Supply and Demand Based Pattern [RH]This indicator focuses on detecting RBR and DBD patterns, which signify periods of increased momentum and potential continuation or reversal of the prevailing trend.

The RBR pattern consists of a rally (upward movement), followed by a base (consolidation or retracement), and then another rally. It suggests that the upward momentum may persist and provide trading opportunities.

On the other hand, the DBD pattern comprises a drop (downward movement), followed by a base, and then another drop. It indicates that the downward momentum might continue, offering potential shorting opportunities.

Bullish(RBR) example:

Bearish(DBD) example:

1. The bullish (RBR) and bearish (DBD) patterns share the same underlying logic, only differing in their directionality.

2. For both RBR and DBD patterns, the first rise/drop can consist of one or multiple candles. However, in the case of multiple candles, all candles must exhibit a bullish nature for RBR and a bearish nature for DBD.

Example:

3. It is a prerequisite for the first rise/drop to include at least one candle with a defined percentage of health, as determined by the user.

4. The base, following the first rise/drop, may comprise one or multiple candles.

Example:

5. To maintain consistency, the base is not allowed to retrace beyond 80%, although this value can be adjusted by the user.

6. Similar to the first rise/drop, the second rise/drop in both RBR and DBD patterns can consist of one or multiple candles. However, all candles within this phase must demonstrate a bullish nature for RBR and a bearish nature for DBD.

7. Confirmation of the bullish (RBR) pattern occurs when a candle closes above the high of the first rise. Conversely, the bearish (DBD) pattern is confirmed when a candle closes below the low of the first drop.

Example:

Alerts can be set for all bullish and bearish pattern or for the first pattern in the range of similar pattern.

Циклический анализ

Revolution SMA-EMA DivergenceThis is an MACD inspired indicator and it analyzes the difference between the SMA and EMA using the same time period. Unlike the MACD, it can give you a better understanding of the overall trend. Values above 0 is bullish and below 0 bearish. It consists of two cycles: Black histogram - the long-term cycle and orange histogram - the short-term cycle, as well as timing signal (red line).

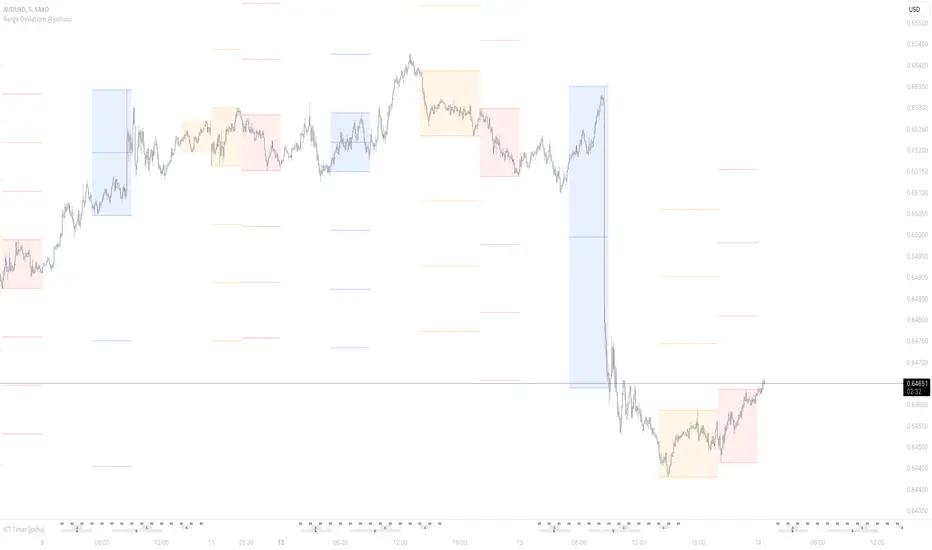

Range Deviations @joshuuuThis indicator is able to show ranges, the equlibrium (50%) and range deviations.

It has four pre-defined options and one custom version.

Asia (2000-0000) ny time

CBDR(1400-2000) ny time

Flout(1400-0000) ny time

ONS (OverNightSession)(0400-0800) chicago time

Custom (you can choose the times)

ICT (Inner Circle Traders) teaches, that those range deviations of asia,cbdr,flout can be used to find the daily high/low.

TCM (The Currency Merchant) teaches, that a move out of the range often is a false move to trap traders into the wrong direction.

