Average True Range ShiftThis indicator builds on the idea of the Average True Range (ATR) as a way of measuring volatility. It uses two different ATRs to show a shift in market volatility.

It is mainly composed of two moving averages of ATR. One fast moving, which looks back at the previous 5 periods. One slow moving, which looks back at the previous 21 periods. Both ATRs have been normalized (show percentage instead of an absolute amount). The third component of this indicator is the histogram that is created by subtracting the slow moving average, from the fast moving average.

By having two ATRs of different lengths, traders can see how short term volatility compares to long term volatility, and how it is shifting over time. When the fast-moving crosses above the slow-moving, it will show a positive value on the histogram, meaning that short term volatility is increasing and higher than normal. When it crosses below, it will show a negative value on the histogram, meaning that short term volatility is decreasing, and lower than normal.

There are a variety of ways to utilize this indicator, and it will work in most markets. I find it is best to analyze macro market conditions on daily charts and above, rather than micro intraday moves.

ATR

ATR for Trailing StopAn ATR (Average True Range) can be used to position a trailing stop

In this script, the true range of today is calculated based on the low of yesterday in order to be more stable.

It only goes up, as a trailing stop should do.

It only goes down when the trailing stop is reached by the price.

ATR for Trailing StopThe calculation of this ATR is based on the low of yesterday in order to not change continuously during the day.

You can use this indicator to create a trailing stop taking into account volatility on the nATRPeriod previous days.

It also always go up as a trailing stop should. It only goes down the price reaches the trailing stop.

ATR smoothed by Hull MAThis is Average True Range indicator, but it is smoothed with Hull MA ( not WMA etc )

It is set to overlay the candles so looks different from normal ATR but i assure you it is ATR

Script open so you can see for yourself.

perhaps different settings are better,

Help me test it, and suggest improvements thankyou

Normalized Average True RangeThis is a Normalized ATR, which means it displays ATR as a percentage instead of absolute price. For example, a value of 1 indicates a true range of 1% in a given period.

This indicator creates a moving average of the volatility of a product going back X number of periods and is useful for deciding what to trade. For example, if used on a daily chart, one product displays a value of 4 you can reasonably expect it to have larger price swings and movement compared to another product that displays 1.

It does not predict direction, rather the size of moves.

Manual Back Test LinesI created this indicator to primarily manually test other indicators in replay mode.

To use this indicator generally you will:

Select trade type: long or short

Enter your ATR (enter the actual ATR). The indicator will then calculate and plot your SL and targets based on your values

Default Stop Loss is ATR * 1.5

Default Target 1 is ATR * 1.5

Default Target 2 is ATR * 3

Using this indicator on Replay mode is great. What you do is go back in time. Hit play and as the indicator(s) you use provide signals pause.

Pull up options:

Select trade type

Update ATR value

Change date to entry date. Typically if you are trading off the daily timeframe you are going to wait for your current day candle to close to provide signal. That would mean your entry would be on the next day.

Click play and watch, track and record how trade unfolds.

Future updates:

I'd like to be able to have some way to click one button and have it fire that enter trade right now on chart. Also I'm working on figuring out how to calculate the ATR on the entry date so that isn't required to be entered.

Finally, I'd like to have some auto calculation on when targets and SL are hit. I have this partially done but it's more important that I use this indicator than spend time or funds to update it to do that. But I do plan on updating.

ATR SL Visualization (on chart)This indicator plots 2 sets of dots (and lines) based on your chosen ATR multiplier (Average True Range).

Generally, when trading on the daily timeframe a good rule of thumb is to use the ATR * 1.5 (the default setting of this indicator).

I created this indicator to quickly test other indicators but I also find it helpful in live trading.

How to use this indicator:

Your trade system provides an entry signal. The red dot (can be connected line in options) would be used as the stop loss for either a long or short.

Then the dot on the other side would be your first 1:1 target.

The blue line is the same ATR multiplier as a target (default but can be modified).

Using an additional tool like the horizontal ray can be helpful to see the exact location the SL might be hit or where the target might hit.

When drawing your ray ensure you’re using the right entry candle.

For instance, in a long scenario you would typically be entering a trade after your signal candle closes. So draw the ray at the point in price on the next candle for both stop loss and target.

Also use these dots (lines) as guides provides an easy way to plot SL and targets if you want to use the Long or Short tool.

For my trade systems I don’t use price targets (I exit when structure or indicators reveal to exit) but I do find it helpful to graph when testing. When something moves in my favor either the ATR or the ATR * 1.5 I take profit and typically move up my stop loss to break even or trailing.

The other strategy that could be possible but have not tested is as long as the SL is making a new high moving up a hard stop to the ATR SL each day the trade goes in your favor.

This should be obvious but if you want to use just the true ATR edit the multiplier to be 1.0

Average True Range (ATR %) Stop Loss CalculatorThis indicator takes the average of a series of ATR to calculate what I would consider an optimum stop loss placement represented in percentage (read below for full overview).

