Ehlers 2 Pole Butterworth Filter V1 [CC]The 2 Pole Butterworth Filter was created by John Ehlers (Cybernetic Analysis For Stocks And Futures pg 192) and this is one of his many filters that cuts out the noise and follows the price very closely. I recommend combining a 2 pole and 3 pole system of the same type of filter. Buy when the indicator line is green and sell when it is red.

Let me know if there are other indicators you would like to see or if you want something custom done!

Filter

Ehlers Super PassBand Filter [CC]The Super PassBand Filter was created by John Ehlers (Stocks & Commodities V. 34:07 (10–13)) and this is a pretty useful indicator to let you know how volatile the market is right now. This is useful for scalpers because this lets you avoid the choppy markets (usually when the rms is 1.50 or less but feel free to choose your own level) and gives you good entry and exit points. Buy when the indicator line is green and sell when it is red.

Let me know if there are other indicators you would like to see me publish or if you want something custom done!

Ehlers 2 Pole Super Smoother Filter V1 [CC]The 2 Pole Super Smoother Filter was created by John Ehlers (Cybernetic Analysis For Stocks And Futures pg 202) and this one of his filters that follows the price very closely. I would recommend to change the default settings to what fits your trading style the best. Buy when the indicator line turns green and sell when it turns red.

Let me know if there are other scripts you would like to see or if you want something custom done!

Ehlers Laguerre Filter [CC]The Laguerre Filter was created by John Ehlers (Cybernetic Analysis For Stocks And Futures pg 216) and this indicator works well with letting you know both the short and long term trend as well as a pretty good moving average. If the indicator line is above the black line then it is a long term uptrend and below the black line is a long term downtrend. Buy when the indicator line is green and sell when it turns red.

Let me know if there are other scripts you would like to see me publish or if you want something custom done!

Ehlers Roofing Filter [CC]The Roofing Filter was created by John Ehlers (Cycle Analytics For Traders pgs 81-82) and this can be interpreted in a few ways. When the indicator crosses over its signal then it is a short term uptrend and when it crosses below its signal then it is a short term downtrend. It is also in a major uptrend or downtrend when it is above 0 and below 0 respectively. Buy when the indicator line is green and sell when the indicator line turns red.

Let me know if there are other indicators you would like to see me publish or if you want something custom done!

Ehlers Truncated BandPass Filter [CC]Hot off the presses! The Truncated BandPass Filter was created by John Ehlers (Stocks & Commodities July 2020) and this is a much more reactive version of his original bandpass filter. When the indicator rises above 0 then it is an uptrend and when it falls below 0 then it is in a downtrend. Buy when the indicator line is red and sell when it is green.

Let me know if there are other scripts you would like to see me publish or if you want something custom done!

Ehlers HighPass-LowPass Roofing Filter [CC]The HighPass-LowPass Roofing Filter was created by John Ehlers (Cycle Analytics For Traders pg78) and this is a variation of a roofing filter that will let you know which direction the stock is trending. If it falls below 0 then the stock is in a downtrend and if it rises above 0 then it is an uptrend. Buy when the indicator line is green and sell when it is red.

Let me know if there are other scripts you would like me to publish or if you want something custom done!

Ehlers 3 Pole Butterworth Filter [CC]The 3 Pole Butterworth Filter was created by John Ehlers (Cycle Analytics For Traders pg 32) and this is a nice filter that follows the price very closely. Buy when the indicator is green and sell when it turns red.

This was a custom request so let me know if you would like me to publish any other scripts or if you want something custom done!

Ehlers Spectrum Derived Filter Bank [CC]The Spectrum Derived Filter Bank was created by John Ehlers (Stocks & Commodities V. 26:3 (16-22)) and this is technically two indicators in one. This will let you know the current cycle period which is in blue and the other indicator will let you know if you should buy the stock or not. Buy when it is green and sell when it is red.

Let me know if you would like me to publish other scripts or if you want something custom done!

Note: I'm republishing this because the original script couldn't be found in searches so this will fix that.

