que "calcula" quanto o preço pode andar ainda no dia em questão .

O script é uma tabela com 3 linhas que calcula:

Primeira Linha - TR do Dia: O Range Verdadeira do dia em questão ( - , incluindo GAP de Abertura se for o caso);

Segunda Linha - ATR de 10 Dias: A média do Range Verdadeira do ativo (incluindo GAPs de abertura) dos últimos 10 dias;

Terceira Linha - Range Consumido: O quanto do ATR de 10dias já foi consumido no dia em questão.

Exemplo de como usar essa informação na tabela e o entendimento do seu propósito:

1) Suponha que você está realizando day trade de um ativo que, durante os últimos 10 dias, se move em torno de $1.00 por dia. Esse é o ATR de 10 dias.

2) Nesse dia, após 2 horas da abertura do pregão, o preço já se moveu $.050 (suponhamos que ele tenha se moveu $0.30 para cima e $0.35 para baixo a partir do fechamento do dia anterior e agora o preço está próximo do fechamento do dia anterior).

3) Nessa situação, sabendo que o preço se move por volta de $1.00 por dia, e sabendo que ele já se moveu $0.65 ($0.30 pra cima e $0.35 pra baixo a partir do fechamento do dia anterior), você deve se atentar para quando o preço romper a máxima ou a mínima do dia, pois ele pode se mover ainda $.035 na direção do rompimento ($1.00 - $0.65).

Rolling HTF Liquidity Levels [CHE]█ OVERVIEW

This indicator displays a Rolling HTF Liquidity Levels . Contrary to HTF Liquidity Levels indicators which use a fix time segment, Rolling HTF Liquidity Levels calculates using a moving window defined by a time period (not a simple number of bars), so it shows better results.

This indicator is inspired by

The indicator introduces a new representation of the previous rolling time frame highs & lows (DWM HL) with a focus on untapped levels.

█ CONCEPTS

Untapped Levels

It is popularly known that the liquidity is located behind swing points or beyond higher time frames highs/lows.

Rolling HTF Liquidity Levels uses a moving window, it does not exhibit the static of the HTF Liquidity Levels plots.

█ HOW TO USE IT

Load the indicator on an active chart (see the Help Center if you don't know how).

Time period

By default, the script uses an auto-stepping mechanism to adjust the time period of its moving window to the chart's timeframe. The following table shows chart timeframes and the corresponding time period used by the script. When the chart's timeframe is less than or equal to the timeframe in the first column, the second column's time period is used to calculate the Rolling HTF Liquidity Levels:

Chart Time

timeframe period

1min 🠆 1H

5min 🠆 4H

1H 🠆 1D

4H 🠆 3D

12H 🠆 1W

1D 🠆 1M

1W 🠆 3M

By default, the time period currently used is displayed in the lower-right corner of the chart. The script's inputs allow you to hide the display or change its size and location.

This indicator should make trading easier and improve analysis. Nothing is worse than indicators that give confusingly different signals.

I hope you enjoy my new ideas

best regards

Chervolino

Q-TrendQ-Trend is an multipurpose indicatorm that can be used for swing- and trend-trading equally on any timeframe (non-volatile markets are better for this thing).

Settings:

Trend period - used to calculate trend line in the special moments(will explain below);

ATR Multiplier - changes sensitivity. The higher the multiplier = the more sensitive it is.

Also option to smooth source data (helps get cleaner signals, as always).

How to use?

Signals are given on the chart. Also ou can use trend line as S/R line.

The idea behind:

Terms:

SRС = Source

TL = trend line;

MP = ATR multiplier;

ATR = ATR :)

TL = (highest of source P-bars back + lowest of source P-bars back) / 2

Epsilon = MP * ATR

I was thinking for a week about combining volatility and relation between highest and lowest price point. That why I called indicator Q-Trend = Quantitative Trend , as I was trying to think about price in a mathematical way.

Okay, time to go philosophical:

1) TL is shows good price trend, but as it is slow enough and not enough informative, we need add additional conditions to produce signals.

