Seasonal Tendency (fadi)Seasonal tendency refers to the patterns in stock market performance that tend to repeat at certain times of the year. These patterns can be influenced by various factors such as economic cycles, investor behavior, and historical trends. For example, the stock market often performs better during certain months like November to April, a phenomenon known as the “best six months” strategy. Conversely, months like September are historically weaker.

These tendencies can help investors and traders make more informed decisions by anticipating potential market movements based on historical data. However, it’s important to remember that past performance doesn’t guarantee future results.

This indicator calculates the average daily move patterns over the specified number of years and then removes any outliers.

Settings

Number of years : The number of years to use in the calculation. The number needs to be large enough to create a pattern, but not so large that it may distort the price move.

Seasonality line color : The plotted line color.

Border : Show or hide the border and the color to use.

Grid : Show or hide the grid and the color to use.

Outlier Factor : The Outlier Factor is used to identify unusual price moves that are not typical and neutralize them to avoid skewing the predictions. It is the amount of deviation calculated using the total median price move.

Forecasting

Shifted Symbol Overlay with OffsetThe Shifted Symbol Overlay Indicator is a custom TradingView indicator designed to overlay the price data of one stock or asset over another, allowing for direct visual comparison. This is particularly useful for comparing the performance of two assets over different time periods. The indicator enables you to shift the data from one asset either forward or backward in time, making it easier to compare historical data from one stock with more recent data from another. The indicator supports shifting both to the right (future periods) and to the left (earlier periods), helping traders and analysts explore correlations or divergences between two financial instruments.

The indicator also includes a normalization option that adjusts the scale of the two assets, so you can compare them even if they have vastly different price levels. This is useful when you're interested in relative performance rather than the absolute price values.

Precision Cloud by Dr ABIRAM SIVPRASAD

Precision Cloud by Dr. Abhiram Sivprasad"

The " Precision Cloud" script, created by Dr. Abhiram Sivprasad, is a multi-purpose technical analysis tool designed for Forex, Bitcoin, Commodities, Stocks, and Options trading. It focuses on identifying key levels of support and resistance, combined with moving averages (EMAs) and central pivot ranges (CPR), to help traders make informed trading decisions. The script also provides a visual "light system" to highlight potential long or short positions, aiding traders in entering trades with a clear strategy.

Key Features of the Script:

Central Pivot Range (CPR):

The CPR is calculated as the average of the high, low, and close of the price, while the top and bottom pivots are derived from it. These act as dynamic support and resistance zones.

The script can plot daily CPR, support, and resistance levels (S1/R1, S2/R2, S3/R3) as well as optional weekly and monthly pivot points.

The CPR helps identify whether the price is in a bullish, bearish, or neutral zone.

Support and Resistance Levels:

Three daily support (S1, S2, S3) and resistance (R1, R2, R3) levels are plotted based on the CPR.

These levels act as potential reversal or breakout points, allowing traders to make decisions around key price points.

EMA (Exponential Moving Averages):

The script includes two customizable EMAs (default periods of 9 and 21). You can choose the source for these EMAs (open, high, low, or close).

The crossovers between EMA1 and EMA2 help identify potential trend reversals or momentum shifts.

Lagging Span:

The Lagging Span is plotted with a customizable displacement (default 26), which helps identify overall trend direction by comparing past price with the current price.

Light System:

A color-coded table provides a visual representation of market conditions:

Green indicates bullish signals (e.g., price above CPR, EMAs aligning positively).

Red indicates bearish signals (e.g., price below CPR, EMAs aligning negatively).

Yellow indicates neutral conditions, where there is no clear trend direction.

The system includes lights for CPR, EMA, Long Position, and Short Position, helping traders quickly assess whether the market is in a buying or selling opportunity.

Trading Strategies Using the Script

1. Forex Trading:

Trend-Following with EMAs: Use the EMA crossovers to capture trending markets in Forex. A green light for the EMA combined with a price above the daily or weekly pivot levels suggests a buying opportunity. Conversely, if the EMA light turns red and price falls below the CPR levels, look for shorting opportunities.

Reversal Strategy: Watch for price action near the daily S1/R1 levels. If price holds above S1 and the EMA is green, this could signal a reversal from support. The same applies to resistance levels.

2. Bitcoin Trading:

Momentum Breakouts: Bitcoin is known for its sharp moves. The script helps to identify breakouts from the CPR range. If the price breaks above the TC (Top Central Pivot) with bullish EMA alignment (green light), it could signal a strong uptrend.

Lagging Span Confirmation: Use the Lagging Span to confirm the trend direction. For Bitcoin's volatility, when the lagging span shows consistent alignment with the price and CPR, it often indicates continuation of the trend.

3. Commodities Trading:

Support/Resistance Bounce: Commodities such as gold and oil often react well to pivot levels. Look for price bouncing off S1 or R1 for potential entry points. A green CPR light along with price above the pivot range supports a bullish bias.

EMA Pullback Strategy: If price moves in a strong trend and pulls back to one of the EMAs, a green EMA light suggests re-entry on a pullback. If the EMA light is red and price breaks below the BC (Bottom Central Pivot), short positions could be considered.

4. Stocks Trading:

Long Position Strategy: For stocks, use the combination of the long position light turning green (price above TC and EMA alignment) as a signal to buy. This could be especially useful for riding bullish trends in growth stocks or during earnings seasons when volatility is high.

Short Position Strategy: If the short position light turns green, indicating price below BC and EMAs turning bearish, this could be an ideal setup for shorting overvalued stocks or during market corrections.

5. Options Trading:

Directional Bias for Options: The light system is particularly helpful for options traders. A green long position light provides a clear signal to buy call options, while a green short position light supports buying puts.

Pivot Breakout Strategy: Buy options (calls or puts) when the price breaks above resistance or below support, with confirmation from the CPR and EMA lights. This helps capture the sharp moves required for profitable options trades.

Conclusion

The S&R Precision Cloud script is a versatile tool for traders across markets, including Forex, Bitcoin, Commodities, Stocks, and Options. It combines critical technical elements like pivot ranges, support and resistance levels, EMAs, and the Lagging Span to provide a clear picture of market conditions. The intuitive light system helps traders quickly assess whether to take a long or short position, making it an excellent tool for both new and experienced traders.

The S&R Precision Cloud by Dr. Abhiram Sivprasad script is a technical analysis tool designed to assist traders in making informed decisions. However, it should not be interpreted as financial or investment advice. The signals generated by the script are based on historical price data and technical indicators, which are inherently subject to market fluctuations and do not guarantee future performance.

Trading in Forex, Bitcoin, Commodities, Stocks, and Options carries a high level of risk and may not be suitable for all investors. You should be aware of the risks involved and be willing to accept them before engaging in such activities. Always conduct your own research and consult with a licensed financial advisor or professional before making any trading decisions.

The creators of this script are not responsible for any financial losses that may occur from its use. Past performance is not indicative of future results, and the use of this script is at your own risk.

AHR999 Bitcoin Buy/Sell Signals Indicator - Accurate Trading OppThis Pine Script indicator combines the AHR999 metric with Bitcoin's historical price trends to provide clear buy and sell signals, assisting you in making informed trading decisions at crucial moments. It calculates the AHR999 index based on Bitcoin's 200-day Geometric Moving Average (GMA) and the estimated price, offering customizable buy and sell thresholds for precise entry and exit points. Ideal for traders looking to capture long-term investment trends, this indicator helps you effectively identify Bitcoin market opportunities.

Bitcoin Logarithmic Growth Curve 2024The Bitcoin logarithmic growth curve is a concept used to analyze Bitcoin's price movements over time. The idea is based on the observation that Bitcoin's price tends to grow exponentially, particularly during bull markets. It attempts to give a long-term perspective on the Bitcoin price movements.

The curve includes an upper and lower band. These bands often represent zones where Bitcoin's price is overextended (upper band) or undervalued (lower band) relative to its historical growth trajectory. When the price touches or exceeds the upper band, it may indicate a speculative bubble, while prices near the lower band may suggest a buying opportunity.

Unlike most Bitcoin growth curve indicators, this one includes a logarithmic growth curve optimized using the latest 2024 price data, making it, in our view, superior to previous models. Additionally, it features statistical confidence intervals derived from linear regression, compatible across all timeframes, and extrapolates the data far into the future. Finally, this model allows users the flexibility to manually adjust the function parameters to suit their preferences.