Ehlers Dominant Cycle Tuned Bypass Filter [CC]The Dominant Cycle Tuned Bypass Filter was created by John Ehlers (Stocks & Commodities V. 26:3 (16-22)) and this is a particularly unique indicator because this does a pretty good job at predicting the future stock movements. If the blue line crosses over the red then a few bars from now the stock price will most likely go up and if the blue line crosses below the red then a few bars from now the stock price should go down. Since this is such a unique indicator to use with entry and exit points, I don't have them color coded but try this out and let me know what you think.

This was a special request so let me know what other scripts you would like to see me publish or if you want anything custom done!

Note: I'm republishing this because the original script couldn't be found in searches so this will fix that.

Ehlers Swiss Army Knife Indicator [CC]The Swiss Army Knife Indicator was created by John Ehlers (Stocks & Commodities V. 24:1 (28-31, 50-53)) and it is 9 different filters in one big mega indicator! This is my first attempt at allowing you all to select different timeframes, to choose if you allow repainting or not, or by letting you choose which indicator you want to see on the chart. I know this may cause problems so feel free to send me a pm if you are stuck or if you have any questions!

This was a custom request so please let me know if you want to see me publish any other scripts or if you want something custom done!

Note: I'm republishing this because the original script couldn't be found in searches so this will fix that.

[LunaOwl] Swing Filter作品: 擺盪濾波器 (Swing Filter)

This is a Swing Filter, the function is to remind you that you do not need to trade during the neutral period, only buy or long when the series is higher than the high-level you set, when the series is lower than the low-level you set, you need to short or hedge. Hope your to use it happily. In a larger time frame, the length can be set smaller, the default value is 100.

這是一個擺盪濾波器,它的功能是提醒您在中性時期不用交易,僅在市場高水平的時候買進持有或做多,當來到低水平時需要做空或對沖。希望使用愉快。此外,在較大的時間框架,期數設定小一點,預設是100。

Long Wick TrialI've created this as a confirmation indicator to help know when market conditions are favorable to enter a trade. It measures volume, volatility, and ATR. It is not intended to tell you when to enter/exit the market, but use it with another indicator such as the mirror macd to filter out many losses and avoid entering the market during low volume or excessive volatility that may trip your stop loss.

Green = Favorable Market conditions

Yellow = Enter with caution, the market is moving sideways but is slightly trending

Orange = Enter with caution, the market is trending but extremely volatile and may trip stop loss early

Black = Shouldn't enter market here, market is moving sideways and volume is also low.

Filter Information Box - PineCoders FAQWhen designing filters it can be interesting to have information about their characteristics, which can be obtained from the set of filter coefficients (weights). The following script analyzes the impulse response of a filter in order to return the following information:

Lag

Smoothness via the Herfindahl index

Percentage Overshoot

Percentage Of Positive Weights

The script also attempts to determine the type of the analyzed filter, and will issue warnings when the filter shows signs of unwanted behavior.

DISPLAYED INFORMATION AND METHODS

The script displays one box on the chart containing two sections. The filter metrics section displays the following information:

- Lag : Measured in bars and calculated from the convolution between the filter's impulse response and a linearly increasing sequence of value 0,1,2,3... . This sequence resets when the impulse response crosses under/over 0.

- Herfindahl index : A measure of the filter's smoothness described by Valeriy Zakamulin. The Herfindahl index measures the concentration of the filter weights by summing the squared filter weights, with lower values suggesting a smoother filter. With normalized weights the minimum value of the Herfindahl index for low-pass filters is 1/N where N is the filter length.

- Percentage Overshoot : Defined as the maximum value of the filter step response, minus 1 multiplied by 100. Larger values suggest higher overshoots.

- Percentage Positive Weights : Percentage of filter weights greater than 0.

Each of these calculations is based on the filter's impulse response, with the impulse position controlled by the Impulse Position setting (its default is 1000). Make sure the number of inputs the filter uses is smaller than Impulse Position and that the number of bars on the chart is also greater than Impulse Position . In order for these metrics to be as accurate as possible, make sure the filter weights add up to 1 for low-pass and band-stop filters, and 0 for high-pass and band-pass filters.

The comments section displays information related to the type of filter analyzed. The detection algorithm is based on the metrics described above. The script can detect the following type of filters:

All-Pass

Low-Pass

High-Pass

Band-Pass

Band-Stop

It is assumed that the user is analyzing one of these types of filters. The comments box also displays various warnings. For example, a warning will be displayed when a low-pass/band-stop filter has a non-unity pass-band, and another is displayed if the filter overshoot is considered too important.