While the data is plotted what is most helpful are the actual numbers presented and for my charts I remove most of the plotting.

This indicator is most helpful on the daily timeframe but can be used for all timeframes such as the 4HR, 1HR or even 15M.

This indicator should not be used alone. It should be used in conjunction with proper price action analysis. It’s also a great indicator if you chart using Value Channels. Ideally you want your stop placement to be below at least one core Value Channel boundary range. In addition to standard support and resistance and some key moving averages the market respects. This also works best when trading with the prevailing BIAS of the instrument (bull or bear).

Cryptos: Generally, that means you’re buying on retracements that fit the end of a structured move. The other option is using this in a clear up trending market where the pull backs are clearly being supported with buying.

FOREX: I built another indicator for FOREX search: ATRPIPS with SL

WTI: Helpful but I have different rules for when I trade WTI. I rely upon VCs and diagnal VCs much more when trading this.

Equities: Helpful but with the increase of volatility as well as uncertainty of Bias of the market-- this should be used as more of a guide than

What is most important is the actual percentage numbers but I've found graphing 1-3 of the actual ATRs is helpful. The rest just uncheck the checkbox in the options.

Indicator Overview:

Value 1 - 3 Period ATR (maroon)

Value 2 - 7 Period ATR (green)

Value 3 - 30 Period ATR (blue)

Value 4 - 90 Period ATR (blue, bold)

Value 5 - 1 Period ATR (green)

Value 6 - 1 Period ATR (red)

Value 6 – Prime Stop Loss Placement (maroon). This is the average of all above ATRs multiplied by 1.5

Value 7 - Move Left (red). Experimental value. This is the difference between (prime stop loss) and 1 day period move. Two ways to use this value. Use as a tighter stop loss placement. The other option is to use as a retrace target for purchase and using the Prime Stop Placement value as you’re stop loss.

All ATRs use the LOW price of the period. After testing both the low and close I’ve settled on the low to capture the most volatility you will typically experience.

Once again, this indicator should be used in conjunction with your proven trade system.

Also, by knowing what the values are within the indicator you could just eye ball what would be the best stop placement depending on the ATR or 1 or 2 ATRs you find most represent the volatility of what you are trading.

I will be expanding on this indicator by bringing in average measured moves as well as volume analysis and most likely with color changes and modifications.

Background:

While using and refining my trade system I've noticed that most moves happen in 3 periods. So we start there. The 7 period is good for a 24 hour market such as crypto (although weekend trading can be a hit or miss) and to some extent FOREX. The longer periods of 30 & 90 are to smooth out the data set. The final value of the 1 period is to bring a little more recency to the calculation.

Why multiply the average by 1.5? I've found in my own trading and system I built to be the best placement (in conjunction with VCs) to ensure you're stop isn't to close and is within the instrument you are trading volatility .

I'm looking at making this more intelligent as well as take into account volume and structured moves.

ATR Pips with Stop LossThis indicator shares ATR pips and a calculated 1.5 x stop loss calculation.

1st number is ATR.

2nd number is ATR x 1.5 (a typical SL when trading daily time frame).

The plot lines are really not that important- it's the actual numbers.

What I do is uncheck the plot line checkboxes (ATR & SL) so it doesn't show up, that way I can reduce the indicator window.

This script is a modified script by ATR Pips . Kept the BB section for now as it might be useful, but doubt it.

Future updates:

- editable the multiple for SL

- static daily numbers (right now this shows the timeframe you are viewing, I'd keep that but add a static daily ATR so you have both)

ATR+VWAP Alert//These signals mostly consist of crossovers between a 13 VWMA and a 62 VWMA. I've found these two moving averages to be quite special in their ability to

//recognize a quick trend using volume data. The VWAP is used in the alert system as well, to give some perspective on which direction we are looking to take. We

//are also using ATR. We only take trades when the ATR is on the move, meaning we have a chance to catch a volatile move! Finally, we use RSI to help weed out bad

//trades. We only take 'longs' with bullish readings from RSI, and we only take 'shorts' with bearish readings from RSI. These alerts are fantastic for catching quick intraday

//trades in either direction. I recommend using a small 'take profit' target rather than using an exit indicator. These trades can move 20-30 pips and reverse just as quickly. Good luck!

//How To Use:

//When the alert system is added to the chart, you will notice up/down symbols appear at various locations. For bullish alerts, right click an 'Up' symbol and choose 'Add Alert on VWap & ATR..'

//There are two condition options. 'Long/short', and right below that 'Buy-Signal/Sell-Signal'. Choose 'long' and 'Buy-Signal'. At options, choose 'Once Per Bar Close'. Design your alert, and you're good to go.

//For bearish signals, find a 'down' signal on the chart. Right click and follow the same process, except choosing 'short/Sell-Signal' conditions.

Tips:

Use VWAP as a stop-loss. If a candle closes below/above the VWAP in the direction against you.. get out of the trade. The losses will be minimal and few compared to the wins. Use discretion and trade carefully. This works great with crypto. Invent your own exit. If you come up with a clever exit, please share!

