Monthly Drawdowns and Moves UP This script allows users to analyze the performance of a specific month across multiple years, focusing on maximum drawdowns and maximum upward moves within the selected month. The script offers the following features:

Dynamic Month Selection : Choose any month to analyze using an intuitive dropdown menu.

Maximum Drawdown and Upward Move Calculations :

Calculate the largest percentage drop (drawdown) and rise (move up) for the selected month each year.

Visual Highlights :

The selected month is visually highlighted on the chart with a semi-transparent overlay.

Dynamic Labels:

Labels display the maximum drawdown and upward move directly on the chart for better visualization.

Comprehensive Table Summary:

A table provides a year-by-year summary of the maximum drawdowns and upward moves for the selected month, making it easy to spot trends over time.

Customizable Display Options:

Toggle the visibility of drawdown labels, move-up labels, and the summary table for a clutter-free experience.

This tool is perfect for traders and analysts looking to identify seasonal patterns, assess risk and opportunity, and gain deeper insights into monthly performance metrics across years. Customize, explore, and make informed decisions with this powerful Pine Script indicator.

Циклический анализ

Master Bitcoin & Litecoin Stock To Flow (S2F) ModelMaster Bitcoin & Litecoin Stock-to-Flow (S2F) Model

This indicator visualizes the Stock-to-Flow (S2F) models for Bitcoin (BTC) and Litecoin (LTC) based on Plan B's methodology. It calculates S2F and projects price models for both assets, incorporating daily changes in circulating supply. The script is designed exclusively for daily timeframes.

Features:

LTC & BTC S2F Models:

Calculates Stock-to-Flow values for both assets using daily new supply and circulating supply data.

Models S2F values with a customizable multiplier for precise adjustments.

500-Day Moving Average Models:

Smoothens the S2F model by applying a 500-day (18-month) moving average, providing a long-term trend perspective.

Customizable Inputs:

Adjust LTC and BTC multipliers to fine-tune the models.

Alert for Timeframe:

Alerts users to switch to the daily timeframe if another period is selected.

Plots:

LTC S2F Model: Blue line representing Litecoin’s calculated S2F-based price model.

BTC S2F Model: Orange line representing Bitcoin’s calculated S2F-based price model.

500-Day Avg Models: Smoothened S2F models for both LTC and BTC.

Notes:

Requires daily timeframe (1D) for accurate calculations.

Supply data is sourced from GLASSNODE:LTC_SUPPLY and GLASSNODE:BTC_SUPPLY.

Disclaimer:

This model is derived from Plan B's S2F methodology and is intended for educational and entertainment purposes only. It does not reflect official predictions or financial advice. Always conduct your own research before making investment decisions.

Smart Money Breakouts [iskess 01-02 11:05]This is an big update to the excellent Smart Money Breakout Script published in Oct 2023 by ChartPrime who, to my knowledge, was the original author.

FULL CREDIT GOES TO CHARTPRIME FOR THIS ORIGINAL WORK.

Per the moderator's rules, you will find below a meaningful, detailed self-contained description that does not rely on delegation to the open source code or links to other content. You will find in the description details on what the script does, how it does that, how to use it, and how it is original.

The "Smart Money Breakouts" indicator is designed to identify breakouts based on changes in character (CHOCH) or breaks of structure (BOS) patterns, facilitating automated trading with user-defined Take Profit (TP) level.

The indicator incorporates essential elements such as volume analysis and a data table to assist traders in optimizing their strategies.

🔸Breakout Detection:

The indicator scans price movements for "Change in Character" (CHOCH) and "Break of Structure" (BOS) patterns, signaling potential breakout opportunities in the market.

🔸User-Defined TP/SL :

Traders can customize the Take Profit (TP) and Stop Loss (SL) through the indicator settings, with these levels dynamically calculated based on the Average True Range (ATR). This allows for precise risk management and profit targets that adapt to market volatility. Traders can also select the lookback period for the TP/SL calculations.

🔸Volume Analysis and Trade Direction Specific Analysis:

The indicator includes a volume checker that provides valuable insights into the strength of the breakout, taking into account trade direction.

🔸If the volume label is red and the trade is long, it suggests a higher likelihood of hitting the Stop Loss (SL).

🔸If the volume label is green and the trade is long, it indicates a higher probability of hitting the Take Profit (TP).

🔸For short trades, a red volume label suggests a higher likelihood of hitting TP, while a green label suggests a higher likelihood of hitting SL.

🔸A yellow volume label suggests that the volume is inconclusive, neither favoring bullish nor bearish movements.

🔸Data Table:

The indicator features a data table that keeps track of the number of winning and losing trades for specific timeframes or configurations. It also shows the percentage of profits vs losses, and the overall profit/loss for the selected lookback period.

This table serves as a valuable tool for traders to analyze performance and discover optimal settings and timeframes.

The "Smart Money Breakouts" indicator provides traders with a comprehensive solution for breakout trading, combining technical analysis of changes in character and breaks of structure, volume insights, and performance tracking while dynamically adjusting TP and SL levels based on market volatility through the ATR.

This version of the script is a "significant improvement" from Chart Prime's original work in the following ways:

- A selectable range of candles for the profit/loss calculations to look back on.

