Index Adaptive Keltner Channels [DW]This study is an experiment in adaptive filtering. The process in this study was inspired by KAMA and ZLEMA filtering techniques.

First, data is given an optional modification for lag reduction.

Then, an adaptive filter of your choice is calculated. There are 6 different adaptive filters to choose from in this study:

-Commodity Channel Index Adaptive Moving Average (CCIAMA)

-Relative Strength Index Adaptive Moving Average (RSIAMA)

-%R Adaptive Moving Average (%RAMA)

-Klinger Volume Oscillator Adaptive Moving Average (KVOAMA)

-Money Flow Index Adaptive Moving Average (MFIAMA)

-Correlation Coefficient Adaptive Moving Average (CCAMA)

Next, ATR is calculated using the specified adaptive filter.

A set of ranges is calculated by multiplying ATR by the square root of the sampling period, then dividing it by 2 and 4.

And Finally, the ranges are added to and subtracted from the adaptive filter to generate the channels.

Custom bar colors are included. The formula for the color scheme is based on filter direction and price.

ATR

Variability Channel Index (by vitelot)This is a momentum, trend, as well as a divergence indicator.

It is similar to CCI, though it is based on a slow and fast EMA in connection to ATR, which

allows to interprete it easily.

Both EMAs and ATR have customisable period.

Further explanation and basic usage can be found in the comment section inside the script.

%ATR - TCTAThe enhanced version of %ATR of "codermua"

The %ATR calculated by EMA(red) , SMA(purple) and WMA(yellow) added to existing indicator which include only RMA(blue) calculation.

Fractal Regression Bands [DW]This study is an experimental regression curve built around fractal and ATR calculations.

First, Williams Fractals are calculated, and used as anchoring points.

Next, high anchor points are connected to negative sloping lines, and low anchor points to positive sloping lines. The slope is a specified percentage of the current ATR over the sampling period.

The median between the positive and negative sloping lines is then calculated, then the best fit line (linear regression) of the median is calculated to generate the basis line.

Lastly, a Golden Mean ATR is taken of price over the sampling period and multiplied by 1/2, 1, 2, and 3. The results are added and subtracted from the basis line to generate the bands.

Williams Fractals are included in the plots. The color scheme indicated whether each fractal is engulfing or non-engulfing.

Custom bar color scheme is included.

FIBONACCI BANDS by KIVANCfr3762Calculated with a default value of 14 periods of EMA and 14 periods of Average True Range ( SMA )

There are 4 levels of upper bands and 4 levels of lower bands in the indicator

its calculated adding and subtracting ATR( SMA ) values with coefficients 1, 1.618, 2.618 and 4.236 (Fibonacci ratios) to EMA of close prices.

Top and Bottom Fibo lines are aceepted as significant Resistance and Support levels.

KAMA Fibonacci Bands [DW]This study is an experimental combination of the Kaufman Adaptive Moving Average with ATR and Fibonacci percentages.

Smooth Regression Bands [DW]This is an experimental study using Kaufman Adaptive Moving Average (KAMA), ATR Decay, Linear Regression Bands, and McGinley Dynamic smoothing.

Umbral de RuidoSe trata de usar el ATR para crear un umbral de ruido alrededor del precio. La rotura de ese umbral nos dara señales de entrada y salida. El ATR viene multiplicado por una constante que suele ser de entre 1.5 y 3.0. Se recomiendan valores cercanos a 3 para el stoploss y 1.5 o 2.0 para la entrada.

Esta estrategia esta recomentada para activos que tengan una volatilidad controlada. Da buenos resultados en los indices, pero por lo que yo he probado no es buena para el EURUSD, me gustaria probarla tambien en acciones. Pero de momento la tengo funcionando en DAX con buenos resultados.

Procedimiento para largos:

Usamos la banda superior para marcar la entrada. Siempre que la banda marque un valor menor colocaremos una orden pendiente ahi. Con stoploss en su banda inferior. Si el valor de la banda aumenta, no actualizaremos la orden. Por lo tanto buscamos el menor valor posible del umbral de ruido.

Cuando el precio atraviese ese valor empezaremos a actualizar el stoploss siempre a un valor superior. Es decir si el umbral nos da un valor de stoploss menor nosotros no lo bajaremos.

La salida se produce por stop loss.

Procedimiento para cortos:

Usamos la banda inferior para marcar la entrada. Siempre que la banda marque un valor mayor colocaremos una orden pendiente ahi. Con stoploss en su banda superior. Si el valor de la banda disminuye, no actualizaremos la orden. Por lo tanto buscamos el mayor valor posible del umbral de ruido.

Cuando el precio atraviese ese valor empezaremos a actualizar el stoploss siempre a un valor inferior. Es decir si el umbral nos da un valor de stoploss menor nosotros no lo subiremos.

La salida se produce por stop loss.

Funciona mejor combinado con una media lenta de 100 o 200 para filtrar si ir a largos o cortos.

ATR+ (Stop Loss Indicator)This script is designed to aid in back-testing and trade execution.

It displays three sets of values - the teal colored value is the current ATR, the green colored value is your stop loss distance (in pips) below the most recent swing low for long trades , and the red colored value is your stop loss distance (in pips) above the most recent swing high for short trades .

