OPEN-SOURCE SCRIPT

VWAP with Standard Deviation Bands

Обновлено

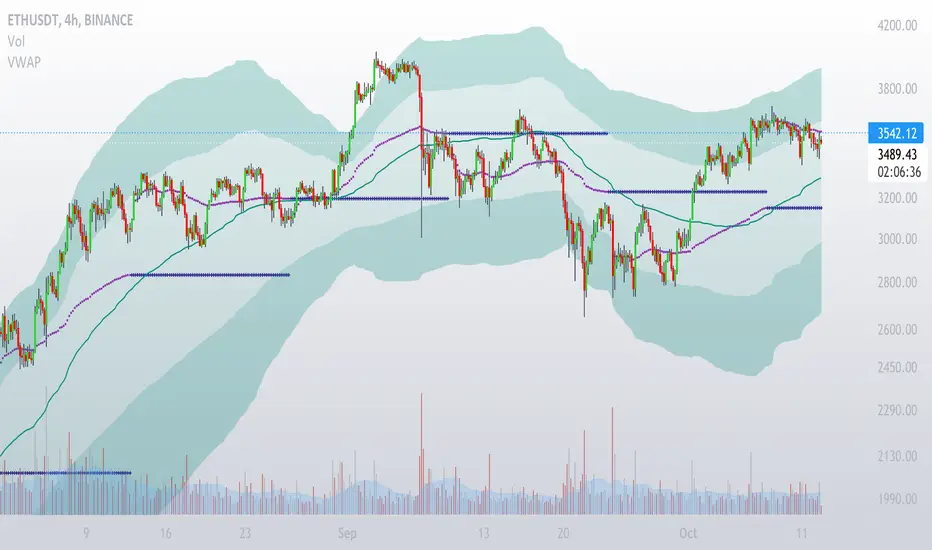

Volume Weighted Average Price (VWAP), with Standard Deviation Bands

VWAP is a moving average with weighting for traded volume, so heavier trading activity has a greater impact on its direction. Low volume periods will move the VWAP less than high volume periods.

The VWAP is important because institutional investors often use it to determine what is ‘fair value’. You can often see the market reacting when it gets close to the VWAP.

This version is time segmented VWAP. It reset ma values when selected time period expires.

Time periods are able to be selected in the settings: "1D", "2D", "W", "14D", "M", "60D", "12M", "24M", "Custom".

Additionally script determines VWAP standard deviations.

Multipliers for VWAP Standard Deviation Bands can be changed in the settings.

There is also option to show previous VWAP and its Standard Deviation Bands before timeframe reset.

VWAP is a moving average with weighting for traded volume, so heavier trading activity has a greater impact on its direction. Low volume periods will move the VWAP less than high volume periods.

The VWAP is important because institutional investors often use it to determine what is ‘fair value’. You can often see the market reacting when it gets close to the VWAP.

This version is time segmented VWAP. It reset ma values when selected time period expires.

Time periods are able to be selected in the settings: "1D", "2D", "W", "14D", "M", "60D", "12M", "24M", "Custom".

Additionally script determines VWAP standard deviations.

Multipliers for VWAP Standard Deviation Bands can be changed in the settings.

There is also option to show previous VWAP and its Standard Deviation Bands before timeframe reset.

Информация о релизе

version=5added rolling VWAP with stdev bands

more divisions in stdev bands (4)

plots style changed

Скрипт с открытым кодом

В истинном духе TradingView автор этого скрипта опубликовал его с открытым исходным кодом, чтобы трейдеры могли понять, как он работает, и проверить на практике. Вы можете воспользоваться им бесплатно, но повторное использование этого кода в публикации регулируется Правилами поведения. Вы можете добавить этот скрипт в избранное и использовать его на графике.

Отказ от ответственности

Все виды контента, которые вы можете увидеть на TradingView, не являются финансовыми, инвестиционными, торговыми или любыми другими рекомендациями. Мы не предоставляем советы по покупке и продаже активов. Подробнее — в Условиях использования TradingView.