Price Cross ━ [whvntr]This oscillator is an attractive way to view hidden price divergence... The formula originated from the Lark, but I have cleanly displayed this information. When the two moving averages (ema) cross with a simple moving average, you find the hidden price divergence. What kind of market should you use this in? It works well when a trend is already established.

Disclaimer: This indicator does not constitute investment advice. Trade at your own

risk with this method of identifying hidden price divergence.

Центральные осцилляторы

1st Gray Cross Signals ━ Histogram SQZMOM [whvntr][LazyBear]This is the Histogram Version of one of my other indicators named: SQZ Momentum + 1st Gray Cross Signals (with arrows) Which is a modification of "Squeeze Momentum Indicator" by user: "LazyBear". In that indicator of his he described, and suggested, the use of his gray cross signals to find points of interest for trading based on the direction of momentum when the first gray cross appears... I have programmed these points, and highlighted them, for ease of use. The 1st gray cross strategy, he said , is from John F. Carter's book, Chapter 11, "Mastering the Trade".

Here we have the Histogram version, with background highlights only, and nothing on the chart, in true SQZ Momentum style.

Disclaimer: using this indicator, or any indicator anywhere, involves risk when trading and isn't a guarantee of 100% accurate results.

Volume Cross ━ (For Volume Crop) [whvntr]This fulfills a request from user: iTibu to make an oscillator to go along with one of my indicators named: " Volume Crop ━ Hidden Volume Divergence ". It essentially does the same thing, without the Midline Tool , so you can better understand where the crosses are happening. Again, the hidden MACD Divergence circles formula originated from TheLark. I converted these values to volume instead of price.

Disclaimer: using this indicator, or any indicator anywhere, involves risk when trading and isn't a guarantee of 100% accurate results.

RedK K-MACD : a MACD with some more musclesMoving Averages are probably the most commonly used analysis tools, and MACD is possibly the first charting indicator a trader gets to learn about.

MACD Basic concept

----------------------------

Without repeating all the tons of documentation about what MACD does, let's quickly re-visit the MACD concept from a 10-mile altitude (note we're keen on simplifying here rather than being technically accurate - so please forgive the use of any "common lingos")

- MACD goal is to represent the distance between 2 Moving Averages (MAs) - one fast and one slow, relatively - as an unrestricted zero-based oscillator.

- The value of the main MACD line is the distance, or the displacement between the 2 MA's

- usually a signal line is used (which is another MA of that distance value) to enable better visualization of the change (and rate of change, since this is all depicted on a time axis) of that displacement - this represents price momentum (price movement in the recent period versus movements for a relatively longer period).

- the difference between the main MACD line and its signal is then represented as a histogram above and below the zero line. in this case, that histogram is really redundant, since it shows a value that is already represented visually by the main line and its signal line.

How K-MACD is different

---------------------------------

K-MACD takes that simple concept of the classic MACD and expands around it - the idea is to use the same simple approach to representing price momentum while bringing in more insight to price moves in the short, medium and long terms, ability to represent more than 2 MA's and to enable better identification of tradeable patterns (like Volatility Contraction and others) - while still keeping things simple and visually clean.

K-MACD is an indicator that allows us to view how price moves against 3 moving averages: a fast / slow pair, and a "market" Filter or Baseline (very long) that will be used as a flag for Bear/Bull market mode. Many traders and trading literature use the 200 day (40 week) SMA as that key filter

so in total, there are 4 MA lines in K-MACD (excluding the "orange" signal line):

* Price Proxy: Which is a very fast moving average that will represent the price itself - let's use a WMA(3) or something close to that here - there will be a signal line to enable better visualization of this similar to a classic MACD - that's the orange line

* Fast & Slow MA's : Use whatever represents the "medium term" momentum for your trading - Some traders use 20 and 50, others use 10 and 20 .. if on your price chart, you keep using a pair of MA's for this, use the same settings in K-MACD - these will be represented by the 3-color Momentum Bars that fluctuate above and below the baseline