- An updated table that includes the percentage of wins/losses, and and overall P&L during the selected lookback range.

- The user can now select only Long trades, Short trades, or both.

- The percentage gain/loss is now indicated for every trade on the chart.

- The user can now select a different multiplier for Stop Loss or Take Profit thresholds.

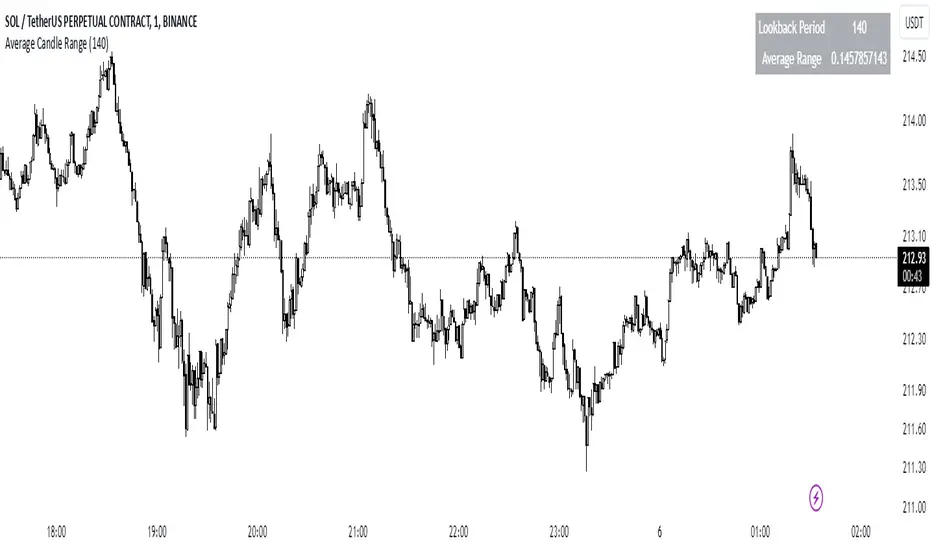

Average Candle RangeThis indicator calculates and displays the average trading range of candles over a specified period, helping traders identify volatility patterns and potential trading opportunities.

Features:

- Customizable lookback period (1-500 bars)

- Clean visual display in a top-right table overlay

- High-precision calculation showing 10 decimal places

- Real-time updates with each new bar

How it Works:

The indicator calculates the range of each candle (High - Low) and then computes the Simple Moving Average (SMA) of these ranges over your specified lookback period. The result is displayed in an easy-to-read table overlay.

Use Cases:

- Volatility Analysis: Monitor market volatility trends

- Position Sizing: Help determine position sizes based on average price movements

- Trading Strategy Development: Use as a reference for setting stop losses and take profits

- Market Phase Identification: Help identify high vs low volatility market phases

Settings:

- Lookback Period: Default is 140 bars, adjustable from 1 to 500

Note:

The indicator displays values with 10 decimal places for high-precision analysis, particularly useful in markets with small price movements.

Landry Light Pine ScannerLandry Light Pine Scanner

The Landry Light Pine Scanner is a comprehensive technical analysis tool designed to identify stocks showing strong upward trends based on the Landry Light methodology. It scans for stocks where:

Today's low and yesterday's low are above the 30 EMA.

The low from two days ago is below the 30 EMA.

SMA 50 is above SMA 150, and SMA 150 is above SMA 200 (a strong bullish SMA hierarchy).

Features:

Trend Detection: Automatically highlights stocks with strong bullish trends based on EMA and SMA alignment.

Customizable Inputs: Users can adjust EMA and SMA lengths to fit their trading style.

Visual Clarity: Plots the 30 EMA, SMA 50, SMA 150, and SMA 200 directly on the chart for easy analysis.

Alert Ready: Integrated with TradingView's alert system to notify users when the conditions are met.

Chart Highlights: Automatically highlights bars that meet the conditions with a subtle green background.

Use Case:

This indicator is ideal for swing traders and position traders looking for potential breakout opportunities. By filtering stocks with a bullish structure, traders can focus on high-probability setups.

Conditions Used:

30 EMA Conditions:

Today's low is above the 30 EMA.

Yesterday's low is above the 30 EMA.

The low from two days ago is below the 30 EMA.

SMA Hierarchy:

SMA 50 is above SMA 150.

SMA 150 is above SMA 200.

Customization Options:

30 EMA Length: Adjustable to match user preferences.

SMA Lengths: SMA 50, SMA 150, and SMA 200 lengths are customizable for flexibility.

Alerts:

Users can set alerts for when the defined conditions are met, making it easy to monitor multiple stocks.

How to Use:

Apply the Indicator:

Add the indicator to your TradingView chart.

Set Alerts:

Use the built-in alert condition for automated notifications.

Analyze Trends:

Look for green-highlighted bars indicating stocks meeting the criteria.

Screen Stocks:

Use this tool as part of your screener to filter stocks efficiently.

Note:

This indicator does not provide buy or sell signals. Always combine it with other technical and fundamental analysis for informed trading decisions.