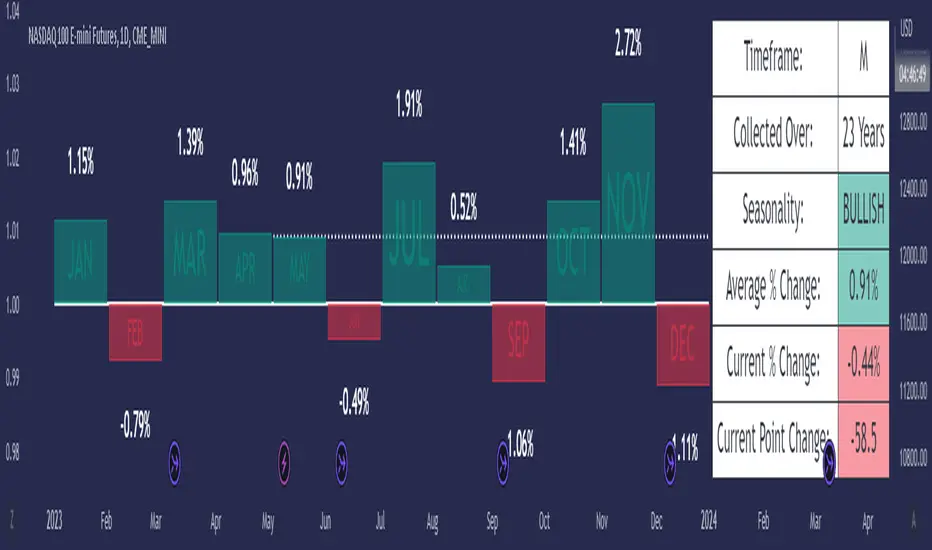

Seasonal Performance for Stocks & CryptoThe Seasonal Performance indicator quickly allows you to see if you are in a bullish or bearish time of year for an underlying security and where the current performance stacks up compared to the same time of year historically. Table is fully customizable from colors to what data to see.

Table Displays

Average Performance

Best Performance

Worst Performance

Last Performance

Current Performance

Note this indicator will only work with Stocks, ETF's, Index's or Crypto.

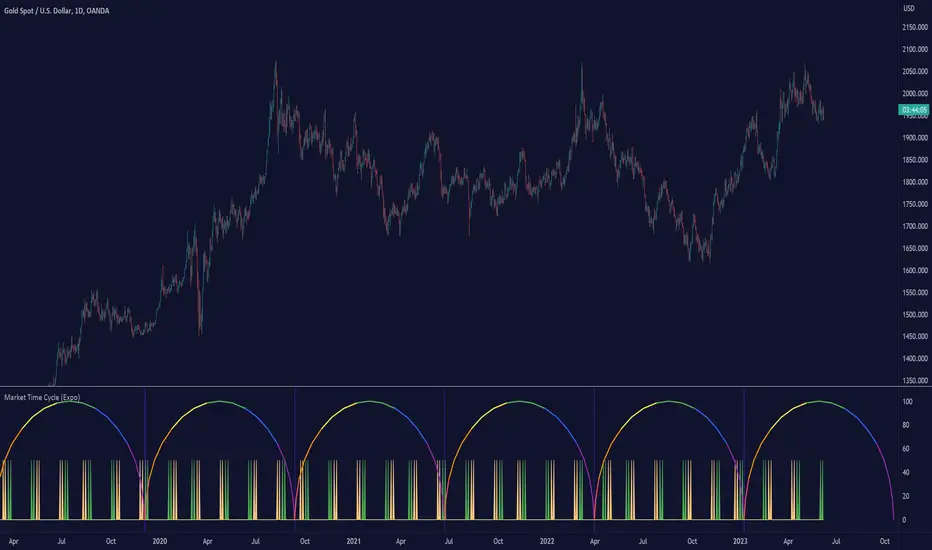

Market Time Cycle (Expo)█ Time Cycles Overview

Time cycles are a fascinating and powerful concept in the world of trading and investing. They are all about understanding and predicting the timing of market moves based on the premise that market events and price movements are not random, but instead occur in repeatable, cyclical patterns.

The Concept of Time Cycles: The foundation of time cycles lies in the belief that historical market patterns tend to repeat themselves over specific periods. These periods or cycles could be influenced by a myriad of factors like economic data releases, earnings reports, geopolitical events, or even natural human behavior. For example, some traders observe increased market activity around the start and end of a trading day, which is a form of intraday time cycle.

Understanding time cycles can provide traders with a roadmap, helping them anticipate potential trend shifts and make more informed decisions about when to buy or sell.

█ Indicator Overview

The Market Time Cycle (Expo) is designed to help traders track and analyze market cycles and generate signals for potential trading opportunities. It uses mathematical techniques to analyze market cycles and detect possible turning points. It does this by projecting the estimated cycle timeline and providing visual indications of cyclical phases through the use of color-coded lines and sine wave cycles.

Time cycles offer a compelling way to forecast market trends and time your trades better. By adding time cycles to your trading toolbox, you could potentially gain a new perspective on market movements and refine your trading strategy further. The indicator generates trading signals based on the sine wave's behavior. When the sine wave crosses certain thresholds, the indicator generates a signal suggesting a potential trading opportunity based on cycle behavior.

█ How to use

This indicator can be a valuable tool to help traders understand and predict market trends and time their trades more accurately. By visualizing the cyclic nature of markets, traders can better anticipate potential turning points and adjust their trading strategies accordingly. It helps traders to spot ideal entry and exit points based on the cyclical nature of financial markets.

