Previous Day High and Low Count with Probabilities

Indicator Explanation

This indicator displays the number of days on which the previous day's high or low prices were not reached and calculates probabilities for future price movements based on this information. It stores the high and low values of the last 45 days and checks daily whether these levels were touched. Based on the number of days without touching either the high or the low, the indicator calculates the probability of future price movements in either direction (Up or Down).

The indicator offers customization options for label placement and color on the chart. The counts for the high and low touches, along with the calculated probabilities (in percentages), are displayed as labels on the chart. These labels can be shifted along the X-axis by up to 50 bars and can be customized in color and size. Additionally, the text for the labels can be freely chosen, giving the user improved flexibility and overview.

In summary, this indicator helps to:

- Track how often previous day's high and low levels were not reached.

- Estimate probabilities for future price movements based on this information.

- Customize the chart display for easier interpretation.

Strategy Concept

Probability and Touch Conditions:

A long position is entered only if:

The probability of reaching the high is at least 60%.

The price has not touched the previous day’s high in the last three days.

Similarly, for short positions:

The probability of reaching the low is at least 60%.

The price has not touched the previous day’s low in the last three days.

Incremental Position Size Increase:

On the 3rd consecutive day without a high/low touch and with the probability condition met, an initial position of 0.01 lots is opened.

On the 4th day, an additional position of 0.01 lots is added.

On the 5th day, an extra position of 0.02 lots is opened.

After a two-day pause, the situation is re-evaluated, and if conditions are still met, a 0.04-lot position is considered.

Trend Reversal Detection:

The strategy also includes a simple trend reversal check. If the market shows clear reversal signals, no new positions will be opened.

Adjustments and Risk Management

This strategy can be adjusted by modifying the probability values, the number of days without a high/low touch, and the lot sizes. Additionally, stop-loss and take-profit levels can be added to further control the risk and secure profits.

Strategy Concept

Probability and Touch Conditions:

A long position is entered only if:

The probability of reaching the high is at least 60%.

The price has not touched the previous day’s high in the last three days.

Similarly, for short positions:

The probability of reaching the low is at least 60%.

The price has not touched the previous day’s low in the last three days.

Incremental Position Size Increase:

On the 3rd consecutive day without a high/low touch and with the probability condition met, an initial position of 0.01 lots is opened.

On the 4th day, an additional position of 0.01 lots is added.

On the 5th day, an extra position of 0.02 lots is opened.

After a two-day pause, the situation is re-evaluated, and if conditions are still met, a 0.04-lot position is considered.

Trend Reversal Detection:

The strategy also includes a simple trend reversal check. If the market shows clear reversal signals, no new positions will be opened.

Risk Disclaimer

The author of this strategy does not assume any liability for potential losses or gains that may arise from the use of this strategy. Trading involves significant risk, and it is important to only trade with capital that you can afford to lose. The strategy presented is for educational purposes only and should not be considered as financial advice. Always conduct your own research and consider seeking advice from a professional financial advisor before making any trading decisions.

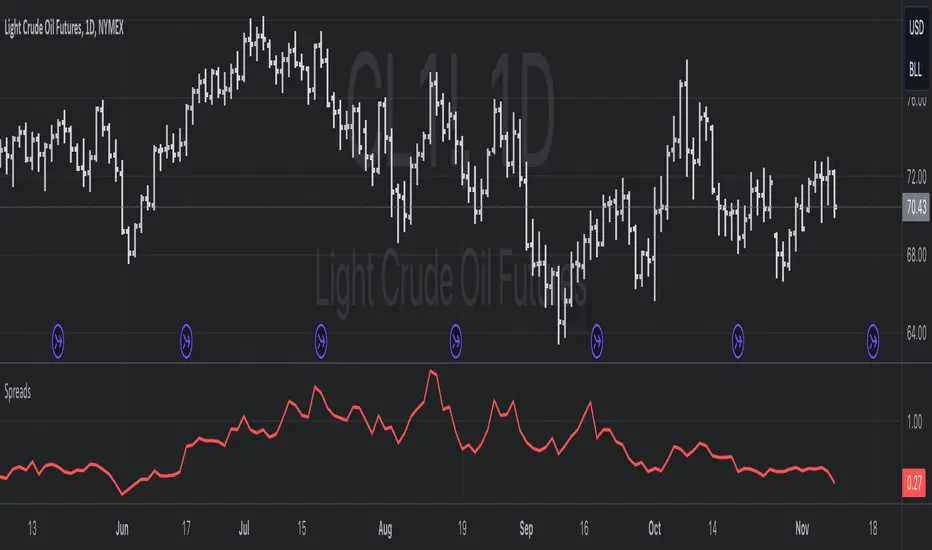

Циклический анализ

Spreads between contractsA simple indicator that automatically calculates and charts the difference between the nearby futures contract (1!) and the next contract (2!), enabling contango and backwardation analysis. If needed, any two contracts can also be manually entered.

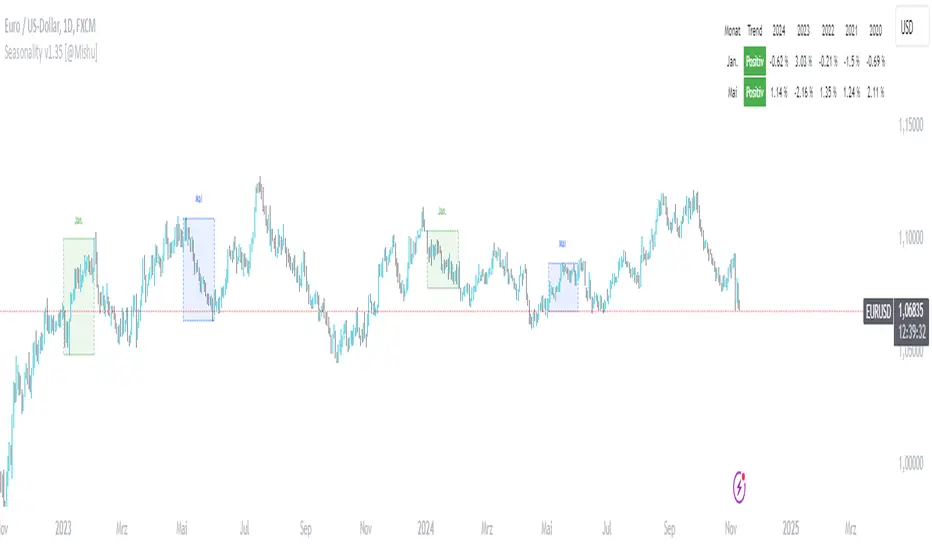

Seasonality v1.33.Seasonality v1.33 - Seasonal Indicator for Trading Trends

Seasonality v1.33 is a tailored indicator designed to analyze seasonal trends in historical price movements, assisting traders in making informed decisions. In its beta version, Seasonality v1.33 allows users to select up to two specific months and compare price changes for these months across several years, helping to identify potential seasonal patterns.

Indicator Features

Identifying Seasonal Trends: By choosing up to two months and a range of years, Seasonality v1.33 offers a visual representation of average price changes and highlights potential positive or negative trends. This supports traders in spotting recurring seasonal price movements that may be influenced by yearly cycles or market conditions.

Historical Comparison Across Multiple Years: The indicator displays the percentage price changes for the selected months over up to 10 years, allowing traders to observe consistency in price fluctuations across different years.

Visual Presentation: A color-coded table shows the dominant trend, either positive or negative, and highlights monthly trends for easy reference. The table size and position can be customized, allowing integration into each user’s preferred chart layout.

How to Use

Month and Year Selection: In the current beta version, traders can select two specific months and a range of years to check for potential seasonal effects.

Trend Summary: The table provides both individual yearly data and an overall trend signal for the selected months, giving a quick overview of prevailing tendencies.

Customizable Display: The table’s position and text size are adjustable to fit seamlessly into the user’s charting interface.

Limitations and Considerations

Data Dependency: The accuracy of analysis relies on the availability of historical price data, which may vary depending on the market or asset.

No Guarantee of Future Trends: While past trends provide insights, they do not guarantee future results. This indicator serves as a supportive tool but should be complemented by thorough analysis and sound risk management.

Feedback and Suggestions

The Seasonality v1.33 indicator is available in beta for free use and testing until the end of the month. Your feedback is highly valued! Comments and suggestions will help us improve future versions and tailor them to the needs of traders.