* Filter/Baseline MA: Should be your long (Bullish/Bearish Mode) MA. so 100 or 200 or any other value you consider your market to be bearish below and bullish above. on K-MACD this is actually the blue zero line - everything else is "relative" to it

Review the sample chart which explains various elements and the "price chart" setup that K-MACD represents. With K-MACD you can clean up your chart from those various Moving Averages - or use a different set than the ones you already have K-MACD represent - or other indicators (like ATR channels..etc)

Other "muscles" in the K-MACD

---------------------------------------------

- Relative vs Classic Calculation Mode

A key issue with the classic MACD is that the displacement between the 2 moving averages is represented as "absolute or direct" values - as the price of the underlying increases with time, you can't really use these values to make useful comparison between the past and now (see below example) - also you can't use them to compare 2 different instruments.

- The "Relative" calculation option in K-MACD addresses that issue by relating all "distances" to the Baseline MA as percentage (above or below) - you can see this clear when you look at the above chart the far left versus the far right and compare K-MACD with the classic MACD - the Classic option is still available

- More MA "type" options for all MA lines: choose between SMA, EMA, WMA, and RSS_WMA (which i use a lot in my trading and is my default for the Price Proxy)

- More Alerts: a total or 9 alerts (in 3 groups) are available with K-MACD (Momentum above or below baseline, Price Proxy crossing signal line, and Price Proxy crossing baseline)

- New 52 week High / Low markers: These will show as Green/red circles on the zero line in K-MACD. this will only work for 1D timeframe and above, i'm just using a simple approach and would like to keep it that way.

- i know i added some more features not covered above :) -- if you have questions about any of the settings, feel free to ask below

Closing thoughts

-------------------------

K-MACD is a combination of couple of indicators i published in the past (xMACD and Mo_Bars) - so you can go back and read about them if needed - I then added improvements to accommodate ideas from swing trading literature and common practices that i plan to focus on in future. So K-MACD is really part of my own trading setup.

I assume here that most traders are familiar with what a MACD is - so kept this post short - if you thing we should expand more about the concepts covered here let me know in the comments - i can make some separate posts with examples and more details.

I hope many fellow traders find this work useful - and feel free let me know in comments below if you do.

ATR Oscillator - Index (Average True range Oscillator)The purpose of converting the ATR value indicator to an oscillator;

It is known that the ATR value is not between the two specified values. So it is not compressed between 0 and 100 like RSI and %B etc. Therefore, conditions such as "A condition if ATR value is X, B condition if ATR value is Y" cannot be created. In order to create these conditions, the max and min value range of the ATR value must be determined. This indicator converts the ATR values into a percentage number according to the maximum and minimum ATR values in the period you will choose. Max value is 100, min value is 0. The considered ATR value, on the other hand, corresponds to the % of the difference between the max and min value in the selected period.

In this way, conditions such as "If the ATR Oscillator value is greater than 10 or 20 or 30" can now be created, or the value of another indicator can be calculated based on the ATR Oscillator value. For example; Let's say we want the standard deviation of BBand to change according to the value of the ATR Oscillator. If BBand Standard Deviation is 3 if ATRO value is 100, BBand Standard Deviation is 2 if ATRO value is 0, and BBand Standard Deviation is 2.5 when ATRO value is 50;

We can encode it as BBand_Std_Dev=((ATRO*0.01)+2 )

If the ATRO value is between .... and ...., you can make improvements such as plot color X.

Volume Crop ━ Hidden Volume Divergence [whvntr] Volume Divergence

• Formula originated from: "Hidden Price Divergence" (circles) by TheLark. I did two things to harness its

effectiveness:

• Firstly, I developed a unique way to filter out the divergence signals that were appearing on both sides of the

midline. This filter will be known as the "Midline Tool" . It filters out a lot of the false signals commonly

associated with oscillators.

• Then, I modified the default format from Price to Volume.

• The midline formula "Midline Tool" was developed by me . It adjusts in the thousands since it's volume.

Let me know in the comments if you would rater have a smaller step value than 10,000. How does it work?