█ Settings

You can customize the number of bars (NumbOfBars) that are taken into consideration for the cycle. Including a higher number of bars will provide more data, which can be helpful for analyzing long-term trends.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Trend Reversal Indicator (Bull/Bear)Simple indicator utilising time series momentum to identify secular/cyclical trends in asset classes. Default setting is weekly timeframe - yearly/quarterly. The indicator helps define when in bull/bear market, and corrections/rebounds within larger trends.

Show Extended Hours (Futures & Crypto)OVERVIEW

This indicator mimics TradingViews "Extended trading hours" background color settings. It is most useful on symbols that do not conventionally have extended hours, but are available to trade during those hours (ie. Futures and Crypto). Because market participation (ie. volatility) in a given symbol can change dramatically at or near these transitions, seeing conventional market open / closures expedites price action context around these transitions.

INPUTS

You can configure:

Background colors for both Premarket and After Hours

Which extended hours you would like to see

Market Hours and Time Zone

AIAE IndicatorAggregate (or Average) Investor Allocation to Equities.

When it comes to predicting long-term equity returns, several well-known indicators come to mind—for example, the CAPE ratio, Tobin’s Q, and Market Cap to GDP, to name a few.

Yet there is another indicator without nearly as high of a profile that has outperformed the aforementioned indicators significantly when it comes to both forecasting and tactical asset allocation.

That indicator, known as the Aggregate (or Average) Investor Allocation to Equities (AIAE), was developed by the pseudonymous financial pundit, Jesse Livermore, and published on his blog in 2013.

In an essay titled, “The Single Greatest Predictor of Future Stock Market Returns,” Livermore makes the case that the primary driver of long-term equity returns is not valuation, but rather the supply of equities relative to the combined supply of bonds and cash.

Accordingly, the AIAE is computed by taking the total market value of equities and dividing by the sum of a) the total market value of equities, b) the total market value of bonds, and c) the total amount of cash available to investors (i.e., that in circulation plus bank deposits):

This ratio gives the market-wide allocation to equities (or, equivalently, the average investor allocation to equities weighted by portfolio size). (Note that every share of stock, every bond, and every unit of cash in existence must be held in some portfolio somewhere at all times.)

Livermore explains that, in practice, the total market value of bonds plus cash can be estimated by the total liabilities held by the five classes of economic borrowers: Households, Non-Financial Corporations, State and Local Governments, the Federal Government, and the Rest of the World.

This follows from the fact that if these entities borrow directly from investors, new bonds are created. Whereas, if they borrow directly from banks, new bank deposits (cash) are created.

As the economy grows, the supply of bonds and cash steadily increases. Historically, the rate of increase of the supply of bonds and cash has been about 7.5% per annum. Consequently, if the market portfolio is to maintain the same allocation to equities, the supply of equities must increase at the exact same rate.

The supply of equities can increase either by new equity issuance or by price increases. Historically, net new equity issuance has been negligible (with issuances being offset by buybacks and acquisitions). Thus, in order for equities not to become an ever-smaller portion of the average investor’s portfolio, the price of stocks must rise over the long-term.

While we often hear that stock prices follow earnings, in the 1980s earnings fell slightly from the beginning of the decade to the end of the decade, yet stocks rose at an annualized rate of 17% during that time. How could this be?

Well, at the beginning of the decade the average investor’s portfolio had a 25% allocation to equities. During the decade, the supply of bonds and cash rose strongly. If the price of equities had not risen, the average investor’s allocation to equities would have fallen to a mere 13% (as the supply of cash and bonds grew). Thus, equities had no choice but to rise despite the fall in earnings.

Turtle Soup IndicatorTurtle Soup Indicator plots a shape when we have a 20-period high or 20-period low.

Turtle Soup Setup

The Turtle Soup setup was published in the book Street Smarts by Laurence A Connors and Linda Raschke. You can learn about it there. It is a great setup for false breakouts or breakdowns in the group failure tests.

Going long

1) We have a new 20-period low

2) that must have occured at least four trading sessions earlier <- this is very important

Then we place a buy stop above 5-10 ticks or 5 to 10 cents above the previous 20-period low.

If filled immediately place a good til cancelled sell stop one tick or one cent below todays low.

Turtle Soup Plus One

Similar to above but occurs one day later. It should close at/below previous 20-period low.

Buy stop at earlier 20 day low. Cancel fi not filled on day 2.

Take partials within 2-6 bars on this one and trail stop rest of position.

Going short

Reverse

Time frames

Works on all timeframes. Only adjust stoplosses accordingly to chosen timeframe.

Settings

You can change the color, shape and placement of the indicator shape. I actually prefer a grey color for both highs and lows as the color actually doesn't add much information. The placement says it all but it is up to you to change this as you like.

