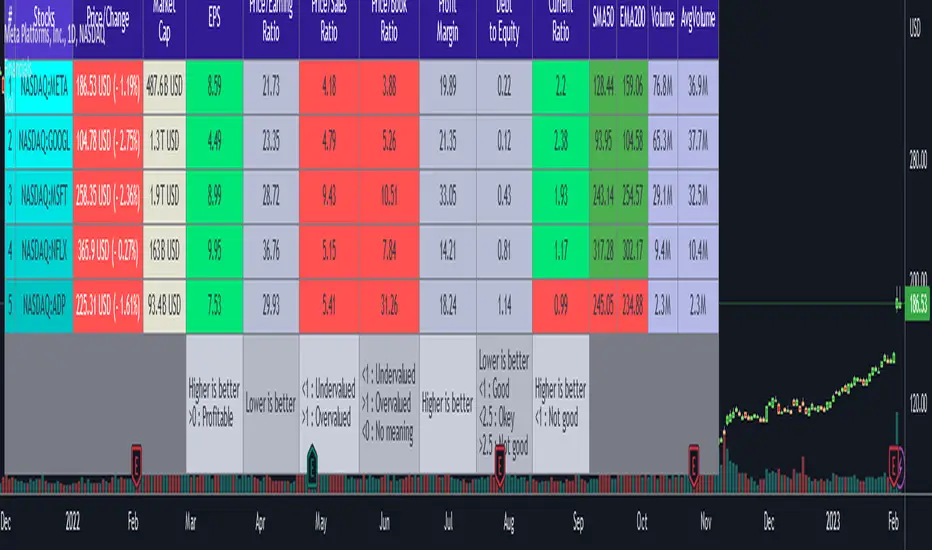

Financials - Comparing CompaniesHello All

For a while I have been working on this indicator to compare financials of the companies and sort them accordingly. Finally I completed and published it. I preferred using new object type feature in Pine language™ and I hope it might be an example and helpful for the developers.

First of all, as we have limitation on security calls, the indicator can get and compare financials for 5 companies only. also Chart time frame must be 1Day or higher! ( I recommend 1Day time frame ). if not then the indicator stops and shows the error message: "Please set the time frame 1Day or higher" . More important than others: You should choose the companies from the same sector! Compare apples to apples :)

The Financials in the indicator:

Earnings Per Share

Price to Earnings Ratio

Price to Sales Ratio

Price to Book Ratio

Profit Margin

Dept to Equity

Current Ratio

Market Capitalization

Also more information shown for each stocks:

Closing Price, sets the color accordingly

2 Simple/Exponential moving average, you can set the length, also it checks if it is rising/falling and sets the color accordingly

Volume info

Average volume (20 days), you can set the period

Currency for each security

Lets see some features in it:

it sorts the companies according to the financials:

If you move the mouse onto any header then it shows explanation about the financial:

You can change location and text size:

You can set the type of Moving averages as SMA or EMA and you can also set the length for both . Headers for both are changed automatically by MA type and length

Colors for Closing price and MA cells are set automatically:

For new Objects in Pine language click here

P.S. You can use this indicator while analyzing the financials of the companies in same sector/industry. So please don't ask for the alerts :)

Enjoy!

Индикаторы и стратегии

Golden PocketGolden Pocket

This marks up the fibonacci retracement levels of 0.65 and 0.618 by default, these levels are often referred to as the golden pocket.

They are known by this because when price has an impulse either to the up or downside, price will end up retracing at some point. This Golden pocket often lines up with other means of confluence where it's considered a good entry price from the retrace.

Unlike standard fib retracement indicators, these boxes will extend with current price until they are hit. As well as this, there is a moving average filter which you can set to higher timeframes meaning that you can choose to only look for golden pockets which are following the higher time frame trend. You can easily monitor all of your settings by setting up just 1 alert.

Settings

You have the option to enable/disable the line which marks out the pivot points the fib is being calculated from, you can also change the colour and style of the line.

Below this you have the option to choose what colour the fib boxes are and what colour they change to once price hits it. If you want them to disappear change the colours opacity to 0%.

If you want to change the golden pocket levels you can do that by changing the 0.618 or 0.65 levels in the settings.

The pivot distance controls what part defines a pivot high or low, it must be the highest/lowest to the left/right of the pivot candle count.

MA filter will only accept golden pockets which are trending with the Moving average.

You can change all the settings of the Moving average which acts as a filter including which timeframe it is calculated on.

Alerts

Simply toggle this on int the settings and then click on the 3 dots next to the indicators name, 'add alert', leave the top boxes as they are, you can name the alert anything you like but once you confirm this, it will monitor all golden pockets on the particular asset and timeframe you are looking at. The alerts are set up to trigger as soon as price touches one of the boxes.

Use Cases

We like setting are moving average up on the daily timeframe and using the Moving average filter so we know we are only trading with the higher timeframe trend. From there we can set up alerts on any lower timeframe.

Feel free to use any part of this script in your own code, please just give us a mention so we can check out your contributions to the community as well!

Happy to take in any suggestions or ways of improving

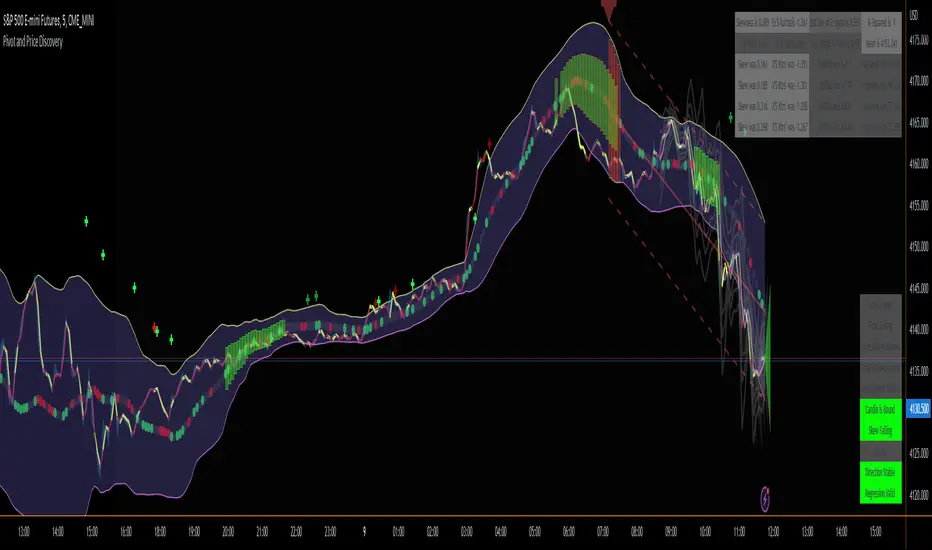

Pivot and Price DiscoveryA Population Sampled linear regression model that provides additional detail about the distribution moments (skew, kurtosis, variance and mean) as well as providing indicators that track when a pivot has enough momentum to trade on as well as expected ranges of future price action based on Std Devs.

For the momentum lines -- red indicates that there has been a reducing pivot with momentum, this continues as a grey line for continuation, and will be cancelled when an increasing pivot with momentum is encountered.

Forward looking trend triangle captures the +/- stated standard deviation from the latest bar_index over 2 periods. Movements that trace outside of this can be considered a precursor to an upcoming pivot, and by analyzing skewness and kurtosis, the probability of an upcoming pivot should be better understood.

I have really only looked at this for timescales greater than 5 minutes. Adjust the lookback length accordingly when moving to different timescales:

For example, 1 hr at 10m timescale will be a lookback length of 6 which is too low for accurate analysis, so keep the lookback length appropriate for the timescales being used.

Also realize that trade volume will skew the deviations and regression if you are including data outside of regular trading hours (futures are different, but also experience volume sensitivity -- I maylook into accounting for this in future versions.)

© TheGeeBee

Fair value bands / quantifytools— Overview

Fair value bands, like other band tools, depict dynamic points in price where price behaviour is normal or abnormal, i.e. trading at/around mean (price at fair value) or deviating from mean (price outside fair value). Unlike constantly readjusting standard deviation based bands, fair value bands are designed to be smooth and constant, based on typical historical deviations. The script calculates pivots that take place above/below fair value basis and forms median deviation bands based on this information. These points are then multiplied up to 3, representing more extreme deviations.

By default, the script uses OHLC4 and SMA 20 as basis for the bands. Users can form their preferred fair value basis using following options:

Price source

- Standard OHLC values

- HL2 (High + low / 2)

- OHLC4 (Open + high + low + close / 4)

- HLC3 (High + low + close / 3)

- HLCC4 (High + low + close + close / 4)

Smoothing

- SMA

- EMA

- HMA

- RMA

- WMA

- VWMA

- Median

Once fair value basis is established, some additional customization options can be employed:

Trend mode

Direction based

Cross based

Trend modes affect fair value basis color that indicates trend direction. Direction based trend considers only the direction of the defined fair value basis, i.e. pointing up is considered an uptrend, vice versa for downtrend. Cross based trends activate when selected source (same options as price source) crosses fair value basis. These sources can be set individually for uptrend/downtrend cross conditions. By default, the script uses cross based trend mode with low and high as sources.

