Forex Relative Strength MatrixTraders often feel uncertain about which Forex pair to open a position with. This indicator is designed to help in that regard.

This indicator was created as described in the book Swing Trading with Heiken Ashi and Stochastics. In the original, the author suggests using it for swing trading. The author recommends applying it to a monthly chart with an 8-period moving average to analyze the context.

The logic of the indicator is to measure the relative strength of each currency by checking if the price of each Forex pair is above or below a chosen moving average. If the price is above the moving average, the base currency is awarded 1 point, indicating strength. If below, it scores 0, indicating weakness. By accumulating points across multiple pairs, the indicator ranks currencies from strongest to weakest, helping traders identify potential pairs for trading.

Trend Identification:

After identifying relative strength, the trader should observe the general trend using a 100-period SMA on 4-hour charts. If the price is above the SMA, the trend is bullish; if below, it is bearish.

Buy Logic:

A buy is triggered when the base currency is strong (price is above the moving average) and the quote currency is weak (price is below the moving average). After identifying the trend direction, the entry is confirmed by a color change in Heiken Ashi candles (from red to green in an uptrend) and a stochastic crossover in the trend’s direction.

Sell Logic:

A sell is triggered when the base currency is weak (price is below the moving average) and the quote currency is strong (price is above the moving average). The sell entry is confirmed by a color change in Heiken Ashi candles (from green to red in a downtrend) and a stochastic crossover aligned with the trend.

Entry Chart:

The entry chart used is the 4-hour chart. The trader should look for entry signals following a pullback in the trend direction, using Heiken Ashi candles. Entry is made when the Heiken Ashi candles change color (from red to green in an uptrend) and there is a smooth crossover of the stochastic indicator in the trend’s direction.

It would also be possible to adapt the indicator for day trading strategies with targets of 1 to 2 days. Here is a recommended setup:

Relative Strength Identification (1-Hour Chart):

Instead of monthly charts, use a 1-hour chart to identify currency strength with a 20-period moving average.

The 20-period moving average on the 1-hour chart captures a balanced view of short- to medium-term direction, covering nearly a day’s worth of trading but with enough sensitivity for day trading.

General Trend (5-Minute Chart with 100 SMA):

On the 5-minute chart, observe the 100-period SMA to identify the general trend direction throughout the day.

Price above the 100 SMA indicates an uptrend, and below indicates a downtrend, confirming the movement in shorter timeframes.

Entry Chart and Signals (5-Minute Chart):

Use the 15-minute chart to look for entry opportunities, focusing on pullbacks in the main trend direction.

Entry Signals: Enter the position when Heiken Ashi candles change color in the trend direction (from red to green in an uptrend) and the stochastic indicator makes a smooth crossover in the trend’s direction.

Циклический анализ

Hodrick-Prescott Cycle Component (YavuzAkbay)The Hodrick-Prescott Cycle Component indicator in Pine Script™ is an advanced tool that helps traders isolate and analyze the cyclical deviations in asset prices from their underlying trend. This script calculates the cycle component of the price series using the Hodrick-Prescott (HP) filter, allowing traders to observe and interpret the short-term price movements around the long-term trend. By providing two views—Percentage and Price Difference—this indicator gives flexibility in how these cyclical movements are visualized and interpreted.

What This Script Does

This indicator focuses exclusively on the cycle component of the price, which is the deviation of the current price from the long-term trend calculated by the HP filter. This deviation (or "cycle") is what traders analyze for mean-reversion opportunities and overbought/oversold conditions. The script allows users to see this deviation in two ways:

Percentage Difference: Shows the deviation as a percentage of the trend, giving a normalized view of the price’s distance from its trend component.

Price Difference: Shows the deviation in absolute price terms, reflecting how many price units the price is above or below the trend.

How It Works

Trend Component Calculation with the HP Filter: Using the HP filter, the script isolates the trend component of the price. The smoothness of this trend is controlled by the smoothness parameter (λ), which can be adjusted by the user. A higher λ value results in a smoother trend, while a lower λ value makes it more responsive to short-term changes.

Cycle Component Calculation: Percentage Deviation (cycle_pct) calculated as the difference between the current price and the trend, divided by the trend, and then multiplied by 100. This metric shows how far the price deviates from the trend in relative terms. Price Difference (cycle_price) simply the difference between the current price and the trend component, displaying the deviation in absolute price units.

Conditional Plotting: The user can choose to view the cycle component as either a percentage or a price difference by selecting the Display Mode input. The indicator will plot the chosen mode in a separate pane, helping traders focus on the preferred measure of deviation.

How to Use This Indicator

Identify Overbought/Oversold Conditions: When the cycle component deviates significantly from the zero line (shown with a dashed horizontal line), it may indicate overbought or oversold conditions. For instance, a high positive cycle component suggests the price may be overbought relative to the trend, while a large negative cycle suggests potential oversold conditions.

Mean-Reversion Strategy: In mean-reverting markets, traders can use this indicator to spot potential reversal points. For example, if the cycle component shows an extreme deviation from zero, it could signal that the price is likely to revert to the trend. This can help traders with entry and exit points when the asset is expected to correct back toward its trend.

Trend Strength and Cycle Analysis: By comparing the magnitude and duration of deviations, traders can gauge the strength of cycles and assess if a new trend might be forming. If the cycle component remains consistently positive or negative, it may indicate a persistent market bias, even as prices fluctuate around the trend.

Percentage vs. Price Difference Views: Use the Percentage Difference mode to standardize deviations and compare across assets or different timeframes. This is especially helpful when analyzing assets with varying price levels. Use the Price Difference mode when an absolute deviation (price units) is more intuitive for spotting overbought/oversold levels based on the asset’s actual price.

Using with Hodrick-Prescott: You can also use Hodrick-Prescott, another indicator that I have adapted to the Tradingview platform, to see the trend on the chart, and you can also use this indicator to see how far the price is deviating from the trend. This gives you a multifaceted perspective on your trades.

Practical Tips for Traders

Set the Smoothness Parameter (λ): Adjust the λ parameter to match your trading timeframe and asset characteristics. Lower values make the trend more sensitive, which might suit short-term trading, while higher values smooth out the trend for long-term analysis.

Cycle Component as Confirmation: Combine this indicator with other momentum or trend indicators for confirmation of overbought/oversold signals. For example, use the cycle component with RSI or MACD to validate the likelihood of mean-reversion.

Observe Divergences: Divergences between price movements and the cycle component can indicate potential reversals. If the price hits a new high, but the cycle component shows a smaller deviation than previous highs, it could signal a weakening trend.

Dual price forecast with Projection Zone [FXSMARTLAB]The Dual Price Forecast with Projection Zone indicator is built to simulate potential future price paths based on historical price movements over two defined lookback periods. By running multiple trials (or simulations) on these historical price movements, the indicator achieves a more robust forecast, incorporating the inherent variability of price behavior.

Key Components and Calculation Details

1. Lookback Periods and Historical Price Movements

Lookback Period 1 and Lookback Period 2 specify the range of past data used to generate each projection. For each period, the indicator calculates the price variations (differences between the closing and opening prices) and stores these in arrays.

These historical price variations capture the volatility and price patterns within each period, serving as templates for future price behavior.

2. Trials: Purpose and Function

The trials are a critical element in the projection calculation. Each trial represents a single simulation of possible future price movements, derived from a random reordering of the historical price variations in each lookback period.

By running multiple trials , the indicator explores various sequences of historical movements, simulating different possible future paths. Each trial adds to the projection’s robustness by capturing a unique potential price path based on past behavior.

Running these multiple trials allows the indicator to account for randomness in price behavior, making the projections more comprehensive by covering a range of scenarios rather than relying on a single deterministic forecast.

3. Reverse Option

The reverse option allows the indicator to invert the direction of price movements within each lookback period. When enabled, historical uptrends are treated as downtrends, and vice versa.

This feature is particularly valuable in scenarios where traders expect a potential reversal in market direction. By enabling the reverse option, the indicator can simulate what might happen if past trends inverted, providing an alternative forecast path that considers possible market reversals.

This allows traders to assess both continuation and reversal scenarios, giving them a more balanced view of potential future price paths and helping them prepare for either market direction.