Publishing Tags:

Landry Light, EMA, SMA, Trend Analysis, Swing Trading, Position Trading, Technical Analysis, Breakout Scanner, TradingView, Pine Script

Session Averages: Open, High, LowThis indicator allows for the user to specify an intraday time based range and calculate the average open price, average high price, and average low price for that session. The indicator plots the 5 most recent sessions on the chart, which allows for the user to identify fair value, Power of 3 movements, trends, and consolidations.

If bullish the user can identify when price is below the average open or low price of a range, and if bearish can identify when price is above the open or high of a range.

Economic RegimeThis indicator, "Economic Regime" , provides a comprehensive analysis of market conditions by combining multiple asset classes and financial metrics. It uses normalized scores and trend analysis to classify the current economic regime into one of four categories: Goldilocks, Reflation, Inflation, or Deflation. The classification is based on inputs like S&P 500 performance, bond yields, commodity prices, volatility indices, and sector ETFs. Additionally, it plots key financial spreads, including the yield spread (10Y-2Y) and credit spread (HYG-LQD), to offer deeper insights into liquidity and market sentiment. The background color dynamically reflects the identified economic regime, facilitating quick visual interpretation.

EMA SHIFT & PARALLEL [n_dot]BINANCE:ETHUSDT.P

This strategy was developed for CRYPTO FUTURES, (the settings for ETHUSDT.P) . I aimed for the strategy to function in a live environment, so I focused on making its operation realistic:

When determining the position, only 80% (adjustable) of the available cash is invested to reduce the risk of position liquidation.

I account for a 0.05% commission, typical on the futures market, for each entry and exit.

Concept:

I modified a simple, well-known method: the crossover of two exponential moving averages (FAST, SLOW) generates the entry and exit signals.

I enhanced the base idea as follows:

For the fast EMA, I incorporated a multiplier (offset) to filter out market noise and focus only on strong signals.

I use different EMAs for long and short entry points; both have their own FAST and SLOW EMAs and their own offset. For longs, the FAST EMA is adjusted downward (<1), while for shorts, it is adjusted upward (>1). Consequently, the signal is generated when the modified FAST EMA crosses the SLOW EMA.

Risk Management:

The position includes the following components:

Separate stop-losses for long and short positions.

Separate trailers for long and short positions.

The strategy operates so that the entry point is determined by the EMA crossover, while the exit is governed only by the Stop Loss or Trailer. Optionally, it can be set to close the position at the EMA recrossing ("Close at Signal").

Trailer Operation:

An entry percentage and offset are defined. The trailer activates when the price surpasses the entry price, calculated automatically by the system.

The trailer closes the position when the price drops by the offset percentage from the highest reached price.

Example for trailer:

Purchase Price = 100

Trailer Enter = 5% → Activation Price = 105 (triggers trailer if market price crosses it).

Trailer Offset = 2%

If the price rises to 110, the exit price becomes 107.8.

If the price goes to 120, the exit price becomes 117.6.

If the price falls below 117.6, the trailer closes the position.

Settings:

Source: Determines the market price reference.

End Close: Closes positions at the end of the simulation to avoid "shadow positions" and provide an objective result.

Lot proportional to free cash (%): Only a portion of free cash is invested to meet margin requirements.

Plot Short, Plot Long: Simplifies displayed information by toggling indicator lines on/off.

Long Position (toggleable):

EMA Fast ws: Window size for FAST EMA.

EMA Slow ws: Window size for SLOW EMA.

EMA Fast down shift: Adjustment factor for FAST EMA.

Stop Loss long (%): Percent drop to close the position.

Trailer enter (%): Percent above the purchase price to activate the trailer.

Trailer offset (%): Percent drop to close the position.

Short Position (toggleable):

EMA Fast ws: Window size for FAST EMA.

EMA Slow ws: Window size for SLOW EMA.

EMA Fast up shift: Adjustment factor for FAST EMA.

Stop Loss short (%): Percent rise to close the position.

Trailer enter (%): Percent below the purchase price to activate the trailer.

Trailer offset (%): Percent rise to close the position.

Operational Framework:

If in a long position and a short EMA crossover occurs, the strategy closes the long and opens a short (flip).

If in a short position and a long EMA crossover occurs, the strategy closes the short and opens a long (flip).

A position can close in three ways:

Stop Loss

Trailer

Signal Recrossing

If none are active, the position remains open until the end of the simulation.

Observations:

Shifts significantly deviating from 1 increase overfitting risk. Recommended ranges: 0.96–0.99 (long) and 1.01–1.05 (short).

The strategy's advantage lies in risk management, crucial in leveraged futures markets. It operates with relatively low DrawDown.

Recommendations:

Bullish Market: Higher entry threshold (e.g., 6%) and larger offset (e.g., 3%).

Volatile/Sideways Market: Tighter parameters (e.g., 3%, 1%).

The method is stable, and minor parameter adjustments do not significantly impact results, helping assess overfitting: if small changes lead to drastic differences, the strategy is over-optimized.

EMA Settings: Adjust FAST and SLOW EMAs based on the asset's volatility and cyclicality.

On the crypto market, especially in the Futures market, short time periods (1–15 minutes) often show significant noise, making patterns/repetitions hard to identify. I recommend setting the interval to at least 1 hour.

I hope this contributes to your success!