Cross based (downtrend not triggered) vs. direction based (downtrend triggered):

Threshold band

Threshold band is calculated using typical deviations when price is trading at fair value basis. In other words, a little bit of "wiggle room" is added around the mean based on expected deviation. This feature is useful for cross based trends, as it allows filtering insignificant crosses that are more likely just noise. By default, threshold band is calculated based on 1x median deviation from mean. Users can increase/decrease threshold band width via input menu for more/less noise filtering, e.g. 2x threshold band width would require price to cross wiggle room that is 2x wider than typical, 0x erases threshold band altogether.

Deviation bands

Width of deviation bands by default is based on 1x median deviations and can be increased/decreased in a similar manner to threshold bands.

Each combination of customization options produces varying behaviour in the bands. To measure the behaviour and finding fairest representation of fair and unfair value, some data is gathered.

— Fair value metrics

Space between each band is considered a lot, named +3, +2, +1, -1, -2, -3. For each lot, time spent and volume relative to volume moving average (SMA 20) is recorded each time price is trading in a given lot:

Depending on the asset, timeframe and chosen fair value basis, shape of the distributions vary. However, practically always time is distributed in a normal bell curve shape, being highest at lots +1 to -1, gradually decreasing the further price is from the mean. This is hardly surprising, but it allows accurately determining dynamic areas of normal and abnormal price behaviour (i.e. low risk area between +1 and -1, high risk area between +-2 to +-3). Volume on the other hand is typically distributed the other way around, being lowest at lots +1 to -1 and highest at +-2 to +-3. When time and volume are distributed like so, we can conclude that 1) price being outside fair value is a rare event and 2) the more price is outside fair value, the more anomaly behaviour in volume we tend to find.

Viewing metric calculations

Metric calculation highlights can be enabled from the input menu, resulting in a lot based coloring and visibility of each lot counter (time, cumulative relative volume and average relative volume) in data window:

— Alerts

Available alerts are the following:

Individual

- High crossing deviation band (bands +1 to +3 )

- Low crossing deviation band (bands -1 to -3 )

- Low at threshold band in an uptrend

- High at threshold band in a downtrend

- New uptrend

- New downtrend

Grouped

- New uptrend or downtrend

- Deviation band cross (+1 or -1)

- Deviation band cross (+2 or -2)

- Deviation band cross (+3 or -3)

— Practical guide

Example #1 : Risk on/risk off trend following

Ideal trend stays inside fair value and provides sufficient cool offs between the moves. When this is the case, fair value bands can be used for sensible entry/exit levels within the trend.

Example #2 : Mean reversions

When price shows exuberance into an extreme deviation, followed by a stall and signs of exhaustion (wicks), an opportunity for mean reversion emerges. The higher the deviation, the more volatility in the move, the more signalling of exhaustion, the better.

Example #3 : Tweaking bands for desired behaviour

The faster the length of fair value basis, the more momentum price needs to hit extreme deviation levels, as bands too are moving faster alongside price. Decreasing fair value basis length typically leads to more quick and aggressive deviations and less steady trends outside fair value.

Motion▮ FEATURES

Now as library version :)

String-based transition-effects

Performance optimization. Reduced memory consumption up to >90% by kicking the output to the "stdout".

Use marquee- or loader-effect on any possible string location.

Example: UI Price-Ticker

----------------------------------------------------------------------------

Library "Motion"

_getStringMono(_len, _str, _sep)

Parameters:

_len

_str

_sep

marquee(this, _extern, _ws, _subLen, _subStart)

Parameters:

this

_extern

_ws

_subLen

_subStart

transition(this, _subLen, _subStart)

Parameters:

this

_subLen

_subStart

hold(this)

Parameters:

this

keyframe

keyframe A keyframe object.

Fields:

seq

intv

step

length

update_no

frame_no

ltr

hold

Machine Learning: Lorentzian Classification█ OVERVIEW

A Lorentzian Distance Classifier (LDC) is a Machine Learning classification algorithm capable of categorizing historical data from a multi-dimensional feature space. This indicator demonstrates how Lorentzian Classification can also be used to predict the direction of future price movements when used as the distance metric for a novel implementation of an Approximate Nearest Neighbors (ANN) algorithm.

█ BACKGROUND

In physics, Lorentzian space is perhaps best known for its role in describing the curvature of space-time in Einstein's theory of General Relativity (2). Interestingly, however, this abstract concept from theoretical physics also has tangible real-world applications in trading.

Recently, it was hypothesized that Lorentzian space was also well-suited for analyzing time-series data (4), (5). This hypothesis has been supported by several empirical studies that demonstrate that Lorentzian distance is more robust to outliers and noise than the more commonly used Euclidean distance (1), (3), (6). Furthermore, Lorentzian distance was also shown to outperform dozens of other highly regarded distance metrics, including Manhattan distance, Bhattacharyya similarity, and Cosine similarity (1), (3). Outside of Dynamic Time Warping based approaches, which are unfortunately too computationally intensive for PineScript at this time, the Lorentzian Distance metric consistently scores the highest mean accuracy over a wide variety of time series data sets (1).

Euclidean distance is commonly used as the default distance metric for NN-based search algorithms, but it may not always be the best choice when dealing with financial market data. This is because financial market data can be significantly impacted by proximity to major world events such as FOMC Meetings and Black Swan events. This event-based distortion of market data can be framed as similar to the gravitational warping caused by a massive object on the space-time continuum. For financial markets, the analogous continuum that experiences warping can be referred to as "price-time".

Below is a side-by-side comparison of how neighborhoods of similar historical points appear in three-dimensional Euclidean Space and Lorentzian Space:

This figure demonstrates how Lorentzian space can better accommodate the warping of price-time since the Lorentzian distance function compresses the Euclidean neighborhood in such a way that the new neighborhood distribution in Lorentzian space tends to cluster around each of the major feature axes in addition to the origin itself. This means that, even though some nearest neighbors will be the same regardless of the distance metric used, Lorentzian space will also allow for the consideration of historical points that would otherwise never be considered with a Euclidean distance metric.

Intuitively, the advantage inherent in the Lorentzian distance metric makes sense. For example, it is logical that the price action that occurs in the hours after Chairman Powell finishes delivering a speech would resemble at least some of the previous times when he finished delivering a speech. This may be true regardless of other factors, such as whether or not the market was overbought or oversold at the time or if the macro conditions were more bullish or bearish overall. These historical reference points are extremely valuable for predictive models, yet the Euclidean distance metric would miss these neighbors entirely, often in favor of irrelevant data points from the day before the event. By using Lorentzian distance as a metric, the ML model is instead able to consider the warping of price-time caused by the event and, ultimately, transcend the temporal bias imposed on it by the time series.

For more information on the implementation details of the Approximate Nearest Neighbors (ANN) algorithm used in this indicator, please refer to the detailed comments in the source code.

█ HOW TO USE

Below is an explanatory breakdown of the different parts of this indicator as it appears in the interface:

Below is an explanation of the different settings for this indicator:

General Settings:

Source - This has a default value of "hlc3" and is used to control the input data source.

Neighbors Count - This has a default value of 8, a minimum value of 1, a maximum value of 100, and a step of 1. It is used to control the number of neighbors to consider.

Max Bars Back - This has a default value of 2000.

Feature Count - This has a default value of 5, a minimum value of 2, and a maximum value of 5. It controls the number of features to use for ML predictions.

Color Compression - This has a default value of 1, a minimum value of 1, and a maximum value of 10. It is used to control the compression factor for adjusting the intensity of the color scale.

Show Exits - This has a default value of false. It controls whether to show the exit threshold on the chart.

Use Dynamic Exits - This has a default value of false. It is used to control whether to attempt to let profits ride by dynamically adjusting the exit threshold based on kernel regression.

Feature Engineering Settings:

Note: The Feature Engineering section is for fine-tuning the features used for ML predictions. The default values are optimized for the 4H to 12H timeframes for most charts, but they should also work reasonably well for other timeframes. By default, the model can support features that accept two parameters (Parameter A and Parameter B, respectively). Even though there are only 4 features provided by default, the same feature with different settings counts as two separate features. If the feature only accepts one parameter, then the second parameter will default to EMA-based smoothing with a default value of 1. These features represent the most effective combination I have encountered in my testing, but additional features may be added as additional options in the future.

Feature 1 - This has a default value of "RSI" and options are: "RSI", "WT", "CCI", "ADX".