HOW TO SET THE SCRIPT UP

In order to use this script, the user must first enter the filter settings in the section provided for this purpose in the top section of the script. The filter to be analyzed must then be entered into the:

f(input)

function, where `input` is the filter's input source. By default, this function is a simple moving average of period length . Be sure to remove it.

If, for example, we wanted to analyze a Blackman filter, we would enter the following:

f(input)=>

pi = 3.14159,sum = 0.,sumw = 0.

for i = 0 to length-1

k = i/length

w = 0.42 - 0.5 * cos(2 * pi * k) + 0.08 * cos(4 * pi * k)

sumw := sumw + w

sum := sum + w*input

sum/sumw

EXAMPLES

In this section we will look at the information given by the script using various filters. The first filter we will showcase is the linearly weighted moving average (WMA) of period 9.

As we can see, its lag is 2.6667, which is indeed correct as the closed form of the lag of the WMA is equal to (period-1)/3 , which for period 9 gives (9-1)/3 which is approximately equal to 2.6667. The WMA does not have overshoots, this is shown by the the percentage overshoot value being equal to 0%. Finally, the percentage of positive weights is 100%, as the WMA does not possess negative weights.

Lets now analyze the Hull moving average of period 9. This moving average aims to provide a low-lag response.

Here we can see how the lag is way lower than that of the WMA. We can also see that the Herfindahl index is higher which indicates the WMA is smoother than the HMA. In order to reduce lag the HMA use negative weights, here 55% (as there are 45% of positive ones). The use of negative weights creates overshoots, we can see with the percentage overshoot being 26.6667%.

The WMA and HMA are both low-pass filters. In both cases the script correctly detected this information. Let's now analyze a simple high-pass filter, calculated as follows:

input - sma(input,length)

Most weights of a high-pass filters are negative, which is why the lag value is negative. This would suggest the indicator is able to predict future input values, which of course is not possible. In the case of high-pass filters, the Herfindahl index is greater than 0.5 and converges toward 1, with higher values of length . The comment box correctly detected the type of filter we were using.

Let's now test the script using the simple center of gravity bandpass filter calculated as follows:

wma(input,length) - sma(input,length)

The script correctly detected the type of filter we are using. Another type of filter that the script can detect is band-stop filters. A simple band-stop filter can be made as follows:

input - (wma(input,length) - sma(input,length))

The script correctly detect the type of filter. Like high-pass filters the Herfindahl index is greater than 0.5 and converges toward 1, with greater values of length . Finally the script can detect all-pass filters, which are filters that do not change the frequency content of the input.

WARNING COMMENTS

The script can give warning when certain filter characteristics are detected. One of them is non-unity pass-band for low-pass filters. This warning comment is displayed when the weights of the filter do not add up to 1. As an example, let's use the following function as a filter:

sum(input,length)

Here the filter pass-band has non unity, and the sum of the weights is equal to length . Therefore the script would display the following comments:

We can also see how the metrics go wild (note that no filter type is detected, as the detected filter could be of the wrong type). The comment mentioning the detection of high overshoot appears when the percentage overshoot is greater than 50%. For example if we use the following filter:

5*wma(input,length) - 4*sma(input,length)

The script would display the following comment:

We can indeed see high overshoots from the filter:

@alexgrover for PineCoders

Look first. Then leap.

Filter Amplitude Response Estimator - A Simple CalculationIn digital signal processing knowing how a system interact with the frequency content of an input signal is extremely important, the mathematical tool that give you this information is called "frequency response". The frequency response regroup two elements, the amplitude response, and the phase response. The amplitude response tells you how the system modify the amplitude of the frequency components in the input signal, the phase response tells you how the system modify the phase of the frequency components in the signal, each being a function of the frequency.

The today proposed tool aim to give a low resolution representation of the amplitude response of any filter.

What Is The Amplitude Response Of A Filter ?