The Bitcoin logarithmic growth curve has the following function:

y = 10^(a * log10(x) - b)

In the context of this formula, the y value represents the Bitcoin price, while the x value corresponds to the time, specifically indicated by the weekly bar number on the chart.

How is it made (You can skip this section if you’re not a fan of math):

To optimize the fit of this function and determine the optimal values of a and b, the previous weekly cycle peak values were analyzed. The corresponding x and y values were recorded as follows:

113, 18.55

240, 1004.42

451, 19128.27

655, 65502.47

The same process was applied to the bear market low values:

103, 2.48

267, 211.03

471, 3192.87

676, 16255.15

Next, these values were converted to their linear form by applying the base-10 logarithm. This transformation allows the function to be expressed in a linear state: y = a * x − b. This step is essential for enabling linear regression on these values.

For the cycle peak (x,y) values:

2.053, 1.268

2.380, 3.002

2.654, 4.282

2.816, 4.816

And for the bear market low (x,y) values:

2.013, 0.394

2.427, 2.324

2.673, 3.504

2.830, 4.211

Next, linear regression was performed on both these datasets. (Numerous tools are available online for linear regression calculations, making manual computations unnecessary).

Linear regression is a method used to find a straight line that best represents the relationship between two variables. It looks at how changes in one variable affect another and tries to predict values based on that relationship.

The goal is to minimize the differences between the actual data points and the points predicted by the line. Essentially, it aims to optimize for the highest R-Square value.

Below are the results:

It is important to note that both the slope (a-value) and the y-intercept (b-value) have associated standard errors. These standard errors can be used to calculate confidence intervals by multiplying them by the t-values (two degrees of freedom) from the linear regression.

These t-values can be found in a t-distribution table. For the top cycle confidence intervals, we used t10% (0.133), t25% (0.323), and t33% (0.414). For the bottom cycle confidence intervals, the t-values used were t10% (0.133), t25% (0.323), t33% (0.414), t50% (0.765), and t67% (1.063).

The final bull cycle function is:

y = 10^(4.058 ± 0.133 * log10(x) – 6.44 ± 0.324)

The final bear cycle function is:

y = 10^(4.684 ± 0.025 * log10(x) – -9.034 ± 0.063)

The main Criticisms of growth curve models:

The Bitcoin logarithmic growth curve model faces several general criticisms that we’d like to highlight briefly. The most significant, in our view, is its heavy reliance on past price data, which may not accurately forecast future trends. For instance, previous growth curve models from 2020 on TradingView were overly optimistic in predicting the last cycle’s peak.

This is why we aimed to present our process for deriving the final functions in a transparent, step-by-step scientific manner, including statistical confidence intervals. It's important to note that the bull cycle function is less reliable than the bear cycle function, as the top band is significantly wider than the bottom band.

Even so, we still believe that the Bitcoin logarithmic growth curve presented in this script is overly optimistic since it goes parly against the concept of diminishing returns which we discussed in this post:

This is why we also propose alternative parameter settings that align more closely with the theory of diminishing returns.

Our recommendations:

Drawing on the concept of diminishing returns, we propose alternative settings for this model that we believe provide a more realistic forecast aligned with this theory. The adjusted parameters apply only to the top band: a-value: 3.637 ± 0.2343 and b-parameter: -5.369 ± 0.6264. However, please note that these values are highly subjective, and you should be aware of the model's limitations.

Conservative bull cycle model:

y = 10^(3.637 ± 0.2343 * log10(x) - 5.369 ± 0.6264)

Birdies [LuxAlgo]The Birdies indicator uses a unique technique to provide support/resistance curves based on a circle connecting the last swing high/low.

A specific, customizable part of this circle acts as a curve of interest, which can trigger visual breakout signals.

🔶 USAGE

The script projects a bird-like pattern when a valid Swing point is found. Multiple customization options are included.

🔹 Trend & Support/Resistance Tool

The color fill patterns and the wing boundaries can give insights into the current trend direction as well as serve as potential support/resistance areas.

In the example above, "Birdies" coincide with pullback and support/resistance zones.

🔹 Swing Length & Buffer

Besides the "Swing Length", with higher values returning longer-term Swing Levels, the script's behavior can be fine-tuned with filters ("Settings" - "Validation").

🔹 Validation

To minimize clutter, three filters are included:

Minimum X-Distance: The minimum amount of bars between subsequent Swings

Minimum Y-Distance: The minimum amount of bars between subsequent Swings

Buffer (Multiple of ATR)

The "Minimum X/Y-Distance" creates a zone where a new Swing is considered invalid. Only when the Swing is out of the zone, can it be considered valid.

In other words, in the example above, a Swing High can only be valid when enough bars/time have passed, and the difference between the last Swing and the previous is more than the ATR multiplied by the "Minimum Y-Distance" factor.

The "Buffer" creates a line above/below the "Birdy", derived from the measured ATR at the conception of the "Birdy" multiplied with a factor ("Buffer").

When the closing price crosses the "Birdy", it must also surpass this buffer line to produce a valid signal, lowering the risk of clutter as a result.

🔶 DETAILS

Birdies are derived from a circle that connects two Swing points. The left-wing curve originates from the most recent "Swing point" to the last value on the circle before crossing its midline. The mirror image of the left wing creates the right wing.

Enabling "Origine" will draw a line from the last Swing to the first.

🔹 Style

The publication includes a style setting with four options.

The first, "Birdy," shows a bird-like shape derived from a circle connecting the last Swing High and Swing Low.

The second option holds everything from the first option but connects both wingtips, providing potential horizontal levels of interest.

When setting "Birdy" to "None", the visual breakout signals will not defer from previous settings, but the focus is shifted towards the fill color, which can help detect potential trend shift.

A fourth setting, "Left Wing", will only show the left part of the "Birdy" pattern, removing the right part from the equation. This will change the visual breakout signals, providing alternative signals.

🔶 SETTINGS

Swing Length: The period used for swing detection, with higher values returning longer-term Swing Levels.

🔹 Validation

Minimum X-Distance: The minimum amount of bars between subsequent Swings

Minimum Y-Distance: The minimum amount of bars between subsequent Swings

Buffer (Multiple of ATR)

🔹 Style

Bullish Patterns: Enable / color

Bearish Patterns: Enable / color

Buffer Zone: Show / Color

Color Fill: Show color fill between two Birdies (if available)

Origine: Show the line between both Swing Points

🔹 Calculation

Calculated Bars: Allows the usage of fewer bars for performance/speed improvement

Standard Deviation based Upper Lower RangeThis script makes use of historical data for finding the standard deviation on daily returns. Based on the mean and standard deviation, the upper and lower range for the stock is shown upto 2x standard deviation. These bounds can be treated as volatility range for the next n trading sessions. This volatility is based on historical data. Users can change the lookback historical period, and can also set the time period (days) for upcoming trading sessions.

This indicator can be useful in determining stoploss and target levels along with the traditional support/resistance levels. It can also be useful in option trading where one needs to determine a range beyond which it is safe to sell an option.

A range of 1 SD has around 65% to 68% probability that it will not be breached. A range of 2 SD has around 95% probability that it will not be breached.

The indicator is based on Normal distribution theory. In future editions, I envision to also calculate the skewness and kurtosis so that we can determine if a stock is properly following Normal Distribution theory. That may further favor the calculated range.

Winning and Losing StreaksThe Pine Script indicator "Winning and Losing Streaks" tracks and visualizes the length of consecutive winning and losing streaks in a financial series, such as stock prices. Here’s a detailed description of the indicator, including the relevance of statistical analysis and streak tracking.

Indicator Description

The "Winning and Losing Streaks" indicator in Pine Script is designed to analyze and display streaks of consecutive winning and losing days in trading data. It helps traders and analysts understand the persistence of trends in price movements.

Here’s how it functions:

Streak Calculation:

Winning Streak: A series of consecutive days where the closing price is higher than the previous day's closing price.

Losing Streak: A series of consecutive days where the closing price is lower than the previous day's closing price.

Doji Candles: The indicator also considers Doji candles, where the difference between the opening and closing prices is minimal relative to the high-low range, and excludes these from being counted as winning or losing days.