Crossover then Crossunder, the arrows only appear during the first sign of hidden volume divergence once

crossing the midline. Normally, these signs appear on both side of the midline both bearish and bullish no

matter if it's on an oversold or overbought side of the spectrum... Also, let

me know in the comments if you would like for me to release an oscillator version of this

indicator for co-witnessing.

Features:

• Volume divergence

• Midline Tool©

• Disclaimer: This indicator does not constitute investment advice. Trade at your own risk with the investments

you can afford to lose because all financial investments have risks and this is not a

guarantee that the volume divergence will be 100% all the time.

[LazyBear] SQZ Momentum + 1st Gray Cross Signals ━ whvntrI have modified LazyBears Squeeze Momentum Indicator with enhancements, plus added signals

LazyBear mentioned that in John F. Carter's book, Chapter 11, "Mastering the Trade", that "Mr. Carter suggests waiting till the first gray after a black cross, and taking a position in the direction of the momentum (for ex., if momentum value is above zero, go long). Exit the position when the momentum changes (increase or decrease --- signified by a color change)." I have done just that. Now at each "first gray after a black cross", there are now Bearish and Bullish signals.. The signals only appear in the direction of the momentum.

Disclaimer: This indicator does not constitute investment advice. Trade at your own

risk with this method of identifying changes in stock market momentum.

DRM StrategyOne of the ways I go when I develop strategies is by reducing the number of parameters and removing fixed parameters and levels.

In this strategy, I'm trying to create an RSI indicator with a dynamic length.

Length is computed based on the correlation between Price and its momentum.

You can set min and max values for the RSI, and if the correlation is close to 1, we'll be at a min RSI value. When it's -1, we'll be at the max level.

I got this idea from Sofien Kaabar's book.

The strategy is super simple, and there might be much room for improvement.

Performance on the deep backtesting is not excellent, so I think the strategy needs some filters for regimes, etc.

Thanks to @MUQWISHI for helping me code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Price Filter [AstrideUnicorn]The indicator calculates a fast price filter based on the closing price of the underlying asset. Overall, it is intended to provide a fast, reliable way to detect trend direction and confirm trend strength, using statistical measures of price movements.

The algorithm was adapted from Marcus Schmidberger's (2018) article "High Frequency Trading with the MSCI World ETF". It demeans the price time series using the long-term average and then normalizes it with the long-term standard deviation. The resulting time series is then compared to specified thresholds to determine the trend direction.

HOW TO USE

The indicator surface is colored green if the price is trending upwards and red if the price is trending downwards. If the indicator outline is the opposite color of the indicator surface, it indicates that the price is moving against the trend and the current trend may be losing strength.

If the 'Use threshold' setting is enabled, the indicator will be colored blue if its value is within the range defined by the upper and lower thresholds. This indicates that the price is trending sideways, or that the current trend is losing strength.

SETTNGS

Length - the length of the long-term average used to calculate the price filter. Recommended range 20 - 200. The sensitivity of the indicator increases as the value becomes smaller, allowing it to detect smaller price moves and swings earlier.

Threshold - the threshold value used to detect trend direction.

Use threshold - a boolean (true/false) input that determines whether to use the threshold value for confirmation.

Percent Volatility MomentumThis pine script calculates percent volatility momentum, negative percent volatility and positive percent volatility. The blue line is the overall momentum of the current percent volatility trend. The red line only includes negative movements in the percent volatility of the source. The green line includes only positive movements of the percent volatility of the source. The script also includes an angle and a normalized angle setting that allows one to determine the angle of the source curve. Note, the angle was transformed from -90 to 90 to 0 to 100. Such that an angle of -90 is transformed to 0. An angle of 0 is transformed to 50 and an angle of 90 is transformed to 100. This is the first draft of this script and my first pine script published. Any feedback is welcome. I borrowed code from TradingView's Linear Regression Channel and Relative Strength Index pine scripts.

NSDT Double MA ShadingThis script is an interesting take on Convergence and Divergence of Moving Averages. With the built-in MACD Indicator, you cannot make these adjustments to the settings.

DESCRIPTION

The top Moving Average is calculated on the High of the candle.

The bottom Move Average is calculated on the Low of the candle.