Bullrun Profit Maximizer [QuantraSystems]Bullrun Profit Maximizer

Quantra Systems guarantees that the information created and published within this document and on the Tradingview platform is fully compliant with applicable regulations, does not constitute investment advice, and is not exclusively intended for qualified investors.

Important Note!

The system equity curve presented here has been generated as part of the process of testing and verifying the methodology behind this script.

Crucially, it was developed after the system was conceptualized, designed, and created, which helps to mitigate the risk of overfitting to historical data. In other words, the system was built for robustness, not for simply optimizing past performance.

This ensures that the system is less likely to degrade in performance over time, compared to hyper optimized systems that are tailored to past data. No tweaks or optimizations were made to this system post backtest.

Even More Important Note!!

The nature of markets is that they change quickly and unpredictably. Past performance does not guarantee future results - this is a fundamental rule in trading and investing.

While this system is designed with broad, flexible conditions to adapt quickly to a range of market environments, it is essential to understand that no assumptions should be made about future returns based on historical data. Markets are inherently uncertain, and this system - like all trading systems - cannot predict future outcomes.

Introduction

The "Adaptive Pairwise Momentum System" is not a prototype to the Bullrun Profit Maximizer (BPM) . The Bullrun Profit Maximizer is a fully re-engineered, higher frequency momentum system.

The Bullrun Profit Maximizer (BPM) uses a completely different filter logic and refines momentum calculations, specifically to support higher frequency trading on Crypto's Blue Chip assets. It correctly calculates fees and slippage by compounding them against System Profit before plotting the equity curve.

Unlike prior systems, this script utilizes a completely new filter logic and refined momentum calculation, specifically built to support higher frequency trading on blue-chip assets, while minimizing the impact of fees and slippage.

While the APMS focuses on Macro Trend Alignment, the BPM instead applies an equity curve based filter, allowing for targeted precision on the current asset’s trend without relying on broader market conditions. This approach delivers more responsive and asset specific signals, enhancing agility in today’s fast paced crypto markets.

The BPM dynamically optimizes capital allocation across up to four high performing assets, ensuring that the portfolio adapts swiftly to changing market conditions. The system logic consists of sophisticated quantitative methods, rapid momentum analysis and alpha cyclicality/seasonality optimizations. The overarching goal is to ensure that the portfolio is always invested in the highest performing asset based on dynamic market conditions, while at the same time managing risk through rapid asset filters and internal mechanisms like alpha cyclicality, volatility and beta analysis.

In addition to these core functionalities, the BPM comes with the typical Quantra Systems UI design, structured to reduce data clutter and provide users with only the most essential, impactful information. The BPM UI format delivers clear and easy to read signals. It enables rapid decision making in a high frequency environment without compromising on depth or accuracy.

Bespoke Logic Filtering with Equity Curve Precision

The BPM script utilizes a completely new methodology and focuses on intraday rotations of blue-chip crypto assets, while previously built systems were designed with a longer term focus in mind.

In response to the need for more precise signal generation, the BPM replaces the previous macro trend filter with a new, highly specific equity curve activation filter. This unique logic filter is driven solely by the performance trends of the asset currently held by the system. By analyzing the equity curve directly, this system can make more targeted, timely allocations based on asset specific momentum, allowing for quick adjustments that are more relevant to the held asset rather than general market conditions.

The benefits of this new, unique approach are twofold: first, it avoids premature allocation shifts based on broader macro movements, and second, it enables the system to adapt dynamically to the performance of each asset individually. This asset specific filtering allows traders to capitalize on localized strength within individual blue-chip cryptoassets without being affected by lags in the overall market trend.

High Frequency Momentum Calculation for Enhanced Flexibility

The BPM incorporates a newly designed momentum calculation that increases its suitability across lower timeframes. This new momentum indicator captures and processes more data points within a shorter window than ever before, rather than extending bar intervals and potentially losing high frequency detail. This creates a smooth, data rich featureset that is especially suited for blue-chip assets, where liquidity reduces slippage and fees, making higher frequency trading viable.

By retaining more data, this system captures subtle shifts in momentum more effectively than traditional approaches, offering higher resolution insights. These modifications result in a system capable of generating highly responsive signals on faster timeframes, empowering traders to act quickly in volatile markets.

User Interface and Enhanced Readability

The BPM also features a reimagined, streamlined user interface, making it easier than ever to monitor essential signals at a glance. The new layout minimizes extraneous data points in the tables, leaving only the most actionable information for traders. This cleaner presentation is purpose built to help traders identify the strongest asset in real time, with clear, color coded signals to facilitate swift decision making in fast moving markets.

Equity Stats Table : Designed for clarity, the stats table focuses on the current allocation’s performance metrics, emphasizing the most critical metrics without unnecessary clutter.

Color Coded Highlights : The interface includes the option to highlight both the current top performing asset, and historical allocations - with indicators of momentum shifts and performance metrics readily accessible.

Clear Signals : Visual cues are presented in an enhanced way to improve readability, including simplified line coloring, and improve visualization of the outperforming assets in the allocation table.

Dynamic Asset Reallocation

The BPM dynamically allocates capital to the strongest performing asset in a selected pool. This system incorporates a re-engineered, pairwise momentum measurement designed to operate at higher frequencies. The system evaluates each asset against others in real time, ensuring only the highest momentum asset receives allocation. This approach keeps the portfolio positioned for maximum efficiency, with an updated weighting logic that favors assets showing both strength and sustainability.

Position Changes and Slippage Calculation

Position changes are optimized for faster reallocation, with realistic slippage and fee calculations factored into each trade. The system’s structure minimizes the impact of these costs on blue-chip assets, allowing for more active management on short timeframes without incurring significant drag on performance.

A Special Note on Fees + Slippage

In the image above, the system has been applied to four different timeframes - 12h, 8h, 4h and 1h - using identical settings and a selected slippage and fees amount of 0.2%. In this stress test, we isolate the choppy downwards period from the previous Bitcoin all time high - set in March 2024, to the current date where Bitcoin is currently sitting at around the same level.

This illustrates an important concept: starting at the 12h, the system performed better as the timeframes decreased. In fact, only on the 4hr chart did the system equity curve make a new all time high alongside Bitcoin. It is worth noting that market phases that are “non-trending” are generally the least profitable periods to use a momentum/trend system - as most systems will get caught by false momentum and will “buy the top,” and then proceed to “sell the bottom.”

Lower timeframes typically offer more data points for the algorithm to compute over, and enable quicker entries and exits within a robust system, often reducing downside risk and compounding gains more effectively - in all market environments.

However, slippage, fees, and execution constraints are still limiting factors. Although blue-chip cryptocurrencies are more liquid and can be traded with lower fees compared to low cap assets, frequent trading on lower timeframes incurs cumulative slippage costs. With the BPM system set to a realistic slippage rate of 0.2% per trade, this example emphasizes how even lower fees impact performance as trade frequency increases.

Finding the optimal balance between timeframe and slippage impact requires careful consideration of factors such as portfolio size, liquidity of selected tokens, execution speed, and the fee rate of the exchange you execute trades on.

Number of Position Changes

Understanding the number of position changes in a strategy is critical to assessing its feasibility in real world trading. Frequent position changes can lead to increased costs due to slippage and fees. Monitoring the number of position changes provides insight into the system’s behavior - helping to evaluate how active the strategy is and whether it aligns with the trader's desired time input for position management.

Equity Curve and Performance Calculations

To provide a benchmark, the script also generates a Buy-and-Hold (or "HODL") equity curve that represents a 100% allocation to Bitcoin, the highest market cap cryptoasset. This allows users to easily compare the performance of the dynamic rotation system with that of a more traditional investment strategy.

The script tracks key performance metrics for both the dynamic portfolio and the HODL strategy, including:

Sharpe Ratio

The Sharpe Ratio is a key metric that evaluates a portfolio’s risk adjusted return by comparing its ‘excess’ return to its volatility. Traditionally, the Sharpe Ratio measures returns relative to a risk-free rate. However, in our system’s calculation, we omit the risk-free rate and instead measure returns above a benchmark of 0%. This adjustment provides a more universal comparison, especially in the context of highly volatile assets like cryptocurrencies, where a traditional risk-free benchmark, such as the usual 3-month T-bills, is often irrelevant or too distant from the realities of the crypto market.