Regime Classifier Oscillator (AiBitcoinTrend)The Regime Classifier Oscillator (AiBitcoinTrend) is an advanced tool for understanding market structure and detecting dynamic price regimes. By combining filtered price trends, clustering algorithms, and an adaptive oscillator, it provides traders with detailed insights into market phases, including accumulation, distribution, advancement, and decline.

This innovative tool simplifies market regime classification, enabling traders to align their strategies with evolving market conditions effectively.

👽 What is a Regime Classifier, and Why is it Useful?

A Regime Classifier is a concept in financial analysis that identifies distinct market conditions or "regimes" based on price behavior and volatility. These regimes often correspond to specific phases of the market, such as trends, consolidations, or periods of high or low volatility. By classifying these regimes, traders and analysts can better understand the underlying market dynamics, allowing them to adapt their strategies to suit prevailing conditions.

👽 Common Uses in Finance

Risk Management: Identifying high-volatility regimes helps traders adjust position sizes or hedge risks.

Strategy Optimization: Traders tailor their approaches—trend-following strategies in trending regimes, mean-reversion strategies in consolidations.

Forecasting: Understanding the current regime aids in predicting potential transitions, such as a shift from accumulation to an upward breakout.

Portfolio Allocation: Investors allocate assets differently based on market regimes, such as increasing cash positions in high-volatility environments.

👽 Why It’s Important

Markets behave differently under varying conditions. A regime classifier provides a structured way to analyze these changes, offering a systematic approach to decision-making. This improves both accuracy and confidence in navigating diverse market scenarios.

👽 How We Implemented the Regime Classifier in This Indicator

The Regime Classifier Oscillator takes the foundational concept of market regime classification and enhances it with advanced computational techniques, making it highly adaptive.

👾 Median Filtering: We smooth price data using a custom median filter to identify significant trends while eliminating noise. This establishes a baseline for price movement analysis.

👾 Clustering Model: Using clustering techniques, the indicator classifies volatility and price trends into distinct regimes:

Advance: Strong upward trends with low volatility.

Decline: Downward trends marked by high volatility.

Accumulation: Consolidation phases with subdued volatility.

Distribution: Topping or bottoming patterns with elevated volatility.

This classification leverages historical price data to refine cluster boundaries dynamically, ensuring adaptive and accurate detection of market states.

Volatility Classification: Price volatility is analyzed through rolling windows, separating data into high and low volatility clusters using distance-based assignments.

Price Trends: The interaction of price levels with the filtered trendline and volatility clusters determines whether the market is advancing, declining, accumulating, or distributing.

👽 Dynamic Cycle Oscillator (DCO):

Captures cyclic behavior and overlays it with smoothed oscillations, providing real-time feedback on price momentum and potential reversals.

Regime Visualization:

Regimes are displayed with intuitive labels and background colors, offering clear, actionable insights directly on the chart.

👽 Why This Implementation Stands Out

Dynamic and Adaptive: The clustering and refit mechanisms adapt to changing market conditions, ensuring relevance across different asset classes and timeframes.

Comprehensive Insights: By combining price trends, volatility, and cyclic behaviors, the indicator provides a holistic view of the market.

This implementation bridges the gap between theoretical regime classification and practical trading needs, making it a powerful tool for both novice and experienced traders.

👽 Applications

👾 Regime-Based Trading Strategies

Traders can use the regime classifications to adapt their strategies effectively:

Advance & Accumulation: Favorable for entering or holding long positions.

Decline & Distribution: Opportunities for short positions or risk management.

👾 Oscillator Insights for Trend Analysis

Overbought/oversold conditions: Early warning of potential reversals.

Dynamic trends: Highlights the strength of price momentum.

👽 Indicator Settings

👾 Filter and Classification Settings

Filter Window Size: Controls trend detection sensitivity.

ATR Lookback: Adjusts the threshold for regime classification.

Clustering Window & Refit Interval: Fine-tunes regime accuracy.

👾 Oscillator Settings

Dynamic Cycle Oscillator Lookback: Defines the sensitivity of cycle detection.

Smoothing Factor: Balances responsiveness and stability.

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Binary Options Pro Helper By Himanshu AgnihotryThe Binary Options Pro Helper is a custom indicator designed specifically for one-minute binary options trading. This tool combines technical analysis methods like moving averages, RSI, Bollinger Bands, and pattern recognition to provide precise Buy and Sell signals. It also includes a time-based filter to ensure trades are executed only during optimal market conditions.

Features:

Moving Averages (EMA):

Uses short-term (7-period) and long-term (21-period) EMA crossovers for trend detection.

RSI-Based Signals:

Identifies overbought/oversold conditions for entry points.

Bollinger Bands:

Highlights market volatility and potential reversal zones.

Chart Pattern Recognition:

Detects double tops (sell signals) and double bottoms (buy signals).

Time-Based Filter:

Trades only within specified hours (e.g., 9:30 AM to 11:30 AM) to avoid unnecessary noise.

Visual Signals:

Plots buy and sell markers directly on the chart for ease of use.

How to Use:

Setup:

Add this script to your TradingView chart and select a 1-minute timeframe.