If the two are moving apart (Divergence), the shaded area between them turns Green.

If the two are moving together (Convergence), the shaded area between them turns Red.

This may help identify when a trend is becoming stronger or weaker, based on the shaded area and Moving Average direction.

POSSIBLE USAGE

For example:

If the MA's are pointing downward and the shaded area is Green - it means that average distance between the candle High and Low is getting wider, which may indicate a stronger downward movement. Then, when the shaded area turns Red, signaling the average distance between the candle High and Low are getting narrower, this may indicate that the downward movement is weakening, and may be the end of that downward trend.

SETTINGS

You can choose from EMA, SMA, WMA, RMA, HMA, TMA, and VWMA.

Although you can choose the MA Source, it is highly recommended to keep one source on the High of the candle and the other on the Low of the candle, for measure Convergence and Divergence.

All indicator settings are editable.

It can be used on Multi Timeframes (MTF).

This script is free and open source.

MAGIC MACDMAGIC MACD ( MACD Indicator with Trend Filter and EMA Crossover confirmation and Momentum). This MACD uses Default Trading view MACD

from Technical indicators library and adding a second MACD along with 3 EMA's to detect Trend and confirm MACD Signal.

Eliminates usage of 3different indicators (Default MACD , MACD-2,EMA5, EMA20, EMA50)

Basic IDEA.

Idea is to filter Histogram when price is above or below 50EMA. Similar to QQE -mod oscillator but Has a EMA Filter

1.Take DEFAULT MACD crossover signals with lower period

2.check with a Higher MACD Histogram.

3.Enter upon EMA crossover signal and Histogram confirmation.

Histogram changes to GRAY when price is below EMA 50 or above EMA 50 (Follows Trend)

4.Exit on next Default MACD crossover signal.

Overview :

Moving Average Convergence Divergence Indicator Popularly Known as MACD is widely used. MACD Usually generates a lots of False signals

and noise in Lower Time Frames, making it difficult to enter a trade in sideways market. Divergence is a major issue along with sideways

movement and tangling of MACD and Signal Lines. There is no way to confirm a Default MACD signal, except to switch time frames and

verify.

Magic MACD Can be used to in combination with other signals.

This MACD uses two MACD Signals to verify the signal given by Default MACD . The Histogram Plot shown is of a higher period

MACD (close,5,50,30) values. When a signal is generated on a lower MACD it is verified by the histogram with higher time period.

Technicals Used:

1. Lower MACD-1 values 12,26 and signal-9 (crossover Signals)

2. Higher MACD-2 values 5,50 and signal-30 (Histogram)

3. EMA 50 (Histogram Filter to allow only if price above or below Ema 50)

4. EMA 5 and EMA 20 for crossover confirmation of trend

What's is in this Indicator?

1.Histogram-(higher period 5,50 and 30signal)

2. MACD crossover Signals-(lower period Default MACD setting)

3.Signal Lines-( EMA 5 & 20)

Implemented & Removed in this Indicator

1. Default MACD and Signal Lines are removed completely

2. MACD crossover are taken on lower periods and plotted as signals(Blue Triangle or Red Triangle)

3. Histogram is plotted from a higher Period providing a clear picture with Higher Time period

4. EMA 5 and EMA 20 are used for MACD signal confirmation

How to use?

Up Signal

1. MACD Default (12,26,30) up signals are shown in Blue

2. Wait till the Histogram changes Blue

3. Look for EMA signals crossover near by

Down Signal

1. MACD Default (12,26,30) up signals are shown in Red

2. Wait till the Histogram changes Red

3. Look for EMA signals crossover near by

Do's

Consider only opposite color as signals

1. Red Triangle on Blue Histogram(likely to move down direction)

2. Blue Triangle on Red Histogram (Likely to move up direction)

Don'ts

1.Ignore Blue Signal on Blue Histogram (pull back signals can be used to enter trade if you miss first crossover)

2.Ignore Red Signal on Red Histogram(pull back signals can be used to enter trade if you miss first crossover)

3.Ignore Up and Down signals till Gray or Blacked out area is finished in Histogram

Tips:

1. EMA plot also shows pull back areas along with signals

2.side by side opposite signals shows sides ways movement

3. EMA 5,20 is plotted on MACD Histogram for Additional Benefit

Thanks & Credits

To Tradingview Team for allowing me to use their default MACD version and coding it in to a MAGIC MACD by adding a few lines of code that

makes it more enhanced.