Statistical Analysis:

The indicator computes the maximum and average lengths of winning and losing streaks.

It also tracks the current streak lengths and maintains arrays to store the historical streak data.

Visualization:

Histograms: Winning and losing streaks are visualized using histograms, which provide a clear graphical representation of streak lengths over time.

Relevance of Statistical Analysis and Streak Tracking

1. Statistical Significance of Streaks

Tracking winning and losing streaks has significant statistical implications for trading strategies and risk management:

Autocorrelation: Streaks in financial time series can reveal autocorrelation, where past returns influence future returns. Studies have shown that financial time series often exhibit autocorrelation, which can be used to forecast future price movements (Lo, 1991; Jegadeesh & Titman, 1993). Understanding streaks helps in identifying and leveraging these patterns.

Behavioral Finance: Streak analysis aligns with concepts from behavioral finance, such as the "hot-hand fallacy," where investors may perceive trends as more persistent than they are (Gilovich, Vallone, & Tversky, 1985). Statistical streak analysis provides a more objective view of trend persistence, helping to avoid biases.

2. Risk Management and Strategy Development

Risk Assessment: Identifying the length and frequency of losing streaks is crucial for managing risk and adjusting trading strategies. Long losing streaks can indicate potential strategy weaknesses or market regime changes, prompting a reassessment of trading rules and risk management practices (Brock, Lakonishok, & LeBaron, 1992).

Strategy Optimization: Statistical analysis of streaks can aid in optimizing trading strategies. For example, understanding the average length of winning and losing streaks can help in setting more effective stop-loss and take-profit levels, as well as in determining the optimal position sizing (Fama & French, 1993).

Scientific References:

Lo, A. W. (1991). "Long-Term Memory in Stock Market Prices." Econometrica, 59(5), 1279-1313. This paper discusses the presence of long-term memory in stock prices, which is relevant for understanding the persistence of streaks.

Jegadeesh, N., & Titman, S. (1993). "Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency." Journal of Finance, 48(1), 65-91. This study explores momentum and reversal strategies, which are related to the concept of streaks.

Gilovich, T., Vallone, R., & Tversky, A. (1985). "The Hot Hand in Basketball: On the Misperception of Random Sequences." Cognitive Psychology, 17(3), 295-314. This paper provides insight into the psychological aspects of streaks and persistence.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). "Simple Technical Trading Rules and the Stochastic Properties of Stock Returns." Journal of Finance, 47(5), 1731-1764. This research examines the effectiveness of technical trading rules, relevant for streak-based strategies.

Fama, E. F., & French, K. R. (1993). "Common Risk Factors in the Returns on Stocks and Bonds." Journal of Financial Economics, 33(1), 3-56. This paper provides a foundation for understanding risk factors and strategy performance.

By analyzing streaks, traders can gain valuable insights into market dynamics and refine their trading strategies based on empirical evidence.

PERFECT PIVOT RANGE DR ABIRAM SIVPRASAD (PPR)PERFECT PIVOT RANGE (PPR) by Dr. Abhiram Sivprasad

The Perfect Pivot Range (PPR) indicator is designed to provide traders with a comprehensive view of key support and resistance levels based on pivot points across different timeframes. This versatile tool allows users to visualize daily, weekly, and monthly pivots along with high and low levels from previous periods, helping traders identify potential areas of price reversals or breakouts.

Features:

Multi-Timeframe Pivots:

Daily, weekly, and monthly pivot levels (Pivot Point, Support 1 & 2, Resistance 1 & 2).

Helps traders understand price levels across various timeframes, from short-term (daily) to long-term (monthly).

Previous High-Low Levels:

Displays the previous week, month, and day high-low levels to highlight key zones of historical support and resistance.

Traders can easily see areas of price action from prior periods, giving context for future price movements.

Customizable Options:

Users can choose which pivot levels and high-lows to display, allowing for flexibility based on trading preferences.

Visual settings can be toggled on and off to suit different trading strategies and timeframes.

Real-Time Data:

All pivot points and levels are dynamically calculated based on real-time price data, ensuring accurate and up-to-date information for decision-making.

How to Use:

Pivot Points: Use daily, weekly, or monthly pivot points to find potential support or resistance levels. Prices above the pivot suggest bullish sentiment, while prices below indicate bearishness.

Previous High-Low: The high-low levels from previous days, weeks, or months can serve as critical zones where price may reverse or break through, indicating potential trade entries or exits.

Confluence: When pivot points or high-low levels overlap across multiple timeframes, they become even stronger levels of support or resistance.

This indicator is suitable for all types of traders (scalpers, swing traders, and long-term investors) looking to enhance their technical analysis and make more informed trading decisions.

Here are three detailed trading strategies for using the Perfect Pivot Range (PPR) indicator for options, stocks, and commodities:

1. Options Buying Strategy with PPR Indicator

Strategy: Buying Call and Put Options Based on Pivot Breakouts

Objective: To capitalize on sharp price movements when key pivot levels are breached, leading to high returns with limited risk in options trading.

Timeframe: 15-minute to 1-hour chart for intraday option trading.

Steps:

Identify the Key Levels:

Use weekly pivots for intraday trading, as they provide more significant levels for options.

Enable the "Previous Week High-Low" to gauge support and resistance from the previous week.

Call Option Setup (Bullish Breakout):

Condition: If the price breaks above the weekly pivot point (PP) with high momentum (indicated by a strong bullish candle), it signifies potential bullishness.

Action: Buy Call Options at the breakout of the weekly pivot.

Confirmation: Check if the price is sustaining above the pivot with a minimum of 1-2 candles (depending on timeframe) and the first resistance (R1) isn’t too far away.

Target: The first resistance (R1) or previous week’s high can be your target for exiting the trade.

Stop-Loss: Set a stop-loss just below the pivot point (PP) to limit risk.

Put Option Setup (Bearish Breakdown):

Condition: If the price breaks below the weekly pivot (PP) with strong bearish momentum, it’s a signal to expect a downward move.

Action: Buy Put Options on a breakdown below the weekly pivot.

Confirmation: Ensure that the price is closing below the pivot, and check for declining volumes or bearish candles.

Target: The first support (S1) or the previous week’s low.

Stop-Loss: Place the stop-loss just above the pivot point (PP).

Example:

Let’s say the weekly pivot point (PP) is at 1500, the price breaks above and sustains at 1510. You buy a Call Option with a strike price near 1500, and the target will be the first resistance (R1) at 1530.

2. Stock Trading Strategy with PPR Indicator

Strategy: Swing Trading Using Pivot Points and Previous High-Low Levels

Objective: To capture mid-term stock price movements using pivot points and historical high-low levels for better trade entries and exits.

Timeframe: 1-day or 4-hour chart for swing trading.

Steps:

Identify the Trend:

Start by determining the overall trend of the stock using the weekly pivots. If the price is consistently above the pivot point (PP), the trend is bullish; if below, the trend is bearish.

Buy Setup (Bullish Trend Reversal):

Condition: When the stock bounces off the weekly pivot point (PP) or previous week’s low, it signals a bullish reversal.

Action: Enter a long position near the pivot or previous week’s low.

Confirmation: Look for a bullish candle pattern or increasing volumes.

Target: Set your first target at the first resistance (R1) or the previous week’s high.

Stop-Loss: Place your stop-loss just below the previous week’s low or support (S1).

Sell Setup (Bearish Trend Reversal):

Condition: When the price hits the weekly resistance (R1) or previous week’s high and starts to reverse downwards, it’s an opportunity to short-sell the stock.

Action: Enter a short position near the resistance.

Confirmation: Watch for bearish candle patterns or decreasing volume at the resistance.

Target: Your first target would be the weekly pivot point (PP), with the second target as the previous week’s low.

Stop-Loss: Set a stop-loss just above the resistance (R1).

Use Previous High-Low Levels:

The previous week’s high and low are key levels where price reversals often occur, so use them as reference points for potential entry and exit.

Example:

Stock XYZ is trading at 200. The previous week’s low is 195, and it bounces off that level. You enter a long position with a target of 210 (previous week’s high) and place a stop-loss at 193.

