Worm *Public*This Pine Script code is designed to create a custom technical indicator called "Worm" that helps identify trends in the market based on momentum. Let's break down the code and its settings:

Indicator Title and Overlay:

The indicator is named "Worm (Clean)" and is set to be overlaid on the price chart.

Input Settings:

The code defines various input settings, which can be customized by the user. These settings include:

Indicator Settings (e.g., Alpha, Gap)

Backtest Settings (e.g., HighlightCrossovers, ApplyNorm)

Color Settings (e.g., Buy Color, Sell Color, Wait Color)

Location Settings for displaying the indicator above, below, or at the price.

Toggleable Inputs:

These settings allow you to choose whether the momentum indicator should be displayed above, below, or at the price chart. You can also specify the colors for buy, sell, and wait signals.

Indicator Calculations:

The code calculates momentum using various formulas involving the source price data (e.g., open, high, low, close). Momentum values are stored in variables L0, L1, L2, L3, and lrsi.

It also calculates the Color values for the indicator based on certain conditions and user-defined settings.

Bcolor and Scolor are used to determine the color of the plotted indicator based on buy and sell conditions.

Bollinger Bands (BB) and Keltner Channels (KC) Calculation:

The code calculates Bollinger Bands (UpperBB and LowerBB) and Keltner Channels (UpperKC and LowerKC) using the source price data.

It also determines whether the market is in a squeeze (SqzOn) or not (NoSqz) based on the relationship between BB and KC.

Signal Generation:

Buy and sell signals are generated based on various conditions, including momentum values and the squeeze state.

The color of the indicator line is determined based on the buy and sell signals.

LagF Calculation:

The LagF variable is calculated based on certain formulas involving the L0Line, L1Line, L2Line, and L3Line values.

Control Color:

The Color variable is used to control the color of the LagF indicator line based on certain conditions.

Plotting:

The momentum indicator (Val) is plotted on the chart with the specified colors and style.

The LagF indicator (Worm) is also plotted with a dynamic color based on market conditions.

Alerts are triggered when buy or sell signals are generated.

Experimental Section:

This section appears to be left for experimentation and may contain additional code or features.

Overall, this Pine Script code calculates and displays a custom momentum-based indicator called "Worm" on a price chart. It generates buy and sell signals based on momentum and squeeze conditions and allows users to customize various settings, including indicator location and colors. The code is designed for technical analysis and trend identification in financial markets.

Полосы и каналы

Supertrend with Stochastic OB/OS Arrows @KING

TradingView Idea: Supertrend with Stochastic Arrows @KING

Overview:

- Combining the Supertrend indicator with Stochastic arrows for a comprehensive market

view, providing insights into trend direction and potential reversal points.

Supertrend Settings:

- ATR Length: The length parameter for calculating the Average True Range (ATR).

- Factor: A multiplier used to determine the distance of the Supertrend line from the

price.

Supertrend Display:

The Supertrend is color-coded:

- During an uptrend, it is displayed in green .

- During a downtrend, it is displayed in red .

- The body of the candlesticks is filled with color during the corresponding trend direction.

Stochastic Settings:

- K Length: The period length for the %K line in the Stochastic oscillator.

- K Smoothing: Smoothing factor for %K.

- D Smoothing: Smoothing factor for %D.

- Overbought Level: The threshold indicating an overbought condition.

- Oversold Level: The threshold indicating an oversold condition.

Arrows:

- Buy arrows are displayed below the bars during a downtrend when Stochastic is below the

oversold level.

- Sell arrows are displayed above the bars during an uptrend when Stochastic is above the

overbought level.

Supertrend Display:

- The Supertrend line is plotted with a color change based on its direction.

- The body of the candlesticks is filled with green during an uptrend and red during a downtrend.

Usage:

- Traders can use this script to identify potential entry and exit points, leveraging the

insights provided by both the Supertrend indicator and Stochastic oscillator. This

combination aims to capture trend strength and potential reversal opportunities.

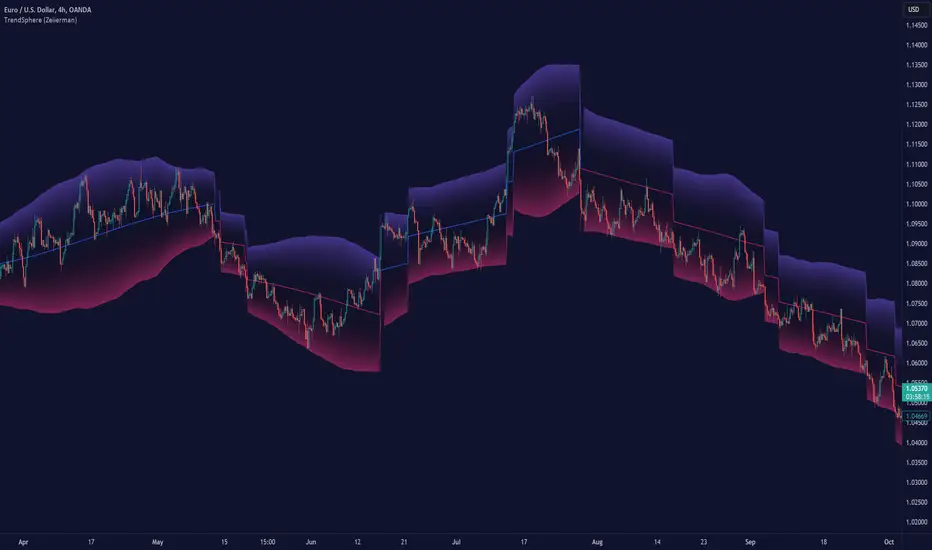

TrendSphere (Zeiierman)█ Overview

TrendSphere is designed to capture and visualize market trends and volatility effectively. It combines various volatility measures and trend analysis techniques, producing dynamic bands and a central trend line on the price chart. Its essence is to offer a real-time, reliable estimate of the underlying linear trend in the price.

█ How It Works

Real-Time Trend Estimation

At its core, TrendSphere is designed to offer instantaneous and accurate insights into the inherent linear trend of asset prices. By continually updating its estimations, it ensures traders are equipped with the most current data. This allows the construction of support and resistance bands around the estimated trend, providing trading opportunities.

