Typical Sweeps: Pivot high/low boxes. Grade sweeps, Handles/PipsTool to show typical pip-grade/ handle-grade sweep distance above pivot highs and pivot lows

-In consolidation/ranging periods (i.e. most of the time); Highs/Lows may by swept by fairly consistent distances in typical stop raids.

-Idea is from ICT teaching on typical Pip-grade sweeps in FX (10,20,30pips). Designed to work on FX, Indices, Commodities, Bitcoin.

-Above chart shows S&P; sweeping below and then above by 5 handles.

///inputs///

~choose sweep distance handles ($) or pips: will auto-calculate depending on the asset: FX= pips; Indices/stocks/commodities = handles ($)

--(2,5,10,20,30,50,100, 500, 1000)

~choose pivot lookback: larger number for more significant swing highs/lows

~choose number of historical boxes to display

~toggle on/off Pivot high boxes and Pivot low boxes independently

~extend boxes fully to the right (default is not extend)

~toggle on/off text

~text & box formatting options

Bitcoin, hourly chart; Pivot lookback = 15; $100 sweep boxes:

Eur/Usd; 15m chart; Pivot lookback = 30; 10pip sweep boxes; Boxes extended fully to the right:

ATR

+ Average Candle Bodies RangeACBR, or, Average Candle Bodies Range is a volatility and momentum indicator designed to indicate periods of increasing volatility and/or momentum. The genesis of the idea formed from my pondering what a trend trader is really looking for in terms of a volatility indicator. Most indicators I've come across haven't, in my opinion, done a satisfactory job of highlighting this. I kept thinking about the ATR (I use it for stops and targets) but I realized I didn't care about highs or lows in regards to a candle's volatility or momentum, nor do I care about their relation to a previous close. What really matters to me is candle body expansion. That is all. So, I created this.

ACBR is extremely simple at its heart. I made it more complicated of course, because why would I want anything for myself to be simple? Originally it was envisaged to be a simple volatility indicator highlighting areas of increasing and decreasing volatility. Then I decided some folks might want an indicator that could show this in a directional manner, i.e., an oscillator, so I spent some more hours tackling that

To start, the original version of the indicator simply subtracts opening price from closing price if the candle closes above the open, and subtracts the close from the open if the candle closes below the open. This way we get a positive number that simply measures candle expansion. We then apply a moving average to these values in order to smooth them (if you want). To get an oscillator we always subtract the close from the open, thus when a candle closes below its open we get a negative number.

I've naturally added an optional signal line as a helpful way of gauging volatility because obviously the values themselves may not tell you much. But I've also added something that I call a baseline. You can use this in a few ways, but first let me explain the two options for how the baseline can be calculated. And what do I mean by 'baseline?' I think of it as an area of the indicator where if the ACBR is below you will not want to enter into any trades, and if the ACBR is above then you are free to enter trades based on your system (or you might want to enter in areas of low volatility if your system calls for that). Waddah Attar Explosion is another indicator that implements something similar. The baseline is calculated in two different ways: one of which is making a Donchian Channel of the ACBR, and then using the basis as the baseline, while the other is applying an RMA to the cb_dif, which is the base unit that makes up the ACBR. Now, the basis of a Donchian Channel typically is the average of the highs and the lows. If we did that here we would have a baseline much too high (but maybe not...), however, I've made the divisor user adjustable. In this way you can adjust the height (or I guess you might say 'width' if it's an oscillator) however you like, thus making the indicator more or less sensitive. In the case of using the ACBR as the baseline we apply a multiplier to the values in order to adjust the height. Apologies if I'm being overly verbose. If you want to skip all of this I have tooltips in the settings for all of the inputs that I think need an explanation.

When using the indicator as an oscillator there are baselines above and below the zero line. One funny thing: if using the ACBR as calculation type for the baselines in oscillator mode, the baselines themselves will oscillate around the zero line. There is no way to fix this due to the calculation. That isn't necessarily bad (based on my eyeball test), but I probably wouldn't use it in such a way. But experiment! They could actually be a very fine entry or confirmation indicator. And while I'm on the topic of confirmation indicators, using this indicator as an oscillator naturally makes it a confirmation indicator. It just happens to have a volatility measurement baked into it. It may also be used as an exit and continuation indicator. And speaking of these things, there are optional shapes for indicating when you might want to exit or take a continuation trade. I've added alerts for these things too.

Lastly, oscillator mode is good for identifying divergences.

Above we have the indicator set to directional, or oscillator, mode. Baselines are Donchian Channels. I changed the default EMA length from 4 to 24 in this case, otherwise all the settings are default, as in the main image for the indicator (which is clearly set to non-directional). The indicator is set to requiring an advancing signal line for background and bar colors. Background color is not on by default. Candle colors, as you can see are aqua when above the top baseline (and only when the signal line is advancing, as per the settings), magenta when below the bottom baseline, and grey for anything else. The red and blue X's are exit signals. There are two types: one, when the signal line weakens and, two, when the ACBR crosses above or below the signal line. There are also arrows. These are continuation signals (ACBR crossing signal line).

Same image as above, but the baselines are set to ACBR rather than Donchian Channels.

Again, the same image, but with everything but the ACBR Baseline turned off. You can see how this might make for an excellent confirmation indicator, but for the areas of chap. Maybe run a second instance of the indicator on your chart as a volatility indicator, as you would not be using it in that way in this instance.

Here I have bar coloring turned off except for signal line crosses NOT requiring the signal line to be advancing. Background coloring is also turned on. You can see that these all line up with continuation signals, or exits for purple candles.

