Nick Rypock Trailing Reverse (NRTR)This indicator was invented in 2001 by Konstantin Kopyrkin. The name "Nick Rypock" is derived from his surname reading in the opposite direction:

Kopyrkin -> Kopyr Kin -> Kin Kopyr -> Nik Rypok

The idea of the indicator is similar to the Chandelier Exit, but doesn't involve ATR component and uses a percentage instead.

A dynamic price channel is used to calculate the NRTR. The calculations involve only those prices that are included in the current trend and exclude the extremes related to the previous trend. The indicator is always at the same distance (in percent) from the extremes reached by prices (below the maximum peak for the current uptrend, above the minimum bottom for the current downtrend).

Индикаторы и стратегии

Machine Learning: Logistic RegressionMulti-timeframe Strategy based on Logistic Regression algorithm

Description:

This strategy uses a classic machine learning algorithm that came from statistics - Logistic Regression (LR).

The first and most important thing about logistic regression is that it is not a 'Regression' but a 'Classification' algorithm. The name itself is somewhat misleading. Regression gives a continuous numeric output but most of the time we need the output in classes (i.e. categorical, discrete). For example, we want to classify emails into “spam” or 'not spam', classify treatment into “success” or 'failure', classify statement into “right” or 'wrong', classify election data into 'fraudulent vote' or 'non-fraudulent vote', classify market move into 'long' or 'short' and so on. These are the examples of logistic regression having a binary output (also called dichotomous).

You can also think of logistic regression as a special case of linear regression when the outcome variable is categorical, where we are using log of odds as dependent variable. In simple words, it predicts the probability of occurrence of an event by fitting data to a logit function.

Basically, the theory behind Logistic Regression is very similar to the one from Linear Regression, where we seek to draw a best-fitting line over data points, but in Logistic Regression, we don’t directly fit a straight line to our data like in linear regression. Instead, we fit a S shaped curve, called Sigmoid, to our observations, that best SEPARATES data points. Technically speaking, the main goal of building the model is to find the parameters (weights) using gradient descent.

In this script the LR algorithm is retrained on each new bar trying to classify it into one of the two categories. This is done via the logistic_regression function by updating the weights w in the loop that continues for iterations number of times. In the end the weights are passed through the sigmoid function, yielding a prediction.

Mind that some assets require to modify the script's input parameters. For instance, when used with BTCUSD and USDJPY, the 'Normalization Lookback' parameter should be set down to 4 (2,...,5..), and optionally the 'Use Price Data for Signal Generation?' parameter should be checked. The defaults were tested with EURUSD.

Note: TradingViews's playback feature helps to see this strategy in action.

Warning: Signals ARE repainting.

Style tags: Trend Following, Trend Analysis

Asset class: Equities, Futures, ETFs, Currencies and Commodities

Dataset: FX Minutes/Hours/Days

VolumeHeatmap | Experimental Version of Marketorders MatrixDear all,

I wish a Happy New Year!

The last time I tried to developing a Volume Heatmap, that the Marketorders made.

With the currently version I achieve my skills for that and I present it for everyone - some bugs I cannot solve today.

It also possible to see the POC - also the dynamic of volume developing:

The background for that is to find the pricelevel with the most volume - this is for valuetrading always the target.

If someone find it useful or have question - let me know!

Kind regards

NXT2017

Relative Volume at Time█ OVERVIEW

This indicator calculates relative volume, which is the ratio of present volume over an average of past volume.

It offers two calculation modes, both using a time reference as an anchor.

█ CONCEPTS

Calculation modes

The simplest way to calculate relative volume is by using the ratio of a bar's volume over a simple moving average of the last n volume values.

This indicator uses one of two, more subtle ways to calculate both values of the relative volume ratio: current volume:past volume .

The two calculations modes are:

1 — Cumulate from Beginning of TF to Current Bar where:

current volume = the cumulative volume since the beginning of the timeframe unit, and

past volume = the mean of volume during that same relative period of time in the past n timeframe units.

2 — Point-to-Point Bars at Same Offset from Beginning of TF where:

current volume = the volume on a single chart bar, and

past volume = the mean of volume values from that same relative bar in time from the past n timeframe units.

Timeframe units

Timeframe units can be defined in three different ways:

1 — Using Auto-steps, where the timeframe unit automatically adjusts to the timeframe used on the chart:

— A 1 min timeframe unit will be used on 1sec charts,

— 1H will be used for charts at 1min and less,

— 1D will be used for other intraday chart timeframes,

— 1W will be used for 1D charts,

— 1M will be used for charts at less than 1M,

— 1Y will be used for charts at greater or equal than 1M.

2 — As a fixed timeframe that you define.

3 — By time of day (for intraday chart timeframes only), which you also define. If you use non-intraday chart timeframes in this mode, the indicator will switch to Auto-steps.

Relative Relativity

A relative volume value of 1.0 indicates that current volume is equal to the mean of past volume , but how can we determine what constitutes a high relative volume value?

The traditional way is to settle for an arbitrary threshold, with 2.0 often used to indicate that relative volume is worthy of attention.

We wanted to provide traders with a contextual method of calculating threshold values, so in addition to the conventional fixed threshold value,

this indicator includes two methods of calculating a threshold channel on past relative volume values:

1 — Using the standard deviation of relative volume over a fixed lookback.

2 — Using the highs/lows of relative volume over a variable lookback.

Channels calculated on relative volume provide meta-relativity, if you will, as they are relative values of relative volume.

█ FEATURES

Controls in the "Display" section of inputs determine what is visible in the indicator's pane. The next "Settings" section is where you configure the parameters used in the calculations. The "Column Coloring Conditions" section controls the color of the columns, which you will see in three of the five display modes available. Whether columns are plotted or not, the coloring conditions also determine when markers appear, if you have chosen to show the markers in the "Display" section. The presence of markers is what triggers the alerts configured on this indicator. Finally, the "Colors" section of inputs allows you to control the color of the indicator's visual components.

Display

Five display modes are available:

• Current Volume Columns : shows columns of current volume , with past volume displayed as an outlined column.

• Relative Volume Columns : shows relative volume as a column.

• Relative Volume Columns With Average : shows relative volume as a column, with the average of relative volume.

• Directional Relative Volume Average : shows a line calculated using the average of +/- values of relative volume.

The positive value of relative volume is used on up bars; its negative value on down bars.

• Relative Volume Average : shows the average of relative volume.

A Hull moving average is used to calculate the average used in the three last display modes.

You can also control the display of:

• The value or relative volume, when in the first three display modes. Only the last 500 values will be shown.

• Timeframe transitions, shown in the background.

• A reminder of the active timeframe unit, which appears to the right of the indicator's last bar.

• The threshold used, which can be a fixed value or a channel, as determined in the next "Settings" section of inputs.

• Up/Down markers, which appear on transitions of the color of the volume columns (determined by coloring conditions), which in turn control when alerts are triggered.

• Conditions of high volatility.

Settings

Use this section of inputs to change:

• Calculation mode : this is where you select one of this indicator's two calculation modes for current volume and past volume , as explained in the "Concepts" section.

• Past Volume Lookback in TF units : the quantity of timeframe units used in the calculation of past volume .

• Define Timeframes Units Using : the mode used to determine what one timeframe unit is. Note that when using a fixed timeframe, it must be higher than the chart's timeframe.

Also, note that time of day timeframe units only work on intraday chart timeframes.

• Threshold Mode : Five different modes can be selected:

— Fixed Value : You can define the value using the "Fixed Threshold" field below. The default value is 2.0.

— Standard Deviation Channel From Fixed Lookback : This is a channel calculated using the simple moving average of relative volume

(so not the Hull moving average used elsewhere in the indicator), plus/minus the standard deviation multiplied by a user-defined factor.