Remember that filters allow to interact with the frequency content of a signal by amplifying, attenuating and/or removing certain frequency components in the input signal, the amplitude (also called magnitude) response of a filter let you know exactly how your filter change the amplitude of the frequency components in the input signal, another way to see the amplitude response is as a tool that tell you what is the peak amplitude of a filter using a sinusoid of a certain frequency as input signal.

For example if the amplitude response of a filter give you a value of 0.9 at frequency 0.5, it means that the filter peak amplitude using a sinusoid of frequency 0.5 is equal to 0.9.

There are several ways to calculate the frequency response of a filter, when our filter is a FIR filter (the filter impulse response is finite), the frequency response of the filter is the absolute value of the discrete Fourier transform (DFT) of the filter impulse response.

If you are curious about this process, know that the DFT of a N samples signal return N values, so if our FIR filter coefficients are composed of only 5 values we would get a frequency response of 5 values...which would not be useful, this is why we "pad" our coefficients with zeros, that is we add zeros to the start and end of our series of coefficients, this process is called "zero-padding", so if our series of coefficients is: (1,2,3,4,5), applying zero padding would give (0,0...1,2,3,4,5,...0,0) while keeping a certain symmetry. This is related to the concept of resolution, a low resolution amplitude response would be composed of a low number of values and would not be useful, this is why we use zero-padding to add more values thus increasing the resolution.

Making a Fourier transform in Pinescript is not doable, as you need the complex number i for computing a DFT, but thats not even the only problem, a DFT would not be that useful anyway (as the processes to make it useful in a trading context would be way too complex) . So how can we calculate a filter amplitude response without using a DFT ? The simple answer is by taking the peak amplitude of a filter using a sinusoid of a certain frequency as input, this is what the proposed tool do.

Using The Tool

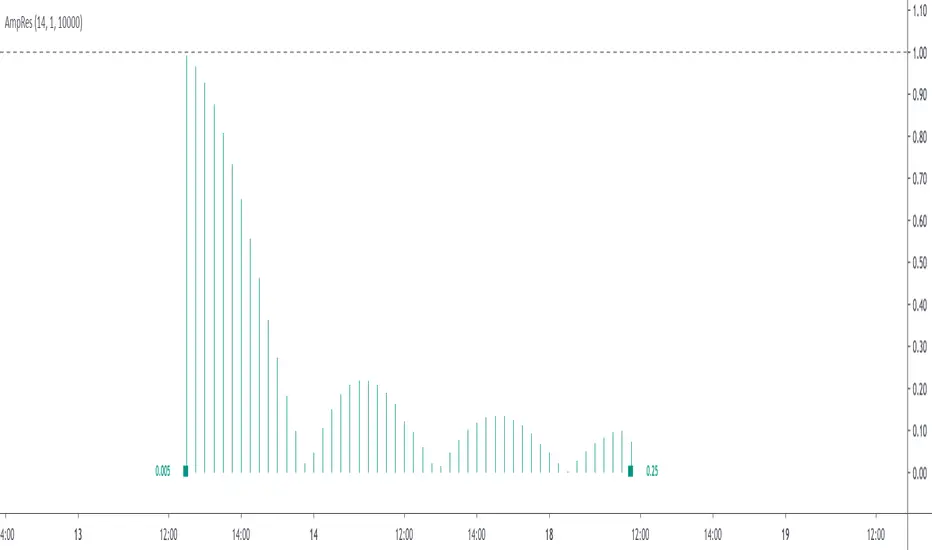

The proposed tool give you a 50 point amplitude response from frequency 0.005 to 0.25 by default. the setting "Range Divisor" allow you to see the amplitude response by using a different range of frequency, for example if the range divisor is equal to 2 the filter amplitude response will be evaluated from frequency 0.0025 to 0.125.

In the script, filt hold the filter you want to see the frequency response, by default a simple moving average.

The position of the frequency response is defined by the "Show Amplitude Response At Bar Number" setting, if you want the frequency response to start at bar number 5000 then enter 5000, by default 10000. If you are not a premium set the number at 4000 and it should work.

amplitude response of a simple moving average of period 14, res = 2.

By default the amplitude response use an amplitude scale, a value of 1 represent an unchanged amplitude. You can use Dbfs (decibel full scale) instead by checking the "To Decibels (Full Scale)" setting.