Signal Interpretation:

Buy Signal: Triggered when EMA crossover occurs, RSI is oversold (<30), and a double bottom pattern is detected.

Sell Signal: Triggered when EMA crossover occurs, RSI is overbought (>70), and a double top pattern is detected.

Timing:

Ensure trades are executed only during the specified time window for better accuracy.

Best Practices:

Use this indicator alongside fundamental analysis or market sentiment.

Test it thoroughly with historical data (backtesting) and in a demo account before live trading.

Adjust parameters (e.g., EMA periods, RSI thresholds) based on your trading style.

Fibonacci RepulseFibonacci Repulse with Trend Table 📉📈

Description: The "Fibonacci Repulse" indicator for TradingView combines Fibonacci retracement levels with dynamic support/resistance detection, providing real-time price action insights. 🔄 This powerful tool plots critical Fibonacci retracement levels (23.6%, 38.2%, and 50%) based on the highest and lowest swing points over a user-defined lookback period. The indicator automatically detects bullish retests, alerting you when the price touches and closes above any of the Fibonacci levels, indicating potential upward momentum. 🚀

Key Features:

Fibonacci Retracement Levels 📊: Plots key levels (23.6%, 38.2%, 50%) dynamically based on the highest and lowest price swings over a customizable lookback period.

Bullish Retests Alerts ⚡: Identifies and marks bullish retests when the price touches the Fibonacci levels and closes above them, signaling potential upward movement.

Real-Time Trend Detection 🔍: Displays the current market trend as "Bullish," "Bearish," or "Sideways" in a clear, easy-to-read table in the bottom right corner of the chart. This is determined based on the price's position relative to the Fibonacci levels.

Customizable Settings ⚙️: Adjust the lookback period and label offsets for optimal visual customization.

How It Works:

The indicator calculates the Fibonacci retracement levels between the highest high and the lowest low within a user-defined period. 🧮

It draws extended lines at the 23.6%, 38.2%, and 50% retracement levels, updating them as the chart moves. 📉

When the price touches a Fibonacci level and closes above it, a "Bullish Retest" label appears, signaling a potential buy opportunity. 💡

A real-time trend status table updates automatically in the chart's bottom-right corner, helping traders quickly assess the market's trend direction: Bullish, Bearish, or Sideways. 🔄

Why Use It: This indicator is perfect for traders looking for a clear and visual way to incorporate Fibonacci levels into their trading strategies, with real-time feedback on trend direction and price action signals. Whether you are a novice or an experienced trader, "Fibonacci Repulse" provides a powerful tool for identifying potential reversal points and confirming trends, enhancing your trading strategy. 📈💪

Logarithmic IndicatorThis logarithmic indicator does the following:

It calculates the logarithm of the chosen price (default is close price) using a user-defined base (default is 10).

It then calculates a Simple Moving Average (SMA) of the logarithmic values.

Both the logarithmic value and its SMA are plotted on the chart.

To improve visibility, it also plots an upper and lower band based on the highest and lowest values over the last 100 periods.

To use this indicator:

Open the TradingView Pine Editor.

Paste the code into the editor.

Click "Add to Chart" or "Save" to apply the indicator to your chart.

Adjust the input parameters in the indicator settings as needed.

You can customize this indicator further by:

Changing the color scheme

Adding more moving averages or other technical indicators

Implementing alerts based on crossovers or other conditions

Remember, logarithmic scales are often used in finance to visualize data that spans several orders of magnitude, making it easier to see percentage changes over time.

Volatility Cycle IndicatorThe Volatility Cycle Indicator is a non-directional trading tool designed to measure market volatility and cycles based on the relationship between standard deviation and Average True Range (ATR). In the Chart GBPAUD 1H time frame you can clearly see when volatility is low, market is ranging and when volatility is high market is expanding.

This innovative approach normalizes the standard deviation of closing prices by ATR, providing a dynamic perspective on volatility. By analyzing the interaction between Bollinger Bands and Keltner Channels, it also detects "squeeze" conditions, highlighting periods of reduced volatility, often preceding explosive price movements.

The indicator further features visual aids, including colored zones, plotted volatility cycles, and highlighted horizontal levels to interpret market conditions effectively. Alerts for key events, such as volatility crossing significant thresholds or entering a squeeze, make it an ideal tool for proactive trading.

Key Features:

Volatility Measurement:

Tracks the Volatility Cycle, normalized using standard deviation and ATR.

Helps identify periods of high and low volatility in the market.

Volatility Zones:

Colored zones represent varying levels of market volatility:

Blue Zone: Low volatility (0.5–0.75).

Orange Zone: Transition phase (0.75–1.0).

Green Zone: Moderate volatility (1.0–1.5).

Fuchsia Zone: High volatility (1.5–2.0).

Red Zone: Extreme volatility (>2.0).

Squeeze Detection:

Identifies when Bollinger Bands contract within Keltner Channels, signaling a volatility squeeze.

Alerts are triggered for potential breakout opportunities.

Visual Enhancements:

Dynamic coloring of the Volatility Cycle for clarity on its momentum and direction.

Plots multiple horizontal levels for actionable insights into market conditions.

Alerts:

Sends alerts when the Volatility Cycle crosses significant levels (e.g., 0.75) or when a squeeze condition is detected.