Warning...!

This is purely for Educational purpose only. Not to be used as a stand alone indicator. Usage is at your own Risk. Please get familiar with its working before implementing. Its not a Financial Advice or Suggestion . Any losses or gains is at your own risk.

Quantum CDV HistogramThis script is an addition to Fixed Quantum Cdv.

It shows vector cdv ratio in columns.

You can select the length as an input to how many bars to look back for the whole calculation.

The green bars represent the bullish values and the red bars the bearish values.

The green line represents an ema of the bullish value and the red line the ema of the bearish value.

The momentum ema (in purple) represent the cdv ratio (bullish - bearish).

When the momentum ema is at 100% or more it’s a good sell opportunity and when the momentum ema is at or under 100% it’s a good buy opportunity. It is not financial advise. Make sure to make your own analysis. This script help to make entries, but do not enter positions only based on this signal.

In the inputs you can select the emas that you want to display on your histogram.

The original script is the Cumulative Delta Volume by LonesomeTheBlue.

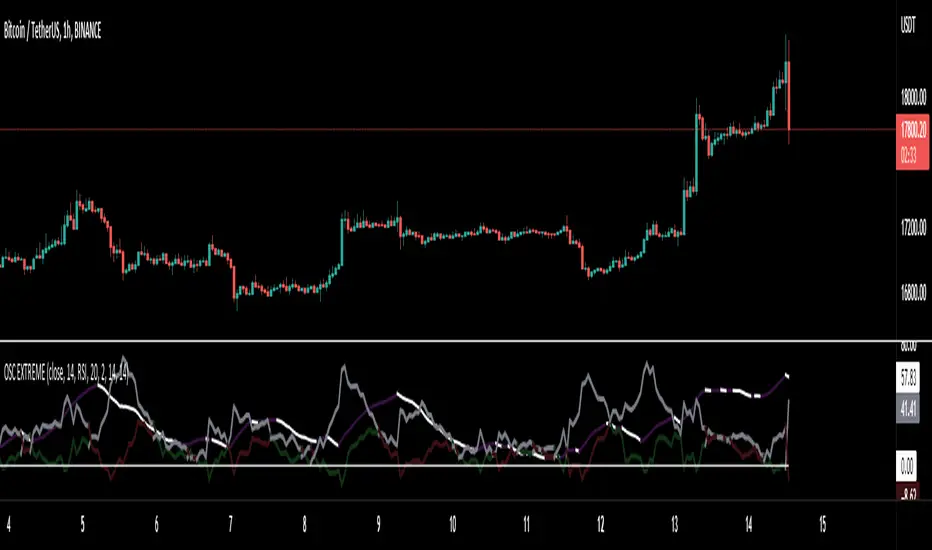

Oscillator ExtremesThe Oscillator Extremes indicator plots the normalized positioning of the selected oscillator versus the Bollinger Bands' upper and lower boundaries. Currently, this indicator has four different oscillators to choose from; RSI, CMO, CCI, and ROC.

When the oscillator pushes towards one extreme, it will bring the value of the prevailing line closer to zero. If the bullish or bearish line crosses the zero line, the oscillator is past the extreme of the Bollinger Band.

Example: If the RSI crosses over the upper boundary of the Bollinger, the bullish(green) line will cross under the zero line.

Crossovers of the bullish and bearish lines can indicate a shift in momentum and are a signal. Where the line crossing under, towards zero, is the prevailing trend. The plotted lines will highlight green(bullish) or red(bearish) to show the prevailing trend. This is similar to a DI+- crossover that is commonly associated with the ADX.

We have included an optional normalized ADX to help validate signals. The ADX will change color based on the slope of the ADX. Purple indicates a positive slope and white for a negative slope.