3. Commodity Trading Strategy with PPR Indicator

Strategy: Trend Continuation and Reversal in Commodities

Objective: To capitalize on the strong trends in commodities by using pivot points as key support and resistance levels for trend continuation and reversal.

Timeframe: 1-hour to 4-hour charts for commodities like Gold, Crude Oil, Silver, etc.

Steps:

Identify the Trend:

Use monthly pivots for long-term commodities trading since commodities often follow macroeconomic trends.

The monthly pivot point (PP) will give an idea of the long-term trend direction.

Trend Continuation Setup (Bullish Commodity):

Condition: If the price is consistently trading above the monthly pivot and pulling back towards the pivot without breaking below it, it indicates a bullish continuation.

Action: Enter a long position when the price tests the monthly pivot (PP) and starts moving up again.

Confirmation: Look for a strong bullish candle or an increase in volume to confirm the continuation.

Target: The first resistance (R1) or previous month’s high.

Stop-Loss: Place the stop-loss below the monthly pivot (PP).

Trend Reversal Setup (Bearish Commodity):

Condition: When the price reverses from the monthly resistance (R1) or previous month’s high, it’s a signal for a bearish reversal.

Action: Enter a short position at the resistance level.

Confirmation: Watch for bearish candle patterns or decreasing volumes at the resistance.

Target: Set your first target as the monthly pivot (PP) or the first support (S1).

Stop-Loss: Stop-loss should be placed just above the resistance level.

Using Previous High-Low for Swing Trades:

The previous month’s high and low are important in commodities. They often act as barriers to price movement, so traders should look for breakouts or reversals near these levels.

Example:

Gold is trading at $1800, with a monthly pivot at $1780 and the previous month’s high at $1830. If the price pulls back to $1780 and starts moving up again, you enter a long trade with a target of $1830, placing your stop-loss below $1770.

Key Points Across All Strategies:

Multiple Timeframes: Always use a combination of timeframes for confirmation. For example, a daily chart may show a bullish setup, but the weekly pivot levels can provide a larger trend context.

Volume: Volume is key in confirming the strength of price movement. Always confirm breakouts or reversals with rising or declining volume.

Risk Management: Set tight stop-loss levels just below support or above resistance to minimize risk and lock in profits at pivot points.

Each of these strategies leverages the powerful pivot and high-low levels provided by the PPR indicator to give traders clear entry, exit, and risk management points across different markets

Auto Signal Buy/SellAuto Signal Buy/Sell with Time Filter and Dynamic ZLEMA (GMT+2) 🌟

Are you looking for an indicator that combines efficiency and simplicity while integrating advanced elements like SuperTrend, ZLEMA (Zero Lag EMA), and a MACD DEMA for clear and precise buy/sell signals? 📈 Introducing Auto Signal Buy/Sell, the ultimate indicator designed for intraday and swing traders, optimized for market hours in GMT+2.

🛠️ Key Features:

- **Advanced SuperTrend**: Follow the dominant trend with a robust SuperTrend, adjustable to your preferences (customizable multiplier and period).

- **Dynamic ZLEMA**: Get a zero-lag EMA curve with a visual signal. Additionally, the ZLEMA turns blue when it’s nearly flat, helping you easily spot market consolidation phases.

- **MACD DEMA**: An enhanced version of the traditional MACD, using the Double EMA to capture more responsive buy/sell cross signals. 📊

- **Buy/Sell Signals**: Visual arrows clearly indicate potential entry and exit points on your chart, filtered by MACD crossovers and the SuperTrend trend.

- **Smart Time Filter (GMT+2)**: This script adapts to trading hours (customizable) and only displays signals during trading hours. The background turns light blue when the market is closed, preventing confusion during inactivity periods. 🕒

⚙️ Full Customization:

- Adjustable trading hours (default 9 AM to 5 PM in GMT+2) with dynamic background indicating when markets are closed.

- Flexible settings for SuperTrend, ZLEMA, and MACD DEMA to suit any strategy.

🎯 Why Choose This Indicator?

- Optimized for maximum precision with advanced algorithms like ZLEMA and DEMA.

- Easy to use: it provides clear, visual signals directly on the chart—no need to decipher complex indicators.

- A complete intraday and swing indicator that combines trend analysis and signal filtering with precise market hours.

🚀 Boost Your Trading!

Add this indicator to your toolkit and enhance your decision-making. Thanks to its intuitive interface and clear visual signals, you can trade with confidence. 💡

Don't forget to like 👍 and comment if you find this indicator useful! Your feedback helps us continue improving such tools. 🚀

📌 How to Use:

1. Add the indicator to your chart.

2. Adjust the SuperTrend and ZLEMA settings to suit your needs.

3. Follow the buy/sell signals and watch for the light blue background outside of trading hours.

4. Trade effectively and stay in control, even during consolidation phases.

Reflected ema Difference (RED) This script, titled "Reflected EMA Difference (RED)," is based on the logic of evaluating the percentage of convergence and divergence between two moving averages, specifically the Hull Moving Averages (HMA), to make price-related decisions. The Hull Moving Average, created by Alan Hull, is used as the foundation of this strategy, offering a faster and more accurate way to analyze market trends. In this script, the concept is employed to measure and reflect price variations.

Script Functionality Overview:

Hull Moving Averages (HMA): The script utilizes two HMAs, one short-term and one long-term. The main idea is to compute the Delta Difference between these two moving averages, which represents how much they are converging or diverging from each other. This difference is key to identifying potential market trend changes.

Reflected HMA Value: Using the Delta Difference between the HMAs, the value of the short-term HMA is reflected, creating a visual reference point that helps traders see the relationship between price and HMAs on the chart.

Percentage Change Index: The second key parameter is the percentage change index. This determines when a trend is reversing, allowing buy or sell orders to be established based on significant changes in the relationship between the HMAs and the price.

Delta Multiplier: The script comes with a default Delta multiplier of 2 for calculating the difference between HMAs, allowing traders to adjust the sensitivity of the analysis based on the time frame being analyzed.

Trend Reversal Signals: When the price crosses the thresholds defined by the percentage change index, buy or sell signals are triggered, based on the detection of a potential trend reversal.

Visual Cues with Boxes: Boxes are drawn on the chart when the HullMA crosses the reflected HMA value, providing a visual aid to identify critical moments where risk should be evaluated.

Alerts for Receiving Signals:

This script allows you to set up buy and sell alerts via TradingView's alert system. These alerts are triggered when trend changes are detected based on the conditions coded in the script. Traders can receive instant notifications, allowing them to make decisions without needing to constantly monitor the chart.

Additional Considerations:

The percentage change parameter is adjustable and should be configured based on the time frame you are trading on. For longer time frames, it's advisable to use a larger percentage change to avoid false signals.

The use of Hull Moving Averages (HMA) provides a faster and more reactive approach to trend evaluation compared to other moving averages, making it a powerful tool for traders seeking quick reversal signals.

This approach combines the power of Hull Moving Averages with an alert system to improve the trader’s response to trend changes.

Spanish

Este script, titulado "Reflected EMA Difference (RED)", está fundamentado en la lógica de evaluar el porcentaje de acercamiento y distancia entre dos medias móviles, específicamente las medias móviles de Hull (HMA), para tomar decisiones sobre el valor del precio. El creador de la media móvil de Hull, Alan Hull, diseñó este indicador para ofrecer una forma más rápida y precisa de analizar tendencias de mercado, y en este script se utiliza su concepto como base para medir y reflejar las variaciones de precio.

Descripción del funcionamiento:

Medias Móviles de Hull (HMA): Se utilizan dos HMAs, una de corto plazo y otra de largo plazo. La idea principal es calcular la diferencia Delta entre estas dos medias móviles, que representa cuánto se están alejando o acercando entre sí. Esta diferencia es clave para identificar cambios potenciales en la tendencia del mercado.

Valor Reflejado de la HMA: Con la diferencia Delta calculada entre las HMAs, se refleja el valor de la HMA corta, creando un punto de referencia visual que ayuda a los traders a observar la relación entre el precio y las HMAs en el gráfico.

Índice de Cambio de Porcentaje: El segundo parámetro clave del script es el índice de cambio porcentual. Este define el momento en que una tendencia está revirtiendo, permitiendo establecer órdenes de compra o venta en función de un cambio significativo en la relación entre las HMAs y el precio.