Non-Directional Nature:

The indicator does not predict the market's direction but rather highlights periods of potential movement, making it suitable for both trend-following and mean-reversion strategies.

How to Trade with This Indicator:

Volatility Squeeze Breakout:

When the indicator identifies a squeeze (volatility compression), prepare for a breakout in either direction.

Use additional directional indicators or chart patterns to determine the likely breakout direction.

Crossing Volatility Levels:

Pay attention to when the Volatility Cycle crosses the 0.75 level:

Crossing above 0.75 indicates increasing volatility—ideal for trend-following strategies.

Crossing below 0.75 signals decreasing volatility—consider mean-reversion strategies.

Volatility Zones:

Enter positions as volatility transitions through key zones:

Low volatility (Blue Zone): Watch for breakout setups.

Extreme volatility (Red Zone): Be cautious of overextended moves or reversals.

Alerts for Proactive Trading:

Configure alerts for squeeze conditions and level crossings to stay updated without constant monitoring.

Best Practices:

Pair the Volatility Cycle Indicator with directional indicators such as moving averages, trendlines, or momentum oscillators to improve trade accuracy.

Use on multiple timeframes to align entries with broader market trends.

Combine with risk management techniques, such as ATR-based stop losses, to handle volatility spikes effectively.

Market Cycles

The Market Cycles indicator transforms market price data into a stochastic wave, offering a unique perspective on market cycles. The wave is bounded between positive and negative values, providing clear visual cues for potential bullish and bearish trends. When the wave turns green, it signals a bullish cycle, while red indicates a bearish cycle.

Designed to show clarity and precision, this tool helps identify market momentum and cyclical behavior in an intuitive way. Ideal for fine-tuning entries or analyzing broader trends, this indicator aims to enhance the decision-making process with simplicity and elegance.

DR Oscillator 8 * Measures price deviation: Calculates the percentage difference between the closing price and a simple moving average.

* Defines upper and lower limits: User-defined upper and lower limits determine overbought and oversold conditions.

* Signal line: A simple moving average of the deviation is plotted as a signal line.

* Deviation smoothing (optional): The deviation can be smoothed using a moving average to create a smoother line.

* Additional signal line (optional): An additional signal line can be added for further analysis.

* Visual representation: The oscillator is plotted with different colors to indicate overbought, oversold, or neutral conditions.

* Background coloring: The background color changes based on the oscillator's value to provide visual cues for buy or sell signals.

In summary:

The DR Oscillator helps traders identify potential buying and selling opportunities by measuring the extent to which a security's price has deviated from its moving average. When the oscillator moves above the upper limit, it suggests that the asset may be overbought and due for a price correction. Conversely, when it moves below the lower limit, it may indicate an oversold condition and a potential buying opportunity.

However, it's important to note that the DR Oscillator is just one tool and should be used in conjunction with other technical indicators and fundamental analysis for more accurate trading decisions.

rsi wf breakoutRSI Breakout Asif

RSI Breakout Asif Indicator

Overview:

The RSI Breakout Asif indicator is a custom script designed to analyze and highlight potential

breakout points using the Relative Strength Index (RSI) combined with Williams Fractals. This

indicator is specifically developed for traders who want to identify key momentum shifts in the

market.

Features:

1. RSI Analysis:

- The RSI is calculated using a user-defined length and price source.

- Horizontal lines are plotted at levels 70 (overbought), 50 (neutral), and 30 (oversold) to visually

aid decision-making.

2. Williams Fractals on RSI:

- Detects fractal highs and lows based on RSI values.

- Highlights these fractal points with dynamic, symmetrical lines for better visibility.

3. Customization:

- Users can adjust the RSI length and price source for personalized analysis.

- Fractal settings (left and right bar length) are also adjustable, making the indicator versatile for

different trading styles.

4. Visual Enhancements:

- Fractal highs are marked in red, while fractal lows are marked in green.

Asif - Page 1

RSI Breakout Asif

- Precise line placement ensures clarity and reduces chart clutter.

5. Practical Utility:

- Use the fractal breakout signals in conjunction with other technical indicators for enhanced

decision-making.

Usage:

- Add the RSI Breakout Asif indicator to your TradingView chart.

- Adjust the settings according to your trading strategy.

- Observe the RSI values and fractal points to identify potential breakout zones.

Disclaimer:

This indicator is a technical analysis tool and should be used in combination with other analysis

methods. It does not guarantee profitable trades.

Watermarked by Asif.

Asif - Page 2

Swing & Day Trading Strategy dddddThis TradingView Pine Script is designed for swing and day trading, incorporating multiple technical indicators and tools to enhance decision-making. It calculates and plots exponential moving averages (EMAs) for 5, 9, 21, 50, and 200 periods to identify trends and crossovers. The Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) provide momentum and overbought/oversold signals. The script dynamically identifies and marks support and resistance levels based on recent highs and lows, while also detecting and labeling key candlestick patterns such as bullish and bearish engulfing, doji, and hammer candles. Bullish and bearish signals are highlighted on the chart with green and red backgrounds, respectively, and alerts are generated to notify traders of these conditions. All visualizations, including EMAs, support/resistance lines, and candlestick labels, are overlaid directly on the stock chart for easy interpretation. This comprehensive approach assists traders in spotting potential trading opportunities effectively.