Dbfs amplitude response, a value of 0 represent an unchanged amplitude.

Some Amplitude Responses

In order to prove the accuracy of the proposed tool we can compare the amplitude response given by the proposed tool with the mathematical function of the amplitude response of a simple moving average, that is:

abs(sin(pi*f*length)/(length*sin(pi*f)))

In cyan the amplitude response given by the proposed tool and in blue the above function. Below are the amplitude responses of some moving averages with period 14.

Amplitude response of an EMA, the EMA is a IIR filter, therefore the amplitude response can't be made by taking the DFT of the impulse response (as this ones has infinite length), however our tool can give its frequency response.

Amplitude response of the Hull MA, as you can see some frequencies are amplified, this is common with low-lag filters.

Gaussian moving average (ALMA), with offset = 0.5 and sigma = 6.

Simple moving average high-pass filter amplitude response

Center of gravity bandpass filter amplitude response

Center of gravity bandreject filter.

IMPORTANT!: The amplitude response of adaptive moving averages is not stationary and might change over time.

Conclusion

A tool giving the amplitude response of any filter has been presented, of course this method is not efficient at all and has a low resolution of 50 points (the common resolution is of 512 points) and is difficult to work with, but has the merit to work on Tradingview and can give the frequency response of IIR filters, if you really need to see the frequency response of a filter then i recommend you to use the function freqz from the scipy package.

I still hope you will enjoy using this tool to have a look at the amplitude responses of your favorite moving averages.

I'am aware of the current situation, however i'am somehow feeling left out from the pinescript community, let me know via PM if i have done something to you and i'll do my best to fix any problems i might have caused (or i might be being parano xD)

Sequential Filter - An Original Filtering ApproachRemoving irregular variations in the closing price remain a major task in technical analysis, indicators used to this end mostly include moving averages and other kind of low-pass filters. Understanding what kind of variations we want to remove is important, irregular (noisy) variations have mostly a short term period, fully removing them can be complicated if the filter is not properly selected, for example we might want to fully remove variations with a period of 2 bars and lower, if we select an arithmetic moving average the filter output might still contain such variations because of the ripples in the frequency response passband, all it would take is a variation of high amplitude for that variation to be clearly visible.

Although all it would take for better filtering is a filter with better performance in the frequency domain (gaussian, Butterworth, Bessel...) we can design innovative approaches that does not rely on the model of classical moving averages, today a new technical indicator is proposed, the technical indicator fully remove variations lower than the selected period.

The Indicator Approach

In order for the indicator output to change the closing price need to produce length consecutive up's/down's, length control the variation threshold of the indicator, variations lower than length are fully removed. Lets see a visual example :

Here length = 3, the closing price need to make 3 consecutive up's/down's, when the sequence happen the indicator output is equal to src , here the closing price, else the indicator is equal to its precedent value, hence removing other variations. The value of 3 is the value by default, this is because i have seen in the past that the average smallest variations period where in general of 3 bars.

Because the indicator focus only on the variation sign, it totally ignore the amplitude of the movement, this provide an effective way to filter short term retracement in a fluctuation as show'n below :

The candle option of the indicator allow the indicator to only focus on the body color of a candle, thus ignoring potential gaps, below is an example with the candle option off :

If we activate the "candle" option we end up with :

Note that the candle option is based on the closing and opening price, if you use the indicator on another indicator output make sure to have the candle option off.

Length and Indicator Color

The closing price is infected by noise, and will rarely make a large sequence of consecutive up's/down's, the indicator can therefore be useful to detect consecutive sequence of length period, here 6 is selected on BTCUSD :

A consecutive up's/down's of period 6 can be considered a relatively rare event.

It is important to note that the color of the indicator used by default has nothing to do with the consecutive sequence detected, that is the indicator turning red doesn't necessarily mean that a consecutive down's sequence has occurred, but only that this sequence has occurred at a lower value than the precedent detected sequence. This is show'n below :

In order to make the indicator color based on the detected sequence check the "Color Based On Detected Sequence" option.

Conclusion

An original approach on filtering price variations has been proposed, i believe the indicator code is elegant as well as relatively efficient, and since high values of length can't really be used the indicator execution speed will remain relatively fast.

