Extreme Trend Reversal Points [HeWhoMustNotBeNamed]Using moving average crossover for identifying the change in trend is very common. However, this method can give lots of false signals during the ranging markets. In this algorithm, we try to find the extreme trend by looking at fully aligned multi-level moving averages and only look at moving average crossover when market is in the extreme trend - either bullish or bearish. These points can mean long term downtrend or can also cause a small pullback before trend continuation. In this discussion, we will also check how to handle different scenarios.

🎲 Components

🎯 Recursive Multi Level Moving Averages

Multi level moving average here refers to applying moving average on top of base moving average on multiple levels. For example,

Level 1 SMA = SMA(source, length)

Level 2 SMA = SMA(Level 1 SMA, length)

Level 3 SMA = SMA(Level 2 SMA, length)

..

..

..

Level n SMA = SMA(Level (n-1) SMA, length)

In this script, user can select how many levels of moving averages need to be calculated. This is achieved through " recursive moving average " algorithm. Requirement for building such algorithm was initially raised by @loxx

While I was able to develop them in minimal code with the help of some of the existing libraries built on arrays and matrix , I also thought why not extend this to find something interesting.

Note that since we are using variable levels - we will not be able to plot all the levels of moving average. (This is because plotting cannot be done in the loop). Hence, we are using lines to display the latest moving average levels in front of the last candle. Lines are color coded in such a way that least numbered levels are greener and higher levels are redder.

🎯 Finding the trend and range

Strength of fully aligned moving average is calculated based on position of each level with respect to other levels.

For example, in a complete uptrend, we can find

source > L(1)MA > L(2)MA > L(3)MA ...... > L(n-1)MA > L(n)MA

Similarly in a complete downtrend, we can find

source < L(1)MA < L(2)MA < L(3)MA ...... < L(n-1)MA < L(n)MA

Hence, the strength of trend here is calculated based on relative positions of each levels. Due to this, value of strength can range from 0 to Level*(Level-1)/2

0 represents the complete downtrend

Level*(Level-1)/2 represents the complete uptrend.

Range and Extreme Range are calculated based on the percentile from median. The brackets are defined as per input parameters - Range Percentile and Extreme Range Percentile by using Percentile History as reference length.

Moving average plot is color coded to display the trend strength.

Green - Extreme Bullish

Lime - Bullish

Silver - range

Orange - Bearish

Red - Extreme Bearish

🎯 Finding the trend reversal

Possible trend reversals are when price crosses the moving average while in complete trend with all the moving averages fully aligned. Triangle marks are placed in such locations which can help observe the probable trend reversal points. But, there are possibilities of trend overriding these levels. An example of such thing, we can see here:

In order to overcome this problem, we can employ few techniques.

1. After the signal, wait for trend reversal (moving average plot color to turn silver) before placing your order.

2. Place stop orders on immediate pivot levels or support resistance points instead of opening market order. This way, we can also place an order in the direction of trend. Whichever side the price breaks out, will be the direction to trade.

3. Look for other confirmations such as extremely bullish and bearish candles before placing the orders.

🎯 An example of using stop orders

Let us take this scenario where there is a signal on possible reversal from complete uptrend.

Create a box joining high and low pivots at reasonable distance. You can also chose to add 1 ATR additional distance from pivots.

Use the top of the box as stop-entry for long and bottom as stop-entry for short. The other ends of the box can become stop-losses for each side.

After few bars, we can see that few more signals are plotted but, the price is still within the box. There are some candles which touched the top of the box. But, the candlestick patterns did not represent bullishness on those instances. If you have placed stop orders, these orders would have already filled in. In that case, just wait for position to hit either stop or target.

For bullish side, targets can be placed at certain risk reward levels. In this case, we just use 1:1 for bullish (trend side) and 1:1.5 for bearish side (reversal side)

In this case, price hit the target without any issue:

Wait for next reversal signal to appear before placing another order :)

Индикаторы и стратегии

Oscillator Workbench — Chart [LucF]█ OVERVIEW

This indicator uses an on-chart visual framework to help traders with the interpretation of any oscillator's behavior. The advantage of using this tool is that you do not need to know all the ins and outs of a particular oscillator such as RSI, CCI, Stochastic, etc. Your choice of oscillator and settings in this indicator will change its visuals, which allows you to evaluate different configurations in the context of how the workbench models oscillator behavior. My hope is that by using the workbench, you may come up with an oscillator selection and settings that produce visual cues you find useful in your trading.

The workbench works on any symbol and timeframe. It uses the same presentation engine as my Delta Volume Channels indicator; those already familiar with it will feel right at home here.

█ CONCEPTS

Oscillators

An oscillator is any signal that moves up and down a centerline. The centerline value is often zero or 50. Because the range of oscillator values is different than that of the symbol prices we look at on our charts, it is usually impossible to display an oscillator on the chart, so we typically put oscillators in a separate pane where they live in their own space. Each oscillator has its own profile and properties that dictate its behavior and interpretation. Oscillators can be bounded , meaning their values oscillate between fixed values such as 0 to 100 or +1 to -1, or unbounded when their maximum and minimum values are undefined.

Oscillator weight

How do you display an oscillator's value on a chart showing prices when both values are not on the same scale? The method I use here converts the oscillator's value into a percentage that is used to weigh a reference line. The weight of the oscillator is calculated by maintaining its highest and lowest value above and below its centerline since the beginning of the chart's history. The oscillator's relative position in either of those spaces is then converted to a percentage, yielding a positive or negative value depending on whether the oscillator is above or below its centerline. This method works equally well with bounded and unbounded oscillators.

Oscillator Channel

The oscillator channel is the space between two moving averages: the reference line and a weighted version of that line. The reference line is a moving average of a type, source and length which you select. The weighted line uses the same settings, but it averages the oscillator-weighted price source.

The weight applied to the source of the reference line can also include the relative size of the bar's volume in relation to previous bars. The effect of this is that the oscillator's weight on bars with higher total volume will carry greater weight than those with lesser volume.

The oscillator channel can be in one of four states, each having its corresponding color:

• Bull (teal): The weighted line is above the reference line.

• Strong bull (lime): The bull condition is fulfilled and the bar's close is above the reference line and both the reference and the weighted lines are rising.

• Bear (maroon): The weighted line is below the reference line.

• Strong bear (pink): The bear condition is fulfilled and the bar's close is below the reference line and both the reference and the weighted lines are falling.

Divergences

In the context of this indicator, a divergence is any bar where the slope of the reference line does not match that of the weighted line. No directional bias is assigned to divergences when they occur. You can also choose to define divergences as differences in polarity between the oscillator's slope and the polarity of close-to-close values. This indicator's divergences are designed to identify transition levels. They have no polarity; their bullish/bearish bias is determined by the behavior of price relative to the divergence channel after the divergence channel is built.

Divergence Channel

The divergence channel is the space between two levels (by default, the bar's low and high ) saved when divergences occur. When price has breached a channel and a new divergence occurs, a new channel is created. Until that new channel is breached, bars where additional divergences occur will expand the channel's levels if the bar's price points are outside the channel.

Price breaches of the divergence channel will change its state. Divergence channels can be in one of five different states:

• Bull (teal): Price has breached the channel to the upside.

• Strong bull (lime): The bull condition is fulfilled and the oscillator channel is in the strong bull state.

• Bear (maroon): Price has breached the channel to the downside.

• Strong bear (pink): The bear condition is fulfilled and the oscillator channel is in the strong bear state.

• Neutral (gray): The channel has not been breached.

█ HOW TO USE THE INDICATOR

Load the indicator on an active chart (see here if you don't know how).

The default configuration displays:

• The Divergence channel's levels.

• Bar colors using the state of the oscillator channel.

The default settings use:

• RSI as the oscillator, using the close source and a length of 20 bars.

• An Arnaud-Legoux moving average on the close and a length of 20 bars as the reference line.

• The weighted version of the reference line uses only the oscillator's weight, i.e., without the relative volume's weight.

The weighted line is capped to three standard deviations of the reference.

• The divergence channel's levels are determined using the high and low of the bars where divergences occur.