[EDU] RSI Momentum BandsRSI Momentum Bands serve a purpose to find best RSI momentum for entering a trade.

Indicator is built simply:

1st RSI MA is smoothed RSI by little period, 2nd RSI MA is smoothed RSI by a bigger period.

Then we calculate standard deviation from the 2nd MA and make upper and lower band.

The rules for trades are simple:

When RSI is above higher band - Buy ;

When RSI is below lower band - Sell .

The indicator is for educational purposes only to present trades a momentum bands concepts, widely used across professionals.

Hope you will find it helpful.

Take your profits!

- Tarasenko Fyodor

Fast EMA above Slow EMA with MACD (by Coinrule)An exponential moving average ( EMA ) is a type of moving average (MA) that places a greater weight and significance on the most recent data points. The exponential moving average is also referred to as the exponentially weighted moving average . An exponentially weighted moving average reacts more significantly to recent price changes than a simple moving average simple moving average ( SMA ), which applies an equal weight to all observations in the period.

Moving average convergence divergence ( MACD ) is a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price. The MACD is calculated by subtracting the 26-period exponential moving average ( EMA ) from the 12-period EMA .

The result of that calculation is the MACD line. A nine-day EMA of the MACD called the "signal line," is then plotted on top of the MACD line, which can function as a trigger for buy and sell signals. Traders may buy the coin when the MACD crosses above its signal line and sell—or short—the security when the MACD crosses below the signal line. Moving average convergence divergence ( MACD ) indicators can be interpreted in several ways, but the more common methods are crossovers, divergences, and rapid rises/falls.

The Strategy enters and closes the trade when the following conditions are met:

LONG

The MACD histogram turns bullish

EMA8 is greater than EMA26

EXIT

Price increases 3% trailing

Price decreases 1% trailing

This strategy is back-tested from 1 January 2022 to simulate how the strategy would work in a bear market and provides good returns.

Pairs that produce very strong results include AXSUSDT on the 5-minute timeframe. This short timeframe means that this strategy opens and closes trades regularly.

Additionally, the trailing stop loss and take profit conditions can also be changed to match your needs.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

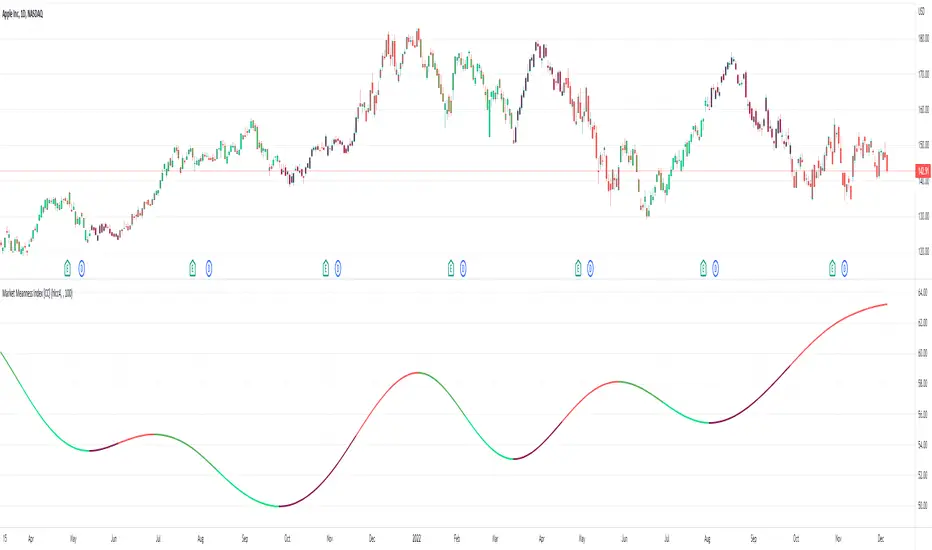

Market Meanness Index [CC]The Market Meanness Index was created by Johann Christian Lotter and I added some smoothing of my own, so feel free to try it without any smoothing to see the differences. This indicator relies on the mean reversion theory that all prices will eventually revert to the mean over a long period of time. Obviously there is more to the theory but the basic idea is if you plot a sma or other typical moving average, you will see the price moving up or below the long term moving average such as a 200 day sma but usually heads back to the average in the short term. This is a good statistical analysis used for volatility which is where this indicator comes in. Simply put, we calculate volatility based on how often a price is both above the median and above the previous price or vice versa.