Dynamic Bands and Trend Line

TrendSphere plots a central trend line and dynamic bands around it on the price chart. Influenced by volatility, the distance between these elements offers a clear view of market conditions and the strength or weakness of trends. These bands not only depict potential turning points but also offer traders valuable opportunities to trade within the confines of the overarching trend.

Volatility Measures

Traders can select their preferred volatility measure and adjust settings to best fit their analysis needs. The bands and trend line dynamically respond to these selections, offering a tailored view of market conditions.

ATR (Average True Range): Reflects market volatility by evaluating the range between high and low prices.

Historical Volatility: Computes price variability using the standard deviation of log returns.

Bollinger Band Width: Measures the distance between Bollinger Bands, providing another angle on market volatility.

Eliminating Common Complications

One of the standout features of TrendSphere is its ability to determine linear price trends without falling prey to challenges like backpainting or repainting. In layman's terms, this means traders get a more trustworthy and unaltered view of price movements, leading to enhanced decision-making in line with the genuine trajectory of price trends.

█ How to Use

Trend Analysis

Observe the central trend line; its direction indicates the prevailing trend. When the price is above the trend line, it suggests an upward trend, and when it's below, it indicates a downward trend.

Volatility Analysis

Wider bands imply higher market volatility, suggesting larger price swings, while narrower bands indicate lower volatility. Traders can use the bands to identify potential reversal points and overbought/oversold conditions.

Potential Trading Signals (Using Bollinger bandwidth as volatility measure)

Consider buying when the price is above the trend line with narrowing bands, suggesting a strong upward trend.

Consider selling when the price is below the trend line with narrowing bands, indicating a strong downward trend.

█ Settings

Select Volatility Measure

Choose the desired volatility measure: ATR, Historical Volatility, or Bollinger Band Width.

Volatility Scaling Factor

Adjusts the scale of the volatility measure, influencing the width of the bands.

Volatility Strength

Modifies the influence of volatility on the bands, adjusting their responsiveness to volatility changes.

Length

Defines the number of periods used in calculating the selected volatility measure, impacting the stability and responsiveness of the bands.

Trend Sensitivity

Adjusts the sensitivity of the trend component, affecting how quickly it reacts to price changes.

█ Related scripts with the same calculation philosophy

TrendCylinder

Predictive Trend and Structure

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Donchian MA Bands [LuxAlgo]The Donchian MA Bands script is a complete trend indicator derived from the popular Donchian channel indicator as well as various customizable moving averages to estimate trend direction and build support/resistance levels & zones.

🔶 USAGE

The indicator outputs various elements, the main ones being a lower dynamic zone (blue by default), an upper dynamic zone (in orange by default), and one support and resistance level/zones (red/green by default).

A prominent lower zone is indicative of an uptrend, while a prominent upper zone is indicative of a downtrend. These zones can be used as support/resistance as well.

Support/resistance zones and levels can be used using a breakout methodology or to determine price bounced if a level was tested multiple times.

The indicator contains various modes affecting the output of the indicator, described below.

🔹 Clouds

Clouds return one upper/lower dynamic zone and look/act similarly to a trailing stop. Price over the lower zone is indicative of an uptrend, and price under the upper zone is indicative of a downtrend.

🔹 Upper Band

The upper band mode returns a dynamic zone closer to prices during an uptrend, and farther away during a downtrend.

This band can act as a support during uptrends.

🔹 Lower Band

The lower band mode returns a dynamic zone closer to prices during an uptrend, and farther away during a downtrend.

This band can act as a resistance during downtrends.

🔹 Bands

Bands return both upper and lower zones, the zones are more apparent depending on the price trend direction, with uptrends being indicated by a more visible lower zone, and downtrends being indicated by a more visible upper zone.

Breakout dots are highlighted when price breakout the indicator displayed extremities, and can be indicative of a confirmed trend reversal.

These breakouts can be more effective for trend following during trending markets. Ranging markets might return breakouts highlighting the top/bottom.

🔶 DETAILS

The core of this script is the highest / lowest mean average (MA) value for a given number of bars back ( Donchian lines).

This is repeated a few times with the obtained values.

When Bands are chosen ( Style ) this will be repeated 1 more time.

The type of mean average can be customized ( Type MA ), as well as the number of bars back ( Length ).

Depending on the choice of bands ( Style ) the script will focus on certain area's of interest.

When the option Clouds , Upper band or Lower band is chosen, an extra feature, support/resistance (S/R), will be shown.

These color-filled areas are visible when there is a difference between the 2nd and 3rd highest/lowest values.

The lines/areas can be used for stop loss, entry, exit,...

You can set the type of MA and Length separately ( Settings -> S/R ).

If you don't need this feature, simply set Type ( Settings -> S/R ) -> NONE

The shape sometimes resembles triangles, indicating a potential direction

Default the average of the highest and lowest values is plotted (Style -> Mid Donchian)

This can act as potential support/resistance or visualization of the trend, the mean average is not plotted but can be (Style -> MA)

🔹 Note

When the option Bands is chosen, an indication is plotted when the closing price breaks above the highest band or breaks below the lower band. This isn't necessarily a buy/sell signal, it is merely a signal that these lines are broken.

Users should decide on their own how they use the bands/lines/areas as entry, exit, trailing stop, stop loss, profit taking,...

🔶 SETTINGS

🔹 Bands

Style: Clouds (default), Upper band, Lower band, Bands

Type MA: choose between SMA, EMA, RMA, HullMA, WMA, VWMA (default), DEMA, TEMA, NONE (off)

Length: Length of moving average and Donchian calculations (default 20)

Colour Bands

🔹 S/R (Support/Resistance, visible with Clouds, Upper band or Lower band)

Type MA: choose between SMA, EMA, RMA, HullMA, WMA, VWMA (default), DEMA, TEMA, NONE (off)

Length: Length of moving average and Donchian calculations (default 20)

Colour S/R

RSI + Fibonacci HH LL Support Resistance I have integrated my past scripts and brushed them up further.