Feature 2 - This has a default value of "WT" and options are: "RSI", "WT", "CCI", "ADX".

Feature 3 - This has a default value of "CCI" and options are: "RSI", "WT", "CCI", "ADX".

Feature 4 - This has a default value of "ADX" and options are: "RSI", "WT", "CCI", "ADX".

Feature 5 - This has a default value of "RSI" and options are: "RSI", "WT", "CCI", "ADX".

Filters Settings:

Use Volatility Filter - This has a default value of true. It is used to control whether to use the volatility filter.

Use Regime Filter - This has a default value of true. It is used to control whether to use the trend detection filter.

Use ADX Filter - This has a default value of false. It is used to control whether to use the ADX filter.

Regime Threshold - This has a default value of -0.1, a minimum value of -10, a maximum value of 10, and a step of 0.1. It is used to control the Regime Detection filter for detecting Trending/Ranging markets.

ADX Threshold - This has a default value of 20, a minimum value of 0, a maximum value of 100, and a step of 1. It is used to control the threshold for detecting Trending/Ranging markets.

Kernel Regression Settings:

Trade with Kernel - This has a default value of true. It is used to control whether to trade with the kernel.

Show Kernel Estimate - This has a default value of true. It is used to control whether to show the kernel estimate.

Lookback Window - This has a default value of 8 and a minimum value of 3. It is used to control the number of bars used for the estimation. Recommended range: 3-50

Relative Weighting - This has a default value of 8 and a step size of 0.25. It is used to control the relative weighting of time frames. Recommended range: 0.25-25

Start Regression at Bar - This has a default value of 25. It is used to control the bar index on which to start regression. Recommended range: 0-25

Display Settings:

Show Bar Colors - This has a default value of true. It is used to control whether to show the bar colors.

Show Bar Prediction Values - This has a default value of true. It controls whether to show the ML model's evaluation of each bar as an integer.

Use ATR Offset - This has a default value of false. It controls whether to use the ATR offset instead of the bar prediction offset.

Bar Prediction Offset - This has a default value of 0 and a minimum value of 0. It is used to control the offset of the bar predictions as a percentage from the bar high or close.

Backtesting Settings:

Show Backtest Results - This has a default value of true. It is used to control whether to display the win rate of the given configuration.

█ WORKS CITED

(1) R. Giusti and G. E. A. P. A. Batista, "An Empirical Comparison of Dissimilarity Measures for Time Series Classification," 2013 Brazilian Conference on Intelligent Systems, Oct. 2013, DOI: 10.1109/bracis.2013.22.

(2) Y. Kerimbekov, H. Ş. Bilge, and H. H. Uğurlu, "The use of Lorentzian distance metric in classification problems," Pattern Recognition Letters, vol. 84, 170–176, Dec. 2016, DOI: 10.1016/j.patrec.2016.09.006.

(3) A. Bagnall, A. Bostrom, J. Large, and J. Lines, "The Great Time Series Classification Bake Off: An Experimental Evaluation of Recently Proposed Algorithms." ResearchGate, Feb. 04, 2016.

(4) H. Ş. Bilge, Yerzhan Kerimbekov, and Hasan Hüseyin Uğurlu, "A new classification method by using Lorentzian distance metric," ResearchGate, Sep. 02, 2015.

(5) Y. Kerimbekov and H. Şakir Bilge, "Lorentzian Distance Classifier for Multiple Features," Proceedings of the 6th International Conference on Pattern Recognition Applications and Methods, 2017, DOI: 10.5220/0006197004930501.

(6) V. Surya Prasath et al., "Effects of Distance Measure Choice on KNN Classifier Performance - A Review." .

█ ACKNOWLEDGEMENTS

@veryfid - For many invaluable insights, discussions, and advice that helped to shape this project.

@capissimo - For open sourcing his interesting ideas regarding various KNN implementations in PineScript, several of which helped inspire my original undertaking of this project.

@RikkiTavi - For many invaluable physics-related conversations and for his helping me develop a mechanism for visualizing various distance algorithms in 3D using JavaScript

@jlaurel - For invaluable literature recommendations that helped me to understand the underlying subject matter of this project.

@annutara - For help in beta-testing this indicator and for sharing many helpful ideas and insights early on in its development.

@jasontaylor7 - For helping to beta-test this indicator and for many helpful conversations that helped to shape my backtesting workflow

@meddymarkusvanhala - For helping to beta-test this indicator

@dlbnext - For incredibly detailed backtesting testing of this indicator and for sharing numerous ideas on how the user experience could be improved.

Hurst Diamond Notation PivotsThis is a fairly simple indicator for diamond notation of past hi/lo pivot points, a common method in Hurst analysis. The diamonds mark the troughs/peaks of each cycle. They are offset by their lookback and thus will not 'paint' until after they happen so anticipate accordingly. Practically, traders can use the average length of past pivot periods to forecast future pivot periods in time🔮. For example, if the average/dominant number of bars in an 80-bar pivot point period/cycle is 76, then a trader might forecast that the next pivot could occur 76-ish bars after the last confirmed pivot. The numbers/labels on the y-axis display the cycle length used for pivot detection. This indicator doesn't repaint, but it has a lot of lag; Please use it for forecasting instead of entry signals. This indicator scans for new pivots in the form of a rainbow line and circle; once the hi/lo has happened and the lookback has passed then the pivot will be plotted. The rainbow color per wavelength theme seems to be authentic to Hurst (or modern Hurst software) and has been included as a default.

Harmonic Patterns Based Trend FollowerEarlier this week, published an idea on how harmonic patterns can be used for trend following. This script is an attempt to implement the same.

🎲 Process

🎯 Derive Zigzag and scan harmonic patterns for last 5 confirmed pivots

🎯 If a pattern is found, highest point of pattern will become the bullish zone and lower point of the pattern will become bearish zone.

🎯 Since it is trend following method, when price reaches bullish zone, then the trend is considered as bullish and when price reaches bearish zone, the trend is considered as bearish.

🎯 If price does not touch both regions, then trend remains unchanged.

🎯 Bullish and bearish zone will change as and when new patterns are formed.

🎲 Note

Patterns are not created on latest pivot as last pivot will be unconfirmed and moving. Due to this, patterns appear after certain delay - patterns will not be real time. But, this is expected and does not impact the overall process.

When new pattern formed

When price breaks over the zones

🎲 Output

🎯 Patterns formed are drawn in blue coloured lines. Due to pine limitation of max 500 lines, older patterns automatically get deleted when new ones come.

🎯 Bullish Zone and Bearish Zone are plotted in green and red colours and the zone will change whenever new pattern comes along.

🎯 Bar colors are changed according to calculated trend. Trend value can be 1 or -1 based on the current trend. You can also find the value in data window.

🎯 For simplicity purpose, input option for selection of specific patterns are not provided and also pattern names are not displayed on the chart.

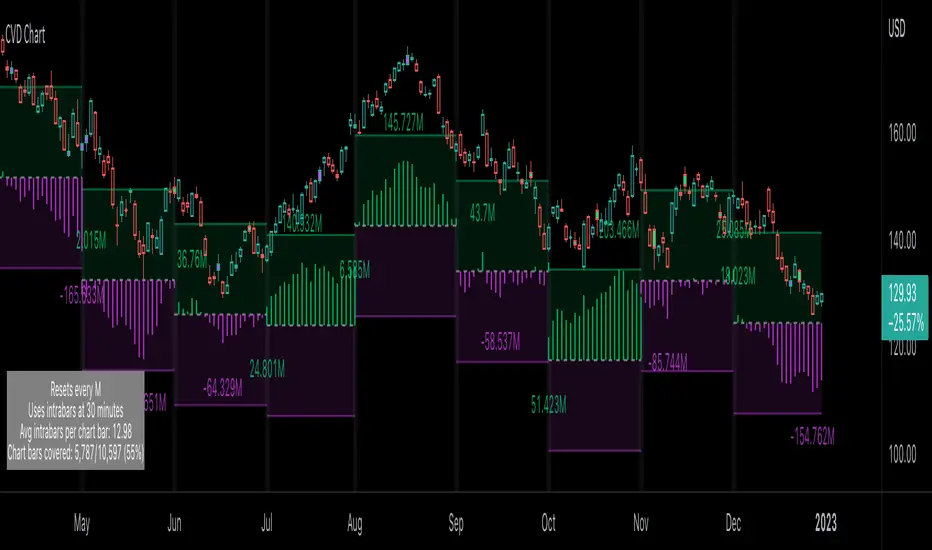

CVD - Cumulative Volume Delta (Chart)█ OVERVIEW

This indicator displays cumulative volume delta (CVD) as an on-chart oscillator. It uses intrabar analysis to obtain more precise volume delta information compared to methods that only use the chart's timeframe.