Same image as above but requiring the signal line to be advancing. You can see that continuation signals are not contingent upon the signal line to be advancing. I had it setup that way at first, but of course it still gave false signals, so I thought more signals (not that there are many) is better than fewer. To be sure, just because the indicator shows a continuation signal does not mean you should always take it.

Rail Line Levels [s3]Plots support/resistance lines based on a neutral signal (white portion) of the Rail Line (variable moving average) for a period of time designated by the user (defaults to 9 bars). Support/Resistance lines will be removed after a period of tests and can be determined by the user (defaults to 26). Support/Resistance is deemed not as important or strong after several touches or tests. The trailer uses a combination of the calculation for the Rail Line (variable moving average) and an ATR to show the overall trend direction.

The indicator is centered around a Variable Moving Average. The Variable Moving Average (VMA) is a study that uses an Exponential Moving Average being able to automatically adjust its smoothing factor according to the market volatility.

In addition to the VMA, the indicator makes use of the ATR which measures market volatility by decomposing the entire range of an asset price for that period. The true range is taken as the greatest of the following: current high less the current low; the absolute value of the current high less the previous close; and the absolute value of the current low less the previous close.

TheATR™: Volatility Extremes (VolEx)Volatility is a crucial aspect of financial markets that is closely monitored by traders and investors alike. The traditional Average True Range (ATR) oscillator is a widely used technical indicator for measuring volatility in financial markets. However, there are limitations to the ATR oscillator, as it does not account for changing market conditions and may not adequately reflect extreme price movements. To address these limitations, TheATR has developed the VolEx indicator, which aims to identify extremes in the ATR oscillator by building dynamic thresholds using either a 'percentage' or 'standard deviation' based comparison with the value of the ATR.

The VolEx indicator utilizes a dynamic approach to measure volatility by considering the current level of the ATR oscillator relative to the dynamically generated thresholds. The dynamic thresholds are calculated based on the current ATR value and the chosen method of comparison (either 'percentage' or 'standard deviation'). If the ATR value exceeds the upper dynamic threshold, the market is experiencing high volatility, while a value below the lower dynamic threshold indicates low volatility.

The VolEx indicator offers several advantages over traditional volatility indicators, such as the ATR oscillator. First, it takes into account the changing market conditions and adjusts the thresholds accordingly. Second, it offers flexibility in the choice of the comparison method, allowing traders to tailor the indicator to their specific trading strategies. Finally, it provides clear signals for identifying extremes in volatility, which can be used to inform trading decisions.

In summary, the VolEx indicator developed by TheATR is a dynamic and flexible technical indicator that offers a robust approach to measuring volatility in financial markets. By utilizing dynamic thresholds and allowing for different comparison methods, the VolEx indicator provides a valuable tool for traders and investors seeking to identify extremes in market volatility..

NOTE: It is important to note that volatility, as measured by the VolEx indicator, does not provide any directional bias for the market movement. Rather, it simply indicates the degree to which the market is moving, regardless of direction. Traders and investors must use other technical or fundamental analysis tools to determine the direction of the market and make informed trading decisions based on their individual strategies and risk tolerance.

Stock Data Table█ OVERVIEW

This is a table that shows some information about stocks. It is divided into four sections:

1) Correlation

2) Shares

3) Daily Data

4) Extended Session Data

The table is completely modular, which means you can add or remove each element from the settings menu, and it will automatically rearrange its spaces.

It is also highly customizable, to the extent that you can change almost any color, remove or change titles, invert section rows, and much more.

1) Correlation

The script checks if the stock is listed on NASDAQ, and if so, uses the QQQ (Nasdaq-100 ETF) as the reference index in the first cell; otherwise, it uses the SPY (S&P 500 ETF). The length of the correlation is shown in the second cell. The table then displays the correlation between the reference index and the other index, and the correlation between the reference index and the stock.

To make it easier to interpret the correlation values, each row's last cell is color-coded with a gradient to highlight the type of correlation, and the direction of the gradient can be customized.

The correlation coefficient is a statistical measure that quantifies the strength and direction of the relationship between two variables, indicating how changes in one variable are associated with changes in the other variable, so it can be used to identify patterns and trends.

If you are interested in correlation, I suggest taking a look at my dedicated indicator:

2) Shares

This feature provides you with quick access to key information about shares and market capitalization.

On one row, you can view the total shares outstanding and the market capitalization for the fiscal year or the quarterly year. The total shares outstanding represents the total number of shares of the stock that have been issued and are currently outstanding, regardless of whether they are held by insiders or public investors. The market capitalization is a widely used measure of the company's value as determined by the stock market, calculated by multiplying its current stock price with the total number of outstanding shares.

The other row shows the float, which is the number of shares of a company that are available for public trading, and the corresponding free-float market cap, calculated by multiplying the company's current stock price with the float. Because Pine Script does not allow retrieving information about quarterly year float, you can view the float and the free-float market cap of the fiscal year only. The data can be displayed at all times or only when the difference between the total shares outstanding and the float is significant enough to result in a difference between the market cap and free-float market cap.

The classification for market cap and free-float market cap is set in this way:

Mega Cap: $200 billion or more

Large Cap: between $10 billion and $200 billion

Mid Cap: between $2 billion and $10 billion

Small Cap: between $300 million and $2 billion

Micro Cap: less than $300 million

Penny Stocks: less than $5 (customizable)

Comparing the free-float market cap to the market cap can provide insights into the liquidity of a stock. In fact, if the float is relatively small compared to the total shares outstanding, it may be more difficult to find buyers or sellers, which could lead to increased volatility. On the other hand, a larger float indicates that the stock is more liquid and may be easier to trade, potentially resulting in lower volatility. However, market conditions can change quickly and significantly, especially for intraday traders, and the free-float can also change as insiders or other large shareholders buy or sell shares. Therefore, comparing the data of the fiscal year with that of the quarterly year may not provide the most up-to-date and accurate information for making trading decisions. This limitation can be mitigated by combining those data with other indicators and tools, such as technical analysis or news events, to gain a better understand of the stock's performance and potential trading opportunities.