A rising Market Meanness Index means that the market is becoming more volatile and that there is a high likelihood of a change in the underlying trend. A falling Market Meanness Index means that the current trend is dying and there is a high likelihood of a trend reversal. Typically I put general buy and sell signals in red or green but in this particular case, this indicator works best as a overall trend filter and you would want to place a trade when this indicator has a peak or valley. Let me know if you find a good overall buy and sell signal system of course.

I know I keep saying that I will get active again and post more indicators but life is very hectic for me. For those who have been following my updates, my twins were finally born a little over a month ago and as you can imagine, they keep me up at all hours of the day so it is hard to create new indicator scripts when I'm getting no sleep lol. I will do my best to start publishing the giant backlog of scripts I have created but in the meantime, please be patient with me. This indicator was a special request so let me know if you have any special requests of your own!

Smart Disparity IndexThe Smart Disparity Index (SDI) is an optimized version of the Disparity Index indicator invented by Steve Nison (book "Beyond Candlesticks").

According to Steve Nison, "The disparity index (or disparity ratio), compares, as a percentage, the latest close to a chosen moving average", which means that the indicator gives the difference in % between the closing price and a simple moving average.

The calculation formula is therefore as follows:

Disparity Index = 100 x (closing_price - simple_moving_average) / simple_moving_average

In order to optimize the calculation, I replaced the closing price with the 6-period exponential moving average (EMA6) which, according to many years of experience, allows prices to be smoothed by eliminating excesses.

Formula for calculating the Smart Disparity Index:

SDI = 100 x (EMA6 - simple_moving_average) / simple_moving_average

The provided script displays the SDI for the 20, 50, 100 and 200 periods.

From my point of view, I recommend using the SDI50 as a priority:

SDI50 = 100 x (EMA6 - SMA50) / SMA50

In the chart, we can see the SDI50 (in purple) is on a long-term support (in green), this indicates a probability of a Bitcoin rise in the coming months.

The SDI can also be used as a momentum type indicator.

Ichimoku Cloud with MACD and Trailing Stop Loss (by Coinrule)The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. It does this by taking multiple averages and plotting them on a chart. It also uses these figures to compute a “cloud” that attempts to forecast where the price may find support or resistance in the future.

The Ichimoku Cloud was developed by Goichi Hosoda, a Japanese journalist, and published in the late 1960s. It provides more data points than the standard candlestick chart. While it seems complicated at first glance, those familiar with how to read the charts often find it easy to understand with well-defined trading signals.

The Ichimoku Cloud is composed of five lines or calculations, two of which comprise a cloud where the difference between the two lines is shaded in.

The lines include a nine-period average, a 26-period average, an average of those two averages, a 52-period average, and a lagging closing price line.

The cloud is a key part of the indicator. When the price is below the cloud, the trend is down. When the price is above the cloud, the trend is up.

The above trend signals are strengthened if the cloud is moving in the same direction as the price. For example, during an uptrend, the top of the cloud is moving up, or during a downtrend, the bottom of the cloud is moving down.

The MACD is a trend following momentum indicator and provides identification of short-term trend direction. In this variation it utilises the 12-period as the fast and 26-period as the slow length EMAs, with signal smoothing set at 9.

This strategy combines the Ichimoku Cloud with the MACD indicator to better enter trades.

Long/Exit orders are placed when three basic signals are triggered.

Long Position:

Tenkan-Sen is above the Kijun-Sen

Chikou-Span is above the close of 26 bars ago

Close is above the Kumo Cloud

MACD line crosses over the signal line

Exit Position:

Price increases 3% trailing

Price decreases 3% trailing

The script is backtested from 1 June 2022 and provides good returns.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

BTC Indicator By Megalodon TradingThis indicator is designed help you see the potential reversal zones and it helps you accumulate for the long run.