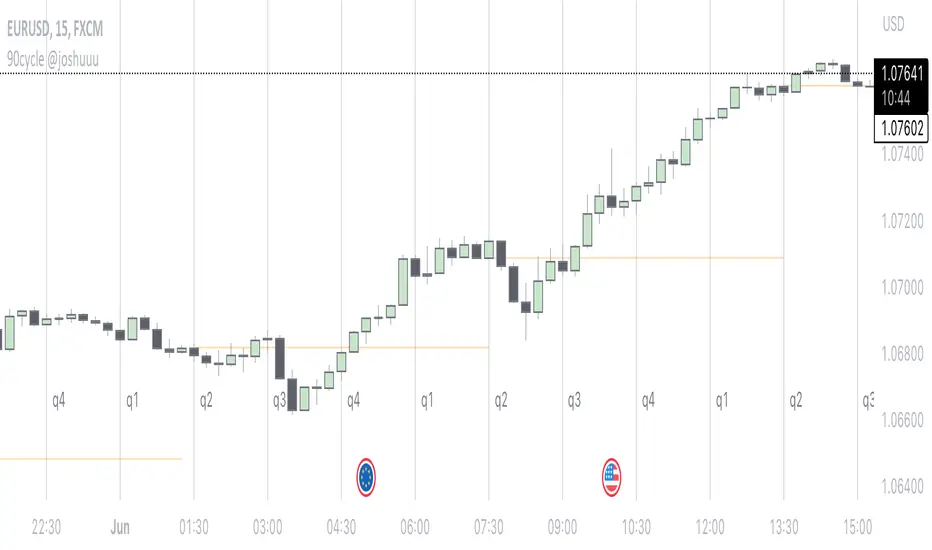

90cycle @joshuuu90 minute cycle is a concept about certain time windows of the day.

This indicator has two different options. One uses the 90 minute cycle times mentioned by traderdaye, the other uses the cls operational times split up into 90 minutes session.

e.g. we can often see a fake move happening in the 90 minute window between 2.30am and 4am ny time.

The indicator draws vertical lines at the start/end of each session and the user is able to only display certain sessions (asia, london, new york am and pm)

For the traderdayes option, the indicator also counts the windows from 1 to 4 and calls them q1,q2,q3,q4 (q-quarter)

⚠️ Open Source ⚠️

Coders and TV users are authorized to copy this code base, but a paid distribution is prohibited. A mention to the original author is expected, and appreciated.

⚠️ Terms and Conditions ⚠️

This financial tool is for educational purposes only and not financial advice. Users assume responsibility for decisions made based on the tool's information. Past performance doesn't guarantee future results. By using this tool, users agree to these terms.

90 Minute Cycles + MTFCredit goes to LuxAlgo for the inspiration from 'Sessions' which allowed users to analyse specific price movements within a user defined period with tools such as trendline, mean and vwap.

Settings

Sessions

Enable Session: Allows to enable or disable all associated elements with a specific user set session.

Session Time: Opening and closing times of the user set session in the hh:mm format.

Range: Highlights the associated session range on the chart.

Ranges Settings

Range Area colour: Set each range to a specific colour.

Range Label: Shows the session label at the mid-point of the session interval.

Usage

By breaking 24hrs in quarters, starting with an Asian range of 18:00 NY time you can visualise the principles of Accumulation, Manipulation, Distribution and Rebalance. Know as AMD or PO3 (Power of Three), the principle is that the Manipulation phase will break above or below the Accumulation, before moving in an apposing direction and then rebalancing. This only works when there is a higher timeframe PD array or liquidity to support an apposing move.

Further to the daily quarters, each one can then be broken down again into 90min cycles. Again, each represents AMD, allowing the user an opportunity to watch for reversals during the 90min manipulation phase.

Note: Ensure the Asian Cycle always begins at 18:00 NY time.

The example shows that the 90min cycle occurs, followed by an apposing move away in price action

Here is the Daily cycle, highlighting the Manipulation phase.

Enjoy!

7 Closes above/below 5 SMAThis script looks for 7 consecutive closes above/below the 5-period SMA. The indicator is inspired by legendary trader Linda Raschke's work.

Usage

The script can can be used in three main ways. I think you will find more uses.

First are the two models for which the indicator was created, both inspired by Raschke:

1) Persistency of trend / Extended run setup.

Around 10-12 times per year we get a persistency of trend in instruments in general.

After 7 consecutive closes above/below the 5-period as price pulls back we can look to enter in the direction of the main trend as it moves up/down above/below 5 ma again. You should use price action trading to pinpoint the entries. Now try to hold this as long as possible. Way longer than you can percieve or think is possible. Up to 24-28 periods is what we are looking for in these cases.

2) Normal usage.

When the trend is not persistent, it is possible to use this as an oscillating signal, for a shorter term trade, where we can look for a short or long term reversal setup in price action.

3) I also use it at as a learning to see the swing trades clearer. You can also use it as a visual aid for developing new variances of the classic swing trading setup.

Read and listen to Linda Raschkes work to learn more.