By using 0% as the baseline, we focus purely on the strategy's ability to generate raw returns in the face of market risk, which makes it easier to compare performance across different strategies or asset classes. In an environment like cryptocurrency, where volatility can be extreme, the importance of relative return against a highly volatile backdrop outweighs comparisons to a risk-free rate that bears little resemblance to the risk profile of digital assets.

Sortino Ratio

The Sortino Ratio improves upon the Sharpe Ratio by specifically targeting downside risk and leaves the upside potential untouched. In contrast to the Sharpe Ratio (which penalizes both upside and downside volatility), the Sortino Ratio focuses only on negative return deviations. This makes it a more suitable metric for evaluating strategies like the Bullrun Profit Maximizer - that aim to minimize drawdowns without restricting upside capture. By measuring returns relative to a 0% baseline, the Sortino ratio provides a clearer assessment of how well the system generates gains while avoiding substantial losses in highly volatile markets like crypto.

Omega Ratio

The Omega Ratio is calculated as the ratio of gains to losses across all return thresholds, providing a more complete view of how the system balances upside and downside risk even compared to the Sortino Ratio. While it achieves a similar outcome to the Sortino Ratio by emphasizing the system's ability to capture gains while limiting losses, it is technically a mathematically superior method. However, we include both the Omega and Sortino ratios in our metric table, as the Sortino Ratio remains more widely recognized and commonly understood by traders and investors of all levels.

Usage Summary:

While the backtests in this description are generated as if a trader held a portfolio of just the strongest tokens, this was mainly designed as a method of logical verification and not a recommended investment strategy. In practice, this system can be used in multiple ways.

It can be used as above, or as a factor in forming part of a broader asset selection tool, or even a method of filtering tokens by strength in order to inform a day trader which tokens might be optimal to look at, for long-only trading setups on an intrabar timeframe.

Summary

The Bullrun Profit Maximizer is an advanced tool tailored for traders, offering the precision and agility required in today’s markets. With its asset specific equity curve filter, reworked momentum analysis, and streamlined user interface, this system is engineered to maximize gains and minimize risk during bullmarkets, with a strong focus on risk adjusted performance.

Its refined approach, focused on high resolution data processing and adaptive reallocation, makes it a powerful choice for traders looking to capture high quality trends on clue-chip assets, no matter the market’s pace.

Trend Titan Neutronstar [QuantraSystems]Trend Titan NEUTRONSTAR

Credits

The Trend Titan NEUTRONSTAR is a comprehensive aggregation of nearly 100 unique indicators and custom combinations, primarily developed from unique and public domain code.

We'd like to thank our TradingView community members: @IkKeOmar for allowing us to add his well-built "Normalized KAMA Oscillator" and "Adaptive Trend Lines " indicators to the aggregation, as well as @DojiEmoji for his valuable "Drift Study (Inspired by Monte Carlo Simulations with BM)".

Introduction

The Trend Titan NEUTRONSTAR is a robust trend following algorithm meticulously crafted to meet the demands of crypto investors. Designed with a multi layered aggregation approach, NEUTRONSTAR excels in navigating the unique volatility and rapid shifts of the cryptocurrency market. By stacking and refining a variety of carefully selected indicators, it combines their individual strengths while reducing the impact of noise or false signals. This "aggregation of aggregators" approach enables NEUTRONSTAR to produce a consistently reliable trend signal across assets and timeframes, making it an exceptional tool for investors focused on medium to long term market positioning.

NEUTRONSTAR ’s powerful trend following capabilities provide investors with straightforward, data driven analysis. It signals when tokens exhibit sustained upward momentum and systematically removes allocations from assets showing signs of weakness. This structure aids investors in recognizing peak market phases. In fact, one of NEUTRONSTAR ’s most valuable applications is its potential to help investors time exits near the peak of bull markets. This aims to maximize gains while mitigating exposure to downturns.

Ultimately, NEUTRONSTAR equips investors with a high precision, adaptable framework for strategic decision making. It offers robust support to identify strong trends, manage risk, and navigate the dynamic crypto market landscape.

With over a year of rigorous forward testing and live trading, NEUTRONSTAR demonstrates remarkable robustness and effectiveness, maintaining its performance without succumbing to overfitting. The system has been purposefully designed to avoid unnecessary optimization to past data, ensuring it can adapt as market conditions evolve. By focusing on aggregating valuable trend signals rather than tuning to historical performance, the NEUTRONSTAR serves as a reliable universal trend following system that aligns with the natural market cycles of growth and correction.

Core Methodology

The foundation of the NEUTRONSTAR lies in its multi aggregated structure, where five custom developed trend models are combined to capture the dominant market direction. Each of these aggregates has been carefully crafted with a specific trend signaling period in mind, allowing it to adapt seamlessly across various timeframes and asset classes. Here’s a breakdown of the key components:

FLARE - The original Quantra Signaling Matrix (QSM) model, best suited for timeframes above 12 hours. It forms the foundation of long term trend detection, providing stable signals.

FLAREV2 - A refined and more sophisticated model that performs well across both high and low timeframes, adding a layer of adaptability to the system.

NEBULA - An advanced model combining FLARE and FLAREV2. NEBULA brings the advantages of both components together, enhancing reliability and capturing smoother, more accurate trends.

SPARK - A high speed trend aggregator based on the QSM Universal model. It focuses on fast moving trends, providing early signals of potential shifts.

SUNBURST - A balanced aggregate that combines elements of SPARK and FLARE, confirming SPARK’s signals while minimizing false positives.

Each of these models contributes its own unique perspective on market movement. By layering fast, medium, and slower trend following signals, NEUTRONSTAR can confirm strong trends while filtering out shorter term noise. The result is a comprehensive tool that signals clear market direction with minimized false signals.

A Unique Approach to Trend Aggregation

One of the defining characteristics of NEUTRONSTAR is its deliberate choice to avoid perfectly time coherent indicators within its aggregation. In simpler terms, NEUTRONSTAR purposefully incorporates trend following indicators with slightly different signal periods, rather than synchronizing all components to a single signaling period. This choice brings significant benefits in terms of diversification, adaptability, and robustness of the overall trend signal.

When aggregating multiple trend following components, if all indicators were perfectly time coherent - meaning they responded to market changes in exactly the same way and over the time periods - the resulting signal would effectively be no different from a single trend following indicator. This uniformity would limit the system’s ability to capture a variety of market conditions, leaving it vulnerable to the same noise or false signals that any single indicator might encounter. Instead, NEUTRONSTAR leverages a balanced mix of indicators with varied timing: some fast, some slower, and some in the medium range. This choice allows the system to extract the unique strengths of each component, creating a combined signal that is stronger and more reliable than any single indicator.

By incorporating different signal periods, NEUTRONSTAR achieves what can be thought of as a form of edge accumulation. The fast components within NEUTRONSTAR , for example, are highly sensitive to quick shifts in market direction. These indicators excel at identifying early trend signals, enabling NEUTRONSTAR to react swiftly to emerging momentum. However, these fast indicators alone would be prone to reacting to market noise, potentially generating too many premature signals. This is where the medium term indicators come into play. These components operate with a slower reaction time, filtering out the short term fluctuations and confirming the direction of the trend established by the faster indicators. The combination of these varying signal speeds results in a balanced, adaptive response to market changes.

This approach also allows NEUTRONSTAR to adapt to different market regimes seamlessly. In fast moving, volatile markets, the faster indicators provide an early alert to potential trend shifts, while the slower components offer a stabilizing influence, preventing overreaction to temporary noise. Conversely, in steadier or trending markets, the medium and slower indicators sustain the trend signal, reducing the likelihood of premature exits. This flexible design enhances NEUTRONSTAR ’s ability to operate effectively across multiple asset classes and timeframes, from short term fluctuations to longer term market cycles.

The result is a powerful, multi-layered trend following tool that remains adaptive, capturing the benefits of both fast and medium paced reactions without becoming overly sensitive to short term noise. This unique aggregation methodology also supports NEUTRONSTAR ’s robustness, reducing the risk of overfitting to historical data and ensuring that the system can perform reliably in forward testing and live trading environments. The slightly staggered signal periods provide a greater degree of resilience, making NEUTRONSTAR a dependable choice for traders looking to capitalize on sustained trends while minimizing exposure during periods of market uncertainty.