Breaches of the channel require a bar's low to move above the top of the channel, and the bar's high to move below the channel's bottom.

No markers appear on the chart; if you want to create alerts from this script, you will need first to define the conditions that will trigger the markers, then create the alert, which will trigger on those same conditions.

To learn more about how to use this indicator, you must understand the concepts it uses and the information it displays, which requires reading this description. There are no videos to explain it.

█ FEATURES

The script's inputs are divided in five sections: "Oscillator", "Oscillator channel", "Divergence channel", "Bar Coloring" and "Marker/Alert Conditions".

Oscillator

This is where you configure the oscillator you want to study. Thirty oscillators are available to choose from, but you can also use an oscillator from another indicator that is on your chart, if you want. When you select an external indicator's plot as the oscillator, you must also specify the value of its centerline.

Oscillator Channel

Here, you control the visibility and colors of the reference line, its weighted version, and the oscillator channel between them.

You also specify what type of moving average you want to use as a reference line, its source and its length. This acts as the oscillator channel's baseline. The weighted line is also a moving average of the same type and length as the reference line, except that it will be calculated from the weighted version of the source used in the reference line. By default, the weighted line is capped to three standard deviations of the reference line. You can change that value, and also elect to cap using a multiple of ATR instead. The cap provides a mechanism to control how far the weighted line swings from the reference line. This section is also where you can enable the relative volume component of the weight.

Divergence Channel

This is where you control the appearance of the divergence channel and the key price values used in determining the channel's levels and breaching conditions. These choices have an impact on the behavior of the channel. More generous level prices like the default low and high selection will produce more conservative channels, as will the default choice for breach prices.

In this section, you can also enable a mode where an attempt is made to estimate the channel's bias before price breaches the channel. When it is enabled, successive increases/decreases of the channel's top and bottom levels are counted as new divergences occur. When one count is greater than the other, a bull/bear bias is inferred from it. You can also change the detection mode of divergences, and choose to display a mark above or below bars where divergences occur.

Bar Coloring

You specify here:

• The method used to color chart bars, if you choose to do so.

• If you want to hollow out the bodies of bars where volume has not increased since the last bar.

Marker/Alert Conditions

Here, you specify the conditions that will trigger up or down markers. The trigger conditions can include a combination of state transitions of the oscillator and the divergence channels. The triggering conditions can be filtered using a variety of conditions.

Configuring the marker conditions is necessary before creating an alert from this script, as the alert will use the marker conditions to trigger.

Realtime values will repaint, as is usually the case with oscillators, but markers only appear on bar closes, so they will not repaint. Keep in mind, when looking at markers on historical bars, that they are positioned on the bar when it closes — NOT when it opens.

Raw values

The raw values calculated by this script can be inspected using the Data Window, including the oscillator's value and the weights.

█ INTERPRETATION

Except when mentioned otherwise, this section's charts use the indicator's default settings, with different visual components turned on or off.

The aim of the oscillator channel is to provide a visual representation of an oscillator's general behavior. The simplest characteristic of the channel is its bull/bear state, determined by whether the weighted line is above or below the reference line. One can then distinguish between its bull and strong bull states, as transitions from strong bull to bull states will generally happen when trends are losing steam. While one should not infer a reversal from such transitions, they can be a good place to tighten stops. Only time will tell if a reversal will occur. One or more divergences will often occur before reversals. This shows the oscillator channel, with the reference line and the thicker, weighted line:

The nature of the divergence channel 's design makes it particularly adept at identifying consolidation areas if its settings are kept on the conservative side. The divergence channel will also reveal transition areas. A gray divergence channel should usually be considered a no-trade zone. More adventurous traders can use the oscillator channel to orient their trade entries if they accept the risk of trading in a neutral divergence channel, which by definition will not have been breached by price. This show only the divergence channels:

This chart shows divergence channels and their levels, and colors bars on divergences and on the state of the oscillator channel, which is not visible on the chart:

If your charts are already busy with other stuff you want to hold on to, you could consider using only the chart bar coloring component of this indicator. Here we only color bars using the combined state of the oscillator and divergence channel, and we do not color the bodies of bars where volume has not increased. Note that my chart's settings do not color the candle bodies:

At its simplest, one way to use this indicator would be to look for overlaps of the strong bull/bear colors in both the oscillator channel and a divergence channel, as these identify points where price is breaching the divergence channel when the oscillator's state is consistent with the direction of the breach.

Tip

One way to use the Workbench is to combine it with my Delta Volume Channels indicator. If both indicators use the same MA as a reference line, you can display its delta volume channel instead of the oscillator channel.

This chart shows such a setup. The Workbench displays its divergence levels, the weighted reference line using the default RSI oscillator, and colors bars on divergences. The DV Channels indicator only displays its delta volume channel, which uses the same MA as the workbench for its baseline. This way you can ascertain the volume delta situation in contrast with the visuals of the Workbench:

█ LIMITATIONS

• For some of the oscillators, assumptions are made concerning their different parameters when they are more complex than just a source and length.

See the `oscCalc()` function in this indicator's code for all the details, and ask me in a comment if you can't find the information you need.

• When an oscillator using volume is selected and no volume information is available for the chart's symbol, an error will occur.

• The method I use to convert an oscillator's value into a percentage is fragile in the early history of datasets

because of the nascent expression of the oscillator's range during those early bars.

█ NOTES

Working with this workbench

This indicator is called a workbench for a reason; it is designed for traders interested in exploring its behavior with different oscillators and settings, in the hope they can come up with a setup that suits their trading methodology. I cannot tell you which setup is the best because its setup should be compatible with your trading methodology, which may require faster or slower transitions, thus different configurations of the settings affecting the calculations of the divergence channels.

For Pine Script™ Coders

• This script uses the new overload of the fill() function which now makes it possible to do vertical gradients in Pine. I use it for both channels displayed by this script.

• I use the new arguments for plot() 's `display` parameter to control where the script plots some of its values,

namely those I only want to appear in the script's status line and in the Data Window.

• I used my ta library for some of the oscillator calculations and helper functions.

• I also used TradingView's ta library for other oscillator calculations.

• I wrote my script using the revised recommendations in the Style Guide from the Pine v5 User Manual.

Average Volume ProfileAverage Volume Profile is an abstract based on a user suggestion.

The information displayed could be summed up as a volume profile divided by a market profile.

This indicator is a profile which displays the average volume of an area (of price).

It also calculates and displays the highest average volume point (HAV) and the relating value zones (calculated in the similar fashion to a volume profile).

Most of the code is directly from my "Volume/Market Profile" Indicator

I am not entirely sure of how to make use of the information displayed in this indicator or how useful it is.

However, I have added some things I figured would be useful to comprehend this information, such as:

- Read-out for highest average volume

- Read-out for current price average volume

- Read-out for current candle distributed volume (labeled as: "Vol")

- Floating line to visualize the current distributed volume in relation to the rest of the profile.

- Color changing labels for when the current distributed volume is higher than the current price avg volume.

Enjoy!

Sector RotationThis script is attempt to create and observe the real-time and historical performance of the all major sectors of Indian Market in one screen.

for Data Presentation I used Short sector names so that I can manage to get space and efficient presentable data.

Short Names and Actual Sector Names

BNF : CNX-BANKNIFTY

IT : CNX-IT

PRMA : CNX - PHARMA

FMCG : CNX-FMCG

AUTO : CNX-AUTO

MTAL : CNX-METAL

MDIA : CNX-MEDIA

RLTY : CNX-REALTY

IFRA : CNX-INFRA

ENGY : CNX-ENERGY

PSU-B : CNX-PSU-BANK

PVT-B : NIFTY-PVT-BANK

F-SRV : CNX-FINANCE

CONSM : CNX-CONSUMPTION

C-DUBL : NIFTY_CONSR_DURBL

You can use this script in 30-min, Daily, Weekly and Monthly Time Frames.

The green Square denotes the current Symbol Performance.

The Blue Border boxes are created when one sector intersects other sector.

In this Update following features are added

Now users have control over sectors, what are all the sectors you wanted to plot you can select from the input menu.

Currently user can highlight any one sector in different border color so that user can easily spot and track particular sector.