Edufx AMD~Accumulation, Manipulation, DistributionEdufx AMD Indicator

This indicator visualizes the market cycles using distinct phases: Accumulation, Manipulation, Distribution, and Reversal. It is designed to assist traders in identifying potential entry points and understanding price behavior during these phases.

Key Features:

1. Phases and Logic:

-Accumulation Phase: Highlights the price range where market accumulation occurs.

-Manipulation Phase:

- If the price sweeps below the accumulation low, it signals a potential "Buy Zone."

- If the price sweeps above the accumulation high, it signals a potential "Sell Zone."

-Distribution Phase: Highlights where price is expected to expand and establish trends.

-Reversal Phase: Marks areas where the price may either continue or reverse.

2. Weekly and Daily Cycles:

- Toggle the visibility of Weekly Cycles and Daily Cycles independently through the settings.

- These cycles are predefined with precise timings for each phase, based on your selected on UTC-5 timezone.

3. Customizable Appearance:

- Adjust the colors for each phase directly in the settings to suit your preferences.

- The indicator uses semi-transparent boxes to represent the phases, allowing easy visualization without obstructing the chart.

4. Static Boxes:

- Boxes representing the phases are drawn only once for the visible chart range and do not dynamically delete, ensuring important consistent reference points.

RRS Separator 3This Pine Script indicator, titled "RRS Separator 3", is designed to draw vertical lines on a chart to separate different time frames. Here's a breakdown of its main features:

1.Time Frame Separators: The script draws vertical lines to mark the beginning of 5-minute, 15-minute, 1-hour, and 4-hour intervals on intraday charts.

2.Customizable Appearance: Users can customize the appearance of each time frame's separator lines, including:

Visibility (show/hide)

Color

Line style (solid, dashed, or dotted)

Line width

3.Dynamic Line Drawing: The script calculates the positions for future time frame separators and draws them in advance, extending beyond the current bar.

4.Compatibility: It's designed to work on various intraday time frames, adjusting its behavior based on the chart's current time frame.

5.Efficient Line Management: The script uses arrays to manage the drawn lines, clearing old lines and redrawing them on each update to ensure accuracy and prevent clutter.

6.Time Calculations: It performs various time-related calculations to determine the correct positioning of lines for each time frame.

7.Conditional Drawing: Lines are only drawn if they meet certain conditions (e.g., the chart's time frame is smaller than the separator's time frame).

8.Performance Considerations: The script includes max_bars_back and max_lines_count parameters to manage memory usage and performance.

SMA Trend Spectrum [InvestorUnknown]The SMA Trend Spectrum indicator is designed to visually represent market trends and momentum by using a series of Simple Moving Averages (SMAs) to create a color-coded spectrum or heatmap. This tool helps traders identify the strength and direction of market trends across various time frames within one chart.

Functionality:

SMA Calculation: The indicator calculates multiple SMAs starting from a user-defined base period (Starting Period) and increasing by a specified increment (Period Increment). This creates a sequence of moving averages that span from short-term to long-term perspectives.

Trend Analysis: Each segment of the spectrum compares three SMAs to determine the market's trend strength: Bullish (color-coded green) when the current price is above all three SMAs. Neutral (color-coded purple) when the price is above some but not all SMAs. Bearish (color-coded red) when the price is below all three SMAs.

f_col(x1, x2, x3) =>

min = ta.sma(src, x1)

mid = ta.sma(src, x2)

max = ta.sma(src, x3)

c = src > min and src > mid and src > max ? bull : src > min or src > mid or src > max ? ncol : bear

Heatmap Visualization: The indicator plots these trends as a vertical spectrum where each row represents a different set of SMAs, forming a heatmap-like display. The color of each segment in the heatmap directly correlates with market conditions, providing an intuitive view of market sentiment.

Signal Smoothing: Users can choose to smooth the trend signal using either a Simple Moving Average (SMA), Exponential Moving Average (EMA), or leave it as raw data (Signal Smoothing). The length of smoothing can be adjusted (Smoothing Length). The signal is displayed in a scaled way to automatically adjust for the best visual experience, ensuring that the trend is clear and easily interpretable across different chart scales and time frames

Additional Features:

Plot Signal: Optionally plots a line representing the average trend across all calculated SMAs. This line helps in identifying the overall market direction based on the spectrum data.

Bar Coloring: Bars on the chart can be colored according to the average trend strength, providing a quick visual cue of market conditions.

Usage:

Trend Identification: Use the heatmap to quickly assess if the market is trending strongly in one direction or if it's in a consolidation phase.

Entry/Exit Points: Look for shifts in color patterns to anticipate potential trend changes or confirmations for entry or exit points.

Momentum Analysis: The gradient from bearish to bullish across the spectrum can be used to gauge momentum and potentially forecast future price movements.

Notes:

The effectiveness of this indicator can vary based on market conditions, asset volatility, and the chosen SMA periods and increments.

It's advisable to combine this tool with other technical indicators or fundamental analysis for more robust trading decisions.

Disclaimer: Past performance does not guarantee future results. Always use this indicator as part of a broader trading strategy.