This tool allows for support/resistance, stop loss, take profit, and trend analysis using RSI and Fibonacci ratios.

For example, the Fibonacci ratio is used as follows

l1 = m - dist * 0.618

l2 = m - dist * 1.618

l3 = m - dist * 2.618

l4 = m - dist * 4.235

l5 = m - dist * 6.857

l6 = m - dist * 11.089

When the Fibonacci ratio reaches 2.618 or higher and the RSI smoothed by the 5-day EMA is oversold/overbought, the bar color is changed by a gradation.

We have tried to make the design as beautiful and good-looking as possible. You can also hide the lines to suit your own preference.

Example usages are here:

BTCUSDT 1Hour Chart

Using Fibonacci numbers

BTCUSDT 15min Chart, for Scalping

Here, to set the highest and lowest prices one hour ago, "4" is substituted as the calculation: 15 minutes x 4 = 60

BTCUSDT 15min Chart, for Scalping

To set the highest and lowest prices 4 hours ago , "4" is substituted as the calculation: 15 minutes x 16 = 240

BTCUSDT 15min Chart, for Scalping

To draw yesterday's high and low as support/resistance lines, I substituted the number "96" as 1440/15=96.

BTCUSDT 1min Chart, for Scalping

Substituted "60" to trail the highest and lowest prices over a 60-minute period on a 1-minute chart, and removed lines to beautify

BTCUSDT 1day Chart, for Long-Term Investers

This is an example of using "90" because it is a 1-day chart and assumes that 3 months = 90 days in order to trail the highest and lowest prices over a 3-month period and no lines.

My past scripts are here:

RSI + FIB HH LL StopLoss Finder/Contrarian Trades

Fibonacci HH LL TRAMA Band

2Mars strategy [OKX]The strategy is based on the intersection of two moving averages, which requires adjusting the parameters (ratio and multiplier) for the moving average.

Basis MA length: multiplier * ratio

Signal MA length: multiplier

The SuperTrend indicator is used for additional confirmation of entry into a position.

Bollinger Bands and position reversal are used for take-profit.

About stop loss:

If activated, the stop loss price will be updated on every entry.

Basic setup:

Additional:

Alerts for OKX:

Educational Inidicators - Ichimoku CloudThis indicator is part of the Indicator Educational Series, intended to help newer traders understand and interact with various indicators. The goal is to allow users to gain a stronger understanding of an indicator's underlying philosophy, and visually see how changes to an indicator's parameters affects the trades suggested by that indicator.

The scripts in this series are all open source, with the code broken up into logical section and notated so beginner users can also understand some PineScript fundamentals.

Please understand that no indicator presented in and of itself constitutes a complete trading strategy. Rather, this series is to help users determine which indicators make sense to them, and which ones to combine to create their own trading strategy. All material presented is purely for educational purposes.

Presented here is the Ichimoku Cloud.

The Ichimoku Cloud was developed by Goichi Hosada, and first published in the late 1960s. It is used by traders to understand price momentum, and help forecast future price movements.

The indicator at its core can be understood from four component parts:

The Conversion Line - An average of the highest and lowest price in a given window. Typically, this is a "fast" average, and as such, this line has the lowest period

The Base Line - An average of the highest and lowest price in a given window. This is a "slower" average than the Conversion Line, and as such should have a larger period than the Conversion Line

Leading Span A - The average of the Conversion Line and the Base Line

[*}Leading Span B - An average of the highest and lowest price in a given window. This is the "slowest" average of all three, and as such should have the largest period

When plotted, the Conversion Line (orange by default), Base Line (purple by default), Leading Span A (blue by default), and Leading Span B (red by defaults) are all drawn on the chart along with the price candles. The area between the Leading Span A and Leading Span B lines are also shaded depending on which of the two lines is greater: whenever Leading Span A is greater the area is shaded positively (blue by default), whenever Leading Span B is greater the area is shaded negatively (red by defaults).

One interesting feature of the Ichimoku Cloud is that it drawn a certain number of candles forward. What this means is that where the cloud is drawn on the chart is reflective of prices that have occurred a number of candles in the past. This is done intentionally to help traders see how the current price is moving in relation to historical price movements on the asset.

See below for how the indicators look in their default colors on the chart

These indicators can then be used to start analyzing the price movement, and making trade decisions.

The first inference we can make is the momentum of the price. Since the lines are drawn from averages of varying speeds, the shaded area between the Leading Span lines can tell us whether the momentum is bullish (up) or bearish (down).

Whenever Leading Span A, the faster of the two lines, is above Leading Span B, that means that price is moving upward faster than it typically has, ergo we are in Bullish Momentum. On the chart, this is indicated in two ways:

The area is shaded positively (blue by default)

A green upward triangle is added to the chart to indicate where the momentum first turned Bullish

Whenever Leading Span A is below Leading Span B, that means that price is moving downward faster than it typically has, ergo we are in Bearish Momentum. On the chart, this is indicated in two ways:

The area is shaded negatively (red by default)

A red downward triangle is added to the chart to indicate where the momentum first turned Bearish

The next inference we can make is possible trading points. When we're in a period of momentum, as determined above, we know that price is going up or down, depending on the momentum we're in. We can then use the Conversion Line, Base Line, and the Price itself to confirm a good trade price.

When the asset is in Bullish Momentum, and the Conversion Line, our fastest average, is above the Base Line, our mid speed average, we know that the price is coming up quickly in the short term. When the Base Line and current Price are also above the cloud, then we have triple confirmation that price is going up, and we should enter a Long position. On the chart, this point is indicated with a green flag.

When the asset is in Bearish Momentum, and the Conversion Line is below the Base Line, we know that the price is going down quickly in the short term. When the Base Line and current Price are also below the cloud, then we have triple confirmation that price is going down, and we should enter a Short position. On the chart, this point is indicated with a red flag.

The script presented here also allows users to customize the various parameters of the Ichimoku Cloud, and visually see how analysis is affected by these changes. This is designed to allow users to modify parameters as they see fit, within certain constraints, to find the best set for them. The lines, cloud, and chart indicators will all update automatically with the users' inputs.

