OPEN-SOURCE SCRIPT

Scalper's Volatility Filter [QuantraSystems]

Обновлено

Scalpers Volatility Filter

Introduction

The 𝒮𝒸𝒶𝓁𝓅𝑒𝓇'𝓈 𝒱𝑜𝓁𝒶𝓉𝒾𝓁𝒾𝓉𝓎 𝐹𝒾𝓁𝓉𝑒𝓇 (𝒮𝒱𝐹) is a sophisticated technical indicator, designed to increase the profitability of lower timeframe trading.

Due to the inherent decrease in the signal-to-noise ratio when trading on lower timeframes, it is critical to develop analysis methods to inform traders of the optimal market periods to trade - and more importantly, when you shouldn’t trade.

The 𝒮𝒱𝐹 uses a blend of volatility and momentum measurements, to signal the dominant market condition - trending or ranging.

Legend

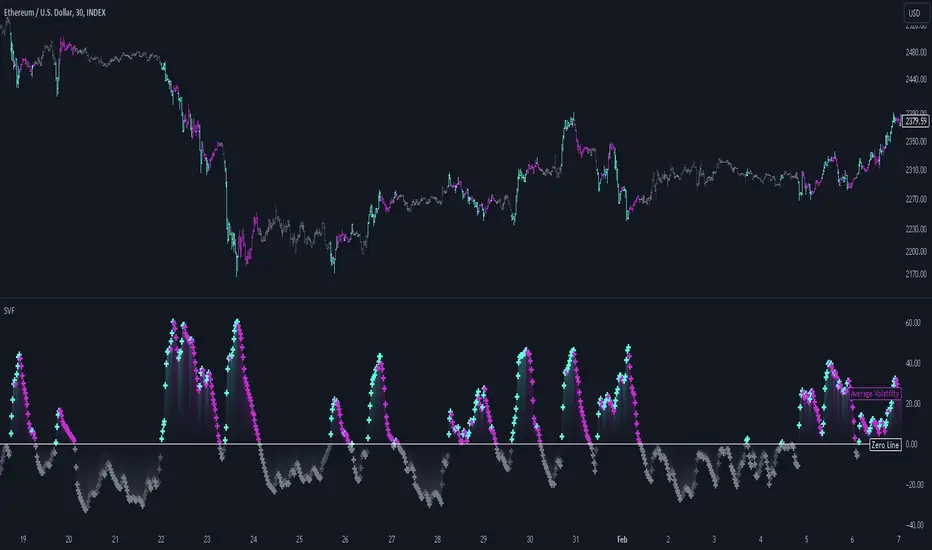

The 𝒮𝒱𝐹 consists of a signal line that moves above and below a central zero line, serving as the indication of market regime.

This distinction is critical for traders in order to align strategies with the prevailing market behaviors - leveraging trends in volatile markets and exercising caution or implementing mean-reversion systems in periods of lower volatility.

Case Study

Here we can see the indicator's unique edge in action.

Methodology

The methodology behind the 𝒮𝒱𝐹 is based upon three components:

Together, these components synthesize a robust, balanced view of market conditions, enabling traders to help align strategies with the prevailing market environment, in order to potentially increase expected value and win rates.

Introduction

The 𝒮𝒸𝒶𝓁𝓅𝑒𝓇'𝓈 𝒱𝑜𝓁𝒶𝓉𝒾𝓁𝒾𝓉𝓎 𝐹𝒾𝓁𝓉𝑒𝓇 (𝒮𝒱𝐹) is a sophisticated technical indicator, designed to increase the profitability of lower timeframe trading.

Due to the inherent decrease in the signal-to-noise ratio when trading on lower timeframes, it is critical to develop analysis methods to inform traders of the optimal market periods to trade - and more importantly, when you shouldn’t trade.

The 𝒮𝒱𝐹 uses a blend of volatility and momentum measurements, to signal the dominant market condition - trending or ranging.

Legend

The 𝒮𝒱𝐹 consists of a signal line that moves above and below a central zero line, serving as the indication of market regime.

- When the signal line is positioned above zero, it indicates a period of elevated volatility. These periods are more profitable for trading, as an asset will experience larger price swings, and by design, trend-following indicators will give less false signals.

- Conversely, when the signal line moves below zero, a low volatility or mean-reverting market regime dominates.

This distinction is critical for traders in order to align strategies with the prevailing market behaviors - leveraging trends in volatile markets and exercising caution or implementing mean-reversion systems in periods of lower volatility.

Case Study

Here we can see the indicator's unique edge in action.

- Out of the four potential long entries seen on the chart - displayed via bar coloring, two would result in losses.

- However, with the power of the 𝒮𝒱𝐹 a trader can effectively filter false signals by only entering momentum-trades when the signal line is above zero.

- In this small sample of four trades, the 𝒮𝒱𝐹 increased the win rate from 50% to 100%

Methodology

The methodology behind the 𝒮𝒱𝐹 is based upon three components:

- By calculating and contrasting two ATR’s, the immediate market momentum relative to the broader, established trend is calculated. The original method for this can be credited to the user xinolia

- A modified and smoothed ADX indicator is calculated to further assess the strength and sustainability of trends.

- The ‘Linear Regression Dispersion’ measures price deviations from a fitted regression line, adding further confluence to the signals representation of market conditions.

Together, these components synthesize a robust, balanced view of market conditions, enabling traders to help align strategies with the prevailing market environment, in order to potentially increase expected value and win rates.

Информация о релизе

Modified normalization logic.Added 'Dynamic' capabilities.

Added 'Compressed Signal Mode'.

Информация о релизе

Updated Dynamic Function Library.Update header name tag.

Информация о релизе

Added a Heikin Ashi volatility visualization - for faster measurements.Added 'HA-Width' another experimental measure of volatility.

Информация о релизе

Updated License.License formatting shout out to RUBIX_BINARY

Скрипт с открытым кодом

В истинном духе TradingView автор этого скрипта опубликовал его с открытым исходным кодом, чтобы трейдеры могли понять, как он работает, и проверить на практике. Вы можете воспользоваться им бесплатно, но повторное использование этого кода в публикации регулируется Правилами поведения. Вы можете добавить этот скрипт в избранное и использовать его на графике.

No statements or claims aim to be financial advice,

neither are any signals from us or our indicators.

Want to learn Trading, Investing or system building?

Join the Community! 👇

discord.gg/FMZDM3bZ9T

neither are any signals from us or our indicators.

Want to learn Trading, Investing or system building?

Join the Community! 👇

discord.gg/FMZDM3bZ9T

Отказ от ответственности

Все виды контента, которые вы можете увидеть на TradingView, не являются финансовыми, инвестиционными, торговыми или любыми другими рекомендациями. Мы не предоставляем советы по покупке и продаже активов. Подробнее — в Условиях использования TradingView.