TIme frames

The principles works in all time frames but may change depending on calendar differences. We will see more instances/year in shorter time frames.

Why closes above the 5 SMA

As you may or may not know the 5 SMA is a very important indicator. You can think of it like this, If price is above 5, it is innocent until proven guilty but if price is below 5 we use the french law system which means it is guilty until proven innocent. 7 closes above 5 is a very good predictor of possible short term direction changes.

Use together with:

I prefer to use this indicator together with either regular SMA:s, one short and one macro term. For example 10 ma and 100 ma.

Or you can use it with a a Hull 21-period MA together with a 240-period WMA.

Settings:

I added settings so you can change preferences for changing shape, where to display the shape and in what color

Visual aid

I wanted to keep one dot for each consecutive day, this way we will get a grouping of days and dots. The amount in this group can be of use in itself to inform you of the strength of trend. This can inform you if this oscillation predicts a short term eversal or a continuation. You need skills in reading price action to use this to your advantage.

TGIF StatsTGIF - "Thank God it's Friday"

After a heavily bearish week (tuesday, wednesday and thursday) price sometimes looks for some retracement on fridays. Vice versa for bullish weeks.

This script shows how often that specific scenario happens and displays that data in a table.

The user has the option to input a starting year for the statistic and is able to filter between bearish or bullish weeks.

*disclaimer : if paired with a higher timeframe pd array taught by ICT the stats should be better, that's not included in the code though*

⚠️ Open Source ⚠️

Coders and TV users are authorized to copy this code base, but a paid distribution is prohibited. A mention to the original author is expected, and appreciated.

⚠️ Terms and Conditions ⚠️

This financial tool is for educational purposes only and not financial advice. Users assume responsibility for decisions made based on the tool's information. Past performance doesn't guarantee future results. By using this tool, users agree to these terms.

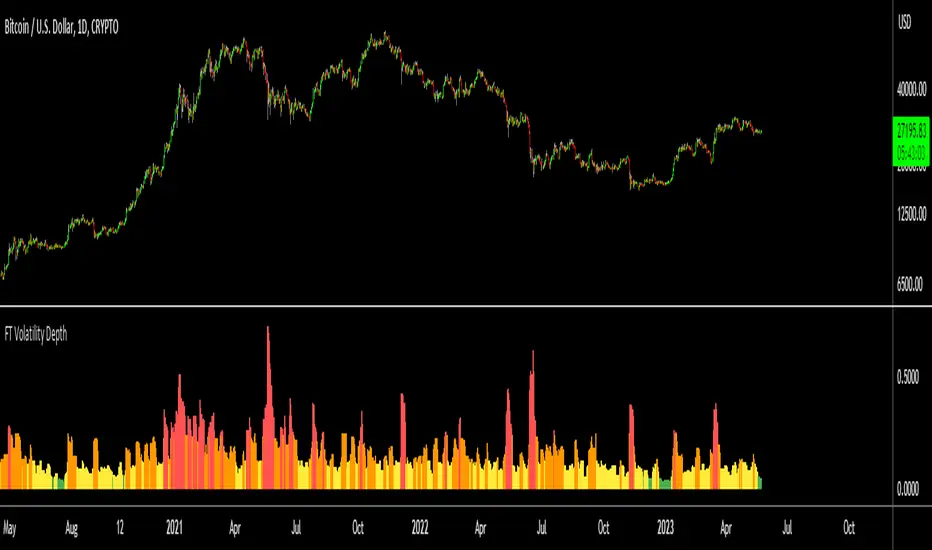

Fierytrading: Volatility DepthDear Tradingview community,

I'd like to share one of my staple indicators with you. The volatility depth indicator calculates the volatility over a 7-day period and plots it on your chart.

This indicator only works for the DAILY chart on BTC/USD.

Colors

I've color coded the indicator as follows:

- Red: Extreme Volatility

- Orange: High Volatility

- Yellow: Normal Volatility

- Green: Low Volatility

Red: extreme changes in price. Often during local tops and bottoms.

Orange: higher than average moves in price. Often before or after a "red" period. Often seen in the middle of bear or bull markets.

Yellow: normal price action. Often seen during early stage bull-markets and late stage bear-markets.

Green: very low price movement. Often during times of indecision. Once this indicator becomes green, you can expect a big move in either direction. Low volatility is always followed by high volatility.

In a long-term uptrend, a green period often signals a bullish break out. In a long-term downtrend it often signals a bearish break out.

How to use

Save the indicator and apply it to your chart. You can change the length in the settings, but it's optimized for 7 days, so no need to change it.

I've build in alerts for all 4 different volatility periods. In most cases, the low volatility alert is enough.

Good luck!

Market Cycle IndicatorThe Market Cycle Indicator is a tool that integrates the elements of RSI, Stochastic RSI, and Donchian Channels. It is designed to detect market cycles, enabling traders to enter and exit the market at the most opportune times.