Thanks for reading !

Grand Trend Forecasting - A Simple And Original Approach Today we'll link time series forecasting with signal processing in order to provide an original and funny trend forecasting method, the post share lot of information, if you just want to see how to use the indicator then go to the section "Using The Indicator".

Time series forecasting is an area dealing with the prediction of future values of a series by using a specific model, the model is the main tool that is used for forecasting, and is often an expression based on a set of predictor terms and parameters, for example the linear regression (model) is a 1st order polynomial (expression) using 2 parameters and a predictor variable ax + b . Today we won't be using the linear regression nor the LSMA.

In time series analysis we can describe the time series with a model, in the case of the closing price a simple model could be as follows :

Price = Trend + Cycles + Noise

The variables of the model are the components, such model is additive since we add the component with each others, we should be familiar with each components of the model, the trend represent a simple long term variation of high amplitude, the cycles are periodic fluctuations centered around 0 of varying period and amplitude, the noise component represent shorter term irregular variations with mean 0.

As a trader we are mostly interested by the cycles and the trend, altho the cycles are relatively more technical to trade and can constitute parasitic fluctuations (think about retracements in a trend affecting your trend indicator, causing potential false signals).

If you are curious, in signal processing combining components has a specific name, "synthesis" , here we are dealing with additive synthesis, other type of synthesis are more specific to audio processing and are relatively more complex, but could be used in technical analysis.

So what to do with our components ? If we want to trade the trend, we should estimate right ? Estimating the trend component involve removing the cycle and noise component from the price, if you have read stuff about filters you should know where i'am going, yep, we should use filters, in the case of keeping the trend we can use a simple moving average of relatively high period, and here we go.

However the lag problem, which is recurrent, come back again, we end up with information easier to interpret (here the trend, which is a simple fluctuation such as a line or other smooth curve) at the cost of decision timing, that is unfortunate but as i said the information, here the moving average output, is relatively simple, and could be easily forecasted right ? If you plot a moving average of high period it would be easier for you to forecast its future values. And thats what we aim to do today, provide an estimate of the trend that should be easy to forecast, and should fit to the price relatively well in order to produce forecast that could determine the position of future closing prices observations.

Estimating And Forecasting The Trend

The parameter of the indicator dealing with the estimation of the trend is length , with higher values of length attenuating the cycle and noise component in the price, note however that high values of length can return a really long term trend unlike a simple moving average, so a small value of length, 14 for example can still produce relatively correct estimate of trend.

here length = 14.

The rough estimate of the trend is t in the code, and is an IIR filter, that is, it is based on recursion. Now i'll pass on the filter design explanation but in short, weights are constants, with higher weights allocated to the previous length values of the filter, you can see on the code that the first part of t is similar to an exponential moving average with :

t(n) = 0.9t(n-length) + 0.1*Price

However while the EMA only use the precedent value for the recursion, here we use the precedent length value, this would just output a noisy and really slow output, therefore in order to create a better fit we add : 0.9*(t(n-length) - t(n-2length)) , and this create the rough trend estimate that you can see in blue. On the parameters, 0.9 is used since it gives the best estimate in my opinion, higher values would create more periodic output and lower values would just create a rougher output.

The blue line still contain a residual of the cycle/noise component, this is why it is smoothed with a simple moving average of period length. If you are curious, a filter estimating the trend but still containing noisy fluctuations is called "Notch" filter, such filter would depending on the cutoff remove/attenuate mid term cyclic fluctuations while preserving the trend and the noise, its the opposite of a bandpass filter.

In order to forecast values, we simply sum our trend estimate with the trend estimate change with period equal to the forecasting horizon period, this is a really really simple forecasting method, but it can produce decent results, it can also allows the forecast to start from the last point of the trend estimate.

Using The Indicator

We explained the length parameter in the precedent section, src is the input series which the trend is estimated, forecast determine the forecasting horizon, recommend values for forecast should be equal to length, length/2 or length*2, altho i strongly recommend length.

here length and forecast are both equal to 14 .

The corrective parameter affect the trend estimate, it reduce the overshoot and can led to a curve that might fit better to the price.

The indicator with the non corrective version above, and the corrective one below.

