Basic Polychromatic Momentum IndicatorBasic Polychromatic Momentum Indicator with alerts

PMI involves taking the difference between the current price and the price n periods ago, and then subtracting from it the difference between the current price and the price n periods ago, divided by n. This gives a smoothed version of the momentum indicator.

The user can also specify a smoothing factor using the "smoothing" input, which applies a simple moving average to the PMI. The resulting smoothed PMI is plotted on the chart in blue, with a dotted gray line at the zero level.

Центральные осцилляторы

Polychromatic Momentum IndicatorPolychromatic Momentum is a generalized Momentum study considering a number of Momentum values controlled by the length input. The greatest weight is given to the most recent Momentum value, while the precedent values are given lesser weight. Each Momentum value is assigned weight equal to inverse square root of Momentum distance (number of bars prior to the current bar). Then the sum of the weighted Momentum values is divided by the sum of the square roots.

RSI-ROC Momentum AlertThis is the RSI-ROC Momentum Alert trading indicator, designed to help traders identify potential buy and sell signals based on the momentum of price movements.

The indicator is based on two technical indicators: the Rate of Change (ROC) and the Relative Strength Index (RSI). The ROC measures the speed of price changes over a given period, while the RSI measures the strength of price movements. By combining these two indicators, this trading indicator aims to provide a comprehensive view of the market momentum.

An RSI below its oversold level, which shows as a green background, in addition to a ROC crossing above its moving average (turns green) signals a buying opportunity.

An RSI above its overbought level, which shows as a red background, in addition to a ROC crossing below its moving average (turns red) signals a selling opportunity.

Traders can use this indicator to identify potential momentum shifts and adjust their trading strategies accordingly.

The ROC component of the indicator uses a user-defined length parameter to calculate the ROC and a simple moving average (SMA) of the ROC. The color of the ROC line changes to green when it is above the ROC SMA and to red when it is below the ROC SMA. The ROC SMA color changes whether it's above or below a value of 0.

The RSI component of the indicator uses a user-defined length parameter to calculate the RSI, and user-defined RSI Low and RSI High values to identify potential buy and sell signals. When the RSI falls below the RSI Low value, a green background color is applied to the chart to indicate a potential buy signal. Conversely, when the RSI rises above the RSI High value, a red background color is applied to the chart to indicate a potential sell signal.

This indicator is intended to be used on any time frame and any asset, and can be customized at will.

Moonhub Cycle IndexMoonhub Cycle Index is a composite index derived from three popular technical analysis indicators: Moving Average Convergence Divergence (MACD), Schaff Trend Cycle (STC), and Detrended Price Oscillator (DPO). The indicator is designed to help identify potential trends and market sentiment by combining the unique characteristics of each indicator.

Key components of the indicator include:

Input Parameters:

COEMA Length (len_DIema): The length of the Exponential Moving Average (EMA) applied to the Custom Index. Default is set to 9.

COSMA Length (len_DIsma): The length of the Simple Moving Average (SMA) applied to the Custom Index. Default is set to 30.

Indicators:

MACD: A momentum oscillator that shows the relationship between two moving averages of a security's price. It is calculated using the difference between the 12-period and 26-period EMA, and a 9-period EMA (signal line) of the MACD.

STC: A cyclic indicator that identifies cyclical trends in the market. It is calculated using the Stochastic oscillator formula applied to the close, high, and low prices over a 10-period lookback window.

DPO: A price oscillator that eliminates the trend from price data to focus on underlying cycles. It is calculated using a custom function that shifts the price by half the length and subtracts the SMA from the shifted price.

Custom Index: The composite index is calculated by taking the average of the MACD line, STC, and DPO.

COEMA and COSMA: Exponential and Simple Moving Averages applied to the Custom Index using the lengths specified by the input parameters (len_DIema and len_DIsma).

Plots: The Custom Index, COEMA, and COSMA are plotted with different colors and line widths to visualize their interaction and provide insights into potential market trends.

This Custom Index Indicator can be useful for traders who want to analyze the market using a combination of these indicators to make more informed decisions. It can also help identify potential trends and market sentiment by combining the unique characteristics of each indicator.

SAR MACDSAR MACD is an idea of implementing Directional MACD with Parabolic SAR to exactly detect and confirm Trend. This p-SAR MACD consist of a HYBRID MACD which acts as MACD TREND oscillator, MACD Oscillator, PSAR Indicator combined with MA line. thus Fake MACD Signals can be eliminated using this SAR MACD. Sideways can be detected using Threshold Levels must be adjusted based on timeframe.

Indicators Hybrid model contains:

1.MACD (12,26,9) Standard with MA Crossovers

2.MACD Trend

3.Parabolic SAR with 0.02

4.Threshold level - indicates Sideways

How to use.

Histogram:

-> HIST MODE: normal MACD indicator

MA Line Color is based on PSAR Direction Blue-Up/ Pink -Down

A crossover upside with a Blue MA line denotes Up confirmation

A Crossover downwards with a red MA line denotes Down Confirmation

Additionally Histogram above zero line and below zero line are to be confirmed

-> MACD MODE: MACD Trend indicator

MA Line Color is based on PSAR Direction Blue-Up/ Pink -Down

A crossover upside with a Blue MA line denotes Up confirmation

A Crossover downwards with a red MA line denotes Down Confirmation

Additionally Histogram above zero line and below zero denotes long term Trend

-> Histogram Color: Indicates candles direction

Yellow indicates Unconfirmed Direction

Green Indicates up direction

Red Indicates Down Direction

Buy Condition:

MA Color - Blue

Histogram- Above Zero

Histogram/Candle -Green

MA Crossover is must

Sell Condition:

MA Color - Red

Histogram- Below Zero

Histogram/Candle -Red

MA Cross under is must

Warning: Must not be used as a standalone indicator. Use for confirmation of your Buy Sell Signals and Entry only.