4. Generating the Average Projection Path

Once the trials are complete, the indicator calculates an average projected price path for each lookback period by averaging the results of all trials. This average represents the most likely price trend based on historical data and provides a smoothed projection that mitigates extreme outliers.

By averaging across all trial paths, the indicator generates a more reliable and balanced forecast line, smoothing out the fluctuations that might appear if only one trial or a small number of trials were used.

5. Projection Zone Visualization

The indicator plots the two average projection paths (one for each lookback period) as Projection 1 and Projection 2, each in a user-defined color.

The Projection Zone is the area between these two lines, filled with a semi-transparent color. This zone visually represents the potential range of future price movement, highlighting where prices are likely to oscillate if historical trends persist.

The Projection Zone effectively functions as a potential support and resistance boundary, providing traders with a visual reference for possible price fluctuations within a specific range.

6. Display of Lookback Zones

To give context to the projections, the indicator can also display colored lookback zones on the chart. These zones correspond to Lookback Period 1 and Lookback Period 2 and are color-coded to match their respective projection lines.

These zones allow traders to see the sections of historical data used in the calculation, helping them understand which past price behaviors influenced the current projections.

Benefits of the Indicator

The "Dual Price Forecast with Projection Zone" indicator provides a multi-scenario forecast based on past price dynamics. Its use of trials ensures that projections are not based on a single deterministic path but on a range of possible scenarios that better reflect the inherent randomness in financial markets.

By generating a probabilistic forecast within a defined zone, the indicator helps traders to:

Anticipate potential price ranges and areas of support/resistance based on historical trends.

Understand the influence of different timeframes (short-term and long-term lookbacks) on future price behavior.

Make informed decisions by visualizing the likely variability of future prices within a controlled projection zone.

Prepare for both continuation and reversal scenarios, thanks to the reverse option. This feature is especially useful in markets where trends may change direction, as it allows traders to explore what might happen

MMRI Chart (Primary)The **Mannarino Market Risk Indicator (MMRI)** is a financial risk measurement tool created by financial strategist Gregory Mannarino. It’s designed to assess the risk level in the stock market and economy based on current bond market conditions and the strength of the U.S. dollar. The MMRI considers factors like the U.S. 10-Year Treasury Yield and the Dollar Index (DXY), which indicate investor confidence in government debt and the dollar's purchasing power, respectively.

The formula for MMRI uses the 10-Year Treasury Yield multiplied by the Dollar Index, divided by a constant (1.61) to normalize the risk measure. A higher MMRI score suggests increased market risk, while a lower score indicates more stability. Mannarino has set certain thresholds to interpret the MMRI score:

- **Below 100**: Low risk.

- **100–200**: Moderate risk.

- **200–300**: High risk.

- **Above 300**: Extreme risk, indicating market instability and potential downturns.

This tool aims to provide insight into economic conditions that may affect asset classes like stocks, bonds, and precious metals. Mannarino often updates MMRI scores and risk analyses in his public market updates.

Quick scan for cycles🙏🏻

The followup for

As I told before, ML based algorading is all about detecting any kind of non-randomness & exploiting it (cuz allegedly u cant trade randomness), and cycles are legit patterns that can be leveraged

But bro would u really apply Fourier / Wavelets / 'whatever else heavy' on every update of thousands of datasets, esp in real time on HFT / nearly HFT data? That's why this metric. It works much faster & eats hell of a less electicity, will do initial rough filtering of time series that might contain any kind of cyclic behaviour. And then, only on these filtered datasets u gonna put Periodograms / Autocorrelograms and see what's going there for real. Better to do it 10x times less a day on 10x less datasets, right?

I ended up with 2 methods / formulas, I called em 'type 0' and 'type 1':

- type 0: takes sum of abs deviations from drift line, scales it by max abs deviation from the same drift line;

- type 1: takes sum of abs deviations from drift line, scales it by range of non-abs deviations from the same drift line.

Finnaly I've chosen type 0 , both logically (sum of abs dev divided by max abs dev makes more sense) and experimentally. About that actually, here are both formulas put on sine waves with uniform noise:

^^ generated sine wave with uniform noise

^^ both formulas on that wave

^^ both formulas on real data

As you can see type 0 is less affected by noise and shows higher values on synthetic data, but I decided to put type 1 inside as well, in case my analysis was not complete and on real data type 1 can actually be better since it has a lil higher info gain / info content (still not sure). But I can assure u that out of all other ways I've designed & tested for quite a time I tell you, these 2 are really the only ones who got there.

Now about dem thresholds and how to use it.

Both type 0 and type 1 can be modelled with Beta distribution, and based on it and on some obvious & tho non mainstream statistical modelling techniques, I got these thresholds, so these are not optimized overfitted values, but natural ones. Each type has 3 thresholds (from lowest to highest):

- typical value (turned off by default). aka basis ;

- typical deviation from typical value, aka deviation ;

- maximum modelled deviation from typical value (idk whow to call it properly for now, this is my own R&D), aka extension .

So when the metric is above one of these thresholds (which one is up to you, you'll read about it in a sec), it means that there might be a strong enough periodic signal inside the data, and the data got to be put through proper spectral analysis tools to confirm / deny it.

If you look at the pictures above again, you'll see gray signal, that's uniform noise. Take a look at it and see where does it sit comparing to the thresholds. Now you just undertand that picking up a threshold is all about the amount of false positives you care to withstand.

If you take basis as threshold, you'll get tons of false positives (that's why it's even turned off by default), but you'll almost never miss a true positive. If you take deviation as threshold, it's gonna be kinda balanced approach. If you take extension as threshold, you gonna miss some cycles, and gonna get only the strongest ones.

More true positives -> more false positives, less false positives -> less true positives, can't go around that mane

Just to be clear again, I am not completely sure yet, but I def lean towards type 0 as metric, and deviation as threshold.

Live Long and Prosper

P.S.: That was actually the main R&D of the last month, that script I've released earlier came out as derivative.

P.S.: These 2 are the first R&Ds made completely in " art-space", St. Petersburg. Come and see me, say wassup🤘🏻

S&P 100 Option Expiration Week StrategyThe Option Expiration Week Strategy aims to capitalize on increased volatility and trading volume that often occur during the week leading up to the expiration of options on stocks in the S&P 100 index. This period, known as the option expiration week, culminates on the third Friday of each month when stock options typically expire in the U.S. During this week, investors in this strategy take a long position in S&P 100 stocks or an equivalent ETF from the Monday preceding the third Friday, holding until Friday. The strategy capitalizes on potential upward price pressures caused by increased option-related trading activity, rebalancing, and hedging practices.

The phenomenon leveraged by this strategy is well-documented in finance literature. Studies demonstrate that options expiration dates have a significant impact on stock returns, trading volume, and volatility. This effect is driven by various market dynamics, including portfolio rebalancing, delta hedging by option market makers, and the unwinding of positions by institutional investors (Stoll & Whaley, 1987; Ni, Pearson, & Poteshman, 2005). These market activities intensify near option expiration, causing price adjustments that may create short-term profitable opportunities for those aware of these patterns (Roll, Schwartz, & Subrahmanyam, 2009).

The paper by Johnson and So (2013), Returns and Option Activity over the Option-Expiration Week for S&P 100 Stocks, provides empirical evidence supporting this strategy. The study analyzes the impact of option expiration on S&P 100 stocks, showing that these stocks tend to exhibit abnormal returns and increased volume during the expiration week. The authors attribute these patterns to intensified option trading activity, where demand for hedging and arbitrage around options expiration causes temporary price adjustments.

Scientific Explanation

Research has found that option expiration weeks are marked by predictable increases in stock returns and volatility, largely due to the role of options market makers and institutional investors. Option market makers often use delta hedging to manage exposure, which requires frequent buying or selling of the underlying stock to maintain a hedged position. As expiration approaches, their activity can amplify price fluctuations. Additionally, institutional investors often roll over or unwind positions during expiration weeks, creating further demand for underlying stocks (Stoll & Whaley, 1987). This increased demand around expiration week typically leads to temporary stock price increases, offering profitable opportunities for short-term strategies.

Key Research and Bibliography

Johnson, T. C., & So, E. C. (2013). Returns and Option Activity over the Option-Expiration Week for S&P 100 Stocks. Journal of Banking and Finance, 37(11), 4226-4240.