The core concepts in this script come from our first CVD indicator , which displays CVD values as plot candles in a separate indicator pane. In this script, CVD values are scaled according to price ranges and represented on the main chart pane.

█ CONCEPTS

Bar polarity

Bar polarity refers to the position of the close price relative to the open price. In other words, bar polarity is the direction of price change.

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 bars at the lower timeframe of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This script utilizes a LTF to analyze intrabars, or price changes within a chart bar. The lower the LTF, the more intrabars are analyzed, but the less chart bars can display information due to the limited number of intrabars that can be analyzed.

Volume delta

Volume delta is a measure that separates volume into "up" and "down" parts, then takes the difference to estimate the net demand for the asset. This approach gives traders a more detailed insight when analyzing volume and market sentiment. There are several methods for determining whether an asset's volume belongs in the "up" or "down" category. Some indicators, such as On Balance Volume and the Klinger Oscillator , use the change in price between bars to assign volume values to the appropriate category. Others, such as Chaikin Money Flow , make assumptions based on open, high, low, and close prices. The most accurate method involves using tick data to determine whether each transaction occurred at the bid or ask price and assigning the volume value to the appropriate category accordingly. However, this method requires a large amount of data on historical bars, which can limit the historical depth of charts and the number of symbols for which tick data is available.

In the context where historical tick data is not yet available on TradingView, intrabar analysis is the most precise technique to calculate volume delta on historical bars on our charts. This indicator uses intrabar analysis to achieve a compromise between simplicity and accuracy in calculating volume delta on historical bars. Our Volume Profile indicators use it as well. Other volume delta indicators in our Community Scripts , such as the Realtime 5D Profile , use real-time chart updates to achieve more precise volume delta calculations. However, these indicators aren't suitable for analyzing historical bars since they only work for real-time analysis.

This is the logic we use to assign intrabar volume to the "up" or "down" category:

• If the intrabar's open and close values are different, their relative position is used.

• If the intrabar's open and close values are the same, the difference between the intrabar's close and the previous intrabar's close is used.

• As a last resort, when there is no movement during an intrabar and it closes at the same price as the previous intrabar, the last known polarity is used.

Once all intrabars comprising a chart bar are analyzed, we calculate the net difference between "up" and "down" intrabar volume to produce the volume delta for the chart bar.

█ FEATURES

CVD resets

The "cumulative" part of the indicator's name stems from the fact that calculations accumulate during a period of time. By periodically resetting the volume delta accumulation, we can analyze the progression of volume delta across manageable chunks, which is often more useful than looking at volume delta accumulated from the beginning of a chart's history.

You can configure the reset period using the "CVD Resets" input, which offers the following selections:

• None : Calculations do not reset.

• On a fixed higher timeframe : Calculations reset on the higher timeframe you select in the "Fixed higher timeframe" field.

• At a fixed time that you specify.

• At the beginning of the regular session .

• On trend changes : Calculations reset on the direction change of either the Aroon indicator, Parabolic SAR , or Supertrend .

• On a stepped higher timeframe : Calculations reset on a higher timeframe automatically stepped using the chart's timeframe and following these rules:

Chart TF HTF

< 1min 1H

< 3H 1D

<= 12H 1W

< 1W 1M

>= 1W 1Y

Specifying intrabar precision

Ten options are included in the script to control the number of intrabars used per chart bar for calculations. The greater the number of intrabars per chart bar, the fewer chart bars can be analyzed.

The first five options allow users to specify the approximate amount of chart bars to be covered:

• Least Precise (Most chart bars) : Covers all chart bars by dividing the current timeframe by four.

This ensures the highest level of intrabar precision while achieving complete coverage for the dataset.

• Less Precise (Some chart bars) & More Precise (Less chart bars) : These options calculate a stepped LTF in relation to the current chart's timeframe.

• Very precise (2min intrabars) : Uses the second highest quantity of intrabars possible with the 2min LTF.

• Most precise (1min intrabars) : Uses the maximum quantity of intrabars possible with the 1min LTF.

The stepped lower timeframe for "Less Precise" and "More Precise" options is calculated from the current chart's timeframe as follows:

Chart Timeframe Lower Timeframe

Less Precise More Precise

< 1hr 1min 1min

< 1D 15min 1min

< 1W 2hr 30min

> 1W 1D 60min

The last five options allow users to specify an approximate fixed number of intrabars to analyze per chart bar. The available choices are 12, 24, 50, 100, and 250. The script will calculate the LTF which most closely approximates the specified number of intrabars per chart bar. Keep in mind that due to factors such as the length of a ticker's sessions and rounding of the LTF, it is not always possible to produce the exact number specified. However, the script will do its best to get as close to the value as possible.

As there is a limit to the number of intrabars that can be analyzed by a script, a tradeoff occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

Display

This script displays raw or cumulative volume delta values on the chart as either line or histogram oscillator zones scaled according to the price chart, allowing traders to visualize volume activity on each bar or cumulatively over time. The indicator's background shows where CVD resets occur, demarcating the beginning of new zones. The vertical axis of each oscillator zone is scaled relative to the one with the highest price range, and the oscillator values are scaled relative to the highest volume delta. A vertical offset is applied to each oscillator zone so that the highest oscillator value aligns with the lowest price. This method ensures an accurate, intuitive visual comparison of volume activity within zones, as the scale is consistent across the chart, and oscillator values sit below prices. The vertical scale of oscillator zones can be adjusted using the "Zone Height" input in the script settings.

This script displays labels at the highest and lowest oscillator values in each zone, which can be enabled using the "Hi/Lo Labels" input in the "Visuals" section of the script settings. Additionally, the oscillator's value on a chart bar is displayed as a tooltip when a user hovers over the bar, which can be enabled using the "Value Tooltips" input.

Divergences occur when the polarity of volume delta does not match that of the chart bar. The script displays divergences as bar colors and background colors that can be enabled using the "Color bars on divergences" and "Color background on divergences" inputs.

An information box in the lower-left corner of the indicator displays the HTF used for resets, the LTF used for intrabars, the average quantity of intrabars per chart bar, and the number of chart bars for which there is LTF data. This is enabled using the "Show information box" input in the "Visuals" section of the script settings.

FOR Pine Script™ CODERS

• This script utilizes `ltf()` and `ltfStats()` from the lower_tf library.

The `ltf()` function determines the appropriate lower timeframe from the selected calculation mode and chart timeframe, and returns it in a format that can be used with request.security_lower_tf() .

The `ltfStats()` function, on the other hand, is used to compute and display statistical information about the lower timeframe in an information box.

• The script utilizes display.data_window and display.status_line to restrict the display of certain plots.

These new built-ins allow coders to fine-tune where a script’s plot values are displayed.

• The newly added session.isfirstbar_regular built-in allows for resetting the CVD segments at the start of the regular session.

• The VisibleChart library developed by our resident PineCoders team leverages the chart.left_visible_bar_time and chart.right_visible_bar_time variables to optimize the performance of this script.

These variables identify the opening time of the leftmost and rightmost visible bars on the chart, allowing the script to recalculate and draw objects only within the range of visible bars as the user scrolls.

This functionality also enables the scaling of the oscillator zones.

These variables are just a couple of the many new built-ins available in the chart.* namespace.

For more information, check out this blog post or look them up by typing "chart." in the Pine Script™ Reference Manual .

• Our ta library has undergone significant updates recently, including the incorporation of the `aroon()` indicator used as a method for resetting CVD segments within this script.

Revisit the library to see more of the newly added content!

Look first. Then leap.

Musashi_Fractal_Dimension === Musashi-Fractal-Dimension ===

This tool is part of my research on the fractal nature of the markets and understanding the relation between fractal dimension and chaos theory.

To take full advantage of this indicator, you need to incorporate some principles and concepts:

- Traditional Technical Analysis is linear and Euclidean, which makes very difficult its modeling.

- Linear techniques cannot quantify non-linear behavior

- Is it possible to measure accurately a wave or the surface of a mountain with a simple ruler?

- Fractals quantify what Euclidean Geometry can’t, they measure chaos, as they identify order in apparent randomness.

- Remember: Chaos is order disguised as randomness.

- Chaos is the study of unstable aperiodic behavior in deterministic non-linear dynamic systems

- Order and randomness can coexist, allowing predictability.

- There is a reason why Fractal Dimension was invented, we had no way of measuring fractal-based structures.

- Benoit Mandelbrot used to explain it by asking: How do we measure the coast of Great Britain?

- An easy way of getting the need of a dimension in between is looking at the Koch snowflake.

- Market prices tend to seek natural levels of ranges of balance. These levels can be described as attractors and are determinant.

Fractal Dimension Index ('FDI')

Determines the persistence or anti-persistence of a market.