This thicker blue line denotes lowest and highest point of the current timeframe.

HH-LL ZZAnother ZigZag, yes...

I believe though this concerns another angle/principle, therefore I wanted to share

How does it work?

Given:

source for level breach -> close

X breaches -> 3

Let's say this is the latest found 'lower low' (LL - blue dot under bar):

This bar has been triggered because 3 bars closed under low of previous 'trigger bar' (TB )

The high and low of this new TB will act as triggers

(aqua blue lines, seen in image above)

Then there are 2 options:

- again 3 bars closes under the latest TB , in that case the TB moves to that new LL.

- 3 bars closes higher than the high of previous TB

The high and low of this new TB act again as trigger

If a new TB LL/HH is found, the script checks previous LL/HH

and searches the highest/lowest point in between.

If necessary, the temporary highest/lowest will be adjusted:

Another example:

The last 2 points can change (repaint).

Yellow coloured lines/labels are set and won't change anymore.

Concluded:

In case of these settings:

source for level breach -> close

X breaches -> 3

once a new TB is found, the high and low act as trigger lines

- when 3 bars closes under that low , a new LL is found, this will be the new TB

- when 3 bars closes above that high , a new HH is found, this will be the new TB

and so on...

Settings:

source for level breach -> close or high/low - H/L

X breaches -> 1 -> 10

line style -> solid, dotted, dashed

show level breaches -> new found TB (blue/lime coloured)

show Support/Resistance (lines at the right)

repaint warning can be removed

show labels / lines

This ZZ can be used for Harmonic patterns, Trend evaluation, support/resistance,...

In this script, I also used new features

- text_font_family = font.family_monospace -> link

- display=display.pane -> link

Cheers!

Black Scholes Option Pricing Model w/ Greeks [Loxx]The Black Scholes Merton model

If you are new to options I strongly advise you to profit from Robert Shiller's lecture on same . It combines practical market insights with a strong authoritative grasp of key models in option theory. He explains many of the areas covered below and in the following pages with a lot intuition and relatable anecdotage. We start here with Black Scholes Merton which is probably the most popular option pricing framework, due largely to its simplicity and ease in terms of implementation. The closed-form solution is efficient in terms of speed and always compares favorably relative to any numerical technique. The Black–Scholes–Merton model is a mathematical go-to model for estimating the value of European calls and puts. In the early 1970’s, Myron Scholes, and Fisher Black made an important breakthrough in the pricing of complex financial instruments. Robert Merton simultaneously was working on the same problem and applied the term Black-Scholes model to describe new generation of pricing. The Black Scholes (1973) contribution developed insights originally proposed by Bachelier 70 years before. In 1997, Myron Scholes and Robert Merton received the Nobel Prize for Economics. Tragically, Fisher Black died in 1995. The Black–Scholes formula presents a theoretical estimate (or model estimate) of the price of European-style options independently of the risk of the underlying security. Future payoffs from options can be discounted using the risk-neutral rate. Earlier academic work on options (e.g., Malkiel and Quandt 1968, 1969) had contemplated using either empirical, econometric analyses or elaborate theoretical models that possessed parameters whose values could not be calibrated directly. In contrast, Black, Scholes, and Merton’s parameters were at their core simple and did not involve references to utility or to the shifting risk appetite of investors. Below, we present a standard type formula, where: c = Call option value, p = Put option value, S=Current stock (or other underlying) price, K or X=Strike price, r=Risk-free interest rate, q = dividend yield, T=Time to maturity and N denotes taking the normal cumulative probability. b = (r - q) = cost of carry. (via VinegarHill-Financelab )

Things to know

This can only be used on the daily timeframe

You must select the option type and the greeks you wish to show

This indicator is a work in process, functions may be updated in the future. I will also be adding additional greeks as I code them or they become available in finance literature. This indictor contains 18 greeks. Many more will be added later.

Inputs

Spot price: select from 33 different types of price inputs

Calculation Steps: how many iterations to be used in the BS model. In practice, this number would be anywhere from 5000 to 15000, for our purposes here, this is limited to 300

Strike Price: the strike price of the option you're wishing to model

% Implied Volatility: here you can manually enter implied volatility

Historical Volatility Period: the input period for historical volatility ; historical volatility isn't used in the BS process, this is to serve as a sort of benchmark for the implied volatility ,

Historical Volatility Type: choose from various types of implied volatility , search my indicators for details on each of these

Option Base Currency: this is to calculate the risk-free rate, this is used if you wish to automatically calculate the risk-free rate instead of using the manual input. this uses the 10 year bold yield of the corresponding country

% Manual Risk-free Rate: here you can manually enter the risk-free rate

Use manual input for Risk-free Rate? : choose manual or automatic for risk-free rate

% Manual Yearly Dividend Yield: here you can manually enter the yearly dividend yield

Adjust for Dividends?: choose if you even want to use use dividends

Automatically Calculate Yearly Dividend Yield? choose if you want to use automatic vs manual dividend yield calculation

Time Now Type: choose how you want to calculate time right now, see the tool tip

Days in Year: choose how many days in the year, 365 for all days, 252 for trading days, etc

Hours Per Day: how many hours per day? 24, 8 working hours, or 6.5 trading hours

Expiry date settings: here you can specify the exact time the option expires

The Black Scholes Greeks

The Option Greek formulae express the change in the option price with respect to a parameter change taking as fixed all the other inputs. ( Haug explores multiple parameter changes at once .) One significant use of Greek measures is to calibrate risk exposure. A market-making financial institution with a portfolio of options, for instance, would want a snap shot of its exposure to asset price, interest rates, dividend fluctuations. It would try to establish impacts of volatility and time decay. In the formulae below, the Greeks merely evaluate change to only one input at a time. In reality, we might expect a conflagration of changes in interest rates and stock prices etc. (via VigengarHill-Financelab )

First-order Greeks

Delta: Delta measures the rate of change of the theoretical option value with respect to changes in the underlying asset's price. Delta is the first derivative of the value

Vega: Vegameasures sensitivity to volatility. Vega is the derivative of the option value with respect to the volatility of the underlying asset.

Theta: Theta measures the sensitivity of the value of the derivative to the passage of time (see Option time value): the "time decay."

Rho: Rho measures sensitivity to the interest rate: it is the derivative of the option value with respect to the risk free interest rate (for the relevant outstanding term).

Lambda: Lambda, Omega, or elasticity is the percentage change in option value per percentage change in the underlying price, a measure of leverage, sometimes called gearing.

Epsilon: Epsilon, also known as psi, is the percentage change in option value per percentage change in the underlying dividend yield, a measure of the dividend risk. The dividend yield impact is in practice determined using a 10% increase in those yields. Obviously, this sensitivity can only be applied to derivative instruments of equity products.

Second-order Greeks

Gamma: Measures the rate of change in the delta with respect to changes in the underlying price. Gamma is the second derivative of the value function with respect to the underlying price.

Vanna: Vanna, also referred to as DvegaDspot and DdeltaDvol, is a second order derivative of the option value, once to the underlying spot price and once to volatility. It is mathematically equivalent to DdeltaDvol, the sensitivity of the option delta with respect to change in volatility; or alternatively, the partial of vega with respect to the underlying instrument's price. Vanna can be a useful sensitivity to monitor when maintaining a delta- or vega-hedged portfolio as vanna will help the trader to anticipate changes to the effectiveness of a delta-hedge as volatility changes or the effectiveness of a vega-hedge against change in the underlying spot price.

Charm: Charm or delta decay measures the instantaneous rate of change of delta over the passage of time.

Vomma: Vomma, volga, vega convexity, or DvegaDvol measures second order sensitivity to volatility. Vomma is the second derivative of the option value with respect to the volatility, or, stated another way, vomma measures the rate of change to vega as volatility changes.

Veta: Veta or DvegaDtime measures the rate of change in the vega with respect to the passage of time. Veta is the second derivative of the value function; once to volatility and once to time.

Vera: Vera (sometimes rhova) measures the rate of change in rho with respect to volatility. Vera is the second derivative of the value function; once to volatility and once to interest rate.