This study specifically examines the S&P 100 stocks and demonstrates that option expiration weeks are associated with abnormal returns and trading volume due to increased activity in the options market.

Stoll, H. R., & Whaley, R. E. (1987). Program Trading and Expiration-Day Effects. Financial Analysts Journal, 43(2), 16-28.

Stoll and Whaley analyze how program trading and portfolio insurance strategies around expiration days impact stock prices, leading to temporary volatility and increased trading volume.

Ni, S. X., Pearson, N. D., & Poteshman, A. M. (2005). Stock Price Clustering on Option Expiration Dates. Journal of Financial Economics, 78(1), 49-87.

This paper investigates how option expiration dates affect stock price clustering and volume, driven by delta hedging and other option-related trading activities.

Roll, R., Schwartz, E., & Subrahmanyam, A. (2009). Options Trading Activity and Firm Valuation. Journal of Financial Markets, 12(3), 519-534.

The authors explore how options trading activity influences firm valuation, finding that higher options volume around expiration dates can lead to temporary price movements in underlying stocks.

Cao, C., & Wei, J. (2010). Option Market Liquidity and Stock Return Volatility. Journal of Financial and Quantitative Analysis, 45(2), 481-507.

This study examines the relationship between options market liquidity and stock return volatility, finding that increased liquidity needs during expiration weeks can heighten volatility, impacting stock returns.

Summary

The Option Expiration Week Strategy utilizes well-researched financial market phenomena related to option expiration. By positioning long in S&P 100 stocks or ETFs during this period, traders can potentially capture abnormal returns driven by option market dynamics. The literature suggests that options-related activities—such as delta hedging, position rollovers, and portfolio adjustments—intensify demand for underlying assets, creating short-term profit opportunities around these key dates.

Payday Anomaly StrategyThe "Payday Effect" refers to a predictable anomaly in financial markets where stock returns exhibit significant fluctuations around specific pay periods. Typically, these are associated with the beginning, middle, or end of the month when many investors receive wages and salaries. This influx of funds, often directed automatically into retirement accounts or investment portfolios (such as 401(k) plans in the United States), temporarily increases the demand for equities. This phenomenon has been linked to a cycle where stock prices rise disproportionately on and around payday periods due to increased buy-side liquidity.

Academic research on the payday effect suggests that this pattern is tied to systematic cash flows into financial markets, primarily driven by employee retirement and savings plans. The regularity of these cash infusions creates a calendar-based pattern that can be exploited in trading strategies. Studies show that returns on days around typical payroll dates tend to be above average, and this pattern remains observable across various time periods and regions.

The rationale behind the payday effect is rooted in the behavioral tendencies of investors, specifically the automatic reinvestment mechanisms used in retirement funds, which align with monthly or semi-monthly salary payments. This regular injection of funds can cause market microstructure effects where stock prices temporarily increase, only to stabilize or reverse after the funds have been invested. Consequently, the payday effect provides traders with a potentially profitable opportunity by predicting these inflows.

Scientific Bibliography on the Payday Effect

Ma, A., & Pratt, W. R. (2017). Payday Anomaly: The Market Impact of Semi-Monthly Pay Periods. Social Science Research Network (SSRN).

This study provides a comprehensive analysis of the payday effect, exploring how returns tend to peak around payroll periods due to semi-monthly cash flows. The paper discusses how systematic inflows impact returns, leading to predictable stock performance patterns on specific days of the month.

Lakonishok, J., & Smidt, S. (1988). Are Seasonal Anomalies Real? A Ninety-Year Perspective. The Review of Financial Studies, 1(4), 403-425.

This foundational study explores calendar anomalies, including the payday effect. By examining data over nearly a century, the authors establish a framework for understanding seasonal and monthly patterns in stock returns, which provides historical support for the payday effect.

Owen, S., & Rabinovitch, R. (1983). On the Predictability of Common Stock Returns: A Step Beyond the Random Walk Hypothesis. Journal of Business Finance & Accounting, 10(3), 379-396.

This paper investigates predictability in stock returns beyond random fluctuations. It considers payday effects among various calendar anomalies, arguing that certain dates yield predictable returns due to regular cash inflows.

Loughran, T., & Schultz, P. (2005). Liquidity: Urban versus Rural Firms. Journal of Financial Economics, 78(2), 341-374.

While primarily focused on liquidity, this study provides insight into how cash flows, such as those from semi-monthly paychecks, influence liquidity levels and consequently impact stock prices around predictable pay dates.

Ariel, R. A. (1990). High Stock Returns Before Holidays: Existence and Evidence on Possible Causes. The Journal of Finance, 45(5), 1611-1626.

Ariel’s work highlights stock return patterns tied to certain dates, including paydays. Although the study focuses on pre-holiday returns, it suggests broader implications of predictable investment timing, reinforcing the calendar-based effects seen with payday anomalies.

Summary

Research on the payday effect highlights a repeating pattern in stock market returns driven by scheduled payroll investments. This cyclical increase in stock demand aligns with behavioral finance insights and market microstructure theories, offering a valuable basis for trading strategies focused on the beginning, middle, and end of each month.

Asian Session ShadingDescription

The "Asian Session Shading" indicator is designed to highlight the trading hours of the Asian market session on TradingView charts. This script shades the background of the chart in a pale blue color to visually distinguish the time period of the Asian trading session. By using this indicator, traders can easily identify when the Asian session is active, helping them to analyze and make informed trading decisions based on time-specific market behavior.

Features

Customizable Timing: The session start and end times can be adjusted to fit different Asian market hours.

Visual Clarity: The pale blue shading helps to visually separate the Asian session from other trading sessions.

Easy to Use: Simple implementation with clear visual cues on the chart.

Best Use Cases

Market Analysis: Traders can use this indicator to analyze market movements and trends specific to the Asian trading session.

Trading Strategies: This tool can assist in developing and implementing trading strategies that take into account the unique characteristics of the Asian market.

Time Management: Helps traders to manage their trading schedule by clearly marking the start and end of the Asian session.

How to Use

Apply to Chart: Save and apply the indicator to your chart to see the shaded Asian session.

This indicator is particularly useful for forex traders, stock traders, and anyone looking to incorporate the Asian market's influence into their trading strategy.

Customizable BTC Seasonality StrategyThis strategy leverages intraday seasonality effects in Bitcoin, specifically targeting hours of statistically significant returns during periods when traditional financial markets are closed. Padysak and Vojtko (2022) demonstrate that Bitcoin exhibits higher-than-average returns from 21:00 UTC to 23:00 UTC, a period in which all major global exchanges, such as the New York Stock Exchange (NYSE), Tokyo Stock Exchange, and London Stock Exchange, are closed. The absence of competing trading activity from traditional markets during these hours appears to contribute to these statistically significant returns.

The strategy proceeds as follows:

Entry Time: A long position in Bitcoin is opened at a user-specified time, which defaults to 21:00 UTC, aligning with the beginning of the identified high-return window.

Holding Period: The position is held for two hours, capturing the positive returns typically observed during this period.

Exit Time: The position is closed at a user-defined time, defaulting to 23:00 UTC, allowing the strategy to exit as the favorable period concludes.

This simple seasonality strategy aims to achieve a 33% annualized return with a notably reduced volatility of 20.93% and maximum drawdown of -22.45%. The results suggest that investing only during these high-return hours is more stable and less risky than a passive holding strategy (Padysak & Vojtko, 2022).

References

Padysak, M., & Vojtko, R. (2022). Seasonality, Trend-following, and Mean reversion in Bitcoin.