- A persistent market follows a market trend. An anti-persistent market results in substantial volatility around the trend (with a low r2), and is more vulnerable to price reversals

- An easy way to see this is to think that fractal dimension measures what is in between mainstream dimensions. These are:

- One dimension: a line

- Two dimensions: a square

- Three dimensions: a cube.

--> This will hint you that at certain moment, if the market has a Fractal Dimension of 1.25 (which is low), the market is behaving more “line-like”, while if the market has a high Fractal Dimension, it could be interpreted as “square-like”.

- 'FDI' is trend agnostic, which means that doesn't consider trend. This makes it super useful as gives you clean information about the market without trying to include trend stuff.

Question: If we have a game where you must choose between two options.

1. a horizontal line

2. a vertical line.

Each iteration a Horizontal Line or a Square will appear as continuation of a figure. If it that iteration shows a square and you bet vertical you win, same as if it is horizontal and it is a line.

- Wouldn’t be useful to know that Fractal dimension is 1.8? This will hint square. In the markets you can use 'FD' to filter mean-reversal signals like Bollinger bands, stochastics, Regular RSI divergences, etc.

- Wouldn’t be useful to know that Fractal dimension is 1.2? This will hint Line. In the markets you can use 'FD' to confirm trend following strategies like Moving averages, MACD, Hidden RSI divergences.

Calculation method:

Fractal dimension is obtained from the ‘hurst exponent’.

'FDI' = 2 - 'Hurst Exponent'

Musashi version of the Classic 'OG' Fractal Dimension Index ('FDI')

- By default, you get 3 fast 'FDI's (11,12,13) + 1 Slow 'FDI' (21), their interaction gives useful information.

- Fast 'FDI' cross will give you gray or red dots while Slow 'FDI' cross with the slowest of the fast 'FDI's will give white and orange dots. This are great to early spot trend beginnings or trend ends.

- A baseline (purple) is also provided, this is calculated using a 21 period Bollinger bands with 1.618 'SD', once calculated, you just take midpoint, this is the 'TDI's (Traders Dynamic Index) way. The indicator will print purple dots when Slow 'FDI' and baseline crosses, I see them as Short-Term cycle changes.

- Negative slope 'FDI' means trending asset.

- Positive most of the times hints correction, but if it got overextended it might hint a rocket-shot.

TDI Ranges:

- 'FDI' between 1.0≤ 'FDI' ≤1.4 will confirm trend following continuation signals.

- 'FDI' between 1.6≥ 'FDI' ≥2.0 will confirm reversal signals.

- 'FDI' == 1.5 hints a random unpredictable market.

Fractal Attractors

- As you must know, fractals tend orbit certain spots, this are named Attractors, this happens with any fractal behavior. The market of course also shows them, in form of Support & Resistance, Supply Demand, etc. It’s obvious they are there, but now we understand that they’re not linear, as the market is fractal, so simple trendline might not be the best tool to model this.

- I’ve noticed that when the Musashi version of the 'FDI' indicator start making a cluster of multicolor dots, this end up being an attractor, I tend to draw a rectangle as that area as price tend to come back (I still researching here).

Extra useful stuff

- Momentum / speed: Included by checking RSI Study in the indicator properties. This will add two RSI’s (9 and a 7 periods) plus a baseline calculated same way as explained for 'FDI'. This gives accurate short-term trends. It also includes RSI divergences (regular and hidden), deactivate with a simple check in the RSI section of the properties.

- BBWP (Bollinger Bands with Percentile): Efficient way of visualizing volatility as the percentile of Bollinger bands expansion. This line varies color from Iced blue when low volatility and magma red when high. By default, comes with the High vols deactivated for better view of 'FDI' and RSI while all studies are included. DDWP is trend agnostic, just like 'FDI', which make it very clean at providing information.

- Ultra Slow 'FDI': I noticed that while using BBWP and RSI, the indicator gets overcrowded, so there is the possibility of adding only one 'FDI' + its baseline.

Final Note: I’ve shown you few ways of using this indicator, please backtest before using in real trading. As you know trading is more about risk and trade management than the strategy used. This still a work in progress, I really hope you find value out of it. I use it combination with a tool named “Musashi_Katana” (also found in TradingView).

Best!

Musashi

Dynamic Linear Regression ChannelsPlots new linear regression channels from points where a previous channel is broken thus keeping the length of bars in the trend dynamic. Regression channels are useful in detecting trend changes, support and resistance levels and to trade mean reversions.

Note: Setting higher values of upper and lower deviation may result in error if the price never breaks the channel and the script references too many bars than supported.

Electrocardiogram ChartThis is an attempt to develop alternative visualisation of financial charts. This script also makes use of new pine feature types which represents User Defined Object Types. You can refer to below documentation to understand more about this feature:

www.tradingview.com

www.tradingview.com

🎲 Structure of new chart components

🎯Instead of candles/bars, this type of chart contains Electrocardiogram blocks which resembles the heartbeat signals on electrocardiogram.

Body color of the block is defined by the open and close prices of the bar. If close is greater than open, body is green. Otherwise, the body is painted red.

Border color of the block is defined by the close prices of current and previous bar. If the close of current bar is greater than that of last bar, then the border color is green. Otherwise, border color is painted red.

🎯Inside each blocks there will be 5 connecting lines called the signal lines.

open-open

open-firstPeak(high or low of the bar whichever comes first)

firstPeak-secondPeak(high or low of the bar whichever comes last)

secondPeak-close

close-close

🎯 Color of the signal lines are determined by which among the high/low of the bar comes last. If highest part of the bar reached after reaching the lowest part of the bar, then signal lines are coloured green signifying bullish sentiment towards the end of bar. If lowest part of the bar reached after reaching the highest part of the bar, then signal lines are coloured red signifying bearish sentiment towards the end of bar.

Pictorial examples here:

🎲 Limitations with pinescript implementation

Since, pinescript can only use maximum 500 lines and each block will take 1 box and 5 lines, it is not possible to display more than 100 bars.

Each block of new Electrocardiogram chart will take the space of 7 bars of candlestick chart. Due to this, the alignment of regular OHLC candles is not inline with the new chart type. Background highlighting is done for the part of the OHLC candles where Electrocardiogram blocks are plotted so that it helps users to map the bars manually

Thanks to @theheirophant for suggestion of name :)

Volume composition / quantifytools— Overview

While net volume is useful information, it can be a blunt data point. Volume composition breaks down the content of volume, allowing a more detailed look inside each volume node. Volume composition consists of the following information:

Total volume (buy and sell). By default gray node.

Dominating volume (buy or sell). By default dark green/dark red node.

Dominating active volume (buy or sell). By default light green/light red node.

Dominating volume as percentage of total volume.

Dominating active volume as percentage of total active volume.

Buy and sell volume is defined by volume associated with lower timeframe up/down moves. This classification is further broken down to passive/active, standing for decreasing/increasing volume, e.g. a move up with volume higher than previous bar volume = active buy volume, a move up with volume lower than previous bar volume = passive buy volume.

Volume data is fetched from a lower timeframe that is automatically adjusted to fit the timeframe you're using. By default, the following settings are applied:

Charts <= 30 min: 1 minute timeframe

Charts > 30 min & <= 3 hours : 5 minute timeframe

Charts > 3 hours & <= 8 hours : 15 minute timeframe

Charts > 8 hours & <= 1D: 1 hour timeframe

Charts > 1D & <= 3D : 2 hour timeframe

Charts > 3D: 4 hour timeframe

Timeframe settings can be changed via input menu. The lower the timeframe, the more precision you get but with the cost of less historical data and slower loading time. Users can also choose which source to use for determining buy/sell volume, e.g. using close as source, a close that is higher than previous close would be considered as buy volume. This could be replaced with OHLC4 for example, resulting in a volume direction based on OHLC average.

Volume composition of current chart can also be replaced with any other chart volume composition:

— Visuals

Breakdown of visual elements:

1. Symbol and timeframe used for volume composition calculations. By default the chart that is viewed and automatically selected lower timeframe.

2. Dominating volume threshold exceeded. Can be defined via input menu, 70% of total volume by default.

3. Dominating volume as percentage of total volume. Plotted below volume nodes, without % symbol.

4. Dominating active volume, + or - symbol, standing for buy and sell. Plotted below dominating volume percentage. When dominating volume and dominating active volume sides are in a disagreement (e.g. dominating volume is on buy side while dominating active volume is on sell side) this symbol will appear inside brackets, (+) or (-).

5. Dominating active volume as percentage of total active volume. Plotted below +/- symbol.

6. Dominating active volume threshold exceeded. Can be defined via input menu, 70% by default.

Dominating volume & active volume percentages can be rounded to single numbers to avoid clutter caused by overlapping values. The percentage values will be rounded to closest single number value, e.g. dominating volume percentage at 54% = 5, dominating volume percentage at 55% = 6.