This combines price data on any chart. The chart isolates between 0 and -100. Below -80 is a buy, above -20 is a sell location.

In these locations, try to Slowly Buy and Slowly Sell (accumulate...)

Story Of This Indicator

~I was always obsessed with Fibonacci and used Fibonacci all the time. Thus, i wanted to make a tool to see buying locations and selling locations.

Instead of drawing fibonacci's and manually interpreting buy/sell locations, i wanted algorithms to do the job for me. So, i created this algorithm and many more like it.

If you think i did a good job and want to do further work with me, feel free to contact.

I have a ton of other tools that can change everything for your trading/investing.

Best wishes

~Megalodon

RSI Objective LinesThe RSI is a contrarian indicator bounded between 0 and 100 where values close to the area of 30 represent an oversold condition and values close to the area of 70 represent an overbought condition.

Generally, we use the area of 70/75 and the area of 30/25 as extremes that signal a market reversal or a correction. But what if we calculate a simple way to make these levels more dynamic?

The main idea from these objective support and resistance levels is that market regime and dynamics move and as such fixed levels are unlikely to always provide value which means that we can try creating variable levels. The objective support and resistance levels are created following these steps:

* Calculate a 14-period RSI on the close price, let's call this RSI_Close.

* Calculate a 14-period RSI on the high price, let's call this RSI_High.

* Calculate a 14-period RSI on the low price, let's call this RSI_Low.

* Calculate the maximum range which is the highest value of RSI_High in the last 200 periods minus the lowest value of RSI_Low in the last 200 periods. Let's call this Max_Range

* Define the range width. By default, it is set to 5%. Let's call this Threshold.

* The objective support is calculated as the sum of the RSI_Low + (Max_Range * Threshold).

* The objective resistance is calculated as the sum of the RSI_High - (Max_Range * Threshold).

The levels are used in the same way as the oversold and overbought levels. They are more dynamic as they take into account the fluctuations of the RSI so you might see at some point in time a support at 20 and at another at 35.

Adaptive Fisherized CMOIntroduction

Heyo, here is another no-repaint adaptive fisherized indicator.

I added Inverse Fisher Transform, Ehlers dominant cycle analysis and smoothing to the Chande Momentum Oscillator (CMO).

Usage

The CMO is a momentum oscillator which shows the usual movement of an asset.

I recommend to use it from a lower timeframe with a higher timeframe set.

Signals

(Signal mode will come soon.)

Zero Line

CMO crosses above zero line => enter long

CMO cross below zero line => ente short

Overbought/Oversold

CMO crosses above bottom band => enter long

CMO crosses under top band => enter short

MA (Maybe this signals will vary. Then, check update notes.)

CMO crosses above MA => enter long

CMO crosses below MA => enter short

Enjoy and share your experience with it!

More to read: CMO Explanationsp

Rob Booker Reversal Tabs StrategyRob Booker Reversal Tabs Strategy is an updated version of Rob Bookers Reversal Tab study: Rob Booker Reversal Tabs

While the original is a Pinescript study, this version can be switched between strategy and indicator mode.

Rob Bookers script generates reversal signal based on MACD and Stochastics, it is not a true reversal system, default pyramiding value is set to 5.

Inputs determine MACD and Stochastics settings. The only additional input is the "Strategy Mode" checkbox.

This script works well on its own for some tickers, but like any reversal pattern generating scripts, traders will profit from looking at overall price action and trend strength before making a trade.

From the original:

A simple reversal pattern indicator that uses MACD and Stochastics.

Created by Rob Booker and programmed by Andrew Palladino.

Please note that I only updated the original to V5 and edited it to be a strategy, which was a grand total of 5 minutes of work. I updated it because I wanted to see how the script performs as a strategy and I'm publishing it in case others would like to use it. I take no credit whatsoever for the original and WILL take this version down if Rob Booker or his Team ask me to or decide to release their own strategy version of the original.

Check out Rob Bookers scripts and ideas on his Tradingview account: robbooker