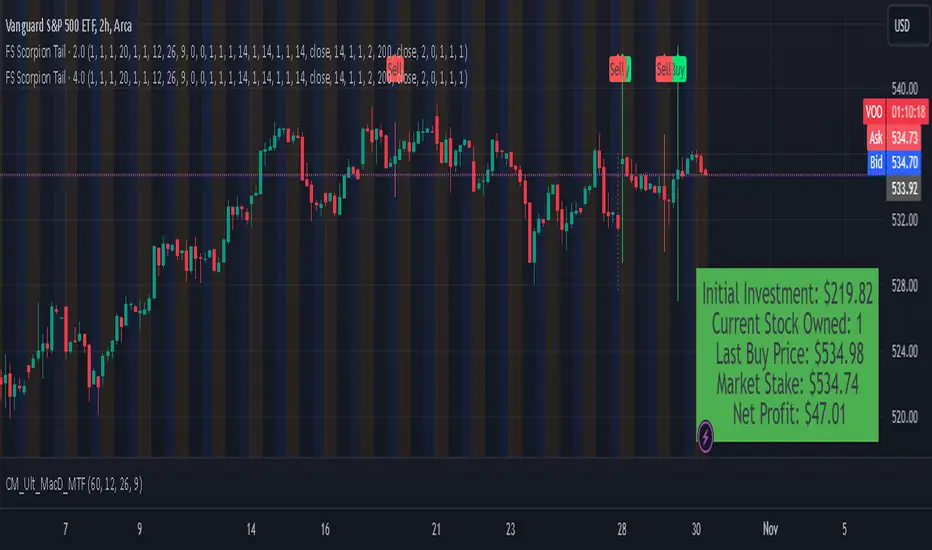

FS Scorpion TailKey Features & Components:

1. Custom Date & Chart-Based Controls

The software allows users to define whether they want signals to start on a specific date (useSpecificDate) or base calculations on the visible chart’s range (useRelativeScreenSumLeft and useRelativeScreenSumRight).

Users can input the number of stocks to buy/sell per signal and decide whether to sell only for profit.

2. Technical Indicators Used

EMA (Exponential Moving Average): Users can define the length of the EMA and specify if buy/sell signals should occur when the EMA is rising or falling.

MACD (Moving Average Convergence Divergence): MACD crossovers, slopes of the MACD line, signal line, and histogram are used for generating buy/sell signals.

ATR (Average True Range): Signals are generated based on rising or falling ATR.

Aroon Indicator: Buy and sell signals are based on the behavior of the Aroon upper and lower lines.

RSI (Relative Strength Index): Tracks whether the RSI and its moving average are rising or falling to generate signals.

Bollinger Bands: Buy/sell signals depend on the basis, upper, and lower band behavior (rising or falling).

3. Signal Detection

The software creates arrays for each indicator to store conditions for buy/sell signals.

The allTrue() function checks whether all conditions for buy/sell signals are true, ensuring that only valid signals are plotted.

Signals are differentiated between buy-only, sell-only, and both buy and sell (dual signal).

4. Visual Indicators

Vertical Lines: When buy, sell, or dual signals are detected, vertical lines are drawn at the corresponding bar with configurable colors (green for buy, red for sell, silver for dual).

Buy/Sell Labels: Visual labels are plotted directly on the chart to denote buy or sell signals, allowing for clear interpretation of the strategy.

5. Cash Flow & Metrics Display

The software maintains an internal ledger of how many stocks are bought/sold, their prices, and whether a profit is being made.

A table is displayed at the bottom right of the chart, showing:

Initial investment

Current stocks owned

Last buy price

Market stake

Net profit

The table background turns green for profit and red for loss.

6. Dynamic Decision Making

Buy Condition: If a valid buy signal is generated, the software decrements the cash balance and adds stocks to the inventory.

Sell Condition: If the sell signal is valid (and meets the profit requirement), stocks are sold, and cash is incremented.

A fallback check ensures the sell logic prevents selling more stocks than are available and adjusts stock holding appropriately (e.g., sell half).

Customization and Usage

Indicator Adjustments: The user can choose which indicators to activate (e.g., EMA, MACD, RSI) via input controls. Each indicator has specific customizable parameters such as lengths, slopes, and conditions.

Signal Flexibility: The user can adjust conditions for buying and selling based on various technical indicators, which adds flexibility in implementing trading strategies. For example, users may require the RSI to be higher than its moving average or trigger sales only when MACD crosses under the signal line.

Profit Sensitivity: The software allows the option to sell only when a profit is assured by checking if the current price is higher than the last buy price.

Summary of Usage:

Indicator Selection: Enable or disable technical indicators like EMA, MACD, RSI, Aroon, ATR, and Bollinger Bands to fit your trading strategy.

Custom Date/Chart Settings: Choose whether to calculate based on specific time ranges or visible portions of the chart.

Dynamic Signal Plotting: Once buy or sell conditions are met, the software will visually plot signals on your chart, giving clear entry and exit points.

Investment Tracking: Real-time tracking of stock quantities, investments, and profit ensures a clear view of your trading performance.

Backtesting: Use this software for backtesting your strategy by analyzing how buy and sell signals would have performed historically based on the chosen indicators.

Conclusion

The FS Scorpion Tail software is a robust and flexible trading tool, allowing traders to develop custom strategies based on multiple well-known technical indicators. Its visual aid, coupled with real-time investment tracking, makes it valuable for systematic traders looking to automate or refine their trading approach.

Momentum Entry & Trend Strategy M5Momentum Entry & Trend Strategy M5

Description:

The Momentum Entry & Trend Strategy M5 is an indicator script designed to assist traders in determining optimal buy and sell moments based on momentum and trend analysis. This script operates using two different momentum levels—Momentum Length for Entry (5) and Momentum Length for Trend (10)—along with the HMA (Hull Moving Average) indicator for trend confirmation.

Key Features:

Momentum Entry: Calculates momentum using the difference between the current price and the price from previous periods to determine the strength and direction of price movements.

Trend Identification: Utilizes two momentum levels (5 and 10) to identify bullish and bearish trend conditions.

HMA for Trend Confirmation: The HMA indicator is used to provide trend confirmation signals. When HMA indicates bullish, a buy signal is displayed; conversely, a bearish HMA results in a sell signal.

Signal Display: Displays buy (BUY) and sell (SELL) signals on the chart when the conditions for market entry are met, providing clear visualization for traders.

Background Color: Offers a green background for uptrends and a red background for downtrends, allowing traders to easily identify the overall market condition.

ATR (Average True Range): Calculates and plots a smoothed ATR to help traders measure market volatility.

Settings:

Momentum Length for Entry: 5 (to determine entry signals)

Momentum Length for Trend: 10 (to determine trend conditions)

HMA Length: 300 (period length for HMA to confirm trends)

ATR Length: 14 (period length for ATR to measure volatility)

Benefits:

This script is designed to provide visual and data-driven guidance for better trading decision-making. By combining momentum and trend analysis, traders can enhance the accuracy of their signals and reduce the risk of errors when identifying entry and exit points in the market.

Note:

This script is intended for use on the M5 time frame but can be adjusted for other time frames as needed. It is always recommended to conduct thorough testing before applying trading strategies on a live account.

EMD Oscillator (Zeiierman)█ Overview

The Empirical Mode Decomposition (EMD) Oscillator is an advanced indicator designed to analyze market trends and cycles with high precision. It breaks down complex price data into simpler parts called Intrinsic Mode Functions (IMFs), allowing traders to see underlying patterns and trends that aren’t visible with traditional indicators. The result is a dynamic oscillator that provides insights into overbought and oversold conditions, as well as trend direction and strength. This indicator is suitable for all types of traders, from beginners to advanced, looking to gain deeper insights into market behavior.

█ How It Works

The core of this indicator is the Empirical Mode Decomposition (EMD) process, a method typically used in signal processing and advanced scientific fields. It works by breaking down price data into various “layers,” each representing different frequencies in the market’s movement. Imagine peeling layers off an onion: each layer (or IMF) reveals a different aspect of the price action.

⚪ Data Decomposition (Sifting): The indicator “sifts” through historical price data to detect natural oscillations within it. Each oscillation (or IMF) highlights a unique rhythm in price behavior, from rapid fluctuations to broader, slower trends.

⚪ Adaptive Signal Reconstruction: The EMD Oscillator allows traders to select specific IMFs for a custom signal reconstruction. This reconstructed signal provides a composite view of market behavior, showing both short-term cycles and long-term trends based on which IMFs are included.

⚪ Normalization: To make the oscillator easy to interpret, the reconstructed signal is scaled between -1 and 1. This normalization lets traders quickly spot overbought and oversold conditions, as well as trend direction, without worrying about the raw magnitude of price changes.

The indicator adapts to changing market conditions, making it effective for identifying real-time market cycles and potential turning points.