The lookback used is the value of the "Channel Lookback" field. Its default is 100.

— High/Low Channel From Beginning of TF : in this mode, the High/Low values reset at the beginning of each timeframe unit.

— High/Low Channel From Beginning of Past Volume Lookback : in this mode, the High/Low values start from the farthest point back where we are calculating past volume ,

which is determined by the combination of timeframe units and the "Past Volume Lookback in TF units" value.

— High/Low Channel From Fixed Lookback : In this mode the lookback is fixed. You can define the value using the "Channel Lookback" field. The default value is 100.

• Period of RelVol Moving Average : the period of the Hull moving average used in the "Directional Relative Volume Average" and the "Relative Volume Average".

• High Volatility is defined using fast and slow ATR periods, so this represents the volatility of price.

Volatility is considered to be high when the fast ATR value is greater than its slow value. Volatility can be used as a filter in the column coloring conditions.

Column Coloring Conditions

• Eight different conditions can be turned on or off to determine the color of the volume columns. All "ON" conditions must be met to determine a high/low state of relative volume,

or, in the case of directional relative volume, a bull/bear state.

• A volatility state can also be used to filter the conditions.

• When the coloring conditions and the filter do not allow for a high/low state to be determined, the neutral color is used.

• Transitions of the color of the volume columns determined by coloring conditions are used to plot the up/down markers, which in turn control when alerts are triggered.

Colors

• You can define your own colors for all of the oscillator's plots.

• The default colors will perform well on light or dark chart backgrounds.

Alerts

• An alert can be defined for the script. The alert will trigger whenever an up/down marker appears in the indicator's display.

The particular combination of coloring conditions and the display settings for up/down markers when you create the alert will determine which conditions trigger the alert.

After alerts are created, subsequent changes to the conditions controlling the display of markers will not affect existing alerts.

• By configuring the script's inputs in different ways before you create your alerts, you can create multiple, functionally distinct alerts from this script.

When creating multiple alerts, it is useful to include in the alert's message a reminder of the particular conditions you used for each alert.

• As is usually the case, alerts triggering "Once Per Bar Close" will prevent repainting.

Error messages

Error messages will appear at the end of the chart upon the following conditions:

• When the combination of the timeframe units used and the "Past Volume Lookback in TF units" value create a lookback that is greater than 5000 bars.

The lookback will then be recalculated to a value such that a runtime error does not occur.

• If the chart's timeframe is higher than the timeframe units. This error cannot occur when using Auto-steps to calculate timeframe units.

• If relative volume cannot be calculated, for example, when no volume data is available for the chart's symbol.

• When the threshold of relative volume is configured to be visible but the indicator's scale does not allow it to be visible (in "Current Volume Columns" display mode).

█ NOTES

For traders

The chart shown here uses the following display modes: "Current Volume Columns", "Relative Volume Columns With Average", "Directional Relative Volume Average" and "Relative Volume Average". The last one also shows the threshold channel in standard deviation mode, and the TF Unit reminder to the right, in red.

Volume, like price, is a value with a market-dependent scale. The only valid reference for volume being its past values, any improvement in the way past volume is calculated thus represents a potential opportunity to traders. Relative volume calculated as it is here can help traders extract useful information from markets in many circumstances, markets with cyclical volume such as Forex being one, obvious case. The relative nature of the values calculated by this indicator also make it a natural fit for cross-market and cross-sector analysis, or to identify behavioral changes in the different futures contracts of the same market. Relative volume can also be put to more exotic uses, such as in evaluating changes in the popularity of exchanges.

Relative volume alone has no directional bias. While higher relative volume values always indicate higher trading activity, that activity does not necessarily translate into significant price movement. In a tightly fought battle between buyers and sellers, you could theoretically have very large volume for many bars, with no change whatsoever in bid/ask prices. This of course, is unlikely to happen in reality, and so traders are justified in considering high relative volume values as indicating periods where more attention is required, because imbalances in the strength of buying/selling power during high-volume trading periods can amplify price variations, providing traders with the generally useful gift of volatility.

Be sure to give the "Directional Relative Volume Average" a try. Contrary to the always-positive ratio widely used in this indicator, the "Directional Relative Volume Average" produces a value able to determine a bullish/bearish bias for relative volume.

Note that realtime bars must be complete for the relative volume value to be confirmed. Values calculated on historical or elapsed realtime bars will not recalculate unless historical volume data changes.

Finally, as with all indicators using volume information, keep in mind that some exchanges/brokers supply different feeds for intraday and daily data, and the volume data on both feeds can sometimes vary quite a bit.

For coders

Our script was written using the PineCoders Coding Conventions for Pine .

The description was formatted using the techniques explained in the How We Write and Format Script Descriptions PineCoders publication.

Bits and pieces of code were lifted from the MTF Selection Framework and the MTF Oscillator Framework , also by PineCoders.

█ THANKS

Thanks to dgtrd for suggesting to add the channel using standard deviation.

Thanks to adolgov for helpful suggestions on calculations and visuals.

Look first. Then leap.

Waindrops [Makit0]█ OVERALL

Plot waindrops (custom volume profiles) on user defined periods, for each period you get high and low, it slices each period in half to get independent vwap, volume profile and the volume traded per price at each half.

It works on intraday charts only, up to 720m (12H). It can plot balanced or unbalanced waindrops, and volume profiles up to 24H sessions.

As example you can setup unbalanced periods to get independent volume profiles for the overnight and cash sessions on the futures market, or 24H periods to get the full session volume profile of EURUSD

The purpose of this indicator is twofold:

1 — from a Chartist point of view, to have an indicator which displays the volume in a more readable way

2 — from a Pine Coder point of view, to have an example of use for two very powerful tools on Pine Script:

• the recently updated drawing limit to 500 (from 50)

• the recently ability to use drawings arrays (lines and labels)

If you are new to Pine Script and you are learning how to code, I hope you read all the code and comments on this indicator, all is designed for you,

the variables and functions names, the sometimes too big explanations, the overall structure of the code, all is intended as an example on how to code

in Pine Script a specific indicator from a very good specification in form of white paper

If you wanna learn Pine Script form scratch just start HERE

In case you have any kind of problem with Pine Script please use some of the awesome resources at our disposal: USRMAN , REFMAN , AWESOMENESS , MAGIC

█ FEATURES

Waindrops are a different way of seeing the volume and price plotted in a chart, its a volume profile indicator where you can see the volume of each price level

plotted as a vertical histogram for each half of a custom period. By default the period is 60 so it plots an independent volume profile each 30m

You can think of each waindrop as an user defined candlestick or bar with four key values:

• high of the period

• low of the period

• left vwap (volume weighted average price of the first half period)

• right vwap (volume weighted average price of the second half period)

The waindrop can have 3 different colors (configurable by the user):

• GREEN: when the right vwap is higher than the left vwap (bullish sentiment )

• RED: when the right vwap is lower than the left vwap (bearish sentiment )

• BLUE: when the right vwap is equal than the left vwap ( neutral sentiment )

KEY FEATURES

• Help menu

• Custom periods

• Central bars

• Left/Right VWAPs

• Custom central bars and vwaps: color and pixels

• Highly configurable volume histogram: execution window, ticks, pixels, color, update frequency and fine tuning the neutral meaning

• Volume labels with custom size and color

• Tracking price dot to be able to see the current price when you hide your default candlesticks or bars

█ SETTINGS

Click here or set any impar period to see the HELP INFO : show the HELP INFO, if it is activated the indicator will not plot

PERIOD SIZE (max 2880 min) : waindrop size in minutes, default 60, max 2880 to allow the first half of a 48H period as a full session volume profile