The source parameter determine the source of the forecast, when "Noisy" is selected the source is the blue line, and produce a noisy forecast, when "Smooth" is selected the source is the moving average of t , this create a smoother forecast.

The width interval control...the width of the intervals, they can be seen above and under the forecast plot, they are constructed by adding/subtracting the forecast with the forecast moving average absolute error with respect to the price. Prediction intervals are often associated with a probability (determining the probability of future values being between the interval) here we can't determine such probability with accuracy, this require (i think) an analysis of the forecasting distribution as well as assumptions on the distribution of the forecasting error.

Finally it is possible to see historical forecasts, that is, forecasts previously generated by checking the "Show Historical Forecasts" option.

Examples

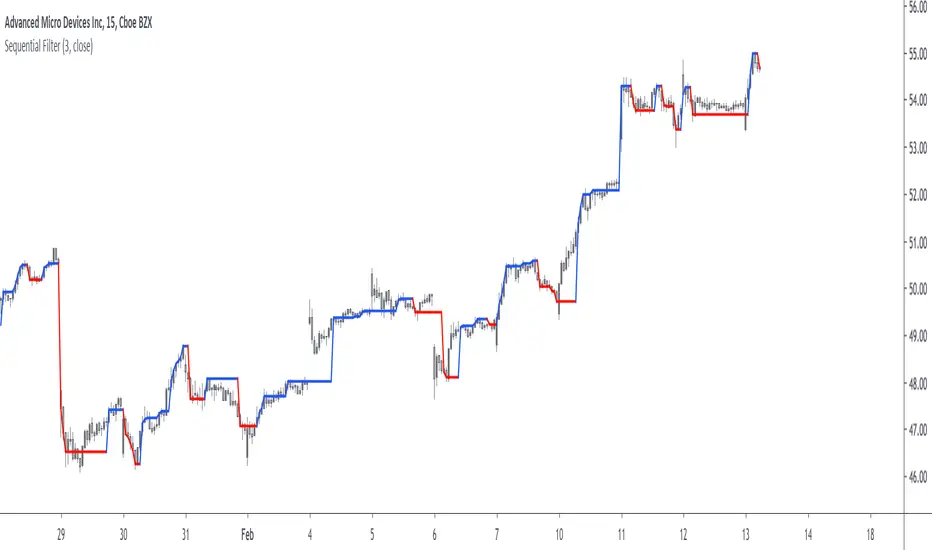

Good forecasts mostly occur when the price is close to the trend estimate, this include the following highlighted periods on AMD 15TF with default settings :

We can see the same thing at the end of EURUSD :

However we can't always obtain suitable fits, here it is isn't sufficient on BTCUSD :

We can see wide intervals, we could change length or use the corrective option to get better results, another option is to use a log scale.

We will end the examples with the log SPX, who posses a linear trend, so for example a linear model such as a linear regression would be really adapted, lets see how the indicator perform :

Not a great fit, we could try to use an higher length value and use "Smooth" :

Most recent fits are quite decent.

Conclusions

A forecasting indicator has been presented in this post. The indicator use an original approach toward estimating the trend component in the closing price. Of course i should have given statistics related to the forecasting error, however such analysis is worth doing with better methods and in more advanced environment allowing for optimization.

But we have learned some stuff related to signal processing as well as time series analysis, seeing a time series as the sum of various components is really helpful when it comes to make sense of chaotic and noisy series and is a basic topic in time series analysis.

You can see that in this new year i work harder on the visual of my indicators without trying to fall in the label addict trap, something that i wasn't really doing before, let me know what do you think of it.

Thanks for reading !

Time Series Lag Reduction Filter by CryptorhythmsTime Series Lag Reduction Filter by Cryptorhythms

Description

A little filter to reduce lag on any time series data. Here we use an EMA to demonstrate how it works, but you could use it in many different ways/appications.

This method can cause overshoot if you get too aggressive with the "lagReduce" setting. In this case lower the lagReduce variable.

👍 We hope you enjoyed this indicator and find it useful! We post free crypto analysis, strategies and indicators regularly. This is our 76th script on Tradingview!

Roofing Filter [DW]This is an experimental study built on the concept of using roofing filters on price data proposed by John Ehlers.