█ Key Calculations: The Math Behind the EMD Oscillator

The EMD Oscillator’s advanced nature lies in its high-level mathematical operations:

⚪ Intrinsic Mode Functions (IMFs)

IMFs are extracted from the data and act as the building blocks of this indicator. Each IMF is a unique oscillation within the price data, similar to how a band might be divided into treble, mid, and bass frequencies. In the EMD Oscillator:

Higher-Frequency IMFs: Represent short-term market “noise” and quick fluctuations.

Lower-Frequency IMFs: Capture broader market trends, showing more stable and long-term patterns.

⚪ Sifting Process: The Heart of EMD

The sifting process isolates each IMF by repeatedly separating and refining the data. Think of this as filtering water through finer and finer mesh sieves until only the clearest parts remain. Mathematically, it involves:

Extrema Detection: Finding all peaks and troughs (local maxima and minima) in the data.

Envelope Calculation: Smoothing these peaks and troughs into upper and lower envelopes using cubic spline interpolation (a method for creating smooth curves between data points).

Mean Removal: Calculating the average between these envelopes and subtracting it from the data to isolate one IMF. This process repeats until the IMF criteria are met, resulting in a clean oscillation without trend influences.

⚪ Spline Interpolation

The cubic spline interpolation is an advanced mathematical technique that allows smooth curves between points, which is essential for creating the upper and lower envelopes around each IMF. This interpolation solves a tridiagonal matrix (a specialized mathematical problem) to ensure that the envelopes align smoothly with the data’s natural oscillations.

To give a relatable example: imagine drawing a smooth line that passes through each peak and trough of a mountain range on a map. Spline interpolation ensures that line is as smooth and close to reality as possible. Achieving this in Pine Script is technically demanding and demonstrates a high level of mathematical coding.

⚪ Amplitude Normalization

To make the oscillator more readable, the final signal is scaled by its maximum amplitude. This amplitude normalization brings the oscillator into a range of -1 to 1, creating consistent signals regardless of price level or volatility.

█ Comparison with Other Signal Processing Methods

Unlike standard technical indicators that often rely on fixed parameters or pre-defined mathematical functions, the EMD adapts to the data itself, capturing natural cycles and irregularities in real-time. For example, if the market becomes more volatile, EMD adjusts automatically to reflect this without requiring parameter changes from the trader. In this way, it behaves more like a “smart” indicator, intuitively adapting to the market, unlike most traditional methods. EMD’s adaptive approach is akin to AI’s ability to learn from data, making it both resilient and robust in non-linear markets. This makes it a great alternative to methods that struggle in volatile environments, such as fixed-parameter oscillators or moving averages.

█ How to Use

Identify Market Cycles and Trends: Use the EMD Oscillator to spot market cycles that represent phases of buying or selling pressure. The smoothed version of the oscillator can help highlight broader trends, while the main oscillator reveals immediate cycles.

Spot Overbought and Oversold Levels: When the oscillator approaches +1 or -1, it may indicate that the market is overbought or oversold, signaling potential entry or exit points.

Confirm Divergences: If the price movement diverges from the oscillator's direction, it may indicate a potential reversal. For example, if prices make higher highs while the oscillator makes lower highs, it could be a sign of weakening trend strength.

█ Settings

Window Length (N): Defines the number of historical bars used for EMD analysis. A larger window captures more data but may slow down performance.

Number of IMFs (M): Sets how many IMFs to extract. Higher values allow for a more detailed decomposition, isolating smaller cycles within the data.

Amplitude Window (L): Controls the length of the window used for amplitude calculation, affecting the smoothness of the normalized oscillator.

Extraction Range (IMF Start and End): Allows you to select which IMFs to include in the reconstructed signal. Starting with lower IMFs captures faster cycles, while ending with higher IMFs includes slower, trend-based components.

Sifting Stopping Criterion (S-number): Sets how precisely each IMF should be refined. Higher values yield more accurate IMFs but take longer to compute.

Max Sifting Iterations (num_siftings): Limits the number of sifting iterations for each IMF extraction, balancing between performance and accuracy.

Source: The price data used for the analysis, such as close or open prices. This determines which price movements are decomposed by the indicator.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

CRT AMD indicatorThis indicator is based on the Power of three (Accumulation Manipulation Distribution) Cycle, by marking the candle that Sweep the low or high of the previous candle and then closed back inside the range of the previous candle, indicating a possibility of a Manipulation or Reversal.

Combining the indicator with HTF Array and LTF Setup Entry will significantly improve the accuracy.

Custom Time Frame BackgroundThis indicator allows you to highlight custom time frames on your chart with alternating background colors. It's particularly useful for visualizing specific intervals that are not standard on TradingView, such as 4-hour, 6-hour, or any other custom duration you choose. Features:

Customizable time frames: Set any combination of minutes, hours, and days

Fallback to daily/weekly coloring if no custom time frame is set

User-defined colors for alternating backgrounds

How to use:

Add the indicator to your chart

In the settings, input your desired custom time frame:

Set 'Custom Minutes' for intervals less than an hour

Use 'Custom Hours' for hourly intervals

Use 'Custom Days' for daily intervals

Adjust 'Color 1' and 'Color 2' to your preferred background colors

Examples:

For a 4-hour time frame: Set Custom Hours to 4

For a 6-hour time frame: Set Custom Hours to 6

For a 2-day time frame: Set Custom Days to 2

If all inputs are set to 0, the indicator will default to daily coloring for intraday charts and weekly coloring for higher timeframes. This indicator helps traders visually segment their charts into custom intervals, making it easier to identify patterns and trends over specific time periods.

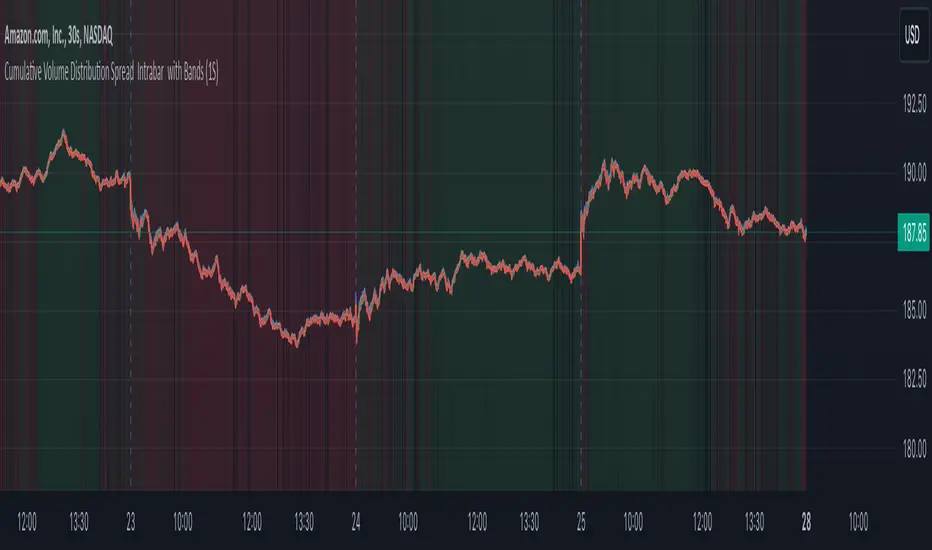

Cumulative Volume Distribution Spread Intrabar with BandsUpdated Description:

This script, "Cumulative Volume Spread by Levels with Histogram", analyzes cumulative buying and selling pressure at various price levels of each bar, based on intra-bar data from a lower timeframe (like 1-second bars). It visualizes the results using lines, histograms, and color-filled areas.

Key Concepts:

Price Levels: The script splits each bar into four distinct levels:

High to max(open, close): The range from the highest price of the bar to the higher of the open or close prices.

Max(open, close) to midline: The range from the higher of the open or close to the midpoint of the bar.

Midline to min(open, close): The range from the midpoint to the lower of the open or close.

Min(open, close) to low: The range from the lower of the open or close to the lowest price of the bar.

Volume Pressures:

The script fetches volume data from a lower timeframe (default is 1-second bars) to capture intra-bar buying and selling pressure.

Buying Pressure: Calculated when the close is greater than the open.