Multiplicador Delta: El script tiene un multiplicador predeterminado de 2 para el cálculo de la diferencia Delta, lo que permite ajustar la sensibilidad del análisis según la temporalidad del gráfico.

Señales de Reversión de Tendencia: Cuando el precio cruza los límites definidos por el índice de cambio porcentual, se emiten señales para comprar o vender, basadas en la detección de una posible reversión de tendencia.

Visualización con Cajas: Se dibujan cajas en el gráfico cuando el indicador HullMA cruza el valor reflejado de la HMA, ayudando a identificar visualmente los momentos críticos en los que se debe evaluar el riesgo de las operaciones.

Alertas para Recibir Señales:

Este script permite configurar alertas de compra y venta desde el apartado de alertas de TradingView. Estas alertas se activan cuando se detectan cambios de tendencia en función de las condiciones establecidas en el código. El trader puede recibir notificaciones instantáneas, lo que facilita la toma de decisiones sin necesidad de estar constantemente observando el gráfico.

Consideraciones adicionales:

El porcentaje de cambio es un parámetro ajustable y debe configurarse según la temporalidad que se esté operando. En temporalidades más largas, es recomendable usar un porcentaje de cambio mayor para evitar señales falsas.

La utilización de las medias móviles de Hull (HMA) proporciona un enfoque más rápido y reactivo para evaluar tendencias en comparación con otras medias móviles, lo que lo convierte en una herramienta poderosa para traders que buscan señales rápidas de reversión.

Este enfoque combina la potencia de las medias móviles de Hull con un sistema de alertas que mejora la reactividad a cambios de tendencia.

VSA Impulse with JOC and SC Forecast BoxesEnglish Description

**Script Title:** VSA Impulse with JOC and SC Forecast Boxes

**Description:**

This Pine Script™ indicator integrates Volume Spread Analysis (VSA) with impulse signals and forecast boxes to help traders visualize key market conditions and potential price movements.

**Features:**

1. **Impulse Movements**: Identifies bullish and bearish impulse movements based on price and volume changes.

- **Impulse Up**: Price is higher and volume is greater than the previous bar.

- **Impulse Down**: Price is lower and volume is greater than the previous bar.

2. **VSA Signals**: Detects specific VSA signals for analysis:

- **Stopping Action (SA)**: Bullish impulse with higher volume and price increase.

- **Spring (SP)**: Bullish impulse with lower volume and price drop.

- **No Demand (ND)**: Bearish impulse with lower volume and price increase.

- **Last Point of Support (LPS)**: Bullish impulse with higher volume and price drop.

- **Jump Over Creek (JOC)**: Bullish impulse with higher volume and price increase.

- **Selling Climax (SC)**: Bearish impulse with higher volume and price drop.

3. **Forecast Boxes**:

- **Jump Over Creek (JOC) Forecast Box**: Displays a green forecast box when a JOC signal is detected, projecting potential bullish movement.

- **Selling Climax (SC) Forecast Box**: Displays a red forecast box when an SC signal is detected, projecting potential bearish movement.

4. **Anomalous Volume Detection**: Highlights significant volume spikes above a set multiplier of the average volume with colored boxes and labels.

**Settings:**

- **Length**: Defines the period for calculating the average volume.

- **Anomalous Volume Multiplier**: Sets the threshold for identifying anomalous volumes.

- **Forecast Period**: Determines the duration for the forecast boxes.

**Visuals:**

- Colored forecast boxes for JOC (green) and SC (red) with corresponding labels.

- Signals for VSA with colored shapes and labels.

- Highlighted anomalous volumes with colored boxes and labels.

Русское описание

**Название скрипта:** Импульс VSA с прогнозными боксами JOC и SC

**Описание:**

Этот Pine Script™ индикатор интегрирует анализ объема и спреда (VSA) с импульсными сигналами и прогнозными боксами, чтобы помочь трейдерам визуализировать ключевые рыночные условия и потенциальные движения цен.

**Функции:**

1. **Импульсные движения**: Определяет бычьи и медвежьи импульсные движения на основе изменений цены и объема.

- **Импульс вверх**: Цена выше и объем больше предыдущего бара.

- **Импульс вниз**: Цена ниже и объем больше предыдущего бара.

2. **Сигналы VSA**: Обнаруживает специфические сигналы VSA для анализа:

- **Stopping Action (SA)**: Бычий импульс с увеличением объема и цены.

- **Spring (SP)**: Бычий импульс с уменьшением объема и падением цены.

- **No Demand (ND)**: Медвежий импульс с уменьшением объема и ростом цены.

- **Last Point of Support (LPS)**: Бычий импульс с увеличением объема и падением цены.

- **Jump Over Creek (JOC)**: Бычий импульс с увеличением объема и ростом цены.

- **Selling Climax (SC)**: Медвежий импульс с увеличением объема и падением цены.

3. **Прогнозные боксы**:

- **Прогнозный бокс Jump Over Creek (JOC)**: Показывает зеленый прогнозный бокс при обнаружении сигнала JOC, проецируя потенциальное бычье движение.

- **Прогнозный бокс Selling Climax (SC)**: Показывает красный прогнозный бокс при обнаружении сигнала SC, проецируя потенциальное медвежье движение.

4. **Обнаружение аномального объема**: Подчеркивает значительные всплески объема выше заданного множителя среднего объема с помощью цветных боксов и меток.

**Настройки:**

- **Length**: Определяет период для расчета среднего объема.

- **Множитель аномального объема**: Устанавливает порог для идентификации аномального объема.

- **Период прогноза**: Определяет продолжительность прогнозных боксов.

**Визуализация:**

- Цветные прогнозные боксы для JOC (зеленые) и SC (красные) с соответствующими метками.

- Сигналы VSA с цветными фигурами и метками.

- Подсвеченные аномальные объемы с цветными боксами и метками.

[DarkTrader] Range Level ProbabilityThis indicator calculates and visualizes significant price levels, such as swing highs, swing lows, and mid-price levels, using advanced mathematical functions and statistical methods. It aims to provide traders with insights into potential support and resistance areas by analyzing past price swings and their statistical properties.

Usage :

Identifying Support and Resistance: The projected swing high and swing low levels can act as potential support and resistance zones. Traders can use these levels to anticipate where the price might reverse or experience a pause in its movement.

Trend Analysis: By analyzing the mid-price level and its relationship to the swing high and low, traders can gain insights into the current market trend and potential price direction.

Customizing for Different Periods: Traders can adjust the input parameters, such as the period for calculating the mean and standard deviation, to tailor the indicator to different timeframes and market conditions.

Enhancing Trading Decisions: The indicator provides additional context for trading decisions by combining statistical analysis with visual projections, helping traders make more informed choices and manage risk effectively.

Key Features :

Statistical Analysis: The indicator utilizes statistical techniques to estimate the probability of future price movements. It calculates the likelihood of price reaching certain levels based on historical data, providing a probabilistic view of potential price targets.

Dynamic Range Calculation: It dynamically calculates important price levels based on a defined period. This period is adjustable, allowing traders to customize the indicator to fit different market conditions and trading strategies.

Customizable Appearance: Traders can customize the colors of the projected lines and labels, making it easier to distinguish between different levels and adjust the visual representation to their preferences.

Real-Time Updates: The indicator updates in real time with each new price bar, ensuring that the projected levels reflect the most current market conditions.

The indicator projects key price levels on the chart, including :

Swing High: The highest price level within a specified period.

Swing Low: The lowest price level within the same period.

Mid-Price: The average price between the swing high and swing low.

These levels are drawn as horizontal lines on the chart, extending into the future, which helps traders anticipate potential support and resistance zones.

Super Trend ReversalsMain Concept

The core idea behind the Super Trend Reversals indicator is to assess the momentum of automated trading bots (often referred to as 'Supertrend bots') that enter the market during critical turning points. Specifically, the indicator is tuned to identify when the market is nearing bottoms or peaks, but just before it shifts direction based on the triggered Supertrend signals. This approach helps traders engage with the market right as the reversal momentum builds up, allowing for entry just as conditions become favorable and exit before momentum wanes.

How It Works

The Super Trend Reversals uses multiple Supertrend calculations, each with different period and multiplier settings, to form a comprehensive view of the trend. The total trend score from these calculations is then analyzed using the Relative Strength Index (RSI) and Exponential Moving Averages (EMA) to gauge the strength and sustainability of the trend.