In summary, the lack of perfect time coherence among NEUTRONSTAR ’s sub components is not a flaw - but a deliberate, robust design choice.

Risk Management through Market Mode Analysis

An essential part of NEUTRONSTAR is its ability to assess the market's underlying behavior and adapt accordingly. It employs a Market Mode Analysis mechanism that identifies when the market is either in a “Trending State” or a “Mean Reverting State.” When enough confidence is established that the market is trending, the system confirms and signals a “Trending State,” which is optimal for maintaining positions in the direction of the trend. Conversely, if there’s insufficient confidence, it labels the market as “Mean Reverting,” alerting traders to potentially avoid trend trades during likely sideways movement.

This distinction is particularly valuable in crypto, where asset prices often oscillate between aggressive trends and consolidation periods. The Market Mode Analysis keeps traders aligned with the broader market conditions, minimizing exposure during periods of potential whipsaws and maximizing gains during sustained trends.

Zero Overfitting: Design and Testing for Real World Resilience

Unlike many trend following indicators that rely heavily on backtesting and optimization, NEUTRONSTAR was built to perform well in forward testing and live trading without post design adjustments. Over a year of live market exposure has all but proven its robustness, with the system’s methodology focused on universal applicability and simplicity rather than curve fitting to past data. This approach ensures the aggregator remains effective across different market cycles and maintains relevance as new data unfolds.

By avoiding overfitting, NEUTRONSTAR is inherently more resistant to the common issue of strategy degradation over time, making it a valuable tool for traders seeking reliable market analysis you can trust for the long term.

Settings and Customization Options

To accommodate a range of trading styles and market conditions, NEUTRONSTAR includes adjustable settings that allow for fine tuning sensitivity and signal generation:

Calculation Method - Users can choose between calculating the NEUTRONSTAR score based on aggregated scores or by using the state of individual aggregates (long, neutral, short). The score method provides faster signals with slightly more noise, while the state based approach offers a smoother signal.

Sensitivity Threshold - This setting adjusts the system’s sensitivity, defining the width of the neutral zone. Higher thresholds reduce sensitivity, allowing for a broader range of volatility before triggering a trend reversal.

Market Regime Sensitivity - A sensitivity adjustment, ranging from 0 to 100, that affects the sensitivity of the sub components in market regime calculation.

These settings offer flexibility for users to tailor NEUTRONSTAR to their specific needs, whether for medium term investment strategies or shorter term trading setups.

Visualization and Legend

For intuitive usability, NEUTRONSTAR uses color coded bar overlays to indicate trend direction:

Green - indicates an uptrend.

Gray - signals a neutral or transition phase.

Purple - denotes a downtrend.

An optional background color can be enabled for market mode visualization, indicating the overall market state as either trending or mean reverting. This feature allows traders to assess trend direction and strength at a glance, simplifying decision making.

Additional Metrics Table

To support strategic decision making, NEUTRONSTAR includes an additional metrics table for in depth analysis:

Performance Ratios - Sharpe, Sortino, and Omega ratios assess the asset’s risk adjusted returns.

Volatility Insights - Provides an average volatility measure, valuable for understanding market stability.

Beta Measurement - Calculates asset beta against BTC, offering insight into asset volatility in the context of the broader market.

These metrics provide deeper insights into individual asset behavior, supporting more informed trend based allocations. The table is fully customizable, allowing traders to adjust the position and size for a seamless integration into their workspace.

Final Summary

The Trend Titan NEUTRONSTAR indicator is a powerful and resilient trend following system for crypto markets, built with a unique aggregation of high performance models to deliver dependable, noise reduced trend signals. Its robust design, free from overfitting, ensures adaptability across various assets and timeframes. With customizable sensitivity settings, intuitive color coded visualization, and an advanced risk metrics table, NEUTRONSTAR provides traders with a comprehensive tool for identifying and riding profitable trends, while safeguarding capital during unfavorable market phases.

Heisenberg Uncertainty Moving Average (HUMA)Overview

This script introduces and approximation of the Heisenberg Uncertainty Moving Average (HUMA), inspired by the principles of quantum physics, particularly the Heisenberg Uncertainty Principle. The indicator dynamically adjusts its moving average length based on price and momentum uncertainty, ensuring adaptability to market conditions. It also features dynamic coloring to indicate the slope of the moving average.

Step-by-Step Explanation

Calculate Uncertainty in Price (Δx):

The price uncertainty is measured over a specified lookback period (length).

This is done by finding the difference between the highest high and lowest low over the period

Momentum uncertainty is defined using the Rate of Change (ROC) of the closing price over the same lookback period (length).

This indicates how much the price has changed over that period, providing a measure of momentum uncertainty.

Introduce Planck’s Constant (h):

Planck’s constant (h) is scaled down for financial use to set a theoretical minimum threshold for the product of uncertainties.

The threshold is defined as h / (4 * π) to simulate a limit that aligns with the Heisenberg Uncertainty Principle in physics.

Calculate the Uncertainty Product (Δx ⋅ Δp):

The product of price uncertainty (Δx) and the absolute value of momentum uncertainty (Δp) is calculated.

To ensure the product respects the minimum threshold set by quantum principles, the value is capped using math.max(uncertainty_product, threshold).

Normalize the Uncertainty Product to Determine the Moving Average Window Size:

The uncertainty product is used to adjust the length of the moving average dynamically.

The formula inversely adjusts the moving average length based on uncertainty: higher uncertainty results in a shorter (more responsive) window and lower uncertainty results in a longer (smoother) window.

Calculate the Heisenberg Uncertainty Moving Average (HUMA):

The slope is determined by finding the difference between the current HUMA value and the value from the previous period, smoothed with a Double Exponential Moving Average (DEMA).

This helps identify the direction of the trend: positive slope indicates an uptrend, and negative slope indicates a downtrend.

Dynamic Coloring Based on the Slope:

Bidirectional MoM w/ Time Weighting | Optional Intrabar DataBidirectional MoM w/ Time Weighting | Optional Intrabar Data

Core Components:

Intrabar Data Extraction:

The script optionally harnesses lower time frame data (e.g., per-second intervals) for high and low prices within each primary bar. You can set it to the current chart time but if you want to use intrabar data it uses the request.security_lower_tf() to properly pull intrabar data.

This fine-grained data enables an in-depth examination of the price action that occurs within a standard timeframe, enhancing the ability to detect subtle market movements.

A key threshold based on Average True Range (ATR) is used to measure significant price changes intrabar, adding a robust filter for volatility sensitivity.

Cumulative Time-to-Threshold Analysis:

The indicator tracks how long it takes for price changes to reach specified thresholds, marking critical time points when upward or downward price movements exceed these levels. This approach provides insights into the speed and intensity of directional shifts within the market.

The calculated time-to-threshold values act as temporal markers that influence subsequent momentum weighting.

Bidirectional Momentum Calculation:

Momentum is assessed in two directions (upward and downward) using a comprehensive array of price changes.

Adaptive Weighting Mechanism:

Each momentum value is weighted by the calculated time-to-threshold, giving preference to momentum that occurs more rapidly and aligning with potential breakout conditions.

The script also factors in correlations between momentum and price change, ensuring that only the most relevant signals contribute to the final analysis.

Iterative Length Analysis:

By iterating over a range of lengths (e.g., 100 to 200 periods), the script aggregates data to assess momentum across different time scales. This provides a more holistic view of market behavior, accommodating both short-term fluctuations and longer-term trends.

Each length is evaluated using moving averages and correlations to determine its contribution to the total weighted momentum.

Final Aggregated Output:

The weighted sums of upward and downward momentum are normalized by the total weight to produce a final composite metric.

The indicator plots these results as separate upward and downward momentum lines, offering traders a visual representation of which direction holds more momentum strength over various intervals.

Practical Application:

This indicator's advanced design is tailored for traders who require a deeper understanding of price movement dynamics and the underlying forces driving market momentum. By incorporating intrabar data, adaptive time-to-threshold calculations, and iterative analysis, this tool seeks to provide a clearer view of potential market direction shifts and their timing.

The indicator can be used to:

Identify potential breakout or reversal points by observing significant shifts in weighted momentum.

Gauge the relative strength of uptrends and downtrends through the plotted momentum lines.

Enhance decision-making with an additional layer of granularity from intrabar data.