This indicator provides a unique perspective on the market, combining multiple strategies into one unified and weighted approach. By factoring in the inputs from each of these popular technical analysis methods, it offers a more holistic view of the market trends and cycles.

Parameter Details:

Donchian Channels (DCO):

- donchianPeriod: Sets the period for the Donchian Channel calculation. Default is set to 14.

- donchianSmoothing: Sets the smoothing factor for the Donchian Channel calculation. Default is set to 3.

- donchianPrice: Selects the price type to be used in the Donchian Channel calculation. Default is set to the closing price.

Relative Strength Index (RSI):

- rsiPeriod: Sets the period for the RSI calculation. Default is set to 14.

- rsiSmoothing: Sets the smoothing factor for the RSI calculation. Default is set to 3.

- rsiPrice: Selects the price type to be used in the RSI calculation. Default is set to the closing price.

Stochastic RSI (StochRSI):

- srsiPeriod: Sets the period for the Stochastic RSI calculation. Default is set to 20.

- srsiSmoothing: Sets the smoothing factor for the Stochastic RSI calculation. Default is set to 3.

- srsiK: Sets the period for the %K line in the Stochastic RSI calculation. Default is set to 5.

- srsiD: Sets the period for the %D line in the Stochastic RSI calculation. Default is set to 5.

- srsiPrice: Selects the price type to be used in the Stochastic RSI calculation. Default is set to the closing price.

Weights:

- rsiWeight: Sets the weight for the RSI in the final aggregate calculation. Default is set to 1.

- srsiWeight: Sets the weight for the Stochastic RSI in the final aggregate calculation. Default is set to 1.

- dcoWeight: Sets the weight for the Donchian Channel in the final aggregate calculation. Default is set to 1.

Limits:

- limitHigh: Sets the upper limit for the indicator. Default is set to 80.

- limitLow: Sets the lower limit for the indicator. Default is set to 20.

By customizing these parameters, users can tweak the indicator to align with their own trading strategies and risk tolerance levels. Whether you're a novice or an experienced trader, the Comprehensive Market Cycle Indicator provides valuable insights into the market's behavior.

Uses library HelperTA

Buying/Selling Pressure Cycle (PreCy)No lag estimation of the buying/selling pressure for each candle.

----------------------------------------------------------------------------------------------------

WHY PreCY?

How much bearish pressure is there behind a group of bullish candles ?

Is this bearish pressure increasing?

When might it overcome the bullish pressure?

Those were my questions when I started this indicator. It lead me through the rabbit hole, where I discovered some secrets about the market. So I pushed deeper, and developped it a lot more, in order to understand what is really happening "behind the scene".

There are now 3 ways to read this indicator. It might look complicated at first, but the reward is to be able to anticipate and understand a lot more.

You can show/hide all the plots in the settings. So you can choose the way you prefer to use it.

----------------------------------------------------------------------------------------------------

FIRST WAY TO READ PreCy : The SIGNAL line

Go in the settings of PreCy, in "DISPLAY", uncheck "The pivot lines of the SIGNAL" and "The CYCLE areas". Make sure "The SIGNAL line" is checked.

The SIGNAL shows an estimation of the buying/selling pressure of each candle, going from 100 (100% bullish candle) to -100 (100% bearish candle). A doji would be shown close to zero.

Formula: Estimated % of buying pressure - Estimated % of selling pressure

It is a very choppy line in general, but its colors help make sense of it.

When this choppiness alternates between the extremes, then there is not much pressure on each candle, and it's very unpredictable.

When the pressure increases, the SIGNAL's amplitude changes. It "compresses", meaning there is some interest in the market. It can compress by alternating above and below zero, or it can stay above zero (bullish), or below zero (bearish) for a while.

When the SIGNAL becomes linear (in opposition to choppy), there is a lot of pressure, and it is directional. The participants agree for a move in a chosen direction.

The trajectory of the SIGNAL can help anticipate when a move is going to happen (directional increase of pressure), or stop (returning to zero) and possibly reverse (crossing zero).

Advanced uses:

The SIGNAL can make more sense on a specific timeframe, that would be aligned with the frequency of the orders at that moment. So it is a good idea to switch between timeframes until it gets less choppy, and more directional.

It is interesting to follow any regular progression of the SIGNAL, as it can reveal the intentions of the market makers to go in a certain direction discretely. There can be almost no volume and no move in the price action, yet the SIGNAL gets linear and moves away from one extreme, slowly crosses the zeroline, and pushes to the other extreme at the same time as the amplitude of the price action increases drastically.

----------------------------------------------------------------------------------------------------

SECOND WAY TO READ PreCy : The PIVOTS of the SIGNAL line

Go in the settings of PreCy, in "DISPLAY", and uncheck "The CYCLE areas". Make sure "The SIGNAL line" and "The pivot lines of the SIGNAL" are checked.

The PIVOTS help make sense of the apparent chaos of the SIGNAL. They can reveal the overall direction of the choppy moves.