[w3ss1] Timeframe SyncThe "Timeframe Sync" indicator provides a comprehensive view of price action across multiple timeframes for a single symbol, allowing traders to analyze market conditions from a multi-timeframe perspective with ease.

Key Features:

Flexible Symbol Selection: Choose between analyzing the symbol of the current chart or select another symbol to monitor.

Customizable Timeframes: Control which timeframes you want to analyze through toggle switches. Choose from 11 different timeframes ranging from 1-minute to Monthly charts, with the ability to customize each one:

1m, 5m, 15m, 30m, 1H, 4H, 8H, 12H, 1D, 1W, 1M

Visual Feedback:

-Candle Close Color: Each timeframe's last closed candle is color-coded. Bullish closes are highlighted in green, bearish in dark shades, and inside candles in orange.

-Bias Indicator: The indicator shows whether the close is "above", "below", or "inside" the previous candle's high/low range, providing insight into the market's momentum.

Table Display: Information is presented in a clear table format:

-The first row shows the symbol being analyzed.

-The second row displays "Candle close" to indicate the relevance of the information below.

-Each subsequent row represents a different timeframe, showing its abbreviation and the bias of the last close.

Conditional Display: Timeframes are only shown if they are relevant to the current chart's timeframe. This ensures that you're not looking at outdated data when on lower timeframes.

Customization:

-Adjust text size, table position, background color, text color, and colors for different candle close scenarios.

Usage:

Ideal for traders who need a quick multi-timeframe analysis without switching charts.

Helps in confirming short-term moves with longer-term trends or spotting divergences across timeframes.

Instructions:

Add the indicator to your chart.

Customize the timeframes you wish to monitor via the toggle switches.

Optionally, select a different symbol if not analyzing the current chart's symbol.

Adjust colors and table settings to your preference.

Observe how price action behaves across different timeframes to make informed trading decisions.

Bitcoin Reversal PredictorOverview

This indicator displays two lines that, when they cross, signal a potential reversal in Bitcoin's price trend. Historically, the high or low of a bull market cycle often occurs near the moment these lines intersect. The lines consist of an Exponential Moving Average (EMA) and a logarithmic regression line fitted to all of Bitcoin's historical data.

Inspiration

The inspiration for this indicator came from the PI Cycle Top indicator, which has accurately predicted past bull market peaks. However, I believe the PI Cycle Top indicator may not be as effective in the future. In that indicator, two lines cross to mark the top, but the extent of the cross has been diminishing over time. This was especially noticeable in the 2021 cycle, where the lines barely crossed. Because of this, I created a new indicator that I think will continue to provide reliable reversal signals in the future.

How It Works

The logarithmic regression line is fitted to the Bitcoin (BTCUSD) chart using two key factors: the 'a' factor (slope) and the 'b' factor (intercept). This results in a steadily decreasing line. The EMA oscillates above and below this regression line. Each time the two lines cross, a vertical colored bar appears, indicating that Bitcoin's price momentum is likely to reverse.

Use Cases

- Price Bottoming:

Bitcoin often bottoms out when the EMA crosses below the logarithmic regression line.

- Price Topping:

In contrast, Bitcoin often peaks when the EMA crosses above the logarithmic regression line.

- Profitable Strategy:

Trading at the crossovers of these lines can be a profitable strategy, as these moments often signal significant price reversals.

Bitcoin Logarithmic Regression BandsOverview

This indicator displays logarithmic regression bands for Bitcoin. Logarithmic regression is a statistical method used to model data where growth slows down over time. I initially created these bands in 2019 using a spreadsheet, and later coded them in TradingView in 2021. Over time, the bands proved effective at capturing Bitcoin's bull market peaks and bear market lows. In 2024, I decided to share this indicator because I believe these logarithmic regression bands offer the best fit for the Bitcoin chart.

How It Works

The logarithmic regression lines are fitted to the Bitcoin (BTCUSD) chart using two key factors: the 'a' factor (slope) and the 'b' factor (intercept). The two lines in the upper and lower bands share the same 'a' factor, but I adjust the 'b' factor by 0.2 to more accurately capture the bull market peaks and bear market lows. The formula for logaritmic regression is 10^((a * ln) - b).

How to Use the Logarithmic Regression Bands

1. Lower Band (Support Band):

The two lines in the lower band create a potential support area for Bitcoin’s price. Historically, Bitcoin’s price has always found its lows within this band during past market cycles. When the price is within the lower band, it suggests that Bitcoin is undervalued and could be set for a rebound.

2. Upper Band (Resistance Band):

The two lines in the upper band create a potential resistance area for Bitcoin’s price. Bitcoin has consistently reached its highs in this band during previous market cycles. If the price is within the upper band, it indicates that Bitcoin is overvalued, and a potential price correction may be imminent.

Use Cases

- Price Bottoming:

Bitcoin tends to bottom out at the lower band before entering a prolonged bull market or a period of sideways movement.

- Price Topping:

In reverse, Bitcoin tends to top out at the upper band before entering a bear market phase.

- Profitable Strategy:

Buying at the lower band and selling at the upper band can be a profitable trading strategy, as these bands often indicate key price levels for Bitcoin’s market cycles.