In essence, this script is an ambitious attempt to blend multi-scale analysis, momentum dynamics, and time-weighted evaluation, creating a unique approach to understanding market behavior beyond conventional indicators.

RSI and Dev Advanced Volatility IndexEnglish Explanation of the "RSI and Dev Advanced Volatility Index" Pine Script Code

Understanding the Code

Purpose:

This Pine Script code creates a custom indicator that combines the Relative Strength Index (RSI) and Deviation (DEV) to provide insights into market volatility.

Key Components:

* Deviation (DEV): Calculates the difference between the closing price and the 10-period simple moving average. This measures the extent to which the price deviates from its recent average, indicating volatility.

* RSI: The traditional RSI is then applied to the calculated deviations. This helps to smooth the data and identify overbought or oversold conditions in terms of volatility.

Calculation Steps:

* Deviation Calculation: The difference between the closing price and its 10-period simple moving average is calculated.

* RSI Calculation: The RSI is calculated on the deviations, providing a measure of the speed and change of volatility relative to recent volatility changes.

* Plotting:

* The RSI of the deviations is plotted on the chart.

* Horizontal lines are plotted at 50, 0, and 110 to visually represent different volatility zones.

* The area between the lines is filled with color to highlight low and high volatility regions.

Interpretation and Usage

* Volatility Analysis:

* High Volatility: When the RSI is above 50, it indicates high volatility, suggesting the market might be in a consolidation or trend reversal phase.

* Low Volatility: When the RSI is below 50, it indicates low volatility, suggesting a relatively calm market.

* Trading Signals:

* Buy Signal: When the RSI crosses above 50 from below, it might signal increasing volatility, which could be a buying opportunity.

* Sell Signal: When the RSI crosses below 50 from above, it might signal decreasing volatility, which could be a selling opportunity.

* Risk Management:

* By monitoring volatility, traders can better manage their risk. During periods of high volatility, traders might reduce their position size or adopt more conservative strategies.

Advantages

* Comprehensive: Combines RSI and DEV for a more holistic view of volatility.

* Sensitivity: Quickly responds to changes in market volatility.

* Visual Clarity: Color-coded zones provide a clear visual representation of different volatility levels.

Limitations

* Parameter Sensitivity: The indicator's performance is sensitive to parameter changes, such as the lookback period for the moving average.

* Lag: Like most technical indicators, it has some lag and might not capture every market movement.

* Not Predictive: It can only indicate current and past volatility, not future movements.

Summary

This custom indicator offers a valuable tool for analyzing market volatility. By combining RSI and DEV, it provides a more nuanced perspective on price fluctuations. However, it should be used in conjunction with other technical indicators and fundamental analysis for more robust trading decisions.

Key points to remember:

* Higher RSI values indicate higher volatility.

* Lower RSI values indicate lower volatility.

* Crossovers of the RSI line above or below 50 can provide potential trading signals.

* The indicator should be used in conjunction with other analysis tools for a more complete picture of the market.

Enhanced Chaikin Money FlowEnhanced Chaikin Money Flow (CMF) with Normalized Distribution

The Enhanced Chaikin Money Flow (CMF) is a sophisticated version of Marc Chaikin's classic volume-weighted indicator that measures buying and selling pressure. This version incorporates statistical normalization and advanced smoothing techniques to provide more reliable signals.

Key Features

Normalized distribution (z-score) for better historical comparison

Multiple smoothing options (SMA, EMA, WMA, RMA) for noise reduction

Standard deviation bands (1σ and 2σ) to identify extreme readings

Adjustable parameters for customization

Alert system for extreme readings

Interpretation

Values represent standard deviations from the mean

Above 0: Indicates net buying pressure

Below 0: Indicates net selling pressure

Outside ±2σ bands: Suggests extreme market conditions

Crossovers of standard deviation bands may signal potential reversals

Technical Details

The indicator combines volume with price location within a bar to determine buying/selling pressure, then normalizes these values using a rolling z-score calculation. This normalization allows for better historical comparison and more reliable overbought/oversold signals.

Best used in conjunction with price action and other indicators for confirmation of potential market turns or trend strength.

Stablecoin Dominance Oscillator

The SDO is a normalized oscillator that tracks the relationship between stablecoin market capitalization (USDT + USDC + DAI) and total crypto market capitalization. It helps identify periods where stablecoins represent an unusually high or low portion of the total crypto market value.

Key components:

Main Signal (Blue Line):

Shows the normalized deviation of stablecoin dominance from its trend. Higher values indicate higher stablecoin dominance relative to history (which often corresponds with market bottoms/fear), while lower values indicate lower stablecoin dominance (often seen during strong bull markets/greed).

Dynamic Bands (Gray):

These adapt to market volatility, expanding during volatile periods and contracting during stable periods

Generally suggest temporary boundaries for the oscillator

Volatility Reference (Purple Line):

Shows the ratio between short-term and long-term volatility

Higher values indicate more volatile market conditions

Helps contextualize the reliability of the current signal

The indicator uses a 500-period lookback for baseline calculations and a 15-period Hull Moving Average for smoothing, making it responsive while filtering out noise. The final signal is normalized and volatility-adjusted to maintain consistent readings across different market regimes.

Enhanced Market Analyzer with Adaptive Cognitive LearningThe "Enhanced Market Analyzer with Advanced Features and Adaptive Cognitive Learning" is an advanced, multi-dimensional trading indicator that leverages sophisticated algorithms to analyze market trends and generate predictive trading signals. This indicator is designed to merge traditional technical analysis with modern machine learning techniques, incorporating features such as adaptive learning, Monte Carlo simulations, and probabilistic modeling. It is ideal for traders who seek deeper market insights, adaptive strategies, and reliable buy/sell signals.

Key Features:

Adaptive Cognitive Learning:

Utilizes Monte Carlo simulations, reinforcement learning, and memory feedback to adapt to changing market conditions.

Adjusts the weighting and learning rate of signals dynamically to optimize predictions based on historical and real-time data.

Hybrid Technical Indicators:

Custom RSI Calculation: An RSI that adapts its length based on recursive learning and error adjustments, making it responsive to varying market conditions.

VIDYA with CMO Smoothing: An advanced moving average that incorporates Chander Momentum Oscillator for adaptive smoothing.

Hamming Windowed VWMA: A volume-weighted moving average that applies a Hamming window for smoother calculations.

FRAMA: A fractal adaptive moving average that responds dynamically to price movements.

Advanced Statistical Analysis:

Skewness and Kurtosis: Provides insights into the distribution and potential risk of market trends.

Z-Score Calculations: Identifies extreme market conditions and adjusts trading thresholds dynamically.

Probabilistic Monte Carlo Simulation:

Runs thousands of simulations to assess potential price movements based on momentum, volatility, and volume factors.

Integrates the results into a probabilistic signal that informs trading decisions.

Feature Extraction:

Calculates a variety of market metrics, including price change, momentum, volatility, volume change, and ATR.

Normalizes and adapts these features for use in machine learning algorithms, enhancing signal accuracy.

Ensemble Learning:

Combines signals from different technical indicators, such as RSI, MACD, Bollinger Bands, Stochastic Oscillator, and statistical features.

Weights each signal based on cumulative performance and learning feedback to create a robust ensemble signal.

Recursive Memory and Feedback:

Stores and averages past RSI calculations in a memory array to provide historical context and improve future predictions.

Adaptive memory factor adjusts the influence of past data based on current market conditions.

Multi-Factor Dynamic Length Calculation:

Determines the length of moving averages based on volume, volatility, momentum, and rate of change (ROC).

Adapts to various market conditions, ensuring that the indicator is responsive to both high and low volatility environments.

Adaptive Learning Rate:

The learning rate can be adjusted based on market volatility, allowing the system to adapt its speed of learning and sensitivity to changes.

Enhances the system's ability to react to different market regimes.

Monte Carlo Simulation Engine:

Simulates thousands of random outcomes to model potential future price movements.

Weights and aggregates these simulations to produce a final probabilistic signal, providing a comprehensive risk assessment.

RSI with Dynamic Adjustments:

The initial RSI length is adjusted recursively based on calculated errors between true RSI and predicted RSI.

The adaptive RSI calculation ensures that the indicator remains effective across various market phases.