Keltner Channel Strategy with Golden CrossOnly trade with the trend.

This Keltner Channel-based strategy that will only enter into a trade if the signal of the Keltner Channel agrees with a moving average crossover as defined by the user.

Long Position Entries

2 Conditions must be present

1. There must be a Golden Cross (lower period moving average is above higher period moving average). ex 50 period MA > 200 period MA.

2. Price must cross above the Keltner Channel ATR defined by the user.

Short Position Entries

2 Conditions must be present

1. There must be a Death Cross (lower period moving average is below higher period moving average). ex 50 period MA < 200 period MA.

2. Price must cross below the Keltner Channel ATR defined by the user

Closing Trades:

The strategy closes trades as follows:

1. Price crossing the Keltner Channel's Take Profit ATR (defined by User)

2. Price crossing the Keltner Channel's Stop Loss ATR (defined by User)

IU Break of any session StrategyHow this script works:

1. This script is an intraday trading strategy script which buy and sell on the bases of user-defined intraday session range breakout and gives alert(if the alert is set) message too when the new position is open.

2. It calculate the session as per the user inputs or user defined custom session.

3. The script stores the highest and lowest value of the whole session.

4. It take a long position on the first break and close above the highest value.

5. It take a short position on the break and close below the lowest value.

6. The script takes one position in one day.

7. The stop loss for this script is the previous low(if long) or high(if short).

8. Take profit is 1:2 and it's adjustable.

9. This script work on every kind of market.

How The Useful For The User :

1. User can backtest any session range breakout he wants to trade.

2. User can get alert when the new position is open.

3. User can change the Risk to Reward in order to find the best Risk to Reward.

4. User can see the highest and lowest value of the session with respect to analyzing his trading objective.

5. This strategy script highlights which session range breakout performs best and which performs worst.

[dharmatech] KBDR Mean ReversionBased on the criteria described in the book "Mean Revision Trading" by Nishant Pant.

Bullish signal criteria:

Bollinger Bands must be outside Keltner Channel

Price near bottom bband

DI+ increasing

DI- decreasing

RSI near bottom and increasing

Bearish signal criteria:

Bollinger Bands must be outside Keltner Channel

Price near upper bband

DI+ decreasing

DI- increasing

RSI near upper and decreasing

A single triangle indicates that all 4 criteria are met.

If letters appear with the triangle, this indicates that there was a partial criteria match.

K : bbands outside Keltner

B : bbands criteria met

D : DI criteria met

R : RSI criteria met

You can use the settings to turn off partial signals. For example:

"Partial 3" means show signals where 3 of the criteria are met.

If you want more insight into the underlying criteria, load these indicators as well:

Bollinger Bands (built-in to TradingView)

Keltner Channels (built-in to TradingView)

RSI (built-in to TradingView)

ADX and DI

Warning:

Not meant to be used as a stand-alone buy/sell signal.

It regularly provides signals which would not be profitable.

It's meant to be used in conjunction with other analysis.

Think of this as a time-saving tool. Instead of manually checking RSI, DI+/DI-, bbands, distance, etc. this does all of that for you on the fly.

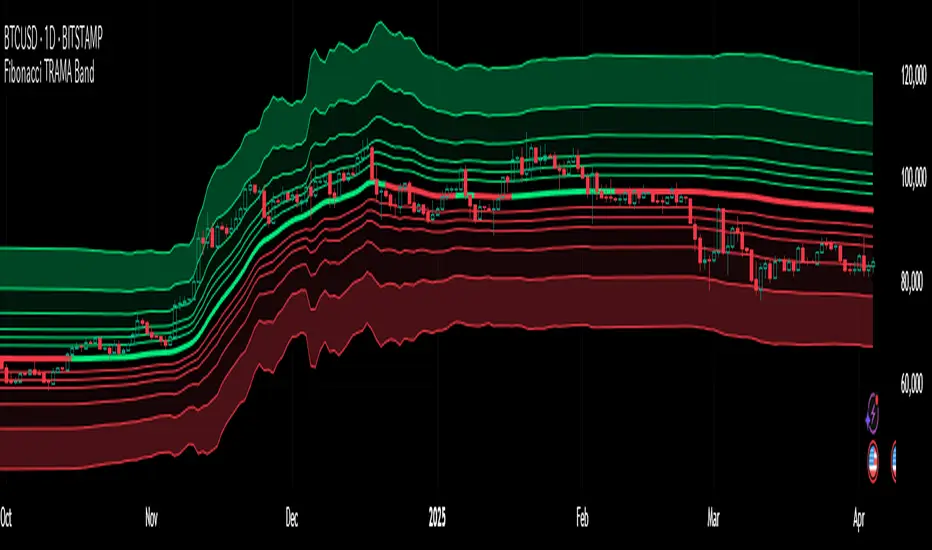

Fibonacci HH LL TRAMA BandLuxAlgo's Trend Moving Adaptive Moving Average was used as a reference to create bands by reading the highest and lowest prices of past bars based on Fibonacci numbers and then multiplying them by the Fibonacci ratio.

LuxAlgo/ LuxAlgo/

In particular, the so-called TRAMA is characterized by its adaptation to the average of the highest and lowest prices over a specific period of time and is used to identify support/resistance.

In order to apply this feature to the maximum extent possible, I used the high or low prices as the source of input, rather than the closing price.

For example,

src = high

not original like

src = close

In addition, I created 6 levels by multiplying the Fibonacci ratio

//Midline

mah = ama1

mal = ama2

m = (mah + mal)/2

//Half Mean Range

dist = (mah - mal)/2

//Levels

h6 = m + dist * 11.089

h5 = m + dist * 6.857

h4 = m + dist * 4.235

h3 = m + dist * 2.618

h2 = m + dist * 1.618

h1 = m + dist * 0.618

l1 = m - dist * 0.618

l2 = m - dist * 1.618

l3 = m - dist * 2.618

l4 = m - dist * 4.235

l5 = m - dist * 6.857

l6 = m - dist * 11.089

If you want to use it for scalping, such as 15 minutes, you can include Fibonacci numbers such as 21,34,55 for a quick reaction type to detect the trend. Also, by including Fibonacci numbers such as 89,144,233, you can see where you stand in the larger trend. Some examples are included below.

For Investors

BTCUSDT 1day Chart Fibonacci number "55"

For Daytraders

BTCUSDT 4hour Chart Fibonacci number "34"

For Scalpers

BTCUSDT 15min Chart Fibonacci number "55"

BTCUSDT 15min Chart Fibonacci number "89"

BTCUSDT 15min Chart Fibonacci number "233"

Fibonacci numbers are 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, etc.,

Fibonacci ratios are 0.618, 1.618, 2.618, 4.236, 6.854, 11.089, etc.,

Z-ScoreDescription:

The Z-Score indicator is a powerful tool for assessing the relative position of a financial instrument's current price compared to its historical price data. It calculates the Z-Score, which is a statistical measure of how many standard deviations an asset's current price is away from its historical mean. This can help traders identify overbought and oversold conditions in the market.

Input Parameters:

Length: This parameter sets the look-back period for calculating the mean and standard deviation. It is set to 20 by default but can be adjusted according to your trading preferences.

How it works:

The indicator first calculates the mean (average) and standard deviation of the selected price source (default: closing prices) over the specified length.

The Z-Score is then computed by measuring how many standard deviations the current price is away from the mean. This value is plotted on the chart, providing insight into the current price's relative position.

Usage:

Overbought: When the Z-Score rises above the upper threshold (e.g., +2 standard deviations, shown in red), it suggests that the asset's price is significantly above its historical average, indicating a potential overbought condition. Traders might consider this as a signal to be cautious about entering long positions or to look for potential short opportunities.

Oversold: Conversely, when the Z-Score falls below the lower threshold (e.g., -2 standard deviations, shown in green), it suggests that the asset's price is significantly below its historical average, indicating a potential oversold condition. Traders might consider this as a signal to be cautious about entering short positions or to look for potential long opportunities.

The Z-Score indicator can be a valuable addition to your technical analysis toolkit, helping you make informed trading decisions based on statistical price deviations.

Please make sure to conduct thorough backtesting and combine this indicator with other analysis techniques before making any trading decisions.

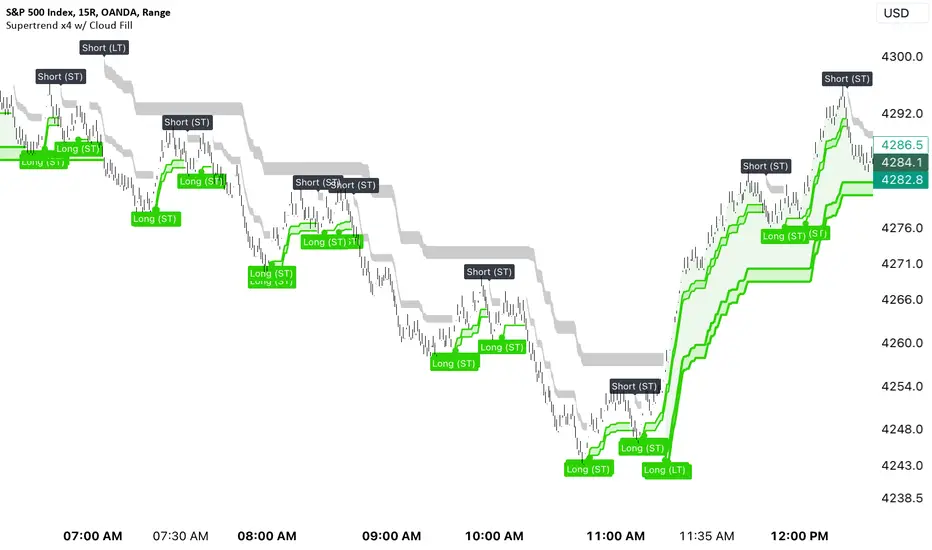

Supertrend x4 w/ Cloud FillSuperTrend is one of the most common ATR based trailing stop indicators.

The average true range (ATR) plays an important role in 'Supertrend' as the indicator uses ATR to calculate its value. The ATR indicator signals the degree of price volatility. In this version you can change the ATR calculation method from the settings. Default method is RMA, when the alternative method is SMA.

The indicator is easy to use and gives an accurate reading about an ongoing trend. It is constructed with two parameters, namely period and multiplier.

The implementation of 4 supertrends and cloud fills allows for a better overall picture of the higher and lower timeframe trend one is trading a particular security in.

The default values used while constructing a supertrend indicator is 10 for average true range or trading period.

The key aspect what differentiates this indicator is the Multiplier. The multiplier is based on how much bigger of a range you want to capture. In our case by default, it starts with 2.636 and 3.336 for Set 1 & Set 2 respectively giving a narrow band range or Short Term (ST) timeframe visual. On the other hand, the multipliers for Set 3 & Set 4 goes up to 9.736 and 8.536 for the multiplier respectively giving a large band range or Long Term (LT) timeframe visual.

A ‘Supertrend’ indicator can be used on equities, futures or forex, or even crypto markets and also on minutes, hourly, daily, and weekly charts as well, but generally, it fails in a sideways-moving market. That's why with this implementation it enables one to stay out of the market if they choose to do so when the market is ranging.

This Supertrend indicator is modelled around trends and areas of interest versus buy and sell signals. Therefore, to better understand this indicator, one must calibrate it to one's need first, which means day trader (shorter timeframe) vs swing trader (longer time frame), and then understand how it can be utilized to improve your entries, exits, risk and position sizing.

Example:

In this chart shown above using SPX500:OANDA, 15R Time Frame, we can see that there is at any give time 1 to 4 clouds/bands of Supertrends. These four are called Set 1, Set 2, Set 3 and Set 4 in the indicator. Set's 1 & 2 are considered short term, whereas Set's 3 & 4 are considered long term. The term short and long are subjective based on one's trading style. For instance, if a person is a 1min chart trader, which would be short term, to get an idea of the trend you would have to look at a longer time frame like a 5min for instance. Similarly, in this cases the timeframes = Multiplier value that you set.

Optional Ideas:

+ Apply some basic EMA/SMA indicator script of your choice for easier understanding of the trend or to allow smooth transition to using this indicator.

+ Split the chart into two vertical layouts and applying this same script coupled with xdecow's 2 WWV candle painting script on both the layouts. Now you can use the left side of the chart to show all bearish move candles only (make the bullish candles transparent) and do the opposite for the right side of the chart. This way you enhance focus to just stick to one side at a given time.

Credits:

This indicator is a derivative of the fine work done originally by KivancOzbilgic

Here is the source to his original indicator: ).

Disclaimer:

This indicator and tip is for educational and entertainment purposes only. This not does constitute to financial advice of any sort.

RSI + FIB HH LL StopLoss Finder/Contrarian TradesThis indicator is a multi-timeframe indicator that works in any timeframe.

It takes a price reading of the highest or lowest bar in the past based on Fibonacci numbers and plots it.

In addition, the RSI smoothed by a 5-day moving average can be used to detect signs that previous highs or lows will be reached in advance.

This gives insight into determining stop-loss values or entering the market in a contrarian manner.

This is an example of BTCUSDT 4Hour Chart

Here is BTCUSDT 1Hour Chart

For scalpers BTCUSDT 15min Chart Example

Fibonacci Number is 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, ...

FIbonacci Ratio is 0.236, 0.382, 0.5, 0.618, 1, 1.618, 2.618, 4.236, ...

[blackcat] L1 NinjaTrader ChannelNinjaTrader is a popular charting software widely used for trading analysis and execution in financial markets such as stocks, futures, and forex. It provides rich features and tools to assist traders in technical analysis, trade strategy development, and trade execution. When I discovered a built-in channel technical indicator in NinjaTrader and became interested in it but didn't understand its principles, I utilized my extensive development experience to simulate a similar version based on its characteristics, naming it "Ninja Channel" for reference only. First, I observed the characteristics and behavior of the built-in channel indicator. Pay attention to how it calculates and plots the channels, as well as its parameter settings and usage methods. This information can help me better understand the principles and functions of this indicator. Then, I attempted to simulate a similar channel indicator using my existing knowledge of technical analysis tools. I used charting tools and indicators to plot and calculate the upper and lower boundaries of the channel according to my needs and preferences. Please remember that this simulated version is for reference only; there is no guarantee that it will be exactly identical to the built-in channel indicator in NinjaTrader. The original built-in indicator may have more complex calculation methods with more precise results. Therefore, before engaging in actual trading activities, it is recommended that you carefully study and understand the principles and usage methods of the original indicator.

The Ninja Channel belongs to a type of technical indicator used for analyzing price range fluctuations and trends. It constructs an upper-lower boundary channel based on high-low points or moving average line fluctuations of prices to assist traders in determining overbought/oversold zones, trend strength/weaknesses,and price reversal points.

The main uses of Ninja Channel include:

1.Trend determination: The Ninja Channel helps traders determine price trends.When prices are located above half partofthechannel,it indicates an uptrend; when prices are located below half partofthechannel,it indicates adowntrend. Traders can formulate corresponding trading strategies based on trend analysis.

2.Overbought/oversold zones: The upper and lower boundaries of the Ninja Channel can be used to determine overbought and oversold zones.When prices touch or exceed the upper boundary of the channel, it may indicate an overbought market condition with a potential price pullback or reversal; when prices touch or fall below the lower boundary of the channel, it may indicate an oversold market condition with a potential price rebound or reversal.Traders can develop counter-trend or reversal trading strategies based on these overbought/oversold zones.

3.Dynamic support and resistance: The upper and lower boundaries of the Ninja Channel can be seen as dynamic support and resistance levels.When prices approach the upper boundary ofthechannel,theupperboundarymay act asresistance, limiting upward price movement; when prices approachthelowerboundaryofthechannel,thelowerboundarymayactassupport,limiting downward price movement.Traderscanmake trading decisions based on these dynamic supportandresistancelevels.

Of course, for this newly created indicator,some aspects are still unfamiliar.However,the learning process can refer to some common channel-type technical indicators including Bollinger Bands,Keltner Channels,and Donchian Channels. Each indicator has its unique calculation method and parameter settings.Traderscan choose suitable indicators according to their own needsandpreferences.

In summary,NinjaChannel is a type of technical indicator used for analyzingprice range fluctuationsandtrends.It helps traders determine trends,overbought/oversoldzones,anddynamic support/resistance levels in order to formulate appropriate trading strategies.However,technicalindicatorsareonly auxiliary tools.Traderstill needsto consider other factorsandsrisk managementstrategiesinorder tomakemore informedtradingdecisions.

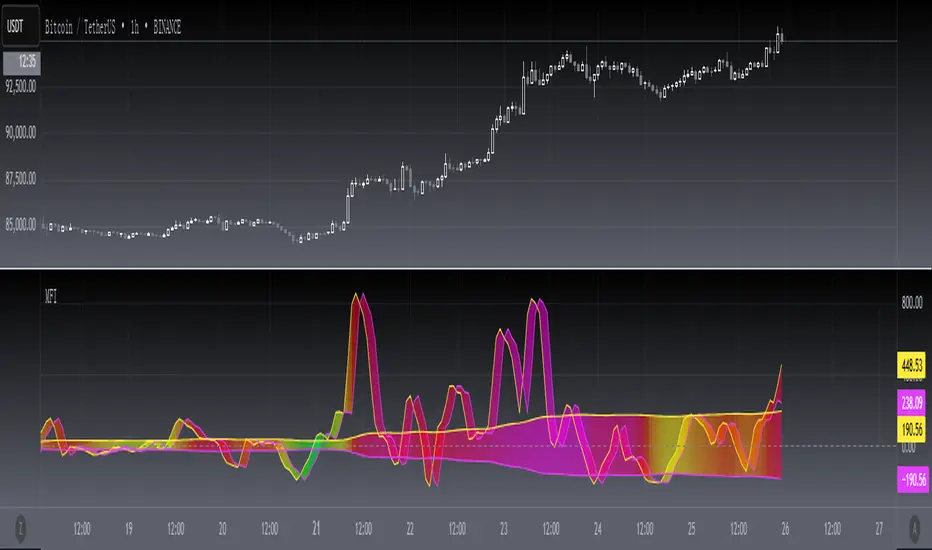

[blackcat] L2 Market Facilitation IndexThe Market Facilitation Index (MFI) is a technical indicator that measures the ease with which the market is able to move based on the volume traded. It was developed by Dr. Bill Williams as part of his trading system.

The MFI is calculated by taking into account the difference between the current typical price (average of high, low, and close) and the previous typical price, multiplied by the volume. This difference is then divided by the sum of volume over a specified period.

The MFI helps traders to identify periods of high or low market facilitation. High MFI values indicate that the market is facilitating trade and moving with ease, suggesting increased activity and potential trading opportunities. Conversely, low MFI values suggest a lack of market facilitation, indicating decreased activity and potential consolidation or sideways movement.

Traders can use the MFI in conjunction with other technical indicators and price analysis techniques to make informed trading decisions. It can be used to confirm trends, identify potential reversals, and assess the strength of market movements.

The Market Facilitation Index provides valuable insights into market dynamics, as it focuses on the relationship between price movement and trading volume. By incorporating volume data into its calculations, the MFI captures the impact of volume on market activity.

This indicator is particularly useful in identifying periods of market consolidation or range-bound trading. When the MFI shows low values, it suggests that market participants are hesitant and there may be a lack of clear trends. Traders can interpret this as a potential signal to avoid entering new positions or to tighten their stop-loss levels.

Conversely, when the MFI indicates high values, it signifies that the market is experiencing high levels of activity and price movement. This can be an indication of a strong trend, and traders may look for opportunities to enter positions in line with the prevailing market direction.

In addition to identifying market trends and potential reversals, the MFI can also help traders gauge the strength of price movements. By comparing the MFI values during different price swings or trends, traders can assess whether the market is experiencing increasing or decreasing levels of facilitation. This information can be valuable in determining the overall momentum and sustainability of a trend.

It's important to note that while the Market Facilitation Index can be a useful tool in technical analysis, it should not be used in isolation. Like any indicator, it has its limitations and may not always accurately reflect market conditions. Therefore, it is advisable to combine the MFI with other technical indicators, chart patterns, and fundamental analysis to gain a more comprehensive understanding of the market.

In conclusion, the Market Facilitation Index is a powerful technical indicator that measures the ease with which the market is able to move based on trading volume. It helps traders identify periods of high or low market facilitation, confirm trends, identify potential reversals, and assess the strength of market movements. However, it should be used in conjunction with other analysis methods for comprehensive market evaluation.

The Opening Range / First Bar By Market Mindset - Zero To EndlesThe script shows the opening range of the instrument based on different resolutions and timeframes.

Inputs :

1. Resolution

It decides the calculation frequency of the script.

In Auto resolution, Standard values have been used.

2. Timeframe

It decides the timeframe for the OHLC values.

By default, it will use the chart timeframe and so chart OHLC values.

3. Lookback

It decides the no. of ranges shown on the chart.

Middle Line can be hidden from the settings.

The script can be used for any instrument and on any timeframe.

If price is above the opening range or the middle line, a trader should look for long opportunities.

If price is below the opening range or the middle line, a trader should look for short opportunities.

A sideways or choppy move is exoected if Middle line is crossed again and again.

For trading, wait for atleast 1st bar to close. and let the opening range build up first.

Happy Trading

DP_52W_HIGH_LOW_INDICATORThis indicator tracks the 52W High and Low of any script and provides a visual interpretation of the stock price movement.

It can be used as a quick tracking indicator for trading stocks / ETFs at their 52W Low.

A typical strategy will include buying such stocks at 52W Low and selling at 52W High.

🐰Born4TradeBorn4Trade : Here we collect the Intraday HIGH and LOW and it's divided by 2 and 3 parts, Which gives an edge to trade.

Fibonacci Ranges (Real-Time) [LuxAlgo]The "Fibonacci Ranges" indicator combines Fibonacci ratio-derived ranges (channels), together with a Fibonacci pattern of the latest swing high/low.

🔶 USAGE

The indicator draws real-time ranges based on Fibonacci ratios as well as retracements. Breakouts from a Fibonacci Channel are also indicated by labels, indicating a potential reversal.

Each range extremity/area can also be used as support/resistance.

🔶 CONCEPTS

Fibonacci Channels

Latest Fibonacci

Both, Latest Fibonacci and Fibonacci Channels , display different Fibonacci levels (labels not included in the code):

However, the 2 react in a totally different way.

🔹 Fibonacci Channels

2 conditions must be fulfilled until a Fibonacci Channel is displayed:

New swing high/low

close has to be between chosen limits/levels ( Break level )

As visual guidance, chosen Break levels are accentuated by 2 small gray blocks:

Once the channel is displayed, it will remain visible until x consecutive bars break out of the chosen Break level at closing time.

• x consecutive bars is set by Break count .

The amount of breaks is counted in the code. When the price, without breaking the user-set limit, closes back between the 2 levels, the count is reset to 0.

By enabling Channels and Shadows you can see previous channels (" Shadows ", which is always delayed with 1 bar)

Previous channels can be helpful in finding potential support/resistance areas, especially from large channel blocks

The more narrow Break levels are set the less chance the price closes between these 2 levels, and the quicker close breaks out.

In other words, narrow levels give fewer & smaller channels, broader levels give more & larger channels.

Note:

• swing settings: L & R

• Break count (x consecutive bars that close outside chosen levels to invalidate the Fibonacci Channel )

will also be of influence in displaying the channels.

• Show breaks enable you to visualize signals when there is a break:

• Alerts can also be set ( Break Down / Break Up )

🔹 Latest Fibonacci

This displays the Fibonacci levels between the latest swing high and swing low, independently from the Fibonacci Channel .

The Lastest Fibonacci can be helpful in detecting the current trend against the larger Fibonacci Channel .