KST-Based MACDAs a follow-up to my previous script:

I am posting a stand-alone KST-based MACD.

Note that this indicator is highly laggy. Specific care must be taken when using it.

The MACD-Signal crossing is quite delayed but it is a definite confirmation.

For earlier signs, the Histogram must be analyzed. A shift from Green-White signals the 1st Bear Signal.

A MACD-Signal crossing signals the 2nd Bear SIgnal.

The same applies for bull-signs.

This indicator is useful for long-term charts on which one might want to pinpoint clear, longterm divergences.

Standard RSI, Stochastic RSI and MACD are notoriously problematic when trying to pinpoint long-term divergences.

Finally, this indicator is not meant for pinpointing entry-exit positions. I find it useful for macro analysis. In my experience, the decreased sensitivity of this indicator can show very strong signs, that can be quite laggy.

Inside the indicator there is a setting for "exotic calculations". This is an attempt to make this chart work in both linear/ negative charts (T10Y2Y) and log charts (SPX)

Tread lightly, for this is hallowed ground.

-Father Grigori

KST con HMA---------- ENGLISH DESCRIPTION ----------

The indicator created is called "KST with HMA" and is used to measure the impulse of an asset's price.

The code begins by defining four variables representing ROC (Rate of Change) period lengths for calculating the KST (Know Sure Thing) and a variable for the length of the HMA (Hull Moving Average).

Next, an HMA function is defined to calculate the Hull Moving Average, a type of weighted moving average that adjusts for price volatility.

ROC values are then calculated for the four periods defined above and KST values are calculated as a weighted sum of the ROC values. These values are then normalized with the HMA and the standard deviation of the HMA is calculated. The normalized value is finally plotted with three different color lines: black for values greater than 1, red for values less than -1, and green for values between -1 and 1.

Finally, a black dashed line is plotted to represent the zero line. The green line indicates a phase of market uncertainty or lateralization, while the indicator can be used to identify buy points above zero and sell points below zero.

---------- ITALIAN DESCRIPTION ----------

L'indicatore creato è chiamato "KST con HMA" e viene utilizzato per misurare l'impulso del prezzo di un asset.

Il codice inizia definendo quattro variabili che rappresentano le lunghezze dei periodi di ROC (Rate of Change) per il calcolo del KST (Know Sure Thing) e una variabile per la lunghezza dell'HMA (Hull Moving Average).

Successivamente viene definita una funzione HMA per il calcolo della Hull Moving Average, un tipo di media mobile ponderata che si adatta alla volatilità del prezzo.

Vengono poi calcolati i valori ROC per i quattro periodi definiti in precedenza e calcolati i valori KST come somma ponderata dei valori ROC. Questi valori vengono poi normalizzati con l'HMA e viene calcolata la deviazione standard dell'HMA. Il valore normalizzato viene infine plottato con tre diverse linee di colore: nero per valori superiori a 1, rosso per valori inferiori a -1 e verde per valori tra -1 e 1.

Infine, viene plottata una linea tratteggiata nera per rappresentare la linea zero. La linea verde indica una fase di incertezza o lateralizzazione del mercato, mentre l'indicatore può essere utilizzato per individuare punti di acquisto sopra lo zero e di vendita al di sotto dello zero.

Bar Color Long / Short Indicator With Advised SLOverview

This script is a trading indicator named "Bar Color Long / Short Indicator With Advised SL" designed for the TradingView platform. The indicator's primary purpose is to provide entry signals for long and short positions, based on various technical analysis methods. Additionally, the indicator suggests stop-loss levels for both long and short positions.

User Inputs

The indicator has several user inputs, such as:

Length

Smoothing

Multiplier

Show bar colors (ON/OFF)

When the bar colors are turned off, the alert signals for long and short positions will be displayed instead.

Custom Risk Calculation

The script calculates a custom risk level based on a modified version of the RSI (Relative Strength Index) formula. The custom risk level is divided into three categories: low, medium, and high.

Sentiment Score Calculation

The indicator calculates a sentiment score based on a combination of methods resembling EMA (Exponential Moving Average), MACD (Moving Average Convergence Divergence), and ROC (Rate of Change). The sentiment score is used to determine if the sentiment is positive or negative.

Bollinger Bands Percent and Combined Signal

The Bollinger Bands Percent is calculated, and the custom risk, sentiment score, and Bollinger Bands Percent are combined to generate a new signal. This signal is used in conjunction with EMA10 to determine the bar colors and provide entry signals.

Bar Colors

Based on the combined signal and EMA10, the script determines the bar colors as follows:

Orange: Positive sentiment

Blue: Negative sentiment

Gray: Neutral

Entry Signals and Alerts

When the bar colors are turned off, the indicator displays large green arrow signals for long (buy) positions and red arrow signals for short (sell) positions based on the sentiment and EMA10 conditions. The script also includes alert conditions for long and short signals, which can be used to set up notifications when these signals are triggered in the TradingView platform.

Advised Stop-Loss Levels

The indicator plots stop-loss lines for both long and short positions at the last candle, accompanied by labels showing the advised stop-loss levels in numeric values.