3) Daily Data

This section is available on daily charts only due to the lack of accuracy of real-time daily data on other time frames. Here, you can view the Average Daily Volume (ADV) over a preferred time range (20 days by default), and the Daily Change, which represents the percentage difference between the closing price on two consecutive trading days.

ADV is useful in measuring the stock's volatility, as it provides an indication of how much trading activity there is in it. Generally speaking, stocks with higher trading volume tend to be less volatile than stocks with lower trading volume. High trading volume means there are more buyers and sellers actively trading the stock, which makes it easier for investors to buy and sell shares at fair prices. This increased liquidity can help to stabilize the stock price, reducing the potential for large swings in either direction. On the other hand, stocks with lower trading volume may experience greater volatility, as there are fewer buyers and sellers actively trading the stock. This can result in larger price swings, as it may be more difficult for investors to buy or sell shares at fair prices.

The daily percentage change can provide an indication of the stock's volatility, with larger values indicating greater volatility and risk. It can also be compared to that of a benchmark such an index or other stocks in the same sector, helping to determine whether the stock is outperforming or underperforming relative to them.

4) Extended Session Data

The fourth section is available on intraday charts only. This section provides two pieces of information: the Extended Session Change and the Pre-Market Volume.

The Extended Session Change indicates the percentage difference between the previous day's closing price and the latest price in the extended session. This gives you the extent and the direction of the price gap that occurred during extended trading hours.

The Pre-Market Volume shows the sum of all shares traded during the pre-market session. This can be helpful in understanding how much interest the stock gained before the market opened.

By default, the two rows will be visible at all times. They will stop updating after the end of their respective time range, and resume updating when it starts again. However, you can choose to automatically hide them outside of their time ranges.

Both the extended session and pre-market time ranges can be customized. Please note that if you select time ranges outside of the regular market session (as set by default), you must enable the extended session to view the corresponding rows.

█ GENERAL NOTES

• Total Shares Outstanding, Float, Average Daily Volume and Pre-Market Volume cells use a customizable color system based on two thresholds, to help you quickly identify whether the value is "too low/acceptable/too high" or "too low/not enough high/acceptable".

• If you cannot see certain data, that simply means it is not available.

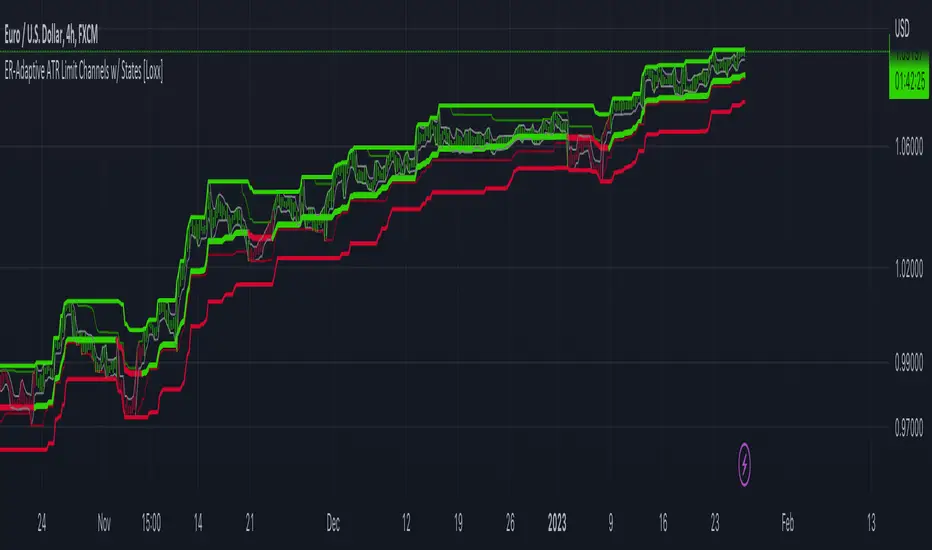

ER-Adaptive ATR Limit Channels w/ States [Loxx]As simple as it gets, channels based on high, low and ATR distances, Shows possible short term support / resistance or can be used as a take profit/stop-loss in some trading systems. It does this by comparing high/low values of price to multiplied by a multiple of ATR to determine when the trend changes. States are included to change the sensitivity to trend changes. 1 is very sensitive, 3 is least sensitive.

This uses Loxx's Expanded Source Types. You can read about them here:

What is ER Adaptive ATR?

Average True Range (ATR) is widely used indicator in many occasions for technical analysis . It is calculated as the RMA of true range. This version adds a "twist": it uses Perry Kaufman's Efficiency Ratio to calculate adaptive true range

TradePro's 2 EMA + Stoch RSI + ATR StrategySaw TradePro's "NEW BEST HIGHEST PROFITING STRATEGY WITH CRAZY RESULTS - 2 EMA+ Stochastic RSI+ ATR", and was curious on the back testing results. This strategy is an attempt to recreate it.

This strategy uses 50 / 200 EMAs, Stochastic RSI and ATR.

Long Entry Criteria:

- 50 EMA > 200 EMA

- Price closes below 50 EMA

- Stochastic RSI has gone into oversold < 20

- Stochastic RSI crosses up while making higher low from previous cross up

Short Entry Criteria:

- 50 EMA < 200 EMA

- Price closes above 50 EMA

- Stochastic RSI has gone into overbought > 80

- Stochastic RSI crosses down while making lower high from previous cross down

Stop-loss is set to ATR stop-loss

Take Profit is 2x the risk

All parameters are configurable.