Hybrid Moving Averages:

Short-Term and Long-Term Averages: Combines FRAMA, VIDYA, and Hamming VWMA with specific weights for a unique hybrid moving average.

Weighted Gradient: Applies a color gradient to indicate trend strength and direction, improving visual clarity.

Signal Generation:

Generates buy and sell signals based on the ensemble model and multi-factor analysis.

Uses percentile-based thresholds to determine overbought and oversold conditions, factoring in historical data for context.

Optional settings to enable adaptation to volume and volatility, ensuring the indicator remains effective under different market conditions.

Monte Carlo and Learning Parameters:

Users can customize the number of Monte Carlo simulations, learning rate, memory factor, and reward decay for tailored performance.

Applications:

Scalping and Day Trading:

The fast response of the adaptive RSI and ensemble learning model makes this indicator suitable for short-term trading strategies.

Swing Trading:

The combination of long-term moving averages and probabilistic models provides reliable signals for medium-term trends.

Volatility Analysis:

The ATR, Bollinger Bands, and adaptive moving averages offer insights into market volatility, helping traders adjust their strategies accordingly.

No Trade Zone Indicator [CHE]No Trade Zone Indicator

The "No Trade Zone Indicator " is a powerful tool designed to help traders identify periods when the market may not present favorable trading opportunities. By analyzing the percentage change in the 20-period Simple Moving Average (SMA20) relative to a dynamically adjusted threshold based on market volatility, this indicator highlights times when it's prudent to stay out of the market.

Why Knowing When Not to Trade Is Important

Understanding when not to trade is just as crucial as knowing when to enter or exit a position. Trading during periods of low volatility or uncertain market direction can lead to unnecessary risks and potential losses. By recognizing these "No Trade Zones," you can:

- Avoid Low-Probability Trades: Reduce the chances of entering trades with unfavorable risk-to-reward ratios.

- Preserve Capital: Protect your investment from unpredictable market movements.

- Enhance Focus: Concentrate on high-quality trading opportunities that align with your strategy.

How the Indicator Works

- SMA20 Calculation: Computes the 20-period Simple Moving Average of closing prices to identify the market's short-term trend.

- ATR Measurement: Calculates the Average True Range (ATR) over a user-defined period (default is 14) to assess market volatility.

- Dynamic Threshold: Determines an adjusted threshold by multiplying the ATR percentage by a Threshold Adjustment Factor (default is 0.05).

- Trend Analysis: Compares the percentage change of the SMA20 against the adjusted threshold to evaluate market momentum.

- Status Identification:

- Long: Indicates a rising SMA20 above the threshold—suggesting a potential upward trend.

- Short: Indicates a falling SMA20 above the threshold—suggesting a potential downward trend.

- No Trade: Signals when the SMA20 change is below the threshold, marking a period of low volatility or indecision.

Features

- Customizable Settings: Adjust the ATR period and Threshold Adjustment Factor to suit different trading styles and market conditions.

- Visual Indicators: Colored columns represent market status—green for "Long," red for "Short," and gray for "No Trade."

- On-Chart Table: An optional table displays the current market status directly on your chart for quick reference.

- Alerts: Set up alerts to receive notifications when the market enters a "No Trade Zone," helping you stay informed without constant monitoring.

How to Use the Indicator

1. Add to Chart: Apply the "No Trade Zone Indicator " to your preferred trading chart on TradingView.

2. Configure Settings: Customize the ATR period and Threshold Adjustment Factor based on your analysis and risk tolerance.

3. Interpret Signals:

- Green Columns: Consider looking for buying opportunities as the market shows upward momentum.

- Red Columns: Consider looking for selling opportunities as the market shows downward momentum.

- Gray Columns: Refrain from trading as the market lacks clear direction.

4. Monitor Alerts: Use the alert feature to get notified when the market status changes, allowing you to make timely decisions.

Conclusion

Incorporating the "No Trade Zone Indicator " into your trading toolkit can enhance your decision-making process by clearly indicating when the market may not be conducive to trading. By focusing on periods with favorable conditions and avoiding low-volatility times, you can improve your trading performance and achieve better results over the long term.

*Trade wisely, and remember—the best trade can sometimes be no trade at all.*

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

best regards

Chervolino

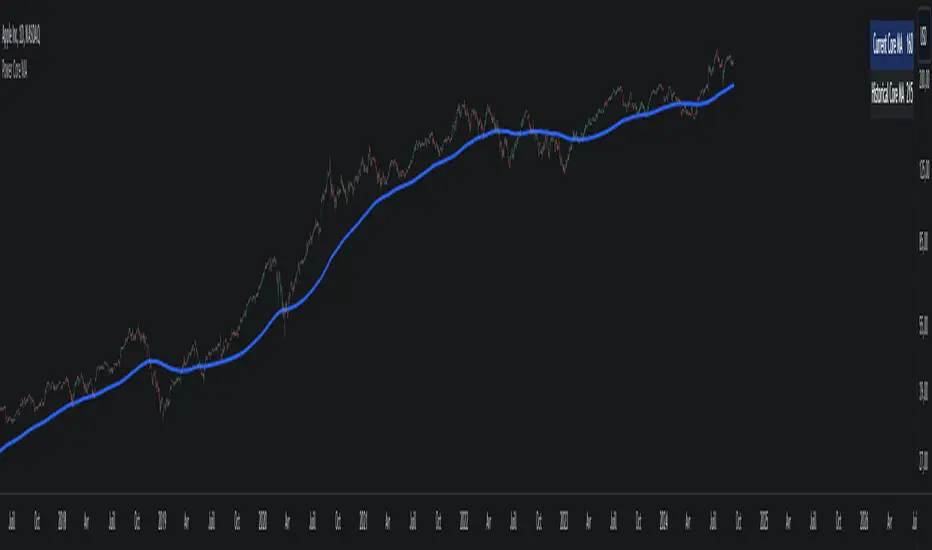

Power Core MAThe Power Core MA indicator is a powerful tool designed to identify the most significant moving average (MA) in a given price chart. This indicator analyzes a wide range of moving averages, from 50 to 400 periods, to determine which one has the strongest influence on the current price action.

The blue line plotted on the chart represents the "Current Core MA," which is the moving average that is most closely aligned with other nearby moving averages. This line indicates the current trend and potential support or resistance levels.

The table displayed on the chart provides two important pieces of information. The "Current Core MA" value shows the length of the moving average that is currently most influential. The "Historical Core MA" value represents the average length of the most influential moving averages over time.

This indicator is particularly useful for traders and analysts who want to identify the most relevant moving average for their analysis. By focusing on the moving average that has the strongest historical significance, users can make more informed decisions about trend direction, support and resistance levels, and potential entry or exit points.

The Power Core MA is an excellent tool for those interested in finding the strongest moving average in the price history. It simplifies the process of analyzing multiple moving averages by automatically identifying the most influential one, saving time and providing valuable insights into market dynamics.

By combining current and historical data, this indicator offers a comprehensive view of the market's behavior, helping traders to adapt their strategies to the most relevant timeframes and trend strengths.

Nami Bands with Future Projection [FXSMARTLAB]The Nami Bands ( Inspired by "Nami", meaning "wave" in Japanese) are two dynamic bands around price data: an upper band and a lower band. These bands are calculated based on an Asymmetric Linear Weighted Moving Average of price and a similarly asymmetric weighted standard deviation. This weighting method emphasizes recent data without overreacting to short-term price changes, thus smoothing the bands in line with prevailing market conditions.

Advantages and Benefits of Using the Indicator

* Volatility Analysis: The bands expand and contract with market volatility, helping traders assess periods of high and low volatility. Narrow bands indicate low volatility and potential consolidation, while wide bands suggest increased volatility and potential price movement.

* Dynamic Support and Resistance Levels: By adapting to recent trends, the bands serve as dynamic support (lower band) and resistance (upper band) levels, which traders can use for entry and exit signals.

* Overbought and Oversold Conditions: When prices reach or cross the bands’ outer limits, it may signal overbought (upper band) or oversold (lower band) conditions, suggesting possible reversals or trend slowdowns.

* Trend Confirmation and Continuation: The slope of the central moving average confirms trend direction. An upward slope generally indicates a bullish trend, while a downward slope suggests a bearish trend.

* Anticipating Breakouts and Reversals: The projected bands help identify where price movements may head, allowing traders to anticipate potential breakouts or reversals based on projected support and resistance.