Volume anomalies can be highlighted on the chart with a color for studying the events and their past implications in greater detail. Available anomalies for highlights are the following:

Buy volume threshold exceeded

Sell volume threshold exceeded

Active buy volume threshold exceeded

Active sell volume threshold exceeded

Volume & active volume divergence

— Practical guide

Volume is arguably one of the most important data points as it directly relates to liquidity. High volume can be an indication of strength (price likely to continue moving) or absorption (price likely to halt/turn). Same applies to active volume, but with an element of aggression. High active volume serves as an indication of exuberance or otherwise forceful transacting, like stop losses triggering. With these principles in mind, the composition of volume allows distinguishing potentially important events.

Example #1 : Identifying areas of trapped market participants

Often when volume spikes distinctively, we can make the case that price has found sufficient liquidity to halt/turn. Since we know which side was absorbed, in what quantity and type (passive/active), we can identify areas of trapped market participants. In such scenarios, the higher the dominant active volume and volume spike itself, the better.

Example #2 : Identifying a healthy trend

A healthy trend is one that has an active and consistent bid driving it. When this is the case, it can be seen in consistently supportive active volume.

Example #3 : Identifying inflection points

When dominant side of volume and dominant side of active volume diverge, something is up. A divergence often marks an area of indecision, hinting an imminent move one way or the other.

Day Trading Booster by DGTTiming when day trading can be everything

In Stock markets typically more volatility (or price activity) occurs at market opening and closings

When it comes to Forex (foreign exchange market), the world’s most traded market, unlike other financial markets, there is no centralized marketplace, currencies trade over the counter in whatever market is open at that time, where time becomes of more importance and key to get better trading opportunities. There are four major forex trading sessions, which are Sydney , Tokyo , London and New York sessions

Forex market is traded 24 hours a day, 5 days a week across by banks, institutions and individual traders worldwide, but that doesn’t mean it’s always active the entire day. It may be very difficult time trying to make money when the market doesn’t move at all. The busiest times with highest trading volume occurs during the overlap of the London and New York trading sessions, because U.S. dollar (USD) and the Euro (EUR) are the two most popular currencies traded. Typically most of the trading activity for a specific currency pair will occur when the trading sessions of the individual currencies overlap. For example, Australian Dollar (AUD) and Japanese Yen (JPY) will experience a higher trading volume when both Sydney and Tokyo sessions are open

There is one influence that impacts Forex matkets and should not be forgotten : the release of the significant news and reports. When a major announcement is made regarding economic data, currency can lose or gain value within a matter of seconds

Cryptocurrency markets on the other hand remain open 24/7, even during public holidays

Until 2021, the Asian impact was so significant in Cryptocurrency markets but recent reasearch reports shows that those patterns have changed and the correlation with the U.S. trading hours is becoming a clear evolving trend.

Unlike any other market Crypto doesn’t rest on weekends, there’s a drop-off in participation and yet algorithmic trading bots and market makers (or liquidity providers) can create a high volume of activity. Never trust the weekend’ is a good thing to remind yourself

One more factor that needs to be taken into accout is Blockchain transaction fees, which are responsive to network congestion and can change dramatically from one hour to the next

In general, Cryptocurrency markets are highly volatile, which means that the price of a coin can change dramatically over a short time period in either direction

The Bottom Line

The more traders trading, the higher the trading volume, and the more active the market. The more active the market, the higher the liquidity (availability of counterparties at any given time to exit or enter a trade), hence the tighter the spreads (the difference between ask and bid price) and the less slippage (the difference between the expected fill price and the actual fill price) - in a nutshell, yield to many good trading opportunities and better order execution (a process of filling the requested buy or sell order)

The best time to trade is when the market is the most active and therefore has the largest trading volume, trading all day long will not only deplete a trader's reserves quickly, but it can burn out even the most persistent trader. Knowing when the markets are more active will give traders peace of mind, that opportunities are not slipping away when they take their eyes off the markets or need to get a few hours of sleep

What does the Day Trading Booster do?

Day Trading Booster is designed ;

- to assist in determining market peak times, the times where better trading opportunities may arise

- to assist in determining the probable trading opportunities

- to help traders create their own strategies. An example strategy of when to trade or not is presented below

For Forex markets specifically includes

- Opening channel of Asian session, Europien session or both

- Opening price, opening range (5m or 15m) and day (session) range of the major trading center sessions, including Frankfurt

- A tabular view of the major forex markets oppening/closing hours, with a countdown timer

- A graphical presentation of typically traded volume and various forext markets oppening/clossing events (not only the major markets but many other around the world)

For All type of markets Day Trading Booster plots

- Day (Session) Open, 5m, 15m or 1h Opening Range

- Day (Session) Referance Levels, based on Average True Range (ATR) or Previous Day (Session) Range (PH - PL)

- Week and Month Open

Day Trading Booster also includes some of the day trader's preffered indicaotrs, such as ;

- VWAP - A custom interpretaion of VWAP is presented here with Auto, Interactive and Manual anchoring options.

- Pivot High/Low detection - Another custom interpretation of Pivot Points High Low indicator.

- A Moving Average with option to choose among SMA, EMA, WMA and HMA

An example strategy - Channel Bearkout Strategy

When day trading a trader usually monitors/analyzes lower timeframe charts and from time to time may loose insight of what really happens on the market from higher time porspective. Do not to forget to look at the larger time frame (than the one chosen to trade with) which gives the bigger picture of market price movements and thus helps to clearly define the trend

Disclaimer : Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitutes professional and/or financial advice. You alone the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

Session candles & reversals / quantifytools— Overview

Like traditional candles, session based candles are a visualization of open, high, low and close values, but based on session time periods instead of typical timeframes such as daily or weekly. Session candles are formed by fetching price at session start (open), highest price during session (high), lowest price during session (low) and price at session end (close). On top of candles, session based moving average is formed and session reversals detected. Session reversals are also backtested, using win rate and magnitude metrics to better understand what to expect from session reversals and which ones have historically performed the best.

By default, following session time periods are used:

Session #1: London (08:00 - 17:00, UTC)

Session #2: New York (13:00 - 22:00, UTC)

Session #3: Sydney (21:00 - 06:00, UTC)

Session #4: Tokyo (00:00 - 09:00, UTC)

Session time periods can be changed via input menu.

— Reversals

Session reversals are patterns that show a rapid change in direction during session. These formations are more familiarly known as wicks or engulfing candles. Following criteria must be met to qualify as a session reversal:

Wick up:

Lower high, lower low, close >= 65% of session range (0% being the very low, 100% being the very high) and open >= 40% of session range.

Wick down:

Higher high, higher low, close <= 35% of session range and open <= 60% of session range.

Engulfing up:

Higher high, lower low, close >= 65% of session range.

Engulfing down:

Higher high, lower low, close <= 35% of session range.

Session reversals are always based on prior corresponding session , e.g. to qualify as a NY session engulfing up, NY session must have a higher high and lower low relative to prior NY session , not just any session that has taken place in between. Session reversals should be viewed the same way wicks/engulfing formations are viewed on traditional timeframe based candles. Essentially, wick reversals (light green/red labels) tell you most of the motion during session was reversed. Engulfing reversals (dark green/red labels) on the other hand tell you all of the motion was reversed and new direction set.

— Backtesting

Session reversals are backtested using win rate and magnitude metrics. A session reversal is considered successful when next corresponding session closes higher/lower than session reversal close . Win rate is formed by dividing successful session reversal count with total reversal count, e.g. 5 successful reversals up / 10 reversals up total = 50% win rate. Win rate tells us what are the odds (historically) of session reversal producing a clean supporting move that was persistent enough to close that way too.

When a session reversal is successful, its magnitude is measured using percentage increase/decrease from session reversal close to next corresponding session high/low . If NY session closes higher than prior NY session that was a reversal up, the percentage increase from prior session close (reversal close) to current session high is measured. If NY session closes lower than prior NY session that was a reversal down, the percentage decrease from prior session close to current session low is measured.

Average magnitude is formed by dividing all percentage increases/decreases with total reversal count, e.g. 10 total reversals up with 1% increase each -> 10% net increase from all reversals -> 10% total increase / 10 total reversals up = 1% average magnitude. Magnitude metric supports win rate by indicating the depth of successful session reversal moves.

To better understand the backtesting calculations and more importantly to verify their validity, backtesting visuals for each session can be plotted on the chart:

All backtesting results are shown in the backtesting panel on top right corner, with highest win rates and magnitude metrics for both reversals up and down marked separately. Note that past performance is not a guarantee of future performance and session reversals as they are should not be viewed as a complete strategy for long/short plays. Always make sure reversal count is sufficient to draw reliable conclusions of performance.