You can change the stop loss settings to base your stop loss on a set pip amount or by however many multiples of the current ATR as you wish (eg. 1.5x ATR).

Feel free to ask any questions or edit the script without permission :)

- Matt.

Supertrend CloudSupertrend is a simple yet great indicator which is based hard data, especially when combined with an additional ST line which has its multiplication doubled.

Enjoy :)

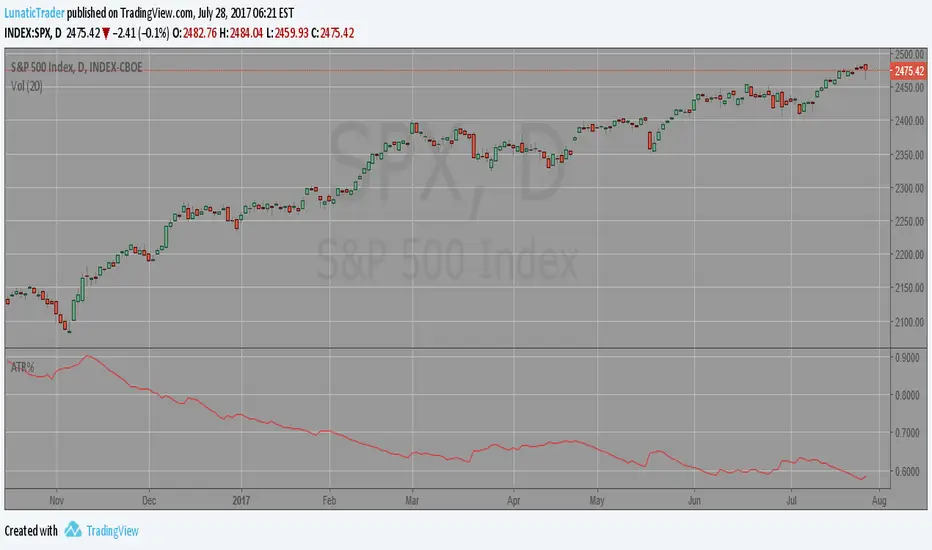

ATR%A useful measure of recent volatility. I use 50 day or 50 week periods, but you can experiment with other values too. Because it measures ranges as a % of current close it can be used to make good comparisons with other historic periods of low (or high) volatility. This measure reached a new 23 year low for daily S&P 500 in July 2017.

Uses and historic examples: lunatictrader.com

Average True Range - without open barBasic ATR without the current open bar in progress, it calculates the closed bars within the chosen ATR Period

[STRATEGY][RS]Open Session Breakout TraderEXPERIMENTAL: use at your own discretion.

custom session breakout strategy, it uses a percentage of daily atr to set breakout limits. strategy only viable for intraday timeframes and is suggested under 1hour.

BullTrading MultiTimeFrame ATR %Good afternoon traders.

Have you ever got trapped on the middle of a consolidation? Well, it just happened to me trading the 1 minute chart last friday!

So, I coded this script to display a percentage of ATR for a given resolution.

Now, how can you benefit using this information?

For example:

Using the standard settings (resolution is calibrated 15 minutes in order to trade 1minute charts), just draw your prefered support and resistance. Then measure the number of pips between support and resistance. This number should be approximately the same the indicator is displaying. If the indicator is displaying a lower value, maybe it will be a good idea to tighten your support/resistance levels (if the price goes against you, you will have confidence and probability on your side to open an opposite position and reach your Take profit before a new reversal take place.

Change colors and resolution for your desired timeframe until you find your particular "sweet spot"

Have a nice trading week.

Up/Down Range MomentumThe Up/Down Range breaks the price range into an upward and a downward moving component, so we can easily turn it into a momentum oscillator. This script does just that.

You can find the Up/Down Range (UDR) indicator here:

Up/Down RangeMeasuring the difference between the highs and lows from the average, this measure can serve as a proxy for the volatility, just like the ATR.

However, it breaks the range into an upward and a downward moving component, so it also gives information about the current trend direction.

In fact, I turned it into a momentum indicator here:

Average True Range BandDraws bounds on the last candle showing the potential movement range basing on the ATR value.

ATR BandThe indicator is intended to be used with daily or higher time frames.

Options:

Mark out of Band: show a symbol if price has moved beyond the band

ATR BandThe indicator is intended to be used with daily or higher time frames.

Options:

Mark out of Band: show a symbol is price has moved beyond the band

ATR BandThe indicator is intended to be used with daily or higher time frames.

Options:

Mark out of Band: show a symbol is price has moved beyond the band

Average True Range OverlayPlots ATR calculated on a daily basis as an overlay on the current chart.

Implemented using the builtin atr function.

ATR is a volatility indicator

originally developed by J. Welles Wilder, Jr. for commodities:

New Concepts in Technical Trading Systems. Greensboro, NC: Trend Research. ISBN 978-0-89459-027-6.

The range of a day's trading is simply R = high − low.

The true range extends it to yesterday's closing price if it was outside of today's range:

TR = max

The average true range is an N-day smoothed moving average of the TR values.

A first stab at a sensible stop loss level might be 3*ATR below recent peak.