Third-order Greeks

Speed: Speed measures the rate of change in Gamma with respect to changes in the underlying price.

Zomma: Zomma measures the rate of change of gamma with respect to changes in volatility.

Color: Color, gamma decay or DgammaDtime measures the rate of change of gamma over the passage of time.

Ultima: Ultima measures the sensitivity of the option vomma with respect to change in volatility.

Dual Delta: Dual Delta determines how the option price changes in relation to the change in the option strike price; it is the first derivative of the option price relative to the option strike price

Dual Gamma: Dual Gamma determines by how much the coefficient will changedual delta when the option strike price changes; it is the second derivative of the option price relative to the option strike price.

Related Indicators

Cox-Ross-Rubinstein Binomial Tree Options Pricing Model

Implied Volatility Estimator using Black Scholes

Boyle Trinomial Options Pricing Model

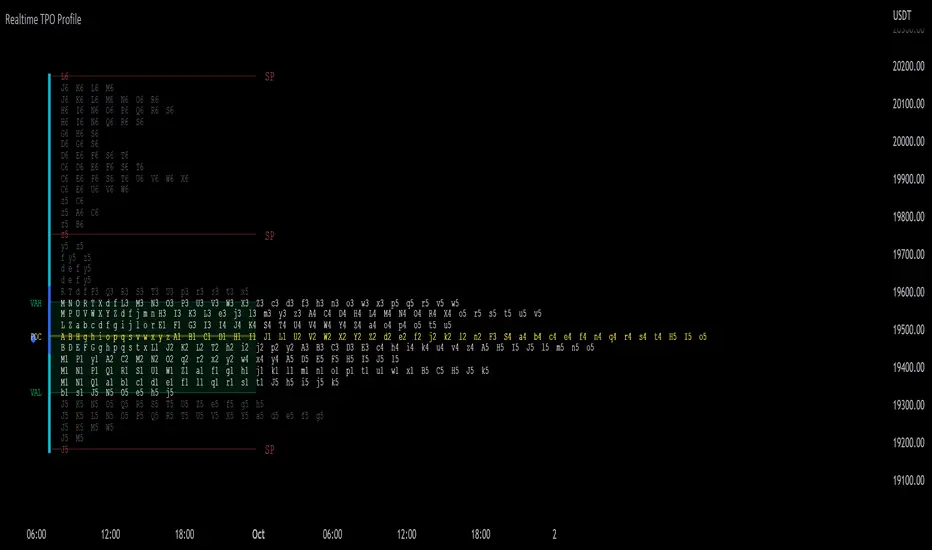

TPO Market Profile [Kioseff Trading]REPOST; SCRIPT WORKS!!

Due to technical error, this script was republished! Thank you for your support (:

Hello!

This indicator comprises a real time TPO Market Profile!

The script works on any timeframe 1 second or greater - the script calculates relative to the timeframe selected for your chart.

The image above shows the 1-minute BTCUSD chart; 650 +/- tick levels are set.

To see the script in full functionality - try using bar replay on a cryptocurrency 1-minute chart (start at the beginning of a regular hours session). Be sure to adjust the tick spread if necessary (:

So far, the script's held up in real time - I've not had any array loop errors or timeouts. The TPO profile updates accordingly with changes in time / high and low prices. Letters are appended to the profile in real time.

The image above shows configurations for the indicator. I plan to update the indicator quite a bit over the coming days - more to come.

You can select the timeframe change the indicator accounts for. For instance, you can have set the indicator to reset every day, every 30 minutes, every 5 minutes, every week, month, etc.

In the image above, I configured the indicator to recalculate every 3 months. Consequently, the indicator will record a TPO profile for three consecutive, reset, then record a TPO profile for the next 3 months. This setting makes the indicator compatible with any timeframe greater than 1 minute.

You can also use a drag & drop time-start bar to modify the starting point for the market profile TPO calculation.

The indicator hosts an option to auto calculate the tick spread between levels. However, as you switch timeframes and assets, sometimes, you'll have to manually set the tick range (:

Thanks for checking it out; more to come!

Sep 4

Release Notes: UPDATE: The indicator can work on seconds-based charts.

The image above shows the indicator working on the 1-second chart.

(Screenshot is old; characters are now numbered instead of strange unicode)

Release Notes: Added value area + vah + val. Font update. Changed characters to numbered once the alphabet is exhausted. POC, VAH, and VAL label located left of the first bar of the interval. Initial balance range can be toggled. Spaced the characters (more legible). Quite a bit of aesthetic changes so check it out!

Soon, I'll release a version of the script that shows VAH, POC, VAL, and TPO letters from previous sessions. I coded this feature into this indicator; however, it was removed due to load time complications. This feature will be its own script (:

If the script has trouble loading please let me know (:

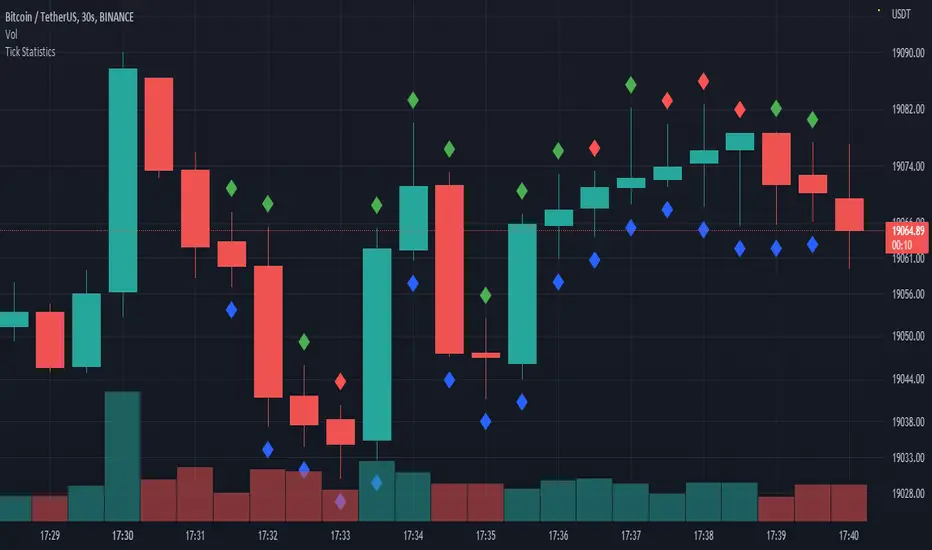

Tick StatisticsTick Statistics:

I have seen many questions/queries related to tick data in TV telegram channels. This script will help pine scripts to understand how ticks work, how to capture and process tick data.

This is an educational indicator script for pine scripters.

The indicator shall work only on real time candles. Tick data capture is initiated as soon as indicator is loaded on the chart. You might not get correct statistics on 1st candle in case indicator is loaded when real time candle is in progress, in such case you can monitor the statistics generated for subsequent candles.

Generated statistics is shown on the chart by placing 2 diamond shapes above and below the candle.

Diamond shape below the candle will have candles ‘tick data’ listed in a table. This can be view by placing mouse pointer on the diamond shape. Refer to point 1 below for more details.

Diamond shape above the candle will have statistics as mentioned in point no 2 onwards. To view the statistics place the mouse point on the diamond shape. The shape will appear in green color when both tick price and tick volume are both moving in the same direction. The diamond shape in red color means tick price and tick volume are moving in opposite direction.

The script captures tick by tick data and generate statistics below:

1. List of tick data with details below: (this is stored in the diamond shape placed below the candle)

a. Tick no

b. Tick type – Up tick (Up), Down tick (Dn), No change (--)

c. Tick price

d. Volume

e. Price difference (as compared to previous tick price)

f. Volume difference (as compared to previous tick volume)

2. Tick statistics

a. Total ticks

b. Number of up ticks

c. Number of down ticks

d. Number of No change ticks

3. Volume Statistics

a. Total volume

b. Up tick volume

c. Down tick volume

d. Volume associated with ticks where there is no change

e. Candle volume (just for reconciliation purpose)

4. Max-min statistics

a. Max volume = <> at price = <> at tick no = <>

b. Min volume = <> at price = <> at tick no = <>

c. Max price = <> at volume = <> at tick no = <>

d. Min price = <> at volume = <> at tick no = <>

5. Candle summary

a. Price << Up >> (if price is up as compared to 1st tick <> otherwise

b. Volume <> (if up tick volume is more than down tick volume <> otherwise

Strength of Divergence Across Multiple IndicatorsOverview:

One-stop shop for all your divergence needs, including:

(1) A single metric for divergence strength across multiple indicators.