Enjoy~~

DTR/ATR Scanner v1.0This indicator allows you to view DTR vs. ATR % for multiple instruments. When colors are Red the instrument is near 90% of its daily ATR.

Short vs Long ATRSimple pinescript that compares a long ATR against short ATR and let you define a threshold in %

ATR+This is an indicator which uses the ATR (average true range) to calculate take profit levels, stop loss levels, and position sizing.

It acts an ATR indicator, based on concepts found in the No Nonsense Forex (NNFX) trading system.

ATR works by looking at the past N periods (14 by default) to see on average, how many pips or dollars an asset has moved. It is widely used by itself or as part of another indicator.

This script also implements money/risk management to determine:

Take Profit : 1.00x ATR (default)

Stop Loss : 1.50x ATR (default)

Risk : 2% of account size (default)

Position Sizing : How many lots/shares/units you need to achieve the indicated risk

Trade Value : The total cost of the lots/shares/units

This indicator only displays information in the status line. It does not guarantee a successful trade, and is only intended to be used to calculate take profit and stop loss levels, or as a point of reference when entering trades. Always do your own research.

Average Range @coldbrewroshTaking the average daily range from low to high or high to low isn't the "best" way to get an idea of how much to set targets. So, I made this indicator to make the system better.

This indicator calculates the daily range from Open to High on Bullish Days & Open to Low on Bearish Days .

Nobody can catch the absolute low of the day on bullish days and get out at the high but one can enter at a reasonable price around the open ( 17:00 EST ) .

To complement the Average Range, another table shows the movement in the opposite direction.

For Instance: On Bullish Days how much it moved from Open to Low so that we have an idea of where to put the stop loss and vice versa. The time ranges calculated are the last 5 days, last 1 month, last 3 months & last 1 year.

Note #1: Even though the date range is predefined, it has a different meaning. For Instance: date range of last 5 days means "calculation of the range of last 5 bullish daily candles & not last 5 days" .

Note #2: Exclusive to Forex at the time of posting this.

Super 8 - 30M BTCWelcome to Super 8, the ultimate automatic trading script for Pine!

This bad boy is designed to go both long and short, and it's equipped with all the tools you need to maximize your profits. Whether you're looking to take profit, set a trailing stop, or protect yourself with a stop loss, Super 8 has you covered.

But that's not all! Super 8 is also loaded with 8 powerful indicators to help you make informed decisions. We've got the EMA, ADX, SAR, MACD, VOLUME, BOLLINGER BANDS, DONCHIAN, and ATR all working together to give you the best possible trading experience.

And if you want to take it to the next level, Super 8 also has a feature that lets you use stepped entries in normal mode or incremental 1,2,3,... to improve your average price. Plus, if you're using trailing stop, you can activate the Backtest precision to use lower timeframes.

But what's in a name? Super 8 is called that because it's just that... super! It's tailored specifically for the OKX:BTCUSDT.P pair, so you know you're getting the best possible results. it's highly adjustable and can be used with any other pair. So no matter what market you're trading in, Super 8 has got you covered.

So if you want to level up your trading game, give Super 8 a try. You won't be disappointed.

Certain Risks of Live Algorithmic Trading:

Backtesting Cannot Assure Actual Results.

The relevant market might fail or behave unexpectedly.

Your broker may experience failures in its infrastructure, fail to execute your orders in a correct or timely fashion or reject your orders.

The system you use for generating trading orders, communicating those orders to your broker, and receiving queries and trading results from your broker may fail.

Time lag at various point in live trading might cause unexpected behavior.

The systems of third parties in addition to those of the provider from which we obtain various services, your broker, and the applicable securities market may fail or malfunction.

ATR Oscillator - Index (Average True range Oscillator)The purpose of converting the ATR value indicator to an oscillator;

It is known that the ATR value is not between the two specified values. So it is not compressed between 0 and 100 like RSI and %B etc. Therefore, conditions such as "A condition if ATR value is X, B condition if ATR value is Y" cannot be created. In order to create these conditions, the max and min value range of the ATR value must be determined. This indicator converts the ATR values into a percentage number according to the maximum and minimum ATR values in the period you will choose. Max value is 100, min value is 0. The considered ATR value, on the other hand, corresponds to the % of the difference between the max and min value in the selected period.

In this way, conditions such as "If the ATR Oscillator value is greater than 10 or 20 or 30" can now be created, or the value of another indicator can be calculated based on the ATR Oscillator value. For example; Let's say we want the standard deviation of BBand to change according to the value of the ATR Oscillator. If BBand Standard Deviation is 3 if ATRO value is 100, BBand Standard Deviation is 2 if ATRO value is 0, and BBand Standard Deviation is 2.5 when ATRO value is 50;

We can encode it as BBand_Std_Dev=((ATRO*0.01)+2 )

If the ATRO value is between .... and ...., you can make improvements such as plot color X.

Big Poppa Code Strat & Momentum Strategy IndicatorThis indicator is a combination of a few things in order to work with a unique trading style gleaned from Callme100k, jrgreatness, TrustMyLevels , FaithInTheStrat, Rob Smith and Saty Mahajan.

This Indicator is created to help you day trade using, ATR Fibonacci Levels, Price Action and Momentum.

It displays Fibonacci Levels Based on ATR to indicate when a security is 0.236, 0.382 +- the Days Open, +- the Days Open, 0.618 +- the Days Open and 1.0 +- Days Open.