BARS : show the central and vwap bars, default true

Central bars : show the central bars, default true

VWAP bars : show the left and right vwap bars, default true

Bars pixels : width of the bars in pixels, default 2

Bars color mode : bars color behavior

• BARS : gets the color from the 'Bars color' option on the settings panel

• HISTOGRAM : gets the color from the Bearish/Bullish/Neutral Histogram color options from the settings panel

Bars color : color for the central and vwap bars, default white

HISTOGRAM show the volume histogram, default true

Execution window (x24H) : last 24H periods where the volume funcionality will be plotted, default 5

Ticks per bar (max 50) : width in ticks of each histogram bar, default 2

Updates per period : number of times the histogram will update

• ONE : update at the last bar of the period

• TWO : update at the last bar of each half period

• FOUR : slice the period in 4 quarters and updates at the last bar of each of them

• EACH BAR : updates at the close of each bar

Pixels per bar : width in pixels of each histogram bar, default 4

Neutral Treshold (ticks) : delta in ticks between left and right vwaps to identify a waindrop as neutral, default 0

Bearish Histogram color : histogram color when right vwap is lower than left vwap, default red

Bullish Histogram color : histogram color when right vwap is higher than left vwap, default green

Neutral Histogram color : histogram color when the delta between right and left vwaps is equal or lower than the Neutral treshold, default blue

VOLUME LABELS : show volume labels

Volume labels color : color for the volume labels, default white

Volume Labels size : text size for the volume labels, choose between AUTO, TINY, SMALL, NORMAL or LARGE, default TINY

TRACK PRICE : show a yellow ball tracking the last price, default true

█ LIMITS

This indicator only works on intraday charts (minutes only) up to 12H (720m), the lower chart timeframe you can use is 1m

This indicator needs price, time and volume to work, it will not work on an index (there is no volume), the execution will not be allowed

The histogram (volume profile) can be plotted on 24H sessions as limit but you can plot several 24H sessions

█ ERRORS AND PERFORMANCE

Depending on the choosed settings, the script performance will be highly affected and it will experience errors

Two of the more common errors it can throw are:

• Calculation takes too long to execute

• Loop takes too long

The indicator performance is highly related to the underlying volatility (tick wise), the script takes each candlestick or bar and for each tick in it stores the price and volume, if the ticker in your chart has thousands and thousands of ticks per bar the indicator will throw an error for sure, it can not calculate in time such amount of ticks.

What all of that means? Simply put, this will throw error on the BITCOIN pair BTCUSD (high volatility with tick size 0.01) because it has too many ticks per bar, but lucky you it will work just fine on the futures contract BTC1! (tick size 5) because it has a lot less ticks per bar

There are some options you can fine tune to boost the script performance, the more demanding option in terms of resources consumption is Updates per period , by default is maxed out so lowering this setting will improve the performance in a high way.

If you wanna know more about how to improve the script performance, read the HELP INFO accessible from the settings panel

█ HOW-TO SETUP

The basic parameters to adjust are Period size , Ticks per bar and Pixels per bar

• Period size is the main setting, defines the waindrop size, to get a better looking histogram set bigger period and smaller chart timeframe

• Ticks per bar is the tricky one, adjust it differently for each underlying (ticker) volatility wise, for some you will need a low value, for others a high one.

To get a more accurate histogram set it as lower as you can (min value is 1)

• Pixels per bar allows you to adjust the width of each histogram bar, with it you can adjust the blank space between them or allow overlaping

You must play with these three parameters until you obtain the desired histogram: smoother, sharper, etc...

These are some of the different kind of charts you can setup thru the settings:

• Balanced Waindrops (default): charts with waindrops where the two halfs are of same size.

This is the default chart, just select a period (30m, 60m, 120m, 240m, pick your poison), adjust the histogram ticks and pixels and watch

• Unbalanced Waindrops: chart with waindrops where the two halfs are of different sizes.

Do you trade futures and want to plot a waindrop with the first half for the overnight session and the second half for the cash session? you got it;

just adjust the period to 1860 for any CME ticker (like ES1! for example) adjust the histogram ticks and pixels and watch

• Full Session Volume Profile: chart with waindrops where only the first half plots.

Do you use Volume profile to analize the market? Lucky you, now you can trick this one to plot it, just try a period of 780 on SPY, 2760 on ES1!, or 2880 on EURUSD

remember to adjust the histogram ticks and pixels for each underlying

• Only Bars: charts with only central and vwap bars plotted, simply deactivate the histogram and volume labels

• Only Histogram: charts with only the histogram plotted (volume profile charts), simply deactivate the bars and volume labels

• Only Volume: charts with only the raw volume numbers plotted, simply deactivate the bars and histogram

If you wanna know more about custom full session periods for different asset classes, read the HELP INFO accessible from the settings panel

EXAMPLES

Full Session Volume Profile on MES 5m chart:

Full Session Unbalanced Waindrop on MNQ 2m chart (left side Overnight session, right side Cash Session):

The following examples will have the exact same charts but on four different tickers representing a futures contract, a forex pair, an etf and a stock.

We are doing this to be able to see the different parameters we need for plotting the same kind of chart on different assets

The chart composition is as follows:

• Left side: Volume Labels chart (period 10)

• Upper Right side: Waindrops (period 60)

• Lower Right side: Full Session Volume Profile

The first example will specify the main parameters, the rest of the charts will have only the differences

MES :

• Left: Period size: 10, Bars: uncheck, Histogram: uncheck, Execution window: 1, Ticks per bar: 2, Updates per period: EACH BAR,

Pixels per bar: 4, Volume labels: check, Track price: check

• Upper Right: Period size: 60, Bars: check, Bars color mode: HISTOGRAM, Histogram: check, Execution window: 2, Ticks per bar: 2,

Updates per period: EACH BAR, Pixels per bar: 4, Volume labels: uncheck, Track price: check

• Lower Right: Period size: 2760, Bars: uncheck, Histogram: check, Execution window: 1, Ticks per bar: 1, Updates per period: EACH BAR,

Pixels per bar: 2, Volume labels: uncheck, Track price: check

EURUSD :

• Upper Right: Ticks per bar: 10

• Lower Right: Period size: 2880, Ticks per bar: 1, Pixels per bar: 1

SPY :

• Left: Ticks per bar: 3

• Upper Right: Ticks per bar: 5, Pixels per bar: 3

• Lower Right: Period size: 780, Ticks per bar: 2, Pixels per bar: 2

AAPL :

• Left: Ticks per bar: 2

• Upper Right: Ticks per bar: 6, Pixels per bar: 3

• Lower Right: Period size: 780, Ticks per bar: 1, Pixels per bar: 2

█ THANKS TO

PineCoders for all they do, all the tools and help they provide and their involvement in making a better community

scarf for the idea of coding a waindrops like indicator, I did not know something like that existed at all

All the Pine Coders, Pine Pros and Pine Wizards, people who share their work and knowledge for the sake of it and helping others, I'm very grateful indeed

I'm learning at each step of the way from you all, thanks for this awesome community;

Opensource and shared knowledge: this is the way! (said with canned voice from inside my helmet :D)

█ NOTE

This description was formatted following THIS guidelines

═════════════════════════════════════════════════════════════════════════

I sincerely hope you enjoy reading and using this work as much as I enjoyed developing it :D

GOOD LUCK AND HAPPY TRADING!

Stop loss and Take Profit in $$ exampleThis is a simple exit example in $$ (symbol's currency) for educational purpose .

Stepped trailing strategy exampleThis is a stepped trailing exit example for educational purpose .

Short brief.

There are 1 stop loss and 3 profit levels.

When first tp is reached we move stop loss to break-even.

When second tp is reached we move stop loss to first tp.

When third tp is reached we exit by profit.

Moving RegressionMoving Regression is a generalization of moving average and polynomial regression.

The procedure approximates a specified number of prior data points with a polynomial function of a user-defined degree. Then, polynomial interpolation of the last data point is used to construct a Moving Regression time series.

Application:

Moving Regression allows one to smooth noise on the analyzed chart, assess momentum, confirm trends, and establish areas of support and resistance.

In addition, it can be used as a simple stand-alone forecasting method to identify trend direction and trend reversal points. When the local polynomial is predicted to move up in the next time step, the color of the Moving Regression curve will be green. Otherwise, the color of the curve is red. This function is (de)activated using the Predict Trend Direction flag.

Selecting the model parameters:

The effects of the moving window Length and the Local Polynomial Degree are confounded. This allows for finding the optimal trade-off between noise (variance) and lag (bias). Higher Length and lower Polynomial Degree (such as 1, i.e. linear), will result in "smoother" time series but at the cost of greater lag. Increasing the Polynomial Degree to, for example, 2 (squared) while maintaining the Length will diminish the lag and thus compromise the noise-lag tradeoff.

Relation to other methods:

When the degree of the local polynomial is set to 0 (i.e., fitting data to a constant level), the Moving Regression time series exactly matches the Simple Moving Average of the same length.

Linear Regression ChannelHello Traders,

There are several nice Linear Regression Channel scripts in the Public Library. and I tried to make one with some extra features too. This one can check if the Price breaks the channel and it shows where is was broken. Also it checks the momentum of the channel and shows it's increasing/decreasing/equal in a label, shape of the label also changes. The line colors change according to direction.

using the options, you can;

- Set the Source (Close, HL2 etc)

- Set the Channel length

- Set Deviation

- Change Up/Down Line colors

- Show/hide broken channels

- Change line width

meaning of arrows:

⇑ : Uptrend and moment incresing

⇗ : Uptrend and moment decreasing

⇓ : Downtrend and moment incresing

⇘ : Downtrend and moment decreasing

⇒ : No trend

An example for how color of lines, arrow direction and shape of label change.

Enjoy!

ProjectionGreetings Traders! I have decided to release a few scripts as open-source as I'm sure others can benefit from them and perhaps make them better.(Be sure to check my Profile for the other scripts as well: www.tradingview.com).

This one is called Projection.

Projection is based off the same Principle as some of my other scripts, such as Trade Manager() and Price Predictor(). I use a simple concept using line.new() to define some potential Price Projections. From the Settings of the Indicator, you can access a couple different Pre-Set options.

Wide Parabola:

Skinny Parabola:

Straight Triangle:

ZigZag1:

ZigZag2:

I wanted to give a Special Thanks to @Pinecoders for the custom RoundToTick Function from Backtesting/Trading Engine --> ()

If you like Projection, be sure to Like, Follow, and if you have any questions, don't be afraid to drop a comment below.

Let it snow... [QuantNomad]It's almost the end of 2020. If you don't have any snow outside but still you want some Christmas mood - feel free to use my indicator.

TradingView added a possibility to use up to 500 labels, so I decided to create something fun and completely useless.

Snowflakes suppose to fall nicely, but labels are not regularly updated by TradingView. If you know how to make it better - let me know )

For the best experience use Dark Theme and play the "Let it snow" song )

Merry Christmas & Happy New Year!

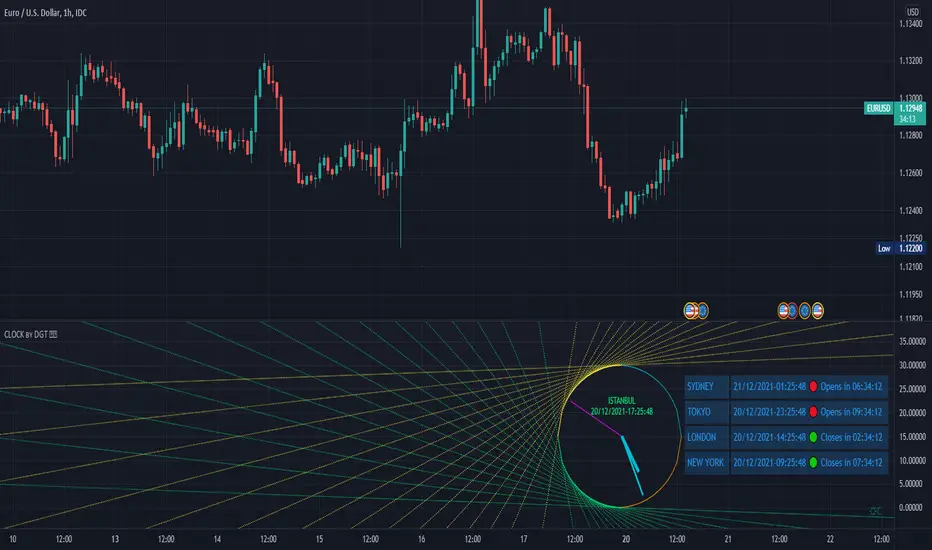

Analog/Digital World Clock by DGTWorld Clocks - something for fun

Happy New Year!

ps: in case no update on the charts then the clock will not update too and will lag or stop till a new update is received

Machine Learning: kNN-based StrategykNN-based Strategy (FX and Crypto)

Description:

This strategy uses a classic machine learning algorithm - k Nearest Neighbours (kNN) - to let you find a prediction for the next (tomorrow's, next month's, etc.) market move. Being an unsupervised machine learning algorithm, kNN is one of the most simple learning algorithms.

To do a prediction of the next market move, the kNN algorithm uses the historic data, collected in 3 arrays - feature1, feature2 and directions, - and finds the k-nearest

neighbours of the current indicator(s) values.

The two dimensional kNN algorithm just has a look on what has happened in the past when the two indicators had a similar level. It then looks at the k nearest neighbours,

sees their state and thus classifies the current point.

The kNN algorithm offers a framework to test all kinds of indicators easily to see if they have got any *predictive value*. One can easily add cog, wpr and others.

Note: TradingViews's playback feature helps to see this strategy in action.

Warning: Signals ARE repainting.

Style tags: Trend Following, Trend Analysis

Asset class: Equities, Futures, ETFs, Currencies and Commodities

Dataset: FX Minutes/Hours+++/Days

Indices Sector SigmaSpikes█ OVERVIEW

“The benchmark Dow Jones Industrial Average is off nearly 300 points as of midday today...”

“So what? Is that a lot or a little? Should we care?”

-Adam H Grimes-

This screener aims to provide Bird-Eye view across sector indices, to find which sector is having significant or 'out-of-norm' move in either direction.

The significance of the move is measured based on Sigma Spikes, a method proposed by Adam H. Grimes, where Standard Deviation of returns used as a baseline.

*You can google his blog or read his book, got some gold in there, especially on how he use indicators for trading

█ Understanding Sigma Spikes

As described by Grimes, moves in markets are only meaningful when we consider what “normal” is for that market.

Without that baseline, the daily change number, and even the percent change on the day doesn’t really mean much.

To overcome that problem, Sigma Spikes, as a measure of volatility, attempt to put todays change in price (aka return) in context of the standard deviation of 20 days daily's return.

Refer chart below:

1. The blue bars refer to each days return

2. The orange line is 1 time standard deviation of past 20days daily's return (today not included)

3. The red line is 2 time standard deviation of past 20days daily's return (today not included)

Using the ratio of today's return over the Std Deviation, determining your threshold (1,2,3,etc) will be the key that tells if today's move is significant or not.

*Threshold referring to times standard deviation, and different market may require different threshold.

*20 Days period are based on the Lookback Period, adjustable from user input window.

█ Features

- Scan up to 13 symbols at a time (Bursa (MYX) indices are defaulted, but you may change to any symbols/index from the user input setting)

█ Limitation

- Due to multiple use of security() function required to call other symbols, expect the screener to be slow at certain times

- Custom Timeframe currently accept only Daily and Weekly. I'll try to include lower timeframe in the next update

█ Disclaimer

Past performance is not an indicator of future results.

My opinions and research are my own and do not constitute financial advice in any way whatsoever.

Nothing published by me constitutes an investment recommendation, nor should any data or Content published by me be relied upon for any investment/trading activities.

I strongly recommends that you perform your own independent research and/or speak with a qualified investment professional before making any financial decisions.

Any ideas to further improve this indicator are welcome :)

Black-Scholes Options Pricing ModelThis is an updated version of my "Black-Scholes Model and Greeks for European Options" indicator, that i previously published. I decided to make this updated version open-source, so people can tweak and improve it.

The Black-Scholes model is a mathematical model used for pricing options. From this model you can derive the theoretical fair value of an options contract. Additionally, you can derive various risk parameters called Greeks. This indicator includes three types of data: Theoretical Option Price (blue), the Greeks (green), and implied volatility (red); their values are presented in that order.

1) Theoretical Option Price:

This first value gives only the theoretical fair value of an option with a given strike based on the Black-Scholes framework. Remember this is a model and does not reflect actual option prices, just the theoretical price based on the Black-Scholes model and its parameters and assumptions.

2)Greeks (all of the Greeks included in this indicator are listed below):

a)Delta is the rate of change of the theoretical option price with respect to the change in the underlying's price. This can also be used to approximate the probability of your option expiring in the money. For example, if you have an option with a delta of 0.62, then it has about a 62% chance of expiring in-the-money. This number runs from 0 to 1 for Calls, and 0 to -1 for Puts.

b)Gamma is the rate of change of delta with respect to the change in the underlying's price.

c)Theta, aka "time decay", is the rate of change in the theoretical option price with respect to the change in time. Theta tells you how much an option will lose its value day by day.

d) Vega is the rate of change in the theoretical option price with respect to change in implied volatility .

e)Rho is the rate of change in the theoretical option price with respect to change in the risk-free rate. Rho is rarely used because it is the parameter that options are least effected by, it is more useful for longer term options, like LEAPs.

f)Vanna is the sensitivity of delta to changes in implied volatility . Vanna is useful for checking the effectiveness of delta-hedged and vega-hedged portfolios.

g)Charm, aka "delta decay", is the instantaneous rate of change of delta over time. Charm is useful for monitoring delta-hedged positions.

h)Vomma measures the sensitivity of vega to changes in implied volatility .

i)Veta measures the rate of change in vega with respect to time.

j)Vera measures the rate of change of rho with respect to implied volatility .

k)Speed measures the rate of change in gamma with respect to changes in the underlying's price. Speed can be used when evaluating delta-hedged and gamma hedged portfolios.

l)Zomma measures the rate of change in gamma with respect to changes in implied volatility . Zomma can be used to evaluate the effectiveness of a gamma-hedged portfolio.

m)Color, aka "gamma decay", measures the rate of change of gamma over time. This can also be used to evaluate the effectiveness of a gamma-hedged portfolio.

n)Ultima measures the rate of change in vomma with respect to implied volatility .

o)Probability of Touch, is not a Greek, but a metric that I included, which tells you the probability of price touching your strike price before expiry.

3) Implied Volatility:

This is the market's forecast of future volatility . Implied volatility is directionless, it cannot be used to forecast future direction. All it tells you is the forecast for future volatility.

How to use this indicator:

1st. Input the strike price of your option. If you input a strike that is more than 3 standard deviations away from the current price, the model will return a value of n/a.

2nd. Input the current risk-free rate.(Including this is optional, because the risk-free rate is so small, you can just leave this number at zero.)

3rd. Input the time until expiry. You can enter this in terms of days, hours, and minutes.

4th.Input the chart time frame you are using in terms of minutes. For example if you're using the 1min time frame input 1, 4 hr time frame input 480, daily time frame input 1440, etc.

5th. Pick what style of option you want data for, European Vanilla or Binary.

6th. Pick what type of option you want data for, Long Call or Long Put.

7th . Finally, pick which Greek you want displayed from the drop-down list.

*Remember the Option price presented, and the Greeks presented, are theoretical in nature, and not based upon actual option prices. Also, remember the Black-Scholes model is just a model based upon various parameters, it is not an actual representation of reality, only a theoretical one.

*Note 1. If you choose binary, only data for Long Binary Calls will be presented. All of the Greeks for Long Binary Calls are available, except for rho and vera because they are negligible.

*Note 2. Unlike vanilla european options, the delta of a binary option cannot be used to approximate the probability of the option expiring in-the-money. For binary options, if you want to approximate the probability of the binary option expiring in-the-money, use the price. The price of a binary option can be used to approximate its probability of expiring in-the-money. So if a binary option has a price of $40, then it has approximately a 40% chance of expiring in-the-money.

*Note 3. As time goes on you will have to update the expiry, this model does not do that automatically. So for example, if you originally have an option with 30 days to expiry, tomorrow you would have to manually update that to 29 days, then the next day manually update the expiry to 28, and so on and so forth.

There are various formulas that you can use to calculate the Greeks. I specifically chose the formulations included in this indicator because the Greeks that it presents are the closest to actual options data. I compared the Greeks given by this indicator to brokerage option data on a variety of asset classes from equity index future options to FX options and more. Because the indicator does not use actual option prices, its Greeks do not match the brokerage data exactly, but are close enough.

I may try to make future updates that include data for Long Binary Puts, American Options, Asian Options, etc.

Screener - Mean Reversion Channel█ OVERVIEW

This is Screener script for Mean Reversion Channel Indicator

█ Description & How To Use

The screener works by scanning through up to 40 symbols and list down symbols that are currently within Overbought/Oversold Zone as defined by Mean Reversion Channel indicator.

The Overbought/Oversold Zone are further categorized and sorted by:

Strong : Indicated by "(Strong)" next to the symbol name

Normal : Indicated by the absence of "(Strong)" or "(Weak)" next to the symbol name

Weak : Indicated by "(Weak)" next to the symbol name

Notes: Refer to chart above to see how the Zone are categorized.

Notes: If the screener displays "Nothing Interesting". It simply means none of the screened assets are within the Overbought/Oversold Zone.

█ Features

- Scan up to 40 symbols at a time (By default, no asset is define. Once configured all the symbols you required, remember to save as default to save you from pain of configuring it again in the future)

- Options to scan by zones

- Custom Timeframe

█ Limitation

Due to multiple use of security() function required to call other symbols, expect the screener to be slow at certain times

█ Disclaimer

Past performance is not an indicator of future results.

My opinions and research are my own and do not constitute financial advice in any way whatsoever.

Nothing published by me constitutes an investment recommendation, nor should any data or Content published by me be relied upon for any investment/trading activities.

I strongly recommends that you perform your own independent research and/or speak with a qualified investment professional before making any financial decisions.

Any ideas to further improve this indicator are welcome :)

Credit: QuantNomad for his script idea on custom screener

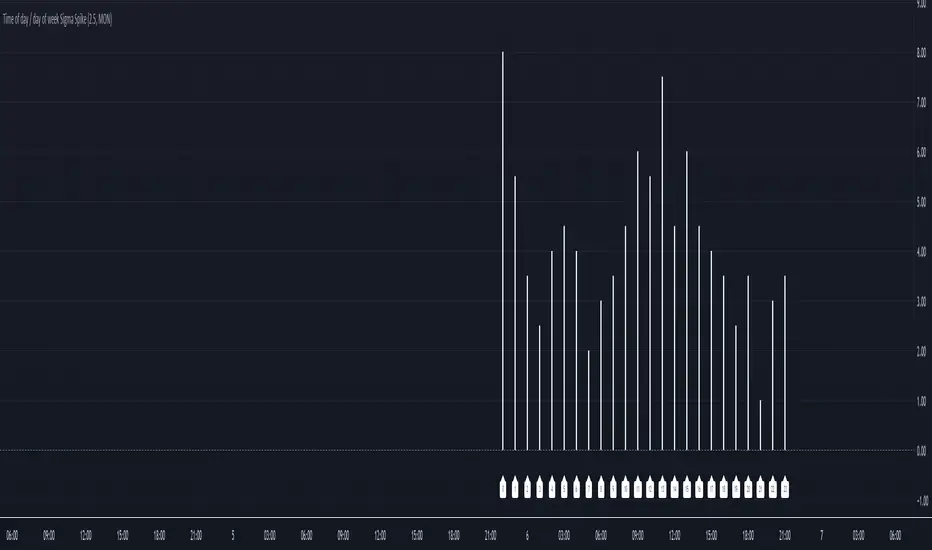

Time of day / day of week Sigma SpikeThis is a follow on from this script

Allows a further breakdown and examination of Sigma spikes by hour of the day or hour of the day & day of the week.

For simplicity it MUST be used on H1 chart.

Divergence for Many Indicators v4Hello Traders,

Here is my new year gift for the community, Digergence for Many Indicators v4 . I tried to make it modular and readable as much as I can. Thanks to Pine Team for improving Pine Platform all the time!

How it works?

- On each candle it checks divergences between current and any of last 16 Pivot Points for the indicators.

- it search divergence on choisen indicators => RSI , MACD , MACD Histogram, Stochastic , CCI , Momentum, OBV, VWMACD, CMF and any External Indicator !

- it checks following divergences for 16 pivot points that is in last 100 bars for each Indicator.

--> Regular Positive Digergences

--> Regular Negative Digergences

--> Hidden Positive Digergences

--> Hidden Negative Digergences

- for positive divergences first it checks if closing price is higher than last closing price and indicator value is higher than perious value, then start searching divergence

- for negative divergences first it checks if closing price is lower than last closing price and indicator value is lower than perious value, then start searching divergence

Some Options:

Pivot Period: you set Pivot Period as you wish. you can see Pivot Points using "Show Pivot Points" option

Source for Pivot Points: you can use Close or High/Low as source

Divergence Type: you can choose Divergence type to be shown => "Regular", "Hidden", "Regular/Hidden"

Show Indicator Names: you have different options to show indicator names => "Full", "First Letter", "Don't Show"

Show Divergence Number: option to see number of indicators which has Divergence

Show Only Last Divergence : if you enable this option then it shows only last Positive and Negative Divergences

you can include any External Indicator to see if there is divergence

- enable "Check External Indicator"

- and then choose External indicator name in the list, "External Indicator"

- External indicator name is shown as Extrn

- related external indicator must be added before enabling this option

Coloring, line width and line style options for different type of divergences.

Following Alerts added:

- Positive Regular Divergence Detected

- Negative Regular Divergence Detected

- Positive Hidden Divergence Detected

- Negative Hidden Divergence Detected

Now lets see some examples:

Hidden Divergences:

Regular and Hidden Divergences together:

Showing first letters of indicators:

You can see only the number of indicators which has divergence:

You can see only divergence lines without indicators names and numbers:

option to used different label/line/text colors:

You have option to see only last divergences:

You can change Pivot Period, in following example Pivot Period = 15:

You can use Close or High/Low as Source for Divergence

You can include external indicators and get divergences on it:

Wish you all a happy new year!

Enjoy!

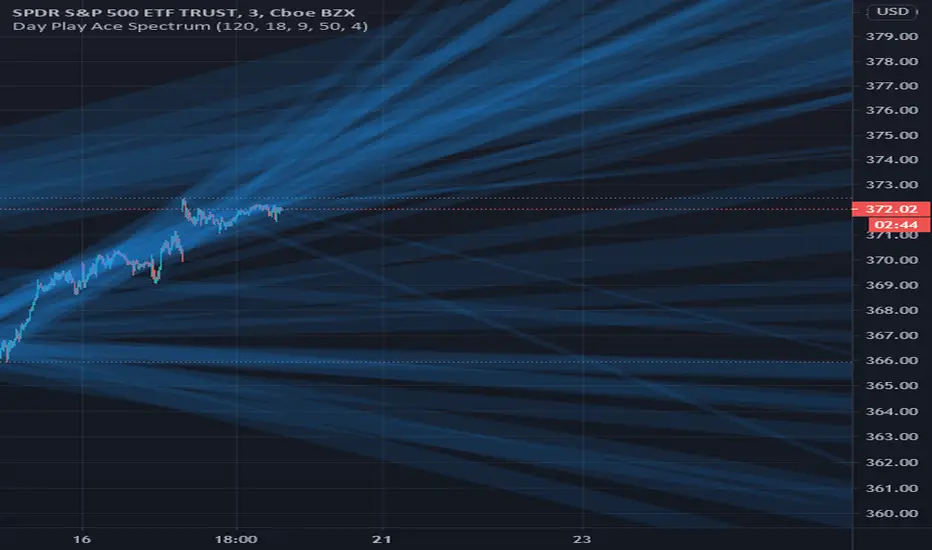

Daily Play Ace SpectrumSo the idea of the Daily Play Ace Spectrum is to extend the Ace Spectrum .

By exposing more parameters, making a variation of the Ace Spectrum which is more configurable.

The idea is this makes the Daily Play Ace Spectrum more suitable for use on shorter (hourly and minute) time scales.

These specific parameters exposed still maintain the original form of the original Ace Spectrum, but loosen up the hard coded assumptions of the original indicator.

By exposing more parameters this now makes the Daily Ace Spectrum more sensitive to input.

Meaning the parameters you choose are important and will set the characteristic reaction of the indicator to the series you give it.

This presents a trade-off, the simplicity of the original indicator is sacrificed.

But what's gained is a more comprehensive indicator that now needs more careful parameter adjustment .

Related to the Ace Spectrum:

MTF Oscillator Framework [PineCoders]This framework allows Pine coders to quickly build a complete multi-timeframe oscillator from any calculation producing values around a centerline, whether the values are bounded or not. Insert your calculation in the script and you have a ready-to-publish MTF Oscillator offering a plethora of presentation options and features.

█ HOW TO USE THE FRAMEWORK

1 — Insert your calculation in the `f_signal()` function at the top of the "Helper Functions" section of the script.

2 — Change the script's name in the `study()` declaration statement and the `alertcondition()` text in the last part of the "Plots" section.

3 — Adapt the default value used to initialize the CENTERLINE constant in the script's "Constants" section.

4 — If you want to publish the script, copy/paste the following description in your new publication's description and replace the "OVERVIEW" section with a description of your calculations.

5 — Voilà!

═════════════════════════════════════════════════════════════════════════

█ OVERVIEW

This oscillator calculates a directional value of True Range. When a bar is up, the positive value of True Range is used. A negative value is used when the bar is down. When there is no movement during the bar, a zero value is generated, even if True Range is different than zero. Because the unit of measure of True Range is price, the oscillator is unbounded (it does not have fixed upper/lower bounds).

True Range can be used as a metric for volatility, but by using a signed value, this oscillator will show the directional bias of progressively increasing/decreasing volatility, which can make it more useful than an always positive value of True Range.

The True Range calculation appeared for the first time in J. Welles Wilder's New Concepts in Technical Trading Systems book published in 1978. Wilder's objective was to provide a reliable measure of the effective movement—or range—between two bars, to measure volatility. True Range is also the building block used to calculate ATR (Average True Range), which calculates the average of True Range values over a given period using the `rma` averaging method—the same used in the calculation of another of Wilder's remarkable creations: RSI.

█ CONCEPTS

This oscillator's design stems from a few key concepts.

Relative Levels

Other than the centerline, relative rather than absolute levels are used to identify levels of interest. Accordingly, no fixed levels correspond to overbought/oversold conditions. Relative levels of interest are identified using:

• A Donchian channel (historical highs/lows).

• The oscillator's position relative to higher timeframe values.

• Oscillator levels following points in time where a divergence is identified.

Higher timeframes

Two progressively higher timeframes are used to calculate larger-context values for the oscillator. The rationale underlying the use of timeframes higher than the chart's is that, while they change less frequently than the values calculated at the chart's resolution, they are more meaningful because more work (trader activity) is required to calculate them. Combining the immediacy of values calculated at the chart's resolution to higher timeframe values achieves a compromise between responsiveness and reliability.

Divergences as points of interest rather than directional clues

A very simple interpretation of what constitutes a divergence is used. A divergence is defined as a discrepancy between any bar's direction and the direction of the signal line on that same bar. No attempt is made to attribute a directional bias to divergences when they occur. Instead, the oscillator's level is saved and subsequent movement of the oscillator relative to the saved level is what determines the bullish/bearish state of the oscillator.

Conservative coloring scheme

Several additive coloring conditions allow the bull/bear coloring of the oscillator's main line to be restricted to specific areas meeting all the selected conditions. The concept is built on the premise that most of the time, an oscillator's value should be viewed as mere noise, and that somewhat like price, it only occasionally conveys actionable information.

█ FEATURES

Plots

• Three lines can be plotted. They are named Main line , Line 2 and Line 3 . You decide which calculation to use for each line:

• The oscillator's value at the chart's resolution.

• The oscillator's value at a medium timeframe higher than the chart's resolution.

• The oscillator's value at the highest timeframe.

• An aggregate line calculated using a weighed average of the three previous lines (see the Aggregate Weights section of Inputs to configure the weights).

• The coloring conditions, divergence levels and the Hi/Lo channel always apply to the Main line, whichever calculation you decide to use for it.

• The color of lines 2 and 3 are fixed but can be set in the "Colors" section of Inputs.

• You can change the thickness of each line.

• When the aggregate line is displayed, higher timeframe values are only used in its calculation when they become available in the chart's history,

otherwise the aggregate line would appear much later on the chart. To indicate when each higher timeframe value becomes available,

a small label appears near the centerline.

• Divergences can be shown as small dots on the centerline.

• Divergence levels can be shown. The level and fill are determined by the oscillator's position relative to the last saved divergence level.

• Bull/bear markers can be displayed. They occur whenever a new bull/bear state is determined by the "Main Line Coloring Conditions".

• The Hi/Lo (Donchian) channel can be displayed, and its period defined.

• The background can display the state of any one of 11 different conditions.

• The resolutions used for the higher timeframes can be displayed to the right of the last bar's value.

• Four key values are always displayed in the Data Window (fourth icon down to the right of your chart):

oscillator values for the chart, medium and highest timeframes, and the oscillator's instant value before it is averaged.

Main Line Coloring Conditions

• Nine different conditions can be selected to determine the bull/bear coloring of the main line. All conditions set to "ON" must be met to determine the bull/bear state.

• A volatility state can also be used to filter the conditions.

• When the coloring conditions and the filter do not allow for a bull/bear state to be determined, the neutral color is used.

Signal

• Seven different averages can be used to calculate the average of the oscillator's value.

• The average's period can be set. A period of one will show the instant value of the oscillator,

provided you don't use linear regression or the Hull MA as they do not work with a period of one.

• An external signal can be used as the oscillator's instant value. If an already averaged external value is used, set the period to one in this indicator.

• For the cases where an external signal is used, a centerline value can be set.

Higher Timeframes

• The two higher timeframes are named Medium timeframe and Highest timeframe . They can be determined using one of three methods:

• Auto-steps: the higher timeframes are determined using the chart's resolution. If the chart uses a seconds resolution, for example,

the medium and highest resolutions will be 15 and 60 minutes.

• Multiples: the timeframes are calculated using a multiple of the chart's resolution, which you can set.

• Fixed: the set timeframes do not change with the chart's resolution.

Repainting

• Repainting can be controlled separately for the chart's value and the higher timeframe values.

• The default is a repainting chart value and non-repainting higher timeframe values. The Aggregate line will thus repaint by default,

as it uses the chart's value along with the higher timeframes values.

Aggregate Weights

• The weight of each component of the Aggregate line can be set.

• The default is equal weights for the three components, meaning that the chart's value accounts for one third of the weight in the Aggregate.

High Volatility

• This provides control over the volatility filter used in the Main line's coloring conditions and the background display.

• Volatility is determined to be high when the short-term ATR is greater than the long-term ATR.

Colors

• You can define your own colors for all of the oscillator's plots.

• The default colors will perform well on both white and black chart backgrounds.

Alerts

• An alert can be defined for the script. The alert will trigger whenever a bull/bear marker appears in the indicator's display.

The particular combination of coloring conditions and the display of bull/bear markers when you create the alert will thus determine when the alert triggers.

Once the alerts are created, subsequent changes to the conditions controlling the display of markers will not affect the existing alert(s).

• You can create multiple alerts from this script, each triggering on different conditions.

Backtesting & Trading Engine Signal Line

• An invisible plot named "BTE Signal" is provided. It can be used as an entry signal when connected to the PineCoders Backtesting & Trading Engine as an external input.

It will generate an entry whenever a marker is displayed.

Look first. Then leap.

Moving Average EntanglementThis script uses the gap in moving averages standardized to the average true range to determine entry and exit points.

The red line represents the current percentage of ATR that is deemed "The Dead Zone" - a move that is too small to be reliable.

The histogram represents the gap between moving averages. When the histogram is above the red line, it confirms a breakout move.

The dashed line an be used as a secondary filter and is a moving average of the histogram.

When Standard Deviation mode is on, a third line is displayed, which represents how many standard Deviations the current histogram bar represents, and can be also used as a filter.

Sigma Spike Filtered Binned OPR ( Adam H. Grimes )As originally described by Adam H. Grimes.

For analyzing the location of Open within the day's range (OPR). The OPR histogram displays the binned distribution of OPR values for the chart history. Fat tails at the extremes indicates that Open occurred more often close to the day's high or low.

The OPR results are filtered according to volatility using Grime's Sigma Spike. So that OPR values are only recorded when volatility exceeds a threshold (relative high range days).

This may (strong emphasis on may) indicate the opportunity for trades early in the day on days that begin with a high amount of relative volatility and trading with the direction that price is moving away from the open.

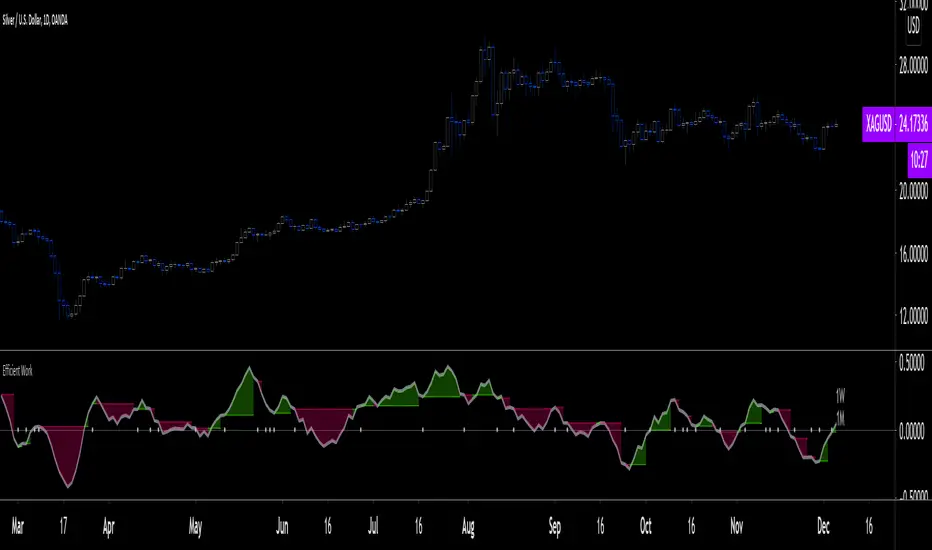

Efficient Work [LucF]█ OVERVIEW

Efficient Work measures the ratio of price movement from close to close ( resulting work ) over the distance traveled to the high and low before settling down at the close ( total work ). The closer the two values are, the more Efficient Work approaches its maximum value of +1 for an up move or -1 for a down move. When price does not change, Efficient Work is zero.

Higher values of Efficient Work indicate more efficient price travel between the close of two successive bars, which I interpret to be more significant, regardless of the move's amplitude. Because it measures the direction and strength of price changes rather than their amplitude, Efficient Work may be thought of as a sentiment indicator.

█ CONCEPTS

This oscillator's design stems from a few key concepts.

Relative Levels

Other than the centerline, relative rather than absolute levels are used to identify levels of interest. Accordingly, no fixed levels correspond to overbought/oversold conditions. Relative levels of interest are identified using:

• A Donchian channel (historical highs/lows).

• The oscillator's position relative to higher timeframe values.

• Oscillator levels following points in time where a divergence is identified.

Higher timeframes

Two progressively higher timeframes are used to calculate larger-context values for the oscillator. The rationale underlying the use of timeframes higher than the chart's is that, while they change less frequently than the values calculated at the chart's resolution, they are more meaningful because more work (trader activity) is required to calculate them. Combining the immediacy of values calculated at the chart's resolution to higher timeframe values achieves a compromise between responsiveness and reliability.

Divergences as points of interest rather than directional clues

A very simple interpretation of what constitutes a divergence is used. A divergence is defined as a discrepancy between any bar's direction and the direction of the signal line on that same bar. No attempt is made to attribute a directional bias to divergences when they occur. Instead, the oscillator's level is saved and subsequent movement of the oscillator relative to the saved level is what determines the bullish/bearish state of the oscillator.

Conservative coloring scheme

Several additive coloring conditions allow the bull/bear coloring of the oscillator's main line to be restricted to specific areas meeting all the selected conditions. The concept is built on the premise that most of the time, an oscillator's value should be viewed as mere noise, and that somewhat like price, it only occasionally conveys actionable information.

█ FEATURES

Plots

• Three lines can be plotted. They are named Main line , Line 2 and Line 3 . You decide which calculation to use for each line:

• The oscillator's value at the chart's resolution.

• The oscillator's value at a medium timeframe higher than the chart's resolution.

• The oscillator's value at the highest timeframe.

• An aggregate line calculated using a weighed average of the three previous lines (see the Aggregate Weights section of Inputs to configure the weights).

• The coloring conditions, divergence levels and the Hi/Lo channel always apply to the Main line, whichever calculation you decide to use for it.

• The color of lines 2 and 3 are fixed but can be set in the "Colors" section of Inputs.

• You can change the thickness of each line.

• When the aggregate line is displayed, higher timeframe values are only used in its calculation when they become available in the chart's history,

otherwise the aggregate line would appear much later on the chart. To indicate when each higher timeframe value becomes available,

a small label appears near the centerline.

• Divergences can be shown as small dots on the centerline.

• Divergence levels can be shown. The level and fill are determined by the oscillator's position relative to the last saved divergence level.

• Bull/bear markers can be displayed. They occur whenever a new bull/bear state is determined by the "Main Line Coloring Conditions".

• The Hi/Lo (Donchian) channel can be displayed, and its period defined.

• The background can display the state of any one of 11 different conditions.

• The resolutions used for the higher timeframes can be displayed to the right of the last bar's value.

• Four key values are always displayed in the Data Window (fourth icon down to the right of your chart):

oscillator values for the chart, medium and highest timeframes, and the oscillator's instant value before it is averaged.

Main Line Coloring Conditions

• Nine different conditions can be selected to determine the bull/bear coloring of the main line. All conditions set to "ON" must be met to determine the bull/bear state.

• A volatility state can also be used to filter the conditions.

• When the coloring conditions and the filter do not allow for a bull/bear state to be determined, the neutral color is used.

Signal

• Seven different averages can be used to calculate the average of the oscillator's value.

• The average's period can be set. A period of one will show the instant value of the oscillator,

provided you don't use linear regression or the Hull MA as they do not work with a period of one.

• An external signal can be used as the oscillator's instant value. If an already averaged external value is used, set the period to one in this indicator.

• For the cases where an external signal is used, a centerline value can be set.

Higher Timeframes

• The two higher timeframes are named Medium timeframe and Highest timeframe . They can be determined using one of three methods:

• Auto-steps: the higher timeframes are determined using the chart's resolution. If the chart uses a seconds resolution, for example,

the medium and highest resolutions will be 15 and 60 minutes.

• Multiples: the timeframes are calculated using a multiple of the chart's resolution, which you can set.

• Fixed: the set timeframes do not change with the chart's resolution.

Repainting

• Repainting can be controlled separately for the chart's value and the higher timeframe values.

• The default is a repainting chart value and non-repainting higher timeframe values. The Aggregate line will thus repaint by default,

as it uses the chart's value along with the higher timeframes values.

Aggregate Weights

• The weight of each component of the Aggregate line can be set.

• The default is equal weights for the three components, meaning that the chart's value accounts for one third of the weight in the Aggregate.

High Volatility

• This provides control over the volatility filter used in the Main line's coloring conditions and the background display.

• Volatility is determined to be high when the short-term ATR is greater than the long-term ATR.

Colors

• You can define your own colors for all of the oscillator's plots.

• The default colors will perform well on both white and black chart backgrounds.

Alerts

• An alert can be defined for the script. The alert will trigger whenever a bull/bear marker appears in the indicator's display.

The particular combination of coloring conditions and the display of bull/bear markers when you create the alert will thus determine when the alert triggers.

Once the alerts are created, subsequent changes to the conditions controlling the display of markers will not affect the existing alert(s).

• You can create multiple alerts from this script, each triggering on different conditions.

Backtesting & Trading Engine Signal Line

• An invisible plot named "BTE Signal" is provided. It can be used as an entry signal when connected to the PineCoders Backtesting & Trading Engine as an external input.

It will generate an entry whenever a marker is displayed.

█ NOTES

• I do not know for sure if the calculations in Efficient Work are original. I apologize if they are not.

• Because this version of Efficient Work only has access to OHLC information, it cannot measure the total distance traveled through all of a bar's ticks, but the indicator nonetheless behaves in a manner consistent with the intentions underlying its design.

For Pine coders

This code was written using the following standards:

• The PineCoders Coding Conventions for Pine .

• A modified version of the PineCoders MTF Oscillator Framework and MTF Selection Framework .