(2) Labels that make it easy to spot where the truly strong divergence is by showing the overall divergence strength value along with the number of divergent indicators. Hovering over the label shows a breakdown of each divergent indicator and its individual divergence strength value.

(3) Fully customizable, including inputs for pivot lengths, divergence types, and weights for every component of the divergence strength calculation. This allows you to quickly and easily optimize the output for any chart. Don't worry, the default settings will have you covered if you're not interested in what's going on under the hood.

The Divergence Strength Calculation:

The total divergence strength value is the sum of the divergence strengths of all indicators for which divergence was detected at a given bar. Each indicator's individual divergence strength is comprised of two basic components: (1) |ΔPrice| - the magnitude of the change in price over the divergence period (pivot-to-pivot), and (2) |ΔIndicator| - the magnitude of the change in indicator value over the divergence period.

Because different indicators' scales and volatility can vary greatly, the Δ values are expressed in terms of standard deviation to ensure that the values are meaningful and equitable across all indicators and assets/instruments/currency pairs, etc:

|ΔIndicator| = |indicator_value_1 - indicator_value_2| / 2 * StDev(indicator_series,100)

Calculation Weights:

All components of the calculation are weighted and can be modified on the Inputs page in settings (weights are simply multipliers). For example, if you think hidden divergence should carry less weight than regular divergence, you can assign it a lesser weight. Or if you think RSI divergence is worth more than OBV divergence, you can adjust their weights accordingly. List of weights:

Regular divergence weight - default = 1

Hidden divergence weight - default = 1

ΔPrice weight - default = 0.5 (multiplied by the ΔPrice component)

ΔIndicator weight - default = 1.5 (multiplied by the ΔIndicator component)

RSI weight - default = 1.1

OBV weight - default = 0.8

MACD weight - default = 0.9

STOCH weight - default = 0.9

Development for additional indicators is ongoing, as is research into the optimal weight configuration(s).

Other Inputs:

Pivot lengths - specify the number of bars before and after each pivot high/low to consider it a valid candidate for divergence.

Lookback bars and Lookback pivots - specify the number of bars or the number of pivots to look back across.

Price sources - specify separate price sources for bullish and bearish divergence

Display settings - specify how lines and labels should display, including which divergence strength values should show the largest labels. Include/exclude specific divergence types and indicators.

Please report any bugs, or let me know if you have any enhancement suggestions or requests for additional indicators.

@reees

RSI Past Can Turn RSI Into a Directional ToolThe Relative Strength Index was created by J. Welles Wilder to measure overbought and oversold conditions. It’s also found popularity as an overall measure of direction because upward-trending stocks often hit overbought conditions. The opposite can be true with underperformers.

Today’s custom script, RSI Past, attempts to capture this secondary use of RSI as a directional indicator.

RSI Past achieves this by comparing how many bars have passed since RSI's most recent overbought and oversold readings. It then plots a simple difference between those two numbers.

Stocks with “bullish” signals will have positive readings that will increase each time RSI hits an overbought condition.

“Bearish” readings are just the opposite, growing more negative as oversold conditions occur.

An examination of some individual stocks may show the usefulness of this approach.

Meta Platforms , for example, hit an oversold condition almost exactly one year ago, and has remained under heavy selling pressure since:

Exxon Mobil , on the other hand, flipped to a bullish reading last October and has trended higher since:

This raises some interesting questions for Apple, shown on the main chart above. AAPL’s RSI Past has maintained a bullish reading for over a year -- unlike most other big technology stocks and the broader Nasdaq-100. Could this reflect bigger directional strength, especially with prices holding the $150 level that’s had relevance several times mid-2021?

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options, futures and cryptocurrencies. See our Overview for more.

Important Information

TradeStation Securities, Inc., TradeStation Crypto, Inc., and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., all operating, and providing products and services, under the TradeStation brand and trademark. You Can Trade, Inc. is also a wholly owned subsidiary of TradeStation Group, Inc., operating under its own brand and trademarks. TradeStation Crypto, Inc. offers to self-directed investors and traders cryptocurrency brokerage services. It is neither licensed with the SEC or the CFTC nor is it a Member of NFA. When applying for, or purchasing, accounts, subscriptions, products, and services, it is important that you know which company you will be dealing with. Please click here for further important information explaining what this means.

This content is for informational and educational purposes only. This is not a recommendation regarding any investment or investment strategy. Any opinions expressed herein are those of the author and do not represent the views or opinions of TradeStation or any of its affiliates.

Investing involves risks. Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options, futures, or digital assets); therefore, you should not invest or risk money that you cannot afford to lose. Before trading any asset class, first read the relevant risk disclosure statements on the Important Documents page, found here: www.tradestation.com .

ABC 123 Harmonic Ratio Custom Range Interactive█ OVERVIEW

This indicator was designed based on Harmonic Trading : Volume One written by Scott Carney.

This is about harmonic ratios which expanded through retracement and projection.

Derivation is pretty much explained here such as Primary, Primary Derivation, Secondary Derivation and Secondary Derivation Extreme.

Derivation value depends on minimum retracement or maximum projection.

This derivation value utilize Fibonacci value which later expand to Harmonic Ratio.

█ INSPIRATION

Inspired by design, code and usage of CAGR . Basic usage of custom range / interactive, pretty much explained here . Credits to TradingView.

This build is based and visualized upon Harmonic Trading Ratios.

This build also was stripped down from XABCD Harmonic Pattern Custom Range Interactive .

█ CREDITS

Scott Carney, Harmonic Trading : Volume One (Page 18)

█ FEATURES

Table can positioned by any position and font size can be resized.

Labels can be either changed to alphabets or numbers.

█ HOW TO USE

Draw points from Point A to Point C.

Dont worry about magnet, point will attached depends on High or Low of the candle.

█ USAGE / TIPS EXAMPLES (Description explained in each image)

Machine Learning: kNN (New Approach)Description:

kNN is a very robust and simple method for data classification and prediction. It is very effective if the training data is large. However, it is distinguished by difficulty at determining its main parameter, K (a number of nearest neighbors), beforehand. The computation cost is also quite high because we need to compute distance of each instance to all training samples. Nevertheless, in algorithmic trading KNN is reported to perform on a par with such techniques as SVM and Random Forest. It is also widely used in the area of data science.

The input data is just a long series of prices over time without any particular features. The value to be predicted is just the next bar's price. The way that this problem is solved for both nearest neighbor techniques and for some other types of prediction algorithms is to create training records by taking, for instance, 10 consecutive prices and using the first 9 as predictor values and the 10th as the prediction value. Doing this way, given 100 data points in your time series you could create 10 different training records. It's possible to create even more training records than 10 by creating a new record starting at every data point. For instance, you could take the first 10 data points and create a record. Then you could take the 10 consecutive data points starting at the second data point, the 10 consecutive data points starting at the third data point, etc.

By default, shown are only 10 initial data points as predictor values and the 6th as the prediction value.

Here is a step-by-step workthrough on how to compute K nearest neighbors (KNN) algorithm for quantitative data:

1. Determine parameter K = number of nearest neighbors.

2. Calculate the distance between the instance and all the training samples. As we are dealing with one-dimensional distance, we simply take absolute value from the instance to value of x (| x – v |).

3. Rank the distance and determine nearest neighbors based on the K'th minimum distance.

4. Gather the values of the nearest neighbors.

5. Use average of nearest neighbors as the prediction value of the instance.

The original logic of the algorithm was slightly modified, and as a result at approx. N=17 the resulting curve nicely approximates that of the sma(20). See the description below. Beside the sma-like MA this algorithm also gives you a hint on the direction of the next bar move.