To understand this script you need to understand

Average True Range (ATR)

1 Bar Inside Bar

2 Bar Outside Bar (Break either the top or bottom)

3 Bar Engulfing Bar

Strat Setups - 212, 322, 312

Fibonacci - 0.236, 0.382, 0.618, 1.0

Moving Averages

A Trend is considered bullish when (green)

Current Price is greater than the Fast EMA Value (8)

Fast EMA is greater than PIVOT EMA Value (21)

Pivot EMA is greater than SLOW EMA Value (34)

OR Hull is trending up and the Price is above the Volume Weighted Moving Average and price is above VWAP

A trend is considered Bearish when (red)

Current Price is less than the Fast EMA Value (8)

Fast EMA is less than PIVOT EMA Value (21)

Pivot EMA is less than SLOW EMA Value (34)

OR Hull is trending down and the Price is below the Volume Weighted Moving Average and price is below VWAP

If these conditions are not met then the Momentum is in Conflict (orange)

The Momentum band will match the color of the current trend

The table that is present can be turned off at any time lets you see

1) If Moving Averages are showing bullish, bearish or in conflict

2) If There us Time Frame Continuity, (if 5 min up, are all the other timeframes up also)

3) How much of the ATR have we moved on the day

4) Are we in Call or Put range for the day based on ATR Fib Levels

The Ideal situation for entering a call

1) Momentum is Green

2) FTFC on Green

3) A Strat Actionable Signal is present

4) You are in the call range, 0.236 - 0.618 ATR + the Price

5) The ATR still has room, I.e only 50% of the ATR has been run already

Ideal situation from entering a put

1) Momentum is red

2) FTFC on Red

3) A Strat Actionable Signal is present

4) You are in the put range, 0.236 - 0.618 ATR - the Price

5) The ATR still has room, I.e only 50% of the ATR has been run already

Exit the trade for these reasons you entered (for profit or loss)

1) ATR has no more room

2) FTFC is now in conflict

3) Momentum has shifted

Take Profit when

1) You reach a new ATR Level 0.618, 1.0 , -0.618, -1, etc

Passive Stop Loss

1) Open Price if you are aggressive

2) Next ATR Level Down or Up

Feel free to take profit and leave runners

This script does not give signals, you should do your own research, I am not a financial advisors, I am simply applying principles of seasoned veterans to code. You make all decisions about how you buy, sell and trade. The creator of this script makes no promises and takes no responsibility for your personal trading.

To research the methods described above look up

Rob Smith : The Strat

Saty Mahajan : ATR Levels

Fibonacci

Using the HULL Moving Average

Exponential Moving Averages

VWAP

VWMA

FBMAEN:

TradingView indicator for FBMA strategy

People oftem ask: “Dmitry, BABA, TSLA, AAPL flies like a rocket! Well, what are we buying!?” - And I say no, the price does not act like a straight rocket upwards or downwards, instead it breathes, inhales moving away from the moving average and exhales returning to it, so we will wait for the first pullback and buy exactly at the value of the moving average.

Your new paradigm: wait for the stock to pull back to the moving average rather than chasing the price

And one more thing... Remember, you don't want to buy a stock when it's going down, you'll start to have doubts. it's against human nature to go long when the price is falling, but that's why this strategy works so well. We buy on the price rollback (pullback to the moving average), but we DO IT WHILE FOLLOWING THE TREND.

The biggest consequence of this strategy, my author's FBMA strategy and this is a game changer (results are in the comments).

So, let's dive into FBMA indicator settings:

Main settings

ATR Period — Period of intergrated ATR Indicator(shows ATR in a small dashboard);

Settings of Moving Averages

Sign Moving Averages? — shows values of moving averages near their lines on the chart;

Fix MAs' signatures overlapping? — automatically MAs' signatures overlapping (specifically for SMAs and EMAs!) ;

Fix MAs' signatures overlapping between SMAs and EMAs? — automatically group overlapping between EMAs' and SMAs' signatures;

Min distance between MAs' signatures (in % of ATR) — minimal distance between MAs' signatures that indicator will push away MAs' signatures from each other if they are overlapped;

Dashboard

Dashboard position — position of dashboard on the chart ( 9 options ).

Settings of MAs

Source;

Period;

Option for showing EMA and/or SMA of chosen period and source;

Line colour ;

Signature colour .

Addons

Show data by selected timeframe? — shows difference of current price opening and opening a "timeframe" time ago;

Shows MAs only if asset has grown by selected growth % in selected timeframe?

Growth, % — percent, which asset has to gain in order for MAs to be plotted;

Timeframe — frequency with which price's current and previous opening are being will be compared;

Show analog MAs' signatures? — shows MAs' value in a small table;

Show cloud between 1st and 2nd MAs? — shows cloud for both EMAs and SMAs simultaneously).

Price Action

This settings are intuitively understandable

Feel free to leave your questions or suggestions in the comments!

* Price Action-section was taken from ChrisMoody's CM_Price_Action and rebuilt.

RU:

Индикатор TradingView для стратегии ПООС

Мне часто пишут в личку: “Дмитрий, BABA, TSLA , AAPL летит ракетой! Ну что покупаем!?”- А я говорю нет, цена не летит по прямой ракетой вверх, она дышит, делает вдохи отдаляясь от скользящей и выдохи возвращаясь к ней, поэтому мы дождёмся первого пуллбэка и купим точно на значении скользящей

Ваша новая парадигма: ждать акцию на пуллбэке к скользящей по тренду, а не гнаться за ценой

И ещё… Помните, вы не захотите покупать акцию в момент, когда она падает, вы начнете сомневаться т.к. это против человеческой природы заходить в лонг при падении цены, но именно поэтому эта стратегия работает так эффективно, т.к. мы покупаем на откате цены (пуллбэке к скользящей), но ПО ТРЕНДУ

Самое большее следствие из этой стратегии, моя авторская стратегия ПООС и это гейм-чейнджер (результаты в комментариях).