Selling Pressure: Calculated when the close is less than the open.

Cumulative Pressures:

The script accumulates buy and sell volumes within each of the four price levels described above.

At the beginning of a new day, these cumulative values are reset.

Spread Calculation:

For each level, the script calculates the spread between cumulative buying and selling volumes (i.e., buy pressure minus sell pressure). A positive spread indicates more buying pressure, and a negative spread indicates more selling pressure.

The script calculates an Exponential Moving Average (EMA) of the spread changes for each section:

EMA Spread High to Max Open/Close

EMA Spread Max Open/Close to Midline

EMA Spread Midline to Min Open/Close

EMA Spread Min Open/Close to Low

Fill Between Levels:

The areas between the key price levels are filled based on whether the EMA of the spread is positive (green) or negative (red). This helps to visually indicate where buying or selling pressure is stronger.

Background Color:

The script determines an overall background color based on the relative strength of cumulative buying vs. selling pressure. If cumulative buying pressure is stronger across the levels, the background turns green; if selling pressure dominates, it turns red.

Harmony Signal Flow By ArunThis Pine Script strategy, titled "Harmony Signal Flow By Arun," uses the Relative Strength Index (RSI) indicator to generate buy and sell signals based on custom thresholds. The script incorporates stop-loss and target management and restricts new trades until the previous position closes. Here's a detailed description:

Custom RSI Metric:

The strategy calculates a 5-period RSI based on the closing price, aiming for a more responsive measure of price momentum.

RSI thresholds are defined:

Lower threshold (30): Indicates oversold conditions, triggering a potential buy.

Upper threshold (70): Indicates overbought conditions, prompting a possible sell.

Entry Conditions:

Buy Signal: The strategy initiates a buy order when the RSI crosses above the lower threshold (30), indicating a shift from oversold conditions.

Sell Signal: A sell order is triggered when the RSI crosses below the upper threshold (70), suggesting an overbought reversal.

Only one order (buy or sell) can be active at a time, ensuring that a new trade begins only when there’s no existing position.

Stop-Loss and Target Management:

For each trade, stop-loss and target conditions are applied to manage risk and secure profits.

For Buy Positions:

Stop-loss is set 100 points below the entry price.

Target is set 150 points above the entry price.

For Sell Positions:

Stop-loss is set 100 points above the entry price.

Target is 150 points below the entry price.

The strategy closes the trade when either the stop-loss or target is met, marking the trade as "closed" and allowing a new trade entry.

Trade Sequencing:

A new trade (buy or sell) is only permitted after the previous position hits either its stop-loss or target, preventing overlapping trades and ensuring clear trade sequences.

This sequential approach enhances risk management by ensuring only one active position at any time.

End-of-Day Closure:

All open positions are closed automatically at 3:25 PM (Indian market time) to avoid overnight exposure, ensuring the strategy remains strictly intraday.

The flag for trade entry is reset at the end of each day, enabling fresh trades the next day.

Chart Indicators:

The script plots buy and sell signals directly on the chart with visible labels.

It also displays the custom RSI metric with horizontal lines for the lower and upper thresholds, providing visual cues for entry and exit points.

Summary

This strategy is a momentum-based intraday trading approach that uses the RSI for identifying potential reversals and manages trades through predefined stop-loss and target levels. By enforcing trade sequencing and closing positions at the end of the trading day, it prioritizes risk management and seeks to capitalize on short-term trends while avoiding overnight market risks.

Indicator SELL UBScript Name: UB Sell Indicator based on 10Y Volume and Trend

Description: This indicator uses the 10-year interest rate (10Y1!) volume and price data to generate sell signals on the UB contract. When the 10Y1! volume exceeds a fixed threshold and the 10Y1! price is rising, a sell signal is issued to help traders anticipate bearish moves on the UB.

Features:

10Y1! Volume: Identifies periods of high volume.

10Y1! Price: Detects bullish trends in the 10Y1!.

Sell Signals: Displays red arrows to indicate selling opportunities on UB when conditions are met.

Visual Indicators: Colors and arrows for easy signal interpretation.

Parameters:

Fixed Volume Threshold: 114 (modifiable as needed).

Moving Average Period: 10 (to calculate the 10Y1! price trend).

Usage:

Watch for red arrows to identify selling opportunities on UB.

Combine with other analyses and indicators for a complete trading strategy.

Author: Jm Smeers

Publication Date: 26/10/2024

Ultimate Machine Learning MACD (Deep Learning Edition)This script is a "Deep Learning MACD" indicator that combines traditional MACD calculations with advanced machine learning techniques, including recursive feedback, adaptive learning rates, Monte Carlo simulations, and volatility-based adjustments. Here’s a breakdown of its key components:

Inputs

Lookback: The length of historical data (1000 by default) used for learning and volatility measurement.

Momentum and Volatility Weighting: Adjusts how much momentum and volatility contribute to the learning process (momentum weight: 1.2, volatility weight: 1.5).

MACD Lengths: Defines the range for MACD fast and slow lengths, starting at minimum of 1 and max of 1000.

Learning Rate: Defines how much the model learns from its predictions (very small learning rate by default).

Adaptive Learning: Enables dynamic learning rates based on market volatility.

Memory Factor: A feedback factor that determines how much weight past performance has in the current model.

Simulations: The number of Monte Carlo simulations used for probabilistic modeling.

Price Change: Calculated as the difference between the current and previous close.

Momentum: Measured using a lookback period (1000 bars by default).

Volatility: Standard deviation of closing prices.

ATR: Average true range over 14 periods for measuring market volatility.

Custom EMA Calculation

Implements an exponential moving average (EMA) formula from scratch using a recursive calculation with a smoothing factor.

Dynamic Learning Rate

Adjusts the learning rate based on market volatility. When volatility is high, the learning rate increases, and when volatility is low, it decreases. This makes the model more responsive during volatile markets and more stable during calm periods.

Error Calculation and Adjustment

Error Calculation: Measures the difference between the predicted value (via Monte Carlo simulations) and the true MACD value.

Adjust MACD Length: Uses the error to adjust the fast and slow MACD lengths dynamically, so the system can learn from market conditions.

Probabilistic Monte Carlo Simulation

Runs multiple simulations (200 by default) to generate probabilistic predictions. It uses random values weighted by momentum and volatility to simulate various market scenarios, enhancing

prediction accuracy.

MACD Calculation (Learning-Enhanced)

A custom MACD function that calculates:

Fast EMA and Slow EMA for MACD line.

Signal Line: An EMA of the MACD line.

Histogram: The difference between the MACD and signal lines.

Adaptive MACD Calculation

Adjusts the fast and slow MACD lengths based on the error from the Monte Carlo prediction.

Calculates the adaptive MACD, signal, and histogram using dynamically adjusted lengths.

Recursive Memory Feedback

Stores previous MACD values in an array (macdMemory) and averages them to create a feedback loop. This adds a "memory" to the system, allowing it to learn from past behaviors and refine future predictions.

Volatility-Based Reinforcement

Introduces a volatility reinforcement factor that influences the signal based on market conditions. It adds volatility awareness to the feedback system, making the system more reactive during high volatility periods.

Smoothed MACD

After all the adjustments, the MACD line is further smoothed based on the current market volatility, resulting in a final smoothed MACD.

Key Features

Monte Carlo Simulation: Runs multiple simulations to enhance predictions based on randomness and market behavior.

Adaptive Learning: Dynamic adjustments of learning rates and MACD lengths based on market conditions.

Recursive Feedback: Uses past data as feedback to refine the system’s predictions over time.

Volatility Awareness: Integrates market volatility into the system, making the MACD more responsive to market fluctuations.

This combination of traditional MACD with machine learning creates an adaptive indicator capable of learning from past behaviors and adjusting its sensitivity based on changing market conditions.

Ultimate Machine Learning RSI (Deep Learning Edition)This script represents an advanced implementation of a Machine Learning-based Relative Strength Index (RSI) indicator in Pine Script, incorporating several sophisticated techniques to create a more adaptive, intelligent, and responsive RSI.

Key Components and Features:

Lookback Period: The period over which the indicator "learns" from past data, set to 1000 bars by default.

Momentum and Volatility Weighting: These factors control how much the momentum and volatility of the market influence the learning and signal generation.