Delta Volume Channels [LucF]█ OVERVIEW

This indicator displays on-chart visuals aimed at making the most of delta volume information. It can color bars and display two channels: one for delta volume, another calculated from the price levels of bars where delta volume divergences occur. Markers and alerts can also be configured using key conditions, and filtered in many different ways. The indicator caters to traders who prefer chart visuals over raw values. It will work on historical bars and in real time, using intrabar analysis to calculate delta volume in both conditions.

█ CONCEPTS

Delta Volume

The volume delta concept divides a bar's volume in "up" and "down" volumes. The delta is calculated by subtracting down volume from up volume. Many calculation techniques exist to isolate up and down volume within a bar. The simplest techniques use the polarity of interbar price changes to assign their volume to up or down slots, e.g., On Balance Volume or the Klinger Oscillator . Others such as Chaikin Money Flow use assumptions based on a bar's OHLC values. The most precise calculation method uses tick data and assigns the volume of each tick to the up or down slot depending on whether the transaction occurs at the bid or ask price. While this technique is ideal, it requires huge amounts of data on historical bars, which usually limits the historical depth of charts and the number of symbols for which tick data is available.

This indicator uses intrabar analysis to achieve a compromise between the simplest and most precise methods of calculating volume delta. In the context where historical tick data is not yet available on TradingView, intrabar analysis is the most precise technique to calculate volume delta on historical bars on our charts. TradingView's Volume Profile built-in indicators use it, as do the CVD - Cumulative Volume Delta Candles and CVD - Cumulative Volume Delta (Chart) indicators published from the TradingView account . My Volume Delta Columns Pro indicator also uses intrabar analysis. Other volume delta indicators such as my Realtime 5D Profile use realtime chart updates to achieve more precise volume delta calculations. Indicators of that type cannot be used on historical bars however; they only work in real time.

This is the logic I use to assign intrabar volume to up or down slots:

• If the intrabar's open and close values are different, their relative position is used.

• If the intrabar's open and close values are the same, the difference between the intrabar's close and the previous intrabar's close is used.

• As a last resort, when there is no movement during an intrabar and it closes at the same price as the previous intrabar, the last known polarity is used.

Once all intrabars making up a chart bar have been analyzed and the up or down property of each intrabar's volume determined, the up volumes are added and the down volumes subtracted. The resulting value is volume delta for that chart bar, which can be used as an estimate of the buying/selling pressure on an instrument.

Delta Volume Percent (DV%)

This value is the proportion that delta volume represents of the total intrabar volume in the chart bar. Note that on some symbols/timeframes, the total intrabar volume may differ from the chart's volume for a bar, but that will not affect our calculations since we use the total intrabar volume.

Delta Volume Channel

The DV channel is the space between two moving averages: the reference line and a DV%-weighted version of that reference. The reference line is a moving average of a type, source and length which you select. The DV%-weighted line uses the same settings, but it averages the DV%-weighted price source.

The weight applied to the source of the reference line is calculated from two values, which are multiplied: DV% and the relative size of the bar's volume in relation to previous bars. The effect of this is that DV% values on bars with higher total volume will carry greater weight than those with lesser volume.

The DV channel can be in one of four states, each having its corresponding color:

• Bull (teal): The DV%-weighted line is above the reference line.

• Strong bull (lime): The bull condition is fulfilled and the bar's close is above the reference line and both the reference and the DV%-weighted lines are rising.

• Bear (maroon): The DV%-weighted line is below the reference line.

• Strong bear (pink): The bear condition is fulfilled and the bar's close is below the reference line and both the reference and the DV%-weighted lines are falling.

Divergences

In the context of this indicator, a divergence is any bar where the slope of the reference line does not match that of the DV%-weighted line. No directional bias is assigned to divergences when they occur.

Divergence Channel

The divergence channel is the space between two levels (by default, the bar's low and high ) saved when divergences occur. When price has breached a channel and a new divergence occurs, a new channel is created. Until that new channel is breached, bars where additional divergences occur will expand the channel's levels if the bar's price points are outside the channel.

Prices breaches of the divergence channel will change its state. Divergence channels can be in one of five different states:

• Bull (teal): Price has breached the channel to the upside.

• Strong bull (lime): The bull condition is fulfilled and the DV channel is in the strong bull state.

• Bear (maroon): Price has breached the channel to the downside.

• Strong bear (pink): The bear condition is fulfilled and the DV channel is in the strong bear state.

• Neutral (gray): The channel has not been breached.

█ HOW TO USE THE INDICATOR

Load the indicator on an active chart (see here if you don't know how).

The default configuration displays:

• The DV channel, without the reference or DV%-weighted lines.

• The Divergence channel, without its level lines.

• Bar colors using the state of the DV channel.

The default settings use an Arnaud-Legoux moving average on the close and a length of 20 bars. The DV%-weighted version of it uses a combination of DV% and relative volume to calculate the ultimate weight applied to the reference. The DV%-weighted line is capped to 5 standard deviations of the reference. The lower timeframe used to access intrabars automatically adjusts to the chart's timeframe and achieves optimal balance between the number of intrabars inspected in each chart bar, and the number of chart bars covered by the script's calculations.

The Divergence channel's levels are determined using the high and low of the bars where divergences occur. Breaches of the channel require a bar's low to move above the top of the channel, and the bar's high to move below the channel's bottom.

No markers appear on the chart; if you want to create alerts from this script, you will need first to define the conditions that will trigger the markers, then create the alert, which will trigger on those same conditions.

To learn more about how to use this indicator, you must understand the concepts it uses and the information it displays, which requires reading this description. There are no videos to explain it.

█ FEATURES

The script's inputs are divided in four sections: "DV channel", "Divergence channel", "Other Visuals" and "Marker/Alert Conditions". The first setting is the selection method used to determine the intrabar precision, i.e., how many lower timeframe bars (intrabars) are examined in each chart bar. The more intrabars you analyze, the more precise the calculation of DV% results will be, but the less chart coverage can be covered by the script's calculations.

DV Channel

Here, you control the visibility and colors of the reference line, its weighted version, and the DV channel between them.

You also specify what type of moving average you want to use as a reference line, its source and length. This acts as the DV channel's baseline. The DV%-weighted line is also a moving average of the same type and length as the reference line, except that it will be calculated from the DV%-weighted source used in the reference line. By default, the DV%-weighted line is capped to five standard deviations of the reference line. You can change that value here. This section is also where you can disable the relative volume component of the weight.

Divergence Channel

This is where you control the appearance of the divergence channel and the key price values used in determining the channel's levels and breaching conditions. These choices have an impact on the behavior of the channel. More generous level prices like the default low and high selection will produce more conservative channels, as will the default choice for breach prices.

In this section, you can also enable a mode where an attempt is made to estimate the channel's bias before price breaches the channel. When it is enabled, successive increases/decreases of the channel's top and bottom levels are counted as new divergences occur. When one count is greater than the other, a bull/bear bias is inferred from it.

Other Visuals

You specify here:

• The method used to color chart bars, if you choose to do so.

• The display of a mark appearing above or below bars when a divergence occurs.

• If you want raw values to appear in tooltips when you hover above chart bars. The default setting does not display them, which makes the script faster.

• If you want to display an information box which by default appears in the lower left of the chart.

It shows which lower timeframe is used for intrabars, and the average number of intrabars per chart bar.

Marker/Alert Conditions

Here, you specify the conditions that will trigger up or down markers. The trigger conditions can include a combination of state transitions of the DV and the divergence channels. The triggering conditions can be filtered using a variety of conditions.

Configuring the marker conditions is necessary before creating an alert from this script, as the alert will use the marker conditions to trigger.

Markers only appear on bar closes, so they will not repaint. Keep in mind, when looking at markers on historical bars, that they are positioned on the bar when it closes — NOT when it opens.

Raw values

The raw values calculated by this script can be inspected using a tooltip and the Data Window. The tooltip is visible when you hover over the top of chart bars. It will display on the last 500 bars of the chart, and shows the values of DV, DV%, the combined weight, and the intermediary values used to calculate them.