Итак, давайте посмотрим сами настройки индикатора:

Основные настройки

ATR Period — период интегрированного индикатора ATR (показывает ATR на небольшой панели);

Настройки скользящих средних

Sign Moving Averages? — показывает значения скользящих средних рядом с их линиями на графике;

Исправить перекрытие сигнатур МА? — автоматически сигнатуры СС перекрываются (специально для SMA и EMA!) ;

Исправить перекрытие сигнатур МА между SMA и EMA? — автоматически группировать перекрытие между сигнатурами EMA и SMA;

Минимальное расстояние между сигнатурами скользящих средних (в % от ATR) — минимальное расстояние между сигнатурами скользящих средних, при котором индикатор будет отталкивать сигнатуры скользящих средних друг от друга, если они перекрываются;

Панель управления

Dashboard position — положение таблицы на графике ( 9 вариантов ).

Настройки МА

Source;

Период;

Опция отображения EMA и/или SMA выбранного периода и source;

Цвет линии ;

Цвет подписи .

Дополнения

Показать данные по выбранному таймфрейму? — показывает разницу текущей цены открытия и цены открытия в прошлом, по времени равному величины параметра "Таймфрейм";

Показывает MA только в том случае, если актив вырос на выбранный % роста за выбранный период времени?

Прирост, % — процент, на который актив должен набраться, чтобы скользящие средние были построены;

Таймфрейм — частота, с которой будет сравниваться текущее и предыдущее открытие цены;

Показать сигнатуры аналоговых МА? — показывает значение МА в небольшой таблице;

Показать облако между 1-й и 2-й скользящими средними? — показывает облако для EMA и SMA одновременно).

Price Action

Эти настройки будут интуитивно понятны

Оставляете свои вопросы и предложения в комментариях, всё учтём!

* Price Action-section was taken from ChrisMoody's CM_Price_Action and rebuilt.

AutoLevelsAuto Levels is a Work in progress.

It is based on the previous days ATR and the current days opening tick.

It takes that info and uses Fibonacci to automatically draw key levels for the day.

I have added the BULL BAR ( Green bar ) and Bear Bar ( Red Bar ) to signal as a Go Long / Go Short line in the sand.

The Tan bars are also proven key "Take Profit" levels.

These are, on average, major points of reversals, dip buys or consolidation.

I use this on the 5min timeframe and a close above or below a key level is my signal and direction. Auto Levels have proven to be a great indicator of major support and resistance.

[-_-] Volatility Calibrated ATRDescription:

An indicator based on ATR adjusted for volatility of the market. It uses Heikin Ashi data to find short and long opportunities and displays a dynamic stop loss level. Additionally, it has alerts for when the trend changes (which is an entry signal).

How it works:

It works by dynamically calculating the Period for ATR which depends on current volatility level that is calculated by a function that uses Standard Deviation of price. ATR is then smoothed by Weighted Moving Average and multiplied by ATR Factor, resulting in a plot that changes its colour to red when we're in a downtrend and green when in an uptrend. This plot should be used as a dynamic Stop Loss level. Trend change is determined by price crossing the dynamic Stop Loss level. The squared red and green labels appear when the trend changes, and should be used as Entry signals.

Parameters:

- Source -> data used for calculations

- ATR Factor -> higher values produce less noise and longer trends, lower values give more signals

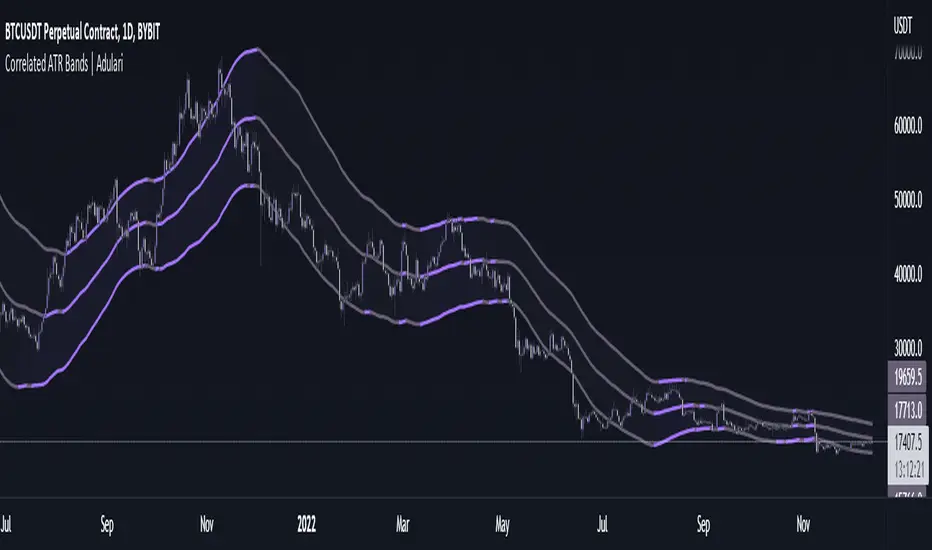

Correlated ATR Bands | AdulariHow do I use it?

Never use this indicator as standalone trading signal, it should be used as confluence.

It is highly recommended to use this indicator on the 15m timeframe and above, try experimenting with the inverse feature and multipliers as well.

When the price is above the moving average this shows the bullish trend is strong.

When the price is below the moving average this shows the bearish trend is strong.

When the moving average is purple, the trend is bullish , when it is gray, the trend is bearish.

When price is above the upper band this may indicate a bearish reversal.

When price is below the lower band this may indicate a bullish reversal.