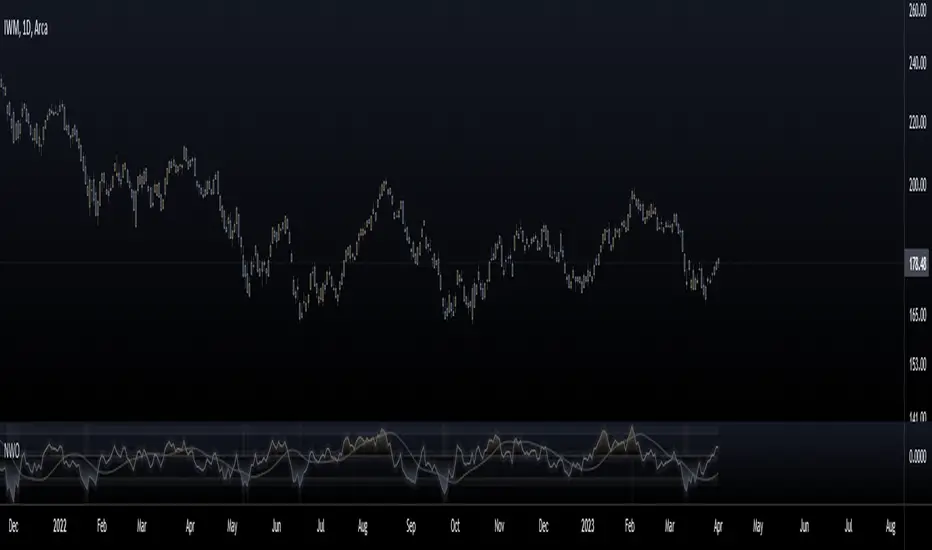

Nadaraya-Watson OscillatorThis indicator is based on the work of @jdehorty and his amazing Nadaraya-Watson Kernel Envelope, which you can see here:

General Description

The Nadaraya-Watson Oscillator (NWO) will give the same information as the Nadaraya-Watson Envelope, but as an oscillator off the main chart, by plotting the relationship between price and the Kernel and its bands. This also means that we can now detect divergences between price and the NWO.

You can see the relationship between the two here:

You can think of this indicator as the kernel envelope version of a Bollinger Band %B. In ranging markets the bands are perfect for mean reversion trades, but in certain situations the break of one of the bands can signal the beggining of a strong trend and price will remain close to the bands for a long period and will only give small pullbacks. As with any indicator, confluence with price and other tools must be taken into account.

Main Features

As with @jdehorty 's Envelope, you can change the following settings:

Lookback Window.

Relative Weighting.

The initial bar for the regression.

ATR period for the bands.

Inner and Outer Multiples for the bands.

I also added the following:

A middle band around the Kernel to filter out false crossovers.

A Hull Moving Average to smoothen out the movements of the oscillator and give extra confirmation of turnover points.

Colors

Some special things to note regarding the coloring:

The zero line features a gradient that changes color every time the Kernel slope changes direction.

The Oscillator plot has a gradient coloring that gets stronger the closer it gets to each of the bands.

Every time the oscillator crosses over/under the outer bands the background will be highlighted.

Happy trading!

Degen Dominator - (Crypto Dominance Tool) - [mutantdog]A fairly simple one this time. Another crypto dominance tool, consider it a sequel to Dominion if you will. Ready to go out-of-the-box with a selection of presets at hand.

The premise is straightforward, rather than viewing the various marketcap dominance indexes as their standard percentage values, here we have them represented as basic oscillators. This allows for multiple indexes to be viewed in one pane and gives a decent overview of their relative changes and thus the flow of capital within the overall crypto market. As a general rule-of-thumb, when a plot is above zero then the dominance is climbing, thus capital is likely flowing in that direction. The inverse applies when below zero. When the market is quiet, all will be close to zero. Basic overbought/oversold conditions can also be inferred too.

Active as default are:

Bitcoin (0range): CRYPTOCAP:BTC.D

Ethereum (Blue): CRYPTOCAP:ETH.D

Stablecoins (Red): CRYPTOCAP:USDT.D + CRYPTOCAP:USDC.D

Altcoins (Green): 100 - (all of the above)

These are plotted according to the selected oscillator preset and it's length parameter. The default is set to 'EMA Centre'. An optional RMA(3) smoothing filter is also included and active as default. Each index plot has its own colour and opacity settings available on the main page.

Additionally, the following are also available (deactivated as default):

Total DeFi : CRYPTOCAP:TOTALDEFI.D

Current Symbol : Will try to match corresponding dominance index for the chart symbol if available.

Custom Input : Manual text input, will try to match if available.

-------------

The included presets determine the oscillator type used, all are fairly simple and easy to interpret:

EMA Centre

SMA Centre

Median Centre

Midrange Centre

The first 4 are all variations on the same theme, simply calculated as the difference between the actual value and its respective average. EMA is the default and is my personal preference, if you generally favour using an SMA then perhaps that would be your better choice. Like the two MAs, median and midrange are also dependant on the length parameter. Midrange is calculated from the difference between highest and lowest values within the length period, with a little extra smoothing from an RMA(3).

Simple Delta

Weighted Delta

Running Delta

Often referred to as momentum, delta is just change over time. 'Simple' is the most basic of these, the difference between the current value and the value (length) bars prior. A more long-winded way of calculating this would be to take the difference between each bar and its previous then average them with an SMA which results in the same value. 'Weighted' adopts that principle but instead uses a WMA, likewise 'Running' is the same but using an RMA. The latter is actually the basis of RSI calculations before any normalisation is applied, as you can see in the next preset.

RSI

CMO

RSI really should not need explaining, it is however applied a little differently here to the usual, in this case centred around 0. The x100 multiplication factor has been dropped too for the sake of consistency. The same principle applies with CMO, which is basically a 'Simple Delta' version of RSI.