█ INTERPRETATION

The aim of the DV channel is to provide a visual representation of the buying/selling pressure calculated using delta volume. The simplest characteristic of the channel is its bull/bear state. One can then distinguish between its bull and strong bull states, as transitions from strong bull to bull states will generally happen when buyers are losing steam. While one should not infer a reversal from such transitions, they can be a good place to tighten stops. Only time will tell if a reversal will occur. One or more divergences will often occur before reversals.

The nature of the divergence channel's design makes it particularly adept at identifying consolidation areas if its settings are kept on the conservative side. A gray divergence channel should usually be considered a no-trade zone. More adventurous traders can use the DV channel to orient their trade entries if they accept the risk of trading in a neutral divergence channel, which by definition will not have been breached by price.

If your charts are already busy with other stuff you want to hold on to, you could consider using only the chart bar coloring component of this indicator:

At its simplest, one way to use this indicator would be to look for overlaps of the strong bull/bear colors in both the DV channel and a divergence channel, as these identify points where price is breaching the divergence channel when buy/sell pressure is consistent with the direction of the breach. I have highlighted all those points in the chart below. Not all of them would have produced profitable trades, but nothing is perfect in the markets. Also, keep in mind that the circles identify the visual you would be looking for — not the trade's entry level.

█ LIMITATIONS

• The script will not work on symbols where no volume is available. An error will appear when that is the case.

• Because a maximum of 100K intrabars can be analyzed by a script, a compromise is necessary between the number of intrabars analyzed per chart bar

and chart coverage. The more intrabars you analyze per chart bar, the less coverage you will obtain.

The setting of the "Intrabar precision" field in the "DV channel" section of the script's inputs

is where you control how the lower timeframe is calculated from the chart's timeframe.

█ NOTES

Volume Quality

If you use volume, it's important to understand its nature and quality, as it varies with sectors and instruments. My Volume X-ray indicator is one way you can appraise the quality of an instrument's intraday volume.

For Pine Script™ Coders

• This script uses the new overload of the fill() function which now makes it possible to do vertical gradients in Pine. I use it for both channels displayed by this script.

• I use the new arguments for plot() 's `display` parameter to control where the script plots some of its values,

namely those I only want to appear in the script's status line and in the Data Window.

• I wrote my script using the revised recommendations in the Style Guide from the Pine v5 User Manual.

█ THANKS

To PineCoders . I have used their lower_tf library in this script, to manage the calculation of the LTF and intrabar stats, and their Time library to convert a timeframe in seconds to a printable form for its display in the Information box.

To TradingView's Pine Script™ team. Their innovations and improvements, big and small, constantly expand the boundaries of the language. What this script does would not have been possible just a few months back.

And finally, thanks to all the users of my scripts who take the time to comment on my publications and suggest improvements. I do not reply to all but I do read your comments and do my best to implement your suggestions with the limited time that I have.

HSV and HSL gradient Tools ( Built-in Drop-in replacement )Library "hsvColor"

HSV and HSL Gradient Tool Alternatives and helpers. Demo'd is built-in in the middle with HSL/HSV gradients on top/bottom

TODO: Solve for #000000 issue

rgbhsv(_col)

RGB Color to HSV Values

Parameters:

_col : Color input (#abc012 or color.name or color.rgb(0,0,0,0))

Returns: values

rgbhsv(_r, _g, _b, _t)

RGB Color to HSV Values

Parameters:

_r : Red 0 - 255

_g : Green 0 - 255

_b : Blue 0 - 255

_t : Transp 0 - 100

Returns: values

hsv(_h, _s, _v, _a)

HSV colors, Auto fix if past boundaries

Parameters:

_h : Hue Input (-360 - 360) or further

_s : Saturation 0.- 1.

_v : Value 0.- 1.

_a : Alpha 0.- 1.

Returns: Color output

hue(_col)

returns 0-359 hue on color wheel

Parameters:

_col :

Returns: 360 degree hue value

hsv_gradient(signal, _startVal, _endVal, _startCol, _endCol)

Color Gradient Replacement Function for HSV calculated Gradents

Parameters:

signal : Control signal

_startVal : start color limit

_endVal : end color limit

_startCol : start color

_endCol : end color

Returns: HSV calculated gradient

hsl_gradient(signal, _startVal, _endVal, _startCol, _endCol)

Color Gradient Replacement Function for HSV calculated Gradents

Parameters:

signal : Control signal

_startVal : start color limit

_endVal : end color limit

_startCol : start color

_endCol : end color

Returns: HSV calculated gradient

STD-Filtered, N-Pole Gaussian Filter [Loxx]This is a Gaussian Filter with Standard Deviation Filtering that works for orders (poles) higher than the usual 4 poles that was originally available in Ehlers Gaussian Filter formulas. Because of that, it is a sort of generalized Gaussian filter that can calculate arbitrary (order) pole Gaussian Filter and which makes it a sort of a unique indicator. For this implementation, the practical mathematical maximum is 15 poles after which the precision of calculation is useless--the coefficients for levels above 15 poles are so high that the precision loss actually means very little. Despite this maximal precision utility, I've left the upper bound of poles open-ended so you can try poles of order 15 and above yourself. The default is set to 5 poles which is 1 pole greater than the normal maximum of 4 poles.

The purpose of the standard deviation filter is to filter out noise by and by default it will filter 1 standard deviation. Adjust this number and the filter selections (price, both, GMA, none) to reduce the signal noise.

What is Ehlers Gaussian filter?

This filter can be used for smoothing. It rejects high frequencies (fast movements) better than an EMA and has lower lag. published by John F. Ehlers in "Rocket Science For Traders".

A Gaussian filter is one whose transfer response is described by the familiar Gaussian bell-shaped curve. In the case of low-pass filters, only the upper half of the curve describes the filter. The use of gaussian filters is a move toward achieving the dual goal of reducing lag and reducing the lag of high-frequency components relative to the lag of lower-frequency components.

A gaussian filter with...

One Pole: f = alpha*g + (1-alpha)f

Two Poles: f = alpha*2g + 2(1-alpha)f - (1-alpha)2f

Three Poles: f = alpha*3g + 3(1-alpha)f - 3(1-alpha)2f + (1-alpha)3f

Four Poles: f = alpha*4g + 4(1-alpha)f - 6(1-alpha)2f + 4(1-alpha)3f - (1-alpha)4f

and so on...

For an equivalent number of poles the lag of a Gaussian is about half the lag of a Butterworth filters: Lag = N*P / pi^2, where,

N is the number of poles, and

P is the critical period

Special initialization of filter stages ensures proper working in scans with as few bars as possible.

From Ehlers Book: "The first objective of using smoothers is to eliminate or reduce the undesired high-frequency components in the eprice data. Therefore these smoothers are called low-pass filters, and they all work by some form of averaging. Butterworth low-pass filters can do this job, but nothing comes for free. A higher degree of filtering is necessarily accompanied by a larger amount of lag. We have come to see that is a fact of life."

References John F. Ehlers: "Rocket Science For Traders, Digital Signal Processing Applications", Chapter 15: "Infinite Impulse Response Filters"

Included

Loxx's Expanded Source Types

Signals

Alerts

Bar coloring

Related indicators

STD-Filtered, Gaussian Moving Average (GMA)

STD-Filtered, Gaussian-Kernel-Weighted Moving Average

One-Sided Gaussian Filter w/ Channels

Fisher Transform w/ Dynamic Zones

R-sqrd Adapt. Fisher Transform w/ D. Zones & Divs .

Portfolio PerformanceThis indicators will help you to compute portfolio performance and display results with a stats table and a nice monthly chart.

In this script you can do following:

Compose portfolio with up to 15 instruments

Change Initial capital / date range / rebalancing period

Compare portfolio performance with a benchmark

Compute basic stats

Compute instruments contribution

Display monthly performance of portfolio and benchmark

Change style for almost everything you see on your chart

Hope it will be useful for you!

Thanks to @MUQWISHI for helping me coding it.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Weighted percentile nearest rankYo, posting it for the whole internet, took the whole day to find / to design the actual working solution for weighted percentile 'nearest rank' algorithm, almost no reliable info online and a lot of library-style/textbook-style solutions that don't provide on real world production level.