— Session moving average

Users can form a session based moving average with their preferred smoothing method (SMA , EMA , HMA , WMA , RMA) and length, as well as choose which sessions to include in the moving average. For example, a moving average based on New York and Tokyo sessions can be formed, leaving London and Sydney completely out of the calculation.

— Visuals

By default, script hides your candles/bars, although in the case of candles borders will still be visible. Switching to bars/line will make your regular chart visuals 100% hidden. This setting can be turned off via input menu. As some sessions overlap, each session candle can be separately offsetted forward, clearing the overlaps. Users can also choose which session candles to show/hide.

Session periods can be highlighted on the chart as a background color, applicable to only session candles that are activated. By default, session reversals are referred to as L (London), N (New York), S (Sydney) and T (Tokyo) in both reversal labels and backtesting table. By toggling on "Numerize sessions", these will be replaced with 1, 2, 3 and 4. This will be helpful when using a custom session that isn't any of the above.

Visual settings example:

Session candles are plotted in two formats, using boxes and lines as well as plotcandle() function. Session candles constructed using boxes and lines will be clear and much easier on the eyes, but will apply only to first 500 bars due to Tradingview related limitations. Rest of the session candles go back indefinitely, but won't be as clean:

All colors can be customized via input menu.

— Timeframe & session time period considerations

As a rule of thumb, session candles should be used on timeframes at or below 1H, as higher timeframes might not match with session period start/end, leading to incorrect plots. Using 1 hour timeframe will bring optimal results as greatest amount historical data is available without sacrificing accuracy of OHLC values. If you are using a custom session that is not based on hourly period (e.g. 08:00 - 15:00 vs. 08.00 - 15.15) make sure you are using a timeframe that allows correct plots.

Session time periods applied by default are rough estimates and might be out of bounds on some charts, like NYSE listed equities. This is rarely a problem on assets that have extensive trading hours, like futures or cryptocurrency. If a session is out of bounds (asset isn't traded during the set session time period) the script won't plot given session candle and its backtesting metrics will be NA. This can be fixed by changing the session time periods to match with given asset trading hours, although you will have to consider whether or not this defeats the purpose of having candles based on sessions.

— Practical guide

Whether based on traditional timeframes or sessions, reversals should always be considered as only one piece of evidence of price turning. Never react to them without considering other factors that might support the thesis, such as levels and multi-timeframe analysis. In short, same basic charting principles apply with session candles that apply with normal candles. Use discretion.

Example #1 : Focusing efforts on session reversals at distinct support/resistance levels

A reversal against a level holds more value than a reversal by itself, as you know it's a placement where liquidity can be expected. A reversal serves as a confirming reaction for this expectation.

Example #2 : Focusing efforts on highest performing reversals and avoiding poorly performing ones

As you have data backed evidence of session reversal performance, it makes sense to focus your efforts on the ones that perform best. If some session reversal is clearly performing poorly, you would want to avoid it, since there's nothing backing up its validity.

Example #3 : Reversal clusters

Two is better than one, three is better than two and so on. If there are rapid changes in direction within multiple sessions consecutively, there's heavier evidence of a dynamic shift in price. In such case, it makes sense to hold more confidence in price halting/turning.

Economic Calendar (Import from Spreadsheet)This script draws vertical lines to mark Economic Calendar Events.

Datetime of events is defined by user in Settings via a standardized line of text.

Motivation for coding this script:

All traders should be aware of economic calendar events. At times, when you really need to pay attention to an upcoming major event, you might even decide to use the vertical-line drawing tool to mark it. However, this takes manual effort.

This script provides a solution to performing mundane tasks such as drawing vertical lines and dragging them ever so slightly, just to have them approximately aligned with exact time.

Parameters:

(1) Source data - String representation of collection of datetime referencing to Economic Calendar Events

(2) Line color, & (3) Width of line - For displaying vertical lines drawn by script.

Standardized format for Source Data :

Example:

If 'GMT;2022,6,1,14,0,0;2022,6,2,12,15,0;' is provided to PineScript, then two vertical lines will be drawn on June 6, 2022 according to the exact time in 'YYYY,MM,DD,hh,mm,ss' format at the specified timezone (GMT in this case).

Template for Source Data :

Included here, link below, is a shared Google Sheet that systematically processes Economic Calendar data provided in the 'Raw Data' tab.

drive.google.com

Users are advised to use their preferred methods* to format the string (for source data param.), and apply their own criteria to sort down the Events. (ie. only include Events of High Impact, etc.)

* Preferred methods (as mentioned above) does not mean being limited to using the template as provided in this post.

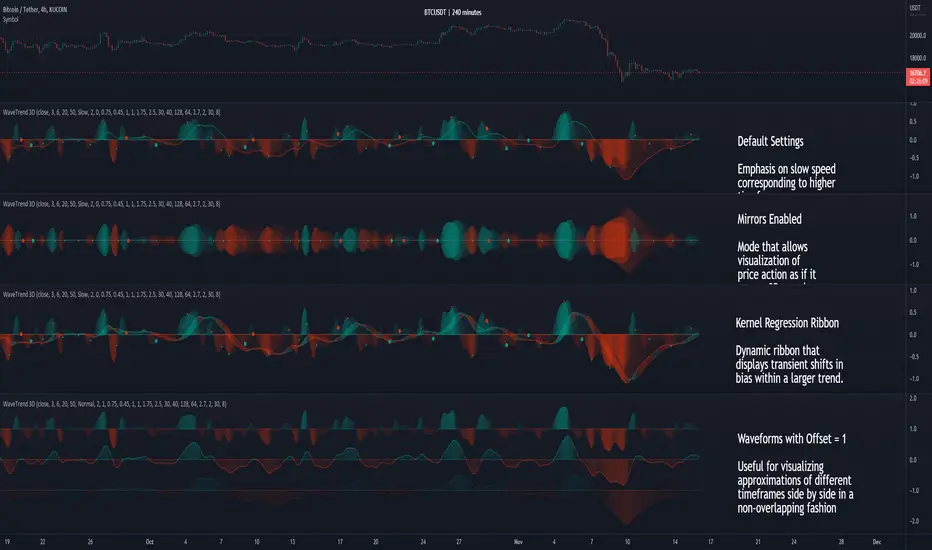

WaveTrend 3D█ OVERVIEW

WaveTrend 3D (WT3D) is a novel implementation of the famous WaveTrend (WT) indicator and has been completely redesigned from the ground up to address some of the inherent shortcomings associated with the traditional WT algorithm.

█ BACKGROUND

The WaveTrend (WT) indicator has become a widely popular tool for traders in recent years. WT was first ported to PineScript in 2014 by the user @LazyBear, and since then, it has ascended to become one of the Top 5 most popular scripts on TradingView.

The WT algorithm appears to have origins in a lesser-known proprietary algorithm called Trading Channel Index (TCI), created by AIQ Systems in 1986 as an integral part of their commercial software suite, TradingExpert Pro. The software’s reference manual states that “TCI identifies changes in price direction” and is “an adaptation of Donald R. Lambert’s Commodity Channel Index (CCI)”, which was introduced to the world six years earlier in 1980. Interestingly, a vestige of this early beginning can still be seen in the source code of LazyBear’s script, where the final EMA calculation is stored in an intermediate variable called “tci” in the code.

█ IMPLEMENTATION DETAILS

WaveTrend 3D is an alternative implementation of WaveTrend that directly addresses some of the known shortcomings of the indicator, including its unbounded extremes, susceptibility to whipsaw, and lack of insight into other timeframes.

In the canonical WT approach, an exponential moving average (EMA) for a given lookback window is used to assess the variability between price and two other EMAs relative to a second lookback window. Since the difference between the average price and its associated EMA is essentially unbounded, an arbitrary scaling factor of 0.015 is typically applied as a crude form of rescaling but still fails to capture 20-30% of values between the range of -100 to 100. Additionally, the trigger signal for the final EMA (i.e., TCI) crossover-based oscillator is a four-bar simple moving average (SMA), which further contributes to the net lag accumulated by the consecutive EMA calculations in the previous steps.

The core idea behind WT3D is to replace the EMA-based crossover system with modern Digital Signal Processing techniques. By assuming that price action adheres approximately to a Gaussian distribution, it is possible to sidestep the scaling nightmare associated with unbounded price differentials of the original WaveTrend method by focusing instead on the alteration of the underlying Probability Distribution Function (PDF) of the input series. Furthermore, using a signal processing filter such as a Butterworth Filter, we can eliminate the need for consecutive exponential moving averages along with the associated lag they bring.