Indicator Parameters

Source (src): The price data used for calculations, by default set to the average of high, low, and close (hlc3).

Length: The period over which calculations are made, defaulted to 50 periods.

Projection Length: The length for future band projection, defaulted to 20 periods.

StdDev Multiplier (mult): A multiplier for the standard deviation, defaulted to 2.0.

Internal Calculations

1. Asymmetric Linear Weighted Moving Average of Price

The indicator uses an Asymmetric Linear Weighted Moving Average (ALWMA) to calculate a central value for the price.

Asymmetric Weighting: This weighting technique assigns the highest weight to the most recent value, with weights decreasing linearly as the data points become older. This structure provides a nuanced focus on recent price trends, while still reflecting historical price levels.

2. Asymmetric Weighted Standard Deviation

The standard deviation in this indicator is also calculated using asymmetric weighting:

Purpose of Asymmetric Weighted Standard Deviation: Rather than aiming for high sensitivity to recent data, this standard deviation measure smooths out volatility by integrating weighted values across the length period, stabilizing the overall measurement of price variability.

This approach yields a balanced view of volatility, capturing broader market trends without being overly reactive to short-lived changes.

3. Upper and Lower Bands

The upper and lower bands are created by adding and subtracting the asymmetric weighted standard deviation from the asymmetric weighted average of price. This creates a dynamic envelope that adjusts to both recent price trends and the smoothed volatility measure:

These bands represent adaptable support and resistance levels that shift with recent market volatility.

Future Band Projection

The indicator provides a projection of the bands based on their current slope.

1. Calculating the Slope of the Bands

The slope for each band is derived from the difference between the current and previous values of each band.

2. Projecting the Bands into the Future

For each period into the future, up to the defined Projection Length, the bands are projected using the current slope.

This feature offers an anticipated view of where support and resistance levels may move, providing insight for future market behavior based on current trends.

ATT Model with Buy/Sell SignalsIndicator Summary

This indicator is based on the ATT (Arithmetic Time Theory) model, using specific turning points derived from the ATT sequence (3, 11, 17, 29, 41, 47, 53, 59) to identify potential market reversals. It also integrates the RSI (Relative Strength Index) to confirm overbought and oversold conditions, triggering buy and sell signals when conditions align with the ATT sequence and RSI level.

Turning Points: Detected based on the ATT sequence applied to bar count. This suggests high-probability areas where the market could turn.

RSI Filter: Adds strength to the signals by ensuring buy signals occur when RSI is oversold (<30) and sell signals when RSI is overbought (>70).

Max Signals Per Session: Limits signals to two per session to reduce over-trading.

Entry Criteria

Buy Signal: Enter a buy trade if:

The indicator displays a green "BUY" marker.

RSI is below the oversold level (default <30), suggesting a potential upward reversal.

Sell Signal: Enter a sell trade if:

The indicator displays a red "SELL" marker.

RSI is above the overbought level (default >70), indicating a potential downward reversal.

Exit Criteria

Take Profit (TP):

Define TP as a fixed percentage or point value based on the asset's volatility. For example, set TP at 1.5-2x the risk, or a predefined point target (like 50-100 points).

Alternatively, exit the position when price approaches a key support/resistance level or the next significant swing high/low.

Stop Loss (SL):

Place the SL below the recent low (for buys) or above the recent high (for sells).

Set a fixed SL in points or percentage based on the asset’s average movement range, like an ATR-based stop, or limit it to a specific risk amount per trade (1-2% of account).

Trailing into Profit

Use a trailing strategy to lock in profits and let winning trades run further. Two main options:

ATR Trailing Stop:

Set the trailing stop based on the ATR (Average True Range), adjusting every time a new candle closes. This can help in volatile markets by keeping the stop at a consistent distance based on recent price movement.

Break-Even and Partial Profits:

When the price moves in your favor by a set amount (e.g., 1:1 risk/reward), move SL to the entry (break-even).

Take partial profit at intermediate levels (e.g., 50% at 1:1 RR) and trail the remainder.

Risk Management for Prop Firm Evaluation

Prop firms often have strict rules on daily loss limits, max drawdowns, and minimum profit targets. Here’s how to align your strategy with these:

Limit Risk per Trade:

Keep risk per trade to a conservative level (e.g., 1% or lower of your account balance). This allows for more room in case of a drawdown and aligns with most prop firm requirements.

Daily Loss Limits:

Set a daily stop-loss that ensures you don’t exceed the firm’s rules. For example, if the daily limit is 5%, stop trading once you reach a 3-4% drawdown.

Avoid Over-Trading:

Stick to the max signals per session rule (one or two trades). Taking only high-probability setups reduces emotional and reactive trades, preserving capital.

Stick to a Profit Target:

Aim to meet the evaluation’s profit goal efficiently but avoid risky or oversized trades to reach it faster.

Avoid Major Economic Events:

News events can disrupt technical setups. Avoid trading around significant releases (like FOMC or NFP) to reduce the chance of sudden losses due to high volatility.

Summary

Using this strategy with discipline, a structured entry/exit approach, and tight risk management can maximize your chances of passing a prop firm evaluation. The ATT model’s turning points, combined with the RSI, provide an edge by highlighting reversal zones, while limiting trades to 1-2 per session helps maintain controlled risk.

Low Price VolatilityI highlighted periods of low price volatility in the Nikkei 225 futures trading.

It is Japan Standard Time (JST)

This script is designed to color-code periods in the Nikkei 225 futures market according to times when prices tend to be more volatile and times when they are less volatile. The testing period is from March 11, 2024, to November 1, 2024. It identifies periods and counts where price movement exceeded half of the ATR, and colors are applied based on this data. There are no calculations involved; it simply uses the results of the analysis to apply color.

New Day [UkutaLabs]█ OVERVIEW

The New Day indicator is a useful trading tool that automatically identifies the first bar of each trading day for the user’s convenience.

█ USAGE

At the beginning of each trading day, this indicator will automatically create a line that will display the first bar of the trading day. This is a useful way to visualize where each day begins and ends.

When this indicator is used on a stock or futures chart, the first bar of the session will be identified as the first bar of the trading day. If this indicator is used on crypto or forex charts, which are tradable for 24 hours, the indicator will identify the bar closest to midnight as the first bar of the trading day.

█ SETTINGS

Configuration

• Line Color: This setting allows the user to determine the color of the New Day line.

• Line Width: This setting allows the user to determine the width of the New Day line.

• Line Style: This setting allows the user to determine the style of the New Day line.

Confirmed market structure buy/sell indicatorOverview

The Swing Point Breakout Indicator with Multi-Timeframe Dashboard is a TradingView tool designed to identify potential buy and sell signals based on swing point breakouts on the primary chart's timeframe while simultaneously providing a snapshot of the market structure across multiple higher timeframes. This dual approach helps traders make informed decisions by aligning short-term signals with broader market trends.

Key Features

Swing Point Breakout Detection

Swing Highs and Lows: Identifies significant peaks and troughs based on a user-defined lookback period.

Breakout Signals:

Bullish Breakout (Buy Signal): Triggered when the price closes above the latest swing high.

Bearish Breakout (Sell Signal): Triggered when the price closes below the latest swing low.

Visual Indicators: Highlights breakout bars with colors (lime for bullish, red for bearish) and plots buy/sell markers on the chart.

Multi-Timeframe Dashboard

Timeframes Monitored: 1m, 5m, 15m, 1h, 4h, 1D, and 1W.

Market Structure Status:

Bullish: Indicates upward market structure.

Bearish: Indicates downward market structure.

Neutral: No clear trend.

Visual Table: Displays each timeframe with its current status, color-coded for quick reference (green for bullish, red for bearish, gray for neutral).

Operational Workflow

Initialization:

Sets up a dashboard table on the chart's top-right corner with headers "Timeframe" and "Status".

Swing Point Detection:

Continuously scans the main timeframe for swing highs and lows using the specified lookback period.

Updates the latest swing high and low levels.

Signal Generation:

Detects when the price breaks above the last swing high (bullish) or below the last swing low (bearish).

Activates potential buy/sell setups and confirms signals based on subsequent price movements.

Dashboard Update:

For each defined higher timeframe, assesses the market structure by checking for breakouts of swing points.

Updates the dashboard with the current status for each timeframe, aiding in trend confirmation.