The principle:

0) initial data

data = 22, 33, 11, 44, 55

weights = 5 , 3 , 2 , 1 , 4

array(s) size = 5

1) sort data array, apply the sorting pattern to the weights array, resulting:

data = 11, 22, 33, 44, 55

weights = 2 , 5 , 3 , 1 , 4

2) get weights cumsum and sum:

weights = 2, 5, 3 , 1 , 4

weights_cum = 2, 7, 10, 11, 15

weights_sum = 15

3) say we wanna find 50th percentile, get a threshold value:

n = 50

thres = weights_sum / 100 * n

7.5 = 15 / 100 * 50

4) iterate through weights_cum until you find a value that >= the threshold:

for i = 0 to size - 1

2 >= 7.5 ? nah

7 >= 7.5 ? nah

10 >= 7.5 ? aye

5) take the iteration index that resulted "aye", and find the data value with the same index, that's gonna be the resulting percentile.

i = 2

data = 33

This one is not an approximation, not an estimator, it's the actual weighted percentile nearest rank as it is.

I tested the thing extensively and it works perfectly.

For the skeptics, check lines 40, 41, 69 in the code, you can comment/uncomment dem to switch for unit (1) weights, resulting in the usual non-weighted percentile nearest rank that ideally matches the TV's built-in function.

Shoutout for @wallneradam for the sorting function mane

...

Live Long and Prosper

(Quartile Vol.; Vol. Aggregation; Range US Bars; Gaps) [Kioseff]Hello!

This indicator is a multifaceted tool that's, hopefully, useful for price action and volume analysis.

(This script makes use of the newly introduced "text_font" parameter)

With this script you'll have access to:

Range US Chart

Volume Aggregation Chart

Gaps Chart

Volume by Quartile

Consequently, you'll have access to:

First Quartile Volume Threshold

Second Quartile Volume Threshold

Third Quartile Volume Threshold

90th Percentile Volume Threshold

Fourth Quartile Volume Threshold

Q2 - Q1 Dispersion

Q3 - Q2 Dispersion

Q4 - Q3 Dispersion

Quartile Deviation

Interquartile Range

Avg. "n" bar return following "high" volume

Avg. "n" bar positive return following "high" volume

Avg. "n" bar negative following "high" volume

# of Positive Returns Following a Gap

# of Negative Returns Following a Gap

# of Gaps

# of Up Gaps

# of Down Gaps

Average # of bars to fill Up Gaps

Average # of bars to dill Down Gaps

Average Gap Up % increase

Average Gap Down % decrease

Cumulative % increase of all Up Gaps

Cumulative % decrease of all Down Gaps

Sort gaps by distance from price

Hide gaps that price substantially deviates from (gaps will reappear when price trades near the gap)

Segment Range US bars by date

Manually configure Range US price thresholds

Identify "congestion" areas with Range US bars

Range US Levels that must be exceeded for a new Range US bar to produce

Manually configure cumulative volume threshold for Volume Aggregation bars

Segment Volume Aggregation bars by date

Largest Volume Aggregation bar increases

Largest Volume Aggregation bar decreases

Calculate log returns after "high" volume sessions

Quartile Volume

The Quartile Volume portion of the script segments price/volume intervals by quartile.

The image above shows features of the indicator.

For statistics, the following metrics are recorded:

First Quartile

Second Quartile

Third Quartile

90th Percentile

Fourth Quartile

Q2 - Q1 Dispersion

Q3 - Q2 Dispersion

Q4 - Q3 Dispersion

Quartile Deviation

Interquartile Range

Color-coordinated price bars (by volume quartiles)

The percent rank for the volume of the current bar

Avg. "n" bar return following "high" volume

Avg. "n" bar positive return following "high" volume

Avg. "n" bar negative following "high" volume

The script colors bars via gradient.

By default, bars are colored lime when volume for the interval is "high" (exceeds upper quartile thresholds). The greener the bar, the higher the volume for the interval.

Bars are colored red when volume for the interval is "low" (fails to exceed lower quartile thresholds). The redder the bar, the lower the volume for the interval.

Naturally, brownish-colored bars reflect a volume interval that concluded near the median.

The image above exemplifies the process. This feature might be useful to categorize / objectively define high-volume clusters, low-volume clusters, high-volume price moves, low-volume price moves, etc.

For greater precision, you can select to color bars by volume quartile they belong to.

The image above shows color-coordinated price bars. More details shown in the image.

Additionally, you can select to plot the quartile/percentile that a price bar belongs to on the chart.

The image above shows price bars numbered by the volume quartile they belong to.

The script will distinguish successive 90th percentile violations, superimpose a linear regression channel atop the data sequence, and record pertinent statistics.

The image above shows the process.

Lastly, the user can plot an anchored VWAP using a built-in time function.

The image above shows the anchored VWAP.

Range US Chart

A Range US chart operates irrespective of time and volume - simply - bars produce after a user-defined price move is achieved/exceeded in either direction. A range us chart produces “trend candles” and “reversal candles”. A reversal candle always moves against the most immediate bar; a trend candle always moves in favor of the most immediate bar. The user defines the dollar amount price must travel up/down for a trend candle to fulfill, and for a reversal candle to fulfill.

Note: if a “down reversal” candle (red) Is produced, it’s impossible for the next candle to also be a down reversal candle - for the downside move to continue the criteria for a down trend candle must be fulfilled. Similarly, if an “up reversal” candle (green) Is produced, it’s impossible for the next candle to also be an up reversal candle - for the upside move to continue, the criteria for an uptrend trend candle must be fulfilled. Consequently, Range US bars frequently trade at the same level for extended periods. This is intentional, as this chart type is theorized to “filter noise” (whether Range US charts fulfill this theory is to your discretion).

Lastly, if an up trend candle (green) is produced, the next candle cannot be up a reversal up candle - only a trend up candle or reversal down candle can produce - vice versa for a trend down candle (the subsequent candle cannot be a reversal down candle). In this sense, an uptrend continues on successive trend up candles; a down trend continues on successive trend down candles.

The image above exemplifies Range US chart functionality.

The lower-right stats table shows the requisite price move for a "Trend" candle to produce and for a "Reversal" candle to produce.

The default settings for this chart time automatically calculate the required "Trend" candle price move and the required "Reversal" candle price move. However, both settings are configurable.

The image above shows manually configured parameters for a trend bar and reversal bar to produce. This feature allows the user to replicate the Range US chart hosted on extrinsic charting platforms.

However, please consider that this script does not use tick data; 1-minute OHLC data is used for calculations.

Consequently, configuring the trend bar and reversal bar requirement too low may return inaccurate data. For instance, if you set trend candles to form after a $1 price move then trend candles will form if price moves up $1 from a green Range US bar or down $1 from a red Range US bar. This is sufficient for lower priced assets; however, if you were trading, for instance, Bitcoin - a $1 price move can happen numerous times in one minute. This script can’t plot bars and record data until a 1-minute bar closes and a new 1-minute bar opens. Further, if Bitcoin moves up $1 twenty times and down $1 twenty times in a 1-minute bar - your Range US chart will record such variations as one price move. This data is inaccurate and likely useless.

To counter this quandary, a warning message will appear if you configure trend bar price moves or reversal bar price moves too low.

The image above shows the concealable warning message.

The image above is a flow diagram (made with shaky hands) illustrating the Range US bar formation process.

A google search will return additional information on the Range US chart type.

Volume Aggregation Bars

TradingView user and member of the TradingView Discord server @ferreirajames informed me of the Volume Aggregation chart type. The user commented in the "Suggestions" channel for the TradingView Discord server asking for the Volume Aggregation chart type. As an interim fix, I tried my hand at recreating the process, which is available in this script.

Similar to the Range US chart type, Volume Aggregation bars aren’t bound to a time-axis; the bars form after a user-defined, cumulative amount of volume is achieved or exceeded. Consequently, once the cumulative amount of volume is achieved or exceeded - a bar is produced at the corresponding price level.

Underlying theory: The chat type is conducive to identifying price levels where traders are “trapped”. Whether the process adequately distinguishes this circumstance is to your discretion.

The image above exemplifies the Volume Aggregation chart type.