A key feature of this indicator is the isCurrentRangeSmaller() function, which evaluates if the current price range is lower than the average over the recent period. This function is critical as it helps determine the stability of the market environment, reducing the likelihood of entering or exiting trades based on erratic price movements that could lead to false signals.

[DarkTrader] Dynamic Level ProjectionThis indicator designed to enhance market analysis by projecting key price levels based on recent highs and lows. This script stands out by offering unique dynamic projections that are tailored to the latest market conditions, making it a valuable tool for both short-term and long-term traders.

Level Projection uses proprietary methods to dynamically project levels above and below recent price extremes. It employs two distinct scaling methods—Short Multiply (SM) and Long Multiply (LM)—to calculate these levels. The SM method is used to project resistance levels above recent highs, while the LM method projects support levels below recent lows. This approach ensures that the projected levels are responsive to current market trends and volatility.

How It Works :

The indicator analyzes recent market data to determine the highest and lowest prices over a customizable lookback period. Using the OHLC Lookback parameter, traders can set the duration for which these extreme prices are calculated. Based on these extremes, the indicator projects additional levels using the defined scaling methods. The result is a series of levels that help identify potential support and resistance zones in real time.

Customization Options :

Level Parameter: Defines the lengths for different projected levels.

OHLC Resolution: Selects the timeframe for OHLC data used in calculations.

Box Padding / Height: Controls the visual spacing of the projected levels on the chart.

Start Color and Extend Color: Customize the colors of the projected levels for better visual differentiation.

Real-Time Updates :

The indicator is designed to update in real-time, recalculating and redrawing levels with each new bar. This ensures that traders always see the most current projections and can make timely decisions based on the latest market data.

How to Use :

Traders should apply the indicator to their charts and customize the parameters according to their trading strategy. The projected levels will help in identifying potential support and resistance zones, which can be used to make informed trading decisions and manage risk effectively.

US Market Support & ResistanceUS Market Support & Resistance Indicator (For 5-30 Minute Timeframes)

This indicator plots key support and resistance levels for the US market based on the high and low of the first candle at the market open. It also shades the area between these levels with a color that dynamically changes to indicate the current trend:

* Green: Price is above the resistance level, suggesting a potential uptrend.

* Red: Price is below the support level, suggesting a potential downtrend.

* Gray: Price is trading between the support and resistance levels, suggesting a sideways trend.

Additionally, the indicator displays a small dashboard in the top right corner of the chart showing the current trend ("Upward", "Downward", or "Sideways") in the corresponding color.

Key Features:

* US Market Time Identification: Accurately identifies US market open and close times in UTC and colors candles red during these times.

* Support & Resistance Plotting: Plots support and resistance lines at the high and low of the first candle at the market open and extends them infinitely on the chart.

* Shaded Area Between Levels: Shades the area between the support and resistance lines with a color that dynamically changes based on the current price location relative to these levels.

* Trend Display: Displays a dashboard showing the current trend based on the shaded area's color.

* Open Alert: Issues an alert when the US market opens.

* Supported Timeframes: Works on timeframes less than 30 minutes and greater than 5 minutes.

* Economic News: Not recommended for use during periods of sporadic economic news releases, as sudden price fluctuations may cause false signals.

How to Use:

* Add the indicator to your chart, ensuring the timeframe is between 5 and 30 minutes.

* Wait for the US market to open.

* Observe the shaded area's color and the dashboard to identify the current trend.

* Use the support and resistance levels to make trading decisions, keeping in mind not to rely solely on it during news releases.

Caution: This indicator relies on support and resistance levels drawn at the US market open and may not always be accurate, especially during periods of high volatility. It should be used in conjunction with other technical analysis tools to confirm the trend and make informed trading decisions.

Note: This description is designed to be compliant with TradingView's policies on indicator publishing.

Forex Macro Metrics [MacroGlide]"Forex Macro Metrics " is a powerful tool for analyzing macroeconomic metrics, designed to help traders make more informed decisions in the forex market. This indicator displays key economic indicators such as interest rates, money supply (M1 and M2), unemployment rate, and government debt for various currencies and their pairs, allowing users to assess the macroeconomic differences between the base and quote currencies.

Key Features:

• Interest Rates Display: Includes interest rates for major world currencies with the ability to show the differential between the base and quote currencies.

• Money Supply Analysis (M1 and M2): Displays the money supply for both the base and quote currencies, including differential calculations.

• Unemployment Rate: Compares the unemployment rates between currencies, showing the differences on the chart.

• Government Debt: Shows government debt levels for the base and quote currencies with differential calculations.

• Customizable Options: Enable/disable specific metrics and adjust colors for better visual clarity.

How to Use:

• Select a Currency Pair: Apply the indicator to your chart and choose the desired currency pair. The indicator will automatically load the relevant data for the base and quote currencies.

• Adjust Display Settings: Use the indicator settings to enable or disable specific metrics and their differentials.

• Analyze the Data: Compare the economic conditions of the two currencies through the charts and identify potential trading opportunities based on macroeconomic differences.

Methodology:

The indicator uses economic data available through TradingView tickers to calculate the values of the base and quote currencies. Differentials are calculated by subtracting the values of the quote currency from the base currency, allowing for a visual assessment of their differences. The displayed data includes historical changes, helping to identify trends and potential reversal points.

Originality and Usefulness:

"Forex Macro Metrics " is a unique tool that combines several key macroeconomic indicators into one comprehensive indicator. This simplifies the analysis process for traders looking to understand the fundamental differences between currencies. Using this approach provides an advantage in assessing long-term trends and potential shifts in currency pairs driven by changes in macroeconomic conditions.

Charts:

The indicator displays data in the form of lines and areas on the chart, with interest rates shown as lines for the base and quote currencies, accompanied by an area representing the differential. For money supply (M1 and M2), lines are drawn for each currency, with areas highlighting the differences. Similarly, the unemployment rate and government debt are displayed with clear visual separation of the data and their differentials, making it easy to compare and analyze the macroeconomic conditions of the currencies involved.

Enjoy the game!

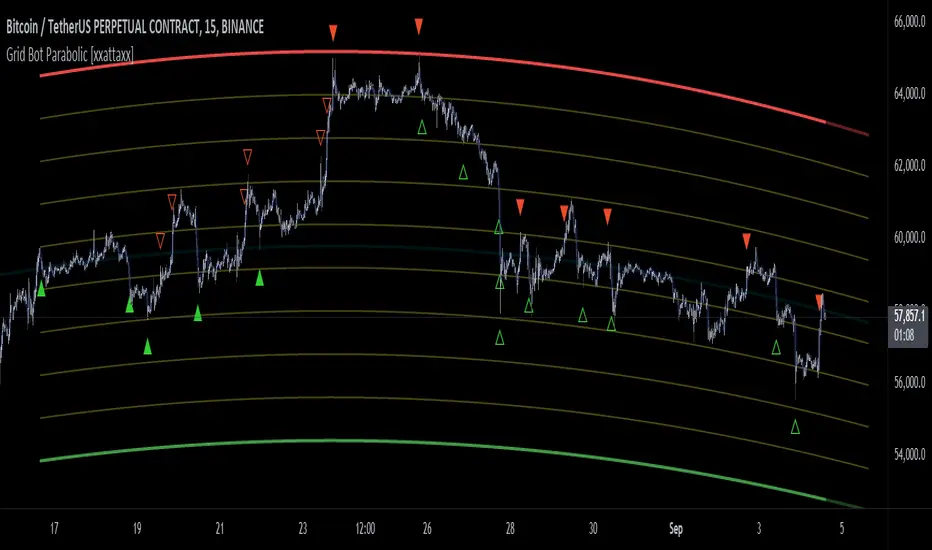

Grid Bot Parabolic [xxattaxx]🟩 The Grid Bot Parabolic, a continuation of the Grid Bot Simulator Series , enhances traditional gridbot theory by employing a dynamic parabolic curve to visualize potential support and resistance levels. This adaptability is particularly useful in volatile or trending markets, enabling traders to explore grid-based strategies and gain deeper market insights. The grids are divided into customizable trade zones that trigger signals as prices move into new zones, empowering traders to gain deeper insights into market dynamics and potential turning points.

