Средний истинный диапазон (ATR)

Advanced Average True RangeThis indicator allows you to improve your stop loss placement. It displays two lines based on the ATR ( Average True Range ), an upper line based on the current price + ATR and a lower line based on the current price - ATR. The ATR is multiplied by 2 but you can change this in the indicator settings.

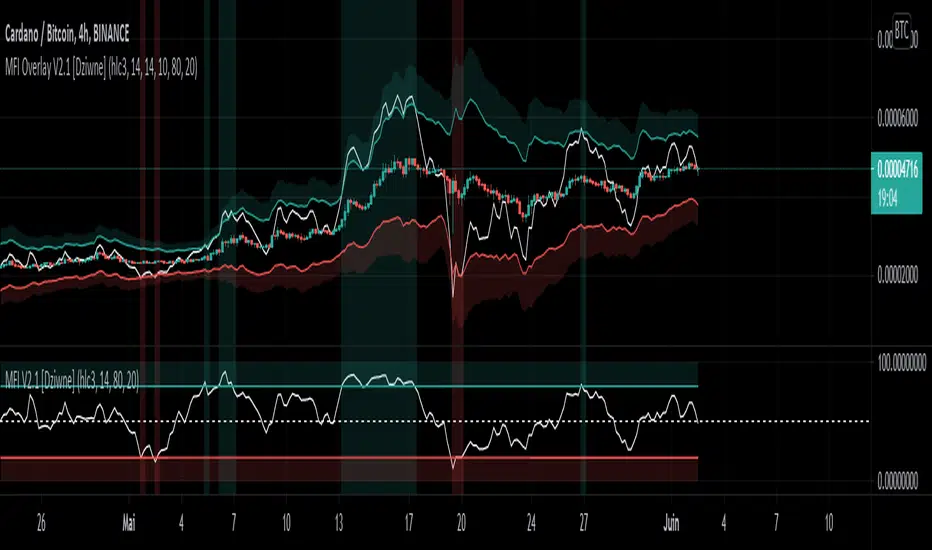

Dziwne MFI Overlay (with highlight)It is simply your traditional MFI , except that your 50 line became the actual price.

Why and how could it be useful? This indicator helps to spot more easily and efficiently divergences .

You could also use it for trend reversals as you usually do with your 50 line, but I would suggest to set a higher length for the MFI, like 155 or something like that.

ATR Stop BandView ATR Stop in a different timeframe, the default timeframe is 1D, the default ATR multiplier is 60%.

upperStop = current high + dayATR * 60%;

lowerStop = current low - dayATR * 60%;

ATR trailing Stop Loss tight to slack [Takazudo]This is a demo of ATR based trailing Stop Loss.

This SL strategy uses 2 types of ATR based SL.

tight SL as initial (ATR * 1.5)

slack SL as trailing (ATR * 4)

When any entry singal occurs by the buy/sell conditions, this SL strategy uses the "tight SL" as the initial SL.

Then the SL will chase the price as trailing SL. However, this strategy uses the "slack SL" in this trailing phase.

So you can set the tight SL first.

Then SL will chase the price as the slack one.

Note: The entry strategy in this script is not intented to win. Check the result. Be careful. Just a module of my strategy.

Kagi Implementation (+ATR)My Own Kagi Indicator Implementation!

I couldn't find anywhere on the internet a simple implementation of the Kagi indicator (apart from a seemingly complicated JavaScript implementation).

So I decided to implement it myself and test it against the built-in Kagi indicator calculated by the built-in security function - They ended up exactly the same! (You can see my orange plot completely covers the security's purple plot)

My calculations are based on this article from a site called "euroland", the article is called "Kagi Chart" (I can't post the link because of TradingView restrictions)

Bonus: The built-in kagi indicator uses only Fixed Amount Reversal Size. One that is interested in an ATR Reversal Size can modify the calculation a bit (see script's comments) to easily create and use it.