Ideally, it is convenient to have the resulting probability distribution oscillate between the values of -1 and 1, with the zero line serving as a median. With this objective in mind, it is possible to borrow a common technique from the field of Machine Learning that uses a sigmoid-like activation function to transform our data set of interest. One such function is the hyperbolic tangent function (tanh), which is often used as an activation function in the hidden layers of neural networks due to its unique property of ensuring the values stay between -1 and 1. By taking the first-order derivative of our input series and normalizing it using the quadratic mean, the tanh function performs a high-quality redistribution of the input signal into the desired range of -1 to 1. Finally, using a dual-pole filter such as the Butterworth Filter popularized by John Ehlers, excessive market noise can be filtered out, leaving behind a crisp moving average with minimal lag.

Furthermore, WT3D expands upon the original functionality of WT by providing:

First-class support for multi-timeframe (MTF) analysis

Kernel-based regression for trend reversal confirmation

Various options for signal smoothing and transformation

A unique mode for visualizing an input series as a symmetrical, three-dimensional waveform useful for pattern identification and cycle-related analysis

█ SETTINGS

This is a summary of the settings used in the script listed in roughly the order in which they appear. By default, all default colors are from Google's TensorFlow framework and are considered to be colorblind safe.

Source: The input series. Usually, it is the close or average price, but it can be any series.

Use Mirror: Whether to display a mirror image of the source series; for visualizing the series as a 3D waveform similar to a soundwave.

Use EMA: Whether to use an exponential moving average of the input series.

EMA Length: The length of the exponential moving average.

Use COG: Whether to use the center of gravity of the input series.

COG Length: The length of the center of gravity.

Speed to Emphasize: The target speed to emphasize.

Width: The width of the emphasized line.

Display Kernel Moving Average: Whether to display the kernel moving average of the signal. Like PCA, an unsupervised Machine Learning technique whereby neighboring vectors are projected onto the Principal Component.

Display Kernel Signal: Whether to display the kernel estimator for the emphasized line. Like the Kernel MA, it can show underlying shifts in bias within a more significant trend by the colors reflected on the ribbon itself.

Show Oscillator Lines: Whether to show the oscillator lines.

Offset: The offset of the emphasized oscillator plots.

Fast Length: The length scale factor for the fast oscillator.

Fast Smoothing: The smoothing scale factor for the fast oscillator.

Normal Length: The length scale factor for the normal oscillator.

Normal Smoothing: The smoothing scale factor for the normal frequency.

Slow Length: The length scale factor for the slow oscillator.

Slow Smoothing: The smoothing scale factor for the slow frequency.

Divergence Threshold: The number of bars for the divergence to be considered significant.

Trigger Wave Percent Size: How big the current wave should be relative to the previous wave.

Background Area Transparency Factor: Transparency factor for the background area.

Foreground Area Transparency Factor: Transparency factor for the foreground area.

Background Line Transparency Factor: Transparency factor for the background line.

Foreground Line Transparency Factor: Transparency factor for the foreground line.

Custom Transparency: Transparency of the custom colors.

Total Gradient Steps: The maximum amount of steps supported for a gradient calculation is 256.

Fast Bullish Color: The color of the fast bullish line.

Normal Bullish Color: The color of the normal bullish line.

Slow Bullish Color: The color of the slow bullish line.

Fast Bearish Color: The color of the fast bearish line.

Normal Bearish Color: The color of the normal bearish line.

Slow Bearish Color: The color of the slow bearish line.

Bullish Divergence Signals: The color of the bullish divergence signals.

Bearish Divergence Signals: The color of the bearish divergence signals.

█ ACKNOWLEDGEMENTS

@LazyBear - For authoring the original WaveTrend port on TradingView

@PineCoders - For the beautiful color gradient framework used in this indicator

@veryfid - For the inspiration of using mirrored signals for cycle analysis and using multiple lookback windows as proxies for other timeframes

Next Pivot Projection [Trendoscope]Still experimental. Extending further on the divergence backtest results - in this script we try to project next 2 pivots (including one unconfirmed pivot)

🎲 Previous experiments

1. Divergence-Backtester

2. Divergence-Backtester-V2

🎲 Additions

Apart from collecting the stats on number of occurrences of HH, HL, LH, LL - this script also keeps track of average ratio for each levels and average bars.

Based on these data, we try to calculate the next pivot projections including possible bar and price.

Cloud covering the candles indicate historical levels of average HH, HL, LH, LL projections.

Hover on projection labels to find more details in tooltips.

🎲 Overall method in a nutshell

🎲 Going bit deeper

🎯 Unconfirmed Pivot and its projection - Last pivot of the zigzag is always unconfirmed. Meaning, it can potentially repaint based on further price movements. But, projection of the unconfirmed pivot will not change as it will be based on previous two pivots - both of which are confirmed.

🎯 Next Pivot Projection - Next pivot is projected based on last two pivots - which include last unconfirmed pivot. Hence, these projections can potentially repaint based on the last pivot repaint.

🎯 Historical projections displayed as cloud - Historical projection values are displayed as cloud around pivots.

A cloud above represents area from average lower high range to average higher high range. Cloud color is green if average ratio of pivot high is more than 1. Red Otherwise.

A cloud below represents area from average higher low range to average lower low range. Cloud color is red if average ratio of pivot high is more than 1. Green otherwise

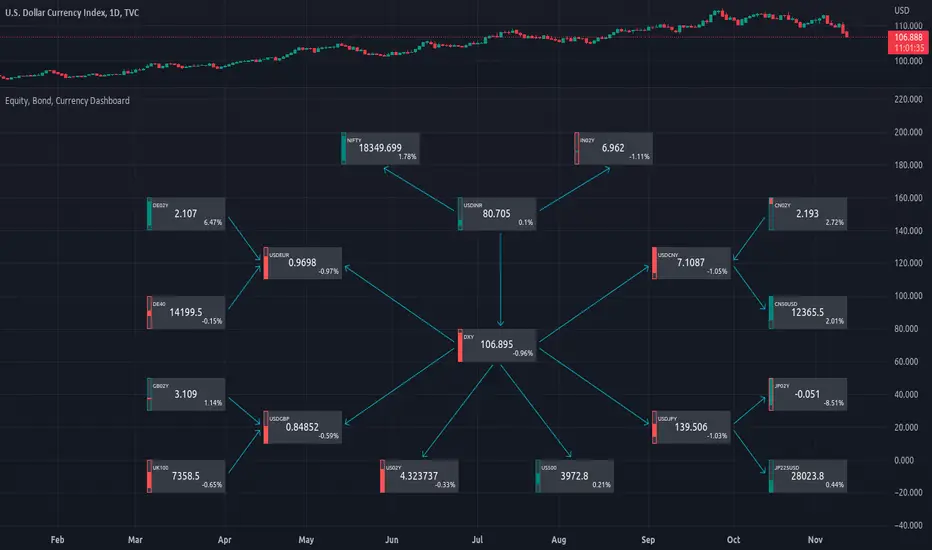

Equity Bond Currency DashboardDepicts demand-flow between Equities, Bonds and Currencies of 6 countries. Useful in tracking the flow of smart money and checking the dynamics of inter-connected markets.

Principle:

DXY lies at the heart of the diagram with usd-currency pairs of 5 countries connected to it. When demand for a currency increases it strengthens against Dollar. This is depicted by a line from DXY to the currency indicating demand flow from Dollar to the currency (DXY is only an indicative symbol for Dollar, the currency may not be part of the dollar index). Similarly when Dollar strengthens against the currency, demand flow is depicted by a line from the currency to DXY. Currency blocks are connected to Equity and Bond Yields of the respective countries. Equities and Bonds, when bought, takes the demand from the respective currencies and vice versa.

Overall, the demand flows in the direction of arrows. The flow is incomplete without commodities, import/export, interest/inflation rates of countries, however, the diagram most of the times explains why an asset class is performing the way it is.

Left side bar of each block is very similar to OHLC candles except for the following -

Instead of wicks, top and bottom of the bar represents high and low for the selected time-frame

Open and close are normalised for high and low

Bar border is red if close < prev.close, green if close >= prev.close

Other notes:

The diagram requires at least 200 bars in the chart to render. Please select the symbol and time-frame that contain at least 200 bars.

The diagram requires a live market to render the flow. To check flows on historical bars, set the option from settings.

Desired indices could be selected for countries of choice. Default settings point to futures wherever possible to have the markets live simultaneously across the countries.

Volume Profile Volume Delta OI Delta [Kioseff Trading]Hello!

This script serves to distinguish volume delta for any asset and open interest delta for Binance perpetual futures.

The image above provides further explanation of functionality and color correspondence.

The image above shows the indicator calculating volume at each tick level and displaying the metric.

The label color outline (neon effect) is configurable; the image above is absent the feature.

The image above shows Open Interest (OI) Delta calculated - similar to how the script calculates volume delta - for a Binance Perpetual Future pair.

This feature only works for Binance Futures pairs; the script will not load when trying to calculate OI Delta on other assets.