Visualization:

Colors the bars where breakouts occur.

Plots buy and sell signals directly on the chart for easy identification.

US Party Rule Indicator**Here's a description you can use for the indicator:**

**US Party Rule Indicator**

This indicator visually represents the political party in power in the United States over a specified period. It overlays a colored 200-day Exponential Moving Average (EMA) on the chart. The color of the EMA changes to reflect the ruling party, providing a visual representation of political influence on market trends.

**Key Features:**

- **Dynamic Color-Coded EMA:** The 200-EMA changes color to indicate the party in power (Red for Republican, Blue for Democrat).

- **Clear Visual Representation:** The colored EMA provides an easy-to-understand visual cue for identifying periods of different political parties.

- **Historical Context:** By analyzing the historical data, you can gain insights into potential correlations between party rule and market trends.

**How to Use:**

1. **Add the Indicator:** Add the "US Party Rule Indicator" to your chart.

2. **Interpret the Color:** The color of the 200-EMA indicates the ruling party at that time.

3. **Analyze Market Trends:** Use the indicator to identify potential correlations between political events and market movements.

**Note:** This indicator is for informational purposes only and should not be used as the sole basis for investment decisions. Always conduct thorough research and consider consulting with a financial advisor.

High/Low Location Frequency [LuxAlgo]The High/Low Location Frequency tool provides users with probabilities of tops and bottoms at user-defined periods, along with advanced filters that offer deep and objective market information about the likelihood of a top or bottom in the market.

🔶 USAGE

There are four different time periods that traders can select for analysis of probabilities:

HOUR OF DAY: Probability of occurrence of top and bottom prices for each hour of the day

DAY OF WEEK: Probability of occurrence of top and bottom prices for each day of the week

DAY OF MONTH: Probability of occurrence of top and bottom prices for each day of the month

MONTH OF YEAR: Probability of occurrence of top and bottom prices for each month

The data is displayed as a dashboard, which users can position according to their preferences. The dashboard includes useful information in the header, such as the number of periods and the date from which the data is gathered. Additionally, users can enable active filters to customize their view. The probabilities are displayed in one, two, or three columns, depending on the number of elements.

🔹 Advanced Filters

Advanced Filters allow traders to exclude specific data from the results. They can choose to use none or all filters simultaneously, inputting a list of numbers separated by spaces or commas. However, it is not possible to use both separators on the same filter.

The tool is equipped with five advanced filters:

HOURS OF DAY: The permitted range is from 0 to 23.

DAYS OF WEEK: The permitted range is from 1 to 7.

DAYS OF MONTH: The permitted range is from 1 to 31.

MONTHS: The permitted range is from 1 to 12.

YEARS: The permitted range is from 1000 to 2999.

It should be noted that the DAYS OF WEEK advanced filter has been designed for use with tickers that trade every day, such as those trading in the crypto market. In such cases, the numbers displayed will range from 1 (Sunday) to 7 (Saturday). Conversely, for tickers that do not trade over the weekend, the numbers will range from 1 (Monday) to 5 (Friday).

To illustrate the application of this filter, we will exclude results for Mondays and Tuesdays, the first five days of each month, January and February, and the years 2020, 2021, and 2022. Let us review the results:

DAYS OF WEEK: `2,3` or `2 3` (for crypto) or `1,2` or `1 2` (for the rest)

DAYS OF MONTH: `1,2,3,4,5` or `1 2 3 4 5`

MONTHS: `1,2` or `1 2`

YEARS: `2020,2021,2022` or `2020 2021 2022`

🔹 High Probability Lines

The tool enables traders to identify the next period with the highest probability of a top (red) and/or bottom (green) on the chart, marked with two horizontal lines indicating the location of these periods.

🔹 Top/Bottom Labels and Periods Highlight

The tool is capable of indicating on the chart the upper and lower limits of each selected period, as well as the commencement of each new period, thus providing traders with a convenient reference point.

🔶 SETTINGS

Period: Select how many bars (hours, days, or months) will be used to gather data from, max value as default.

Execution Window: Select how many bars (hours, days, or months) will be used to gather data from

🔹 Advanced Filters

Hours of day: Filter which hours of the day are excluded from the data, it accepts a list of hours from 0 to 23 separated by commas or spaces, users can not mix commas or spaces as a separator, must choose one

Days of week: Filter which days of the week are excluded from the data, it accepts a list of days from 1 to 5 for tickers not trading weekends, or from 1 to 7 for tickers trading all week, users can choose between commas or spaces as a separator, but can not mix them on the same filter.

Days of month: Filter which days of the month are excluded from the data, it accepts a list of days from 1 to 31, users can choose between commas or spaces as separator, but can not mix them on the same filter.

Months: Filter months to exclude from data. Accepts months from 1 to 12. Choose one separator: comma or space.

Years: Filter years to exclude from data. Accepts years from 1000 to 2999. Choose one separator: comma or space.

🔹 Dashboard

Dashboard Location: Select both the vertical and horizontal parameters for the desired location of the dashboard.

Dashboard Size: Select size for dashboard.

🔹 Style

High Probability Top Line: Enable/disable `High Probability Top` vertical line and choose color

High Probability Bottom Line: Enable/disable `High Probability Bottom` vertical line and choose color

Top Label: Enable/disable period top labels, choose color and size.

Bottom Label: Enable/disable period bottom labels, choose color and size.

Highlight Period Changes: Enable/disable vertical highlight at start of period

Multi-Timeframe Period Separators█ OVERVIEW

This indicator plots period separators for up to four higher timeframes. The separators are fully customizable and designed to work on any symbols.

█ FEATURES

Reference

You can choose to plot the separators starting from midnight 00:00 or the opening of the exchange trading session.

Timezone

You can specify to localize midnight 00:00 to the region of your liking. The timezone format conveniently requires no manual adjustment during clock changes.

█ NOTES

Scans the bar opening and closing times

The script checks the bar ` time ` and ` time_close ` to pinpoint the separators that can occur intrabar.

Tracks from the last separator

The script tracks the time elapsed since the last separator, which is useful when there is no trading activity or the market is closed. As it can result in missing bars, it plots the separator on the first available bar.

Others

The script automatically hides the separators when navigating to an equal or higher chart timeframe.

Bg color with 5 Date and 3 Time each by nitesh Bg color with 5 Date and 3Time each by nitesh this indicator will plot background color on the chart on your selected date and time spaan it hase three time spaan you can select time according to your need i have created this indicator to backtest time based price movments may this be helpful to you too (jai shree ram)

Pulse DPO: Major Cycle Tops and Bottoms█ OVERVIEW

Pulse DPO is an oscillator designed to highlight Major Cycle Tops and Bottoms .

It works on any market driven by cycles. It operates by removing the short-term noise from the price action and focuses on the market's cyclical nature.

This indicator uses a Normalized version of the Detrended Price Oscillator (DPO) on a 0-100 scale, making it easier to identify major tops and bottoms.

Credit: The DPO was first developed by William Blau in 1991.

█ HOW TO READ IT

Pulse DPO oscillates in the range between 0 and 100. A value in the upper section signals an OverBought (OB) condition, while a value in the lower section signals an OverSold (OS) condition.

Generally, the triggering of OB and OS conditions don't necessarily translate into swing tops and bottoms, but rather suggest caution on approaching a market that might be overextended.

Nevertheless, this indicator has been customized to trigger the signal only during remarkable top and bottom events.

I suggest using it on the Daily Time Frame , but you're free to experiment with this indicator on other time frames.

The indicator has Built-in Alerts to signal the crossing of the Thresholds. Please don't act on an isolated signal, but rather integrate it to work in conjunction with the indicators present in your Trading Plan.

█ OB SIGNAL ON: ENTERING OVERBOUGHT CONDITION

When Pulse DPO crosses Above the Top Threshold it Triggers ON the OB signal. At this point the oscillator line shifts to OB color.

When Pulse DPO enters the OB Zone, please beware! In this Area the Major Players usually become Active Sellers to the Public. While the OB signal is On, it might be wise to Consider Selling a portion or the whole Long Position.

Please note that even though this indicator aims to focus on major tops and bottoms, a strong trending market might trigger the OB signal and stay with it for a long time. That's especially true on young markets and on bubble-mode markets.

█ OB SIGNAL OFF: EXITING OVERBOUGHT CONDITION