Features:

Purple line for bullish trend and gray line for bearish trend.

Custom formula combining an ATR and Hull MA to clearly indicate trend strength and direction.

Unique approach to moving averages and bands by taking the average of 2 types of MA's combined with custom ATR's, then multiplying these by correlation factors.

Bands to indicate possible trend reversals when price crosses them.

How does it work?

1 — ATR value is calculated, then the correlation between the source and ATR is calculated.

2 — Final value is calculated using the following formula:

correlation * atr + (1 - correlation) * nz(atr , atr)

3 — Moving average is calculated with the following formula:

ta.hma((1-(correlation/100*(1+weight/10)))*(ta.sma(source+value, smoothing)+ta.sma(source-value,smoothing))/2,flength)

4 — Bands calculation using multipliers.

Average True Range Refurbished💡 Objective

This script is a rebuild of the pre-existing ATR indicator, with improvements and fine-tuning.

🪄Improvements

1. Normalization option (range 0 to 100)

2. Optional calculation of the ratio between current volatility and average volatility

3. Optional smoothing

4. Show a moving average

5. Show Bollinger Bands with 3 bands

6. Change bar colors according to ATR and Bollinger Bands

📚 Definition

'The Average True Range (ATR) is a tool used in technical analysis to measure volatility. Unlike many of today's popular indicators, the ATR is not used to indicate the direction of price. Rather, it is a metric used solely to measure volatility, especially volatility caused by price gaps or limit moves.'

(TradingView)

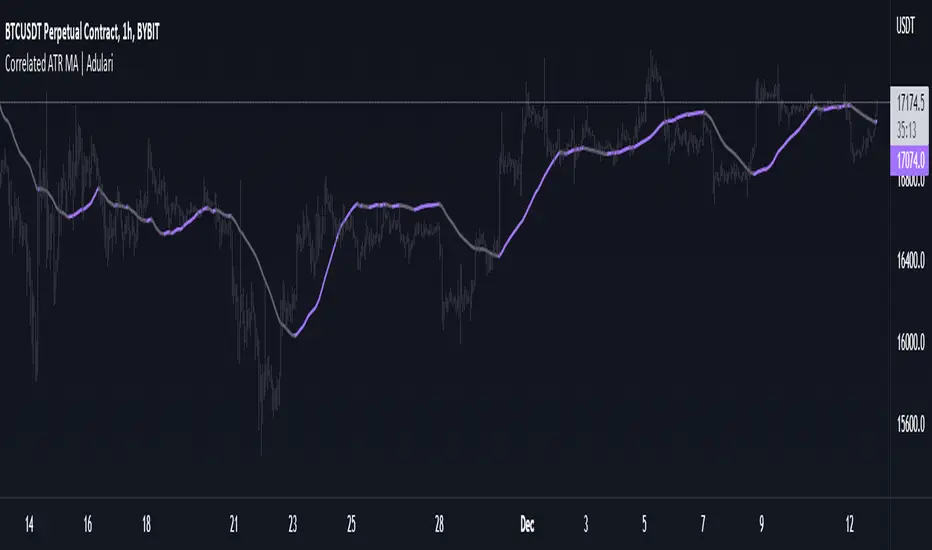

Correlated ATR MA | AdulariHow do I use it?

Never use this indicator as standalone trading signal, it should be used as confluence.

When the price is above the moving average this shows the bullish trend is strong.

When the price is below the moving average this shows the bearish trend is strong.

When the moving average is purple, the trend is bullish, when it is gray, the trend is bearish.

Features:

Purple line for bullish trend and gray line for bearish trend.

Custom formula combining an ATR and Hull MA to clearly indicate trend strength and direction.

Unique approach to moving averages by taking the average of 3 types of MA's combined with custom ATR's.

How does it work?

1 — ATR value is calculated, then the correlation between the source and ATR is calculated.

2 — Signal value is calculated from the difference between the previous source and ATR values.

3 — Final value is being calculated using the following formula:

cor * target + (1 - cor) * nz(atr , target)

4 — Moving average is calculated by getting the average of 3 values: a normal HMA, HMA plus final value, and HMA minus final value.

ATR & APCAverage True Range (ATR) and Average Price Change (APC). Shows the ATR and APC as well as the TR and PC for the current bar, colour coded to indicate very large/small bars. The ATR and APC are also colour coded to reflect whether they are increasing or decreasing. Style will need to be customized.

Interactive SAR Stop-Loss [TANHEF]This indicator is "Interactive" which means some inputs can are manually added through the first click after adding the indicator to the chart (SAR Trailing Stop-loss start point).

Unlike the normal Parabolic SAR, this indicator allows for the modification of the start point of the Parabolic SAR’s first bar calculation. Normally, the Parabolic SAR automatically has a start point after the first bar of an asset’s historical price that will then switch between trailing above and below price respectively. It must be noted that due to how the first position of the Parabolic SAR is calculated, on occasion the Parabolic SAR will immediately flip on the next bar to the opposite side relative to price that it was just located. Modifying the setting “⭐Initial Interactive SAR Position Source”, then selecting either 'Clicked' or 'ATR' level as the vertical start position will prevent this. See images below for more explanation.

Why use a trailing stop-loss?

A trailing stop-loss provides an exit when price moves against you but also enables you to move the exit point further into profit when price is moving in the desired direction of a trade. The Parabolic SAR ( stop and reverse ) which is used to determine price direction as well as when price direction is changing, is very effective at functioning as a trailing stop loss.

Indicator Explanation

Initially when this indicator is added to the chart, you will be prompted to select where to begin the SAR Trailing Stop-loss.

For a long stop-loss, select below price.

For a short stop-loss, select above price.