While traditional grid bots excel in ranging markets, the Grid Bot Parabolic’s introduction of acceleration and curvature adds new dimensions, enabling its use in trending markets as well. It can function as a traditional grid bot with horizontal lines, a tilted grid bot with linear slopes, or a fully parabolic grid with curves. This dynamic nature allows the indicator to adapt to various market conditions, providing traders with a versatile tool for visualizing dynamic support and resistance levels.

🔑 KEY FEATURES 🔑

Adaptable Grid Structures (Horizontal, Linear, Curved)

Buy and Sell Signals with Multiple Trigger/Confirmation Conditions

Secondary Buy and Secondary Sell Signals

Projected Grid Lines

Customizable Grid Spacing and Zones

Acceleration and Curvature Control

Sensitivity Adjustments

📐 GRID STRUCTURES 📐

Beyond its core parabolic functionality, the Parabolic Grid Bot offers a range of grid configurations to suit different market conditions and trading preferences. By adjusting the "Acceleration" and "Curvature" parameters, you can transform the grid's structure:

Parabolic Grids

Setting both acceleration and curvature to non-zero values results in a parabolic grid.This configuration can be particularly useful for visualizing potential turning points and trend reversals. Example: Accel = 10, Curve = -10)

Linear Grids

With a non-zero acceleration and zero curvature, the grid tilts to represent a linear trend, aiding in identifying potential support and resistance levels during trending phases. Example: Accel =1.75, Curve = 0

Horizontal Grids

When both acceleration and curvature are set to zero, the indicator reverts to a traditional grid bot with horizontal lines, suitable for ranging markets. Example: Accel=0, Curve=0

⚙️ INITIAL SETUP ⚙️

1.Adding the Indicator to Your Chart

Locate a Starting Point: To begin, visually identify a price point on your chart where you want the grid to start.This point will anchor your grid.

2. Setting Up the Grid

Add the Grid Bot Parabolic Indicator to your chart. A “Start Time/Price” dialog will appear

CLICK on the chart at your chosen start point. This will anchor the start point and open a "Confirm Inputs" dialog box.

3. Configure Settings. In the dialog box, you can set the following:

Acceleration: Adjust how quickly the grid reacts to price changes.

Curve: Define the shape of the parabola.

Intervals: Determine the distance between grid levels.

If you choose to keep the default settings, with acceleration set to 0 and curve set to 0, the grid will display as traditional horizontal lines. The grid will align with your selected price point, and you can adjust the settings at any time through the indicator’s settings panel.

⚙️ CONFIGURATION AND SETTINGS ⚙️

Grid Settings

Accel (Acceleration): Controls how quickly the price reacts to changes over time.

Curve (Curvature): Defines the overall shape of the parabola.

Intervals (Grid Spacing): Determines the vertical spacing between the grid lines.

Sensitivity: Fine tunes the magnitude of Acceleration and Curve.

Buy Zones & Sell Zones: Define the number of grid levels used for potential buy and sell signals.

* Each zone is represented on the chart with different colors:

* Green: Buy Zones

* Red: Sell Zones

* Yellow: Overlap (Buy and Sell Zones intersect)

* Gray: Neutral areas

Trigger: Chooses which part of the candlestick is used to trigger a signal.

* `Wick`: Uses the high or low of the candlestick

* `Close`: Uses the closing price of the candlestick

* `Midpoint`: Uses the middle point between the high and low of the candlestick

* `SWMA`: Uses the Symmetrical Weighted Moving Average

Confirm: Specifies how a signal is confirmed.

* `Reverse`: The signal is confirmed if the price moves in the opposite direction of the initial trigger

* `Touch`: The signal is confirmed when the price touches the specified level or zone

Sentiment: Determines the market sentiment, which can influence signal generation.

* `Slope`: Sentiment is based on the direction of the curve, reflecting the current trend

* `Long`: Sentiment is bullish, favoring buy signals

* `Short`: Sentiment is bearish, favoring sell signals

* `Neutral`: Sentiment is neutral. No secondary signals will be generated

Show Signals: Toggles the display of buy and sell signals on the chart

Chart Settings

Grid Colors: These colors define the visual appearance of the grid lines

Projected: These colors define the visual appearance of the projected lines

Parabola/SWMA: Adjust colors as needed. These are disabled by default.

Time/Price

Start Time & Start Price: These set the starting point for the parabolic curve.

* These fields are automatically populated when you add the indicator to the chart and click on an initial location

* These can be adjusted manually in the settings panel, but he easiest way to change these is by directly interacting with the start point on the chart

Please note: Time and Price must be adjusted for each chart when switching assets. For example, a Start Price on BTCUSD of $60,000 will not work on an ETHUSD chart.

🤖 ALGORITHM AND CALCULATION 🤖

The Parabolic Function

At the core of the Parabolic Grid Bot lies the parabolic function, which calculates a dynamic curve that adapts to price action over time. This curve serves as the foundation for visualizing potential support and resistance levels.

The shape and behavior of the parabola are influenced by three key user-defined parameters:

Acceleration: This parameter controls the rate of change of the curve's slope, influencing its tilt or steepness. A higher acceleration value results in a more pronounced tilt, while a lower value leads to a gentler slope. This applies to both curved and linear grid configurations.

Curvature: This parameter introduces and controls the curvature or bend of the grid. A higher curvature value results in a more pronounced parabolic shape, while a lower value leads to a flatter curve or even a straight line (when set to zero).

Sensitivity: This setting fine-tunes the overall responsiveness of the grid, influencing how strongly the Acceleration and Curvature parameters affect its shape. Increasing sensitivity amplifies the impact of these parameters, making the grid more adaptable to price changes but potentially leading to more frequent adjustments. Decreasing sensitivity reduces their impact, resulting in a more stable grid structure with fewer adjustments. It may be necessary to adjust Sensitivity when switching between different assets or timeframes to ensure optimal scaling and responsiveness.

The parabolic function combines these parameters to generate a curve that visually represents the potential path of price movement. By understanding how these inputs influence the parabola's shape and behavior, traders can gain valuable insights into potential support and resistance areas, aiding in their decision-making process.

Sentiment

The Parabolic Grid Bot incorporates sentiment to enhance signal generation. The "Sentiment" input allows you to either:

Manually specify the market sentiment: Choose between 'Long' (bullish), 'Short' (bearish), or 'Neutral'.

Let the script determine sentiment based on the slope of the parabolic curve: If 'Slope' is selected, the sentiment will be considered 'Long' when the curve is sloping upwards, 'Short' when it's sloping downwards, and 'Neutral' when it's flat.

Buy and Sell Signals

The Parabolic Grid Bot generates buy and sell signals based on the interaction between the price and the grid levels.

Trigger: The "Trigger" input determines which part of the candlestick is used to trigger a signal (wick, close, midpoint, or SWMA).

Confirmation: The "Confirm" input specifies how a signal is confirmed ('Reverse' or 'Touch').

Zones: The number of "Buy Zones" and "Sell Zones" determines the areas on the grid where buy and sell signals can be generated.

When the trigger condition is met within a buy zone and the confirmation criteria are satisfied, a buy signal is generated. Similarly, a sell signal is generated when the trigger and confirmation occur within a sell zone.

Secondary Signals

Secondary signals are generated when a regular buy or sell signal contradicts the prevailing sentiment. For example:

A buy signal in a bearish market (Sentiment = 'Short') would be considered a "secondary buy" signal.

A sell signal in a bullish market (Sentiment = 'Long') would be considered a "secondary sell" signal.

These secondary signals are visually represented on the chart using hollow triangles, differentiating them from regular signals (filled triangles).

While they can be interpreted as potential contrarian trade opportunities, secondary signals can also serve other purposes within a grid trading strategy:

Exit Signals: A secondary signal can suggest a potential shift in market sentiment or a weakening trend. This could be a cue to consider exiting an existing position, even if it's currently profitable, to lock in gains before a potential reversal

Risk Management: In a strong trend, secondary signals might offer opportunities for cautious counter-trend trades with controlled risk. These trades could utilize smaller position sizes or tighter stop-losses to manage potential downside if the main trend continues

Dollar-Cost Averaging (DCA): During a prolonged trend, the parabolic curve might generate multiple secondary signals in the opposite direction. These signals could be used to implement a DCA strategy, gradually accumulating a position at potentially favorable prices as the market retraces or consolidates within the larger trend

Secondary signals should be interpreted with caution and considered in conjunction with other technical indicators and market context. They provide additional insights into potential market reversals or consolidation phases within a broader trend, aiding in adapting your grid trading strategy to the evolving market dynamics.