RSI Length Range: The minimum and maximum values for the RSI length, allowing the algorithm to adjust the RSI length dynamically.

Learning Rate: Controls how quickly the system adapts to new data. An adaptive learning rate can change based on market volatility.

Memory Factor: Influences how much the system "remembers" previous performance when making adjustments.

Monte Carlo Simulations: Used for probabilistic modeling to create a more robust signal.

\

Price Change: Tracks the difference between the current close and the previous close.

Momentum: A measure of the rate of change in the price over the lookback period.

Volatility: Calculated using the standard deviation of the close prices.

ATR (Average True Range): Tracks the volatility of the market over a short period to influence decisions.

Monte Carlo Simulation:

Probabilistic Signal: This uses multiple random simulations (Monte Carlo) to generate potential future signals. These simulations are weighted by the momentum and volatility of the market. A cluster factor further enhances the simulation based on volatility regimes.

Z-Score for Extreme Conditions:

Z-Score: Measures how extreme current price movements are compared to the historical average, providing context for identifying overbought and oversold conditions.

Dynamic Learning Rate:

The learning rate adjusts based on the volatility of the market, becoming more responsive in high-volatility periods and slower in low-volatility markets. This prevents the system from overreacting to noise but ensures responsiveness to significant shifts.

Recursive Learning and Feedback:

Error Calculation: The system calculates the difference between the true RSI and the predicted RSI, creating an error that is fed back into the system to adjust the RSI length and other parameters dynamically.

RSI Length Adjustment: Based on the error, the RSI length is adjusted, ensuring that the system evolves over time to better reflect market conditions.

Adaptive Smoothing:

In periods of high volatility, the indicator applies a Triple Exponential Moving Average (TEMA) for faster adaptation, while in quieter markets, it uses an Exponential Moving Average (EMA) for smoother adjustments.

Recursive Memory Feedback:

The system maintains a memory of past RSI values, which helps refine the output further. The memory factor influences how much weight is given to past performance versus the current adaptive signal.

Volatility-Based Reinforcement: Higher market volatility increases the impact of this memory feedback, making the model more reactive in volatile conditions.

Multi-Factor Dynamic Thresholds:

Dynamic Overbought/Oversold: Instead of fixed RSI levels (70/30), the thresholds adjust dynamically based on the Z-Score, making the system more sensitive to extreme market conditions.

Combined Multi-Factor Signal:

The final output signal is the result of combining the true RSI, adaptive RSI, and the probabilistic signal generated from the Monte Carlo simulations. This creates a robust, multi-factor signal that incorporates various market conditions and machine learning techniques.

Visual Representation:

The final combined signal is plotted in blue on the chart, along with reference lines at 55 (overbought), 10 (oversold), and 35 (neutral).

Alerts are set up to trigger when the combined signal crosses above the dynamic overbought level or below the dynamic oversold level.

Conclusion:

This "Ultimate Machine Learning RSI" script leverages multiple machine learning techniques—probabilistic modeling, adaptive learning, recursive feedback, and dynamic thresholds—to create an advanced, highly responsive RSI indicator. The result is an RSI that continuously learns from market conditions, adjusts itself in real-time, and provides a more nuanced and robust signal compared to traditional fixed-length RSI. This indicator pushes the boundaries of what's possible with Pine Script and introduces cutting-edge techniques for technical analysis.

Ultimate Multi-Physics Financial IndicatorThe Ultimate Multi-Physics Financial Indicator is an advanced Pine Script designed to combine various complex theories from physics, mathematics, and statistical mechanics to create a holistic, multi-dimensional approach to market analysis. Let’s break down the core concepts and how they’re applied in this script:

1. Fractal Geometry: Recursive Pattern Recognition

Purpose: This part of the script uses fractal geometry to recursively analyze price pivots (highs and lows) for detecting patterns.

Fractals: The fractalHigh and fractalLow signals represent key turning points in the market. The script goes deeper by recursively analyzing layers of pivot sequences, adding "depth" to the recognition of patterns.

Recursive Depth: It breaks down each detected pivot into smaller components, giving more nuance to market pattern recognition. This provides a broader context for how prices have behaved historically at various levels of recursion.

2. Quantum Mechanics: Adaptive Probabilistic Monte Carlo with Correlation

Purpose: This component integrates randomness (from Monte Carlo simulations) with current market behavior using correlation.

Randomness Weighted by Correlation: By generating random probabilities and weighting them based on how well the market aligns with recent trends, it creates a probabilistic signal. The random values are scaled by a correlation factor (close prices and their moving average), adding adaptive elements where randomness is adjusted by current market conditions.

3. Thermodynamics: Adaptive Efficiency Ratio (Entropy-Like Decay)

Purpose: This section uses principles from thermodynamics, where efficiency in price movement is dynamically adjusted by recent volatility and changes.

Efficiency Ratio: It calculates how efficiently the market is moving over a certain period. The "entropy decay factor" reflects how stable the market is. Higher entropy (chaos) results in lower efficiency, while stable periods maintain higher efficiency.

4. Chaos Theory: Lorenz-Driven Market Oscillation

Purpose: Instead of using a basic Average True Range (ATR) indicator, this section applies chaos theory (using a Lorenz attractor analogy) to describe complex market oscillations.

Lorenz Attractor: This models market behavior with a chaotic system that depends on the historical price changes at different time intervals. The attractor value quantifies the level of "chaos" or unpredictability in the market.

5. String Theory: Multi-Layered Dimensional Analysis of RSI and MACD

Purpose: Combines traditional indicators like the RSI (Relative Strength Index) and MACD (Moving Average Convergence Divergence) with momentum for multi-dimensional analysis.

Interaction of Layers: Each layer (RSI, MACD, and momentum) is treated as part of a multi-dimensional structure, where they influence one another. The final signal is a blended outcome of these key metrics, weighted and averaged for complexity.

6. Fluid Dynamics: Adaptive OBV (Pressure-Based)

Purpose: This section uses fluid dynamics to understand how price movement and volume create pressure over time, similar to how fluids behave under different forces.

Adaptive OBV: Traditional OBV (On-Balance Volume) is adapted by using statistical smoothing to measure the "pressure" exerted by volume over time. The result is a signal that shows where there might be building momentum or pressure in the market based on volume dynamics.

7. Recursive Synthesis of Signals

Purpose: After calculating all the individual signals (fractal, quantum, thermodynamic, chaos, string, and fluid), the script synthesizes them into one cohesive signal.

Recursive Feedback Loop: Each signal is recursively influenced by others, forming a feedback loop that allows the indicator to continuously learn from new data and self-adjust.

8. Signal Smoothing and Final Output

Purpose: To avoid noise in the output, the final combined signal is smoothed using an Exponential Moving Average (EMA), which helps stabilize the output for easier interpretation.

9. Dynamic Color Coding Based on Signal Extremes

Purpose: Visual clarity is enhanced by using color to highlight different levels of signal strength.

Color Coding: The script dynamically adjusts colors (green, orange, red) based on the strength of the final signal relative to its percentile ranking in historical data, making it easier to spot bullish, neutral, or bearish signals.

The "Ultimate Multi-Physics Financial Indicator" integrates a diverse array of scientific principles — fractal geometry, quantum mechanics, thermodynamics, chaos theory, string theory, and fluid dynamics — to provide a comprehensive market analysis tool. By combining probabilistic simulations, multi-dimensional technical indicators, and recursive feedback loops, this indicator adapts dynamically to evolving market conditions, giving traders a holistic view of market behavior across various dimensions. The result is an adaptive and flexible tool that responds to both short-term and long-term market changes

INDIA/NIFTY DOWN DAY MARKERINDIA/NIFTY DOWN DAY MARKER is indicator designed for Indian investors that provides visual cues on whole universe of stock charts marking volatile days based on the performance of selected Indian market indices. This indicator helps traders and investors assess the relative strength of individual stocks during extreme market movements

Key Features:

1) Index Selection: Users can choose from four major Indian indices: Nifty 50, Nifty Midcap 100, Nifty Smallcap 100, and Nifty MIDSMALLCAP 400. This flexibility allows for tailored analysis based on market focus.