Some interesting info about the security function I discovered while doing this script:

After I implemented it I noticed that my calculations are the same except the fact that all my values are delayed by 1 bar (relative to the security's indicator). After some research I discovered that the security function uses future data in it's calculation and therefore it cannot be trusted for testing live-trading strategies, unless it is given the appropriate parameters (see script for example).

Have fun trading and don't lose money!

ATR For Stop Loss (Overlay)This script is an enhancement of ATR Indicator.

It is used to determine the stop loss position by using the ATR indicator, in conjunction with the low of the candle.

Formula = Stop Loss = Lowest(Lowest Length) - (ATR Multiplier * ATR (Smoothing, Length))

However, the user needs to manually identify the swing low for a better stop loss placement.

Parameter Information :

- Length : Period to calculate the average true range.

- Smoothing : The method used for averaging.

- ATR Multiplier : Multiplier factor to determine the Stop Loss from the lowest reference point. (1 ATR Multiplier means the stop loss would be = Low - ATR)

- Lowest Length : A total number of candle to determine the lowest reference point. (1 means only using the latest candle's low as a lowest reference point)

Have fun and good luck!

Trend Surfers - Premium Breakout + AlertsTrend Surfers - Premium Breakout Strategy with Alerts

I am happy today to release the first free Trend Surfers complete Breakout Strategy!

The strategy includes:

Entry for Long and Short

Stoploss

Position Size

Exit Signal

Risk Management Feature

How the strategy works

This is a Trend Following strategy. The strategy will have drawdowns, but they will be way smaller than what you would go through with buy and old.

As a Trend Following strategy, we will buy on strength, when a breakout occurs. And sell on weakness.

The strategy includes a FIX Stoploss determined by an ATR multiple and a trailing Stoploss/Takeprofit also determined by an ATR multiple.

You can also manage your risk by entering the maximum % you are willing to risk on every trade. Additionally, there is an option to enter how many pairs you will be trading with the strategy. This will change your position size in order to make sure that you have enough funds to trade all your favorite pairs.

Use the strategy with alerts

This strategy is alert-ready. All you have to do is:

Go on a pair you would like to trade

Create an alert

Select the strategy as a Trigger

Wait for new orders to be sent to you

Every Entry (Long/Short) will include:

Market Entry (Enter position NOW!)

Stoploss price

Position Size

Leverage

* If you do not wish to use leverage, you can multiply the Position Size by the Leverage. But doing that, you might end up with a position greater than your equity. Trading on Futures is better in order to have accurate risk management.

Exit signals:

When you receive an exit signal, you need to close the position ASAP. If you want to keep your results as close as possible to the backtest results, you need to execute quickly and follow what the strategy is telling you.

Do not try to outsmart the strategy

Leave your emotion out of trading! If you trust the strategy, you will have way better returns than if you try to outsmart it. Follow each signal you receive even if it doesn't seem logical at the moment.

Become a machine that executes. Don't look at fundamentals. Follow the trend! Trust the strategy!

I hope you enjoy it!

ATR PercentAverage True Range in Percent to price

- 2 customizable horizontal line: to be used as custom levels.

Normalized Quantitative Qualitative Estimation nQQENormalized version of Quantitative Qualitative Estimation QQE:

Normalized QQE tries to overcome the problems of false signals due to RSI divergences on the original QQE indicator.

The main purpose is to determine and ride the trend as far as possible.

So users can identify:

UPTREND : when nQQE Histogram is GREEN (nQQE is above 10)

DOWNTREND : when nQQE Histogram is RED (nQQE is below -10)

SIDEWAYS: when nQQE Histogram is YELLOW (nQQE is between -10 and 10)

Calculation is very simple;

RSI based QQE oscillates between 0-100

nQQE is simply calculated as:

nQQE=QQE-50

to make the indicator fluctuate around 0 level to get more accurate signals.

Various alarms added.

Kıvanç Özbilgiç

Renko + CandlesThis indicator has been designed to show you both candle chart and Renko chart in one place.

I think most of you are familiar with candle chart which is working with the time and price movements but Renko chart is based on price differences and is not related to the "time" parameter.

so if you see a Renko brick is appear up(or down) to the previous brick it means that a certain and fixed price movement has been occurred (which mostly calculate by ATR). and also this indicator works in any time frame.