Especially when the 2 PIVOTS lines are parallel and oriented.

----------------------------------------------------------------------------------------------------

THIRD WAY TO READ PreCy : The CYCLE

Go in the settings of PreCy, in "DISPLAY", and uncheck "The SIGNAL line" and "The pivot lines of the SIGNAL". Make sure "The CYCLE areas" is checked.

The CYCLE is a Moving Average of the SIGNAL in relation to each candle's size.

Formula: 6 periods Moving Average of the SIGNAL * (body of the current candle / 200 periods Moving Average of the candle's bodies)

The result goes from 200 to -200.

The CYCLE shows longer term indications of the pressures of the market.

Analysing the trajectory of the CYCLE can help predict the direction of the price.

When the CYCLE goes above or below the gray low intensity zone, it signals some interest in the move.

When the CYCLE stays above 100 or below -100, it is a sign of strength in the move.

When it stayed out of the gray low intensity zone, then returns inside it, it is a strong signal of a probable change of behavior.

----------------------------------------------------------------------------------------------------

ALERTS

In the settings, you can pick the alerts you're interested in.

To activate them, right click on the chart (or alt+a), choose "Add alert on Buying/Selling Pressure Cycle (PreCy)" then "Any alert()", then "Create".

Feel free to activate them on different timeframes. The alerts show which timeframe they are from (ex: "TF:15" for the 15 minutes TF).

I have added a lot more conditions to my PreCy, taken from FREMA Trend, for ex. You can do the same with your favorite scripts, to make PreCy more accurate for your style.

----------------------------------------------------------------------------------------------------

Borrowed scripts:

To estimate the buying and selling pressures, PreCy uses the wicks calculations of "Volume net histogram" by RafaelZioni

To filter the alerts, PreCy uses the calculations of "Amplitude" by Koholintian:

----------------------------------------------------------------------------------------------------

DO NOT BASE YOUR TRADING DECISIONS ON 1 SINGLE INDICATOR'S SIGNALS.

Always confirm your ideas by other means, like price action and indicators of a different nature.

Benner-Fibonacci Reversal Points [CC]This is an original script based on a very old idea called the Benner Theory from the Civil War times. Benner discovered a pattern in pig iron prices (no clue what those are), and this turned out to be a parallel idea to indicators based on Fibonacci numbers. Because a year is 365 days (nearly 377, which is a Fibonacci number), made up of 52 weeks (nearly 55, which is another Fibonacci number), or 12 months (nearly 13, which is another Fibonacci number), Benner theorized that he could find both past and future turning points in the market by using a pattern he found. He discovered that peaks in prices seemed to follow a pattern of 8-9-10, meaning that after a recent peak, it would be 8 bars until the next peak, 9 bars until after that peak for the next, and 10 bars until the following peak. For past peaks, he would just need to reverse this pattern, and so the previous peak would be 10 bars before the most current peak, 9 bars before that peak, and 8 bars before the previous one, and these patterns seemed to repeat. For troughs, he found a pattern of 16,18,20 which follows the same logic, and this idea also seemed to work on long-term peaks and troughs as well.

This is my version of the Benner theory and the major difference between my version and his is that he would manually select a year or date and either work backwards or forwards from that point. I chose to go with an adaptive version that will automatically detect those points and plot those past and future points. I have included several options such as allowing the algorithm to be calculated in reverse which seems to work well for Crypto for some reason. I also have both short and long term options to only show one or both if you choose and of course the option to enable repainting or leave it disabled.

Big thanks to @HeWhoMustNotBeNamed and @RicardoSantos for helping me fix some bugs in my code and for @kerpiciwuasile for suggesting this idea in the first place.

OverNightSession @joshuuuThis indicator highlights the Overnightsession (ONS), taught by TheCurrenyMerchant.

The Overnightsession is from 4-8 am UTC-5. This session can be used to form trades, e.g. after one side has been taken out.

It has the options to display Projection and the equilibrium level. Equilibrium level (50%) can be used to identify if price is currently in premium/discount of the range and the projections (standard deviations of the range) can be used to identify possible targets.

A classic setup he teaches is:

Price trades agressively out of the range taking liquidity. As soon as we trade above the high of the candle that took liquidity, that candle can be considered an orderblock, where the 50% level can be used for long setups.

⚠️ Open Source ⚠️

Coders and TV users are authorized to copy this code base, but a paid distribution is prohibited. A mention to the original author is expected, and appreciated.

⚠️ Terms and Conditions ⚠️

This financial tool is for educational purposes only and not financial advice. Users assume responsibility for decisions made based on the tool's information. Past performance doesn't guarantee future results. By using this tool, users agree to these terms.

BTC bottom top MACRO indicator based on: Cost per transaction(w)Predicting tops and bottoms in any market is a challenging task, and the Bitcoin market is no exception. Many traders and analysts use a combination of various indicators and models to help them make educated guesses about where the market might be heading. One such metric that can provide valuable insights is the Bitcoin cost per transaction indicator.