2) Customizable Thresholds: Users can set their desired percentage thresholds for both rise and fall days, with default values of 2%. This customization enables users to adapt the indicator to their trading strategies.

3) Visual Indicators:

Rise Days: When the selected index rises by the specified percentage, the chart background turns green, indicating a bullish trend.

Fall Days: Conversely, if the index falls by the defined percentage, the background changes to red, signaling a bearish trend.

Advanced Physics Financial Indicator Each component represents a scientific theory and is applied to the price data in a way that reflects key principles from that theory.

Detailed Explanation

1. Fractal Geometry - High/Low Signal

Concept: Fractal geometry studies self-similar patterns that repeat at different scales. In markets, fractals can be used to detect recurring patterns or turning points.

Implementation: The script detects pivot highs and lows using ta.pivothigh and ta.pivotlow, representing local turning points in price. The fractalSignal is set to 1 for a pivot high, -1 for a pivot low, and 0 if there is no signal. This logic reflects the cyclical, self-similar nature of price movements.

Practical Use: This signal is useful for identifying local tops and bottoms, allowing traders to spot potential reversals or consolidation points where fractal patterns emerge.

2. Quantum Mechanics - Probabilistic Monte Carlo Simulation

Concept: Quantum mechanics introduces uncertainty and probability into systems, much like how future price movements are inherently uncertain. Monte Carlo simulations are used to model a range of possible outcomes based on random inputs.

Implementation: In this script, we simulate 100 random outcomes by generating a random number between -1 and 1 for each iteration. These random values are stored in an array, and the average of these values is calculated to represent the Quantum Signal.

Practical Use: This probabilistic signal provides a sense of randomness and uncertainty in the market, reflecting the possibility of price movement in either direction. It simulates the market’s chaotic nature by considering multiple possible outcomes and their average.

3. Thermodynamics - Efficiency Ratio Signal

Concept: Thermodynamics deals with energy efficiency and entropy in systems. The efficiency ratio in financial terms can be used to measure how efficiently the price is moving relative to volatility.

Implementation: The Efficiency Ratio is calculated as the absolute price change over n periods divided by the sum of absolute changes for each period within n. This ratio shows how much of the price movement is directional versus random, mimicking the concept of efficiency in thermodynamic systems.

Practical Use: A high efficiency ratio suggests that the market is trending smoothly (high efficiency), while a low ratio indicates choppy, non-directional movement (low efficiency, or high entropy).

4. Chaos Theory - ATR Signal

Concept: Chaos theory studies how complex systems are highly sensitive to initial conditions, leading to unpredictable behavior. In markets, chaotic price movements can often be captured through volatility indicators.

Implementation: The script uses a very long ATR period (1000) to reflect slow-moving chaos over time. The Chaos Signal is computed by measuring the deviation of the current price from its long-term average (SMA), normalized by ATR. This captures price deviations over time, hinting at chaotic market behavior.

Practical Use: The signal measures how far the price deviates from its long-term average, which can signal the degree of chaos or extreme behavior in the market. High deviations indicate chaotic or volatile conditions, while low deviations suggest stability.

5. Network Theory - Correlation with BTC

Concept: Network theory studies how different components within a system are interconnected. In markets, assets are often correlated, meaning that price movements in one asset can influence or be influenced by another.

Implementation: This indicator calculates the correlation between the asset’s price and the price of Bitcoin (BTC) over 30 periods. The Network Signal shows how connected the asset is to BTC, reflecting broader market dynamics.

Practical Use: In a highly correlated market, BTC can act as a leading indicator for other assets. A strong correlation with BTC might suggest that the asset is likely to move in line with Bitcoin, while a weak or negative correlation might indicate that the asset is moving independently.

6. String Theory - RSI & MACD Interaction

Concept: String theory attempts to unify the fundamental forces of nature into a single framework. In trading, we can view the RSI and MACD as interacting forces that provide insights into momentum and trend.

Implementation: The script calculates the RSI and MACD and combines them into a single signal. The formula for String Signal is (RSI - 50) / 100 + (MACD Line - Signal Line) / 100, normalizing both indicators to a scale where their contributions are additive. The RSI represents momentum, and MACD shows trend direction and strength.

Practical Use: This signal helps in detecting moments where momentum (RSI) and trend strength (MACD) align, giving a clearer picture of the asset's direction and overbought/oversold conditions. It unifies these two indicators to create a more holistic view of market behavior.

7. Fluid Dynamics - On-Balance Volume (OBV) Signal

Concept: Fluid dynamics studies how fluids move and flow. In markets, volume can be seen as a "flow" that drives price movement, much like how fluid dynamics describe the flow of liquids.

Implementation: The script uses the OBV (On-Balance Volume) indicator to track the cumulative flow of volume based on price changes. The signal is further normalized by its moving average to smooth out fluctuations and make it more reflective of price pressure over time.

Practical Use: The Fluid Signal shows how the flow of volume is driving price action. If the OBV rises significantly, it suggests that there is strong buying pressure, while a falling OBV indicates selling pressure. It’s analogous to how pressure builds in a fluid system.

8. Final Signal - Combining All Physics-Based Indicators

Implementation: Each of the seven physics-inspired signals is combined into a single Final Signal by averaging their values. This approach blends different market insights from various scientific domains, creating a comprehensive view of the market’s condition.

Practical Use: The final signal gives you a holistic, multi-dimensional view of the market by merging different perspectives (fractal behavior, quantum probability, efficiency, chaos, correlation, momentum/trend, and volume flow). This approach helps traders understand the market's dynamics from multiple angles, offering deeper insights than any single indicator.

9. Color Coding Based on Signal Extremes

Concept: The color of the final signal plot dynamically reflects whether the market is in an extreme state.

Implementation: The signal color is determined using percentiles. If the Final Signal is in the top 55th percentile of its range, the signal is green (bullish). If it is between the 45th and 55th percentiles, it is orange (neutral). If it falls below the 45th percentile, it is red (bearish).

Practical Use: This visual representation helps traders quickly identify the strength of the signal. Bullish conditions (green), neutral conditions (orange), and bearish conditions (red) are clearly distinguished, simplifying decision-making.

Night Low Liquidity Congestions with 4 Trading SessionsThis indicator is designed to help traders visualize and analyze key market periods of low liquidity during the night and identify high-activity zones in the morning. It also includes customizable time sessions for major global markets, including the European and American sessions, as well as the London Close session.

T he main functionalities include:

- Night Low Liquidity Phase: This highlights periods with typically low market activity during the night (default: 20:01–5:59). It also displays the total range (in pips) during this phase, allowing traders to identify potential price consolidations.

- Morning Hot Zone: This focuses on high-activity periods in the early morning (default: 6:00–7:59), providing visual cues without altering bar colors.

- European Trading Session: Displays the European market’s open hours (default: 8:00–12:00), shaded in blue, to mark increased volatility typically seen during this period.

- American Trading Session: Marks the active hours of the U.S. market (default: 12:01–16:59), where market activity tends to peak.

- London Close Area: Highlights the closing hours of the London market (default: 17:00–20:00), allowing traders to track potential liquidity shifts.

Key Features:

1. Customizable Time Sessions:

- The indicator allows for full customization of the start and end times for each market session, making it adaptable to different instruments and trading style.

- Traders can choose their preferred color and opacity for each time zone to suit their charting preferences.

2. Night Low Liquidity Pip Range Calculation:

- Automatically calculates and displays the pip range for the Night Low Liquidity phase.

- The range is colored red if it exceeds the specified threshold and green if it remains below it.

3. Alarm System:

- Customizable alerts for H1, M15, and M5 timeframes.

- Traders can set alerts to trigger just before a bar closes during specific sessions (European, American, or London Close) and on selected days of the week (Monday–Friday).

- The alarm system allows for full customization of active hours and days, giving traders full control over their notifications.

4. Clear Visual Cues:

- The indicator uses transparent shading to differentiate market sessions, making it easy to spot different phases of the trading day.

- Each session is visually distinct and can be toggled on or off based on trader preferences.

Ideal For:

- Traders who focus on intraday strategies and want to understand how market sessions affect liquidity and volatility.

- Those looking to trade during specific time windows like the Night Low Liquidity or Morning Hot Zones.

- Traders who need to automate their alerts based on specific market hours and close events for major timeframes.