🔶 SETTINGS

🔹 Swing Settings

L: set left of pivothigh / pivotlow

R: set right of pivothigh / pivotlow

🔹 Fibonacci Channels

Channel : Channel / Channels + Shadows / None

Break level

-0.382 - 1.382

0.000 - 1.000

0.236 - 0.764

0.382 - 0.618

Break count

🔹 Fibonacci

Toggle

Colours: [ -0.382 - 0 ], [ 0.236 - 0.382 ], [ 0.5 ], [ 0.618 - 0.764 ], [ 1 - 1.382 ]

[blackcat] L2 Zero Lag Hull Moving AverageZero Lag Hull Moving Average (ZLHMA) is a technical indicator that is based on the principles of Zero Lag Hull Moving Average (HMA). It is designed to provide a smoother and more accurate representation of price trends by reducing lag and improving the responsiveness of the moving average line.

Compared to traditional moving average lines, the Zero Lag Hull Moving Average has the advantage of being able to capture price trend changes more precisely. It achieves this by utilizing a higher degree of smoothness through the use of weighted moving averages, and by incorporating the calculation method of Hull Moving Average (HMA) to further eliminate lag.

The calculation process of the Zero Lag Hull Moving Average involves two main steps. First, the Hull Moving Average (HMA) is calculated by taking the difference between two weighted moving averages applied to the price data. This helps to smooth out the price fluctuations and reduce lag. Then, the difference between two weighted moving averages is applied once again to the HMA, resulting in the Zero Lag Hull Moving Average. This final step further enhances the accuracy and timeliness of the indicator.

The Zero Lag Hull Moving Average offers several advantages for traders. Firstly, it provides a quicker response to changes in price trends, allowing traders to make more timely and informed trading decisions. This can be particularly useful in fast-moving markets where speed is crucial. Secondly, by reducing lag, the Zero Lag Hull Moving Average helps traders avoid missing important market signals and potential trading opportunities. It provides a more accurate representation of the current market conditions, enabling traders to act with greater confidence.

However, it is important to note that the Zero Lag Hull Moving Average should not be used as the sole basis for making trading decisions. It is recommended to consider other technical indicators, as well as fundamental and market analysis, to gain a comprehensive understanding of the market dynamics. Traders should also conduct thorough backtesting and validation of their trading strategies to ensure their effectiveness.

In conclusion, the Zero Lag Hull Moving Average is a powerful tool that can enhance the accuracy and responsiveness of technical analysis. By reducing lag and providing a more accurate representation of price trends, it can assist traders in making better-informed trading decisions. However, it should be used in conjunction with other indicators and analysis methods for a comprehensive approach to trading.

Please note that the information provided by blackcat1402 is for educational purposes only and should not be considered as financial advice. It is essential to conduct thorough research, backtesting, and validation before implementing any trading strategies.

Momentum ChannelbandsThe "Momentum Channelbands" is indicator that measures and displays an asset's momentum. It includes options to calculate Bollinger Bands and Donchian Channels around the momentum. Users can customize settings for a comprehensive view of momentum-related insights. This tool helps assess trend strength, identify overbought/oversold conditions, and pinpoint highs/lows. It should be used alongside other indicators due to potential lag and false signals.

Nifty 50 5mint Strategy

The script defines a specific trading session based on user inputs. This session is specified by a time range (e.g., "1000-1510") and selected days of the week (e.g., Monday to Friday). This session definition is crucial for trading only during specific times.

Lookback and Breakout Conditions:

The script uses a lookback period and the highest high and lowest low values to determine potential breakout points. The lookback period is user-defined (default is 10 periods).

The script also uses Bollinger Bands (BB) to identify potential breakout conditions. Users can enable or disable BB crossover conditions. BB consists of an upper and lower band, with the basis.

Additionally, the script uses Dema (Double Exponential Moving Average) and VWAP (Volume Weighted Average Price) . Users can enable or disable this condition.

Buy and Sell Conditions:

Buy conditions are met when the close price exceeds the highest high within the specified lookback period, Bollinger Bands conditions are satisfied, Dema-VWAP conditions are met, and the script is within the defined trading session.

Sell conditions are met when the close price falls below the lowest low within the lookback period, Bollinger Bands conditions are satisfied, Dema-VWAP conditions are met, and the script is within the defined trading session.

When either condition is met, it triggers a "long" or "short" position entry.

Trailing Stop Loss (TSL):

Users can choose between fixed points ( SL by points ) or trailing stop (Profit Trail).

For fixed points, users specify the number of points for the stop loss. A fixed stop loss is set at a certain distance from the entry price if a position is opened.

For Profit Trail, users can enable or disable this feature. If enabled, the script uses a "trail factor" (lookback period) to determine when to adjust the stop loss.

If the price moves in the direction of the trade and reaches a certain level (determined by the trail factor), the stop loss is adjusted, trailing behind the price to lock in profits.

If the close price falls below a certain level (lowest low within the trail factor(lookback)), and a position is open, the "long" position is closed (strategy.close("long")).

If the close price exceeds a certain level (highest high within the specified trail factor(lookback)), and a position is open, the "short" position is closed (strategy.close("short")).

Positions are also closed if they are open outside of the defined trading session.

Background Color:

The script changes the background color of the chart to indicate buy (green) and sell (red) signals, making it visually clear when the strategy conditions are met.

In summary, this script implements a breakout trading strategy with various customizable conditions, including Bollinger Bands, Dema-VWAP crossovers, and session-specific rules. It also includes options for setting stop losses and trailing stop losses to manage risk and lock in profits. The "trail factor" helps adjust trailing stops dynamically based on recent price movements. Positions are closed under certain conditions to manage risk and ensure compliance with the defined trading session.

CE=Buy, CE_SL=stoploss_buy, tCsl=Trailing Stop_buy.

PE=sell, PE_SL= stoploss_sell, tpsl=Trailing Stop_sell.

Remember that trading involves inherent risks, and past performance is not indicative of future results. Exercise caution, manage risk diligently, and consider the advice of financial experts when using this script or any trading strategy.