Here's how it could potentially be superior to just using price action for predicting macro tops and bottoms:

Transaction Cost as an Indicator of Network Activity: The cost per transaction on the Bitcoin network can give an indication of how much activity is taking place. When transaction costs are high, it may signal increased network usage, which often coincides with periods of market enthusiasm or FOMO (Fear of Missing Out) that can precede market tops. Conversely, lower transaction costs might indicate reduced network activity, potentially signaling a lack of investor interest that might precede market bottoms.

Reflects Real-World Use and Demand: Unlike price action, which can be influenced by speculative trading and may not always reflect the underlying fundamentals, the cost per transaction is directly tied to the use of the Bitcoin network. It offers a more fundamental approach to understanding market dynamics.

Complements Price Action Analysis: While price action can give signals about potential tops and bottoms based on historical price patterns and technical analysis, the cost per transaction can add an additional layer of information by reflecting network activity. In this way, the two can be used together to give a more complete picture of the market.

May Precede Price Changes: Changes in transaction costs could potentially precede price changes, giving advanced warning of tops and bottoms. For instance, a sudden increase in transaction costs might indicate a surge in network activity and investor interest, potentially signaling a market top. On the other hand, a decrease in transaction costs might suggest declining network activity and investor interest, potentially signaling a market bottom.

However, it's important to note that while the cost per transaction can provide valuable insights, it's not a foolproof method for predicting market tops and bottoms. Like all indicators, it should be used in conjunction with other tools and analysis methods, and traders should also consider the broader market context. As always, past performance is not indicative of future results, and all trading and investment strategies carry the risk of loss.

ICT Time Windows by Scuba SteveJust an easy to use time based indicator that allows you to track ICT London Open Killzone, New York Open killzone, AM session Silver Bullet time window & PM Session Silver Bullet Time Window, and last but not least the Last Hour of trading which often has nice moves.

Digital Root 9 Time HighlightsTitle: Digital Root 9 Indicator

Description: The Digital Root 9 Indicator is a custom TradingView tool that identifies all times in which the digital root of the current time is 9. The digital root is calculated by summing the digits of the current time and then continuing to sum the resulting digits until a single digit is obtained. For instance, the time 3:33 has a digital root of 9 because 3+3+3=9.

What sets the Digital Root 9 Indicator apart from other TradingView indicators is its focus on identifying times with a numerological significance. It is particularly useful for traders who incorporate numerology into their trading strategies and are looking for a tool that highlights these significant times.

To use the Digital Root 9 Indicator, simply add it to your TradingView chart. The indicator will highlight all times when the digital root of the current time is 9, allowing you to see at a glance which times have numerological significance. You can customize the indicator's color scheme and other settings to suit your preferences.

The Digital Root 9 Indicator is intended to help traders identify times when the potential for luck and prosperity is heightened according to numerology. However, it should not be used as the sole basis for making trading decisions. It is important to conduct thorough analysis and risk management before making any trades.

The Digital Root 9 Indicator is suitable for use in any market condition and time frame.

Seasonality [TFO]This Seasonality indicator is meant to provide insight into an asset's average performance over specified periods of time (Daily, Monthly, and Quarterly). It is based on a 252 trading day calendar, not a 365 day calendar. Therefore, some estimations are used in order to aggregate the Daily data into higher timeframes, as we assume every Month to be 21 trading days, and every Quarter to be 63 trading days. Instead of collecting data on the 1st day of a given month, we are actually treating it as the "nth" trading day of the year. Some years exceed 252 trading days, some fall short; however 252 is the average that we are working with for US stocks and indices. Results may vary for non-US markets.

Main features:

- Statistics Table

- Performance Analysis

- Seasonal Pivots

The Statistics Table provides a summarized view of the current seasonality: whether the average Day/Month/Quarter tends to be bullish or bearish, what the average percent change is, and what the current (actual) change is relative to the historical value. It is shown in the top right of this chart.

The Performance Analysis shows a histogram of the average percentage performance for the selected timeframe. Here we have options for Daily, Monthly, and Quarterly. The previous chart showed the Monthly timeframe, here we have the Daily and Quarterly.

Lastly, Seasonal Pivots show where highs and lows tend to be created throughout the year, based on an aggregation of the Daily performance data collected over the available years. If we anchor our data to the beginning of the current year, and then manually offset it by ~252 (depending on the year), we can line this data up with the previous years' data and observe how well these Seasonal Pivots lined up with major Daily highs and lows.

Styling options are available for every major component of this indicator. Please consider sharing if you find it useful!

Weekly and daily separatorsThis script plots vertical line between each trading week (thick, solid) and smaller lines (dotted) between each trading day. This helps kepping a better overview on the aspect of time on the higher timeframes below 1D. The distance of the lines to the top and bottom of the chart is controlled by your chart settings menu under Appearance -> Margins.