Hard Floor

Soft Floor

These last two are a little different but both can provide useful interpretations. The floor here is simply the lowest value within the chosen length period. 'Hard' plots the difference between the current value and the floor, thus giving a value that is always above 0. In this case, focus should be given to the relative heights of each with a simple interpretation that capital is flowing into those that are climbing and out of those descending. 'Soft' is essentially the same except that the floor is smoothed with an RMA(3), the result being that when new lows are made, the plot will break below 0 before the floor corrects a few bars later. This soft break provides additional information to that given by 'Hard' so is probably the more useful of the two.

------------

To finish it off, a bunch of preset alerts are included for the various 0 crossings.

So that just about covers everything then, all quite straightforward really. Future updates may include some extra stuff, the composition of the stablecoin index may change if necessary too. While this is not really a tweaker's tool like some of my other projects, there's still some room for experimentation here. The 'current' and 'custom' indexes can provide some useful data for compatible altcoins and the possibility to compare inter-related tokens (eg: Doge vs Shib). While i introduced this as a sort of sequel to Dominion, it is not intended as a replacement but more of a companion. This initially started as a feature intended for that one but it quickly grew into its own thing. Both the oscillator view here and the more traditional view have merits, i personally use this one primarily now but frequently refer to Dominion for confirmations etc.

That's it for now anyway. As always, feedback is welcome below. Enjoy!

Momentum Ratio Oscillator [Loxx]What is Momentum Ratio Oscillator?

The theory behind this indicator involves utilizing a sequence of exponential moving average (EMA) calculations to achieve a smoother value of momentum ratio, which compares the current value to the previous one. Although this results in an outcome similar to that of some pre-existing indicators (such as volume zone or price zone oscillators), the use of EMA for smoothing is what sets it apart. EMA produces a smooth step-like output when values undergo sudden changes, whereas the mathematics used for those other indicators are completely distinct. This is a concept by the beloved Mladen of FX forums.

To utilize this version of the indicator, you have the option of using either levels, middle, or signal crosses for signals. The indicator is range bound from 0 to 1.

What is an EMA?

EMA stands for Exponential Moving Average, which is a type of moving average that is commonly used in technical analysis to smooth out price data and identify trends.

In a simple moving average (SMA), each data point is given equal weight when calculating the average. For example, if you are calculating the 10-day SMA, you would add up the prices for the past 10 days and divide by 10 to get the average. In contrast, in an EMA, more weight is given to recent prices, while older prices are given less weight.

The formula for calculating an EMA involves using a smoothing factor that is multiplied by the difference between the current price and the previous EMA value, and then adding this to the previous EMA value. The smoothing factor is typically calculated based on the length of the EMA being used. For example, a 10-day EMA might use a smoothing factor of 2/(10+1) or 0.1818.

The result of using an EMA is that the line produced is more responsive to recent price changes than a simple moving average. This makes it useful for identifying short-term trends and potential trend reversals. However, it can also be more volatile and prone to whipsaws, so it is often used in combination with other indicators to confirm signals.

Overall, the EMA is a widely used and versatile tool in technical analysis, and its effectiveness depends on the specific context in which it is applied.

What is Momentum?

In technical analysis, momentum refers to the rate of change of an asset's price over a certain period of time. It is often used to identify trends and potential trend reversals in financial markets.

Momentum is calculated by subtracting the closing price of an asset X days ago from its current closing price, where X is the number of days being used for the calculation. The result is the momentum value for that particular day. A positive momentum value suggests that prices are increasing, while a negative value indicates that prices are decreasing.

Traders use momentum in a variety of ways. One common approach is to look for divergences between the momentum indicator and the price of the asset being traded. For example, if an asset's price is trending upwards but its momentum is trending downwards, this could be a sign of a potential trend reversal.

Another popular strategy is to use momentum to identify overbought and oversold conditions in the market. When an asset's price has been rising rapidly and its momentum is high, it may be considered overbought and due for a correction. Conversely, when an asset's price has been falling rapidly and its momentum is low, it may be considered oversold and due for a bounce back up.

Momentum is also often used in conjunction with other technical indicators, such as moving averages or Bollinger Bands, to confirm signals and improve the accuracy of trading decisions.

Overall, momentum is a useful tool for traders and investors to analyze price movements and identify potential trading opportunities. However, like all technical indicators, it should be used in conjunction with other forms of analysis and with consideration of the broader market context.

Extras

Alerts

Signals

Loxx's Expanded Source Types, see here for details

Vorse4**Vorse4 Indicator**

The Vorse4 Indicator is a technical analysis tool that combines Chaikin Oscillator, Intraday Momentum Index (IMI), MACD, and Parabolic SAR indicators. This indicator generates trading signals when all four indicators simultaneously provide buy or sell signals and visually presents these signals on the chart.

**How to Use:**

1. Buy signal: A buy signal is generated when there is a positive crossover in the Chaikin Oscillator, the IMI is above 50, the MACD line crosses the signal line upwards, and the price is above the Parabolic SAR. It is marked with a green arrow below the chart.

2. Sell signal: A sell signal is generated when there is a negative crossover in the Chaikin Oscillator, the IMI is below 50, the MACD line crosses the signal line downwards, and the price is below the Parabolic SAR. It is marked with a red arrow above the chart.

3. Turning zones: Areas with a high probability of transitioning from buy to sell or sell to buy are marked in yellow. These zones are determined by monitoring turning points in the Chaikin Oscillator, MACD, and Intraday Momentum Index.

**How to Apply:**

1. In your TradingView chart, go to the indicators menu and search for the "Vorse4" indicator.

2. Add the indicator to your chart. You will see green and red arrows indicating buy and sell signals, as well as yellow-colored areas representing turning zones on your chart.

3. Observe the buy and sell signals and trade according to your strategy. Analyze the performance of the indicator on historical data to evaluate the reliability of the signals.

**Note:** You can adjust the indicator parameters to balance the frequency and accuracy of buy and sell signals. Each strategy has a different risk-reward balance, so you can try different values to find the one that works best for you.

Jdawg Sentiment Momentum Oscillator EnhancedThe Jdawg Sentiment Momentum Oscillator Enhanced (JSMO_E) is a versatile technical analysis indicator designed to provide traders with insights into potential trend changes and overbought or oversold market conditions. JSMO_E combines the principles of the Relative Strength Index (RSI), the Simple Moving Average (SMA), and the Rate of Change (ROC) to create a comprehensive tool for assessing market sentiment and momentum.

The uniqueness of JSMO_E lies in its ability to integrate the RSI, SMA of RSI, and ROC of RSI, while also allowing users to customize the weight of the ROC component. This combination of features is not commonly found in other indicators, which increases its distinctiveness.

To effectively use JSMO_E, follow these steps:

Apply the JSMO_E indicator to the price chart of the asset you are analyzing.

Observe the plotted JSMO_E line in relation to the zero line, overbought, and oversold levels.

When the JSMO_E line crosses above the zero line, it may signal the beginning of an uptrend or bullish momentum. Conversely, when the JSMO_E line crosses below the zero line, it may indicate the start of a downtrend or bearish momentum.

Overbought and oversold levels, marked by the red and green dashed lines, respectively, can serve as a warning that a trend reversal may be imminent. When the JSMO_E line reaches or surpasses the overbought level, it might indicate that the asset is overvalued and could experience a price decline. Conversely, when the JSMO_E line reaches or goes below the oversold level, it can signal that the asset is undervalued and may experience a price increase.

Adjust the input parameters (RSI Period, SMA Period, ROC Period, and ROC Weight) as needed to optimize the indicator for the specific market and time frame you are analyzing.

The JSMO_E indicator is suitable for various markets, including stocks, forex, commodities, and cryptocurrencies. However, its effectiveness may vary depending on the market conditions and time frames used. It is recommended to use JSMO_E in conjunction with other technical analysis tools and methods to confirm potential trade setups and improve overall trading performance. Always conduct thorough backtesting and forward-testing before employing any indicator in a live trading environment.

CoffeeShopCrypto 3pl MAThe CoffeeShopCrypto 3pl MA indicator is a technical analysis tool that uses three different moving averages to identify trends in the price of an asset. The three moving averages have lengths of 12, 26, and 50. If these numbers sound familiar its because they are based off the standard of the MACD indicator, and can be either simple moving averages (SMA) or exponential moving averages (EMA), depending on user preference.

The following is plotted on the chart

The fast EMA/SMA (based on the 12-period length) in yellow.

The mid EMA/SMA (based on the 26-period length) in gray.

The slow EMA/SMA (based on the 50-period length) in either green or red, depending on whether the current close price is above or below the Overall Trend MA.

In addition to the moving averages, the indicator also calculates the MACD (Moving Average Convergence Divergence), and uses it to color the bars based on the momentum of the asset.

The MACD is calculated using two user-defined lengths (fast and slow), as well as a user-defined smoothing length for the signal line. The oscillator and signal line can be either SMA or EMA, and the colors of the MACD bars are based on whether the histogram is growing or falling, and whether it is above or below the zero line.

Overall, this indicator provides traders with a comprehensive tool for understanding the trend of an asset, as well as the momentum behind that trend. The moving averages provide a clear visual representation of the trend, while the MACD bars give insight into the strength of that trend and potential shifts in momentum.

---------------LONG ENTRY----------------

MA1 above MA2 and Overall trend = Green

IF RSI is above its midline you are confirmed for a long entry

-----------Short Entry--------------

MA1 below MA2 and Overall trend = Red

IF RSI is below its midline you are confirmed for a short entry

TRIX with Momentum----------- ENGLISH --------------

This indicator is called "TRIX with Momentum" and is used to analyze the momentum of an asset's price and predict potential trend reversals. The logic of operation is based on the combination of two indicators: the Triple Exponential Moving Average (TRIX) and the momentum oscillator.

The TRIX is calculated using three exponential moving averages (EMA) of the asset's closing price, with a user-defined length (set to 14 by default). The TRIX is then normalized and centered around 0 to facilitate analysis of its relationship with the momentum oscillator.

The momentum oscillator is calculated using the EMA of the normalized TRIX with a user-defined length (set to 14 by default).

The indicator plots the normalized TRIX and the momentum oscillator on a chart, using different colors to indicate whether the TRIX is above or below 0. Additionally, the color of the y-axis label changes based on the position of the oscillator, while the color of the x-axis label remains gray.

The indicator uses a weighted average between the normalized TRIX and the momentum oscillator to create a colored background of the chart, which changes based on the weighted average. If the weighted average is positive, the chart's background is green, otherwise it is red. Finally, a horizontal line is drawn at point 0 to facilitate visual analysis of the chart.

------------ ITALIANO -------------

Questo indicatore è chiamato "TRIX with Momentum" ed è utilizzato per analizzare il momentum del prezzo di un asset e prevedere eventuali inversioni di trend. La logica di funzionamento è basata sulla combinazione di due indicatori: il TRIX (Indicatori di media mobile Tripla Esponenziale) e l'oscillatore momentum.

L'indicatore consente all'utente di impostare la lunghezza del TRIX e dell'oscillatore momentum come input personalizzato. Il TRIX viene calcolato utilizzando tre medie mobili esponenziali (EMA) della chiusura dei prezzi dell'asset, mentre l'oscillatore momentum viene calcolato utilizzando l'EMA del TRIX normalizzato.

Il TRIX normalizzato viene centrato intorno allo 0 per facilitare l'analisi della sua relazione con l'oscillatore momentum. L'indicatore plotta il TRIX normalizzato e l'oscillatore momentum su un grafico, utilizzando diversi colori per indicare se il TRIX è sopra o sotto lo 0.

L'indicatore utilizza una media pesata tra il TRIX normalizzato e l'oscillatore momentum per creare uno sfondo colorato del grafico, che cambia in base alla media pesata. L'utente può impostare il peso da dare al TRIX e all'oscillatore momentum come input personalizzato, e il peso dell'oscillatore momentum verrà automaticamente impostato come complementare al peso del TRIX.

Se la media pesata è positiva, lo sfondo del grafico è verde, altrimenti è rosso. Viene tracciata anche una linea orizzontale al punto 0 per facilitare l'analisi visiva del grafico.

Infine, il colore dell'etichetta dell'asse y cambia in base alla posizione dell'oscillatore, mentre il colore dell'etichetta dell'asse x rimane sempre grigio.

Bulls v BearsThis script helps you identify the relative strength of bulls and bears in the market. It calculates the difference between the high and the moving average for bulls, and the difference between the moving average and the low for bears. Then it normalizes the values between -100 and 100 using the highest and lowest values of the last "bars back" periods. This allows you to compare the current strength of bulls and bears relative to their historical strength.

The output of the script is a colored column chart that represents the difference between the normalized bulls and bears values. If the chart is mostly green, it means the bulls are currently stronger than the bears, and vice versa for a mostly red chart. Additionally, the script provides bullish and bearish signals based on when the normalized bulls cross above or below the user-defined "Line Height" value.

You can use this script to help you identify potential trend changes in the market, as well as to confirm existing trends.

OBV-MACDThe OBV-MACD indicator is a momentum-based technical analysis tool that helps traders identify trend reversals and trend strength. This Pine script is an implementation of the OBV-MACD indicator that uses the On-Balance Volume (OBV) and Moving Average Convergence Divergence (MACD) indicators to provide a momentum data of OBV.

The OBV-MACD indicator uses the OBV to calculate the cumulative volume, which is then smoothed using two moving averages - fast and slow. The difference between these moving averages is plotted as a histogram, with a signal line plotted over it. A buy signal is generated when the histogram crosses above the signal line, indicating a bullish trend, while a sell signal is generated when the histogram crosses below the signal line, indicating a bearish trend.

This Pine script also includes an OBV-MACD-Donchian version that incorporates Donchian channels for the OBV-MACD. The Donchian channel is a technical analysis indicator that helps traders identify the highs and lows of an asset's price over a certain period. The OBV-MACD-Donchian version uses the OBV-MACD indicator along with the Donchian channels to provide signals that the momentum of OBV is making new high/low during that period of time.

Traders can customize the input parameters of the OBV-MACD indicator, such as the timeframe, method of calculation for the moving averages, and the lengths of the moving averages and breakout lengths. The colors of the plot can also be customized to suit the trader's preferences.

Impulse Momentum MACD - Slow and FastImpulse Momentum MACD - Slow and Fast

The Momentum indicator is a technical indicator that measures the speed and strength of the price movement of a financial asset. This indicator is used to identify the underlying strength of a trend and predict potential changes in price direction, when the indicator crosses the zero line, it can signal a change of direction in the price trend.

On the other hand, the MACD is an indicator used to identify the trend and strength of the market and shows the difference between two exponential moving averages ( EMA ) of different periods. The MACD is commonly used to determine the direction of an asset's price trend.

COPOSITION AND USE OF THE INDICATOR

This script is an implementation of the Impulse Momentum MACD indicator with two variations: slow and fast. It uses a combination of the Momentum indicator and the Moving Average Convergence/Divergence (MACD) indicator to identify trend reversals and momentum changes in an asset's price.

The combination of both indicators can help traders identify market entry and exit opportunities. The Impulse Momentum MACD is a Modified MACD, it is formed by filtering the values in a range of Modifiable Moving Averages by calculating their high and low ranges,This indicator has two parts: a slow part and a fast part. The slow part uses input values for the lengths of the moving averages and the length of the signal for the MACD indicator. The fast part uses different input values for the lengths of the moving averages. Also, each part has its own set of line colors and histogram colors for easy visualization.

The script also includes inputs to choose the type of moving average to use (SMA, EMA, etc.), the lookback period, the colors for the histogram lines and bars, and a zero trend line (also known as a horizontal trend line). ).

* Highest performing custom settings for the zero trend line. For Operations of:

- One Minute: Trend Line Time Frame = Five Minutes.

- Three Minutes: Trend Line Time Frame = Fifteen Minutes.

- Five Minutes: Trend Line Time Frame = Thirty Minutes.

- Fifteen Minutes: Trend Line Time Frame = Sixty Minutes.

Rules For Trading

🔹 Bullish:

* The Zero Horizontal Trend Line should be in Green Color.

* The Slow Histogram Bar should be in Green Color.

* The Fast Histogram Bar must be in Blue or Black Color or No Bar Appears.

* The Momentum Line or Momentum Area must be in Green Color.

crosses:

- When the Impulse Momentum MACD Slow line crosses the Impulse Momentum MACD Slow signal line upwards.

- When the Impulse Momentum MACD Fast line crosses the Impulse Momentum MACD Fast signal line upwards.

- Note 1: A Position is Opened when the condition of any of the aforementioned crossovers is met.

- Note 2: If the two aforementioned crossings anticipate the condition of the Zero Horizontal Tendency Line because it is in Red; A position is only opened immediately when the Zero Horizontal Trend line turns Green.

🔹 Bearish:

* The Zero Horizontal Trend Line should be in Red Color.

* The Slow Histogram Bar should be in Red Color.

* The Fast Histogram Bar must be in Blue or Black Color or No Bar Appears.

* The Momentum Line or Momentum Area must be in Red Color.

crosses:

- When the Impulse Momentum MACD Slow line crosses the Impulse Momentum MACD Slow signal line downwards.

- When the Impulse Momentum MACD Fast line crosses the Impulse Momentum MACD Fast signal line downwards.

- Note 1: A Position is Opened when the condition of any of the aforementioned crossovers is met.

- Note 2: If the two aforementioned crossings anticipate the condition of the Zero Horizontal Tendency Line because it is Green, an immediate position is only opened when the Zero Horizontal Tendency line turns Red.

This script can be used in different markets such as forex, indices and cryptocurrencies for analysis and trading. However, it is important to note that no trading strategy is guaranteed to be profitable, and traders should always conduct their own research and risk management.

Know Sure Thing + RibbonFrom now on this will be the main indicator I will be using.

The mathematical foundation of KST is elegant and trustworthy. I took the time to share this beautiful (in my opinion) indicator, because you will probably be seeing it in my future ideas.

I am not a trader, this indicator was made to analyze mainly long-term charts, and trend-continuation/change analysis.

The purpose of this indicator is not to give entry/exit points. However, the 9-period EMA (tightest EMA) can serve as an alternative to the classic "9-period MA signal line".

Tread lightly, for this is hallowed ground.

-Father Grigori

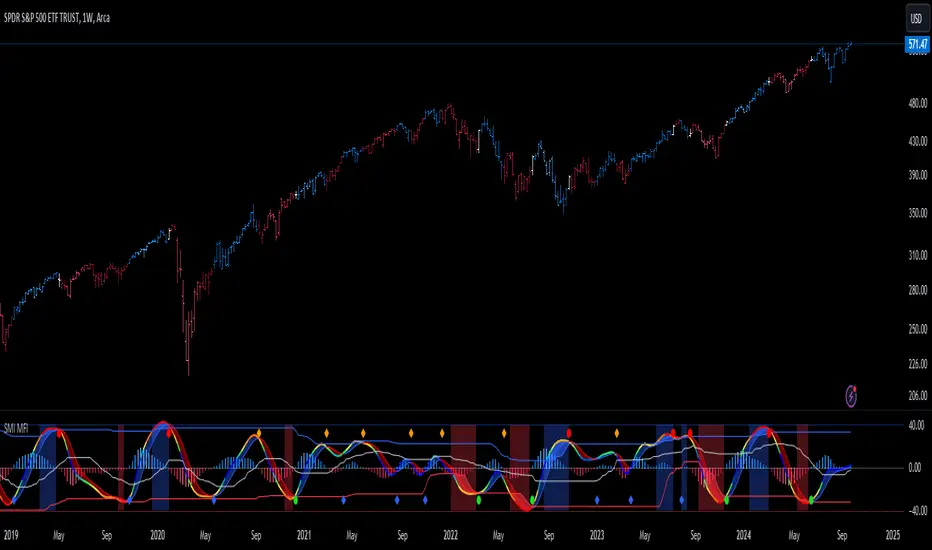

Stochastic Momentum Index (SMI) of Money Flow Index (MFI)"He who does not know how to make predictions and makes light of his opponents, underestimating his ability, will certainly be defeated by them."

(Sun Tzu - The Art of War)

▮ Introduction

The Stochastic Momentum Index (SMI) is a technical analysis indicator that uses the difference between the current closing price and the high or low price over a specific time period to measure price momentum.

On the other hand, the Money Flow Index (MFI) is an indicator that uses volume and price to measure buying and selling pressure.

When these two indicators are combined, they can provide a more comprehensive view of price direction and market strength.

▮ Improvements

By combining SMI with MFI, we can gain even more insights into the market. One way to do this is to use the MFI as an input to the SMI, rather than just using price.

This means we are measuring momentum based on buying and selling pressure rather than just price.

Another way to improve this indicator is to adjust the periods to suit your specific trading needs.

▮ What to look

When using the SMI MFI indicator, there are a few things to look out for.

First, look at the SMI signal line.

When the line crosses above -40, it is considered a buy signal, while the crossing below +40 is considered a sell signal.

Also, pay attention to divergences between the SMI MFI and the price.

If price is rising but the SMI MFI is showing negative divergence, it could indicate that momentum is waning and a reversal could be in the offing.

Likewise, if price is falling but the SMI MFI is showing positive divergence, this could indicate that momentum is building and a reversal could also be in the offing.

In the examples below, I show the use in conjunction with the price SMI, in which the MFI SMI helps to anticipate divergences:

In summary, the SMI MFI is a useful indicator that can provide valuable insights into market direction and price strength.

By adjusting the timeframes and paying attention to divergences and signal line crossovers, traders can use it as part of a broader trading strategy.

However, remember that no indicator is a magic bullet and should always be used in conjunction with other analytics and indicators to make informed trading decisions.