Roofing filters are a type of bandpass filter conventionally used in HF radio receivers in the first IF stage to limit the frequency spectrum passed on to later stages in the receiver.

The goal in applying roofing filters to a price signal is to simultaneously attenuate high frequency noise and low frequency distortion to pass an oscillating signal with a nearly zero mean for analysis and/or further calculation.

In this study, there are three filter types to choose from:

-> Ehlers Roofing Filter, which passes data through a 2 pole high pass filter, then through a Super Smoother filter.

-> Gaussian Roofing Filter, which passes data through a 2 pole Gaussian high pass filter, then through a 2 pole Gaussian low pass filter.

-> Butterworth Roofing Filter, which passes data through a 2 pole Butterworth high pass filter, then through a 2 pole Butterworth low pass filter.

Each filter type has different amplitude and delay characteristics, so play around with each type and see which response suits your needs best.

There is an option to normalize the scale of the output as well. The normalization process in this script is computed by comparing positive and negative outputs to the filter's moving RMS value.

The resulting oscillator can be fed through numerous conventional indicators including Stochastic Oscillator, RSI, CCI, etc. to generate smoother, less distorted indicators for a clearer view of turning points.

Alternatively, it can also act as an indicator itself, as implied by the corresponding color scheme included in the script.

Although roofing filters are not conventionally used in the analysis of market data, applying such spectral analysis techniques may prove to be quite useful for the design of more efficient indicators and more reliable predictions.

Low Pass Channel [DW]This is an experimental study designed to attenuate higher frequency oscillations in price and volatility with minimal lag.

In this study, a single pole low pass filter is used. The low pass filter's cutoff period is determined either by a fixed user input, or by using an Instantaneous Frequency Measurement (IFM) algorithm.

Most radar warning, electronic countermeasures, and electronic intelligence systems employ IFM to identify threats, map the electronic battlefield, and implement deceptive countermeasures.

The IFM technique used for this study was devised by John Ehlers. It calculates In Phase and Quadrature (IQ) components using the Hilbert Transform and uses them to determine the dominant price cycle.

To generate the channel, the same filter approach is applied to true range then added to and subtracted from the price filter.

Custom bar colors are included for simple wave and trend indication.

Damped Sine Wave Weighted FilterIntroduction

Remember that we can make filters by using convolution, that is summing the product between the input and the filter coefficients, the set of filter coefficients is sometime denoted "kernel", those coefficients can be a same value (simple moving average), a linear function (linearly weighted moving average), a gaussian function (gaussian filter), a polynomial function (lsma of degree p with p = order of the polynomial), you can make many types of kernels, note however that it is easy to fall into the redundancy trap.

Today a low-lag filter who weight the price with a damped sine wave is proposed, the filter characteristics are discussed below.

A Damped Sine Wave

A damped sine wave is a like a sine wave with the difference that the sine wave peak amplitude decay over time.

A damped sine wave

Used Kernel

We use a damped sine wave of period length as kernel.

The coefficients underweight older values which allow the filter to reduce lag.

Step Response

Because the filter has overshoot in the step response we can conclude that there are frequencies amplified in the passband, we could have reached to this conclusion by simply seeing the negative values in the kernel or the "zero-lag" effect on the closing price.

Enough ! We Want To See The Filter !

I should indeed stop bothering you with transient responses but its always good to see how the filter act on simpler signals before seeing it on the closing price. The filter has low-lag and can be used as input for other indicators

Filter with length = 100 as input for the rsi.

The bands trailing stop utility using rolling squared mean average error with length 500 using the filter of length 500 as input.

Approximating A Least Squares Moving Average

A least squares moving average has a linear kernel with certain values under 0, a lsma of length k can be approximated using the proposed filter using period p where p = k + k/4 .

Proposed filter (red) with length = 250 and lsma (blue) with length = 200.

Conclusions

The use of damping in filter design can provide extremely useful filters, in fact the ideal kernel, the sinc function, is also a damped sine wave.

Keltner Channel with signals [ChuckBanger]This is Keltner Channel where I added Bull and Bear signals. It has a lot of settings to play around with. Have fun...

For more information on Keltner Channel: www.investopedia.com