2) Okay, so what can we add as conditions? We need to take volatility into account, as it is crucial in the moments of market uncertainty. So let's use ATR (Average True Range) somehow. My idea is that if SRC breaks TL + ATR , then it means that there will be upmove and we update our TL . Analogically for SRC breaking TL - ATR (breaks are crosses of TL +- ATR lines) .

Conclusion:

- if SRC breaks TL + ATR , it is a BUY signal and update of trend line;

- if SRC breaks TL - ATR , it is a SELL signal and update of trend line;

I think that such indicator already exisits on TradingView, as I've already saw something similar, but long ago, so please don't report, if such thing already exists.

But if not, then I hope, that you will gain some profits with Q-Trend :)

I will continue my work on this thing, so stay tuned.

Trade with your own risks and have your profits!

Wish you all the best!

- Tarasenko Fyodor

VOLQ Sigma TableThis indicator replaces the implied volatility of VOLQ with the daily volatility and reflects that value into the price on the NDX chart to create the VOLQ standard deviation table.

It will only be useful for stocks related to the Nasdaq Index.

For example, NDX, QQQ or so.

And we want to predict the range of weekly fluctuations by plotting those values as a line in the future.

It is expressed as High 2σ by adding the standard deviation 2 sigma value of the VOLQ value from last week's closing price.

It is expressed as High 1σ by adding the standard deviation 1 sigma value of the VOLQ value from last week's closing price.

It is expressed as Low 1σ by subtracting the standard deviation 1 sigma value of the VOLQ value from the closing price of the previous week.

It is expressed as Low 2σ by subtracting the standard deviation 2 sigma value of the VOLQ value from last week's closing price.

1day predicts daily fluctuations.

2day predicts 2-day fluctuations.

3day predicts 3-day fluctuations.

4day predicts 4-day fluctuations.

5day predicts 5-day fluctuations.

In the settings you can select the start date to display the VOLQ line via input.

-----------------------------

What motivated me to create this indicator?

From my point of view, the reason for classifying vix volq historical volatility (realized volatility) is that the most important point is that VIXX and VolQ are calculated from implied volatility. It can be standardized as one-month volatility. There are many strike prices, but exchanges use the implied volatility of options traded on their own exchanges.

Because historical volatility depends on how the period is set, to compare with VIXX, we compare it with a month, that is, 20 business days. One-month implied volatility means (actually different depending on the strike price), because option traders expect that the one-month volatility will be this much, and it is the volatility created by volatility trading.

So we see it as the volatility expected by derivatives traders, especially volatility traders.

I'm trying to infer what the market thinks will fluctuate this much from the numbers generated there.

ILM Seasonality Big Moves - TableUse this script on Daily Timeframe.

This script calculates Daily Moves ( Intraday / Close basis ) and buckets them into 1% / 2% / 3% moves

Also calculates MAX DD for the financial year from Peak to Trough

Helps in identifying volatility of the instrument and high drawdowns due to volatility

Pinbar by BirdCoinIt is the most customizable Pinbars indicator that you can find.

The indicator autonomously detects the Pinbars to which filters can be placed. The available adjustments are:

- The spread of the Pinbars

- The wick and the body ratio of the Pinbars

- The volume of the Pinbars

- Number of the previous candles that the Pinbars hunted

Happy trading!

~ Birdcoin

Spider Lines For Bitcoin (Daily And Weekly)I haven't seen any indicator do this, so I decided to publish this to form automatic Spider Charts without actually going through the effort of drawing them!

This script charts dotted lines (spider lines) all over, depicting support and resistance levels.

It works by connecting some candles from the 2018 bear market to the candle from 1st July 2019, followed by extending the lines to the right, making support and resistance levels for the future. The script works only for the daily and weekly charts for Bitcoin.

The levels are accurate to a good extent.

If the lines don't load, zoom out until the 2018 bear market top and it should load then.

Have fun with this indicator!