You can contact me at my Discord!

discord.gg

DD ATR stop trailsATR based stop trails.

The top trail is basically lowest ATR since the last candle hit (with given length and multiplication) added to candle high.

The bottom trail is analogic.

RSI ATR ChannelDraws a channel based on ATR (Average True Range) and RSI. Detects band touches and colors the background appropriately.

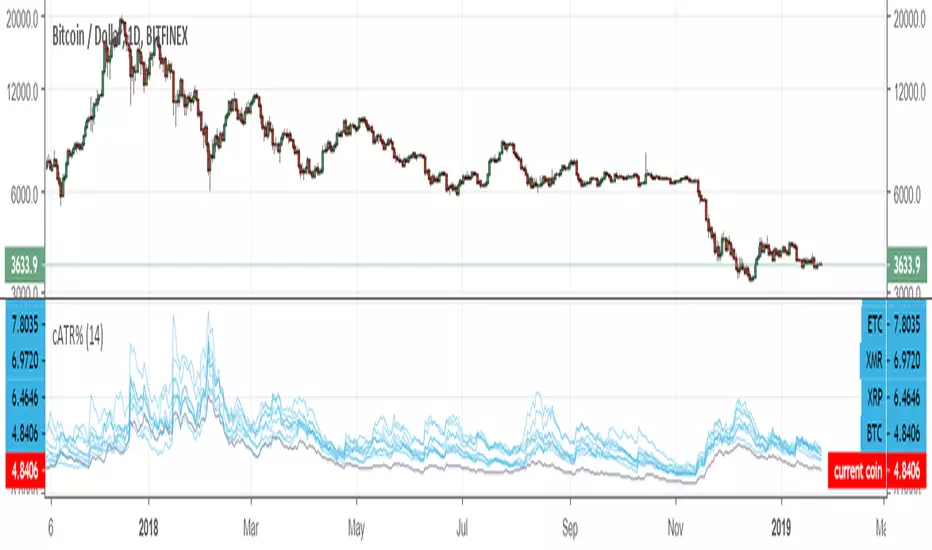

Comparative ATR%Comparison of the ATR (Average Trading Range) of multiple coins. The ATRs are shown as percentage.

Powerfull strategy MACD + RSI + Stoch buy on High exit on ATRMy strategy uses a combination of three indicators MACD Stochastic RSI .

The Idea is to buy when ( MACD > Signal and RSI > 50 and Stochastic > 50) occures at the same time the BUY STop we place on previous day HIGH

We exit on Take profit or Stop loss which is calculated by ATR (10) or on the opposite signal "Volatility breakout"

This strategy works well on stocks, commodities and cryptos especially during market breaking up after consolidation

The best results are on Daily charts , so its NOT a scalping strategy. But it can work also on 1H charts.

The strategy does not have any stops and profit targets, so we can take all the market can give us at the moment.

The exit point only when MACD goes under Signal

Its Preformance is significantly better with "buy stop on High.1" idea and exit on "volatility price breakout"

So, use it, trade it.

If it will help you to imprive your trading results, please donate me

BTC: 12kd1F8buWisUBdq27BBwRkUvzW7Ey3og5

pooya ATRthis is modified ATR for signal strength test

with custom ATR in multi time chart

comment your opinion...

Filtered ATRThis script defines an average true range where extreme events are filtered out.

Extreme events are those bars with a true range larger than 3*sigma+average,

where average and standard deviation are estimated from the last 200 bars.

In this way the ATR is not altered by exceptional events (e.g. the flash crash of Jan 3rd 2019)

and can still be used safely for Stop Losses and Take Profits.

Hitting the like button is a free sign of gratitude, thanks.

ATR Volatility Spectrum

This indicator estimates price volatility and it is based on ATR only.

The advantage of this indicator is that it can be used with any pair, any time frame.

The fluctuations of a short period ATR with respect to a gently ATR with high period

are calculated.

The only parameters are the periods of the reference ATR and fast ATR, which could be

safely let untouched and modified by experts.

RED areas depict low volatility

GREEN areas depict high volatility.

When the clouds are outside the region delimited by the aqua lines we have

extreme conditions:

Extremely low volatility = red cloud outside the aqua bands

Extremely high volatility = green cloud outside the aqua bands

Vitelot/yanez/Vts December 2018.

Hitting the like button is free act of gratitude

Normalized Average True RangeThis indicator was originally developed by John Forman (Stocks & Commodities, V.24:6 (May, 2006): "Cross-Market Evaluations With Normalized Average True Range").

Mr. Forman uses a normalized average true range indicator to analyze tradables across markets.

Good luck!

ATR 0.5 & 0.7 rangesIt good to look to ATR on intraday trading.

According to our team research only 4.8% of days security goes out of their ATR.

So we developed ATR indicator which shows Daily ATR ranges on smaller time frames.

When price crosses 70% of previous day ATR is good to look for signal to trade backward.