Remember because we want both charts we have time parameter in this indicator, and if the price doesn't move up or down a certain percentage from previous bars, it will plot a renko bar beside the previous one.

you can use this indicator to see if the price moves up or down.

Or you can determine the important support and resistances with much less noises.

it can be used as a confirmation for you to keep your positions or exit.

go ahead and discover it...

If you have any questions, don't hesitate! ask in the comments section below.

Quantitative Qualitative Estimation QQE

The QQE indicator is a momentum based indicator to determine trend and sideways.

The Qualitative Quantitative Estimation (QQE) indicator works like a smoother version of the popular Relative Strength Index (RSI) indicator. QQE expands on RSI by adding two volatility based trailing stop lines. These trailing stop lines are composed of a fast and a slow moving Average True Range (ATR). These ATR lines are smoothed making this indicator less susceptible to short term volatility.

The most common method of using QQE is to look for crosses of the fast and slow moving trailing stop lines during periods when the QQE line reflects overbought or oversold conditions

Qualitative Quantitative Estimation made up of a smoothed Relative Strength Index (RSI) indicator plus fast and slow volatility-based trailing levels.

Qualitative Quantitative Estimation can be used in two directions:

1.Determine the trend, i.e. if the line is above the 50 level, the trend is ascending, if below - descending;

2.Search for signals at the moment of crossing of the QQE FAST (maroon) and QQE SLOW (blue) lines.

The QQE itself is generally considered to indicate an up-trend ifQQE FAST is above QQE SLOW, and a down-trend if below QQE SLOW.

Often a middle-range between 40 and 60 is set and if the indicator is in that range, then the market is considered to be tracking sideways, or in no trend.

You will need to set only one parameter – “SF” "RSI SMoothing Factor", an analogue of the period in RSI.

By the way, judging from the open source information, the algorithm used the standard strength index with a period of 14 for calculations.

Various signals can be created from the indicator such as:

-Buy when QQE FAST crosses above QQE SLOW below 50 level or just buy when QQE lines crosses above 50 level.

-Sell when QQE FAST crosses below QQE SLOW above 50 level or just sell when QQE lines crosses below 50 level.

WARNING: QQE IS A RSI BASED INDICATOR SO THAT IT CAN TRIGGER FALSE SIGNALS DURING DIVERGENCES!

Kıvanç Özbilgiç

Position SizingATR based position sizing calculator that takes into account the capital, risk percentage and commissions to be paid. Color changes to green as the affordable position size significantly increases relative to recent history.

EMA with RSI Backed Divergence BandsEMA200 with bands around it showing the effect of changes in RSI scaled by ATR . When the filling is green it indicates the bullish momentum and bearish when it is red.

Stochastic ATR IIStochastic ATR(Higher timeframe)

- stochastic of macd of ATR.

- stochastic rsi of ATR

atr_channelThe original bollinger bands have a fixed deviation of 2%, this channel calculates the ATR % (Atr Percentage) and places the upper and lower bands

Up-Down RangeHere is an attempt to segregate ATR into ATR of up days and down days.

While setting trailing stops based on ATR, you probably need to consider more on how an instrument can drop during red days. Hence, ATR of only red days makes more compelling case than overall ATR. Another use case for this kind of indicator may be in options if you are selling puts and calls with the intent of pocketing premiums on expiry.

Parameters are as explained below:

Range Type : Different range types are tr (True Range) , close (difference between close prices), highlow (difference between high and low of candle)

Period : ATR Period

Moving Average Type : Moving Average Type for calculating ATR. Two additional types - min and max are added which calculates lowest and highest range in last n bars

HideFullAtr : Hides combined ATR if checked.

ATR+(Experimental)

I often use the ATR as a volatility filter, to get better entries or to just get a quick understand of the volatility when screening different stocks.

With this indicator you can use the ATR in a few different ways:

-- Dynamic ATR --

To get more comparability between stocks I use a dynamic/normalized ATR, so I've experimented with two different methods.