After this indicator is placed, it can be modified via dragging or from within the settings by modifying the time and the price input. Or simply re-add the indicator to the chart. Another option is to have this Parabolic SAR begin directly on the price that was initially ‘Clicked’ or the ‘ATR’ level, which requires selecting the option in settings labeled “⭐Initial Interactive SAR Position Source”

The SAR Stop Loss plotted. Note that the calculation that occurs on this first bar of the ‘Interactive SAR’ is as if the prior bar was the oldest historical bar of the asset. Due to the SAR’s calculations, if the ‘Normal SAR’ were to also flip sides over to the position that has been manually set for the ‘Interactive SAR’, they won’t necessarily have the same result.

An optional fixed profit target can be added within the settings. This profit target will only actively be plotted when the SAR Trailing Stop-loss has not be hit yet or until the profit target has been hit.

Here shows that the profit target was hit, then later on the SAR Trailing Stop-loss was hit.

Note, trailing stop-loss will continue to be plotted until it has been hit regardless of the profit target being hit or not.

Here is an example of when the Parabolic SAR will immediately flip on the next bar to the opposite side relative to price that it was just first located. This is due to how the Parabolic SAR is calculated and will also occur with the traditional Parabolic SAR that is not interactively (manually) given a start location. To prevent this, either relocate this time in which this SAR beings or consider modifying the SAR’s (start, increment, max) settings specifically.

Here instead of using the SAR’s calculation for an initial bar, the ‘ATR’ was selected as the start point within the setting “⭐Initial Interactive SAR Position Source”.

Alerts

1. 'Check' alerts to use within indicator settings (trailing stop hit and/or profit target hit).

2. Select 'Create Alert'

3. Set the condition to 'Interactive SAR''

4. Select create.

Trend & atr day & calcHi!

Why for what and how in this script?

At the time of publication the script consists of three modules, it may increase in the future.

1. Bottom left corner : daytime ATR module

(idea and basis of the author's script - ???)

- The size of the daily ATR based on 14 bars;

- intraday ATR progress;

- colour indication of the progress status, for easier visual perception (green < 70%, yellow 70-90 and red over 90% of ATR)

By evaluating the progress of the daily ATR, it is possible to suggest and expedient to enter/exit/hold a trade.

2. Top right: trend module

The trend is calculated based on Bill Williams' alligator indicator

- trend status on specified timeframes for the current ticker;

- colour indication for visual perception (green - growing trend, yellow - alligator is sleeping, red - downtrend)

Do not forget that the alligator is based on moving averages with the resulting consequences.

Its purpose is to assess the state of the trend on other ticker TFs, without additional actions (switching to another screen or TF)

3. In the bottom left corner - risk and position calculator

(based on an idea of the risk calculator by @andrei.bunulu)

It helps to determine the advisability of entering the trade and also what size position to enter into the trade, within money management strategy chosen.

- The calculator works in two directions: long deal and short deal (short deal calculation is enabled by check-box in settings)

- two calculation methods:

a. based on the set stop loss % (default is 0.3%), in this mode the stop and takeout level is automatically calculated (default is 1 / 3).

b. by entering the desired price levels (entry, stop and take profit points)

To make this work correctly please do not forget to choose the type of calculation (% or price) in the settings, and the currency symbol (for visual representation in the results).

The calculator can take into account the set commissions and spreads.

When hovering over the module - tooltips are displayed.

Each module can be enabled / disabled in the settings.

The size and arrangement of the modules is made for joint use with the script - "Abnormal Bar".

/// а по-русски это так ///

Привет!

Зачем для чего и как в этом скрипте?

На момент публикации скрипт состоит из трех модулей, возможно в будущем увеличится.

1. В левом нижнем углу : модуль дневного ATR

(идея и основа скрипт автора - ???)

- размер дневной ATR на основании 14 баров;

- прогресс ATR внутри дня;

- цветовая индикация состояния прогресса, для более простого визуального восприятия (зеленый < 70%, желтый 70-90 и красный более 90% ATR)

Оценивая прогресс дневного ATR, можно предположить и целесообразности входа / выхода / удержания из сделки.

2. В правом верхнем углу: модуль тренда

Тренд рассчитывается на основе индикатора - аллигатор Билла Вильямса

- состояние тренда на указанных таймфреймах для текущего тикера;

- цветовая индикация для визуального восприятия (зеленый - растущий тренд, желтый - аллигатор спит, красный - нисходящий тренд)

Не забываем, что аллигатор построен на основе скользящих средних с вытекающими последствиями.

Назначение - оценить состояние тренда на других ТФ тикера, без дополнительных действий (переключения на другой экран или ТФ)

3. В нижнем левом углу - калькулятор рисков и позиции

(на основе идеи калькулятора аuthor: @andrei.bunulu)

Помогает определить целесообразность входа в сделку, а также каким размером позиции входить в сделку, в рамках выбранной стратегии мани менеджмента.

- калькулятор работает в два направления: длинная и короткая сделка (расчет по короткой включается в настройках чек-боксом)

- два варианта расчета:

а. на основании установленного % стоп лосса (по-умолчанию 0,3%), при этом режиме происходит автоматический расчет уровня стопа и тейка (по умолчанию 1 / 3).

b. путем ввода данных желаемых уровней цены (точки входа, стопа и тейк профита)

Для корректной работы не забываем в настройках выбирать тип расчета (% или цена), а также символ валюты (для визуального отображения в итогах).

Калькулятор может учитывать установленный размер комиссий и спреда.

При наведении на модуль - отображаются подсказки.

Каждый модуль можно включить / выключить в настройках.

Размер и расположение модулей сделано для совместного использования со скриптом - "Abnormal Bar"