WillyCycle Oscillator&DoubleMa/ErkOzi/"This code creates a technical analysis indicator used to calculate and visualize the WillyCycle oscillator and double moving average indicators on the price of a financial asset. The functionality can be summarized as follows:

*Calculate the WillyCycle oscillator: The WillyCycle is an oscillator calculated based on the highest and lowest values of an asset. This oscillator is used to measure overbought or oversold conditions of the asset.

*Calculate the double moving average: The double moving average helps determine trends by calculating the short-term and long-term moving averages of asset prices.

*Use the WillyCycle oscillator and double moving average indicators together: The WillyCycle oscillator is combined with the double moving averages to provide a clearer indication of overbought and oversold conditions.

*Visualize the indicator with color coding: The indicator is color-coded to show overbought and oversold conditions. Additionally, line and background colors are changed to make the indicator more readable.

Many parameters can be adjusted on the indicator: The indicator can be customized and modified by the user. For example, the period of the WillyCycle oscillator and the lengths of the double moving averages can be adjusted."

The strategy is based on two indicators - the WillyCycle oscillator and the double moving average. The WillyCycle oscillator measures overbought and oversold conditions of the asset based on its highest and lowest values. The double moving average calculates short-term and long-term moving averages of the asset's price, which can help identify trends.

The WillyCycle oscillator and the double moving average are combined in this strategy to provide a clearer indication of overbought and oversold conditions. When the WillyCycle oscillator indicates that the asset is oversold and the short-term moving average crosses above the long-term moving average, it may signal a buy opportunity. Conversely, when the WillyCycle oscillator indicates that the asset is overbought and the short-term moving average crosses below the long-term moving average, it may signal a sell opportunity.

To make it easier for traders to read and interpret the indicator, color-coding is used to indicate overbought and oversold conditions. The user can also customize the indicator by adjusting parameters such as the period of the WillyCycle oscillator and the lengths of the double moving averages.

*ıt provides successful buy and sell signals for price reversals.

*You can open counter trades in overbought and oversold areas by following the averages.

Stochastic Momentum Index (SMI) Refurbished▮Introduction

Stochastic Momentum Index (SMI) Indicator is a technical indicator used in technical analysis of stocks and other financial instruments.

It was developed by William Blau in 1993 and is considered to be a momentum indicator that can help identify trend reversal points.

Basically, it's a combination of the True Strength Index with a signal line to help identify turning points in the market.

SMI uses the stochastic formula to compare the current closing price of an asset with the maximum and minimum price range over a specific period.

He then compares this ratio to a short-term moving average to create an indicator that oscillates between -100 and +100.

When the SMI is above 0, it is considered positive, indicating that the current price is above the short-term moving average.

When it is below 0, it is considered negative, indicating that the current price is below the short-term moving average.

Traders use the SMI to identify potential trend reversal points.

When the indicator reaches an extreme level above +40 or below -40, a trend reversal is possible.

Furthermore, traders also watch for divergences between the SMI and the asset price to identify potential trading opportunities.

It is important to remember that the SMI is a technical indicator and as such should be used in conjunction with other technical analysis tools to get a complete picture of the market situation.

▮ Improvements

The following features were added:

1. 7 color themes, for TSI, Signal and Histogram.

2. Possibility to customize moving average type for TSI/Signal.

3. Dynamic Zones.

4. Crossing Alerts.

5. Alert points on specific ranges.

5. Coloring of bars according to TSI/Signal/Histogram.

▮ Themes

Examples:

▮ About Dynamic Zones

'Most indicators use a fixed zone for buy and sell signals.

Here's a concept based on zones that are responsive to the past levels of the indicator.'

The concept of Dynamic Zones was described by Leo Zamansky ( Ph .D.) and David Stendahl, in the magazine of Stocks & Commodities V15:7 (306-310).

Basically, a statistical calculation is made to define the extreme levels, delimiting a possible overbought/oversold region.

Given user-defined probabilities, the percentile is calculated using the method of Nearest Rank.

It is calculated by taking the difference between the data point and the number of data points below it, then dividing by the total number of data points in the set.

The result is expressed as a percentage.

This provides a measure of how a particular value compares to other values in a data set, identifying outliers or values that are significantly higher or lower than the rest of the data.

▮ What to look for

1. Divergences/weakening of a trend/reversal:

2. Supports, resistances, pullbacks:

3. Overbought/Oversold Points:

▮ Thanks and Credits

- TradingView and PineCoders: for SMI and Moving Averages

- allanster: for Dynamic Zones

Colorful Moving Averageswhat is Colorful Moving Averages?

This indicator allows you to use your favorite moving averages in their advanced form.

what it does?

It gives you easy access to the following information with a single indicator: the direction and momentum of the price,

rate of change of momentum (acceleration),

time-dependent change in momentum,

and all the other information a moving average provides.

it paints the selected moving average type according to the momentum it has, and also shows the momentum and acceleration values in a table. colors are interpreted as follows: the color of the moving average is red, the momentum is negative; A green color means the momentum is positive, and a yellow color means the momentum is 0. As the momentum changes, the moving average takes on different shades of these 3 colors. how it actually works can be easily understood at a glance.

"Δ" sign indicates momentum compressed between 100 and -100.

"Γ" sign indicates the momentum of the momentum, that is the acceleration. its values are compressed between 100 and -100.

how it does it?

it uses this formulas:

how to use it?

First, select the moving average type you want to use. then set the length and source. Now, with a single indicator, you can observe both the distance of the price from the mean, its instantaneous momentum relative to the last candle by looking at the symbol "Δ", the current change of momentum by looking at the symbol "Γ", and the time-dependent change in its momentum by looking at the colors. you can also see the maximum and minimum points where the momentum is equal to 0.