ATR% can be calculated using John Forman’s approach called Normalized ATR (ATR / Close * 100). Or it can be calculated using what I call "Non Forman",

where the normalization happens to the true range and not to the average true range (average of (TR / Close * 100)). I think this method is "cleaner",

though the difference between the two is minimal. For more on this see www.macroption.com

You can chose between normal ATR (not normalized), Forman's normazation method, and "Non-Forman" normalization.

-- Smoothed ATR --

I originally used an ATR on a higher timeframe to get an idea of the overall volatility. But with higher time frames you always end up lag (or repainting

issues when combining into an indicator). So I expertimented on smoothing the true range, by including several bars into the calculation. I most trade

on a daily time frame so to my default "smoothing" is calculating the true range based on the last 5 days. This pretty much equals how the weekly TR

would be calculated, but since it updates daily we get a different result.

You can chose between displaying the standard ATR, the smoothed ATR or both.

-- Thresholds --

To make it more clear and visually more appealing I added thresholds and I'm plotting warning zones for low volatily.

-- Moving Average Method --

I think the best results from ATR comes when using RMA. But since I wanted to experiment with different options, the moving averages can be done using

RMA, SMA, EMA, Hull MA, or WMA.

MA Candles - SupertrendConverting strategy to indicator for those who want to use it as indicator.

Concepts are simple :

Calculate moving average of High, Low, Open and Close and make candles of them

Calculate ATR and derive supertrend on the moving average candles.

Alerts :

Bullish Crossover - When supertrend turns green

Bearish Crossover - When supertrend turns red

Bullish Pullback - Supertrend is green but close crossed below Moving average high

Bearish Pullback - Supertrend is red but close crossed above Moving average low

Original strategy is present here:

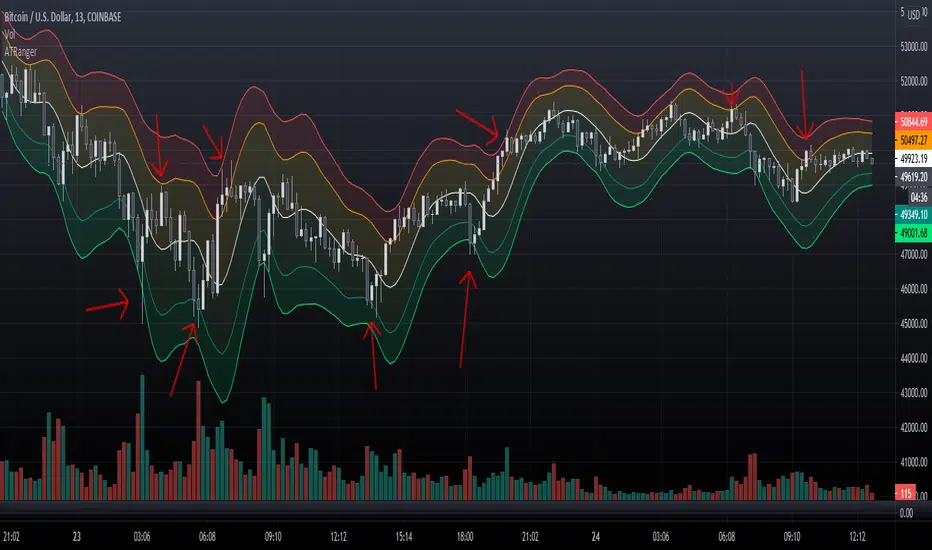

ATRangerATRanger uses Average True Range plus a variety of Moving Averages of the ATR in band format.

This is another way to identify overbought and oversold (poking out of the bands, or bouncing from them as support or resistance.)

A variety of Time-Frames can be selected, as well as several Moving Average Types to draw the bands with. (SMA, WMA, VWMA, SMMA, HMA, EMA)

Open Source

ATR Without OutliersIt is an ATR indicator which filters out outliers.

Outliers are values which are higher than the standard deviation of the true range.

It may be better than normal ATR for stop loss, because it does not keep large values after pump or dump.

It is very useful for high volatile markets like crypto markets.