Examples

Trigger=Wick, Confirm=Touch. Signals are generated when the wick touches the next gridline.

Trigger=Close, Confirm=Touch. Signals require the close to touch the next gridline.

Trigger=SWMA, Confirm=Reverse. Signals are triggered when the Symmetrically Weighted Moving Average reverse crosses the next gridline.

🧠THEORY AND RATIONALE 🧠

The innovative approach of the Parabolic Grid Bot can be better understood by first examining the limitations of traditional grid trading strategies and exploring how this indicator addresses them by incorporating principles of market cycles and dynamic price behavior

Traditional Grid Bots: One-Dimensional and Static

Traditional grid bots operate on a simple premise: they divide the price chart into a series of equally spaced horizontal lines, creating a grid of trading zones. These bots excel in ranging markets where prices oscillate within a defined range. Buy and sell orders are placed at these grid levels, aiming to profit from mean reversion as prices bounce between the support and resistance zones.

However, traditional grid bots face challenges in trending markets. As the market moves in one direction, the bot continues to place orders in that direction, leading to a stacking of positions. If the market eventually reverses, these stacked trades can be profitable, amplifying gains. But the risk lies in the potential for the market to continue trending, leaving the trader with a series of losing trades on the wrong side of the market

The Parabolic Grid Bot: Adding Dimensions

The Parabolic Grid Bot addresses the limitations of traditional grid bots by introducing two additional dimensions:

Acceleration (Second Dimension): This parameter introduces a second dimension to the grid, allowing it to tilt upwards or downwards to align with the prevailing market trend. A positive acceleration creates an upward-sloping grid, suitable for uptrends, while a negative acceleration results in a downward-sloping grid, ideal for downtrends. The magnitude of acceleration controls the steepness of the tilt, enabling you to fine-tune the grid's responsiveness to the trend's strength

Curvature (Third Dimension): This parameter adds a third dimension to the grid by introducing a parabolic curve. The curve's shape, ranging from gentle bends to sharp turns, is controlled by the curvature value. This flexibility allows the grid to closely mirror the market's evolving structure, potentially identifying turning points and trend reversals.

Mean Reversion in Trending Markets

Even in trending markets, the Parabolic Grid Bot can help identify opportunities for mean reversion strategies. While the grid may be tilted to reflect the trend, the buy and sell zones can capture short-term price oscillations or consolidations within the broader trend. This allows traders to potentially pinpoint entry and exit points based on temporary pullbacks or reversals.

Visualize and Adapt

The Parabolic Grid Bot acts as a visual aid, enhancing your understanding of market dynamics. It allows you to "see the curve" by adapting the grid to the market's patterns. If the market shows a parabolic shape, like an upward curve followed by a peak and a downward turn (similar to a head and shoulders pattern), adjust the Accel and Curve to match. This highlights potential areas of interest for further analysis.

Beyond Straight Lines: Visualizing Market Cycle

Traditional technical analysis often employs straight lines, such as trend lines and support/resistance levels, to interpret market movements. However, many analysts, including Brian Millard, contend that these lines can be misleading. They propose that what might appear as a straight line could represent just a small part of a larger curve or cycle that's not fully visible on the chart.

Markets are inherently cyclical, marked by phases of expansion, contraction, and reversal. The Parabolic Grid Bot acknowledges this cyclical behavior by offering a dynamic, curved grid that adapts to these shifts. This approach helps traders move beyond the limitations of straight lines and visualize potential support and resistance levels in a way that better reflects the market's true nature

By capturing these cyclical patterns, whether subtle or pronounced, the Parabolic Grid Bot offers a nuanced understanding of market dynamics, potentially leading to more accurate interpretations of price action and informed trading decisions.

⚠️ DISCLAIMER⚠️

This indicator utilizes a parabolic curve fitting approach to visualize potential support and resistance levels. The mathematical formulas employed have been designed with adaptability and scalability in mind, aiming to accommodate various assets and price ranges. While the resulting curves may visually resemble parabolas, it's important to note that they might not strictly adhere to the precise mathematical definition of a parabola.

The indicator's calculations have been tested and generally produce reliable results. However, no guarantees are made regarding their absolute mathematical accuracy. Traders are encouraged to use this tool as part of their broader analysis and decision-making process, combining it with other technical indicators and market context.

Please remember that trading involves inherent risks, and past performance is not indicative of future results. It is always advisable to conduct your own research and exercise prudent risk management before making any trading decisions.

🧠 BEYOND THE CODE 🧠

The Parabolic Grid Bot, like the other grid bots in this series, is designed with education and community collaboration in mind. Its open-source nature encourages exploration, experimentation, and the development of new grid trading strategies. We hope this indicator serves as a framework and a starting point for future innovations in the field of grid trading.

Your comments, suggestions, and discussions are invaluable in shaping the future of this project. We welcome your feedback and look forward to seeing how you utilize and enhance the Parabolic Grid Bot.

Enhanced Overbought/Oversold IndicatorEnhanced Overbought/Oversold Indicator

Description:

The Enhanced Overbought/Oversold Indicator is a custom technical analysis tool designed to identify potential reversal points in the market by highlighting conditions of overbought and oversold levels on any timeframe. This indicator is based on the Relative Strength Index (RSI), a momentum oscillator that measures the speed and change of price movements.

Features:

Overbought & Oversold Levels:

Overbought (RSI > 70): Indicates that the market is potentially overvalued and might be due for a pullback. The candles are highlighted in Red to signal caution.

Oversold (RSI < 30): Indicates that the market is potentially undervalued and might be due for a bounce. The candles are highlighted in Green to signal potential buying opportunities.

Extreme Conditions:

Extreme Overbought (RSI > 85): Indicates an extremely overbought condition, suggesting a very high likelihood of a reversal or correction. The candles are highlighted in Blue.

Extreme Oversold (RSI < 15): Indicates an extremely oversold condition, suggesting a strong potential for a reversal upwards. The candles are highlighted in Yellow.

Dynamic Highlighting:

The indicator dynamically adjusts the candle colors based on the current RSI value, providing a clear visual representation of market conditions.

Applications:

Trend Reversals: By identifying extreme RSI levels, the indicator helps traders anticipate possible trend reversals.

Entry & Exit Points: Traders can use the highlighted signals to make more informed decisions about entering or exiting trades.

Risk Management: The color-coded signals can be used to manage risk, especially during extreme market conditions.

This indicator is particularly useful for traders looking for a straightforward visual representation of market conditions across different timeframes. By combining standard and extreme RSI levels, it helps identify not just overbought and oversold conditions but also extreme levels where significant reversals are more likely.

Multi Adaptive Moving Average (MAMA)The Multi Adaptive Moving Average (MAMA) indicator is an advanced tool for technical analysis, designed to provide traders with a detailed understanding of market trends and potential future price movements. This indicator utilizes multiple Simple Moving Averages (SMAs) and forecasting techniques to enhance decision-making processes.

Simple Moving Averages (SMAs):

Short MA (20-period): This moving average is highly responsive to price changes, making it ideal for capturing short-term trends. It helps traders identify quick market shifts and potential entry or exit points.

Mid MA (50-period): This average strikes a balance between short- and long-term trends, offering insights into the market's intermediate direction. It aids in confirming the sustainability of short-term trends.

Long MA (100-period): By smoothing out price data over a longer period, this moving average is useful for identifying long-term trends and filtering out short-term volatility.

Very Long MA (200-period): Often considered a critical indicator for determining the overall market trend, this average helps confirm the direction and strength of long-term movements.

Forecasting:

Flat Forecast: This approach assumes that prices will remain constant in the near future, which is particularly useful in markets trading sideways without a clear trend direction.

Linear Regression Forecast: This method uses historical data to project future price movements, offering a dynamic forecast based on existing trends. It helps traders anticipate potential price changes and plan their strategies accordingly.

Advantages: