Full‑Featured Multi‑Signal Strategy By Andi TanThis is my first strategy indicator, please try the backtest and use it, hopefully it will be useful

Циклический анализ

Bitcoin NUPL IndicatorThe Bitcoin NUPL (Net Unrealized Profit/Loss) Indicator is a powerful metric that shows the difference between Bitcoin's market cap and realized cap as a percentage of market cap. This indicator helps identify different market cycle phases, from capitulation to euphoria.

// How It Works

NUPL measures the aggregate profit or loss held by Bitcoin investors, calculated as:

```

NUPL = ((Market Cap - Realized Cap) / Market Cap) * 100

```

// Market Cycle Phases

The indicator automatically color-codes different market phases:

• **Deep Red (< 0%)**: Capitulation Phase - Most coins held at a loss, historically excellent buying opportunities

• **Orange (0-25%)**: Hope & Fear Phase - Early accumulation, price uncertainty and consolidation

• **Yellow (25-50%)**: Optimism & Anxiety Phase - Emerging bull market, increasing confidence

• **Light Green (50-75%)**: Belief & Denial Phase - Strong bull market, high conviction

• **Bright Green (> 75%)**: Euphoria & Greed Phase - Potential market top, historically good profit-taking zone

// Features

• Real-time NUPL calculation with customizable smoothing

• RSI indicator for additional momentum confirmation

• Color-coded background reflecting current market phase

• Reference lines marking key transition zones

• Detailed metrics table showing NUPL value, market sentiment, market cap, realized cap, and RSI

// Strategy Applications

• **Long-term investors**: Use extreme negative NUPL values (deep red) to identify potential bottoms for accumulation

• **Swing traders**: Look for transitions between phases for potential trend changes

• **Risk management**: Consider taking profits when entering the "Euphoria & Greed" phase (bright green)

• **Mean reversion**: Watch for overbought/oversold conditions when NUPL reaches historical extremes

// Settings

• **RSI Length**: Adjusts the period for RSI calculation

• **NUPL Smoothing Length**: Applies moving average smoothing to reduce noise

// Notes

• Premium TradingView subscription required for Glassnode and Coin Metrics data

• Best viewed on daily timeframes for macro analysis

• Historical NUPL extremes have often marked cycle bottoms and tops

• Use in conjunction with other indicators for confirmation

4H Color Sync for 15m, 30m, 90m, 1H4H Time Theory Session Colour Sync

- session colour sync to lower timeframes

- highlighting the sessions of 4h candles

- using the fractal nature of 4h time theory and applying it to the 1h/15m/5m/1m chart

- option to change the colours of 3 PAIRS for the 4h timeframe candles

- automatically syncs to your timezone

Vinicius Setup ATR

Description:

This script is a strategy based on the Supertrend indicator combined with volume analysis, candle strength, and RSI. Its goal is to identify potential entry points for buy and sell trades based on technical criteria, without promising profitability or guaranteed results.

Script Components:

Supertrend: Used as the main trend compass. When the trend is positive (direction = 1), buy signals are considered; when negative (direction = -1), sell signals are considered.

Volume: Entries are only validated if the volume is above the average of the last 20 candles, adjusted with a 1.2 multiplier.

Candle Body: The candle body must be larger than a certain percentage of the ATR, ensuring sufficient strength and volatility.

RSI: Used as a filter to avoid trades in extreme overbought or oversold zones.

Support and Resistance: Identified based on simple pivots (5 periods before and after).

Customizable Parameters:

ATR Length and Multiplier: Controls the sensitivity of the Supertrend.

RSI Period: Adjusts the relative strength filter.

Minimum Volume and Candle Body: Settings to validate entry signals.

Entry Conditions:

Buy: Positive trend + strong candle + high volume + RSI below 70.

Sell: Negative trend + strong candle + high volume + RSI above 30.

Exit Conditions:

The trade is closed upon the appearance of an opposite signal.

Notes:

This is a technical system with no profit guarantees.

It is recommended to test with realistic capital values and parameters suited to your risk management.

The script is not optimized for specific profitability, but rather to support study and the construction of setups with objective criteria.

Time Cycles# New York Time Cycles Indicator

## Overview

The Time Cycles indicator is a specialized technical analysis tool designed to divide the trading day into distinct time blocks based on New York trading hours. Developed for TradingView, this indicator helps traders identify and analyze market behavior during specific time periods throughout the trading session. The indicator displays six consecutive time blocks, each representing 90-minute segments of the trading day, while tracking price ranges within each block.

## Core Concept

The Time Cycles indicator is built on the premise that different periods during the trading day often exhibit unique market characteristics and behaviors. By segmenting the trading day into standardized 90-minute blocks, traders can:

1. Identify recurring patterns at specific times of day

2. Compare price action across different time blocks

3. Recognize potential support and resistance levels based on the high and low of previous time blocks

4. Develop time-based trading strategies specific to certain market hours

## Time Block Structure

The indicator divides the trading day into six sequential 90-minute blocks based on New York time:

1. **Box 1**: 07:00 - 08:30 ET

2. **Box 2**: 08:30 - 10:00 ET

3. **Box 3**: 10:00 - 11:30 ET

4. **Box 4**: 11:30 - 13:00 ET

5. **Box 5**: 13:00 - 14:30 ET

6. **Box 6**: 14:30 - 16:00 ET

These time blocks cover the core US trading session from pre-market into regular market hours.

## Visual Representation

Each time block is represented on the chart as a visual box that:

- Spans the exact time period of the block (horizontally)

- Extends from the highest high to the lowest low recorded during that time period (vertically)

- Is displayed with customizable colors and transparency levels

- Automatically builds in real-time as price action develops

Additionally, the indicator draws dashed projection lines that:

- Display the high and low of the most recently completed time block

- Extend forward in time (for up to 24 hours)

- Help traders identify potential support and resistance levels

## Technical Implementation

The indicator employs several key technical features:

1. **Time Detection**: Accurately identifies the current New York time to place each box in the correct time period

2. **Dynamic Box Creation**: Initializes and updates boxes in real-time as price action develops

3. **Range Tracking**: Continuously monitors and adjusts the high and low of each active time block

4. **Projection Lines**: Creates horizontal dashed lines projecting the high and low of the most recently completed time block

5. **Daily Reset**: Automatically resets all boxes and lines at the start of each new trading day

6. **Customization**: Allows users to set custom colors and transparency levels for each time block

This Time Cycles indicator provides traders with a structured framework for analyzing intraday market movements based on specific time periods. By understanding how the market typically behaves during each 90-minute block, traders can develop more targeted strategies and potentially identify higher-probability trading opportunities throughout the trading day.

Market Open Options Strategytrades directionally whatever first 90 seconds of trading day are for either 10 minutes or a reversal whatever comes first

Global M2/M3 Liquidity IndexThis Indicator takes M3 data from 20 of the largest Central banks. M3 data is not available for USA and CHINA and has been substituted with M2.

Overall M3 captures far more than M2 and is therefore a superior model when attempting to track global liquidity.

This indicator also allows the data to be pushed forward to adjust for the lagged effect global liquidity has on markets.

The recommended lag is 90 days.

Lunar Cycle Tracker - (Moon + 3 Mercury Retrogrades)This script overlays the lunar and Mercury retrograde cycles directly onto your chart, helping traders visualize natural timing intervals that may influence market behavior.

Key Features:

🌑 New Moon & Full Moon Markers:

Vertical lines and labels indicate new and full moon events each month. You can fully customize their colors.

🌗 Last Quarter Moon Fill:

A soft pink background highlights the last quarter moon phase (from 7.4 days after the full moon to the next new moon).

🪐 Three Mercury Retrograde Zones:

Highlight up to three retrograde periods per year with customizable date inputs and background color. Great for spotting potential reversal or volatility windows.

Customization:

Moon event dates and colors

Manual input for Mercury retrograde periods (year, month, day)

Full compatibility with all timeframes (1H, 4H, daily, etc.)

Great for astro-cycle traders, Gann-based analysts, or anyone who respects time symmetry in the markets.

Fully customizable & works across all timeframes.

This tool was created by AngelArt as part of a larger astro-market model using lunar timing and planetary retrogrades for cycle-based market analysis.

No Trading ZoneNo trading zone

This indicator highlights the time range between 03:00 and 11:00 UTC as a "danger zone" for trading.

Based on data-driven backtesting, this period consistently showed:

- High frequency of moving average (MA) crossovers without meaningful trend

- A high concentration of sideways market conditions

- Increased likelihood of false breakouts and stop-loss hunting

On average, strong directional trends tend to emerge after 12:00 UTC, especially between 12:00–15:00 UTC.

Avoiding trades during this time zone can help reduce exposure to low-probability setups and enhance strategy reliability.

Prior sessions High/Low/MidThis indicator highlights the High, Low, and Midpoint of the most recently completed trading sessions. It helps traders visualize key price levels from the previous session that often act as support, resistance, or reaction zones.

It draws horizontal lines for the high and low of the last completed session, as well as the midpoint, which is calculated as the average of the high and low. These lines extend to the right side of the chart, remaining visible as reference levels throughout the day.

You can independently enable or disable the Tokyo, London, and New York sessions depending on your preferences. Each session has adjustable start and end times, as well as time zone settings, so you can align them accurately with your trading strategy.

This indicator is particularly useful for intraday and swing traders who use session-based levels to define market structure, bias, or areas of interest. Session highs and lows often align with institutional activity and can be key turning points in price action.

Please note that this script is designed to be used only on intraday timeframes such as 1-minute to 4-hour charts. It will not function on daily or higher timeframes.

Global M2 sandboxThis indicator aggregates global sources of liquidity to use as a proxy for the global money supply and allows an offsetting number of days to be implemented to use as a leading indicator.

// EUROZONE Data

EUM2D = request.security("ECONOMICS:EUM2*FX:EURUSD", "D", close, lookahead=barmerge.lookahead_on)

// North America Data

USM2D = request.security("ECONOMICS:USM2", "D", close, lookahead=barmerge.lookahead_on)

CAM2D = request.security("ECONOMICS:CAM2*FX_IDC:CADUSD", "D", close, lookahead=barmerge.lookahead_on)

// Non-EU Europe Data

CHM2D = request.security("ECONOMICS:CHM2*FX_IDC:CHFUSD", "D", close, lookahead=barmerge.lookahead_on)

GBM2D = request.security("ECONOMICS:GBM2*FX:GBPUSD", "D", close, lookahead=barmerge.lookahead_on)

FIPOP = request.security("ECONOMICS:FIM2/FX_IDC:USDFIM", "D", close, lookahead=barmerge.lookahead_on)

RUM2D = request.security("ECONOMICS:RUM2*FX_IDC:RUBUSD", "D", close, lookahead=barmerge.lookahead_on)

// Pacific Data

NZM2D = request.security("ECONOMICS:NZM2*FX_IDC:NZDUSD", "D", close, lookahead=barmerge.lookahead_on)

// Asia Data

CNM2D = request.security("ECONOMICS:CNM2*FX_IDC:CNYUSD", "D", close, lookahead=barmerge.lookahead_on)

TWM2D = request.security("ECONOMICS:TWM2*FX_IDC:TWDUSD", "D", close, lookahead=barmerge.lookahead_on)

HKM2D = request.security("ECONOMICS:HKM2*FX_IDC:HKDUSD", "D", close, lookahead=barmerge.lookahead_on)

INM2D = request.security("ECONOMICS:INM2*FX_IDC:INRUSD", "D", close, lookahead=barmerge.lookahead_on)

JPM2D = request.security("ECONOMICS:JPM2*FX_IDC:JPYUSD", "D", close, lookahead=barmerge.lookahead_on)

PHM2D = request.security("ECONOMICS:PHM2*FX_IDC:PHPUSD", "D", close, lookahead=barmerge.lookahead_on)

SGM2D = request.security("ECONOMICS:SGM2*FX_IDC:SGDUSD", "D", close, lookahead=barmerge.lookahead_on)

// Latin America Data

BRM2D = request.security("ECONOMICS:BRM2*FX_IDC:BRLUSD", "D", close, lookahead=barmerge.lookahead_on)

COM2D = request.security("ECONOMICS:COM2*FX_IDC:COPUSD", "D", close, lookahead=barmerge.lookahead_on)

MXM2D = request.security("ECONOMICS:MXM2*FX_IDC:MXNUSD", "D", close, lookahead=barmerge.lookahead_on)

// Middle East Data

AEM2D = request.security("ECONOMICS:AEM2*FX_IDC:AEDUSD", "D", close, lookahead=barmerge.lookahead_on)

TRM2D = request.security("ECONOMICS:TRM2*FX_IDC:TRYUSD", "D", close, lookahead=barmerge.lookahead_on)

// Africa Data

ZAM2D = request.security("ECONOMICS:ZAM2*FX_IDC:ZARUSD", "D", close, lookahead=barmerge.lookahead_on)

// Calculate Global Money Supply M2

total = (EUM2D + USM2D + CAM2D + CHM2D + GBM2D + FIPOP + RUM2D + NZM2D + CNM2D + TWM2D + HKM2D + INM2D + JPM2D + PHM2D + SGM2D + BRM2D + COM2D + MXM2D + AEM2D + TRM2D + ZAM2D) / 1000000000000

Oscura 23:00 - 00:00 (Italia)Hiding spread zone.

Usefull to hide zone where the broker make new contract and erase spread

Fractal Wave MarkerFractal Wave Marker is an indicator that processes relative extremes of fluctuating prices within 2 periodical aspects. The special labeling system detects and visually marks multi-scale turning points, letting you visualize fractal echoes within unfolding cycles dynamically.

What This Indicator Does

Identifies major and minor swing highs/lows based on adjustable period.

Uses Phi in power exponent to compute a higher-degree swing filter.

Labels of higher degree appear only after confirmed base swings — no phantom levels, no hindsight bias. What you see is what the market has validated.

Swing points unfold in a structured, alternating rhythm . No two consecutive pivots share the same hierarchical degree!

Inspired by the Fractal Market Hypothesis, this script visualizes the principle that market behavior repeats across time scales, revealing structured narrative of "random walk". This inherent sequencing ensures fractal consistency across timeframes. "Fractal echoes" demonstrate how smaller price swings can proportionally mirror larger ones in both structure and timing, allowing traders to anticipate movements by recursive patterns. Cycle Transitions highlight critical inflection points where minor pivots flip polarity such as a series of lower highs progress into higher highs—signaling the birth of a new macro trend. A dense dense clusters of swing points can indicate Liquidity Zones, acting as footprints of institutional accumulation or distribution where price action validates supply and demand imbalances.

Visualization of nested cycles within macro trend anchors - a main feature specifically designed for the chartists who prioritize working with complex wave oscillations their analysis.

Market Sessions by BASSWELLThis TradingView indicator visually highlights major global trading sessions (Tokyo, London, New York) directly on intraday charts. It provides a clear, color-coded display of session activity and key statistics to help traders better understand session dynamics and overlaps.

✅ Key Features:

Visual Session Boxes: Draws background boxes for each session with configurable colors.

Session Names: Displays the name of each session as a label above the session box.

Open/Close Lines: Optionally shows dashed lines at session open and close prices.

Average Price Line: Plots the average session price as a dotted line.

Tick Range Display: Calculates and shows the high-low range in ticks.

Time Zone Support: Fully timezone-aware via IANA definitions (e.g. "Europe/London").

Overlap Handling: Automatically dims older sessions when a new one starts for visual clarity.

🔧 Configurable Parameters:

Show/hide each session individually.

Set session times and timezones.

Customize label visibility and box contents.

Adjust session colors with transparency.

Includes basic visual styling for better chart readability.

⚠️ Note: Works only on intraday timeframes. Daily/weekly/monthly charts are not supported.

Opening Price Levels (by Period)This indicator draws clean horizontal lines at the opening prices of key time periods: Year, Quarter, Month, Week, and Day.

Each line is plotted only within its own time range, so there's no visual clutter or vertical jumps between periods.

Perfect for traders who want to:

Identify and react to institutional levels.

Track price behavior relative to major opens.

Keep charts clean and easy to read.

Features:

✅ Toggle visibility for each period (Year, Quarter, Month, Week, Day).

🎯 Accurate open levels, aligned with your chart's timeframe and session settings.

✨ Clean segments — each line only spans its original period.

Buffett Indicator (Wilshire 5000 / GDP)The Buffett Indicator (Wilshire 5000 / GDP) is a macroeconomic metric used to assess whether the U.S. stock market is overvalued or undervalued. It is calculated by dividing the total market capitalization (represented by the Wilshire 5000 Index) by the U.S. Gross Domestic Product (GDP). A value above 1 (or 100%) may indicate an overvalued market, while a value below 1 suggests potential undervaluation. This indicator is best suited for long-term investment analysis.

Triple StochasticTriple Stochastic Elasticity Indicator

This custom indicator leverages the power of multi-timeframe analysis by combining three Stochastic Oscillators across different timeframes to identify potential trade entries based on elasticity and divergence between momentum curves.

📊 How It Works:

The indicator plots Stochastic values from three timeframes (e.g., 5m, 15m, and 1h), allowing you to observe how momentum behaves at different scales.

It highlights moments of elasticity—where the Stochastics stretch apart and then begin to converge—potentially signaling a reversion opportunity or trend continuation.

By identifying these stretches and snapbacks in momentum alignment, you can better time your entries and exits with improved confidence.

🔍 Use Case:

Look for divergence or convergence between the Stochastics.

Ideal for trend-following entries, pullback setups, and momentum reversal spotting.

Works best when combined with price action, S/R zones, or volume confirmation.

🛠 Customization:

Timeframes for each Stochastic are fully customizable.

Options to tweak %K, %D, and smoothing values to fit your strategy.

I recommend to remove the D%

And set the following settings

5 : 3 : 3

14 : 3 : 3

56 : 12 :12

Visual alerts can be added for when certain conditions are met (e.g., all three Stochs cross overbought/oversold levels).

90-Day Beta to BTCOverview:

The 90-Day Beta to BTC indicator measures the volatility of a specific token relative to Bitcoin (BTC) over the past 90 days. Beta is a widely used statistical measure in financial markets that indicates how much a token's price moves in relation to BTC. A higher beta means the token is more volatile compared to BTC, while a lower beta means it is less volatile or moves similarly to BTC.

How It Works:

This indicator calculates the daily logarithmic returns of both the token and Bitcoin, then computes the covariance between their returns and the variance of Bitcoin’s returns. The resulting Beta value reflects the degree to which the token’s price fluctuates relative to Bitcoin's price over the past 90 days.

Beta > 1: The token is more volatile than Bitcoin, showing higher price swings.

Beta = 1: The token moves in lockstep with Bitcoin, exhibiting similar volatility.

Beta < 1: The token is less volatile than Bitcoin, showing smaller price fluctuations.

Beta = 0: The token's price movement is uncorrelated with Bitcoin’s price.

Negative Beta: The token moves opposite to Bitcoin, indicating an inverse relationship.

Use Case:

This indicator is particularly useful for traders or investors looking to identify tokens with high speculative volatility. Tokens with Beta values above 1 are typically high-risk, high-reward assets, often driven by hype, social trends, or market speculation. Conversely, tokens with Beta values below 1 offer a more stable price relationship with Bitcoin, making them less volatile and potentially safer.

In the context of a Trash Token Tournament, tokens with a higher Beta (greater than 1) may be more attractive due to their heightened volatility and potential for larger price swings, making them the “wild cards” of the market.

Visual Representation:

The Beta value is plotted as a line chart beneath the main price chart, offering a visual representation of the token’s volatility relative to Bitcoin over the last 90 days. Spikes in Beta indicate periods of increased volatility, while drops suggest stability.

Quarterly Theory ICT 04 [TradingFinder] SSMT 4Quarter Divergence🔵 Introduction

Sequential SMT Divergence is an advanced price-action-based analytical technique rooted in the ICT (Inner Circle Trader) methodology. Its primary objective is to identify early-stage divergences between correlated assets within precise time structures. This tool not only breaks down market structure but also enables traders to detect engineered liquidity traps before the market reacts.

In simple terms, SMT (Smart Money Technique) occurs when two correlated assets—such as indices (ES and NQ), currency pairs (EURUSD and GBPUSD), or commodities (Gold and Silver)—exhibit different reactions at key price levels (swing highs or lows). This lack of alignment is often a sign of smart money manipulation and signals a lack of confirmation in the ongoing trend—hinting at an imminent reversal or at least a pause in momentum.

In its Sequential form, SMT divergences are examined through a more granular temporal lens—between intraday quarters (Q1 through Q4). When SMT appears at the transition from one quarter to another (e.g., Q1 to Q2 or Q3 to Q4), the signal becomes significantly more powerful, often aligning with a critical phase in the Quarterly Theory—a framework that segments market behavior into four distinct phases: Accumulation, Manipulation, Distribution, and Reversal/Continuation.

For instance, a Bullish SMT forms when one asset prints a new low while its correlated counterpart fails to break the corresponding low from the previous quarter. This usually indicates absorption of selling pressure and the beginning of accumulation by smart money. Conversely, a Bearish SMT arises when one asset makes a higher high, but the second asset fails to confirm, signaling distribution or a fake-out before a decline.

However, SMT alone is not enough. To confirm a true Market Structure Break (MSB), the appearance of a Precision Swing Point (PSP) is essential—a specific candlestick formation on a lower timeframe (typically 5 to 15 minutes) that reveals the entry of institutional participants. The combination of SMT and PSP provides a more accurate entry point and better understanding of premium and discount zones.

The Sequential SMT Indicator, introduced in this article, dynamically scans charts for such divergence patterns across multiple sessions. It is applicable to various markets including Forex, crypto, commodities, and indices, and shows particularly strong performance during mid-week sessions (Wednesdays and Thursdays)—when most weekly highs and lows tend to form.

Bullish Sequential SMT :

Bearish Sequential SMT :

🔵 How to Use

The Sequential SMT (SSMT) indicator is designed to detect time and structure-based divergences between two correlated assets. This divergence occurs when both assets print a similar swing (high or low) in the previous quarter (e.g., Q3), but in the current quarter (e.g., Q4), only one asset manages to break that swing level—while the other fails to reach it.

This temporal mismatch is precisely identified by the SSMT indicator and often signals smart money activity, a market phase transition, or even the presence of an engineered liquidity trap. The signal becomes especially powerful when paired with a Precision Swing Point (PSP)—a confirming candle on lower timeframes (5m–15m) that typically indicates a market structure break (MSB) and the entry of smart liquidity.

🟣 Bullish Sequential SMT

In the previous quarter, both assets form a similar swing low.

In the current quarter, one asset (e.g., EURUSD) breaks that low and trades below it.

The other asset (e.g., GBPUSD) fails to reach the same low, preserving the structure.

This time-based divergence reflects declining selling pressure, potential absorption, and often marks the end of a manipulation phase and the start of accumulation. If confirmed by a bullish PSP candle, it offers a strong long opportunity, with stop-losses defined just below the swing low.

🟣 Bearish Sequential SMT

In the previous quarter, both assets form a similar swing high.

In the current quarter, one asset (e.g., NQ) breaks above that high.

The other asset (e.g., ES) fails to reach that high, remaining below it.

This type of divergence signals weakening bullish momentum and the likelihood of distribution or a fake-out before a price drop. When followed by a bearish PSP candle, it sets up a strong shorting opportunity with targets in the discount zone and protective stops placed above the swing high.

🔵 Settings

⚙️ Logical Settings

Quarterly Cycles Type : Select the time segmentation method for SMT analysis.

Available modes include: Yearly, Monthly, Weekly, Daily, 90 Minute, and Micro.

These define how the indicator divides market time into Q1–Q4 cycles.

Symbol : Choose the secondary asset to compare with the main chart asset (e.g., XAUUSD, US100, GBPUSD).

Pivot Period : Sets the sensitivity of the pivot detection algorithm. A smaller value increases responsiveness to price swings.

Activate Max Pivot Back : When enabled, limits the maximum number of past pivots to be considered for divergence detection.

Max Pivot Back Length : Defines how many past pivots can be used (if the above toggle is active).

Pivot Sync Threshold : The maximum allowed difference (in bars) between pivots of the two assets for them to be compared.

Validity Pivot Length : Defines the time window (in bars) during which a divergence remains valid before it's considered outdated.

🎨 Display Settings

Show Cycle :Toggles the visual display of the current Quarter (Q1 to Q4) based on the selected time segmentation

Show Cycle Label : Shows the name (e.g., "Q2") of each detected Quarter on the chart.

Show Bullish SMT Line : Draws a line connecting the bullish divergence points.

Show Bullish SMT Label : Displays a label on the chart when a bullish divergence is detected.

Bullish Color : Sets the color for bullish SMT markers (label, shape, and line).

Show Bearish SMT Line : Draws a line for bearish divergence.

Show Bearish SMT Label : Displays a label when a bearish SMT divergence is found.

Bearish Color : Sets the color for bearish SMT visual elements.

🔔 Alert Settings

Alert Name : Custom name for the alert messages (used in TradingView’s alert system).

Message Frequency :

All: Every signal triggers an alert.

Once Per Bar: Alerts once per bar regardless of how many signals occur.

Per Bar Close: Only triggers when the bar closes and the signal still exists.

Time Zone Display : Choose the time zone in which alert timestamps are displayed (e.g., UTC).

Bullish SMT Divergence Alert : Enable/disable alerts specifically for bullish signals.

Bearish SMT Divergence Alert : Enable/disable alerts specifically for bearish signals

🔵 Conclusion

The Sequential SMT (SSMT) indicator is a powerful and precise tool for identifying structural divergences between correlated assets within a time-based framework. Unlike traditional divergence models that rely solely on sequential pivot comparisons, SSMT leverages Quarterly Theory, in combination with concepts like liquidity sweeps, market structure breaks (MSB) and precision swing points (PSP), to provide a deeper and more actionable view of market dynamics.

By using SSMT, traders gain not only the ability to identify where divergence occurs, but also when it matters most within the market cycle. This empowers them to anticipate major moves or traps before they fully materialize, and position themselves accordingly in high-probability trade zones.

Whether you're trading Forex, crypto, indices, or commodities, the true strength of this indicator is revealed when used in sync with the Accumulation, Manipulation, Distribution, and Reversal phases of the market. Integrated with other confluence tools and market models, SSMT can serve as a core component in a professional, rule-based, and highly personalized trading strategy.

AI-123's BTC vs Gold (Lag Correlation)

DISCLAIMER

I made this indicator with the help of ChatGPT and using what I have learned so far from The Pine Script Mastery Course, LOTS of edits based on what I have learned so far had to be made as well as additions and modifications to my liking thanks to what I have learned so far. I am aware this already exists but I have done my best to make a first ever script/indicator while learning how to properly publish as well, so please bear that in mind.

Overview

This indicator analyzes the correlation between Bitcoin (BTC) and Gold (XAUUSD), with a customizable lag applied to the Gold price, providing insight into the macro relationship between these two assets.

It is designed for traders and investors who want to track how Bitcoin and Gold move in relation to each other, particularly when Gold is lagged by a specific number of days.

Key Features:

BTC and Gold (Lagged) Price Overlay: Display Bitcoin (BTC) and Gold (XAUUSD) prices on the chart, with an adjustable lag applied to the Gold price.

Rolling Correlation Calculation: Measures the correlation between Bitcoin and lagged Gold prices over a customizable lookback period.

Adjustable Lag: The number of days that Gold is lagged relative to Bitcoin is fully customizable (default: 20 days).

Customizable Correlation Length: Allows you to choose the lookback period for the correlation (default: 50 days), providing flexibility for short-term or long-term analysis.

Normalized Plotting: Prices of Bitcoin and Gold are normalized for better visual alignment with the correlation values. BTC is divided by 1000, and Gold by 100.

Correlation Scaling: The correlation value is amplified by 10 for better visual clarity and comparison with price data.

Zero Line: Horizontal line representing a correlation of 0, making it easier to identify positive or negative correlation shifts.

Maximum Correlation Lines: Horizontal lines at +10 and -10 values for extreme correlation scenarios.

Input Settings:

Gold Symbol: Customize the Gold ticker (default: OANDA:XAUUSD).

Bitcoin Symbol: Customize the Bitcoin ticker (default: BINANCE:BTCUSDT).

Lag (in trading days): Adjust the number of trading days to lag the Gold price relative to Bitcoin (default: 20).

Correlation Length (days): Set the number of days over which the rolling correlation is calculated (default: 50).

How to Use:

Price Comparison: The BTC (Spot) and Lagged Gold plots give you a side-by-side visual comparison of the two assets, normalized for clarity.

Correlation Line: The correlation line helps you gauge the strength and direction of the relationship between BTC and lagged Gold. Positive values indicate a strong positive correlation, while negative values indicate a negative correlation.

Visual Analysis: Watch how the correlation shifts with changes in lag and correlation length to identify potential market dynamics between Bitcoin and Gold.

Potential Applications:

Macro Trading: Track how Bitcoin and Gold behave in relation to each other during periods of economic uncertainty or inflation.

Sentiment Analysis: Use the correlation data to understand the sentiment between digital and traditional assets.

Strategic Timing: Identify potential opportunities where Bitcoin and Gold show a strong correlation or diverge based on the lag adjustment.

Understanding Macro Trends/Correlations.

Disclaimer:

This indicator is for informational purposes only. The correlation between Bitcoin and Gold does not guarantee future performance, and users should conduct their own research and use risk management strategies when making trading decisions.

Notes: This script uses historical data, so results may vary across different timeframes.

Customization options allow users to adjust the lag and correlation length to better fit their trading strategy.

Future Enhancements: Additional Correlation Line: A second correlation line for different lengths of lag or different assets.

Color-Coding of Correlation: Future updates may include color-coded correlation strength, visually indicating positive or negative correlation more effectively.

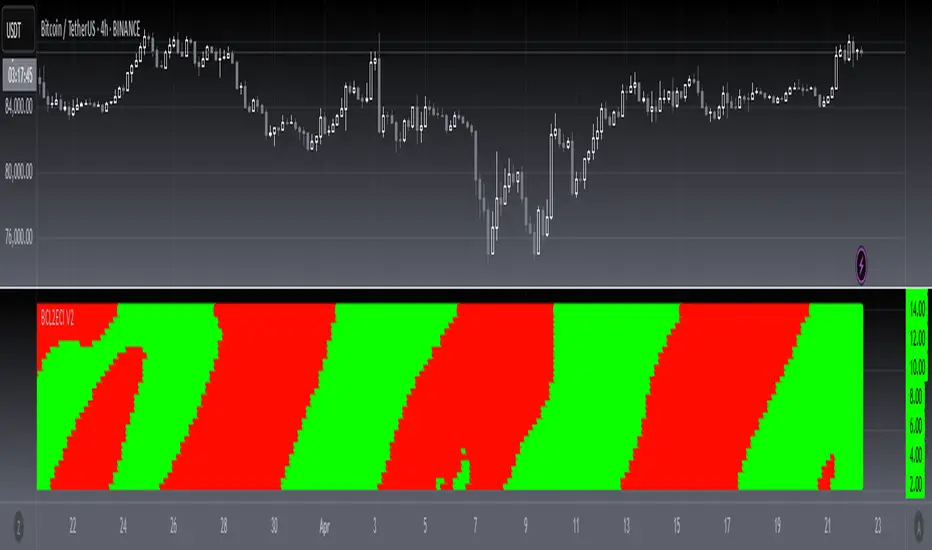

[blackcat] L2 Ehlers Convolution Indicator V2OVERVIEW The L2 Ehlers Convolution Indicator V2 is an advanced technical analysis tool that applies convolution techniques to identify market trends and potential reversal points. It uses adaptive filtering to analyze price movements across multiple timeframes.

FEATURES

• Advanced convolution algorithm based on Ehlers' methodology

• Multiple timeframe analysis (S2 through S60)

• Dynamic color coding for trend direction:

Red: Downward trend

Green: Upward trend • Adjustable sensitivity through period inputs

HOW TO USE

Input Parameters:

• ShortestPeriod: Minimum period length for calculations

• LongestPeriod: Maximum period length for calculations

Interpretation:

• Red bars indicate downward momentum

• Green bars indicate upward momentum

• Bar height corresponds to the timeframe analyzed

LIMITATIONS

• Requires sufficient historical data for accurate calculations

• May produce false signals during volatile markets

• Performance depends on selected period parameters

NOTES

• The indicator uses arrays to store correlation, slope, and convolution values

• Each bar represents a different timeframe analysis

• Color intensity varies based on the strength of the signal

[blackcat] L2 Ehlers Autocorrelation Periodogram V2OVERVIEW

The Ehlers Autocorrelation Periodogram is a sophisticated technical analysis tool that identifies market cycles and their dominant frequencies using autocorrelation and spectral analysis techniques.

BACKGROUND

Developed by John F. Ehlers and detailed in his book "Cycle Analytics for Traders" (2013), this indicator combines autocorrelation functions with discrete Fourier transforms to extract cyclic information from price data.

FUNCTION

The indicator works through these key steps:

Calculates autocorrelation using minimum three-bar averaging

Applies discrete Fourier transform to extract cyclic information

Uses center-of-gravity algorithm to determine dominant cycle

ADVANTAGES

• Rapid response within half-cycle periods

• Accurate relative cyclic power estimation over time

• Correlation constraints between -1 and +1 eliminate amplitude compensation needs

• High resolution independent of windowing functions

HOW TO USE

Add the indicator to your chart

Adjust AvgLength input parameter:

• Default: 3 bars

• Higher values increase smoothing

• Lower values increase sensitivity

Interpret the results:

• Colored bars represent spectral power

• Red to yellow spectrum indicates cycle strength

• White line shows dominant cycle period

INTERPRETATION

• Strong colors indicate significant cyclic activity

• Sharp color transitions suggest potential cycle changes

• Dominant cycle line helps identify primary market rhythm

LIMITATIONS

• Requires sufficient historical data

• Performance may vary in non-cyclical markets

• Results depend on proper parameter settings

NOTES

• Uses highpass and super smoother filtering techniques

• Spectral estimates are normalized between 0 and 1

• Color intensity varies based on spectral power

THANKS

This implementation is based on Ehlers' original work and has been adapted for TradingView's Pine Script platform.